Attached files

| file | filename |

|---|---|

| EX-32.1 - EXHIBIT 32.1 - BIOCANCELL THERAPEUTICS INC. | exhibit321.htm |

| EX-31.2 - EXHIBIT 31.2 - BIOCANCELL THERAPEUTICS INC. | exhibit312.htm |

| EX-31.1 - EXHIBIT 31.1 - BIOCANCELL THERAPEUTICS INC. | exhibit311.htm |

| EX-32.2 - EXHIBIT 32.2 - BIOCANCELL THERAPEUTICS INC. | exhibit322.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-K

(Mark One)

|

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

|

FOR THE FISCAL YEAR ENDED: DECEMBER 31, 2009

|

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from ___ to ____

Commission File Number: 333-156252

BIOCANCELL THERAPEUTICS INC.

(Exact name of Registrant as specified in its charter)

|

Delaware

|

20-4630076

|

|

(State or Other Jurisdiction of Incorporation or Organization)

|

(I.R.S. Employer Identification No.)

|

|

Beck Science Center, 8 Hartom St, Har Hotzvim, Jerusalem, Israel

|

97775

|

|

(Address of principal executive offices)

|

(Zip Code)

|

|

972-2- 548-6555

|

|

|

(Registrant’s telephone number)

|

|

|

Securities registered pursuant to Section 12(b) of the Act:

|

|

Common Stock, $.01 par value

|

Tel Aviv Stock Exchange

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act.

Yes o No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

Yes o No x

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer", "accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated Filer o Accelerated filer o Non-accelerated filer o

Smaller reporting company x

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes o No x

The aggregate market value of the registrant’s voting stock held by non-affiliates was approximately $5,950,353 as of June 30, 2009.

The number of shares of the registrant’s common stock, par value $.01, outstanding as of March 17, 2010 was 19,989,150.

BIOCANCELL THERAPEUTICS INC.

FORM 10-K

TABLE OF CONTENTS

|

PART I

|

Page

|

|

|

Item 1.

|

Business

|

1 |

|

Item 2.

|

Properties

|

7 |

|

Item 3.

|

Legal Proceedings

|

7 |

|

PART II

|

||

|

Item 5.

|

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

|

8 |

|

Item 7.

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

9

|

|

Item 8.

|

Report of Independent Registered Public Accounting Firm

|

16 |

|

Consolidated Balance Sheets as of December 31, 2009 and 2008

|

17 | |

|

|

||

|

Consolidated Statements of Operations for the year ended December 31 , 2009 and 2008

|

19 | |

|

|

||

| Consolidated Statements of Changes in Shareholders' Equity and Comprehensive Loss | 20 | |

|

Consolidated Statements of Cash Flows for the year ended December 31, 2009 and 2008

|

23 | |

|

|

||

|

Notes to Consolidated Financial Statements

|

26 | |

|

|

||

|

Item 9A(T).

|

Controls and Procedures

|

52

|

|

Item 9B.

|

Other Information

|

52 |

|

PART III

|

||

|

Item 10.

|

Directors, Executive Officers and Corporate Governance

|

53 |

|

Item 11.

|

Executive Compensation

|

60 |

|

Item 12.

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters.

|

65 |

|

Item 13.

|

Certain Relationships and Related Transactions, and Director Independence.

|

66

|

|

Item 14.

|

Principal Accountant Fees and Services.

|

67 |

|

PART IV

|

||

|

Item 15.

|

Exhibits

|

68

|

|

Signatures

|

69

|

|

INTRODUCTORY NOTE ON FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K for BioCancell Therapeutics Inc. (“BioCancell” or the “Company”) may contain forward-looking statements. You can identify these statements by forward-looking words such as “may,” “will,” “expect,” “intend,” “anticipate,” believe,” “estimate” and “continue” or similar words. Forward-looking statements include information concerning possible or assumed future business success or financial results. You should read statements that contain these words carefully because they discuss future expectations and plans, which contain projections of future results of operations or financial condition or state other forward-looking information. We believe that it is important to communicate future expectations to investors. The forward-looking statements included herein are based on current expectations that involve a number of risks and uncertainties, which are discussed in Item 1A, “Risk Factors” and in other sections of this Annual Report on Form 10-K and in our other filings with the Securities and Exchange Commission (SEC). These risks and uncertainties could cause actual results or events to differ materially from those expressed or implied by the forward-looking statements that we make.

Although, there may be events in the future that we are not able to accurately predict or control, we do not undertake any obligation to update any forward-looking statements for any reason, even if new information becomes available or other events occur in the future.Accordingly, to the extent that this Annual Report on Form 10-K contains forward-looking statements regarding the financial condition, operating results, business prospects or any other aspect of the Company, please be advised that BioCancell's actual financial condition, operating results and business performance may differ materially from that projected or estimated by the Company in forward-looking statements.

PART I

Item 1. Our Business

We are a clinical development-stage biopharmaceutical company focused on the discovery, development and commercialization of novel therapies for treating cancer-related diseases. We were formed on July 26, 2004, under the laws of the State of Delaware. Our research and development activities build upon the research of Professor Abraham Hochberg of the Hebrew University of Jerusalem, Israel who isolated the human H19 gene and determined that it is expressed in over forty different forms of cancer, including superficial bladder carcinoma and pancreatic, ovarian and metastatic liver cancer, while laying dormant and non-expressed in non-cancerous cells. Professor Hochberg’s research discovered that the H19 gene is significantly expressed in cancerous cells of adults. Research has also demonstrated that the H19 gene plays a significant role in the tumor development process by enabling tumor cells to survive under stress conditions, such as low serum and low oxygen levels, that are typical conditions of the environment in which cancerous cells develop. This survival supports the growth of the tumor and the development of metastases.

Recently-conducted research has led to significant scientific breakthroughs in the understanding of cancer, in particular with respect to the contribution of stem cells to the development of the disease. Stem cells possess the ability to regenerate themselves through mitotic cell division and differentiate into a diverse range of specialized cell types. Pluripotent stem cells have the potential to differentiate into any of the three germ layers: endoderm (interior stomach lining, gastrointestinal tract, the lungs), mesoderm (muscle, bone, blood, urogenital), or ectoderm (epidermal tissues and nervous system); thus, Pluripotent stem cells can give rise to any fetal or adult cell type. Pluripotent cells soon undergo further specialization into multipotent cells, which can give rise to several other limited cell types. A hematopoietic cell, for example, can develop into several types of blood cells, but cannot develop into muscle cells or other types of cells. Leading researchers have opined that adult multipotent stem cells are also the source of adult cancer stem cells, which are present in many, and are possibly in all, cancerous tumors. This theory is consistent with a number of other theories which are currently accepted by cancer researchers.

A significant problem with each of the current methods for treatment of cancer is the return of tumors. According to the new theory described above, even the most aggressive anti-cancer drugs, such as those used in chemotherapy, destroy the tumor cells, but in fact do not treat the source of the tumor — adult cancer stem cells. As a result, the theory postulates that anti-cancer drugs should treat adult cancer stem cells which are the source of returning tumors. In addition, according to the accepted theory among cancer researchers, the disease is created as a result of a long process of accumulation of genetic mutations. The fact that cells in most body tissues continuously undergo self-renewal, however, undermines the theory regarding the accumulation of genetic mutations. Only adult cancer stem cells, which are present in each tissue for many years, accumulate genetic mutations throughout the years, thus supporting the creation and return of tumors.

