Attached files

| file | filename |

|---|---|

| EX-23.1 - CONSENT OF AUDITOR - Feihe International Inc | v177416_ex23-1.htm |

| EX-31.2 - SECTION 302 CERTIFICATION OF PFO - Feihe International Inc | v177416_ex31-2.htm |

| EX-31.1 - SECTION 302 CERTIFICATION OF PEO - Feihe International Inc | v177416_ex31-1.htm |

| EX-32.1 - SECTION 906 CERTIFICATION OF PEO AND PFO - Feihe International Inc | v177416_ex32-1.htm |

| EX-21.1 - SUBSIDIARIES OF THE REGISTRANT - Feihe International Inc | v177416_ex21-1.htm |

U.S.

SECURITIES AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

10-K

|

x

|

ANNUAL

REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES AND EXCHANGE ACT OF

1934

|

For the fiscal year ended December 31,

2009

|

o

|

TRANSITION

REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

|

For the transition period from

______________ to ________________

Commission

File Number: 001-32473

AMERICAN

DAIRY, INC.

(Exact

name of registrant as specified in its charter)

|

Utah

|

90-0208758

|

|

(State

or other jurisdiction of Incorporation or

organization)

|

(I.R.S.

Employer Identification No.)

|

Star

City International Building, 10 Jiuxianqiao Road, C-16th Floor

Chaoyang

District, Beijing, China 100016

(Address

of principal executive offices)

Registrant’s

telephone number, including area code: 86 (10) 6431-9357

Securities

registered under Section 12(b) of the Exchange Act:

|

Title

of each class

|

Name

of each exchange on which registered

|

|

Common

Stock

|

New

York Stock Exchange, Inc.

|

Securities

registered under Section 12(g) of the Exchange Act: None

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in

Rule 405 of the Securities Act. o Yes

x No

Indicate

by check mark if the registrant is not required to file reports pursuant to

Section 13 or Section 15(d) of the Act. o Yes

x No

Indicate

by check mark whether the registrant (1) has filed all reports required to be

filed pursuant to Section 13 or Section 15(d) of the Securities Exchange Act of

1934 during the preceding 12 months (or for such shorter period that the

registrant was required to file such reports), and (2) has been subject to such

filing requirements for the past 90 days. x Yes

o

No

Indicate

by check mark whether the registrant has submitted electronically and posted on

its corporate Web site, if any, every Interactive Data File required to be

submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this

chapter) during the preceding 12 months (or for such shorter period that the

registrant was required to submit and post such files). o Yes

o

No

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K is not contained herein, and will not be contained, to the best

of registrant’s knowledge, in definitive proxy or information statements

incorporated by reference in Part III of this Form 10-K or any amendment to this

Form 10-K. x

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, or a non-accelerated filer. See definition

of “accelerated filer and large accelerated filer” in Rule 12b-2 of

the Exchange Act. (Check one):

|

Large

accelerated filer o

|

Accelerated

filer x

|

Non-accelerated

filer o

|

Smaller Reporting Company x

|

Indicate

by check mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Act). o Yes

x No

The

aggregate market value of the voting and non-voting common equity held by

non-affiliates of the registrant as of the last business day of the

registrant’s most recently completed second fiscal quarter, based upon the

closing sale price of the registrant’s common stock on June 30, 2009 as

reported on the NYSE, was approximately $267,000,000.

As of

March 10, 2010, there were 21,707,376 shares of the

registrant’s common stock outstanding.

DOCUMENTS

INCORPORATED BY REFERENCE

Certain

information is incorporated by reference to the Proxy Statement for the

registrant’s 2010 Annual Meeting of Shareholders to be filed with the Securities

and Exchange Commission pursuant to Regulation 14A not later than 120 days after

the end of the fiscal year covered by this Form 10-K.

TABLE

OF CONTENTS

|

PART I

|

||||

|

Item 1.

|

Business

|

1

|

||

|

Item 1A.

|

Risk Factors

|

11

|

||

|

Item 1B.

|

Unresolved Staff Comments

|

21

|

||

|

Item 2.

|

Properties

|

21

|

||

|

Item 3.

|

Legal Proceedings

|

22

|

||

|

Item 4.

|

(Removed and Reserved)

|

22

|

||

|

PART II

|

||||

|

Item 5.

|

Market for the Registrant’s Common Stock, Related

Shareholder Matters and Issuer Repurchases of Equity

Securities

|

23

|

||

|

Item 6.

|

Selected Financial Data

|

25

|

||

|

Item 7.

|

Management’s Discussion and Analysis of Financial

Condition and Results of Operations

|

26

|

||

|

Item 7A.

|

Quantitative and Qualitative Disclosures About

Market Risk

|

36

|

||

|

Item 8.

|

Financial Statements and Supplementary

Data

|

37

|

||

|

Item 9.

|

Changes in and Disagreements with Accountants on

Accounting and Financial Disclosure

|

37

|

||

|

Item 9A.

|

Controls and Procedures

|

37

|

||

|

Item 9B.

|

Other Information

|

39

|

||

|

PART III

|

||||

|

Item 10.

|

Directors, Executive Officers and Corporate

Governance

|

40

|

||

|

Item 11.

|

Executive Compensation

|

40

|

||

|

Item 12.

|

Security Ownership of Certain Beneficial Owners

and Management and Related Shareholder Matters

|

40

|

||

|

Item 13.

|

Certain Relationships and Related Transactions,

and Director Independence

|

40

|

||

|

Item 14.

|

Principal Accountant Fees and

Services

|

40

|

||

|

PART IV

|

||||

|

Item 15.

|

Exhibits and Financial Statement

Schedules

|

41

|

In

this Annual Report on Form 10-K, references to “dollars” and “$” are to United

States dollars and, unless the context otherwise requires, references to

“American Dairy,” “we,” “us” and “our” refer to American Dairy, Inc. and its

consolidated subsidiaries.

