Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Employers Holdings, Inc. | form8-k.htm |

Exhibit 99.1

Employers Holdings, Inc.

Investor Presentation

March, 2010

1

Safe Harbor Disclosure

This slide presentation is for informational purposes only. It should be read in conjunction with our Form 10-K for the year 2009, our Form 10-Qs and our

Form 8-Ks filed with the Securities and Exchange Commission (SEC), all of which are available on the “Investor Relations” section of our website at

www.employers.com.

Form 8-Ks filed with the Securities and Exchange Commission (SEC), all of which are available on the “Investor Relations” section of our website at

www.employers.com.

Non-GAAP Financial Measures

In presenting Employers Holdings, Inc.’s (EMPLOYERS) results, management has included and discussed certain non-GAAP financial measures, as

defined in Regulation G. Management believes these non-GAAP measures better explain EMPLOYERS results allowing for a more complete

understanding of underlying trends in our business. These measures should not be viewed as a substitute for those determined in accordance with GAAP.

The reconciliation of these measures to their most comparable GAAP financial measures is included in this presentation or in our Form 10-K for the year

2009, our Form 10-Qs and our Form 8-Ks filed with the Securities and Exchange Commission (SEC) and available in the “Investor Relations” section of our

website at www.employers.com.

defined in Regulation G. Management believes these non-GAAP measures better explain EMPLOYERS results allowing for a more complete

understanding of underlying trends in our business. These measures should not be viewed as a substitute for those determined in accordance with GAAP.

The reconciliation of these measures to their most comparable GAAP financial measures is included in this presentation or in our Form 10-K for the year

2009, our Form 10-Qs and our Form 8-Ks filed with the Securities and Exchange Commission (SEC) and available in the “Investor Relations” section of our

website at www.employers.com.

Forward-looking Statements

This presentation may contain certain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-

looking statements include statements regarding anticipated future results and can be identified by the fact that they do not relate strictly to historical or

current facts. They often include words like "believe”, "expect”, "anticipate”, "estimate" and "intend" or future or conditional verbs such as "will”, "would”,

"should”, "could" or "may”. All subsequent written and oral forward-looking statements attributable to us or individuals acting on our behalf are expressly

qualified in their entirety by these cautionary statements.

looking statements include statements regarding anticipated future results and can be identified by the fact that they do not relate strictly to historical or

current facts. They often include words like "believe”, "expect”, "anticipate”, "estimate" and "intend" or future or conditional verbs such as "will”, "would”,

"should”, "could" or "may”. All subsequent written and oral forward-looking statements attributable to us or individuals acting on our behalf are expressly

qualified in their entirety by these cautionary statements.

Any forward-looking statements made in this presentation reflect EMPLOYERS current views with respect to future events, business transactions and

business performance and are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Such statements

involve risks and uncertainties, which may cause actual results to differ materially from those set forth in these statements.

business performance and are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Such statements

involve risks and uncertainties, which may cause actual results to differ materially from those set forth in these statements.

We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

Copyright © 2010 EMPLOYERS. All rights reserved. EMPLOYERS® and America’s small business insurance specialist.® are registered trademarks of Employers Insurance

Company of Nevada. Employers Holdings, Inc. is a holding company with subsidiaries that are specialty providers of workers’ compensation insurance and services focused

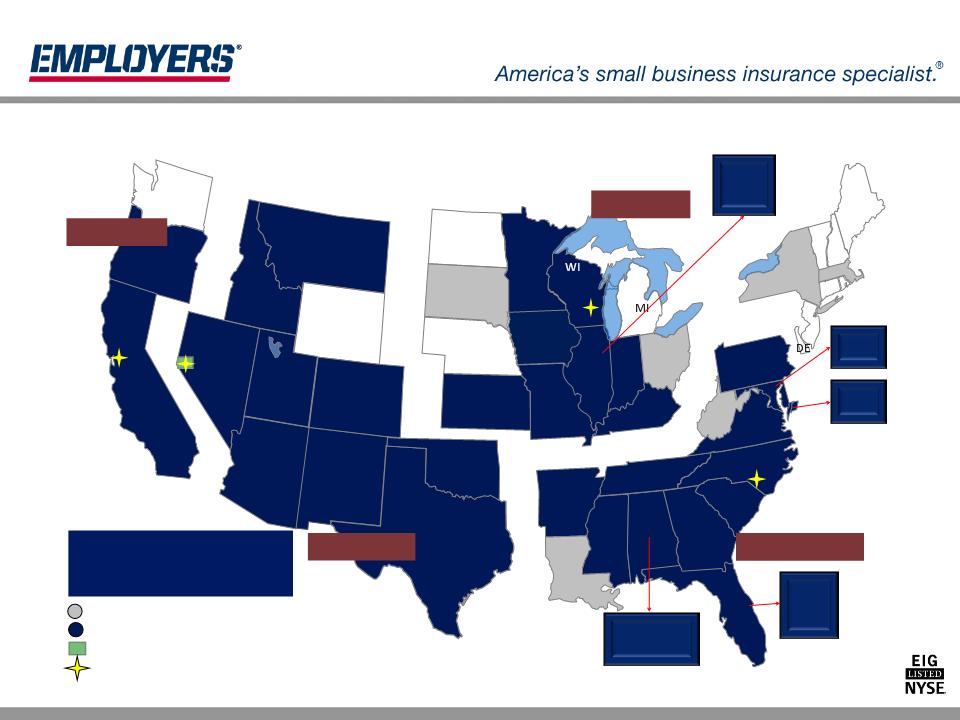

on select, small businesses engaged in low to medium hazard industries. The company, through its subsidiaries, operates in 30 states. Insurance subsidiaries include

Employers Insurance Company of Nevada, Employers Compensation Insurance Company, Employers Preferred Insurance Company, and Employers Assurance Company, all

rated A- (Excellent) by A.M. Best Company. Additional information can be found at: http://www.employers.com.

Company of Nevada. Employers Holdings, Inc. is a holding company with subsidiaries that are specialty providers of workers’ compensation insurance and services focused

on select, small businesses engaged in low to medium hazard industries. The company, through its subsidiaries, operates in 30 states. Insurance subsidiaries include

Employers Insurance Company of Nevada, Employers Compensation Insurance Company, Employers Preferred Insurance Company, and Employers Assurance Company, all

rated A- (Excellent) by A.M. Best Company. Additional information can be found at: http://www.employers.com.