The research and understanding of the origin of cancer and metastases has progressed significantly in recent years. It is currently understood that embryogenesis, which is the process by which the embryo is formed and develops, and the process of the development of cancer, possess similar characteristics. The H19 gene is expressed and has a significant role in both processes. The process of formation of metastases is similar in its characteristics to epithelial mesenchymal transition, or EMT, which is a program of development of biological cells characterized by loss of cell adhesion, repression of E-cadherin expression, and increased cell mobility. EMT is essential for numerous developmental processes including mesoderm formation and neural tube formation. Similar to EMT, the process of formation of metastasis is also characterized by loss of cell adhesion, repression of E-cadherin expression, and increased cell mobility. Studies have demonstrated the involvement of the H19 gene in EMT.

In light of the recently achieved scientific breakthroughs in cancer research, and the role of the H19 gene in such processes, we believe that an anti-cancer drug based on the H19 gene has the potential to provide benefits that are competitive with existing treatment methods.

Our Prospective Drugs

We are currently focused on developing our prospective drug, BC-819. The detection of expression of the H19 gene is the prerequisite for the use of our potential therapy. Our development of BC-819 builds upon the research of Professor Hochberg who discovered that the H19 gene is a diagnostic marker for cancerous growths, through the identification of the expression of the H19 gene. Based upon these discoveries, we have developed BC-819, which is a double stranded DNA plasmid construct that incorporates the gene for diphtheria toxin (DTA) under the regulation of the H19 promoter sequence. The DTA gene is transcribed into a cell-killing DTA peptide only in cells that produce H19 RNA. The H19 regulatory gene, which is crucial to the growth of tumor cells, is utilized instead as the activator of the intra-cellular synthesis of DTA. The synthesis of this toxin peptide inhibits cellular protein synthesis, thereby causing the cancer cells to commit suicide. Once the BC-819 enters an H19-positive cancer cell, the cell can offer no resistance and is marked for death. The net result of this mechanism is highly selective tumor cell destruction. The strong safety profile of the plasmid is due, in part, to the fact that it produces the “A” portion only of diphtheria toxin inside cancerous cells. This toxin lacks the ability to penetrate other cells provided by the “B” portion, and consequently only acts to destroy the cell in which it is produced. Therefore, this new therapeutic modality is specific for the H19-positive cancer cell and thus far has not been detected with known toxic effects on normal cells — a safety feature that is unique when compared to currently available cancer treatments.

BC-819 has also demonstrated potential with respect to combination therapy. Even in cells that produce small amounts of H19 regulatory RNA, it appears that BC-819 acts to reverse the resistance of the cancer cells to chemotherapeutic agents. Moreover, as a result of our therapeutic approach, the plasmid being used to deliver the cytotoxic DTA gene does not incorporate into the genome of the host. We believe that this has significant advantages over gene therapy platforms for cancer that depend on a “genetic correction” strategy.

We are developing two BC-819-based strategies. The first therapy is for bladder cancer wherein BC-819is mixed with a transfection agent (to facilitate entry of BC-819 molecules into the cancer cells) for bladder instillation. The second BC-819 approach is for advanced stage cancers such as pancreatic, ovarian, and liver carcinomas in which plasmid DNA is injected directly into the tumor or instilled into the peritoneal cavity. Different routes of administration are employed depending upon the type of tumor (intravesical administration for bladder cancer, intratumoral injection for pancreatic and hepatocellular carcinoma, intraperitoneal administration for ovarian cancer with ascites, and hepatic artery infusion for liver metastases).

Pursuant to an agreement with Yissum Research Development Company of the Hebrew University of Jerusalem, which we refer to in this report as “Yissum”, Yissum has granted to us an exclusive, worldwide license for the use, development and commercialization of the H19 gene in consideration of which we have agreed to pay certain royalties to Yissum described elsewhere in this report.

Our primary strategic objective is to continue development of our prospective drug BC-819 for the treatment of superficial bladder carcinoma while broadening the scope of development to include additional applications.

We completed Phase I/IIa trials of one of our therapies — BC-819 — designed for use in patients suffering from bladder carcinoma. The Phase I/IIa trials resulted in no severe adverse side effects directly attributable to the tested therapy. In March 2008, we began the FDA-approved Phase IIb trial for this therapy. We filed IND applications for final FDA approval of the clinical trials during December 2008. On January 8, 2009, we were entitled to commence a Phase I/IIa clinical trial for treatment of pancreatic cancer, as the FDA has not contacted us regarding potential concerns or objections to our IND application within 30 days of its submission. On July 21, 2009 we received the approval of the Israeli Ministry of Health to commence the Phase I/IIa clinical trial for treatment of pancreatic cancer. We commenced such trial in Israel in August 2009. On January 12, 2009, we were entitled to commence Phase I/IIa clinical trials for treatment of ovarian cancer as the FDA has not contacted us regarding potential concerns or objections to our IND application within 30 days of its submission. We commenced the trial and began screening and treating patients in Israel in May 2009 and in the United States in June 2009. On August 20, 2009, the United States Department of Health and Human Services informed us that it has granted orphan drug status to BC-819 for its use in treating ovarian cancer. An "orphan drug" is a drug for a disease that affects a relatively small number of people in a population. In the USA, an orphan drug is defined as one that treats a disease affecting less than 200,000 people each year. In order to encourage the development of drugs for such diseases, benefits and incentives can be granted to the drug developers. The main standard benefit for orphan drugs in the USA is the right to market the drug exclusively for 7 years from the date it is approved. Additional benefits include tax benefits on R&D expenses, and waived FDA fees.

In addition to pursuing clinical trials of BC-819 for the treatment of superficial bladder carcinoma, pancreatic and ovarian cancer, we intend to continue, depending on available financial resources, our pre-clinical research related to the use of BC-819 for the treatment of various other forms of cancer as we seek to develop additional drugs based on various implementations of the technology developed by Professor Hochberg. The following is a summary of some of our other research and development activities that are in the preliminary stage of laboratory research:

|

•

|

BC-820. BC-820 is a potential therapeutic product that activates both the synthesis of DTA and the protein Tumor Necrosis Factor (TNF) of the cytokine family. Like BC-819, BC-820 penetrates cancerous cells expressing the H19 gene and activates the synthesis of DTA and TNF in a targeted manner.

|

|

•

|

BC-821. BC-821 is a potential therapeutic product that penetrates cancerous cells and activates the synthesis of DTA only in cells expressing the P4 promoter of the target gene IGF2, which like the H19 target gene is expressed only in cancerous cells and not in non-cancerous cells. It thus has the potential to serve as a complementary product to BC-819, allowing the targeted destruction of cancer cells in a larger number of patients.

|

|

•

|

BC-822. This potential therapeutic product seeks to suppress the growth of cancerous cells by re-sequencing a cancer cell’s RNA by way of inserting a small interfering Ribonucleic Acid (siRNA) sequence that prevents the expression of the H19 gene. Like BC-819, the potential therapy would first penetrate cells expressing the H19 gene and then covalently attach the new siRNA sequence.

|

In pursuing our objectives, we may enter into strategic collaborations with third parties who have the expertise and the resources necessary for the performance of large scale clinical trials, who have well established marketing, distribution and manufacturing infrastructures or who have experience and expertise in preparing registrations with the FDA and other regulatory authorities for the receipt of marketing approval.

Potentially Treatable Diseases

Superficial Bladder Carcinoma. We believe that BC-819 may be effective in treating superficial bladder carcinoma. Superficial bladder carcinoma is a specific form of bladder cancer resulting from the development and progression of cancerous tumors within the urothelium layer. The H19 gene is expressed at high levels in areas afflicted by superficial bladder carcinoma.