PART

I

Item

1. Business

Overview

We are a

leading producer and distributor of milk powder, soybean milk powder, and

related dairy products in the People’s Republic of China, or the

PRC. Using proprietary processing techniques, we make products that

are specially formulated for particular ages, dietary needs and health

concerns. We have over 200 company-owned milk collection stations,

two company-owned dairy farms, seven production facilities with an aggregate

milk powder production capacity of approximately 1,234 tons per day and an

extensive distribution network that reaches over 95,000 retail outlets

throughout China.

Corporate

History and Structure

We were

incorporated in the State of Utah on December 31, 1985, originally under the

corporate name of Gaslight, Inc. We were inactive until March 30, 1988, when we

changed our corporate name to Lazarus Industries, Inc. and engaged in the

business of manufacturing and marketing medical devices. We

discontinued this business in 1991 and became a non-operating public company

shell. Effective May 7, 2003, we acquired 100% of the issued and

outstanding capital stock of American Flying Crane Corporation, or AFC, a

Delaware corporation that operates a dairy business in China through various

subsidiaries. In connection with that acquisition, we changed our

name to American Dairy, Inc.

Today, we

own various subsidiaries in the PRC that operate our business,

including:

|

·

|

Heilongjiang

Feihe Dairy Co., Limited, or Feihe Dairy, which produces, packages and

distributes milk powder and other dairy

products;

|

|

·

|

Gannan

Flying Crane Dairy Products Co., Limited, or Gannan Feihe, which produces

milk products;

|

|

·

|

Shanxi

Feihesantai Biotechnology Scientific and Commercial Co., Limited, or

Shanxi Feihe, which produces walnut and soybean products;

|

|

|

·

|

Langfang

Flying Crane Dairy Products Co., Limited, or Langfang Feihe, which

packages and distributes finished

products;

|

|

·

|

Baiquan

Feihe Dairy Co., Limited, or Baiquan Dairy, which produces milk

products;

|

|

·

|

Heilongjiang

Feihe Kedong Feedlots Co., Limited, or Kedong Farms, which operates dairy

farms;

|

|

·

|

Heilongjiang

Feihe Gannan Feedlots Co., Limited, or Gannan Farms, which operates dairy

farms;

|

|

·

|

Heilongjiang

Aiyingquan International Trading Co., Limited, or Aiyingquan, which

markets and distributes water and cheese, specifically marketed for

consumption by children; and

|

|

·

|

Heilongjiang

Flying Crane Trading Co., Limited, or Heilongjiang Trading, which sells

milk and soybean related products.

|

1

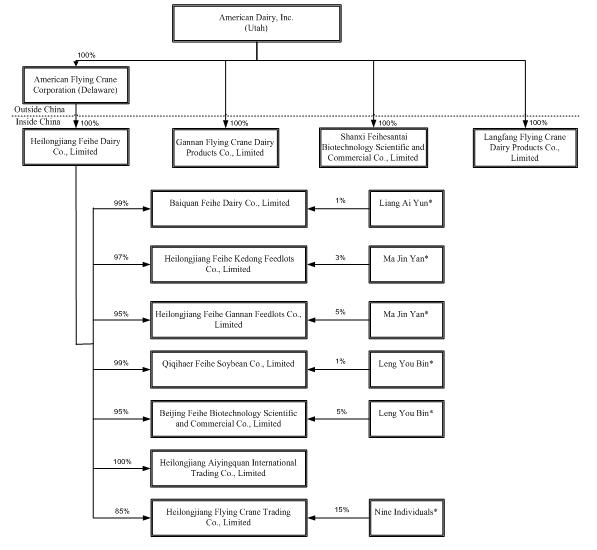

The following chart reflects the current corporate structure of the American Dairy entities:

* Indicates

a nominee shareholder who, pursuant to a former requirement under the PRC

Company Law that certain PRC companies have at least two shareholders, holds its

equity interest for the benefit of the majority shareholder.

Principal

Products

Our

products fall into four main product categories: milk powder, soybean

powder, rice cereal and walnut and other products.

Milk

Powder

Milk

powder is our primary product and is divided into several

sub-categories. We produce milk powder for infants and young children

formulated for zero to six months, six months to one year, one to three years

and three to six years of age. We also produce milk powder for

expectant mothers, students and for the middle-aged and elderly

populations. In addition, we occasionally purchase semi-finished milk

powder, which we refer to as “raw milk powder,” from third parties, which we

then process and distribute to beverage manufacturers and other wholesalers for

use in their blended drink products.

2

Soybean

Powder

Soybean

powder is an auxiliary product to our milk powders and represents a low fat,

high calcium alternative to milk powder, particularly for seniors.

Rice

Cereal

Rice

cereal is an auxiliary product to our milk powders and represents a low fat,

high calcium alternative to milk powder, particularly for young children,

teenagers, and seniors. We purchase semi-finished rice cereal from

third parties, process it, and then distribute it to wholesalers and

retailers.

Walnut

and Other Products

We

produce other auxiliary products that we market in conjunction with our infant

milk powder, as well as to health-conscious adults. Walnut products

include walnut powder and walnut oil. Other products include cream,

skim milk powder, full milk powder, butter, cheese and other related milk powder

products and water and cheese marketed specifically for children.

