Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2009

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 1-13677

MID PENN BANCORP, INC.

(Exact Name of Registrant as Specified in its Charter)

| Pennsylvania | 25-1666413 | |

| (State or Other Jurisdiction of Incorporation or Organization) |

(I.R.S. Employer Identification Number) |

| 349 Union Street Millersburg, Pennsylvania |

17061 | |

| (Address of Principal Executive Offices) | (Zip Code) |

Registrant’s telephone number, including area code 717.692.2133

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class |

Name of Each Exchange on Which Registered | |

| Common Stock, $1.00 | The NASDAQ Stock Market, Inc. |

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of “large accelerated filer”, “accelerated filer”, and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check One).

| Large accelerated filer | ¨ | Accelerated Filer | x | |||

| Non-accelerated Filer | ¨ | Smaller Reporting Company | ¨ | |||

Indicated by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the registrant’s voting and non-voting common equity held by non-affiliates computed by reference to the closing price of the common equity of $15.80 per share, as reported by NASDAQ, on June 30, 2009, the last business day of the registrant’s most recently completed second fiscal quarter was approximately $54,980,524.

As of February 1, 2010, the registrant had 3,479,780 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement to be used in connection with the 2010 Annual Meeting of Shareholders is incorporated herein by reference in partial response to Part III, hereof.

Table of Contents

MID PENN BANCORP, INC.

FORM 10-K

2

Table of Contents

MID PENN BANCORP, INC.

PART I

The disclosures set forth in this Item are qualified by the section captioned “Special Cautionary Notice Regarding Forward-Looking Statements” contained in Part II, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations of this report and other cautionary statements set forth elsewhere in this report.

Mid Penn Bancorp, Inc., Inc.

Mid Penn Bancorp, Inc., Inc. is a one-bank holding company, incorporated in the Commonwealth of Pennsylvania in August 1991. Mid Penn Bancorp, Inc., Inc. and its wholly owned subsidiaries are collectively referred to herein as “Mid Penn” or the “Corporation.” On December 31, 1991, Mid Penn acquired, as part of the holding company formation, all of the outstanding common stock of Mid Penn Bank, and the Bank became a wholly owned subsidiary of Mid Penn. Mid Penn’s other wholly owned subsidiaries are Mid Penn Insurance Services, LLC, which provides a range of personal and investment insurance products and Mid Penn Investment Corporation, which is engaged in investing activities. Mid Penn’s primary business is to supervise and coordinate the business of its subsidiaries and to provide them with capital and resources.

Mid Penn’s consolidated financial condition and results of operations consist almost entirely of that of Mid Penn Bank, which is managed as a single business segment. At December 31, 2009, Mid Penn had total consolidated assets of $606,010,000, total deposits of $500,015,000, and total shareholders’ equity of $46,704,000.

As of December 31, 2009, Mid Penn Bancorp, Inc., Inc. did not own or lease any properties. Mid Penn Bank owns the banking offices as identified in Item 2.

All Mid Penn employees are employed by Mid Penn Bank. At December 31, 2009, the Bank had 155 full-time and 33 part-time employees. The Bank and its employees are not subject to a collective bargaining agreement, and the Bank believes it enjoys good relations with its personnel.

Mid Penn Bank

Millersburg Bank, the predecessor to Mid Penn Bank (the “Bank”), was organized in 1868, and became a state chartered bank in 1931, obtaining trust powers in 1935, at which time its name was changed to Millersburg Trust Company. In 1962, the Lykens Valley Bank merged with and into Millersburg Trust Company. In 1971, Farmer’s State Bank of Dalmatia merged with Millersburg Trust Company and the resulting entity adopted the name “Mid Penn Bank.” In 1985, the Bank acquired Tower City National Bank. In 1998, Mid Penn acquired Miners Bank of Lykens, which was merged into Mid Penn Bank. The Pennsylvania Department of Banking and the Federal Deposit Insurance Corporation supervise the Bank. Mid Penn’s and the Bank’s legal headquarters are located at 349 Union Street, Millersburg, Pennsylvania 17061. The Bank presently has 14 offices located in Dauphin, Northumberland, Schuylkill, and Cumberland Counties, Pennsylvania.

Mid Penn’s primary business consists of attracting deposits from its network of community banking offices operated by the Bank. The Bank engages in full-service commercial banking and trust business, making available to the community a wide range of financial services, including, but not limited to, installment loans, personal loans, mortgage and home equity loans, secured and unsecured commercial and consumer loans, lines of credit, construction financing, farm loans, community development and local government loans and various types of time and demand deposits. Deposits of the Bank are insured by the Bank Insurance Fund of the FDIC to the maximum extent provided by law. In addition, the Bank provides a full range of trust services through its Trust Department. The Bank also offers other services such as Internet banking, telephone banking, cash management services, automated teller services and safe deposit boxes.

Business Strategy

The Bank provides an array of sophisticated products typically found only in major regional banks. These services are provided to small and middle market businesses, high net worth individuals, and retail consumers through 14 full service banking facilities. Several banking locations have seasoned management with significant lending experience who are responsible for credit and pricing decisions, subject to loan committee approval for larger credits. This decentralized relationship management approach, coupled with the continuity of service by its banking officers, enables the Bank to develop long-term customer relationships, maintain high quality service and provide quick responses to customer needs. Mid Penn believes that its emphasis on local relationship building, together with its conservative approach to lending, are important factors in the success and the growth of Mid Penn.

The Bank seeks credit opportunities of good quality within its target market that exhibit positive historical trends, stable cash flows and secondary sources of repayment from tangible collateral. The Bank extends credit for the purpose of obtaining and continuing long-term relationships. Lenders are provided with detailed underwriting policies for all types of credit risks accepted by the Bank and must obtain appropriate approvals for credit extensions in excess of conservatively assigned lending limits. The Bank also maintains strict documentation requirements and extensive credit quality assurance practices in order to identify credit portfolio weaknesses as early as possible so any exposures that are discovered might be reduced.

1

Table of Contents

MID PENN BANCORP, INC.

Lending Activities

The Bank offers a variety of loan products to its customers, including loans secured by real estate, commercial and consumer loans. The Bank’s lending objectives are as follows:

| • | to establish a diversified commercial loan portfolio; and |

| • | to provide a satisfactory return to Mid Penn’s shareholders by properly pricing loans to include the cost of funds, administrative costs, bad debts, local economic conditions, competition, customer relationships, the term of the loan, credit risk, collateral quality and a reasonable profit margin. |

Credit risk is managed through portfolio diversification, underwriting policies and procedures and loan monitoring practices. The Bank generally secures its loans with real estate with such collateral values dependent and subject to change based on real estate market conditions within its market area. As of December 31, 2009, the Bank’s highest concentrations of credit were in Commercial Real Estate, Hotel/Motel, Commercial Construction and Land Development, and Restaurant financings. Most of the Bank’s business activity with customers was located in Central Pennsylvania, specifically in Dauphin, lower Northumberland, western Schuylkill, and eastern Cumberland Counties.

Investment Activities

Mid Penn’s investment portfolio is used to improve earnings through investments of funds in higher-yielding assets, while maintaining asset quality, which provides the necessary balance sheet liquidity for Mid Penn. Mid Penn does not have any significant concentrations within investment securities.

Mid Penn’s entire portfolio of investment securities is considered available for sale. As such, the investments are recorded on the balance sheet at fair value. Mid Penn’s investments include US Treasury, agency and municipal securities that are given a market price relative to investments of the same type with similar maturity dates. As the interest rate environment changes, Mid Penn’s fair value of existing securities will change. This difference in value, or unrealized gain, amounted to $1,238,000, as of December 31, 2009. A majority of the investments are high quality United States and municipal securities that, if held to maturity, are expected to result in no loss to the Bank.