Pancreatic Cancer. Cancerous cells may develop in either the exocrine cells or the endocrine cells of the pancreas and the H19 gene is expressed at high levels in these cancerous regions.

Ovarian Cancer. Ovarian cancer is a disease in which normal ovarian cells begin to grow in an uncontrolled, abnormal manner and produce tumors in one or both ovaries. The H19 gene is expressed at high levels in areas afflicted by ovarian cancer.

1

Metastatic Liver Cancer. Metastasis is a secondary malignant tumor as it involves the spread of cancer from a primary site to other parts of the body. A metastasis in the liver may arise as a result of the spread of a cancer from another part of the body. The liver is a common site of metastatic disease. The portal vein drains the abdominal viscera and is presumably the conduit for metastases from tumors of the colon and rectum, stomach, pancreas and small intestine. The H19 gene is expressed at high levels in areas afflicted by metastatic liver cancer.

Our Process of Research and Development — Target Identification and Validation.

Target validation involves proving that DNA, RNA or a protein molecule is directly involved in a disease process and can be a suitable target for development of a new therapeutic drug. Drug target validation is among the most critical challenges facing pharmaceutical companies today. Our efforts have been conducted by a research team headed by Professor Hochberg at the Hebrew University of Jerusalem and include the following milestones:

|

•

|

Diagnostics — Use of H19 as a Diagnostic and Prognostic Tool. Professor Hochberg's research team has discovered that the H19 gene serves as a diagnostic marker for cancerous growths, through the identification of the expression of the H19 gene. A sensitive method called In-Situ Hybridization analysis (ISH) can detect even a single malignant cell expressing the H19 gene. ISH enables the detection of the expression of H19 in the examined tissue, while providing precise anatomic information regarding the location of the H19 presence in the tissue and cell. The detection of expression of the H19 gene is the biotechnological foundation of our potential therapy. The diagnostic marker enables the diagnosis of cancerous tumors in early stages. Such diagnosis supports the prognosis of the tumor.

|

|

•

|

Pre-Clinical Studies. Between the years 2000 – 2005, Professor Hochberg's research team conducted extensive animal studies in BC-819. Plasmid was introduced into the bladders of bladder-carcinoma carrying rats (orthotropic model) and mice (heterotopic model). Significant tumor growth inhibition was observed after treatment. Non-good laboratory practices (GLP) toxicology studies were performed in mice and in rats (syngeneic and nude models). Between the years 2006 – 2007, Harlen Biotech Israel Ltd. conducted toxicology studies in rats and mice, in accordance with Good Laboratory Practices Regulations. The studies included repeated injections at increasing dosages into the abdominal cavity of mice and intravesical administration into the urinary bladder of rats. The equivalent dosage given to the animals was higher than the expected human dosage. No gross pathological findings were evident in the intravesical administration study, and mild to moderate side effects were evident in the intraperitoneal administration study. In recent experiments which were conducted in the laboratories of the University of Munich, lung cancer carrying mice were treated with BC-819. More tumor growth inhibition was observed in mice which were treated with BC-819 than in mice which did not receive treatment. We are currently reviewing the results of the study and will consider further development of this application subject to our available resources.

|

|

•

|

Compassionate Use Patients. BC-819 has been administered, under “compassionate use” provisions in Israel, to ovarian and liver cancer patients who had failed chemotherapy and were in the ultimate stages of cancer, and bladder cancer patients who had failed chemotherapy and were in the ultimate stages of cancer, and urinary bladder and renal pelvis transitional cell carcinoma (TCC) patients who had failed chemotherapy and were candidates for radical cystectomy and nephrectomy, respectively. In 2003, two patients with resistant bladder cancer were treated with BC-819. Prior to the BC-819 treatment, the patients underwent a transurethral resection, but the tumors returned. Both patients were treated by direct introduction of BC-819 into the bladder using a catheter. The BC-819 treatment resulted in a significant decrease of the superficial bladder tumor, no unwanted toxicity was demonstrated in healthy cells, no severe adverse side effects which can be related to the drug were diagnosed, and no plasmid was detected in the patients' blood.

Two additional patients with very large metastases in their livers showed shrinkage of these tumors following treatment with BC-819 in 2004 and 2006. No unwanted toxicity was demonstrated in healthy cells and no severe adverse side effects which can be related to the drug were diagnosed.

A patient suffering from ovarian cancer characterized by intra-peritoneal distribution of metastases and ascites (liquid containing cancerous cells that builds up in the peritoneum as a result of the cancer) was treated with BC-819 between 2007 and 2008, after the failure of conventional chemotherapy treatment. In the framework of the treatments, the patient received a number of different doses of BC-819 administered by intra-peritoneal infusions via catheter. The results indicated that the drug caused no serious adverse events at any dosage, and a decrease of 50% in the ovarian cancer marker protein CA-125 in the patient’s blood was measured, as well as a significant decrease in the number of cancerous cells in the ascites.

A patient suffering from TCC in his renal pelvis, who had previously undergone nephrectomy of his right kidney for this disease, and was a candidate for nephrectomy of his left kidney, was treated with BC-819 between 2008 and 2009. The results showed that no new growths were formed in the renal pelvis, and the treatment did not cause any serious adverse effects.

|

The safety of BC-819 has been demonstrated through the following results of pre-clinical and clinical studies:

|

—

|

No unwanted toxicity was demonstrated in healthy cells and no severe adverse side effects which can be related to the drug were diagnosed, except for one case which was possibly related to BC-819 or to the catheterization procedure.

|

In addition, the potential safety is supported by the following considerations:

|

—

|

The use of the H19 gene as a marker ensures the selective destruction of cancerous cells without any impact on healthy cells, and the A portion of diphtheria toxin cannot attach to and enter cells in the absence of the B portion of diphtheria toxin, and consequently only acts to destroy the cell in which it is produced.

|

|

—

|

The transfection is consummated with the use of a nonviral transfection agent and takes place in cells undergoing cell division.

|

|

—

|

According to the World Health Organization, the majority of the western world's population is immunized to diphtheria toxin.

|

|

•

|

Phase I/IIa Clinical Trials. In 2006 – 2007, we conducted a Phase I/IIa, Dose-Escalation, Safety and Proof of Concept Study of BC-819 in Refractory Superficial Bladder Cancer. This study was designed to assess the safety and preliminary efficacy of BC-819 given by intravesical infusions into the bladder of 18 patients with superficial bladder cancer who had failed previous treatment. Escalating doses of 2 mg, 4 mg, 6 mg, 12mg and 20mg of BC-819 were utilized. No severe adverse side effects which can be related to the drug were diagnosed, other than in one case for which the reason was uncertain. This patient was hospitalized following complaint of urination urgency. The patient was released after two days and did not suffer additional adverse side effects during the treatment. We did not discover any dose limiting toxicity. As a result of the Phase I/IIa study, we concluded that the optimal dose to be used in Phase II trials would be 20mg.