Product

Sales

The

following table reflects the sales of our principal products during the fiscal

years ended December 31, 2009 and 2008:

|

2009

|

2008

|

2009

over 2008

|

||||||||||||||||||||||||||||||||||

|

Product name

|

Quantity

(Kg’000)

|

Amount

($’000)

|

% of

Sales

|

Quantity

(Kg’000)

|

Amount

($’000)

|

% of

Sales

|

Quantity

(Kg’000)

|

Amount

($’000)

|

% of

Sales

|

|||||||||||||||||||||||||||

|

Milk

powder

|

28,783

|

216,230

|

79.8

|

16,311

|

121,255

|

62.8

|

12,472

|

94,975

|

78.3

|

|||||||||||||||||||||||||||

|

Raw

milk powder

|

11,637

|

34,328

|

12.7

|

16,572

|

60,753

|

31.4

|

(4,935)

|

(26,425)

|

(43.5)

|

|||||||||||||||||||||||||||

|

Soybean

powder

|

3,349

|

7,319

|

2.7

|

2,153

|

4,400

|

2.3

|

1,196

|

2,919

|

66.3

|

|||||||||||||||||||||||||||

|

Rice

cereal

|

1,103

|

6,730

|

2.5

|

816

|

4,631

|

2.4

|

287

|

2,099

|

45.3

|

|||||||||||||||||||||||||||

|

Walnut

products

|

601

|

3,070

|

1.1

|

327

|

1,663

|

0.9

|

274

|

1,407

|

84.6

|

|||||||||||||||||||||||||||

|

Other

|

543

|

3,401

|

1.3

|

727

|

490

|

0.3

|

(184)

|

2,911

|

594.1

|

|||||||||||||||||||||||||||

|

Total

|

46,016

|

271,078

|

100

|

36,906

|

193,192

|

100

|

9,110

|

77,886

|

40

|

|||||||||||||||||||||||||||

Sources

of Milk

We have

entered into supply contracts with numerous small dairy farmers that have

provided us access to over 200,000 cows that provide milk to our over 200

company-owned milk collection stations. On average, each cow provides

four tons of milk per year, which farmers deliver to our milk collection

stations. In addition, we own two dairy farms, Gannan Farms and

Kedong Farms, construction of which we completed in the fourth quarter of

2009. Gannan Farms and Kedong Farms currently house a total of

approximately 14,000 Australian Holstein cows, each of which, on average,

provides us with 8-10 tons of milk per year. We expect that each

of our dairy farms will have annual capacity to source up to 70,000 tons of

fresh milk per year.

Raw

Milk Processing

We

believe that, through purchasing raw milk locally and employing minimal

processing techniques, we are able to preserve the fresh taste of

milk. The industry standard for the time it takes for raw milk to be

converted to milk powder is approximately 48 hours. Many large

regional dairies, we believe, process raw milk that may be three to four days

old. Milk processed by conventional farms for sale to regional

dairies is typically stored at the farm for a minimum of two days, commonly

spends a full day in transit to the dairy facility, and is processed the

following day.

3

However,

our standard is to process the raw milk within 6-24 hours after milking,

depending upon the time of day the raw milk is delivered to

us. Within this time, the milk is chilled, transported, separated,

sterilized and spray-dried. The raw milk is first received from milk

collection centers or from our company-owned dairy farms. Fully

enclosed, stainless-steel vacuum milking machines are used to receive the raw

milk. Once received, the raw milk will no longer have any contact

with air and is immediately processed with refrigeration equipment that cools

the raw milk within four seconds to approximately zero to four degrees

Celsius. The raw milk is then stored in air-tight tanks in

preparation for advanced processes, which include milk fat separation,

sterilization and spray-drying.

The milk

used in our products is not homogenized. During homogenization,

pressurized milk is forced through openings smaller than the size of the fat

globules present in milk, breaking them into smaller particles. Thus

treated, the milk fat remains suspended and does not separate out in the form of

cream. We believe that this process adversely affects the taste and

feel of milk. In addition, our milk is pasteurized at the lowest

temperatures allowed by law to avoid imparting a cooked flavor to the

milk. When the milk is clarified and the butterfat removed to yield

cream and skim milk, a process of cold separation is used, rather than the more

commonly employed hot separation, which we believe adversely affects the flavor

of the milk.

Dairy

Product Processing

Our

products are made in small batches using minimal processing techniques to

maintain freshness and allow maximum flavor and nutrition retention. They

are made with wholesome ingredients and no chemicals or additives are

employed. Our dairy products arrive to consumers in our marketing

area sooner after production than most other dairy products because they are

produced locally. To assure product quality, the beginning of each

production run is sampled for flavor, aroma, texture and appearance. In

addition, inspectors conduct spot-checks for bacteria and butterfat content in

our products, as well as sanitary conditions in our facilities.

Quality

Assurance

We are

committed to delivering high-quality dairy products. We apply a

25-step quality control process that involves over a hundred points of testing

from the feed for the dairy cows, throughout our manufacturing process, and

extending to semi-finished products, which we purchase from third parties for

further processing, and finished products.

The

production facilities we have constructed comply with pharmaceutical good

manufacturing practice, or GMP, standards, a higher level of quality control

than required for consumer goods manufacturing facilities. Since

2000, our production facilities have obtained ISO 9002 and HACCP quality

assurance certifications, as well as quality certifications from the PRC

regulatory authorities. Our processing equipment is manufactured by

well-known European manufacturing companies. We use whole-sealing and

mechanized vacuum milk-pressing devices with freezing equipment for each milk

station, which allows us to reduce the temperature of raw milk to zero to four

degrees Celsius within seconds for storage. Our equipment also

eliminates external air contact from the time milk is collected through the time

that it is fully processed. We employ automated processes and

scientific parameters throughout the manufacturing process that are designed to

ensure that all products meet our quality requirements. We have

in-house laboratories that utilize proprietary in-line sampling techniques to

ensure the quality and safety of the entire production process, from raw

materials to semi-finished products to finished products. We believe

that our rigorous testing and inspection procedures have been critical in

ensuring that our products are free from melamine and other contaminants, are

premium quality products and are safe and healthy for customers.

