Attached files

| file | filename |

|---|---|

| EX-23.1 - EX-23.1 - TECHWELL INC | a2197105zex-23_1.htm |

| EX-32.1 - EX-32.1 - TECHWELL INC | a2197105zex-32_1.htm |

| EX-21.1 - EX-21.1 - TECHWELL INC | a2197105zex-21_1.htm |

| EX-32.2 - EX-32.2 - TECHWELL INC | a2197105zex-32_2.htm |

| EX-31.2 - EX-31.2 - TECHWELL INC | a2197105zex-31_2.htm |

| EX-31.1 - EX-31.1 - TECHWELL INC | a2197105zex-31_1.htm |

Use these links to rapidly review the document

Table of Contents

ITEM 8. Financial Statements and Supplementary Data

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| (Mark one) | ||

ý |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the fiscal year ended December 31, 2009 |

||

OR |

||

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the transition period from to |

||

Commission file number 000-52014

TECHWELL, INC.

(Exact name of Registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

77-0451738 (I.R.S Employer Identification No.) |

|

408 E. Plumeria Drive San Jose, California (Address of principal executive offices) |

95134 (Zip Code) |

Registrant's telephone number, including area code: (408) 435-3888

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class: | Name of each exchange on which registered | |

|---|---|---|

| Common Stock, par value $0.001 per share | The NASDAQ Stock Market LLC |

Securities registered pursuant to section 12(g) of the Act:

| |

(Title of class) | |

||

|---|---|---|---|---|

| None |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. o Yes ý No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. o Yes ý No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ý Yes o No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files) o Yes o No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of "large accelerated filer", "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large Accelerated filer o | Accelerated filer ý | Non-Accelerated filer o (Do not check if a smaller reporting company) |

Smaller Reporting Company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). o Yes ý No

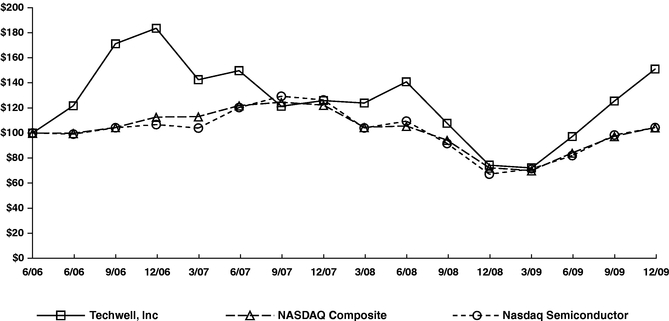

The aggregate market value of the registrant's common stock held by non-affiliates of the registrant, based upon the closing price of a share of the registrant's common stock on June 30, 2009 as reported by the NASDAQ Global Market on that date, was $134,229,739.

Number of shares of the registrant's common stock outstanding as of February 28, 2010: 22,133,012, at $0.001 par value.

DOCUMENTS INCORPORATED BY REFERENCE

Items 10 (as to directors, audit committee financial expert and Section 16(a) Beneficial Ownership Reporting Compliance), 11, 12, 13 and 14 of Part III of this Annual Report on Form 10-K incorporate by reference information from the Registrant's proxy statement to be filed with the Securities and Exchange Commission within 120 days of the fiscal year ended December 31, 2009 in connection with the solicitation of proxies for the Registrant's 2010 Annual Meeting of Stockholders.

2

This Annual Report on Form 10-K contains forward-looking statements that involve risks and uncertainties. These statements relate to future periods, future events or our future operating or financial plans or performance. These statements can often be identified by the use of forward-looking terminology such as "expects," "believes," "intends," "anticipates," "estimates," "plans," "may," or "will," or the negative of these terms, and other similar expressions. These forward-looking statements include statements as to the source of our revenue, our ability to generate revenue, our ability to sustain our growth rate and profitability, expected growth in our target markets and application-specific products, our expectation regarding the increase in certain expenses, our cash needs, our capital requirements, our market risk sensitivity, our business and product strategies, our anticipated tax rate, industry trends and our anticipation that developments in our technologies and new products will increase our target market share.

These forward-looking statements reflect our current views with respect to future events, are based on assumptions and are subject to risks and uncertainties. These risks and uncertainties could cause actual results to differ materially from those projected and include, but are not limited to, fluctuations in our revenue and operating results, our ability to sustain profitability, the demand for our products in our target markets, our ability to compete, our dependence on key and highly skilled personnel, the ability to develop new products and to enhance our existing products, the continued seasonality of our business due to our target markets and location of our customers, our ability to integrate businesses that we may acquire, our ability to estimate and predict customer demand, economic volatility in either domestic or foreign markets, the impact of any change in United States federal income tax laws and the loss of any beneficial tax treatment that we currently enjoy, our reliance on independent foundries and subcontractors for the manufacture, assembly and testing of our products, the length of our sales cycle and reliance on distributors, our ability to protect our intellectual property, the cyclical nature of the semiconductor industry, our ability to raise capital, the potential volatility of our stock, the outcome of future litigation and the other risks set forth under Item 1A. "Risk Factors." Given these risks and uncertainties, you should not place undue reliance on these forward-looking statements. Except as required by federal securities laws, we undertake no obligation to update any forward-looking statements for any reason, even if new information becomes available or other events occur in the future.

In this report all references to "Techwell," "we," "us" or "our" mean Techwell, Inc.

Techwell is our registered trademark. We also refer to trademarks of other corporations and organizations in this Form 10-K.

We are a fabless semiconductor company that designs, markets and sells mixed signal integrated circuits for two primary markets, security surveillance and automotive infotainment. We design application-specific products for these markets that enable the conversion of analog video signals to digital form and perform advanced digital video processing to facilitate the display, storage and transport of video content. We believe this application-specific product strategy allows us to better address varying customer requirements and fully leverage our technology capabilities within our two core markets. Our semiconductors are based on our proprietary architecture and mixed signal technologies that we believe provide high video quality under a wide range of signal conditions, enable high levels of integration and are cost-effective.

3

Growth in Video Applications Based on Digital Technology

Video applications based on digital technology are experiencing rapid growth in the security surveillance and automotive infotainment markets. This growth is largely attributable to significant improvements in the user experience, including enhanced video quality, increased functionality and reduced form factors as well as the lower cost of such systems.

The security surveillance market is comprised of systems that receive video from multiple surveillance cameras. Security surveillance systems are increasingly incorporating digital technologies that provide advanced functionalities such as video motion detection, hard disk drive storage, intelligent video content analysis and remote monitoring over the Internet. In addition, a heightened focus on security and declining system prices are driving increased demand for security surveillance systems.

Applications such as navigation, DVD entertainment, enhanced driver information systems and backup cameras are causing the proliferation of in-car LCD displays in the automotive infotainment market. These displays are capable of displaying video and graphics signals from a variety of sources, including navigation systems, DVDs, game consoles, TV tuners and cameras. In addition to being incorporated into new automobiles by manufacturers, these systems are also increasingly being purchased by consumers in the aftermarket.