At the beginning of the BC-819 treatment of patients in this study, all of the bladder tumors were removed, except for one (the diameter of which was 0.5 cm to 1 cm), which was left as a marker to gauge the influence of the treatment, despite the fact that the standard of care for bladder cancer patients involves removing all tumors. The parameters for examination of the initial efficacy include the reappearance of tumors, elimination or decrease in the size of the marker, and the aggravation of the disease. We examined efficacy in all patients participating in the trial, including patients who did not receive the optimal dose, although no control group was used in the trial as it is not the accepted practice to use a control group in a Phase I trial, whose primary purpose relates to the safety of the drug. Due to the small size of the trial and the absence of a control group, no p-values were calculated. Approximately 72% of the patients presented response to the treatment. The initial estimation of the drug's efficacy indicates that it has the ability to eliminate or decrease the size of tumors, and to prevent the reappearance of new tumors. Approximately 56% of the patients finished the study without new tumors. We detected reappearance of tumors mainly in patients who received doses which were substantially lower than the optimal dose. Intravesical administration of BC-819 resulted in complete ablation of the marker tumor without any new tumors in 4 of the 18 patients for a 22% overall complete response rate. The marker was eliminated, or reduced by at least 50%, in approximately 44% of the patients in the study. We detected only one patient with aggravation of the disease, meaning aggravation of the stage or the appearance of high grade tumors. Based on these positive results, we filed an investigational new drug (IND) application with the FDA for the performance of a Phase IIb clinical trial with patients suffering from superficial bladder cancer who had failed previous treatment. The application was approved on January 2008, and we immediately began recruiting patients. The purpose of this trial is to measure the efficacy and safety of BC-819 at a dose of 20mg, as tested in the previous Phase I/IIa clinical trial. The trial is being conducted in a U.S.-based medical center in Arizona by BCG Oncology, PC and at seven medical centers in Israel. This two-stage trial includes 33 patients, divided into groups of 18 and 15. Each participant will receive six weekly treatments of BC-819. Patients responding to the treatment will be offered nine additional maintenance treatments. Results of the trial are expected to be released when enough patients have been treated. The tough FDA inclusion criteria have made patient recruitment a more difficult and time-consuming issue than was initially expected. Notwithstanding the foregoing, as clinical studies are currently ongoing, we are expected to continue gathering safety and efficacy data on larger subject populations. Subsequent studies, and additional data which we expect to obtain from additional research and development activities may not corroborate previous findings with respect to safety and efficacy, which were obtained during the studies previously conducted. The FDA alone will determine whether our BC-819 product is both safe and effective for commercial use in the United States after substantial additional clinical studies.

|

|

•

|

Future Research Plan. On March 6, 2008, we filed with the FDA a pre-IND application regarding future potential Phase I/IIa clinical trials for testing BC-819 for the treatment of pancreatic, ovarian and liver cancer. The purpose of the trials, as presented to the FDA, is to examine the safety and preliminary efficacy of BC-819, in a series of increased doses and various indications. At the Pre-IND meeting in April 2008, the proposed clinical trial protocols were approved, the proposed pre-clinical protocol design (animal species and mode of administration) was accepted but further toxicology studies were requested (more pharmacokinetics and histopathology studies), which studies have been successfully completed recently. On January 8, 2009, we were entitled to commence a Phase I/IIa clinical trial for treatment of pancreatic cancer, as the FDA has not contacted us regarding potential concerns or objections to our IND application within 30 days of its submission. On July 21, 2009 we received the approval of the Israeli Ministry of Health to commence the Phase I/IIa clinical trial for treatment of pancreatic cancer. We commenced such trial in Israel in August 2009. We entered into a partnership with the Virginia Bioscience Commercialization Center to perform a Phase I/IIa clinical trial for the use of BC-819 as a treatment for pancreatic cancer. The clinical trial will be performed at the University of Maryland, Baltimore and will, subject to the execution of a collaboration agreement between the parties, be partly funded by a $950,000 grant from the Israel-US Binational Industrial Research and Development Fund. On January 12, 2009, we were entitled to commence Phase I/IIa clinical trials for treatment of ovarian cancer as the FDA has not contacted us regarding potential concerns or objections to our IND application within 30 days of its submission. We commenced the trial and began screening and treating patients in Israel in May 2009 and the United States in June 2009.

|

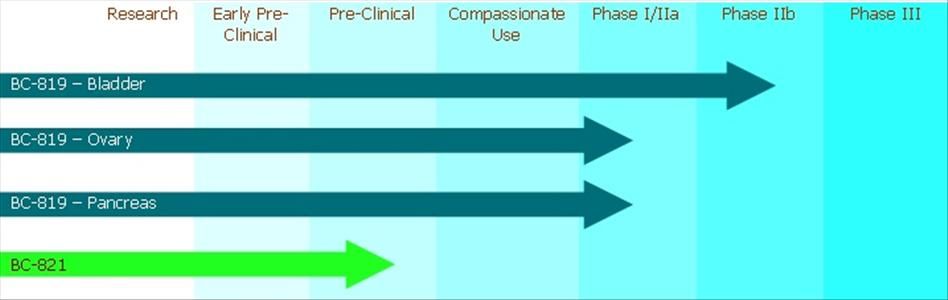

The following chart illustrates the stages to which each of our potential therapies has been developed, reflecting the relative development status of each of our potential therapies (but does not represent the relative amounts invested by us in each initiative):

2

Competition for Our Prospective Therapeutic Products

Our principal competitors in the field of researching and developing drugs for the treatment of cancer types including superficial bladder carcinoma, pancreatic cancer and ovarian cancer, include biotechnology and multinational pharmaceutical companies. We also compete with research and academic institutions around the world in the race to discover genes, techniques and other patentable assets central to the research and development of drugs for the treatment of such diseases. To the best of our knowledge, there are a number of treatment methods for treating these cancer types that would compete with any drug that we may develop and commercialize, including our prospective drug BC-819, which include:

|

•

|

Surgery. Surgery is the most common treatment method for invasive cancerous growths related to bladder cancer. Transurethral resection is the surgical method that is most often utilized for the removal of superficial bladder cancer tumors.

For patients with pancreatic cancer, surgery offers the only known possibility of cure, but even this is effective in only a small number of patients (10 – 20%). Even when resection is possible, the median survival times of 13 – 25 months and five-year survival rates of 10 – 20% have been reported. Prognosis is poor because of a high rate of local recurrence and metastases despite resection.

Initial surgery is almost always necessary in the management of suspected ovarian cancer. A total abdominal hysterectomy and bilateral salpingo-oophorectomyare typically performed.

|

|

|

•

|

Radiation Therapy. Radiation therapy involves the use of X-rays to destroy cancerous cells.

|

|

•

|

Chemotherapy. Chemotherapy uses special anti-cancer drugs that destroy cancerous cells. For bladder cancer patients, chemotherapy is administered directly into the bladder using a catheter for patients who are in the early stages of superficial bladder carcinoma. Chemotherapy is otherwise administered intravenously when superficial bladder carcinoma has become invasive.

To the best of our knowledge, some of the more commonly prescribed drugs used in intravesical chemotherapy are: Mitomycin-C, which has not been approved by the FDA for the treatment of bladder cancer and is marketed by the Bristol-Myers Squibb Company and Supergene; Epirubicin, which is marketed by Pfizer, Inc.; and Doxorubicin, which is marketed by Ortho Biotech, Thiotepa (marketed by Bedford Laboratories) and Valrubicin (supplied by SYNCHEM OHG), which are approved by the FDA for the treatment of superficial TCC. To the best of our knowledge, some of the more commonly prescribed drugs used in intravenous chemotherapy are Taxol, Carboplatin, Cisplatin and Gemcitabine.

The chemotherapy treatment plan in pancreatic cancer includes the downstaging of the tumor by shrinking the tumor volume to the extent that vascular involvement is lessened and resection is then rendered possible. Recently, many investigators have reported the utility of chemotherapy using gemcitabine, in which early studies showed that patients experienced an improvement in disease-related symptoms. However, the median survival time of 5.65 months and the 12-month survival rate of 18% for gemcitabine-treated patients is considered by most experts to be disappointing. The combination of gemcitabine and irradiation cause both acute and late toxicity of the gastrointestinal tract.