For additional information with respect to Mid Penn’s business activities, see Part II, Item 7 of this report, which is incorporated herein by reference.

Sources of Funds

The Bank primarily uses deposits and borrowings to finance lending and investment activities. Borrowing sources include advances from the Federal Home Loan Bank of Pittsburgh, reverse repurchase agreements with investment banks and overnight borrowings from the Bank’s customers and correspondent bank. All borrowings, except for the line of credit with the Bank’s correspondent bank, require collateral in the form of loans or securities. Collateral levels therefore, limit borrowings and the available lines of credit extended by the Bank’s creditors. As a result, deposits remain key to the future funding and growth of the business. Deposit growth within the banking industry has been subject to strong competition from a variety of financial services companies. This competition may require financial institutions to adjust their product offerings and pricing to adequately grow deposits.

Competition

The banking business is highly competitive, and the profitability of Mid Penn depends principally upon the Bank’s ability to compete in its market area. The Bank actively competes with other financial services companies for deposit and loan business. Competitors include other commercial banks, savings banks, savings and loan associations, insurance companies, securities brokerage firms, credit unions, finance companies, mutual funds, and money market funds. Financial institutions compete primarily on the quality of services rendered, interest rates on loans and deposits, service charges, the convenience of banking facilities, location and hours of operation and, in the case of loans to larger commercial borrowers, relative lending limits.

Many competitors are significantly larger than the Bank and have significantly greater financial resources, personnel and locations from which to conduct business. In addition, the Bank is subject to banking regulations while certain competitors may not be. There are relatively few barriers for companies wanting to enter into the financial services industry. For more information, see the “Supervision and Regulation” section below.

2

Table of Contents

MID PENN BANCORP, INC.

Mid Penn has been able to compete effectively with other financial institutions by emphasizing technology and customer service, including local decision making on loans, establishing long-term customer relationships and building customer loyalty, and providing products and services designed to address the specific needs of its customers. The Gramm-Leach-Bliley Act (see discussion below), which breaks down many barriers between the banking, securities and insurance industries, may significantly affect the competitive environment in which Mid Penn operates.

The growth of mutual funds over the past decade has made it increasingly difficult for financial institutions to attract deposits. The continued flow of cash into mutual funds, much of which is made through tax deferred investment vehicles such as 401(k) plans, and a generally strong economy, have, until recently, fueled high returns for these investments, in particular, certain equity funds. The recent economic turmoil has negatively impacted the returns on many of these investments and impacted the manner in which investors distribute their funds across investment alternatives. The safety of traditional bank products has recently become an attractive option during this period of market volatility. Mid Penn’s ability to attract funds in the future will be impacted by the public’s appetite for the safety of insured or local investments versus the returns offered by alternative choices as part of their personal investment mix.

Mid Penn’s success is dependent to a significant degree on economic conditions in Central Pennsylvania, especially in Dauphin, lower Northumberland, western Schuylkill and eastern Cumberland Counties, which Mid Penn defines as our primary market. The banking industry is affected by general economic conditions including the effects of inflation, recession, unemployment, real estate values, trends in the national and global economics, and other factors beyond our control. An economic recession or a delayed recovery over a prolonged period of time in the Central Pennsylvania area could cause an increase in the level of the Bank’s non-performing assets and loan and lease losses, thereby causing operating losses, impairing liquidity and eroding capital. Mid Penn cannot assure you that adverse changes in the local economy would not have a material adverse effect on Mid Penn’s consolidated financial condition, results of operations, and cash flows.

Supervision and Regulation

General

Bank holding companies and banks are extensively regulated under both Federal and state laws. The regulation and supervision of Mid Penn and the Bank are designed primarily for the protection of depositors, the Deposit Insurance Fund, and the monetary system, and not Mid Penn or its shareholders. Enforcement actions may include the imposition of a conservator or receiver, cease-and-desist orders and written agreements, the termination of insurance on deposits, the imposition of civil money penalties and removal and prohibition orders. If a banking regulator takes any enforcement action, the value of an equity investment in Mid Penn could be substantially reduced or eliminated.

Federal and state banking laws contain numerous provisions affecting various aspects of the business and operations of Mid Penn and the Bank. Mid Penn is subject to, among others, the regulations of the Securities and Exchange Commission and the Federal Reserve Board, and the Bank is subject to, among others, the regulations of the Pennsylvania Department of Banking and the Federal Deposit Insurance Corporation. The following descriptions of and references to applicable statutes and regulations are not intended to be complete descriptions of these provisions or their effects on Mid Penn or the Bank. They are summaries only and are qualified in their entirety by reference to such statutes and regulations.

Holding Company Regulation

Mid Penn is a registered bank holding company subject to supervision and regulation by the Board of Governors of the Federal Reserve System (the “Federal Reserve”). As such, it is subject to the Bank Holding Company Act of 1956 (“BHCA”) and many of the Federal Reserve’s regulations promulgated thereunder. The Federal Reserve has broad enforcement powers over bank holding companies, including the power to impose substantial fines and civil penalties.

The BHCA requires Mid Penn to file an annual report with the Federal Reserve regarding the holding company and its subsidiary bank. The Federal Reserve Board also makes examinations of the holding company. The Bank is not a member of the Federal Reserve System; however, the Federal Reserve possesses cease-and-desist powers over bank holding companies and their subsidiaries where their actions would constitute an unsafe or unsound practice or violation of law. The Federal Reserve Board also makes policy that guides the declaration and distribution of dividends by bank holding companies.

The BHCA restricts a bank holding company’s ability to acquire control of additional banks. In addition, the BHCA restricts the activities in which bank holding companies may engage directly or through non-bank subsidiaries.

Gramm-Leach-Bliley Financial Modernization Act

The Gramm-Leach-Bliley Act (“GLB”) became effective on March 11, 2000. The primary purpose of GLB was to eliminate barriers between investment banking and commercial banking and to permit, within certain limitations, the affiliation of financial service providers. Generally, GLB:

| • | repealed the historical restrictions against, and eliminated many federal and state law barriers to affiliations among banks, securities firms, insurance companies and other financial service providers; |

| • | provided a uniform framework for the activities of banks, savings institutions and their holding companies; |

3

Table of Contents

MID PENN BANCORP, INC.

| • | broadened the activities that may be conducted by and through national banks and other banking subsidiaries of bank holding companies; |

| • | provided an enhanced framework for protecting the privacy of consumers’ information; |

| • | adopted a number of provisions related to the capitalization, membership, corporate governance and other measures designed to modernize the Federal Home Loan Bank System; |

| • | modified the laws governing the implementation of the Community Reinvestment Act; and |

| • | addressed a variety of other legal and regulatory issues affecting both day-to-day operations and long-term activities of financial institutions. |

More specifically, under GLB, bank holding companies, such as Mid Penn, that meet certain management, capital, and Community Reinvestment Act standards, are permitted to become financial holding companies and, by doing so, to affiliate with securities firms and insurance companies and to engage in other activities that are financial in nature, incidental to such financial activities, or complementary to such activities. A bank holding company may become a financial holding company if each of its subsidiary banks is well capitalized under the FDIC Improvement Act’s prompt corrective action provisions, is well managed and has at least a satisfactory rating under the Community Reinvestment Act. The required filing is a declaration that the bank holding company wishes to become a financial holding company and meets all applicable requirements. Mid Penn has not elected to become a financial holding company at this time.

No prior regulatory approval will be required for a financial holding company to acquire a company, other than a bank or savings association, engaged in activities permitted under GLB. Activities cited by GLB as being financial in nature include:

| • | securities underwriting, dealing and market making; |

| • | sponsoring mutual funds and investment companies; |

| • | insurance underwriting and agency; |

| • | merchant banking activities; and |

| • | activities that the Federal Reserve has determined to be closely related to banking. |

In addition to permitting financial services providers to enter into new lines of business, the law allows firms the freedom to streamline existing operations and to potentially reduce costs. The Act may increase both opportunity as well as competition. Many community banks are less able to devote the capital and management resources needed to facilitate broad expansion of financial services including insurance and brokerage services.