Production

and Packaging Facilities

We own

and operate seven production and packaging facilities. The production

facilities we have constructed comply with pharmaceutical GMP standards, a

higher level of quality control than required for consumer goods manufacturing

facilities. Since 2000, our production facilities have obtained ISO

9002 and HACCP quality assurance certifications, as well as quality

certifications from the PRC regulatory authorities. We believe that

our design standards help us assure our product quality. We believe

that we are one of the few PRC milk producers that has processing areas that

meet a 300,000 cleanliness purification standard, which means that there are

less than 300,000 dust particles per cubic centimeter of air. In a

standard room, dust particles can reach over two million dust particles per

cubic centimeter of air. Continuing our commitment to quality, we

have also added testing equipment and other quality control procedures to our

processing equipment manufactured by known European and American manufacturing

companies.

4

Feihe

Dairy

Located

in Kedong, Heilongjiang Province, China, the Feihe Dairy premises comprise

approximately 88,221 square meters. The plant is approximately 9

years old, although it was completely remodeled in 2005. Feihe Dairy

principally produces infant milk formula and has a production capacity of 550

tons per day of milk powder. In addition, Feihe Dairy serves as a

packaging facility and packages approximately 22,000 tons of products per

year.

Gannan

Feihe

Located

in Heilongjiang Province, China, the Gannan Feihe premises comprise

approximately 300,000 square meters. The plant is approximately 4

years old and commenced milk powder production in 2008. It is

currently under expansion and is expected to be finished in August

2010. Gannan Feihe principally produces infant milk formula and has a

production capacity of approximately 300 tons per day of milk

powder.

Langfang

Feihe

Located

in Hebei Province, China, the Langfang Feihe premises comprise approximately

80,243 square meters. The plant is approximately 4 years old and

commenced operations in 2007. Langfang Feihe primarily serves as a

packaging and distribution facility and packages approximately 50,000 tons of

products per year.

Shanxi

Feihe

Located

in Shanxi Province, China, the Shanxi Feihe premises comprise approximately

40,000 square meters. The plant is approximately 6 years

old. Shanxi Feihe principally produces soybean powder, walnut powder

and walnut oil and has a production capacity of approximately 5,000 tons per

year of soybean powder and walnut powder combined, and 1,000 tons per year of

walnut oil.

Baiquan

Dairy

Located

in Heilongjiang Province, China, the Baiquan Dairy premises comprise

approximately 36,000 square meters. The plant is approximately 18

years old, although it was completely remodeled in 2004. Baiquan

Dairy principally produces infant milk formula and has a production capacity of

approximately 100 tons per day of milk powder.

Qiqihaer

Feihe

Located

in Heilongjiang Province, China, the Qiqihaer Feihe premises comprise

approximately 90,000 square meters. The plant is approximately 5

years old. Qiqihaer Feihe principally produces infant milk formula

and adult milk formula and has a production capacity of approximately 270 tons

per day of milk powder. Qiqihaer Feihe also produces butter and has a

production capacity of approximately 15 tons per day.

Longjiang

Feihe

Located

in Heilongjiang Province, China, the Longjiang Feihe premises comprise

approximately 29,690 square meters. The plant is approximately 19 years old and

is currently under expansion which is expected to be complete in May 2011.

Longjiang Feihe produces adult milk formula and has a production capacity of

approximately 16 tons per day of milk powder. Longjiang Feihe also produces raw

milk powder and has a production capacity approximately 11 tons per

day.

5

The table

below summarizes key information regarding our production and packaging

plants.

|

Facility

|

Province/

Region

|

Products

|

Production

Capacity

|

Packaging Capacity

(tons/year)

|

||||||

|

Feihe Dairy

|

Heilongjiang

|

Infant milk formula

|

550 (tons/day)

|

22,000

|

||||||

|

Gannan Feihe

|

Heilongjiang

|

Infant milk formula

|

300 (tons/day)

|

N/A

|

||||||

|

Langfang Feihe

|

Hebei

|

N/A

|

N/A

|

50,000

|

||||||

|

Shanxi Feihe

|

Shanxi

|

Walnut powder

& Soybean powder;

|

5,000 (tons/year)

|

N/A

|

||||||

| Walnut oil |

1,000 (tons/year)

|

|||||||||

|

Baiquan Dairy

|

Heilongjiang

|

Infant milk formula

|

100 (tons/day)

|

N/A

|

||||||

|

Qiqihaer Feihe

|

Heilongjiang

|

Infant milk formula; Adult milk powder

|

270 (tons/day)

|

N/A

|

||||||

| Butter |

15 (tons/day)

|

|||||||||

|

Longjiang

Feihe

|

Heilongjiang

|

Adult milk powder;

|

14

(tons/day)

|

N/A

|

||||||

| Raw milk powder |

10

(tons/day)

|

|||||||||

Sources

of Walnut and Soybeans

We order

walnuts and soybeans from local farmers for delivery to the Feihe

Dairy. We then distribute these raw materials to our facilities as

necessary.

Product

Distribution

Currently,

our products are sold in stores nationwide throughout China, except in Hong Kong

SAR, Macau SAR and Taiwan. Prior to distribution, we route our

products to our Feihe Dairy and Langfang Feihe for final

packaging. Feihe Dairy then distributes our finished products

primarily in northeastern China, including Heilongjiang, Jilin and Liaoning

Provinces, and Langfang Feihe distributes our finished products throughout the

rest of China. We have a distribution team based in our corporate

headquarters that coordinates with a network of over 450 dealers or

representatives in key provinces across China. The dealers, in turn,

each typically hire one or two secondary agents who assist in the distribution

process, including inventory management, product sales, customer service and

payments. Dealer agents display and sell our products in specially

designated areas in stores. In addition, in 2008 we began

distributing our raw milk powder to beverage manufacturers and other wholesalers

for use in their blended drink products. In 2010, we established a system to

monitor distributor inventory levels and cross-territory selling

activity.

Generally,

we deliver our products only after receipt of payment from the

dealer. We typically enter into new agreements with our dealers each

year that specify sales targets and territories, among other

provisions. We seek to expand the number of key provinces served by

our dealer network as part of our growth strategy and ultimately to establish a

distribution system based upon local production at local dairies. We

currently distribute our products to 29 provinces in China and to over 95,000

retail outlets.