2

Overview

Business

· Specialty provider of workers’ compensation

insurance

insurance

· Coverage required by statute

Ø Medical, temporary/permanent indemnity, death

Geographic

· 30 states with concentrations in CA, FL, WI, IL and

NV

NV

Ø Unique markets by state and area

Customers

· Small “main street” businesses

· Low-to-medium hazard exposure industries

Ø Top classes include restaurants, physicians, dentists,

clerical, retail stores

clerical, retail stores

· Distribution through agents and strategic partners

$45 billion

per year

industry

(2008, A.M. Best)

per year

industry

(2008, A.M. Best)

Highly

focused

business

model

focused

business

model

Operate in

74% of total

market

(2008, A.M. Best)

74% of total

market

(2008, A.M. Best)

3

Key Strategies

FOCUS

GROWTH

CAPITAL

• Target attractive

small business

market

• Maintain

disciplined risk

selection,

underwriting,

pricing and

claims operations

• Focus on

underwriting

profitability

• Selectively

expand into

additional

markets

• Increase

penetration in

current markets

• Leverage

infrastructure,

technology and

systems

• Develop existing

and new

distribution

partners

• Invest in core

operations

• Invest in strategic

acquisitions

• Return capital to

shareholders

4

2000

2002

2006

2007

FL

NM

MD

TX

OK

KS

NE

SD

ND

MT

WY

CO

UT

ID

AZ

NV

WA

CA

OR

KY

PA

NH

MA

CT

VA

WV

OH

IN

IL

NC

TN

SC

AL

AR

LA

MO

IA

MN

MS

VT

NJ

DE

2008

1913 - 1999

State WC

fund in NV

State WC

fund in NV

2000

Privatization

Privatization

2007

Demutualization

and IPO - entry

into FL, IL and

OR

Demutualization

and IPO - entry

into FL, IL and

OR

2002

Acquisition,

book of

business in

CA, UT, ID,

MT, CO

Acquisition,

book of