Corporate Governance

On July 30, 2002, the Sarbanes-Oxley Act of 2002 was enacted. The Sarbanes-Oxley Act represents a comprehensive revision of laws affecting corporate governance, auditor independence and accounting standards, executive compensation, insider loans, whistleblower protection, and enhanced and timely disclosure of corporate information. The Sarbanes-Oxley Act is applicable to all companies with equity securities registered or that file reports under the Securities Exchange Act of 1934. In particular, the Sarbanes-Oxley Act established:

| • | new requirements for audit committees, including independence, expertise and responsibilities; |

| • | additional responsibilities regarding financial statements for the Chief Executive Officer and Chief Financial Officer of the reporting company; |

| • | new standards for auditors and regulation of audits; |

| • | increased disclosure and reporting obligations for the reporting company and its directors and executive officers; and |

| • | new and increased civil and criminal penalties for violations of the securities laws. |

The SEC and NASDAQ have adopted numerous rules implementing the provisions of the Sarbanes-Oxley Act that affect Mid Penn. The changes are intended to allow shareholders to monitor more effectively the performance of companies and management.

Bank Regulation

The Bank, a Pennsylvania-chartered institution, is subject to supervision, regulation and examination by the Pennsylvania Department of Banking and the FDIC. The deposits of the Bank are insured by the FDIC to the extent provided by law. The FDIC assesses deposit insurance premiums the amount of which may, in the future, depend in part on the condition of the Bank. Moreover, the FDIC may terminate deposit insurance of the Bank under certain circumstances. The Bank regulatory agencies have broad enforcement powers over depository institutions under their jurisdiction, including the power to terminate deposit insurance, to impose fines and other civil and criminal penalties, and to appoint a conservator or receiver if any of a number of conditions is met. In addition, the Bank is subject to a variety of local, state and federal laws that affect its operations.

Banking regulations include, but are not limited to, permissible types and amounts of loans, investments and other activities, capital adequacy, branching, interest rates on loans and the safety and soundness of banking practices.

4

Table of Contents

MID PENN BANCORP, INC.

Capital Requirements

Under risk-based capital requirements for bank holding companies, Mid Penn is required to maintain a minimum ratio of total capital to risk-weighted assets (including certain off-balance-sheet activities, such as standby letters of credit) of eight percent. At least half of the total capital is to be composed of common equity, retained earnings and qualifying perpetual preferred stock, less goodwill (“Tier 1 Capital” and together with Tier 2 Capital, Total Capital”). The remainder may consist of subordinated debt, non-qualifying preferred stock and a limited amount of the loan loss allowance (“Tier 2 Capital”).

In addition, the Federal Reserve Board has established minimum leverage ratio requirements for bank holding companies. These requirements provide for a minimum leverage ratio of Tier 1 Capital to adjusted average quarterly assets (“leverage ratio”) equal to 3% for bank holding companies that meet certain specified criteria, including having the highest regulatory rating. All other bank holding companies will generally be required to maintain a leverage ratio of at least 4-5%. The requirements also provide that bank holding companies experiencing internal growth or making acquisitions will be expected to maintain strong capital positions substantially above the minimum supervisory levels without significant reliance on intangible assets. Furthermore, the requirements indicate that the Federal Reserve Board will continue to consider a “Tangible Tier 1 Leverage Ratio” (deducting all intangibles) in evaluating proposals for expansion or new activity. The Federal Reserve Board has not advised Mid Penn of any specific minimum Tier 1 leverage ratio.

The Bank is subject to similar capital requirements adopted by the FDIC. The FDIC has not advised the Bank of any specific minimum leverage ratios.

The capital ratios of Mid Penn and the Bank are described in Note 18 to Mid Penn’s Consolidated Financial Statements, which are incorporated herein by reference.

Banking regulators continue to indicate their desire to further develop capital requirements applicable to banking organizations. Changes to capital requirements could materially affect the profitability of Mid Penn or the fair value of Mid Penn stock.

FDIC Improvement Act

As a result of the FDIC Improvement Act of 1991, banks are subject to increased reporting requirements and more frequent examinations by the bank regulatory agencies. The agencies also have the authority to dictate certain key decisions that formerly were left to management, including compensation standards, loan underwriting standards, asset growth, and payment of dividends. Failure to comply with these standards, or failure to maintain capital above specified levels set by the regulators, could lead to the imposition of penalties or the forced resignation of management. If a bank becomes critically undercapitalized, the banking agencies have the authority to place an institution into receivership.

Safety and Soundness Standards

Pursuant to FDICIA, the federal banking regulatory agencies have adopted a set of guidelines prescribing safety and soundness standards for depository institutions such as the Bank. The guidelines establish general standards relating to internal controls and information systems, internal audit systems, loan documentation, credit underwriting, interest rate exposure, asset growth, asset quality, earnings and compensation, fees and benefits. In general, the guidelines require, among other things, appropriate systems and practices to identify and manage the risks and exposures specified in the guidelines. The guidelines prohibit excessive compensation as an unsafe and unsound practice and describe compensation as excessive when the amounts paid are unreasonable or disproportionate to the services performed by an executive officer, employee, director or principal shareholder. In addition, the agencies adopted regulations that authorize an agency to order an institution that has been given notice by an agency that it is not satisfying any of such safety and soundness standards to submit a compliance plan. If the institution fails to submit an acceptable compliance plan or fails to implement an accepted plan, the agency must issue an order directing action to correct the deficiency and may issue an order directing other actions be taken, including restricting asset growth, restricting interest rates paid on deposits, and requiring an increase in the institution’s ratio of tangible equity to assets.

Payment of Dividends and Other Restrictions

Mid Penn is a legal entity separate and distinct from its subsidiary, the Bank. There are various legal and regulatory limitations on the extent to which the Bank can, among other things, finance, or otherwise supply funds to, Mid Penn. Specifically, dividends from the Bank are the principal source of Mid Penn’s cash funds and there are certain legal restrictions under Pennsylvania law and Pennsylvania banking regulations on the payment of dividends by state-chartered banks. The relevant regulatory agencies also have authority to prohibit Mid Penn and the Bank from engaging in what, in the opinion of such regulatory body, constitutes an unsafe or unsound banking practice. The payment of dividends could, depending upon the financial condition of Mid Penn and the Bank, be deemed to constitute such an unsafe or unsound practice. Further, under the terms of the Capital Purchase Program (“CPP”), Mid Penn is restricted from increasing its dividends on its common stock above the last per share quarterly dividend declared prior to October 14, 2008 ($0.20 per share) without permission as long as the CPP preferred stock is outstanding.

5

Table of Contents

MID PENN BANCORP, INC.

Prompt Corrective Action

In addition to the required minimum capital levels described above, federal law establishes a system of “prompt corrective actions” which Federal banking agencies are required to take, and certain actions which they have discretion to take, based upon the capital category into which a federally regulated depository institution falls. Regulations set forth detailed procedures and criteria for implementing prompt corrective action in the case of any institution, which is not adequately capitalized. Under the rules, an institution will be deemed to be “adequately capitalized” if it exceeds the minimum Federal regulatory capital requirements. However, it will be deemed “undercapitalized” if it fails to meet the minimum capital requirements, “significantly undercapitalized” if it has a total risk-based capital ratio that is less than 6.0%, a Tier 1 risk-based capital ratio that is less than 3.0%, or a leverage ratio that is less than 3.0%, and “critically undercapitalized” if the institution has a ratio of tangible equity to total assets that is equal to or less than 2.0%.