The Complexity of Video

To display, store and transport video content, digital video applications receive analog video signals based on multiple standards from a variety of sources. For example, a security surveillance system receives analog video signals from multiple surveillance cameras for storage on a hard disk drive, display on a TV or PC monitor or transport over the Internet. In addition, an in-car LCD display typically receives analog signals from navigation systems, DVDs, game consoles, TV tuners and cameras.

Video sources such as security surveillance cameras, DVD players, and game consoles generate video signals that conform to popular analog video standards such as composite, S-video, component and Syndicate of Radio and Television Manufacturers, or SCART. However, these sources may generate video signals that are off-specification or weak, both of which deteriorate video quality. Off-specification signals are signals that have been generated with slight variations to specifications under a particular standard. Weak signals are signals that conform to specifications but result in high levels of noise. Digital video applications must support these standard analog video signals, even if they are off-specification or weak, without sacrificing video quality.

Opportunity for Mixed Signal Video Semiconductors

Mixed signal video semiconductors are critical components of digital video applications and enable the conversion of standard analog video signals to digital form, even if they are off-specification or weak. In addition, these semiconductors incorporate advanced digital video processing to improve video quality and provide enhanced functionality. Designing these semiconductors requires an extensive knowledge of TV broadcast and popular analog video standards as well as significant digital video processing expertise and advanced analog design capability. We believe that semiconductor companies that possess the combination of these capabilities will benefit most from the growth in digital video applications.

Since our inception, we have internally developed the combination of technologies, expertise and capabilities necessary for the conversion and processing of video signals. We do not depend on third-

4

parties for any material technology, expertise or capability. We believe we have the following technology strengths:

Advanced Analog Design Capability. As a result of our advanced analog design capability, we have developed multiple technologies that enable analog video signals to be processed digitally. One of the key analog technologies we have developed internally is our high performance, cost-effective and low power analog front-end that conditions and converts analog video signals into a digital format. The multiple core functions performed within our analog front-end are anti-aliasing filtering, automatic gain control signal clamping and analog to digital conversion. Other key analog technologies we have developed internally are phase lock loops, high frequency and sigma delta analog to digital converters, video and audio digital to analog converters and low voltage differential signaling.

Advanced Digital Video Processing Technology. We have a proprietary video decoding architecture for decoding analog video. This architecture allows us to cost-effectively implement two dimension, or 2D, and three dimension, or 3D, comb filtering, color demodulating and sync processing, which are the key technologies required for high performance video decoding. Comb filtering enables improved video quality, while sync processing enables support of weak and off-specification signals. In addition, we have developed a number of digital technologies targeted at specific applications in the security surveillance and automotive infotainment markets. For example, we have developed deinterlacing, scaling and image enhancement algorithms, which are important technologies for displaying video signals in in-car LCD display and advanced TV applications. Similarly, we have developed multiplexing, motion detection, multiple picture-in-picture and motion JPEG compression technologies for security surveillance systems.

Expertise in TV Broadcast and Popular Analog Video Standards. Our focus on video has enabled us to develop expertise in analog TV broadcast and popular analog video signals, including off-specification and weak signals that are difficult to support. As a result, we have the extensive knowledge base required to perform the analog, mixed signal and digital processing necessary for the display, storage and transport of video signals. This is particularly important because no standards body exists to determine and qualify products developed to meet analog video standards.

Integrated Analog and Digital Technologies in a Standard CMOS Process. We integrate our advanced digital technologies with our analog technologies on a single semiconductor using a standard complementary metal-oxide semiconductor, or CMOS, process. We believe this provides us with performance, cost and power advantages over other processes such as bipolar.

We believe that the combination of the technology strengths listed above allows us to provide our customers with significant benefits, including:

High Performance. We enable our customers to achieve high video quality by limiting artifacts such as cross-color, crawling or dangling dots and stair-stepping or jagging that are commonly found when processing analog video signals. Our technology also enables our customers' products to support multiple standard signals, even if off-specification or weak, without sacrificing video quality. The result is high video quality under a wide range of signal conditions.

High Levels of Integration. We integrate our analog conversion and digital processing technologies into a single semiconductor. For example, in the security surveillance market, we integrate multiple video decoders and a system controller into a single highly integrated semiconductor, allowing for increased functionality and enabling our customers to reduce system-level costs significantly. Similarly, in the automotive infotainment market, we integrate a video decoder, display processor and a timing controller into a single semiconductor, also enabling our customers to reduce system-level costs.

5

Cost-effectiveness. Our proprietary video decoding architecture and our standard CMOS process design expertise allow us to reduce the number of transistors required to design semiconductors cost-effectively.

Our objective is to be the leading provider of high performance, cost-effective mixed signal semiconductors to the security surveillance and automotive infotainment markets. To achieve this objective, we expect to continue to pursue the following strategies:

Target Multiple High Growth Digital Video Applications. We address a number of digital video applications in the security surveillance and automotive infotainment markets that provide us with multiple high growth opportunities. Our products are incorporated into numerous security surveillance applications, including embedded digital video recorders, or DVRs, networked video recorders, or NVRs, and multiplexers. Our products are also incorporated into numerous automotive infotainment applications such as rear seat entertainment, front console navigation and rear view mirror displays.

Develop Additional Application-Specific Products. We provide our customers with application-specific products designed specifically to address the requirements of the specific market we target. These application-specific products integrate our video decoder with our advanced digital processing technologies and target the security surveillance and automotive infotainment markets. We believe that our application-specific product strategy allows us to better address varying customer requirements and fully leverage our technology capabilities. We plan to maintain and expand upon this product strategy in the future.

Develop New Technologies. We plan to continue to develop additional technologies to address evolving customer requirements. For example, we have expanded our research and development efforts and are developing H.264 encoding and decoding technologies, which are important functions for storing, displaying and networking video. Consistent with our product strategy, we intend to incorporate these H.264 encoding and decoding technologies into our application-specific products in the future.

We have also developed a new technology that will enable full high definition display using the existing coaxial infrastructure that currently enables standard definition display. We are now in the process of productizing the technology for use by customers supplying DVR and camera components to the security surveillance market.

Expand Customer Relationships. Our mixed signal semiconductors are used by over 100 companies in the security surveillance and automotive infotainment markets. We sell our semiconductors through sales and customer support personnel and sales and marketing offices in the United States, Japan, South Korea, Taiwan and China. We intend to continue to expand our sales, marketing and technical support capabilities to pursue additional design wins with our existing customers and to develop relationships with new customers in our target markets.