The majority of patients with epithelial ovarian cancer will require chemotherapy following the operation in an attempt to eradicate residual disease. Platinum-based adjuvant treatment, or immune system stimulator, can reduce the risk of relapse in patients with early-stage ovarian cancer, resulting in disease-free survival of approximately 80% of patients. Intravenous administration of taxane- and platinum- based chemotherapy is the current standard of postoperative care for patients with advanced ovarian cancer. Platinum analogues, such as carboplatin and cisplatin, are the most active agents in this disease. In contrast, taxanes such as paclitaxel and docetaxel exert their cytotoxic effects through a unique mechanism of action involving binding to and stabilization of the tubulin polymer. Despite the improved median overall survival in patients with regimens such as paclitaxel and carboplatin, relapse still occurs in the majority of those with advanced disease, and only 10 to 30% of such patients have long-term survival.

|

|

•

|

Immunotherapy. Immunotherapy is a method that employs a patient’s immune system to fight cancerous cells. Although the precise biological mechanism of activation is unknown, the administration of Bacille Calmette Guerin (BCG) is used to treat a number of superficial bladder cancer types because BCG is believed to stimulate a patient’s immune system to thwart the growth of cancerous cells.

|

|

|

•

|

Interferon. Interferons are human proteins that are introduced into the human body in order to stimulate the host’s immune system to thwart the growth of cancerous cells. Although the precise biological mechanism of activation is unknown, it is believed that interferons impede or suspend the growth of cancerous cells, compromise the ability of cancerous cells to defend against the host’s immune system and strengthen the host’s immune system. Interferons have been administered in combination with BCG. The University of Iowa has conducted Phase III clinical trials to examine the relative effectiveness of the interferon/BCG combined therapy as compared to each of the stand alone treatments.

|

In addition to the foregoing, we are aware of several new treatment methods for superficial bladder carcinoma have been approved for marketing including photodynamic treatment, which kills cancerous cells using laser, and synergo technology, which combines hypothermia with chemotherapeutical substances, but has not been approved by the FDA. We are also aware of several drugs for the treatment of bladder cancer in phase III development, including: (i) Urocidin, Mycobacterial Cell Wall-DNA Complex (MCC) developed by Bioniche Life Sciences Inc., and (iii) EOquin (Apaziquone), a bio-reductive pro-drug that form cytotoxic alkylating agent, developed by Spectrum Pharmaceuticals.

We are also aware of several drugs for the treatment of ovarian cancer in various stages of development, including: (i) Avastin, recombinant humanized monoclonal antibody that targets vascular endothelial growth factor (VEGF), developed by Genentech; (ii) Tarceva, small molecule human epidermal growth factor type 1 or epidermal growth factor receptor (HER1/EGFR) inhibitor, developed by Roche Holdings Ltd; and (iii) epothilone B, a cytotoxic, novel tubulin polymerizing compound known as an epothilone which inhibits cancer cells with a similar mechanism as paclitaxel, developed by Novartis.

We are likewise aware of several drugs for the treatment of liver cancer that are in stages of development, including: (i) Larotaxel, a cytotoxic agent that is active in cell lines resistant to chemotherapy, developed by Sanofi-Aventis; (ii) combination therapies such as, Avastin with Tarceva and Chemotherapy tested by Roche Holdings Ltd; and (iii) triacetyluridine, a prodrug of the nucleoside uridine which acts by inhibiting RNA and DNA synthesis, developed by Wellstat Therapeutics Corporation.

The results of our Phase I/IIa bladder carcinoma clinical study showed that the safety profile of BC-819 is excellent. The incidence and severity of adverse events in this small study population were lower than published results for BCG and chemotherapy. For instance in a typical Phase III study of BCG and epirubicin (de Reijke et al. 2005), adverse events included hematuria in 41% and 28% of patients treated with BCG or epirubicin, respectively, while only 11% of patients treated with BC-819 suffered hematuria. Severe dysuria was reported in 26% and 10% of patients treated with BCG and epirubicin, respectively, whereas there were no cases of severe dysuria reported for BC-819. No local reactions caused cessation of treatment with BC-819, whereas 26% and 9% of patients treated with BCG and epirubicin, respectively, had to have treatment stopped due to local toxicities. Using a plasmid with an expression cassette of the diphtheria toxin, no immune response will be encountered as happens when using an adenovirus; moreover, people born in Western countries are routinely immunized against this toxin. Further, our treatments are not affected by multi-drug resistance effects, a major problem in chemotherapy. Notwithstanding the foregoing, the FDA alone will determine whether our BC-819 product is both safe and effective for commercial use in the United States after substantial additional clinical studies.

Expenditures on Research and Development

From the time of our inception on July 26, 2004 through December 31, 2009, we invested approximately $11,269,000 in our research and development activities. We have funded our research and development expenses from our own resources and from various non-diluting grants, including grants from the Office of the Chief Scientist of the Israeli Ministry of Industry, Trade and Labor (OCS).

Our aggregate research and development budgetary expenditures for our first year of OCS funding (July 2005 to June 2006) were NIS 2,734,000 (approximately $850,000), of which NIS 1,225,000 (approximately $380,000) was funded by the OCS. Our aggregate research and development budgetary expenditures for the second year (August 2006 to July 2007) and third year (August 2007 to July 2008) were NIS 4,127,000 (approximately $1,280,000) and NIS 5,473,000 (approximately $1,700,000), respectively. In the second and third years, the OCS funded 60% of the approved research and development expenditures paid in Israel and 30% of the research and development costs paid to sub-contractors and consultants outside Israel. During July 2009, the OCS approved a fourth year of funding, in an aggregate amount of NIS 2,815,000 (approximately $718,000).

3

According to the Israeli Regulations for the Promotion of Research and Development in Industry 1996, we must pay the OCS royalties at a rate between 3% and 5% of revenue from sales of the product developed with the aid of the OCS, up to repayment of the full amount of the obligation, which is linked to the U.S. Dollar and bears annual interest at LIBOR rates. As of the date of this report, we have not began repayments, as we have not yet generated sales.

In December 2007, the Israel-U.S. Binational Industrial Research and Development Foundation (BIRD) approved a grant in the amount of $950,000 for our collaboration with the Virginia Bioscience Commercialization Center. The grant will partially fund our Phase I/IIa clinical trial for the use of BC-819 as a treatment for pancreatic cancer, which will be conducted at the University of Maryland, Baltimore.

Under the terms of the grant agreement between BIRD, the Virginia Bioscience Commercialization Center and us, we will have to repay the grant within twelve months of the successful completion of the project. We are entitled to extend the repayment period to 2 years in return for total repayment of 113% of the grant amount, to 3 years in return for total repayment of 125%, to 4 years in return for total repayment of 138%, or to 5 years or more in return for total repayment of 150% of the grant amount.

In March 2009, the OCS approved a grant for us to perform a Phase I/IIa clinical trial of BC-819 for ovarian cancer. The OCS will fund up to 60% of NIS 1,700,000 (approximately $447,000) in local expenses and up to 30% of NIS 1,800,000 (approximately $484,000) in foreign expenses. In July 2009, the OCS approved a grant for us to perform a Phase IIb clinical trial of BC-819 for bladder cancer. The OCS will fund up to 60% of NIS 1,900,000 (approximately $500,000) in local expenses and up to 30% of NIS 700,000 (approximately $179,000) in foreign expenses.