business in

CA, UT, ID,

MT, CO

2005

Formation of

mutual hold co

Formation of

mutual hold co

2008

Acquisition of

AmCOMP

Incorporated,

entry into IA

Acquisition of

AmCOMP

Incorporated,

entry into IA

2006 Entry

into TX, AZ

into TX, AZ

5

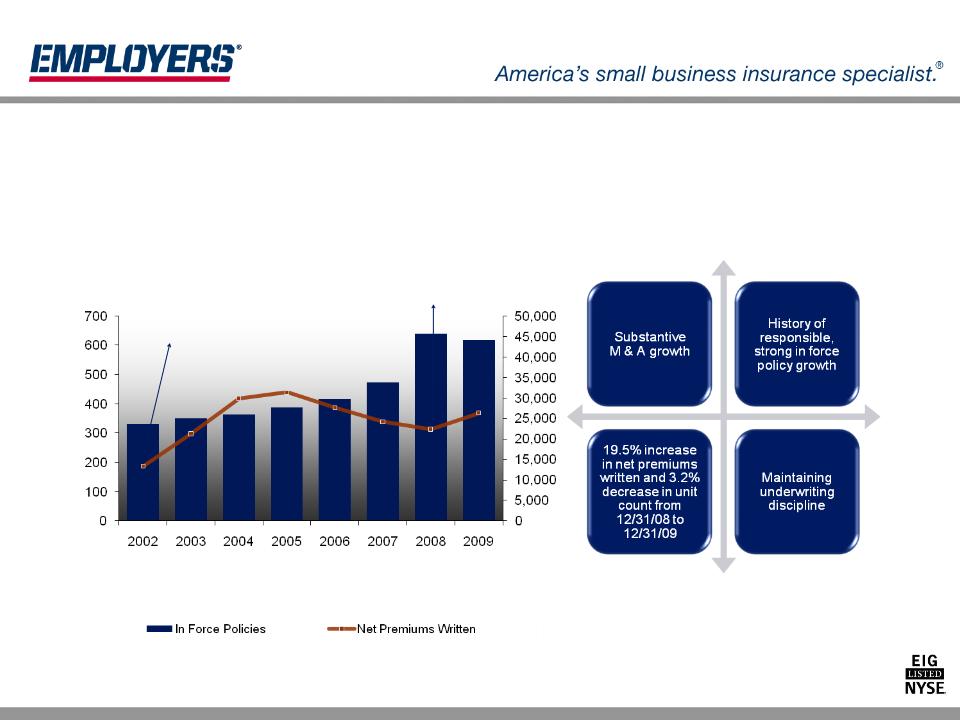

$ million

# policies

Increasing Market Penetration

Purchased

Fremont Book

of Business

Fremont Book

of Business

Purchased

AmCOMP

Incorporated

AmCOMP

Incorporated

Policy Count ‘02-’09

CAGR = 9.3%

NPW ‘02-’09 CAGR = 10.2%

6

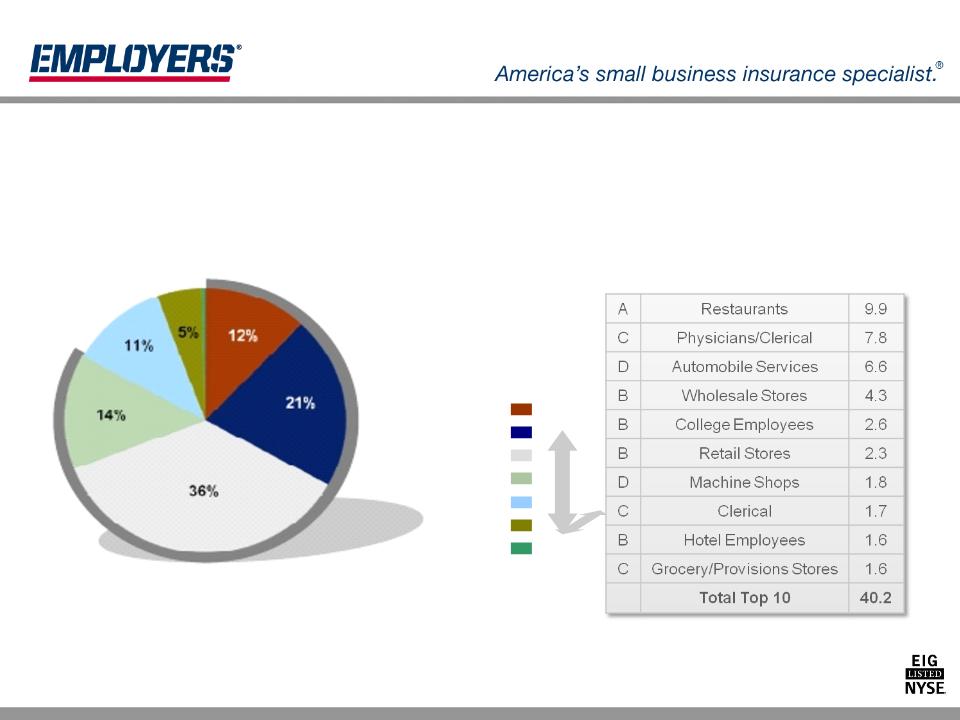

Disciplined Risk Selection

Hazard Group A

Hazard Group B

Hazard Group C

Hazard Group D

Hazard Group E

Hazard Group F

Hazard Group G

Lower

Risk

Risk

Higher

Risk

Risk

EMPLOYERS = 83% of

Total In Force Premium,

Hazard Groups A - D

Total In Force Premium,

Hazard Groups A - D

% In Force Premiums, 12/31/09

Top 10 Classes

Top 10 Classes

NCCI

Hazard

Group

Hazard

Group

%

In Force

Premium

In Force

Premium

Focused Guidelines and Selection within Industry-defined Classes

7

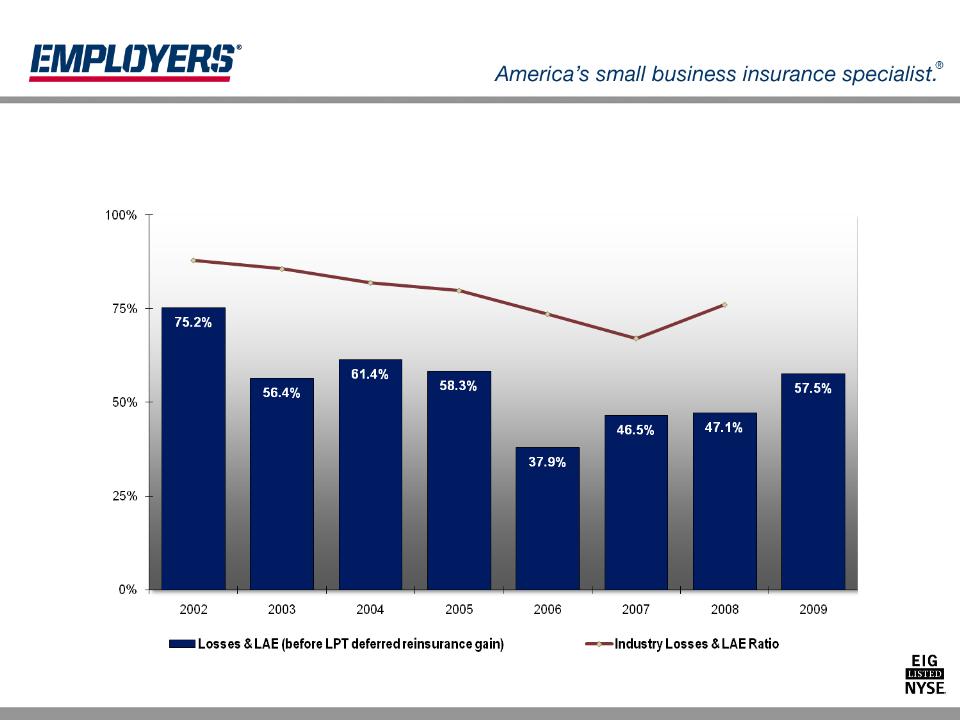

Delivering Superior Loss Ratios

Consistently Lower Loss and LAE Ratios than the Industry

A.M. Best, “Aggregates and Averages”

8

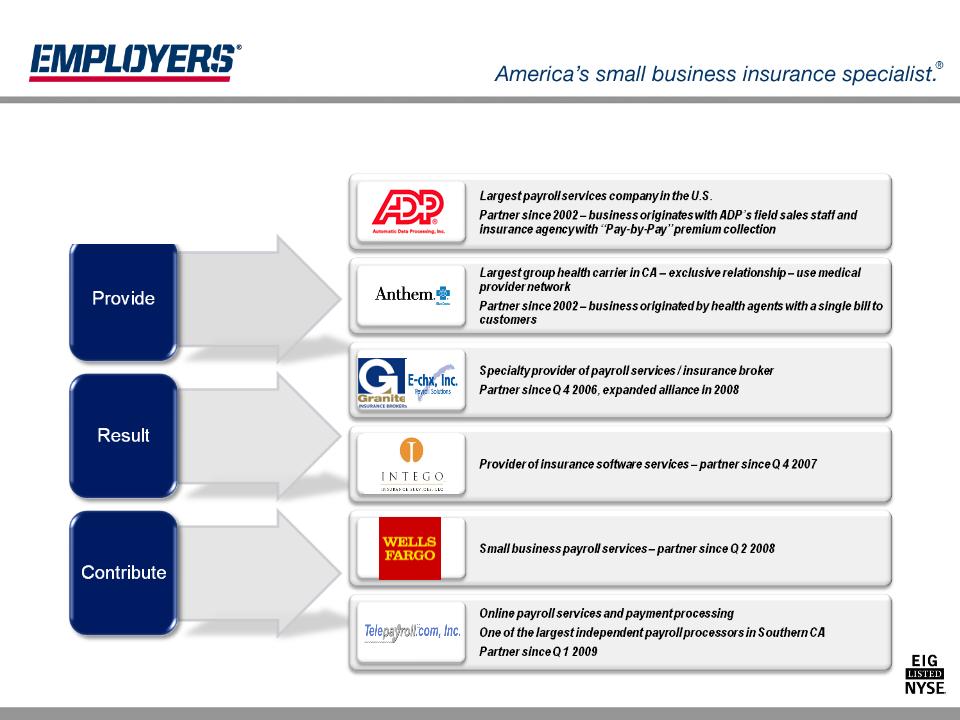

Strategic Partnerships

Unique Distribution Network

Industry Focused

• 1,600 in place

• Strong relationships

with agents

with agents

• Two key partners

Ø ADP

Ø Anthem Blue Cross

Restaurants and physicians

are our top two classes of

customers

are our top two classes of

customers

• California Restaurant Association

provider of choice

provider of choice

• California Medical Association

sponsorship

sponsorship

• NFIB (National Federation of

Independent Businesses)

Independent Businesses)