The prompt corrective action rules require an undercapitalized institution to file a written capital restoration plan, along with a performance guaranty by its holding company or a third party. In addition, an undercapitalized institution becomes subject to certain automatic restrictions including a prohibition on payment of dividends, a limitation on asset growth and expansion, in certain cases, a limitation on the payment of bonuses or raises to senior executive officers, and a prohibition on the payment of certain “management fees” to any “controlling person”. Institutions that are classified as undercapitalized are also subject to certain additional supervisory actions, including increased reporting burdens and regulatory monitoring, a limitation on the institution’s ability to make acquisitions, open new branch offices, or engage in new lines of business, obligations to raise additional capital, restrictions on transactions with affiliates, and restrictions on interest rates paid by the institution on deposits. In certain cases, bank regulatory agencies may require replacement of senior executive officers or directors, or sale of the institution to a willing purchaser. If an institution is deemed “critically undercapitalized” and continues in that category for four quarters, the statute requires, with certain narrowly limited exceptions, that the institution be placed in receivership.

Deposit Insurance

The FDIC insures deposits of the Bank through the Deposit Insurance Fund (“DIF”). The FDIC maintains the DIF by assessing depository institutions an insurance premium. The amount each institution is assessed is based upon a variety of factors that include the balance of insured deposits as well as the degree of risk the institution poses to the insurance fund. The FDIC recently increased the amount of deposits it insures from $100,000 to $250,000. This increase is temporary and will continue through December 31, 2013. The Bank pays an insurance premium into the DIF based on the quarterly average daily deposit liabilities net of certain exclusions. The FDIC uses a risk-based premium system that assesses higher rates on those institutions that pose greater risks to the DIF. The FDIC places each institution in one of four risk categories using a two-step process based first on capital ratios (the capital group assignment) and then on other relevant information (the supervisory group assignment). Subsequently, the rate for each institution within a risk category may be adjusted depending upon different factors that either enhance or reduce the risk the institution poses to the DIF, including the unsecured debt, secured liabilities and brokered deposits related to each institution. Finally, certain risk multipliers may be applied to the adjusted assessment. In 2009, the FDIC increased the amount assessed from financial institutions by increasing its risk-based deposit insurance assessment scale. The quarterly annualized assessment scale for 2009 ranged from twelve basis points of assessable deposits for the strongest institutions to 77.5 basis points for the weakest. In 2009, the FDIC also adopted a uniform special assessment rate for all institutions not to exceed 10 basis points on the individual bank’s assessment base. The total amount paid by the Bank for FDIC insurance for the year ended December 31, 2009 under these provisions was $1,163,000.

On November 12, 2009, the FDIC approved a rule to require insured institutions to prepay their estimated quarterly risk-based assessments for the fourth quarter of 2009, and for all of 2010, 2011, and 2012. An insured institution’s risk-based deposit insurance assessments will continue to be calculated on a quarterly basis, but will be paid from the amount the institution prepaid until the later of the date that amount is exhausted or June 30, 2013, at which point any remaining funds would be returned to the insured institution. Consequently, Mid Penn’s prepayment of DIF premiums made in December 2009 resulted in a prepaid asset of $2,719,000.

Environmental Laws

Management does not anticipate that compliance with environmental laws and regulations will have any material effect on Mid Penn’s capital, expenditures, earnings, or competitive position. However, environmentally related hazards have become a source of high risk and potentially unlimited liability for financial institutions.

In 1995, the Pennsylvania General Assembly enacted the Economic Development Agency, Fiduciary and Lender Environmental Liability Protection Act, which among other things, provides protection to lenders from environmental liability and remediation costs under the environmental laws for releases and contamination caused by others. A lender who engages in activities involved in the routine practices of commercial lending, including, but not limited to, the providing of financial services, holding of security interests, workout practices, foreclosure or the recovery of funds from the sale of property shall not be liable under the environmental acts or common law equivalents to the Pennsylvania Department of Environmental Resources or to any other person by virtue of the fact that the lender engages in such commercial lending practice. A lender, however, will be liable if it, its employees or agents, directly cause an immediate release or directly exacerbate a release of regulated substance on or from the property, or known and willfully compelled the borrower to commit an action which caused such release or violate an environmental act. The Economic Development Agency, Fiduciary and Lender Environmental Liability Protection Act does not limit federal liability which still exists under certain circumstances.

6

Table of Contents

MID PENN BANCORP, INC.

Consumer Protection Laws

A number of laws govern the relationship between the Bank and its customers. For example, the Community Reinvestment Act is designed to encourage lending by banks to persons in low and moderate income areas. The Home Mortgage Disclosure Act and the Equal Credit Opportunity Act attempt to minimize lending decisions based on impermissible criteria, such as race or gender. The Truth-in-Lending Act and the Truth-in-Savings Act require banks to provide certain disclosure of relevant terms related to loans and savings accounts, respectively. Anti-tying restrictions (which prohibit conditioning the availability or terms of credit on the purchase of another banking product) further restrict the Bank’s relationships with its customers.

Privacy Laws

In 2000, the federal banking regulators issued final regulations implementing certain provisions of GLB governing the privacy of consumer financial information. The regulations limit the disclosure by financial institutions, such as Mid Penn and the Bank, of nonpublic personal information about individuals who obtain financial products or services for personal, family, or household purposes. Subject to certain exceptions allowed by law, the regulations cover information sharing between financial institutions and nonaffiliated third parties. More specifically, the regulations require financial institutions to:

| • | provide initial notices to customers about their privacy policies, describing the conditions under which they may disclose nonpublic personal financial information to nonaffiliated third parties and affiliates; |

| • | provide annual notices of their privacy policies to their current customers; and |

| • | provide a reasonable method for consumers to “opt out” of disclosures to nonaffiliated third parties. |

Protection of Customer Information

In 2001, the federal banking regulators issued final regulations implementing the provisions of GLB relating to the protection of customer information. The regulations, applicable to Mid Penn and the Bank, relate to administrative, technical, and physical safeguards for customer records and information. These safeguards are intended to:

| • | insure the security and confidentiality of customer records and information; |

| • | protect against any anticipated threats or hazards to the security or integrity of such records; and |

| • | protect against unauthorized access to or use of such records or information that could result in substantial harm or inconvenience to any customer. |

Affiliate Transactions

Transactions between Mid Penn and the Bank and its affiliates are governed by Sections 23A and 23B of the Federal Reserve Act. An “affiliate” of a bank or savings institution is any company or entity that controls, is controlled by, or is under common control with the bank or savings institution. Generally, a subsidiary of a depository institution that is not also a depository institution is not treated as an affiliate of the bank for purposes of Sections 23A and 23B. Sections 23A and 23B are intended to protect insured depository institutions from suffering losses arising from transactions with non-insured affiliates, by limiting the extent to which a bank or its subsidiaries may engage in covered transactions with any one affiliate and with all affiliates of the bank in the aggregate, and requiring that such transactions be on terms that are consistent with safe and sound banking practices.

Effective April 1, 2003, Regulation W of the Federal Reserve comprehensively amended Sections 23A and 23B. The regulation unifies and updates staff interpretations issued over the years, incorporates several new interpretative proposals (such as to clarify when transactions with an unrelated third party will be attributed to an affiliate), and addresses new issues arising as a result of the expanded scope of non-banking activities engaged in by bank and bank holding companies in recent years and authorized for financial holding companies under the GLB.