We design, market and sell mixed signal semiconductor products that enable the conversion of analog video signals to digital form and perform advanced digital video processing to facilitate the display, storage and transport of video content. Historically, we classified our initial products as general purpose products in that they serviced multiple markets. In the process of supplying products to these markets, we developed specific knowledge regarding the requirements for certain markets. We then concentrated our development efforts on video applications within a limited number of target markets. Today, our application-specific products include products specifically designed for security surveillance systems and automotive infotainment displays. We intend to continue to develop new generations of products for each of these application-specific product lines. To a lesser extent, we continue to design,

6

market and sell general purpose video decoders for applications in consumer products. Accordingly, we classify our products in three primary lines: security surveillance, automotive infotainment and consumer.

Security Surveillance. Our security surveillance products integrate important functions required to display, store and transport analog video signals from security surveillance cameras. For example, we integrate multiple video decoders into a single semiconductor. As a result, this semiconductor is able to receive and decode analog video signals from multiple cameras into a standard digital format. In addition, we integrate a multiplexer, a key technology required to combine multiple video signals into a single video signal, and a display processor, a key technology required to display multiple video channels. In December 2008, we introduced a new security surveillance product which includes a 16 channel multiplexer and supports the display of multiple standard definition and high definition video sources. We currently sell our security surveillance products to customers for use in numerous applications including DVRs, PC-based DVRs, NVRs and multiplexers.

Automotive Infotainment. Our automotive infotainment display products integrate important functions required to display popular analog video, high definition video and PC graphics signals on a LCD display. These key functions include a video decoder, deinterlacer and scaler. In addition, our newer generation LCD display products integrate a timing controller to interface directly with certain types of LCD displays and image enhancement functionality to improve overall video quality. In January 2008, we announced the introduction of five new LCD display processors designed for the automotive end market. These new products are designed to offer our customers a comprehensive set of capabilities including advanced image processing, an integrated programmable timing controller and multiple analog and digital video inputs.

Consumer. Our consumer video decoder products are high performance mixed signal semiconductors that decode analog TV broadcast signals, including NTSC, PAL and SECAM, and popular analog video signals, including composite, S-Video, component and SCART, into a standard digital format. Our video decoder products integrate proprietary sync processing, color demodulating and digital 2D and 3D comb filtering, which are the key technologies required for high performance video decoding. We offer a broad range of video decoder products at various price points and with varying features.

7

The following table summarizes the features and diverse applications of our primary product lines:

| Product Line | Key Features | Target Applications | ||

|---|---|---|---|---|

Security Surveillance |

• Integrates four NTSC and PAL video decoders |

Embedded DVR, PC based DVR, NVR and multiplexer | ||

Automotive Infotainment |

• Integrates NTSC, PAL, SECAM video decoder, deinterlacer,

scaler, timing controller and image enhancement |

In-car LCD display, including front console, rear seat and rear view mirror displays | ||

Consumer |

• Supports NTSC, PAL and SECAM analog TV broadcast

formats |

Advanced TV, DVD recorder, multifunction LCD monitor, camcorders and PC peripherals including TV tuner cards and USB TV boxes | ||

Our other products include early generation mixed signal semiconductors for digital video applications and a PCI video decoder product, which is a video decoder that utilizes peripheral component interconnect, or PCI, technology for personal computer applications.

We have several core competencies that enable us to design important analog, mixed signal and digital technologies that can be implemented across our application-specific product lines. Over the last ten years, we have internally developed the combination of technologies, expertise and capabilities necessary for the conversion and processing of video signals. We do not depend on third-parties for any material technology, expertise or capability.

We have developed a proprietary high performance and cost-effective video decoder technology that receives and converts various analog video signals, including TV broadcast, composite video, S-video, component and SCART, into a standard digital format. Our video decoder uses both analog and digital circuitry. Our video decoder uses our high performance, cost-effective and low power analog front-end for signal conditioning and sampling the analog signal into digital format. It uses our advanced digital processing circuitry, including a 2D and 3D comb filter, a color demodulator and a sync processor for deciphering the raw digital stream into the four principal components: luminance,

8

U, V and synchronization. These are important technologies required for high performance video decoding. Comb filtering is a technique for separating TV broadcast and composite video signals into luminance and modulated chrominance. Our advanced comb filter provides separation resulting in high-resolution image with minimal visible artifacts such as cross color and crawling or dangling dots. Our color demodulator converts the modulated chrominance signals based on NTSC, PAL and SECAM standards and sub-standards into baseband U and V components. Our sync processor extracts the vertical and horizontal synchronization information from the video stream, which is required for the display device to reconstruct the original video content. Both our advanced color demodulator and our advanced sync processor are critical to our decoder's ability to support off-specification and weak signals.

We have expertise in analog TV broadcast and popular analog video standards. These standards typically define video signal characteristics such as line period, field rate, signal amplitude, chrominance modulation scheme and frequency, among others. Notwithstanding the existence of standards, terrestrial TV stations and video applications such as TVs, VCRs, DVD players, game consoles, camcorders and security cameras sometimes generate signals that are off-specification due to their mechanical nature or other characteristics. In addition, these video sources sometimes contain noise from interference, additional modulation/de-modulation processing or RF transmission. These variations in signal standards and signal strength create significant challenges for original equipment manufacturers, or OEMs, and, in turn, semiconductor companies. To deal with these challenges, we believe these semiconductor companies require expertise in analog TV broadcast and popular analog video standards to assure manufacturers that their products can support these signals, even if they are off-specification or weak.

We design semiconductors that receive an analog signal, convert the analog signal to a digital signal represented by ones and zeroes and then use digital circuitry to process the signal. Using digital circuitry to process analog video signals allows us to achieve high performance video, integrate more functionality and reduce costs. As a result, we combine analog functionality on the same semiconductor substrate with digital functionality. Digital circuits perform high speed switching between logic states that generate transients known as electromagnetic interference as well as electrical noise on the substrate and on the power bus. By contrast, analog circuits are extremely sensitive to noise. There are significant design and development challenges involved in mixing noisy digital circuits with noise-sensitive analog circuits on the same semiconductor substrate. Our design engineers are skilled at solving these problems to achieve high quality video performance on a mixed signal semiconductor.

We have also developed a technology that will enable full high definition display using the existing coaxial infrastructure that currently enables standard definition display. We are now in the process of productizing the technology for use by customers supplying DVR and camera components to the security surveillance market.

We principally sell our products to distributors who, in turn, sell to OEMs, original design manufacturers, or ODMs, contract manufacturers and design houses. In addition, we sell our products, though to a lesser extent, directly to OEMs and ODMs. ODMs typically design and manufacture electronic products to sell to OEMs. In 2009, 2008 and 2007, our largest customers have been distributors, who typically support multiple OEMs and ODMS. In 2009, 2008 and 2007, our largest customer was Lacewood International Corporation, or Lacewood, our largest distributor in China, who accounted for 35%, 34% and 22% of our revenue, respectively. Our agreements to sell our products through distribution channels generally provide for a non-exclusive right to sell, and to promote and develop a market for our products in a specified geographic area. These agreements generally may be terminated by either party on 30 days notice and do not require price protection. Our direct sales to OEMs and ODMs are accomplished through purchase orders.