Independent Agents and Brokers

9

Increasing Points of Access

Partnerships

… a distribution

advantage by

expanding market

reach and providing

local knowledge

advantage by

expanding market

reach and providing

local knowledge

… in high persistency

… about 19% of in

force premiums in 2009

force premiums in 2009

10

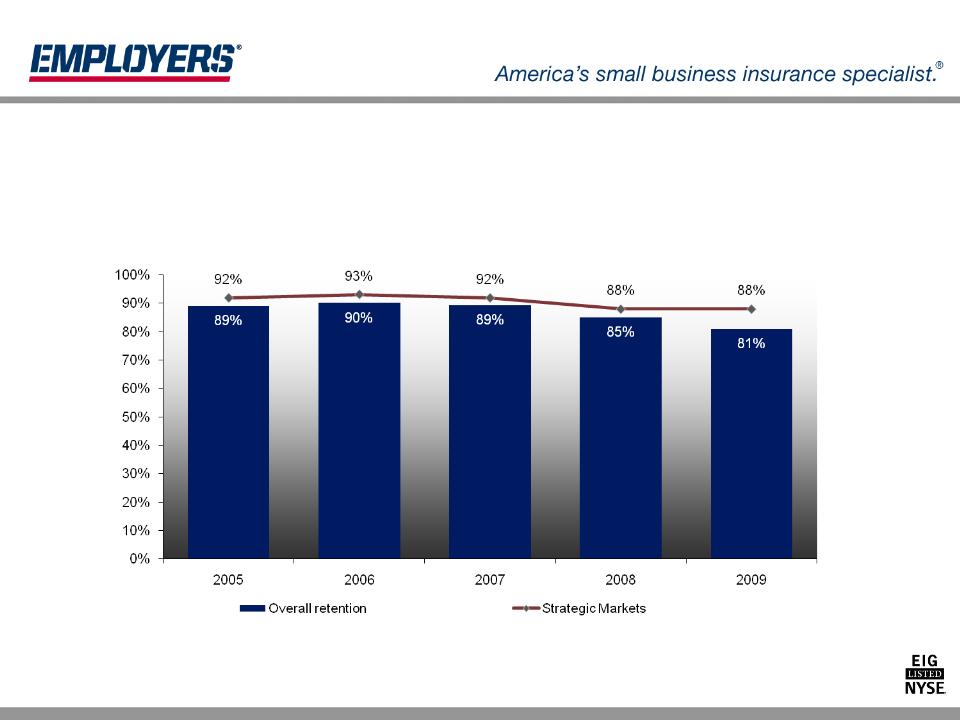

Strong Retention Rates

Strategic Partnerships Result in Consistently Higher Retention Rates

11

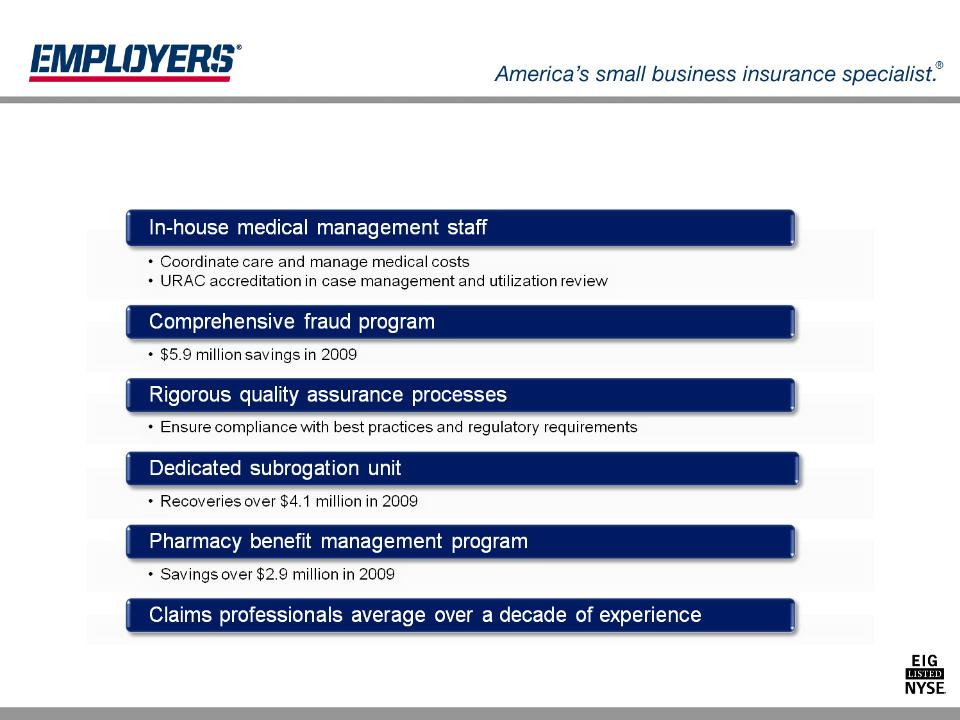

Superior Claims Management

12

Key Highlights

|

Income Statement

($ million except $ per share) |

Q 4 2009

|

Q 4 2008

|

2009

|

2008

|

|

Net Written Premium

|

72.2

|

89.0

|

368.3

|

308.3

|

|

Net Earned Premium

|

90.0

|

106.1

|

404.2

|

328.9

|

|

Net Investment Income

|

21.8

|

22.1

|

90.5

|

78.1

|

|

Net Income

|

11.3

|

15.9

|

83.0

|

101.8

|

|

Net Income Before LPT

|

6.6

|

11.3

|

65.0

|

83.4

|

|

Earnings Before LPT per Share

|

.15

|

.23

|

1.41

|

1.69

|

|

Balance Sheet ($ million)