The USA Patriot Act

In 2001, the Uniting and Strengthening America by Providing Appropriate Tools Required to Intercept and Obstruct Terrorism Act of 2001 (USA Patriot Act) was signed into law. The USA Patriot Act broadened the application of anti-money laundering regulations to apply to additional types of financial institutions, such as broker-dealers, and strengthened the ability of the U.S. government to detect and prosecute international money laundering and the financing of terrorism. The principal provisions of Title III of the USA Patriot Act require that regulated financial institutions, including state-chartered banks:

| • | establish an anti-money laundering program that includes training and audit components; |

| • | comply with regulations regarding the verification of the identity of any person seeking to open an account; |

| • | take additional required precautions with non-U.S. owned accounts; and |

| • | perform certain verification and certification of money laundering risk for their foreign correspondent banking relationships. |

The USA Patriot Act also expanded the conditions under which funds in a U.S. interbank account may be subject to forfeiture and increased the penalties for violation of anti-money laundering regulations. Failure of a financial institution to comply with the USA Patriot Acts requirements could have serious legal and reputational consequences for the institution. The Bank has adopted policies, procedures and controls to address compliance with the requirements of the USA Patriot Act under the existing regulations and will continue to revise and update its policies, procedures and controls to reflect changes required by the USA Patriot Act and implementing regulations.

7

Table of Contents

MID PENN BANCORP, INC.

Anti-Money Laundering and Anti-Terrorism Financing

Under Title III of the USA PATRIOT Act, also known as the International Money Laundering Abatement and Anti-Terrorism Financing Act of 2001, all financial institutions, including Mid Penn and the Bank, are required in general to identify their customers, adopt formal and comprehensive anti-money laundering programs, scrutinize or prohibit altogether certain transactions of special concern, and be prepared to respond to inquiries from U.S. law enforcement agencies concerning their customers and their transactions. Additional information-sharing among financial institutions, regulators, and law enforcement authorities is encouraged by the presence of an exemption from the privacy provisions of the GLB Act for financial institutions that comply with this provision and the authorization of the Secretary of the Treasury to adopt rules to further encourage cooperation and information-sharing. The effectiveness of a financial institution in combating money-laundering activities is a factor to be considered in any application submitted by the financial institution under the Bank Merger Act, which applies to the Bank.

Emergency Economic Stabilization Act of 2008 and Related Programs

Mid Penn is subject to the rules and regulations promulgated under the Emergency Economic Stabilization Act of 2008 (“EESA”) and related legislation as a result of its sale of preferred stock to the U.S. Treasury under the U.S. Treasury’s Capital Purchase Program (“CPP”). Additional information relating to the CPP, including restrictions on dividends and redemptions of common stock, is included in the information set forth in Item 7 of this report under the caption, “Capital Purchase Program Participation.” Furthermore, under rules and regulations of EESA to which the Mid Penn is subject, no dividends may be declared or paid on Mid Penn’s common stock and Mid Penn may not repurchase or redeem any common stock unless dividends then due and payable with respect to Treasury’s preferred stock have been paid in full. Moreover, the consent of Treasury would be required for any increase in the per share dividend amount on the common stock beyond the per share dividend declared immediately prior to October 14, 2008 ($0.20 per share per quarter) until the third anniversary of the date of Treasury’s investment, unless prior to the third anniversary, Treasury’s preferred stock is redeemed in whole or Treasury has transferred all of its preferred shares to third parties. Because of Mid Penn’s participation in the CPP, Mid Penn is subject to certain restrictions on its executive compensation practices, which are discussed in Item 7 of this report under the caption, “Capital Purchase Program Participation.”

In November 2008, the FDIC created the Temporary Liquidity Guaranty Program to strengthen confidence and encourage liquidity in the banking system by guaranteeing newly issued senior unsecured debt of banks, thrifts, and certain holding companies via its Debt Guaranty Program, and by providing full coverage of noninterest bearing deposit transaction accounts and capped NOW accounts, regardless of dollar amount via its Temporary Account Guaranty Program. As of October 31, 2009, banks were no longer eligible to issue additional debt under the Temporary Liquidity Guaranty Program and Mid Penn has opted not to participate in the Temporary Account Guaranty Program beyond December 31, 2009.

Effects of Government Policy and Potential Changes in Regulation

Changes in regulations applicable to Mid Penn or the Bank, or shifts in monetary or other government policies, could have a material affect on our business. Mid Penn’s and the Bank’s business is also affected by the state of the financial services industry in general. As a result of legal and industry changes, management believes that the industry will continue to experience an increased rate of change as the financial services industry strives for greater product offerings, market share and economies of scale.

From time to time, legislation is enacted that has the effect of increasing the cost of doing business, limiting or expanding permissible activities or affecting the competitive balance between banks and other financial institutions. Proposals to change the laws and regulations governing the operations and taxation of banks, bank holding companies and other financial institutions are frequently made in Congress, and before various bank regulatory agencies. Mid Penn cannot predict the likelihood of any major changes or the impact such changes might have on Mid Penn and/or the Bank. Various congressional bills and other proposals have proposed a sweeping overhaul of the banking system, including provisions for: limitations on deposit insurance coverage; changing the timing and method financial institutions use to pay for deposit insurance; expanding the power of banks by removing the restrictions on bank underwriting activities; and tightening the regulation of bank derivatives activities; and allowing commercial enterprises to own banks.

Mid Penn’s earnings are, and will be affected by domestic economic conditions and the monetary and fiscal policies of the United States government and its agencies. The monetary policies of the Federal Reserve have had, and will likely continue to have, an impact on the operating results of commercial banks because of the Federal Reserve’s power to implement national monetary policy to, among other things, curb inflation or combat recession. The Federal Reserve has a major impact on the levels of bank loans, investments and deposits through its open market operations in United States government securities and through its regulation of, among other things, the discount rate on borrowings of member banks and the reserve requirements against member bank deposits. It is not possible to predict the nature and impact of future changes in monetary and fiscal policies.

From time to time, various types of federal and state legislation have been proposed that could result in additional regulation of, and restrictions on, the business of Mid Penn and the Bank. As a consequence of the extensive regulation of commercial banking activities in the United States,

8

Table of Contents

MID PENN BANCORP, INC.

the Bank’s business is particularly susceptible to being affected by federal legislation and regulations that may increase the costs of doing business. Congress is currently debating major legislation that may fundamentally change the regulatory oversight of banking institutions in the United States. Whether any legislation will be enacted or additional regulations will be adopted, and how they might impact Mid Penn cannot be determined at this time.

Available Information

Mid Penn’s common stock is registered under Section 12(b) of the Securities Exchange Act of 1934 and is traded on the NASDAQ Stock Market under the trading symbol MPB. Mid Penn is subject to the informational requirements of the Exchange Act, and, accordingly, files reports, proxy statements and other information with the Securities and Exchange Commission. The reports, proxy statements and other information filed with the SEC are available for inspection and copying at the SEC’s Public Reference Room at 100 F Street, NE, Room 1580, Washington, D.C. 20549. You may obtain information on the operation of the Public Reference Room by calling the SEC at (202) 551-8090. Mid Penn is an electronic filer with the SEC. The SEC maintains an Internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC. The SEC’s Internet site address is www.sec.gov.

Mid Penn’s headquarters are located at 349 Union Street, Millersburg, Pennsylvania 17061, and its telephone number is (717) 692-2133. Mid Penn’s Internet address is www.midpennbank.com. Mid Penn makes available through its website, free of charge, its annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports as soon as reasonably practicable after filing with the Securities and Exchange Commission. Mid Penn has adopted a Code of Ethics that applies to all employees. This document is also available on Mid Penn’s website. The information included on our website is not a part of this document.

| ITEM 1A. | RISK FACTORS |

Future dividend payments and common stock repurchases are restricted by the terms of the U.S. Treasury’s equity investment in Mid Penn

Under the terms of the CPP, for so long as any preferred stock issued under the CPP remains outstanding, Mid Penn is prohibited from increasing dividends to holders of its common stock above the last per share quarterly amount in effect immediately prior to October 14, 2008 ($0.20 per share), and from making certain repurchases of equity securities, including our common stock, without the U.S. Treasury’s consent until the third anniversary of the U.S. Treasury’s investment or until the U.S. Treasury has transferred all of the preferred stock it purchased under the CPP to third parties. As long as the preferred stock issued to the U.S. Treasury is outstanding, dividend payments and repurchases or redemptions relating to certain equity securities, including Mid Penn’s common stock, are prohibited until all accrued and unpaid dividends are paid on such preferred stock, subject to certain limited exceptions.