9

Substantially all of our sales are to customers in Asia, which sales accounted for approximately 97%, 98% and 98% of our revenue in 2009, 2008 and 2007, respectively. The table below indicates the percentage of total revenue by geographic location for the periods indicated:

| |

Year Ended December 31, |

||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2009 | 2008 | 2007 | ||||||||

China |

54 | % | 37 | % | 26 | % | |||||

South Korea |

21 | 27 | 29 | ||||||||

Taiwan |

16 | 29 | 40 | ||||||||

Japan |

6 | 5 | 3 | ||||||||

Other |

3 | 2 | 2 | ||||||||

Total revenue |

100 | % | 100 | % | 100 | % | |||||

We sell our products worldwide through multiple channels, utilizing our direct sales force and applications engineering staff and our network of domestic and international independent distributors as well as OEMs and ODMs who are supported by our independent sales representatives. Each of these sales channels is supported by our customer service and marketing organizations. We have marketing and customer support personnel in the United States as well as China, Japan, South Korea and Taiwan. We intend to expand our sales and support capabilities and our network of independent distributors and sales representatives in key regions domestically and internationally.

Our sales cycle typically ranges from six to 24 months. We work directly with system designers to create demand for our semiconductors by providing them with application-specific product information for their system design, engineering and procurement groups. We actively engage these groups during their design processes to introduce them to our semiconductors. We endeavor to design our products to meet anticipated, increasingly complex and specific design requirements, but which will also support widespread demand for the products and future enhancements to them. If successful, this process culminates in a system designer deciding to use our products in their system, which we refer to as a design win. Once our product is accepted and designed into an application, the system designer is likely to continue to use the same or enhanced versions of our product across a number of their models, which tends to extend the life cycles of our product. If we fail to achieve an initial design win, we may lose the opportunity for sales to a customer for a number of its products and for a lengthy period of time.

Our sales are made primarily pursuant to standard individual purchase orders. Our backlog consists of orders that we have received from customers that have not yet shipped. Historically, management has not used backlog as an indicator of future business. As our order lead times may vary and as industry practice allows customers to reschedule or cancel orders on relatively short notice, we believe that backlog is not necessarily a good indicator of future sales. In addition, a substantial portion of our quarterly revenue typically depends on orders booked and shipped in that quarter.

Our research and development efforts are focused on the development of new technologies for our application-specific product lines. As of December 31 2009, we had 114 persons engaged in research and development. Our research and development expense was $19.6 million, $17.1 million and $12.3 million in 2009, 2008 and 2007, respectively.

10

We seek to protect our proprietary technology, documentation and other written materials primarily under trade secret and copyright laws. We also typically require employees and consultants with access to our proprietary information to execute confidentiality agreements. The steps taken by us to protect our proprietary information may not be adequate to prevent misappropriation of our technology.

Although we rely primarily on trade secret laws and contractual restrictions to protect the technology in the semiconductors we currently design and market, our success and ability to compete in the future may also depend to a significant degree upon obtaining and enforcing patent protection for our video decoding architecture and other mixed signal technologies. As of December 31, 2009, we had two issued patents and eleven patent applications pending in the United States and seven patent applications pending in foreign jurisdictions. These patents and patent applications cover aspects of the technology in the semiconductors we currently design and market, including a patent for our video decoding architecture. Our issued patents have expiration dates ranging from January 9, 2029 to November 11, 2029. Patents that we currently own do not cover all of the semiconductors that we presently design and market. Our present and future patents may provide only limited protection for our technology and may not be sufficient to provide competitive advantages to us. For example, competitors could be successful in challenging any issued patents or, alternatively, could develop similar or more advantageous technologies on their own or design around our patents.

The laws of other countries in which we market our semiconductors, such as some countries in the Asia/Pacific region, may offer little or no protection for our proprietary technologies. Reverse engineering, unauthorized copying or other misappropriation of our proprietary technologies could enable third-parties to benefit from our technologies without paying us for doing so. Any inability to protect our proprietary rights could harm our ability to compete, generate revenue and grow our business.

We may be required to resort to litigation to enforce our intellectual property rights. We may also be subject to legal proceedings and claims relating to our intellectual property in the ordinary course of our business. Intellectual property litigation is expensive and time-consuming and could divert management's attention away from running our business. This litigation could also require us to pay substantial damages to the party claiming infringement, stop selling products or using technology that contains the allegedly infringing intellectual property, develop non-infringing technology or enter into royalty or license arrangements.

We do not own or operate a semiconductor fabrication, packaging or testing facility. We depend on third-party vendors to manufacture, package and test our products. By outsourcing manufacturing, we are able to avoid the cost associated with owning and operating our own manufacturing facility. This allows us to focus our efforts on the design and marketing of our products.

Semiconductor Fabrication. We currently outsource our semiconductor manufacturing primarily to Taiwan Semiconductor Manufacturing Company, or TSMC. We work closely with TSMC to forecast on a monthly basis our manufacturing capacity requirements. Our semiconductors are currently fabricated in several advanced, sub-micron manufacturing processes. Because finer manufacturing processes lead to enhanced performance, smaller silicon chip size and lower power requirements, we continually evaluate the benefits and feasibility of migrating to smaller geometry process technologies in order to reduce cost and improve performance. Our products are manufactured using CMOS process technology. The processes we select permit us to engage independent silicon foundries to fabricate our integrated circuits. By subcontracting our manufacturing requirements, we can focus our resources on design and test applications where we believe we have greater competitive advantages. This strategy

11

also eliminates the high cost of owning and operating semiconductor wafer fabrication facilities. Nevertheless, because we do not have a formal, long-term pricing agreement with TSMC, our wafer costs and services are subject to sudden price fluctuations based on the cyclical demand for semiconductors. Our engineers work closely with TSMC to increase yields, lower manufacturing costs and improve quality. Our operations and quality engineering teams closely manage the interface between manufacturing and design engineering. As a result, we are responsible for the complete functional and parametric performance testing of our devices, including quality. We employ an operations and quality organization to work very closely with our semiconductor wafer manufacturers. We also arrange with our foundries to have online work-in-process control.

Assembly and Test. Our products are shipped from our semiconductor manufacturers to third-party sort, assembly and test facilities where they are assembled into finished semiconductors and tested. We outsource all packaging and testing of our products to assembly and test subcontractors, primarily to Advanced Semiconductor Engineering, Inc., or ASE, in Taiwan. Our products are designed to use low cost, standard packages and be tested with widely available test equipment. We have also qualified and retained additional vendors to assemble and test our semiconductors.

Quality Assurance. We focus on product reliability from the initial stage of the design cycle through each specific design process, including layout and production test design. We prequalify each assembly and foundry subcontractor. This prequalification process consists of a series of industry standard environmental product stress tests, as well as an audit and analysis of the subcontractor's quality system and manufacturing capability. We also participate in quality and reliability monitoring through each stage of the production cycle by reviewing electrical and parametric data from our wafer foundry and assembly subcontractors. We closely monitor wafer foundry production to ensure consistent overall quality, reliability and yield levels.