Intellectual Property

As of the date of this report, our patent portfolio includes 55 patent applications in seven families in various stages of examination, 25 of which have been granted in the United States, Europe, Israel, China, Australia, South Korea, Russia, Singapore, Mexico, Canada and the Czech Republic. All of our patents and patent applications were licensed to us from Yissum and are subject to the Yissum license agreement. The table below details which patent groups are related to which of our product candidates.

|

Patent Group

|

Product

|

Expiration Dates

|

|||

|

USE OF THE H19 GENE AS A TUMOR MARKER

|

BC-819

|

Between

03/07/2014

and

03/06/2015

|

|||

|

METHODS AND COMPOSITIONS FOR INDUCING TUMOR-SPECIFIC CYTOTOXICITY

|

BC-819

BC-821

|

Between

10/03/2017

and

10/04/2018

|

|||

|

NUCLEIC ACID AGENTS FOR DOWN REGULATING H19, AND METHODS OF USING SAME

|

BC-822

|

—

|

|||

|

NUCLEIC ACID CONSTRUCTS, PHARMACEUTICAL COMPOSITIONS AND METHODS OF USING SAME FOR TREATING CANCER

|

BC-820

|

—

|

|||

|

NUCLEIC ACID CONSTRUCTS AND METHODS FOR SPECIFIC SILENCING OF H19

|

BC-822

|

—

|

|||

|

H19 SILENCING NUCLEIC ACID AGENTS FOR TREATING RHEUMATOID ARTHRITIS (siRNA + RA)

|

BC-822

|

—

|

|||

|

CONSTARCTS CONTAINING MULTIPLE DIPHTHERIA TOXIN EXPRESSION CASSETTES

|

BC-821

|

—

|

|||

Pursuant to an exclusive license agreement with Yissum, which is described in more detail below, we have an exclusive, worldwide license for the development, use, manufacturing and commercialization of products arising out of patents owned by, and patent applications filed by, Yissum in connection with the H19 gene. All of our patents and patent applications were licensed to us from Yissum and are subject to the Yissum license agreement.

Suppliers of Raw Materials

For purposes of the translational research conducted by us, we use a variety of biological technologies and methods. The technology used in the process of detecting target proteins is siRNA technology, which is protected by many patents. We purchase siRNA molecules from suppliers that have licenses to sell these molecules strictly for research purposes in order to conduct our research operations. We may be required to enter into license agreements with one or more of the holders of patents relating to siRNA technology to the extent that we begin to use siRNA technology for the purpose of drug development. We also purchase chemical substances, synthesis and other services from various suppliers, as necessary. See “Our Business — Material Operating Agreements”.

Government Regulation

Our operations are subject to many governmental regulations. In the event that we complete Phase III clinical trials and are in a position to manufacture and market our prospective therapeutic products, the marketing of our prospective therapeutic products would be conditioned upon obtaining the consent of health authorities in each of the countries in which our prospective therapeutic products would be marketed, including the FDA and the European Agency for the Evaluation of Medicinal Products. In order to market our products outside of the United States, we must comply with numerous and varying regulatory requirements of other countries regarding safety and efficacy. Approval procedures vary among countries and can involve additional product testing and additional administrative review periods. The time required to obtain approval in countries outside of the United States might differ from that required to obtain FDA approval. The regulatory approval process in other countries may include all of the risks detailed below regarding FDA approval as well as other risks. Regulatory approval in one country does not ensure regulatory approval in another, but a failure or delay in obtaining regulatory approval in one country may have a negative effect on the regulatory process in others.

United States Food and Drug Administration. We must obtain the approval of the FDA to market any drugs that we may develop in the United States, as well as adhere to other U.S. and state regulations. If we seek to market new drugs, we will be required to file a new drug application and obtain FDA approval. FDA regulations govern the following activities that we may perform, or that we may have performed on our behalf, to ensure that any drugs that we may develop are safe and effective for their intended uses:

|

•

|

pre-clinical (animal) testing including toxicology studies;

|

|

|

•

|

submission of an investigational new drug application (IND);

|

|

|

•

|

human testing in clinical trials, Phases I, II and III;

|

|

|

•

|

recordkeeping and retention;

|

|

|

•

|

pre-marketing review through submission of a new drug application (NDA);

|

|

|

•

|

drug labeling and manufacturing, the latter of which must comply with current good manufacturing practice regulations;

|

|

|

•

|

drug marketing, sales and distribution; and

|

|

|

•

|

post-marketing study commitments (Phase IV), post-marketing surveillance, complaint handling, reporting of deaths or serious injuries and repair or recall of drugs.

|

Failure to comply with applicable regulatory requirements can result in enforcement action by the FDA, which may include any of the following sanctions:

|

•

|

warning letters, untitled letters, fines, injunctions, consent decrees and civil penalties;

|

|

|

•

|

disqualification of clinical investigator and/or sponsor from current and future studies;

|

|

|

•

|

clinical hold on clinical trials;

|

|

|

•

|

operating restrictions, partial suspension or total shutdown of production;

|

|

|

•

|

refusal to approve an NDA;

|

|

|

•

|

post-marketing withdrawal of approval; and

|

|

|

•

|

criminal prosecution.

|

The FDA’s Pre-clinical and IND Requirements. The first step to obtaining FDA approval of a new drug involves development, purification and pre-clinical testing of a pharmaceutically active agent in laboratory animals. Once sufficient pre-clinical data has been collected to demonstrate that the drug is reasonably safe for initial use in humans, an IND can be prepared and submitted to the FDA for review. In the IND review process, FDA physicians and scientists evaluate the proposed clinical trial protocol, chemistry and manufacturing control, pharmacologic mechanisms of action of the drug and toxicologic effects of the drug in animals and in vitro. Within 30 days of the IND’s submission, the drug review division of the FDA may contact us regarding potential concerns and, if necessary, implement a clinical hold until certain issues are resolved satisfactorily. If it does not take any action, we may proceed with clinical trials on the 31st day.

Clinical Trials. Clinical trials represent the ultimate pre-market testing ground for unapproved drugs, generally taking several years to complete. Before testing can begin, an institutional review board (IRB) must have reviewed and approved the use of human subjects in the clinical trial. During clinical trials, an investigational compound is administered to humans and evaluated for its safety and effectiveness in treating, preventing or diagnosing a specific disease or condition. The clinical trials consist of Phase I, Phase II, and Phase III testing. During clinical trials, the FDA and IRB closely monitor the studies and may suspend or terminate trials at any time for a number of reasons, such as finding that patients are being exposed to an unacceptable health risk. The results of clinical trials comprise the single most important factor in the approval or disapproval of a new drug.

4

NDA Review. An NDA, requesting approval to market the drug for one or more indications, may be submitted to the FDA once sufficient data has been gathered through pre-clinical and clinical testing. An NDA includes all animal and human testing data and analyses of the data, as well as information about how the drug behaves in the human body and how it is manufactured. The NDA is reviewed by a team of FDA physicians, chemists, statisticians, microbiologists, pharmacologists and other experts, who evaluate whether the studies submitted show that the drug is safe and effective for its proposed use. The FDA reviewers may request further information from us, consult with outside experts or disagree with our findings or interpretation of the data. Each reviewer prepares a written evaluation, and the reviewing team discusses the evaluations. Accelerated approval may be given to some new drugs for serious and life-threatening illnesses that lack satisfactory treatments. At the end of its review, the FDA may approve the new drug to be marketed or decide that a new drug is “approvable” or “not approvable.” In either of the latter cases, we may meet with FDA officials to discuss and correct deficiencies.