|

12/31/2009

|

12/31/2008

|

||

|

Total Investments

|

2,029.6

|

2,042.9

|

||

|

Cash and Cash Equivalents

|

191.6

|

202.9

|

||

|

Total Assets

|

3,676.7

|

3,825.1

|

||

|

Reserves for Loss and LAE

|

2,425.7

|

2,506.5

|

||

|

Shareholders’ Equity

|

498.4

|

444.7

|

||

|

Equity Including LPT Deferred Gain

|

887.0

|

851.3

|

||

|

Underwriting Ratios

|

Q 4 2009

|

Q 4 2008

|

2009

|

2008

|

|

Loss Ratio Before LPT

|

58.2%

|

57.2%

|

57.5%

|

47.1

|

|

Combined Ratio Before LPT

|

111.7%

|

103.4%

|

102.5%

|

91.5

|

|

Financial Ratios

|

2009

|

2008

|

||

|

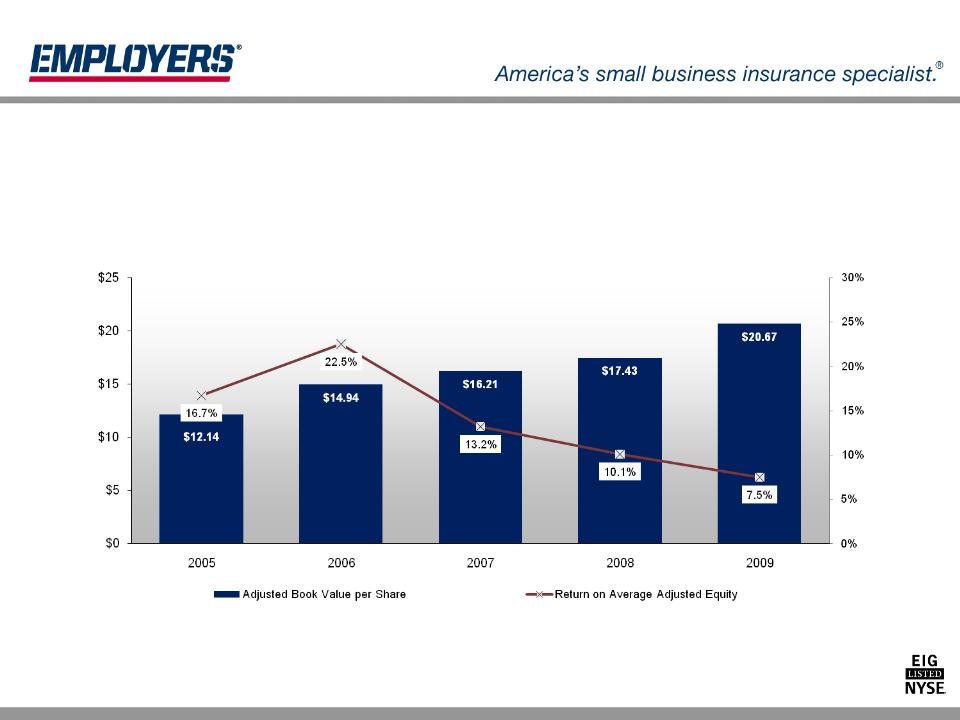

Book Value per Share

|

$20.67

|

$17.43

|

||

|

Return on Average Adjusted Equity

|

7.5%

|

10.1%

|

||

13

Strong Capital Position

($ million)

.6 to 1

NPW/Statutory

Surplus Ratio

NPW/Statutory

Surplus Ratio

$355 million

extraordinary

dividends to

parent in 2008

extraordinary

dividends to

parent in 2008

Strong Growth in Statutory Surplus Provides a Solid Basis for Underwriting

14

Loss Portfolio Transfer (LPT)

Claims 6/30/1995 and prior - Approximately 3,500 claims

open as of 12/31/09 with 5% closing each year

open as of 12/31/09 with 5% closing each year

Remaining liabilities at 12/31/09: $888.4 million

15

NOTE: 50,000,002 pro forma shares prior to February 5, 2007 (IPO date)

(millions)

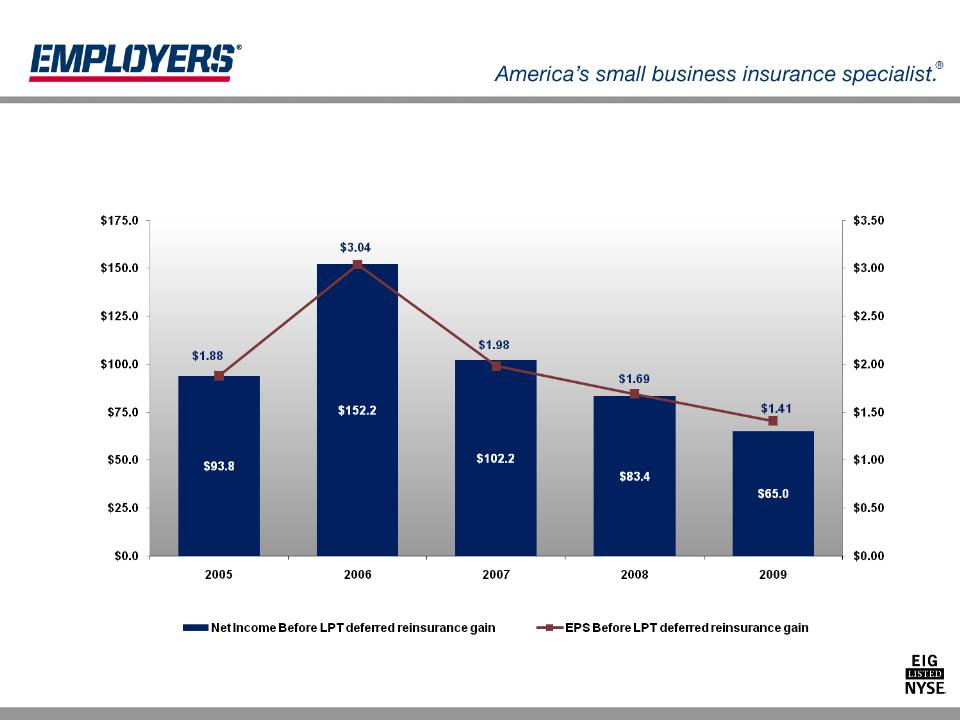

Continuing Profits

16

Return on Average Adjusted Equity, Increasing Book

Value per Share

Value per Share

NOTE: 50,000,002 pro forma shares prior to February 5, 2007 (IPO date)

Return on Average Equity includes deferred gain related to the LPT - equity in the ROE calculation is averaged for the period

(Pro forma)

(Pro forma)

(Pro forma)

17

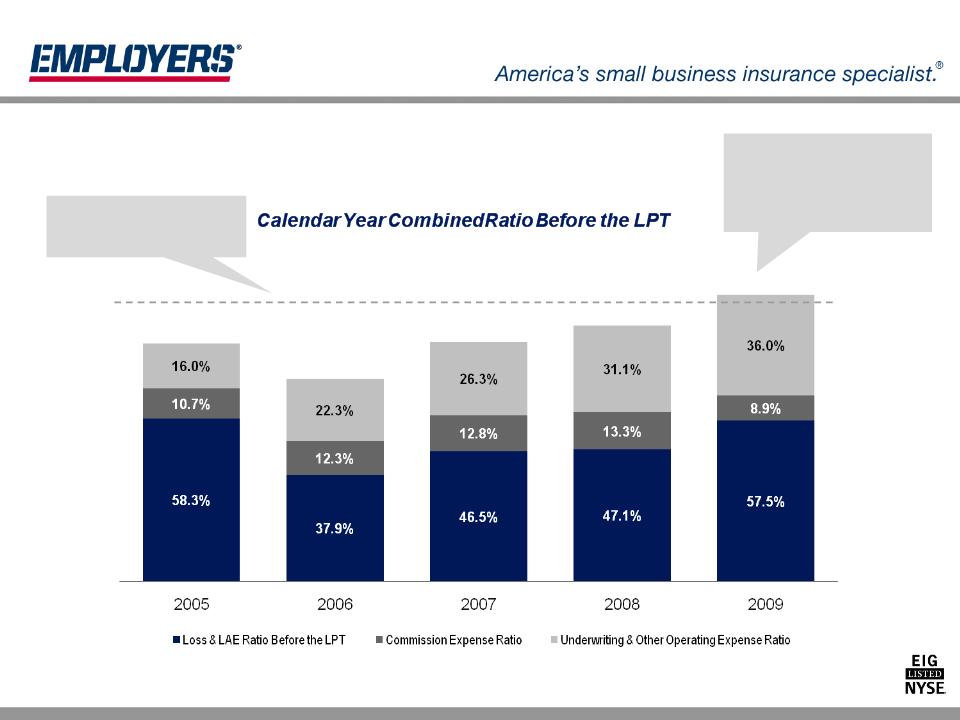

Consistently Profitable Underwriting

Underwriting model targets a

100% combined ratio and a 12-

13% return on a premium dollar

100% combined ratio and a 12-

13% return on a premium dollar

NOTE: LPT percentages include reserve adjustments

84.9%

72.6%

85.6%

(LPT is 10%)

(LPT is 4.9%)

91.5%

(LPT is 5.2%)

(LPT is 5.6%)

(LPT is 4.5%)

102.5%

Expense ratio includes 1.4 points of non-

recurring integration costs . The policyholder

dividend ratio was 1.7 points versus 0.4 last

year. LPT contingent profit commission of

$15 million lowered commission expense

ratio by 3.7 points.

recurring integration costs . The policyholder

dividend ratio was 1.7 points versus 0.4 last

year. LPT contingent profit commission of

$15 million lowered commission expense

ratio by 3.7 points.