All of our principal independent foundries and package assembly facilities are currently ISO 9001 certified.

The market in which we operate is extremely competitive, and is characterized by rapid technological change, continuously evolving customer requirements and declining average selling prices. We may not be able to compete successfully against current or potential competitors. We compete with numerous domestic and international semiconductor manufacturers and designers, including NXP, Inc. (formerly Philips Semiconductors), Texas Instruments Inc., MStar Semiconductor Inc., Conexant Systems Inc. and Nextchip Company Ltd. Most of our current and potential competitors have longer operating histories, significantly greater resources and name recognition and a larger base of customers than we do. This may allow them to respond more quickly than us to new or emerging technologies or changes in customer requirements. Some of our competitors currently offer product features or technologies that we do not currently offer but intend to sell in the future. We must, therefore, compete against competitors that have more experience in developing and selling products and technologies that we do not currently offer but intend to offer in the future. Some of our competitors also use smaller geometry process technologies in their products, which can result in better manufacturing yields and decreased costs. In addition, these competitors may have greater credibility with our existing and potential customers. Many of our current and potential customers have their own internally developed semiconductor solutions, and may choose not to purchase products from third-party suppliers like us. Increased competition could harm our business, by, for example, increasing pressure on our profit margins or causing us to lose customers. In addition, delivery of products with defects or reliability, quality or compatibility problems may damage our reputation and competitive position.

12

Our ability to compete successfully depends on a number of factors, including:

- •

- performance and robustness;

- •

- functionality;

- •

- price and cost-effectiveness;

- •

- rapid time-to-market; and

- •

- customer service and support.

We believe we currently compete favorably with respect to these factors in the aggregate. However, we cannot assure you that our semiconductor products will continue to compete favorably or that we will be successful in the face of increasing competition from new products and enhancements introduced by existing competitors or new companies entering our market.

As of December 31, 2009, we employed 206 full-time employees, including 114 in research and development, 56 in sales, marketing and support, 19 in operations and 17 in general and administration. We have never had a work stoppage and none of our employees is represented by a labor organization or under any collective bargaining arrangements. We consider our employee relations to be good.

We were incorporated in California in 1997 and reincorporated in Delaware in 2006. The mailing address of our headquarters is 408 E. Plumeria Drive, San Jose, California 95134, and our telephone number at that location is (408) 435-3888. Our website is www.techwellinc.com. Through a link on the Investor Relations section of our website, we make available the following filings as soon as reasonably practicable after they are electronically filed with or furnished to the Securities and Exchange Commission, or SEC: our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and any amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934. All such filings are available free of charge.

Executive Officers and Other Key Employees

The following table shows information about our executive officers and other key employees as of February 28, 2010:

Name

|

Age | Position | ||

|---|---|---|---|---|

| Fumihiro Kozato | 50 | President, Chief Executive Officer and Director | ||

| Mark Voll | 55 | Vice President of Finance and Administration and Chief Financial Officer | ||

| Dr. Feng Kuo | 52 | Senior Vice President and Chief Technical Officer | ||

| Dong Wook (David) Nam | 42 | Vice President of Sales and Marketing | ||

| Joe Kamei | 53 | Vice President of Operations |

Fumihiro Kozato founded Techwell in 1997 and has served as our president and chief executive officer since inception. From 1995 to 1996, Mr. Kozato was president of Sigmax Technologies, Inc., a CD-ROM controller chip development company. From 1991 to 1995, Mr. Kozato was the business control manager for Ricoh Co., Ltd, a global manufacturer of office automation equipment. Mr. Kozato holds a B.S. in mathematics from the University of California, Santa Barbara.

13

Mark Voll has served as our vice president of finance and administration and chief financial officer since November 2005. From December 2004 to July 2005, Mr. Voll served as the interim chief executive officer of Monolithic System Technology, Inc., a semiconductor intellectual property licensing company. From June 2002 to November 2005, Mr. Voll served as chief financial officer at Monolithic System Technology, Inc. From June 2000 to June 2002, Mr. Voll served as the chief financial officer for Axis Systems, Inc., a developer of semiconductor verification tools. Mr. Voll holds a B.S. in accounting from Providence College.

Dr. Feng Kuo has served as our vice president of engineering from 1998 to 2000, our chief technical officer since 2000 and our senior vice president and chief technical officer since 2009. From 1994 to 1996, Dr. Kuo was the vice president of engineering of Sigmax Technologies, Inc., a CD-ROM controller chip development company. From 1991 to 1994, Dr. Kuo was a design manager at S-MOS systems, a Seiko Epson Corporation affiliated company responsible for semiconductor development and silicon foundry service. Dr. Kuo holds a B.S. in electrical engineering from National Taiwan University and an M.S. and Ph.D. from Stony Brook University of New York.

Dong Wook (David) Nam has served as our vice president of sales and marketing since July 2005. From October 2002 to June 2005, Mr. Nam served as our director of sales and from January 2001 to February 2002, he served as our field applications engineer manager. From January 1994 to January 2001, Mr. Nam was a technical applications and marketing engineer at Samsung Electronics Co., Ltd., a large consumer electronics company. Mr. Nam holds a B.S. in electrical engineering from KyungPook National University in South Korea.

Joe Kamei has served as our vice president of operations since July 2007 and our director of operations from May 2000 to June 2006. From 1998 to 2000, Mr. Kamei was a manager at Kanematsu USA Inc., a Japanese general trading company. From 1991 to 1998, Mr. Kamei was an engineering manager at Ricoh Co., Ltd., a global manufacturer of office automation equipment. Mr. Kamei holds a B.S. of precise machinery engineering from Tokyo University.

If any of the following risks actually occur, our business, results of operations and financial condition could suffer significantly.

Risks Related to Our Business

Fluctuations in our revenue and operating results on a quarterly basis could cause the market price of our common stock to decline.

Our revenue and operating results are difficult to predict, have in the past fluctuated, and may in the future fluctuate from quarter to quarter. It is possible that our operating results in some quarters will be below market expectations. This would likely cause the market price of our common stock to decline. Our quarterly operating results are affected by a number of factors, including:

- •

- unpredictable volume and timing of customer orders, which are not fixed by contract and vary on a purchase order basis;

- •

- uncertain demand in our two primary end markets for our products;

- •

- the loss of one or more of our customers, causing a significant reduction or postponement of orders from these customers;

- •

- decreases in the overall average selling prices of our products;

- •

- changes in the relative sales mix of our products;

- •

- changes in our cost of finished goods;

14

- •

- the availability, pricing and timeliness of delivery of other components used in our customers' products;

- •

- our customers' sales outlook, purchasing patterns and inventory adjustments based on demands and general economic

conditions;

- •

- product obsolescence and our ability to manage product transitions;

- •

- our ability to successfully develop, introduce and sell new or enhanced products in a timely manner;

- •

- the timing of new product announcements or introductions by us or by our competitors; and

- •

- fluctuations in our effective tax rate.