Pervasive and Continuing Regulation in the United States. After a drug is approved for marketing and enters the marketplace, numerous regulatory requirements continue to apply. These include, but are not limited to:

|

•

|

The FDA’s current good manufacturing practice regulations require manufacturers, including third party manufacturers, to follow stringent requirements for the methods, facilities and controls used in manufacturing, processing and packing of a drug product;

|

||

|

•

|

Labeling regulations and the FDA prohibitions against the promotion of drug for uncleared or unapproved uses (known as off-label uses), as well as requirements to provide adequate information on both risks and benefits during promotion of the drug;

|

||

|

•

|

Clearance or approval of product modifications or use of the drug for an indication other than approved in the NDA;

|

||

|

•

|

Adverse drug experience regulations, which require us to report information on rare, latent or long-term drug effects not identified during pre-market testing;

|

||

|

•

|

Post-market testing and surveillance requirements, including Phase IV trials, when necessary to protect the public health or to provide additional safety and effectiveness data for the drug; and

|

||

|

•

|

The FDA’s recall authority, whereby it can ask, or under certain conditions order, drug manufacturers to recall from the market a product that is in violation of governing laws and regulations.

|

After a drug receives approval, any modification in conditions of use, active ingredient(s), route of administration, dosage form, strength or bioavailability, will require a new clearance or approval. We may be able to submit a 505(b)(2) NDA referring to pre-clinical and certain clinical studies presented in the drug’s original NDA, accompanied by additional clinical data necessary to demonstrate the safety and effectiveness of the product with the proposed changes. Additional clinical studies may be required for proposed changes.

Fraud and Abuse Laws in the United States. A variety of U.S. federal and state laws apply to the sale, marketing and promotion of drugs that are paid for, directly or indirectly, by U.S. federal or state healthcare programs such as Medicare and Medicaid. The restrictions imposed by these laws are in addition to those imposed by the FDA, the United States Federal Trade Commission and corresponding state agencies. Some of these laws significantly restrict or prohibit certain types of sales, marketing and promotional activities by drug manufacturers. Violation of these laws may result in significant criminal, civil and administrative penalties, including imprisonment of individuals, fines and penalties and exclusion or debarment from U.S. federal and state healthcare and other programs. Many private health insurance companies also prohibit payment to entities that have been sanctioned, excluded or debarred by U.S. federal agencies.

Anti-Kickback Statutes in the United States. The U.S. federal anti-kickback statute prohibits persons from knowingly and willfully soliciting, offering, receiving or providing remuneration, directly or indirectly, in exchange for or to induce either the referral of an individual, or the furnishing, arranging for or recommending of a good or service, for which payment may be made in whole or in part under a U.S. federal healthcare program such as the Medicare and Medicaid programs. The definition of “remuneration” has been broadly interpreted to include anything of value, including gifts, discounts, the furnishing of supplies or equipment, payments of cash and waivers of payments. Several courts have interpreted the statute’s intent requirement to mean that, if any one purpose of an arrangement involving remuneration is to induce referrals or otherwise generate business involving goods or services reimbursed in whole or in part under U.S. federal healthcare programs, the statute has been violated. Penalties for violations include criminal penalties and civil sanctions such as fines, imprisonment and possible exclusion from Medicare, Medicaid and other U.S. federal healthcare programs. In addition, some kickback allegations have been claimed to violate the United States False Claims Act (as discussed below).

The U.S. federal anti-kickback statute is broad and prohibits many arrangements and practices that are lawful in businesses outside of the healthcare industry. Recognizing that the statute is broad and may technically prohibit many innocuous or beneficial arrangements, the Office of Inspector General of the Department of Health and Human Services, or OIG, has issued a series of regulations, known as the “safe harbors.” These safe harbors set forth provisions that, if all their applicable requirements are met, will assure healthcare providers and other parties that they will not be prosecuted under the anti-kickback statute. The failure of a transaction or arrangement to fit precisely within one or more safe harbors does not necessarily mean that it is illegal or that prosecution will be pursued. However, conduct and business arrangements that do not fully satisfy an applicable safe harbor may result in increased scrutiny by government enforcement authorities such as the OIG or the U.S. Department of Justice.

Many states have adopted laws similar to the U.S. federal anti-kickback statute. Some of these state prohibitions are broader than the U.S. federal statute, and apply to the referral of patients and recommendations for healthcare items or services reimbursed by any source, not only the Medicare and Medicaid programs. Government officials have focused certain enforcement efforts on marketing of healthcare items and services, among other activities, and have brought cases against individuals or entities with sales personnel who allegedly offered unlawful inducements to potential or existing physician customers in an attempt to procure their business.

United States False Claims Act. The United States False Claims Act prohibits any person from knowingly presenting, or causing to be presented, a false claim for payment to the U.S. federal government or knowingly making, or causing to be made, a false statement in order to have a false claim paid. The U.S. federal government’s interpretation of the scope of the law has in recent years grown increasingly broad. Most states also have statutes or regulations similar to the United States False Claims Act, which apply to items and services reimbursed under Medicaid and other state programs, or, in several states, apply regardless of the payor. Sanctions under these U.S. federal and state laws may include civil monetary penalties, exclusion of a manufacturer’s products from reimbursement under government programs, criminal fines and imprisonment. Several drug manufacturers have been prosecuted under the false claims laws for allegedly providing free drugs to physician customers with the expectation that the physician customers would bill U.S. federal programs for the product. In addition, several recent cases against drug manufacturers have alleged that the manufacturers improperly promoted their products for “off-label” use, outside of the scope of the FDA-approved labeling.

United States Health Insurance Portability and Accountability Act of 1996. The United States Health Insurance Portability and Accountability Act of 1996, or HIPAA, created a new U.S. federal healthcare fraud statute that prohibits knowingly and willfully executing a scheme to defraud any healthcare benefit program, including private payors. A violation of this statute is a felony and may result in fines, imprisonment or exclusion from government-sponsored programs. Among other things, HIPAA also imposes new criminal penalties for knowingly and willfully falsifying, concealing or covering up a material fact or making any materially false, fictitious or fraudulent statement in connection with the delivery of or payment for healthcare benefits, items or services, along with theft or embezzlement in connection with a healthcare benefits program and willful obstruction of a criminal investigation involving a U.S. federal healthcare offense.

Regulations in Europe. In Europe, we must obtain authorization from the European Agency for the Evaluation of Medicinal Products, commonly known as the European Medicines Evaluation Agency (EMEA) before marketing medicinal products. Authorization can be obtained through either the (i) “centralized” procedure, with applications made directly to the EMEA leading to the grant of a European marketing authorization by the European Commission, or (ii) “mutual recognition” procedure, in which applications are made to one or more Member States leading to national marketing authorizations mutually recognized by other Member States. If and when we receive marketing authorization, EU law regulates our distribution, classification for supply, labeling and packaging, and advertising of medicinal products for human use. The EU also regulates the manufacture of medicinal products, requiring us to meet the Good Manufacturing Practice requirements set forth in the Quality System regulation (cGMP). EU pharmacovigilance directives and regulations require us to establish post-market surveillance systems that include individual adverse reaction case reports, periodic safety update reports, and company-sponsored post-authorization safety studies. If a medicinal product’s overall risk and benefit profile is found to have changed significantly for any reason, we may be required to vary, withdraw or suspend the use of any such EMEA-approved drug.