Mid Penn is subject to interest rate risk

Mid Penn’s earnings and cash flows are largely dependent upon its net interest income. Net interest income is the difference between interest income earned on interest-earning assets such as loans and securities and interest expense paid on interest-bearing liabilities such as deposits and borrowed funds. Interest rates are highly sensitive to many factors that are beyond Mid Penn’s control, including general economic conditions and policies of various governmental and regulatory agencies and, in particular, the Board of Governors of the Federal Reserve System. Changes in monetary policy, including changes in interest rates, could influence not only the interest Mid Penn receives on loans and securities and the amount of interest it pays on deposits and borrowings, but such changes could also affect (i) Mid Penn’s ability to originate loans and obtain deposits, (ii) the fair value of Mid Penn’s financial assets and liabilities, and (iii) the average duration of Mid Penn’s mortgage-backed securities portfolio. If the interest rates paid on deposits and other borrowings increase at a faster rate than the interest rates received on loans and other investments, Mid Penn’s net interest income, and therefore earnings, could be adversely affected. Earnings could also be adversely affected if the interest rates received on loans and other investments fall more quickly than the interest rates paid on deposits and other borrowings.

Management believes it has implemented effective asset and liability management strategies to reduce the potential effects of changes in interest rates on Mid Penn’s results of operations. Any substantial, unexpected, prolonged change in market interest rates could have a material adverse effect on Mid Penn’s financial condition and results of operations.

Mid Penn is subject to lending risk

As of December 31, 2009, approximately 70.7% of Mid Penn’s loan portfolio consisted of commercial and industrial, construction and commercial real estate loans. These types of loans are generally viewed as having more risk of default than residential real estate loans or consumer loans. These types of loans are also typically larger than residential real estate loans and consumer loans. Because Mid Penn’s loan portfolio contains a significant number of commercial and industrial, construction and commercial real estate loans with relatively large balances, the deterioration of one or a few of these loans could cause a significant increase in non-performing loans. An increase in non-performing loans could result in a net loss of earnings from these loans, an increase in the provision for possible loan and lease losses and an increase in loan charge-offs, all of which could have a material adverse effect on Mid Penn’s financial condition and results of operations.

9

Table of Contents

MID PENN BANCORP, INC.

Mid Penn’s allowance for possible loan and lease losses may be insufficient

Mid Penn maintains an allowance for possible loan and lease losses, which is a reserve established through provisions for possible losses charged to expense, that represents management’s best estimate of probable losses that have been incurred within the existing portfolio of loans. The allowance, in the judgment of management, is necessary to reserve for estimated loan and lease losses and risks inherent in the loan portfolio. The level of the allowance reflects management’s continuing evaluation of industry concentrations; specific credit risks; loan loss experience; current loan portfolio quality; present economic, political and regulatory conditions and unidentified losses inherent in the current loan portfolio. The determination of the appropriate level of the allowance for possible loan and lease losses inherently involves a high degree of subjectivity and requires Mid Penn to make significant estimates of current credit risks and future trends, all of which may undergo material changes. Changes in economic conditions affecting borrowers, new information regarding existing loans, identification of additional problem credits and other factors, both within and outside of Mid Penn’s control, may require an increase in the allowance. In addition, bank regulatory agencies periodically review Mid Penn’s allowance for possible loan and lease losses and may require an increase in the provision for possible loan and lease losses or the recognition of further loan charge-offs, based on judgments different than those of management. In addition, if charge-offs in future periods exceed the allowance, Mid Penn will need additional provisions to increase the allowance for possible loan and lease losses. Any increases in the allowance will result in a decrease in net income and, possibly, capital, and may have a material adverse effect on Mid Penn’s financial condition and results of operations.

Competition from other financial institutions may adversely affect Mid Penn’s profitability

Mid Penn’s banking subsidiary faces substantial competition in originating, both commercial and consumer loans. This competition comes principally from other banks, savings institutions, mortgage banking companies and other lenders. Many of its competitors enjoy advantages, including greater financial resources and higher lending limits, a wider geographic presence, more accessible branch office locations, the ability to offer a wider array of services or more favorable pricing alternatives, as well as lower origination and operating costs. This competition could reduce the Corporation’s net income by decreasing the number and size of loans that its banking subsidiary originates and the interest rates it may charge on these loans.

In attracting business and consumer deposits, its banking subsidiary faces substantial competition from other insured depository institutions such as banks, savings institutions and credit unions, as well as institutions offering uninsured investment alternatives, including money market funds. Many of Mid Penn’s competitors enjoy advantages, including greater financial resources, more aggressive marketing campaigns, better brand recognition and more convenient branch locations. These competitors may offer higher interest rates than Mid Penn, which could decrease the deposits that Mid Penn attracts or require Mid Penn to increase its rates to retain existing deposits or attract new deposits. Increased deposit competition could adversely affect Mid Penn’s ability to generate the funds necessary for lending operations. As a result, Mid Penn may need to seek other sources of funds that may be more expensive to obtain and could increase its cost of funds.

Mid Penn’s banking subsidiary also competes with non-bank providers of financial services, such as brokerage firms, consumer finance companies, credit unions, insurance agencies and governmental organizations, which may offer more favorable terms. Some of its non-bank competitors are not subject to the same extensive regulations that govern its banking operations. As a result, such non-bank competitors may have advantages over Mid Penn’s banking subsidiary in providing certain products and services. This competition may reduce or limit Mid Penn’s margins on banking services, reduce its market share and adversely affect its earnings and financial condition.

Mid Penn’s controls and procedures may fail or be circumvented

Management regularly reviews and updates Mid Penn’s internal controls, disclosure controls and procedures, and corporate governance policies and procedures. Any system of controls, however well designed and operated, is based in part on certain assumptions and can provide only reasonable, not absolute, assurances that the objectives of the system are met. Any failure or circumvention of Mid Penn’s controls and procedures or failure to comply with regulations related to controls and procedures could have a material adverse effect on Mid Penn’s business, results of operations, and financial condition.

Mid Penn’s ability to pay dividends depends primarily on dividends from its banking subsidiary, which is subject to regulatory limits

Mid Penn is a bank holding company and its operations are conducted by its subsidiaries. Its ability to pay dividends depends on its receipt of dividends from its subsidiaries. Dividend payments from its banking subsidiary are subject to legal and regulatory limitations, generally based on net profits and retained earnings, imposed by the various banking regulatory agencies. The ability of Mid Penn’s subsidiaries to pay dividends is also subject to their profitability, financial condition, capital expenditures and other cash flow requirements. There is no assurance that Mid Penn’s subsidiaries will be able to pay dividends in the future or that Mid Penn will generate adequate cash flow to pay dividends in the future. Mid Penn’s failure to pay dividends on its common stock could have a material adverse effect on the market price of its common stock.

10

Table of Contents

MID PENN BANCORP, INC.

Mid Penn may not be able to attract and retain skilled people

Mid Penn’s success depends, in large part, on its ability to attract and retain key people. Competition for the best people in most activities engaged in by Mid Penn can be intense and Mid Penn may not be able to hire people or to retain them. The unexpected loss of services of one or more of Mid Penn’s key personnel could have a material adverse impact on Mid Penn’s business because of their skills, knowledge of Mid Penn’s market, years of industry experience, and the difficulty of promptly finding qualified replacement personnel.