We base our planned operating expenses in part on our expectations of future revenue, and a significant portion of our expenses is relatively fixed in the short-term. We have limited historical financial data from which to predict future sales for our products. As a result, it is difficult for us to forecast our future revenue and budget our operating expenses accordingly. If revenue for a particular quarter is lower than we expect, we likely will be unable to proportionately reduce our operating expenses for that quarter, which would harm our operating results for that quarter.

We may not sustain or increase profitability in the future, which may cause the market price of our common stock to decline.

To sustain or increase profitability, we will need to generate and sustain substantially higher revenue while maintaining reasonable cost and expense levels. We currently expect to increase expense levels in each of the next several quarters to support increased research and development efforts. These expenditures may not result in increased revenue or customer growth. Because many of our expenses are fixed in the short-term, or are incurred in advance of anticipated sales, we may not be able to decrease our expenses in a timely manner to offset any shortfall of sales. We also believe our future effective tax rate will be at or near the current statutory tax rate, which is higher than our average historical annual effective tax rate. This will harm our future financial results and negatively impact our profitability. We may not be able to sustain or increase profitability on a quarterly or an annual basis. This may, in turn, cause the price of our common stock to decline.

The demand for our products is affected by general economic conditions, which could impact our business.

The United States and international economies are currently experiencing a period of economic downturn. The timing of sustained economic recovery, if any, is uncertain. In addition, terrorist acts and similar events, turmoil in the Middle East or war in general, could contribute to a slowdown of the market demand for our products. If the economy continues to slow down as a result of the recent economic, political and social turmoil, or if there are further terrorist attacks in the United States or elsewhere, we may experience decreases in the demand for our products, which may harm our operating results. Our business has been adversely affected by the current economic downturn. Demand for our products has suffered as customers delay purchasing decisions or change or reduce their discretionary spending.

Fluctuations in demand for our products may harm our financial results and are difficult to forecast.

Current uncertainty in global economic conditions pose a risk to the overall economy as consumers and businesses may delay or postpone purchases in response to tighter credit and negative financial

15

news, which could negatively affect demand for our products. Consequently, demand could be different from our expectations due to many factors including:

- •

- changes in business and economic conditions, including conditions in the credit market that could affect consumer

confidence;

- •

- customer acceptance of our products;

- •

- changes in customer order patterns including order cancellations; and

- •

- changes in the level of inventory at customers.

If the growth of demand for digital video applications for the security surveillance and automotive infotainment markets does not continue, our ability to increase our revenue could suffer.

Our ability to increase our revenue will depend on increased demand for digital video applications in the security surveillance and automotive infotainment markets. In 2009, 70% of our revenue was derived from the sale of our products designed for the security surveillance market. If our products sold into this market decline or do not increase, or if demand slows in this market generally, our operating results would suffer. In addition, we have increased our focus on the automotive infotainment market and devoted substantial resources to the development of products for digital video applications that address this market. If we are not successful in selling our products into this market, or if the automotive infotainment industry in general continues to experience weak demand, we may not recover the costs associated with our efforts in this area and our operating results could suffer.

The growth of our target markets is uncertain and will depend in particular upon:

- •

- the pace at which new digital video applications are adopted;

- •

- a continued reduction in the costs of products in these markets;

- •

- the availability, at a reasonable price, of components required by such products, such as LCD panels; and

- •

- consumer confidence and the continued increase of consumer spending levels.

Our success depends on our ability to develop and introduce new products, which we may not be able to do in a timely manner, as product development in smaller wafer fabrication geometries becomes more complex and costly.

The development of new products is highly complex, and we have experienced some delays in bringing new products to the market in the past. As our products integrate new, more advanced functions, they become more complex and increasingly difficult to design. In addition, in our effort to decrease cost, we intend to design new products in smaller fabrication geometries, some of which we may have no prior experience of success. In the past, we have experienced some difficulties in shifting to smaller geometry process technologies.

Completing these projects is extremely challenging, time-consuming and expensive, and we can give no assurance that we will succeed or succeed in a timely and cost-effective manner. Product development delays may result from unanticipated engineering complexities, changing market or competitive product requirements or specifications, difficulties in overcoming resource limitations, the inability to license third-party technology or other factors. If we are unable to develop products successfully, in a timely and cost-effective manner, our business, financial condition and results of operations could suffer.

16

The average selling prices of our semiconductor products may be subject to rapid price declines, which could harm our revenue and gross profits.

The semiconductor products we develop and sell may be subject to rapid declines in average selling prices. From time to time, we have had to reduce our prices significantly to meet customer requirements, and we may be required to reduce our prices in the future. This would cause our gross margins to decline which in turn may negatively impact our operating results. Our financial results will suffer if we are unable to offset any reductions in our average selling prices by increasing our sales volumes, reducing our costs or developing new or enhanced products on a timely basis with higher selling prices or gross margins.

We face intense competition and may not be able to compete effectively, which could reduce our market share and decrease our revenue and profitability.

The markets in which we operate are extremely competitive and are characterized by rapid technological change, continuous evolving customer requirements and declining average selling prices. We may not be able to compete successfully against current or potential competitors. If we do not compete successfully, our market share and revenue may decline. We compete with large semiconductor manufacturers and designers, and our current and potential competitors have longer operating histories, significantly greater resources and name recognition and a larger base of customers than we do. This may allow them to respond more quickly than we can to new or emerging technologies or changes in customer requirements. In addition, these competitors may have greater credibility with our existing and potential customers. Many of our current and potential customers have their own internally developed semiconductor solutions and may choose not to purchase products from third-party suppliers like us.

We depend on key and highly skilled personnel to operate our business, and if we are unable to retain our current personnel and hire additional personnel, our ability to develop and market our products could be harmed.

We believe our future success will depend in large part upon our ability to attract and retain highly skilled managerial, engineering and sales and marketing personnel. The loss of any key employees or the inability to attract or retain qualified personnel could delay the development and introduction of, and harm our ability to sell, our products and harm the market's perception of us. We believe that our future success is highly dependent on the contributions of Fumihiro Kozato, our president and chief executive officer, and Dr. Feng Kuo, our senior vice president and chief technical officer. We do not have long-term employment contracts with these or any other key personnel, and their knowledge of our business and industry would be extremely difficult to replace.

If we fail to develop new products and enhance our existing products in order to react to rapid technological change and market demands, our business will suffer.

We must develop new products and enhance our existing products with improved technologies to meet rapidly evolving customer requirements. We need to design products for customers who continually require higher performance and functionality at lower costs. We must, therefore, continue to cost-effectively add features that enhance performance and functionality to our products. The development process for these advancements is lengthy and requires us to accurately anticipate market trends. Our failure to accurately anticipate market trends in a timely manner will harm the market acceptance of our products and the sales of our products.