18

History of Reserve Strength

Reserve Review

Reserve Development

Net reserves for workers’ comp industry estimated to be deficient by $6 Billion at 12/31/08 (1)

(1) NCCI, “2009 State of the Line”

Net Calendar Year Reserve Releases for

Prior Accident Years ($ million)

Prior Accident Years ($ million)

19

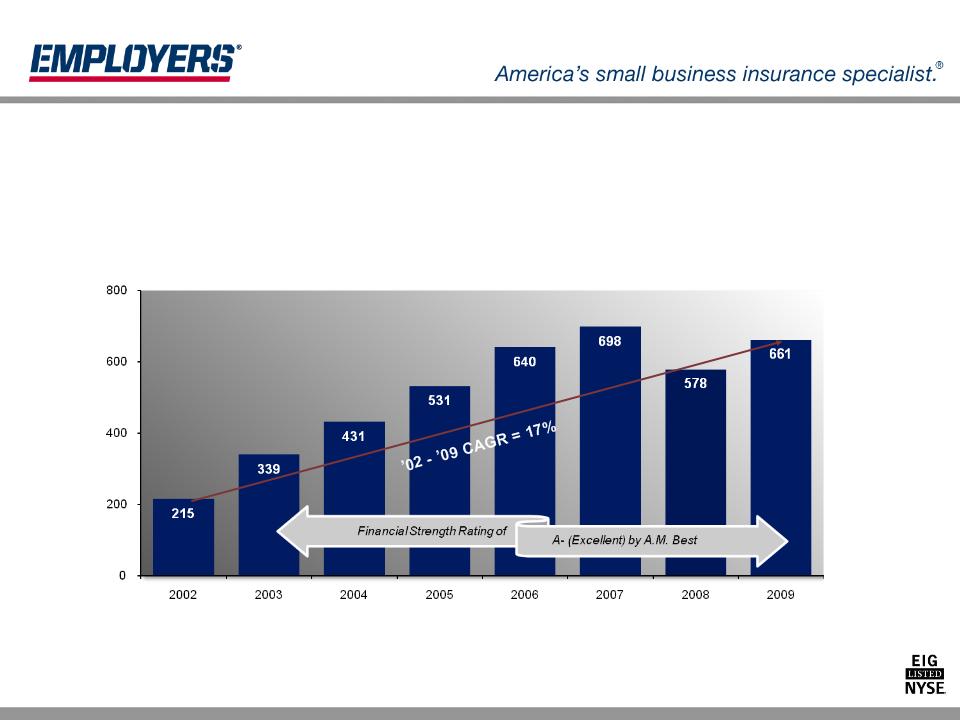

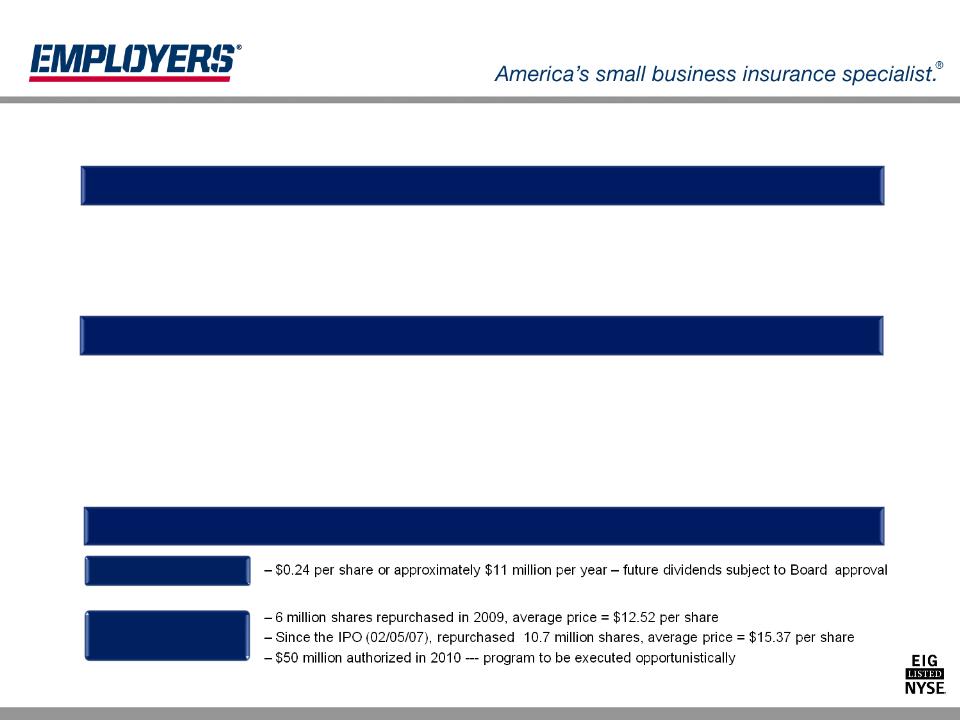

Prudent Capital Management

Share

Repurchases

Repurchases

Investing in the Future

Returning Capital to Shareholders

Holding Company Flexibility at 12/31/09

• Debt ratio - 15%

– Wells Fargo Secured Credit Facility - $100 million remaining

– $32 million of acquired surplus notes

• $197 million in cash and securities (two thirds tied to Wells Fargo Credit Facility)

• Ordinary dividend capacity from operating companies in 2010 - $114.5 million

• Generating capital to invest in operations/securities

• Deploying capital - opportunistic acquisitions

– Acquired AmCOMP (October, 2008) - equity value $189 million with expected savings of $20 - $22 million in 2010

• Controlling costs

– Generally flat Q 4 expenses excluding integration/restructuring

– Extensive budget review with staff reductions in 2009 and 2010 (acquisition savings, consolidation and recognized

efficiencies)

efficiencies)