Customers

No single

customer equaled or exceeded 10% of our sales during the years ended December

31, 2009 or 2008.

Intellectual

Property

We rely

principally on trade secrets and confidentiality agreements to protect our

proprietary product formulations and production processes. We have

obtained trademark registrations for the use of our trade name “Feihe,” as well

as our “Feifan,” “Feihui,” “Feirei,” “Feiyue,” and “Beidiqi” Chinese brands and

our “Firmus” and “Babyrich” English brand names, which have been registered with

the PRC Trademark Bureau of the State Administration for Industry and Commerce

with respect to our milk products. We believe our trademarks are

important to the establishment of consumer recognition of our

products. However, due to uncertainties in PRC trademark law, the

protection afforded by our trademarks may be less than we currently expect and

may, in fact, be insufficient. Moreover, even if it is sufficient, in

the event any of our trademarks are challenged or infringed, we may not have the

financial resources to defend it against any challenge or infringement and such

defense could in any event be unsuccessful. Moreover, any events or

conditions that negatively impact our trademark could have a material adverse

effect on our business, operations and finances.

6

Research

and Development

As of

March 10, 2010, we had six technicians engaged in research and development

activities. These technicians monitor quality control at our

production facilities to ensure that the processing, packaging and distribution

of our milk products result in high quality premium milk products that are safe

and healthy for customers. These technicians also pursue methods and

techniques to improve the taste and quality of our milk products and to evaluate

new milk products for further production based upon changes in consumer tastes,

trends and the introduction of competitive products by other milk

producers.

During

the fiscal years ended December 31, 2009 and 2008, we spent approximately

$66,000 and $137,000, respectively, per year on research and development,

representing amounts paid in compensation to our six quality control technicians

described above.

Growth

Strategy

We

believe the market for dairy products in China is growing rapidly, including the

market for high quality dairy products. Our growth strategy involves

increasing market share during this rapid growth phase. To implement

this strategy, we plan to:

|

·

|

Enhance

distribution capabilities in PRC markets. We plan to

expand our distribution network in first-tier markets in the PRC,

including Beijing, Shanghai, Guangzhou, Shenzhen and other major second

and third-tier cities in the Pearl River Delta. In addition, we plan

to further increase our sales points across China, focusing on southern

and western China. Our currently extensive distribution network,

which reaches many provincial capital and sub-provincial cities, has

special channels into first-tier markets that we plan to expand. We

believe that positioning our brand as a high-quality line of products in

these markets will facilitate our

expansion.

|

|

·

|

Strengthen

our premium quality brand awareness. We

believe that our products enjoy a reputation for high quality among those

familiar with them, and our products routinely pass government and

internal quality inspections. We have increased our advertising

expenses and plan to continue advertising on China Central Television, or

CCTV, as well as provincial stations in China, in order to market our

products as premium and super-premium products. We believe many

consumers in China tend to regard higher prices as indicative of higher

quality and higher nutritional value, and as a result consumers with

higher disposable incomes are increasingly inclined to purchase higher

priced products, particularly in the areas of infant formula and

nutritional products.

|

|

·

|

Align

sourcing, production and distribution by region. We believe

that we can increase our efficiency and decrease our costs if our products

are produced from local sources and sold in local markets. We plan

to select strategic locations for our company-owned collection stations

and production facilities that will enhance this efficiency.

|

|

|

·

|

Maintaining

quality through world-class production processes. We

believe we can maintain our production of high quality dairy products by

continuing to enter exclusive contracts with dairy farmers who can deliver

quality milk, strengthening our company-owned large-scale dairy farm

operations, expanding our company-owned collection stations and production

facilities, and employing comprehensive testing and quality control

measures.

|

7

Competition

The dairy

industry in China is highly competitive. We face significant

competition from large multinational producers, such as Dumex, Mead Johnson,

Abbott and Wyeth, and large national milk companies, such as Synutra, Yashili

and Yili, particularly in more affluent major urban areas. Many of

our competitors have greater resources and sell more products than we

do. We believe that our competitive position has improved following

the melamine crisis in 2008, which did not involve any of our

products. Our products are positioned as premium products and,

accordingly, are generally priced higher than many similar competitive

products. We believe that the principal competitive factors in

marketing our products are quality, taste, freshness, price and product

recognition. While we believe that we compete favorably in terms of

quality, taste and freshness, our products are more expensive and less well

known than certain other established brands. Our premium products may

also be considered in competition with non-premium quality dairy products for

discretionary food dollars.

Government

Regulation

We are

regulated under national, provincial and local laws in China. The

following information summarizes aspects of those regulations that apply to us

and is qualified in its entirety by reference to all particular statutory or

regulatory provisions. Regulations at the national, provincial and

local levels in China are subject to change. To date, compliance with

governmental regulations has not had a material impact on our level of capital

expenditures, earnings or competitive position, but, because of the evolving

nature of such regulations, we are unable to predict the impact such regulations

may have in the foreseeable future.

As a

producer and distributor of nutritional products, and particularly dairy-based

food products in China, we are subject to the regulations of China’s

Agricultural Ministry. This regulatory scheme governs the manufacture

(including composition and ingredients), labeling, packaging and safety of

food. Specific PRC laws and regulations we face include:

|

·

|

the

PRC Product Quality Law;

|

|

·

|

the

PRC Food Hygiene Law;

|

|

·

|

the

Access Conditions for Dairy Products Processing

Industry;

|

|

·

|

the

Implementation Rules on the Administration and Supervision of Quality and

Safety in Food Producing and Processing

enterprises;

|

|

·

|

the

Regulation on the Administration of Production Licenses for Industrial

Products;

|

|

·

|

the

General Measure on Food Quality Safety Market Access

Examination;

|

|

·

|

the

General Standards for the Labeling of Prepackaged

foods;

|

|

·

|

the

Implementation Measures on Examination of Dairy Product Production

Permits;

|

|

·

|

the

Standardization Law;

|

|

·

|

the

Raw Milk Collection Standard;

|

|

·

|

the

Whole Milk Powder, Skimmed Milk Powder, Sweetened Whole Milk Powder and

Flavored Milk Powder Standards; and

|

|

·

|

the

General Technical Requirements for Infant Formula Powder and Supplementary

Cereal for Infants and Children.

|

8

We and

our products are also subject to provincial and local regulations through such

measures as the licensing of dairy manufacturing facilities, enforcement of

standards for our products, inspection of our facilities and regulation of our

trade practices in connection with the sale of dairy products.