Mid Penn is subject to claims and litigation pertaining to fiduciary responsibility

From time to time, customers make claims and take legal action pertaining to Mid Penn’s performance of its fiduciary responsibilities. Whether customer claims and legal action related to Mid Penn’s performance of its fiduciary responsibilities are founded or unfounded, if such claims and legal actions are not resolved in a manner favorable to Mid Penn they may result in significant financial liability and/or adversely affect the market perception of Mid Penn and its products and services as well as impact customer demand for those products and services. Any financial liability or reputation damage could have a material adverse effect on Mid Penn’s business, which, in turn, could have a material adverse effect on Mid Penn’s financial condition and results of operations.

The trading volume in Mid Penn’s common stock is less than that of other larger financial services companies

Mid Penn’s common stock is listed for trading on NASDAQ; the trading volume in its common stock is less than that of other larger financial services companies. A public trading market having the desired characteristics of depth, liquidity and orderliness depends on the presence in the marketplace of willing buyers and sellers of Mid Penn’s common stock at any given time. This presence depends on the individual decisions of investors and general economic and market conditions over which Mid Penn has no control. Given the lower trading volume of Mid Penn’s common stock, significant sales of Mid Penn’s common stock, or the expectation of these sales, could cause Mid Penn’s stock price to fall.

Mid Penn operates in a highly regulated environment and may be adversely affected by changes in federal, state and local laws and regulations

Mid Penn is subject to extensive regulation, supervision and examination by federal and state banking authorities. Any change in applicable regulations or federal, state or local legislation could have a substantial impact on Mid Penn and its operations. Additional legislation and regulations that could significantly affect Mid Penn’s powers, authority and operations may be enacted or adopted in the future, which could have a material adverse effect on its financial condition and results of operations. Further, regulators have significant discretion and authority to prevent or remedy unsafe or unsound practices or violations of laws by banks and bank holding companies in the performance of their supervisory and enforcement duties. The exercise of regulatory authority may have a negative impact on Mid Penn’s results of operations and financial condition.

Mid Penn must comply with significant anti-money laundering and anti-terrorism laws. Under these laws, Mid Penn is required, among other things, to enforce a customer identification program and file currency transaction and suspicious activity reports with the federal government. Government agencies have substantial discretion to impose significant monetary penalties on institutions, which fail to comply with these laws or make required reports.

The soundness of other financial institutions may adversely affect Mid Penn

Financial services institutions are interrelated as a result of trading, clearing, counterparty, or other relationships. Mid Penn has exposure to many different industries and counterparties, and routinely executes transactions with counterparties in the financial services industry, including commercial banks, brokers and dealers, investment banks, and other institutional clients. Many of these transactions expose Mid Penn to credit risk in the event of a default by a counterparty or client. In addition, Mid Penn’s credit risk may be exacerbated when the collateral held by Mid Penn cannot be realized upon or is liquidated at prices not sufficient to recover the full amount of the credit or derivative exposure due to Mid Penn. Any such losses could have a material adverse affect on the Mid Penn’s financial condition and results of operations.

Current levels of market volatility are unprecedented and may have materially adverse effects on our liquidity and financial condition

The capital and credit markets have been experiencing extreme volatility and disruption for more than two years. In some cases, the markets have exerted downward pressure on stock prices, security prices and credit availability for certain issuers without regard to their underlying financial strength. If the current levels of market disruption and volatility continue or worsen, there can be no assurance that we will not experience adverse effects, which may be material, on our liquidity, financial condition, and profitability.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

11

Table of Contents

MID PENN BANCORP, INC.

With the exception of the Market Square Office in Harrisburg, PA, the Bank owns its main office, branch offices and certain parking facilities related to its banking offices, all of which are free and clear of any lien. The Bank’s main office and all branch offices are located in Pennsylvania. All of these properties are in good condition and are deemed by management to be adequate for the Bank’s purposes. The table below sets forth the location of each of the Bank’s properties.

| Property Location |

Description of Property |

Property Location |

Description of Property | |||

| Main Office |

Lykens Office | |||||

| 349 Union Street |

Main Bank Office | 550 Main Street | Branch Office | |||

| Millersburg, PA 17061 |

Lykens, PA 17048 | |||||

| Elizabethville Office |

Allentown Boulevard Office | |||||

| 4642 State Route 209 |

Branch Office | 5500 Allentown Boulevard | Branch Office | |||

| Elizabethville, PA 17023 |

Harrisburg, PA 17112 | |||||

| Dalmatia Office |

Market Square Office | |||||

| 132 School House Road |

Branch Office | 17 N. Second Street | Branch Office | |||

| Dalmatia, PA 17017 |

Harrisburg, PA 17101 | |||||

| Carlisle Pike Office |

Steelton Office | |||||

| 4622 Carlisle Pike |

Branch Office | 51 South Front Street | Branch Office | |||

| Mechanicsburg, PA 17050 |

Steelton, PA 17113 | |||||

| Derry Street Office |

Middletown Office | |||||

| 4098 Derry Street |

Branch Office | 1100 Spring Garden Drive | Branch Office | |||

| Harrisburg, PA 17111 |

Middletown, PA 17057 | |||||

| Front Street Office |

Camp Hill Office | |||||

| 2615 North Front Street |

Branch Office | 2101 Market Street | Branch Office | |||

| Harrisburg, PA 17110 |

Camp Hill, PA 17011 | |||||

| Tower City Office |

Operations Center | |||||

| 545 East Grand Avenue |

Branch Office | 894 N. River Road | Operations Center | |||

| Tower City, PA 17980 |

Halifax, PA 17032 | |||||

| Dauphin Office |

||||||

| 1001 Peters Mountain Road |

Branch Office | |||||

| Dauphin, PA 17018 |

||||||

Management is not aware of any litigation that would have a material adverse effect on the consolidated financial position of the Corporation. Mid Penn and the Bank have no proceedings pending other than ordinary routine litigation occurring in the normal course of business. In addition, management does not know of any material proceedings contemplated by governmental authorities against Mid Penn or the Bank or any of its properties.

ITEM 4. (REMOVED AND RESERVED)

12

Table of Contents

MID PENN BANCORP, INC.

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED SHAREHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

The Corporation’s common stock is traded on the NASDAQ Stock Market under the symbol MPB. The following table shows the range of high and low sale prices for the Corporation’s stock and cash dividends paid for the quarters indicated.

| High | Low | Cash Dividends Paid | |||||||

| Quarter Ended: |

|||||||||

| March 31, 2009 |

$ | 22.00 | $ | 17.36 | $ | 0.20 | |||

| June 30, 2009 |

24.00 | 15.80 | 0.16 | ||||||

| September 30, 2009 |

17.99 | 14.00 | 0.16 | ||||||

| December 31, 2009 |

15.06 | 9.75 | — | ||||||

| March 31, 2008 |

$ | 26.70 | $ | 23.00 | $ | 0.20 | |||

| June 30, 2008 |

27.50 | 22.85 | 0.20 | ||||||

| September 30, 2008 |

25.85 | 21.60 | 0.20 | ||||||

| December 31, 2008 |

24.00 | 14.75 | 0.20 | ||||||

Transfer Agent: Registrar and Transfer Company, 10 Commerce Drive, Cranford, NJ 07016. Phone: 1-800-368-5948.

Number of Shareholders: As of February 16, 2010, there were approximately 1,476 shareholders of record of Mid Penn’s common stock.

Dividends: Quarterly cash dividends of $0.52 in the aggregate were paid during 2009. Quarterly cash dividends of $0.80 in the aggregate were paid during 2008. The quarterly dividend payment was suspended during the fourth quarter of 2009 consistent with the Federal Reserve Board policy that dividend payouts should not exceed net income for the previous four quarters, net of dividends previously paid during that period. Mid Penn presently plans to resume a quarterly dividend payment to common shareholders once the provisions of the Federal Reserve policy can be satisfied.