Dividends

20

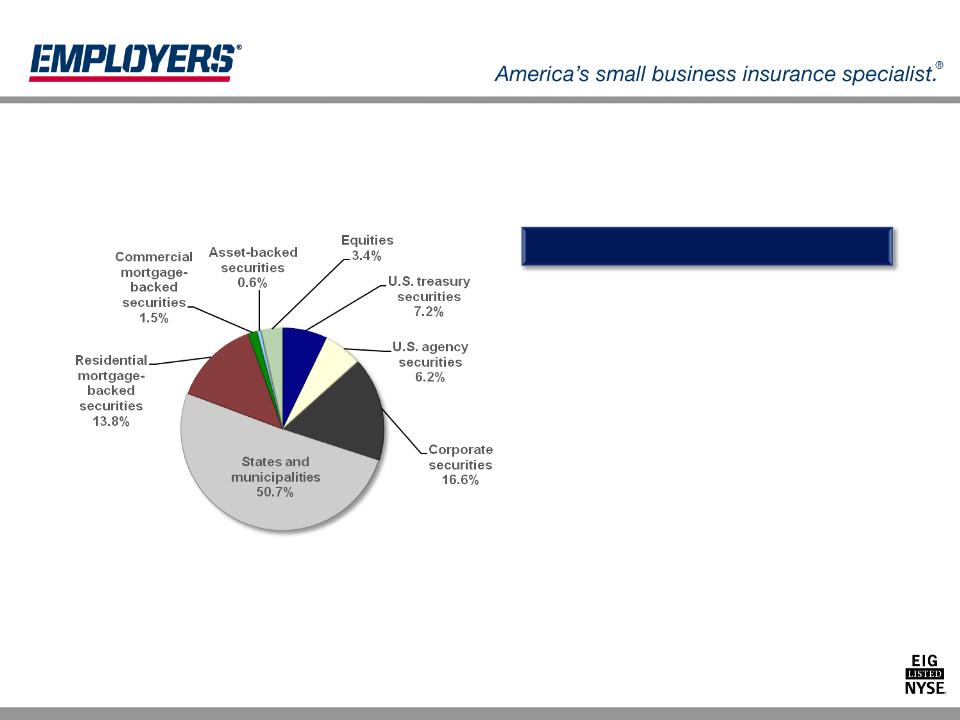

• 97% fixed maturities with an average

weighted AA+ rating

weighted AA+ rating

• Average book yield of 4.5%

• Tax equivalent book yield of 5.6%

• Effective duration of 5.02

• Managed by Conning Asset Management

• Minimal impacts during challenging

markets

markets

– 2009 OTTI of $1.9 million

– 2008 OTTI of $12.7 million

High Quality Investment Portfolio

Portfolio at 12/31/09

$2.0 billion fair market value

21

High Quality Reinsurance

Program Structure, Effective 7/1/09

Reinsurance Management

Reinsurers by Market

22

Summary of Financial Strength

Strong

Underwriting

Leverage

Conservative

Reserving

Reserving

High Quality

Investment

Portfolio

Investment

Portfolio

Catastrophe

Reinsurance

Program

Reinsurance

Program

.6 to 1 NPW to

Surplus at

12/31/09

Surplus at

12/31/09

$2 billion - 97%

invested in fixed

maturity with average

weighted rating of AA+

invested in fixed

maturity with average

weighted rating of AA+

Track record of

reserve strength:

since IPO, $183

million favorable

prior AY reserve

development as of

12/31/09

reserve strength:

since IPO, $183

million favorable

prior AY reserve

development as of

12/31/09

Coverage up to

$200 M loss

$200 M loss

23

Key Strengths

• Strong underwriting franchise with established presence in attractive

markets

markets

– 97 year operating history - attractive, underserved target market segment with growth

opportunities

opportunities

• Unique, long-standing strategic distribution relationships

• Conservative risk profile and prudent capital management

• Strong financial position and strong balance sheet

– rated A- by A.M. Best

• Experienced management team with deep knowledge of workers’

compensation

compensation

– average 27 years experience with the ability to manage through challenging operating

conditions

conditions

24

Douglas D. Dirks

President & Chief Executive Officer

Employers Holdings, Inc.

William E. (Ric) Yocke

Chief Financial Officer

Employers Holdings, Inc.

President & Chief Executive Officer

Employers Holdings, Inc.

William E. (Ric) Yocke

Chief Financial Officer

Employers Holdings, Inc.

Analyst Contact:

Vicki Erickson

Vice President, Investor Relations

Employers Holdings, Inc.

(775) 327-2794

verickson@employers.com

Vicki Erickson

Vice President, Investor Relations

Employers Holdings, Inc.

(775) 327-2794

verickson@employers.com

10375 Professional Circle

Reno, NV 89521

(775) 327-2700

Reno, NV 89521

(775) 327-2700

25

Stock Ownership Limitations

As a reminder to investors, Employers Holdings, Inc. (“EIG”) owns several insurance companies, domiciled in several

different states. These wholly-owned insurers are regulated by insurance commissioners and are subject to the statutes and

regulations of the various states where they are domiciled and authorized to transact insurance. As a result, EIG has the

following stock ownership limitations, which must be satisfied prior to certain stock transactions.

different states. These wholly-owned insurers are regulated by insurance commissioners and are subject to the statutes and

regulations of the various states where they are domiciled and authorized to transact insurance. As a result, EIG has the

following stock ownership limitations, which must be satisfied prior to certain stock transactions.

●For a period of five years following the effective date of the Plan of Conversion of EIG, which is February 5, 2007, no

person may directly or indirectly acquire or offer to acquire in any manner beneficial ownership of 5% or more of any class of

EIG’s voting securities without the prior approval by the Nevada Commissioner of Insurance of an application for acquisition

under Section 693A.500 of the Nevada Revised Statutes.

person may directly or indirectly acquire or offer to acquire in any manner beneficial ownership of 5% or more of any class of

EIG’s voting securities without the prior approval by the Nevada Commissioner of Insurance of an application for acquisition

under Section 693A.500 of the Nevada Revised Statutes.

●Under Nevada insurance law, the Nevada Commissioner of Insurance may not approve an application for such acquisition

unless the Commissioner finds that (1) the acquisition will not frustrate the plan of conversion as approved by our members

and the Commissioner, (2) the board of directors of Employers Insurance Company of Nevada has approved the acquisition

or extraordinary circumstances not contemplated in the plan of conversion have arisen which would warrant approval of the

acquisition, and (3) the acquisition is consistent with the purpose of relevant Nevada insurance statutes to permit

conversions on terms and conditions that are fair and equitable to the members eligible to receive consideration.

unless the Commissioner finds that (1) the acquisition will not frustrate the plan of conversion as approved by our members

and the Commissioner, (2) the board of directors of Employers Insurance Company of Nevada has approved the acquisition

or extraordinary circumstances not contemplated in the plan of conversion have arisen which would warrant approval of the

acquisition, and (3) the acquisition is consistent with the purpose of relevant Nevada insurance statutes to permit

conversions on terms and conditions that are fair and equitable to the members eligible to receive consideration.