In March

2008, the PRC National Development and Reform Commission, or the NDRC,

promulgated the Access Conditions for Dairy Products Processing Industry, or the

Access Conditions. The Access Conditions set forth the conditions an

entity must satisfy in order to engage, or continue to engage, in the dairy

products processing business in China, including technique and equipment,

product quality, energy and water consumption, sanitation and environmental

protection, as well as production safety. Any new or continuing dairy

products processing projects or enterprises will be required to meet all the

conditions and requirements set forth in the Access Conditions. For

projects or enterprises that already commenced operations before the

promulgation of the Access Conditions, improvements or rectification actions may

need to be taken in order to have such projects or enterprises meet the

conditions within two years of the effective date of the Access Conditions on

April 1, 2010.

The

Access Conditions also set forth requirements relating to the location,

processing capacity and raw milk source for any new or continuing dairy products

processing project or enterprise. Any new or continuing dairy

processing projects or enterprises that fail to meet the requirements will not

be able to procure land, license, permits, loan facilities and electricity

necessary for the processing of dairy products, and those projects or

enterprises already in operation before the promulgation of the Access

Conditions will be deregistered and ordered to shut down if they fail to meet

the conditions within a two-year rectification period.

In May

2008, the NDRC issued the Dairy Industry Policies, or the

Policies. According to the PRC government, the Policies are the first

set of comprehensive government policies on the dairy industry in China,

covering a broad range of matters such as industry planning, closure of

inefficient capacity, milk supply, quality control and product safety,

environmental protection and promotion of milk consumption. Moreover,

the Policies provide conditions that new entrants to the dairy industry must

meet in addition to the conditions set forth in the Access

Conditions.

As a

result of the melamine crisis, PRC governmental authorities have conducted

several dairy industry inspections. In addition to the initial 22

companies implicated in the melamine crisis, these subsequent government

inspections have identified other companies with unacceptable contaminants in

dairy products. The melamine crisis did not involve any of our

products, and we have passed all of these government inspections. In

addition, we are working with the PRC government and attended several emergency

meetings to discuss ways to improve the dairy and overall food industry in

China.

Environmental

Matters

Our

manufacturing facilities are subject to various pollution control regulations

with respect to noise, water and air pollution and the disposal of waste and

hazardous materials. We are also subject to periodic inspections by

local environmental protection authorities. Our operating

subsidiaries have received certifications from the relevant PRC government

agencies in charge of environmental protection indicating that their business

operations are in material compliance with the relevant PRC environmental laws

and regulations. We are not currently subject to any pending actions

alleging any violations of applicable PRC environmental laws.

Employees

As of

March 10, 2010, we had approximately 3,411 employees on our

payroll. We had eight group administrators, approximately 634

employees were in marketing and sales, approximately 79 employees provided

marketing support, approximately 320 people were working in our Nutrition

Department as consultants and managers, approximately 236 employees were

performing administrative functions, including financing, auditing and human

resources, and approximately 2,134 employees were in production, storage and

distribution. Our employees are not represented by a labor union or

covered by a collective bargaining agreement. We have not experienced

any work stoppages. We believe that our relations with our employees

are good.

9

Financial

Information about Segments and Geographic Areas

Although

we have historically operated and managed our business as a single

reportable segment, in 2008, with the initial operations of our dairy farms, we

have two reportable segments: dairy products and dairy farm. Our

dairy products segment produces and sells dairy products, such as wholesale and

retail milk powders, as well as soybean powder, rice cereal, walnut powder and

walnut oil. Our dairy farm segment operates our two company-owned

dairy farms, Gannon Farms and Kedong Farms, construction of which we completed

in the fourth quarter of 2009. Our dairy farms provide milk to us and

not to external customers. Please see Note 30 to our audited financial

statements included elsewhere in this report for further discussion about

segments. As we primarily generate our revenues from customers in the PRC,

we do not present geographical segments.

Available

Information

Our

website is www.americandairyinc.com. We

provide free access to various reports that we file with, or furnish to, the

U.S. Securities and Exchange Commission, or the SEC, through our website, as

soon as reasonably practicable after they have been filed or

furnished. These reports include, but are not limited to, our annual

reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form

8-K, and any amendments to those reports. Also available on our

website are printable versions of our Code of Business Conduct and Ethics and

charters of our Audit Committee, Compensation Committee, Nominating/Corporate

Governance Committee and other committees of our board of

directors. Information on our website does not constitute part of and

is not incorporated by reference into this Annual Report on Form 10-K or any

other report we file or furnish with the SEC. Our SEC reports can

also be accessed through the SEC’s website at www.sec.gov and may

be read or copied at the SEC’s Public Reference Room located at 100 F Street,

NE, Washington, D.C., 20549. Information regarding the Public

Reference Room may be obtained by calling the SEC at

1-800-SEC-0330.