Developing and enhancing these products is uncertain and can be time-consuming, costly and complex. There is a risk that these developments and enhancements will be late, fail to meet customer or market specifications or not be competitive with products from our competitors that offer

17

comparable or superior performance and functionality. Any new products or product enhancements may not be accepted in new or existing markets. Our business will suffer if we fail to develop and introduce new products or product enhancements on a cost-effective basis.

If we fail to achieve initial design wins for our products, we may lose the opportunity for sales for a significant period of time to customers and be unable to recoup our investments in our products.

We expend considerable resources in order to achieve design wins for our products, especially our new products and product enhancements. Once a customer designs a semiconductor into a product, it is likely to continue to use the same semiconductor or enhanced versions of that semiconductor from the same supplier across a number of similar and successor products for a lengthy period of time due to the significant costs associated with qualifying a new supplier and potentially redesigning the product to incorporate a different semiconductor. If we fail to achieve an initial design win in a customer's qualification process, we may lose the opportunity for significant sales to that customer for a number of its products and for a lengthy period of time. This may cause us to be unable to recoup our investments in our products, which would harm our business.

If we fail to develop, in a timely manner, or at all, technologies that address the demands of a shift from analog video signals to digital video signals, our operating results could suffer.

Our semiconductors are principally designed to decode analog video signals into digital images. On June 12, 2009, transmission of broadcast TV signals were no longer permitted in analog and all broadcast signals must be in a digital format. Current forecasts project that many other electronic products and applications will similarly transition to digital transmission. We are developing mixed signal and digital technologies to decode digital signals. However, transmission of digital video involves a combination of emerging technologies. The complexities of these technologies and the variability in implementations between manufacturers may cause our development of semiconductors to be costly and time-consuming. We may never obtain the benefits of our investment in developing these technologies. The complexities of digital broadcast technologies may also cause some of the semiconductors we are developing to ultimately work incorrectly for reasons that may be either related or unrelated to our products, or not be interoperable with other key products. Delays or difficulties in integrating our semiconductors into digital broadcast products or the failure of products incorporating digital video to achieve broad market acceptance could have an adverse effect on our business.

Our business is subject to seasonality, which is likely to cause our revenue to fluctuate.

Our business is subject to seasonality as a result of the location of our customers. We sell a significant number of our semiconductors to customers located in Asia, primarily to customers located in regions who observe the Lunar New Year holiday, also referred to as Chinese New Year. Typically, our foreign offices and those of our customers are closed for a week or more during the extended holiday period. In 2009, 91% of our revenue was attributable to customers located in regions that observe the Lunar New Year holiday. As a result, we typically experience fluctuations in our first calendar quarter due in part to a slowing of business activity around the period of the Lunar New Year holiday.

We manufacture our products based on our estimates of customer demand, and if our estimates are incorrect our financial results could be negatively impacted.

Our sales are made on the basis of purchase orders rather than long-term purchase commitments. In addition, our customers may cancel purchase orders or defer the shipments of our products. We manufacture our products according to our estimates of customer demand. This process requires us to make multiple demand forecast assumptions, each of which may introduce error into our estimates. If we overestimate customer demand, we may manufacture products that we may not be able to sell. As a result, we would have excess inventory, which would increase our losses. Conversely, if we underestimate customer demand or if sufficient manufacturing capacity were unavailable, we would forego revenue opportunities, lose market share and damage our customer relationships.

18

We do not expect to sustain the growth rate of our recent revenue.

Our revenue increased 109% in 2005 from 2004 and 49% in 2006 from 2005. We do not expect to achieve similar growth rates in future periods. For example, our revenue increased 11% in 2007 from 2006 and 13% in 2008 compared to 2007 and decreased 7% in the 2009 compared to 2008. You should not rely on the results of any prior quarterly or annual periods as an indication of our future operating performance. If we are unable to maintain adequate revenue growth, our stock price may decline and we may not have adequate financial resources to execute our business objectives.

We may pursue acquisitions or investments in complementary technologies and businesses, which could harm our operating results and may disrupt our business.

We have pursued and may continue to pursue acquisitions of, or investments in, complementary technologies and businesses. For example, we acquired substantially all of the assets of a development stage company in October 2009. Acquisitions present a number of potential risks and challenges that could, if not successfully addressed, disrupt our business operations, increase our operating costs and reduce the value to us of the acquired company. Even if we are successful, we may not be able to integrate the acquired businesses, products or technologies into our existing business and products. Furthermore, potential acquisitions and investments, whether or not consummated, may divert management's attention and require considerable cash outlays at the expense of existing operations. In addition, to complete future acquisitions, we may issue equity securities, incur debt, assume contingent liabilities or have amortization expenses and write-downs of acquired assets, which could adversely affect our profitability.

Changes in our tax rates will affect our future results.

Our future effective tax rates will be favorably or unfavorably affected by the absolute amount and future geographic distribution of our pre-tax income, our ability to take advantage of the available tax planning strategies and the availability of tax credits. In addition, we are subject to the examination of our income tax returns by the Internal Revenue Service and other tax authorities. The outcomes of these examinations, when and if they occur, could harm our financial condition.

We may not be able to manage our future growth effectively, and we may need to incur significant expenditures to address the additional operational and control requirements of our growth.

We have experienced a period of significant growth and expansion, which has placed, and any future expansion will continue to place, a significant strain on management, personnel, systems and financial resources. We have hired additional employees to support an increase in research and development as well as increase our sales and marketing efforts, which resulted in increasing our headcount from 96 employees as of December 31, 2006 to 206 employees as of December 31, 2009. To manage our growth successfully, we believe we must effectively:

- •

- train, integrate and manage additional qualified engineers for research and development activities, sales and marketing

personnel and financial and information technology personnel;

- •

- continue to enhance our customer resource management and manufacturing management systems;

- •

- implement additional and improve existing administrative, financial and operations systems, procedures and controls,

including the requirements of the Sarbanes-Oxley Act of 2002;

- •

- expand and upgrade our technological capabilities; and

- •

- manage multiple relationships with our customers, distributors, suppliers and other third-parties.

19

Our efforts may require substantial managerial and financial resources and may increase our operating costs even though these efforts may not be successful. If we are unable to manage our growth effectively, we may not be able to take advantage of market opportunities, develop new products, satisfy customer requirements, execute our business plan or respond to competitive pressures.

We may experience unforeseen delays, expenses or lower than expected product yields for our semiconductors manufactured by our third-party vendors, which could increase our costs and prevent us from recognizing the benefits of new technologies we develop.