Dividend Reinvestment and Stock Purchases: Shareholders of Mid Penn may acquire additional shares of common stock by reinvesting their cash dividends under the Dividend Reinvestment Plan without paying a brokerage fee. Voluntary cash contributions may also be made under the Plan. For additional information about the Plan, contact the Transfer Agent.

Annual Meeting: The Annual Meeting of the Shareholders of Mid Penn will be held at 10:00 a.m. on Tuesday, May 4, 2010, at 349 Union Street, Millersburg, Pennsylvania.

Accounting, Auditing and Internal Control Complaints: Information on how to report a complaint regarding accounting, internal accounting controls or auditing matters is available at Mid Penn’s website: www.midpennbank.com.

13

Table of Contents

MID PENN BANCORP, INC.

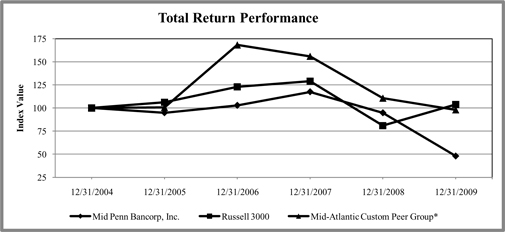

Stock Performance Graph

| Period Ending | ||||||||||||

| Index |

12/31/2004 | 12/31/2005 | 12/31/2006 | 12/31/2007 | 12/31/2008 | 12/31/2009 | ||||||

| Mid Penn Bancorp, Inc. |

100.0 | 94.8 | 102.8 | 117.5 | 94.7 | 47.9 | ||||||

| Russell 3000 |

100.0 | 106.1 | 122.8 | 129.1 | 80.9 | 103.9 | ||||||

| Mid-Atlantic Custom Peer Group* |

100.0 | 100.7 | 168.2 | 155.9 | 110.7 | 98.0 | ||||||

| * | Mid-Atlantic Custom Peer Group consists of Mid-Atlantic commercial banks with assets less than $1B. |

Source : SNL Financial LC, Charlottesville, VA

© 2010

A detailed list of the Banks comprising the Mid-Atlantic Custom Peer Group is incorporated herein by reference to Exhibit 99.1, which is attached to this Annual Report on Form 10-K.

14

Table of Contents

MID PENN BANCORP, INC.

ITEM 6. SELECTED FINANCIAL DATA

Summary of Selected Financial Data

| (Dollars in thousands, except per share data) | ||||||||||||||||||||

| 2009 | 2008 | 2007 | 2006 | 2005 | ||||||||||||||||

| INCOME: |

||||||||||||||||||||

| Total Interest Income |

$ | 31,336 | $ | 31,856 | $ | 31,444 | $ | 28,214 | $ | 23,294 | ||||||||||

| Total Interest Expense |

13,304 | 14,890 | 15,339 | 12,732 | 9,557 | |||||||||||||||

| Net Interest Income |

18,032 | 16,966 | 16,105 | 15,482 | 13,737 | |||||||||||||||

| Provision for Loan and Lease Losses |

9,520 | 1,230 | 925 | 735 | 225 | |||||||||||||||

| Noninterest Income |

3,656 | 3,682 | 3,481 | 3,028 | 2,953 | |||||||||||||||

| Noninterest Expense |

16,671 | 14,726 | 12,596 | 11,263 | 10,262 | |||||||||||||||

| Income (Loss) Before (Benefit from) Provision for Income Taxes |

(4,503 | ) | 4,692 | 6,065 | 6,512 | 6,203 | ||||||||||||||

| (Benefit from) Provision for Income Taxes |

(2,208 | ) | 1,104 | 1,394 | 1,624 | 1,600 | ||||||||||||||

| Net (Loss) Income |

(2,295 | ) | 3,588 | 4,671 | 4,888 | 4,603 | ||||||||||||||

| Preferred Stock Dividends and Discount Accretion |

514 | 16 | — | — | — | |||||||||||||||

| Net (Loss) Income Available to Common Shareholders |

(2,809 | ) | 3,572 | 4,671 | 4,888 | 4,603 | ||||||||||||||

| COMMON STOCK DATA PER SHARE: |

||||||||||||||||||||

| (Loss) Earnings Per Common Share (Basic) |

$ | (0.81 | ) | $ | 1.03 | $ | 1.34 | $ | 1.39 | $ | 1.31 | |||||||||

| (Loss) Earnings Per Common Share (Fully Diluted) |

(0.81 | ) | 1.03 | 1.34 | 1.39 | 1.31 | ||||||||||||||

| Cash Dividends |

0.52 | 0.80 | 0.80 | 0.80 | 0.80 | |||||||||||||||

| Book Value |

10.55 | 11.75 | 11.56 | 11.12 | 10.48 | |||||||||||||||

| AVERAGE SHARES OUTSTANDING (BASIC) |

3,479,780 | 3,483,097 | 3,497,806 | 3,514,820 | 3,515,714 | |||||||||||||||

| AVERAGE SHARES OUTSTANDING (FULLY DILUTED) |

3,479,780 | 3,483,153 | 3,497,806 | 3,514,820 | 3,515,714 | |||||||||||||||

| AT YEAR-END: |

||||||||||||||||||||

| Investments |

$ | 47,345 | $ | 52,739 | $ | 50,250 | $ | 57,261 | $ | 54,549 | ||||||||||

| Loans and Leases, Net of Unearned Discount |

480,385 | 434,643 | 377,128 | 358,612 | 311,837 | |||||||||||||||

| Allowance for Loan and Lease Losses |

7,686 | 5,505 | 4,790 | 4,187 | 3,704 | |||||||||||||||

| Total Assets |

606,010 | 572,999 | 509,757 | 491,694 | 438,110 | |||||||||||||||

| Total Deposits |

500,015 | 436,824 | 372,817 | 364,226 | 325,274 | |||||||||||||||

| Short-term Borrowings |

16,044 | 23,977 | 37,349 | 24,275 | 12,342 | |||||||||||||||

| Long-term Debt |

38,057 | 55,223 | 54,581 | 59,713 | 59,838 | |||||||||||||||

| Shareholders’ Equity |

46,704 | 50,890 | 40,444 | 39,085 | 36,861 | |||||||||||||||

| RATIOS: |

||||||||||||||||||||

| Return on Average Assets |

-0.39 | % | 0.67 | % | 0.94 | % | 1.08 | % | 1.10 | % | ||||||||||

| Return on Average Shareholders’ Equity |

-4.43 | % | 8.87 | % | 11.84 | % | 12.93 | % | 12.87 | % | ||||||||||

| Cash Dividend Payout Ratio |

-64.40 | % | 77.67 | % | 59.70 | % | 54.79 | % | 55.56 | % | ||||||||||

| Allowance for Loan and Lease Losses to Loans and Leases |

1.60 | % | 1.27 | % | 1.27 | % | 1.17 | % | 1.19 | % | ||||||||||

| Average Shareholders’ Equity to Average Assets |

8.88 | % | 7.55 | % | 7.82 | % | 8.34 | % | 8.55 | % | ||||||||||

15

Table of Contents

| MID PENN BANCORP, INC. | Management’s Discussion and Analysis |

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

SPECIAL CAUTIONARY NOTICE REGARDING FORWARD-LOOKING STATEMENTS

Certain of the matters discussed in this document may constitute forward-looking statements for purposes of the Securities Act of 1933, as amended, and the Securities Exchange Act of 1934, as amended, and as such may involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of Mid Penn to be materially different from future results, performance or achievements expressed or implied by such forward-looking statements. The words “expect,” “anticipate,” “intend,” “plan,” “believe,” “estimate,” and similar expressions are intended to identify such forward-looking statements.

Mid Penn’s actual results may differ materially from the results anticipated in these forward-looking statements due to a variety of factors, including, without limitation:

| • | The effects of future economic conditions on Mid Penn and its customers; |

| • | Governmental monetary and fiscal policies, as well as legislative and regulatory changes; |