10

FORWARD-LOOKING

STATEMENTS

The

statements included in this report that are not purely historical are

forward-looking statements within the meaning of Section 21E of the

Exchange Act, and Section 27A of the Securities Act of 1933, as amended, or

the Securities Act. These statements include, but are not limited to, statements

about our plans, objectives, expectations, strategies, intentions or other

characterizations of future events or circumstances and are generally identified

by the words “may,” “expects,” “anticipates,” “intends,” “plans,” “believes,”

“seeks,” “estimates,” “could,” “would,” and similar expressions. Because these

forward-looking statements are subject to a number of risks and uncertainties,

our actual results could differ materially from those expressed or implied by

these forward-looking statements. Factors that could cause or contribute to such

differences include, but are not limited to, those discussed under the heading

“Risk Factors” and in other documents we file from time to time with the

Securities and Exchange Commission. All forward-looking statements included in

this report are based on information available to us on the date hereof. Our

business and the associated risks may have changed since the date this report

was originally filed with the SEC. We assume no obligation to update any such

forward-looking statements.

Item

1A. Risk Factors

Investing

in our common stock involves a high degree of risk. You should carefully

consider the following risk factors and all other information contained in this

prospectus before purchasing our common stock. If any of the following events

were to occur, our business, financial condition or results of operations could

be materially and adversely affected. In these circumstances, the market price

of our common stock could decline, and you could lose some or all of your

investment. Additional risks and uncertainties not currently known to us or that

we currently believe to be immaterial could also materially and adversely affect

our business, financial condition, operating results and/or cash

flow.

Any

negative public perception regarding our products or industry, or any ill

effects or product liability claims, could harm our reputation, damage our

brand, result in costly and damaging recalls, and expose us to government

investigations and sanctions, which would materially and adversely affect our

results of operations.

We sell

products for human consumption, which involves risks such as product

contamination, spoilage and tampering. In 2008, sales in China of substandard

milk formula contaminated with a substance known as melamine caused the death of

six infants as well as illness of nearly 300,000 others. In 2009, new

incidents of substandard milk formula contaminated with melamine also appeared

and again, none of our products were involved. Although our products

were not involved in these incidents, China’s Administration of Quality

Supervision, Inspection and Quarantine found that the products of at least 22

Chinese milk and formula producers were contaminated by melamine, a substance

not approved for use in food, which caused significant negative publicity for

the entire dairy industry in China. The mere publication of

information asserting that our milk powder, infant formula or other products

contain melamine or other contaminants could have a material adverse effect on

us, regardless of whether these reports are scientifically supported or concern

our products or the raw materials used in our products. In addition,

if the consumption of any of our products causes injury, illness or death, we

may face product liability claims, product recalls, temporary or permanent

suspensions of operations, government investigations or sanctions, any of which

could be extremely expensive and damaging to our business.

Prior to

the 2008 melamine crisis, there have also been widely publicized occurrences of

counterfeit, substandard milk products in China. For example, in

April 2004, such sales of counterfeit and substandard infant formula in Anhui

Province, China caused the deaths of 13 infants and harmed many

others. Counterfeiting or imitation of our products may occur in the

future, and we may not be able to detect it and deal with it effectively. Any

occurrence of counterfeiting or imitation could negatively impact our corporate

brand and image or consumers’ perception of our products or similar nutritional

products generally, particularly if the counterfeit or imitation products cause

injury or death to consumers.

11

Our

products may not achieve market acceptance.

We are

currently selling our products principally in northern, central, and eastern

China. Achieving market acceptance for our products, particularly in

new markets, will require substantial marketing efforts and the expenditure of

significant funds. There is substantial risk that any new markets may

not accept or be as receptive to our products. In addition, we intend

to market our products as premium and super-premium products and to adopt a

corresponding pricing model, which may not be accepted in new or existing

markets. Market acceptance of our current and proposed products will

depend, in large part, upon our ability to inform potential customers that the

distinctive characteristics of our products make them superior to competitive

products and justify their pricing. Our current and proposed products

may not be accepted by consumers or able to compete effectively against other

premium or non-premium dairy products. Lack of market acceptance would limit our

revenues and profitability.

Our

planned growth may require more raw milk than is available and could diminish

the quality of our dairy products.

Our

business requires a supply of raw milk. Our growth will be limited if the supply

of raw milk is insufficient to meet demand. Moreover, as we attempt to implement

our growth strategy, it may become difficult to maintain current levels of

quality control. Inadequate quality control could harm our reputation and the

demand for our products, which would also limit our growth. A significant amount

of the raw milk used in our products is supplied to us by numerous local farms

under output contracts. We believe that our farmers can increase their

production of raw milk. We further believe, however, that this supply may not be

sufficient to meet increased demand for our products associated with our

proposed marketing efforts and that such increase may compromise quality. Though

we believe that additional raw milk is available locally, if needed, we may not

be able to enter into arrangements with the producers of such milk on terms

acceptable to us, if at all. Our efforts to source milk through our

company-owned dairy farms are new, may involve unforeseen difficulties, and may

not supply the quantity of raw milk we need to maintain and expand our levels of

production. An inadequate supply of raw milk, coupled with concern over quality

control, could increase costs for raw milk or decrease the sales price for our

products, which could limit our ability to grow, cause our earnings to decline

and make our business less profitable.

The

recent global economic and financial market crisis could significantly impact

our financial condition.

Current

global economic conditions could have a negative effect on our business and

results of operations. Economic activity in China, the United States and

throughout much of the world has undergone a sudden, sharp economic downturn

following the recent housing crisis in the real estate and credit markets in

both the United States and Europe. Market disruptions have included

extreme volatility in securities prices, as well as severely diminished

liquidity and credit availability. The economic crisis may adversely

affect us in a variety of ways. Access to lines of credit or the capital markets

may be severely restricted, which may preclude us from raising funds required

for operations and to fund continued expansion. It may be more

difficult for us to complete strategic transactions with third parties. The

financial and credit market turmoil could also negatively impact our suppliers

and customers, which could decrease our ability to source, produce and

distribute our products and could decrease demand for our products. While it is

not possible to predict with certainty the duration or severity of the current

disruption in financial and credit markets, if economic conditions continue to

worsen, it is possible these factors could significantly impact our financial

condition.