We occasionally have experienced delays in completing the development and introduction of new products and product enhancements, and we could experience delays in the future that may render our new or enhanced products, when introduced, obsolete and unmarketable. In addition, it is often difficult for semiconductor foundries to achieve satisfactory product yields. Product yields depend on both our product design and the manufacturing process technology unique to the semiconductor foundry. Since low yields may result from either design or process difficulties, identifying yield problems can only occur well into the production cycle after a product that can be physically analyzed and tested exists. Poor yields from our foundry could cause us to sell our products at lower gross margins and therefore harm our financial results.

Defects in our products could increase our costs, cause customer claims and delay our product shipments.

Although we test our products, they are complex and may contain defects and errors. In the past, we have encountered defects and errors in our products. Delivery of products with defects or reliability, quality or compatibility problems may damage our reputation and our ability to retain existing customers and attract new customers. In addition, product defects and errors could result in additional development costs, diversion of technical resources, delayed product shipments, increased product returns and product liability claims against us, which may not be fully covered by insurance. Any of these could harm our business.

We rely on a limited number of independent subcontractors for the manufacture, assembly and testing of our semiconductors, and the failure of any of these third-party vendors to deliver products or otherwise perform as requested could damage our relationships with our customers, decrease our sales and limit our growth.

We do not have our own manufacturing or assembly facilities and have very limited in-house testing facilities. Therefore, we must rely on third-party vendors to manufacture, assemble and test the products we design. We currently rely on Taiwan Semiconductor Manufacturing Company, or TSMC, to produce the majority of our semiconductors. We rely on Advanced Semiconductor Engineering, Inc., or ASE, to assemble, package and test many of our products. If these vendors do not provide us with high-quality products, services and production and test capacity in a timely manner, or if one or more of these vendors terminates its relationship with us, we may be unable to obtain satisfactory replacements to fulfill customer orders on a timely basis, our relationships with our customers could suffer and our sales could decrease. Other significant risks associated with relying on these third-party vendors include:

- •

- reduced control over product cost, delivery schedules and product quality;

- •

- potential price increases;

- •

- inability to achieve required production or test capacity and achieve acceptable yields on a timely basis;

- •

- longer delivery times;

- •

- increased exposure to potential misappropriation of our intellectual property;

- •

- shortages of materials that foundries use to manufacture products;

20

- •

- labor shortages or labor strikes; and

- •

- quarantines or closures of manufacturing facilities due to the outbreak of viruses, such as SARS, the avian flu or any similar future outbreaks in Asia.

We currently do not have long-term supply contracts with any of our third-party vendors. Therefore, they are not obligated to perform services or supply products to us for any specific period, in any specific quantities or at any specific price, except as may be provided in a particular purchase order. Neither TSMC nor ASE has provided contractual assurances to us that adequate capacity will be available for us to meet future demand for our products. These third-party vendors may allocate capacity to the production of other companies' products while reducing deliveries to us on short notice. In particular, other customers that are larger and better financed than we are or that have long-term agreements with TSMC or ASE may cause either or both of them to reallocate capacity to those customers, decreasing the capacity available to us.

We plan to retain additional foundries to manufacture our semiconductors, which could disrupt our current manufacturing process and negatively impact our sales volumes and revenue.

We are a fabless semiconductor company which relies on third-party manufacturers or foundries to manufacture our semiconductors. We are reliant on these foundries for the manufacture of our products as well as providing services to assist us in getting our products into production. As a result of the complexity in manufacturing our semiconductors, it is difficult to determine if a new foundry will be able to successfully produce our products. We may not be able to enter into a relationship with a new foundry that produces satisfactory yields on a cost-effective basis. If we need another foundry because of increased demand, or the inability to obtain timely and adequate deliveries from our current provider, we might not be able to cost-effectively and quickly retain other vendors to satisfy our requirements. Any failure to successfully integrate a new foundry could negatively impact our sales volumes and revenue.

Our business depends on customers, suppliers and operations in Asia, and as a result we are subject to regulatory, operational, financial and political risks, which could adversely affect our financial results.

The percentage of our revenue attributable to sales to customers in Asia was 97%, 98% and 98% in 2009, 2008 and 2007, respectively. We expect that revenue from customers in Asia will continue to account for substantially all of our revenue. All our sales currently are denominated in U.S. dollars. As a result, an increase in the value of the U.S. dollar relative to foreign currencies could make our products less competitive in international markets.

Currently, we maintain international sales offices in Asia, and we rely on a network of third-party sales representatives to sell our products internationally. We have offices in China, Japan, Taiwan and South Korea, which serve various aspects of our business. Moreover, we have in the past relied on, and expect to continue to rely on, suppliers, manufacturers and subcontractors primarily located in Taiwan. Accordingly, we are subject to several risks and challenges, any of which could harm our business and financial results. These risks and challenges include:

- •

- difficulties and costs of staffing and managing international operations across different geographic areas and cultures;

- •

- compliance with a wide variety of domestic and foreign laws and regulations, including those relating to the import or

export of semiconductor products;

- •

- legal uncertainties regarding taxes, tariffs, quotas, export controls, export licenses and other trade barriers;

- •

- foreign currency exchange fluctuations relating to our international operating activities;

21

- •

- our ability to receive timely payment and collect our accounts receivable;

- •

- political, legal and economic instability, foreign conflicts and the impact of regional and global infectious illnesses,

such as the SARS outbreak or avian flu in the countries in which we and our customers, suppliers, manufacturers and subcontractors are located;

- •

- legal uncertainties regarding protection for intellectual property rights in some countries; and

- •

- fluctuations in freight rates and transportation disruptions.

Our sales cycle can be lengthy, which could result in uncertainty and delays in generating revenue.

Because our products are based on constantly evolving technologies, we have experienced a lengthy sales cycle for some of our semiconductors, particularly those designed for digital video applications in the automotive infotainment market. Our sales cycle typically ranges from six to 24 months. We may experience a delay between the time we increase expenditures for research and development, sales and marketing efforts and inventory to the time we generate revenue, if any, from these expenditures. In addition, because we do not have long-term commitments from our customers, we must repeat our sales process on a continual basis even for current customers looking to purchase a new product. As a result, our business could be harmed if a customer reduces or delays its orders, chooses not to release products incorporating our semiconductors or elects not to purchase a new product or product enhancements from us.

We primarily sell our products through a limited number of distributors, and if our relationships with one or more of those distributors were to terminate, our operating results may be harmed.

We market and distribute our products primarily through a limited number of distributors, most of which are located in Asia. This distribution channel has been characterized by rapid change and consolidations. Distributors have accounted for a significant portion of our revenue in the past. Sales to our distributors represented 72%, 79% and 77% of our revenue in 2009, 2008 and 2007, respectively. In 2009, one of our distributors, Lacewood International Corporation, accounted for 35% of our revenue. We do not have any long-term contractual commitments with our distributors.

Our operating results and financial condition could be significantly disrupted by the loss of one or more of our current distributors and sales representatives, volume pricing discounts, order cancellations, delays in shipment by one of our major distributors or sales representatives or the failure of our distributors or sales representatives to successfully sell our products.

We face risks associated with doing business in China.