Regulations in Israel. Our operations in Israel also are subject to approval by Israel’s Ministry of Health and the Helsinki Committee. All phases of clinical studies conducted in Israel must be conducted in accordance with the Public Health Regulations (Medical Experiments Involving Human Subjects, 1980, including amendments and addenda thereto) and the International Conference for Harmonization Good Clinical Practice Guidelines. The regulations stipulate that a medical trial on humans will only be approved after the Helsinki Committee at the hospital intending to perform the trial has approved the medical trial and notified the medical director at the hospital in writing. The Helsinki Committee will not approve the performance of the medical trial unless it is fully satisfied that it has advantages to the trial participants and society at large that justify the risk and inconvenience for the participants and that the medical and scientific information justifies the performance of the requested medical trial. The medical director also must be satisfied that the trial is not contrary to the Helsinki Declaration or to other regulations. The Ministry of Health also licenses and inspects pharmaceutical manufacturers, requiring manufacturers to meet internationally recognized cGMP standards.

Under the Israeli Law for the Encouragement of Industrial Research and Development, 1984 and related regulations, which we refer to as the “Research Law”, recipients of grants from the OCS are prohibited from manufacturing products developed using these grants outside of the State of Israel without special approvals, although the Research Law does enable companies to seek prior approval for conducting certain manufacturing activities outside of Israel without being subject to increased royalties. If we receive approval to manufacture the products developed with government grants outside of Israel, we will be required to pay an increased total amount of royalties to OCS, up to 300% of the grant amounts plus interest, depending on the manufacturing volume that is performed outside of Israel, as well as at a possibly increased royalty rate.

Additionally, under the Research Law, we are prohibited from transferring OCS-financed technologies and related intellectual property rights outside of the State of Israel except under limited circumstances, and only with the approval of the Research Committee of the OCS.

We may not receive the required approvals for any proposed transfer and, if received, we may be required to pay the OCS a portion of the consideration that we receive upon any sale of such technology to a non-Israeli entity. The scope of the support received, the royalties that we have already paid to the OCS, the amount of time that has elapsed between the date on which the know-how was transferred and the date on which the OCS grants were received and the sale price and the form of transaction will be taken into account in order to calculate the amount of the payment to the OCS. Approval of the transfer of technology to non-residents of the State of Israel is required, and may be granted in specific circumstances only if the recipient abides by the provisions of applicable laws, including the restrictions on the transfer of know-how and the obligation to pay royalties. No assurances can be made that approval to any such transfer, if requested, will be granted.

5

In March 2005, an amendment to the Research Law was enacted. One of the main modifications included in the amendment was an authorization of the Research Committee to allow the transfer outside of Israel of know-how derived from an approved program and the related manufacturing rights. In general, the Research Committee may approve transfer of know-how in limited circumstances as follows:

|

•

|

in the event of a sale of the know-how itself to a non affiliated third party, provided that upon such sale the owner of the know-how pays to the OCS an amount, in cash, as set forth in the Research Law. In addition, the amendment provides that if the purchaser of the know-how gives the selling Israeli company the right to exploit the know-how by way of an exclusive, irrevocable and unlimited license, the research committee may approve such transfer in special cases without requiring a cash payment.

|

|

•

|

in the event of a sale of the company which is the owner of know-how, pursuant to which the company ceases to be an Israeli company, provided that upon such sale, the owner of the know-how makes a cash payment to the OCS as set forth in the Research Law.

|

|

•

|

in the event of an exchange of know-how such that in exchange for the transfer of know-how outside of Israel, the recipient of the know-how transfers other know-how to the company in Israel in a manner in which the OCS is convinced that the Israeli economy realizes a greater, overall benefit from the exchange of know-how.

|

Another provision in the amendment concerns the transfer of manufacturing rights. The Research Committee of the OCS may, in special cases, approve the transfer of manufacture or of manufacturing rights of a product developed within the framework of the approved program or which results therefrom, outside of Israel.

The State of Israel does not own intellectual property rights in technology developed with OCS funding and there is no restriction on the export of products manufactured using technology developed with OCS funding. The technology is, however, subject to transfer of technology and manufacturing rights restrictions as described above. OCS approval is not required for the export of any products resulting from the research or development or for the licensing of any technology in the ordinary course of business.

Material Operating Agreements

Exclusive License Agreement with Yissum. On November 14, 2005, we entered into a license agreement with Yissum, which was subsequently amended on November 22, 2005 and September 11, 2007, pursuant to which Yissum has granted to us an exclusive, worldwide license for the development, use, manufacturing and commercialization of products arising out of patents owned by, and patent applications filed by, Yissum in connection with the H19 gene.

Under the terms of the Yissum license, Yissum retains right, title and interest in the products, technologies or other inventions arising out of our research and development of these patents and patent applications, except for intellectual property developed with funding from the OCS, which will be owned by us and transferred to Yissum only upon our dissolution or upon decision by the OCS that it no longer requires us to own the intellectual property developed with its funding. We have the right to grant sub-licenses to third parties in accordance with the terms set forth in the Yissum license.

We have agreed to provide research and development funding to Yissum in connection with the license, which we may terminate upon 90 days prior written notice to Yissum. In such event, we are required to compensate Yissum for all expenses incurred by it prior to the notification date in connection with its research efforts and all additional expenses that Yissum had assumed the obligation to cover prior to the notification date. The research and development funding was initially set for a period of two years with the possibility to extend the term by mutual agreement. We have been extending the funding period on a yearly basis, and it is currently valid until June 2010.

In addition, we have agreed to prepare, register and maintain any patent application or patent that may arise out of our research and development efforts pursuant to our license with Yissum and to bear all expenses of preparation, registration and maintenance. We agreed to keep Yissum informed of filing and prosecutions pursuant to the agreement, including submission of copies of all official actions, relevant correspondence, applications, continuations or like proceedings, and responses thereto. We agreed to consult Yissum regarding any abandonment of the prosecution of patent applications arising out of the license. In the event that we decide not to commence or continue the process of patent registration in a certain country, we must notify Yissum of this decision. Yissum may then individually prepare, register and maintain any such patent. We must inform Yissum of our desire to assume the expenses incurred by Yissum in connection with its patent registration within 90 days from the date in which Yissum notifies us of its decision to prepare, register and maintain such patent. In the event that we decide not to assume these expenses, or in the absence of our reply within the above 90 day period, the exclusive, worldwide license granted to us by Yissum will no longer be applicable in such countries in which we elected not to file or to abandon the filing, prosecution or maintenance of patents pursuant to the license. We undertook to use commercially reasonable efforts at our own expense to protect against third party's infringement of the patents arising out of the license and to advise Yissum upon learning of such infringement. We also undertook to use commercially reasonable efforts at our own expense to defend any action, claim or demand made by any entity in connection with rights in the patents, and to notify Yissum immediately upon learning of any such action or claim.

We have agreed to pay Yissum 5% of all of our “net sales” as royalties and to pay Yissum 10% of the income that we receive from granting sub-licenses to third parties up to revenues of $30,000,000 each year, and 6.5% of all additional income that we receive from granting sub-licenses to third parties.

We are required to indemnify Yissum, the Hebrew University of Jerusalem, their employees, their executive officers, delegates and any other persons acting on their behalf under the license against any liability, including product liability, damages, losses, expenses, fees and reasonable legal expenses arising out of our actions or omissions in performing the Yissum license, including the use, development and manufacturing of patents arising out of it and the granting of sub-licenses thereunder, provided that any such loss was not caused by the intentional misconduct or gross negligence of the indemnitees.

We have agreed to maintain, and to add Yissum as an additional insured party with respect to, product liability insurance as well as an insurance policy with respect to the foregoing indemnification prior to the time when we commence clinical trials and close our first commercial sale. We also have agreed to obtain liability insurance with respect to clinical trials prior to the time when we commence clinical trials.