●Furthermore, any person or entity who individually or together with an affiliate (as defined by applicable law) seeks to

directly or indirectly acquire in any manner, at any time, beneficial ownership of 5% or more of any class of EIG’s voting

securities, will be subject to certain requirements, including the prior approval of the proposed acquisition by certain state

insurance regulators, depending upon the circumstances involved. Any such acquisition without prior satisfaction of

applicable regulatory requirements may be deemed void under state law.

directly or indirectly acquire in any manner, at any time, beneficial ownership of 5% or more of any class of EIG’s voting

securities, will be subject to certain requirements, including the prior approval of the proposed acquisition by certain state

insurance regulators, depending upon the circumstances involved. Any such acquisition without prior satisfaction of

applicable regulatory requirements may be deemed void under state law.

Appendix

26

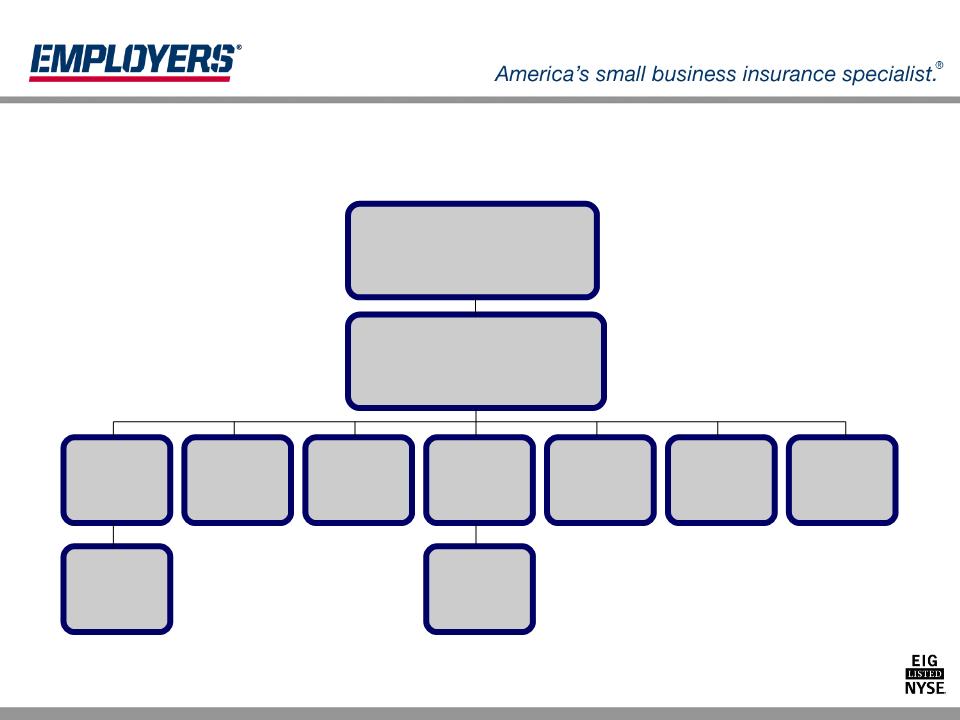

Organization

Employers Holdings, Inc.

Employers

Insurance

Company

Company

of Nevada

Employers

Compensation

Insurance

Company

Employers

Preferred

Insurance

Company

Company

Employers

Occupational

Health, Inc.

Employers

Assurance

Company

Elite

Insurance

Services

EIG Services,

Inc.

Inc.

Pinnacle

Benefits, Inc.

AmSERV,

Inc.

Employers Group, Inc.

27

|

Income Statement ($ million)

|

2005

|

2006

|

2007

|

2008

|

2009

|

|

Gross Written Premium

|

$ 451.4

|

$ 386.8

|

$ 351.8

|

$ 318.4

|

$ 379.9

|

|

Net Written Premium

|

432.5

|

372.2

|

339.7

|

308.3

|

368.3

|

|

Net Earned Premium

|

438.3

|

393.0

|

346.9

|

328.9

|

404.2

|

|

Net Investment Income

|

54.4

|

68.2

|

78.6

|

78.1

|

90.5

|

|

Net Income

|

137.6

|

171.6

|

120.3

|

101.8

|

83.0

|

|

Net Income Before LPT

|

93.8

|

152.2

|

102.2

|

83.4

|

65.0

|

|

Balance Sheet ($ million)

|

2005

|

2006

|

2007

|

2008

|

2009

|

|

Total Investments

|

$ 1,595.8

|

$ 1,715.7

|

$ 1,726.3

|

$ 2,042.9

|

$ 2,029.6

|

|

Cash and Cash Equivalents

|

61.1

|

80.0

|

149.7

|

202.9

|

191.6

|

|

Total Assets

|

3,188.8

|

3,266.8

|

3,264.3

|

3,825.1

|

3,676.7

|

|

Reserves for Loss and LAE

|

2,350.0

|

2,307.8

|

2,269.7

|

2,506.5

|

2,425.7

|

|

Shareholders’ Equity

|

144.6

|

303.8

|

379.5

|

444.7

|

498.4

|

|

Equity Including LPT Deferred Gain

|

607.0

|

746.8

|

804.5

|

851.3

|

887.0

|

Selected Operating Results

28

Regional, Pricing Trends 09/30/09 thru 04/01/10

ME

NY

NH

MA

CT

VT

NJ

RI

KY

OH

IN

MO

IA

MN

IL

MIDWEST

KS

NE

SD

ND

NM

TX

OK

MT

WY

CO

UT

ID

AZ

NV

WESTERN

WA

CA

OR

PACIFIC

Corporate Headquarters

Regional Headquarters

MD

PA

VA

WV

NC

TN

AL

AR

LA

GA

MS

DC

SC

FL

SOUTHEAST

States Licensed, actively writing

States Licensed, not actively writing

% Employers Insurance Co of NV (EICN)

% Employers Comp Ins Company (ECIC)

% Employers Assurance Co (EAC)

% Employers Preferred Insurance Co (EPIC)

+3.0%

-7.4%

-4.2%

-9.7%

-2.6%

-18.8%

-0.1%

-24.5%

+7.0%

-6.8%

-6.8%

-6.8%

-6.7%

-37.4%

+2.3%

-28.7%

+22.0%

-6.1%

-27.0%

-29.8%

+3.7%

-14.3%

+14.2%

-28.1%

-19.1%

-28.3%

+4.4%

-37.8%

-13.7%

-1.1%

-1.3%

-34.7%

+2.2%

-42.1%

-9.6%

-9.6%

+5.8%

-32.6%

-21.2%

-10.0%

-2.8%

+0.4%

+0.4%

-4.2%

-7.6%

-7.5%

+6.2%

-28.1%

-5.8%

-5.8%

+8.7%

-24.1%

-0.1%

-0.1%