Our

results of operations may be affected by fluctuations in availability and price

of raw materials.

The raw

materials we use are subject to price fluctuations due to various factors beyond

our control, including, among other pertinent factors:

|

·

|

increasing

market demand;

|

12

|

·

|

inflation;

|

|

·

|

severe

climatic and environmental

conditions;

|

|

·

|

seasonal

factors, with dairy cows generally producing more milk in temperate

weather as opposed to cold or hot weather and extended unseasonably cold

or hot weather potentially leading to lower than expected

production;

|

|

·

|

commodity

price fluctuations;

|

|

·

|

currency

fluctuations; and

|

|

·

|

changes

in governmental and agricultural regulations and

programs.

|

For

example, our raw milk cost increased by approximately 45% in 2008 due to various

factors, including, we believe, general economic conditions, such as inflation

and fuel prices, and rising production costs and decreased by approximately

20% in 2009 due to various other factors, including increased competition abroad

and currency appreciation. We also expect that our raw material prices

will continue to fluctuate and be affected by all of these factors in the

future. Changes to our raw materials prices may result in increases

in production and packaging costs, and we may be unable to raise the prices of

our products to offset such increases in the short term or at all. As a result,

our results of operations may be materially and adversely affected.

We

are subject to public company reporting and other requirements for which we will

incur substantial costs and our accounting and other management systems and

resources may not be adequately prepared.

We incur

significant legal, accounting, insurance and other expenses as a result of being

a public company. For example, laws and regulations affecting public

companies, including the provisions of the Sarbanes-Oxley Act of 2002, or SOX,

and rules related to corporate governance and other matters subsequently adopted

by the SEC and the NYSE, result in substantial costs to us, including legal and

accounting costs, and may divert our management’s attention from other matters

that are important to our business. Compliance with Section 404 of

SOX requires that our management annually assess the effectiveness of our

internal control over financial reporting and that our independent auditors

report on management’s assessment. During our review of our financial

statements and results for the year ended December 31, 2008, our management

identified several internal control matters that constituted material weaknesses

and significant deficiencies and, consequently, concluded that our internal

control over financial reporting was not effective at December 31,

2008. In addition, management concluded, based primarily on the

identification of the material weaknesses and significant deficiencies, that our

disclosure controls and procedures were not effective at December 31,

2008. Since the end of 2008, we implemented remedial measures

described below under “Management’s Report on Internal

Control Over Financial Reporting—Changes in Internal

Controls,” including hiring additional accounting, internal audit and

finance staff, engaging consultants to assist with these functions, upgrading

our systems, and implementing additional financial and management controls and

reporting systems and procedures, as well as improving certain processes

surrounding our Audit Committee activities. These measures have cost

us an aggregate of approximately $1.0 million to date. Although

management has concluded the measures have partially remediated many of our

historical material weaknesses, as of December 31, 2009 our management concluded

we had a material weakness relating to the accounting and treatment of routine

and non-routine transactions: we did not effectively and timely

assess the accounting treatment for certain transactions, including sales,

purchases, government subsidy income, and operating expenses. The measures we

take to remediate material weaknesses may not ensure the adequacy of our

internal controls over our financial processes and reporting in the

future.

13

A control

system, no matter how well conceived and operated, can provide only reasonable,

not absolute, assurance that the objectives of the control system are met.

Because of the inherent limitations in all control systems, no evaluation of

controls can provide absolute assurance that all control issues and instances of

fraud, if any, within our company have been detected.

We

significantly depend on our management team.

Each of

our executive officers is responsible for an important aspect of our

operations. In addition, we rely on management and senior personnel

to ensure that our sourcing, production, sales, distribution and other business

functions are effective. Losing the services of our executive

officers or key personnel could be detrimental to our operations. We

do not have key-man life insurance for any of our executive officers or other

employees.

Investors

may not be able to enforce judgments entered by United States courts against

certain of our officers and directors.

We are

incorporated in the State of Utah. However, a majority of our

directors and executive officers, and certain of our principal shareholders,

live outside of the U.S., principally in China. As a result, you may not be able

to effect service of process upon those persons within the U.S. or enforce

against those persons judgments obtained in U.S. courts.

We

face substantial competition in connection with the marketing and sale of our

products.

Our

products compete with other premium quality dairy brands as well as less

expensive, non-premium brands. Our products face competition from non-premium

producers distributing in our marketing area and other producers packaging their

products in our marketing area. Many of our competitors are well established,

have greater financial, marketing, personnel and other resources, have more

established distribution channels into major markets, and have products that

have gained wide customer acceptance in the marketplace. Our largest competitors

are multi-national dairy companies owned by the government of China. The greater

financial resources of such competitors will permit them to procure retail store

shelf space and to implement extensive marketing and promotional programs, both

generally and in direct response to advertising efforts by us. The dairy

industry in China is also characterized by the frequent introduction of new

products, accompanied by substantial promotional campaigns, such as large

discounts to distributors. In addition, distributors in China often engage in

cross-territory selling activities, which involves their diversion of products

into different geographic regions, which can disrupt the price of our products

and adversely impact our revenues. We may be unable to compete

successfully with our competitors in some or all of our markets, and our

competitors may develop products which have superior qualities or gain wider

market acceptance than ours.

We

expect to incur costs related to potential acquisitions and expansion into new

plants and ventures, which may not prove to be profitable. Moreover, any delays

in our expansion plans could cause our profits to decline and jeopardize our

business.

We

anticipate that any proposed expansion of our milk production facilities may

include the acquisition and construction of new or additional facilities. Our

cost estimates and projected completion dates for construction of new production

facilities may change significantly as the projects progress. In

addition, projects could entail significant construction risks,

including shortages of materials or skilled labor, unforeseen environmental or

engineering problems, weather interferences and unanticipated cost increases,

any of which could have a material adverse effect on the projects and could

delay their scheduled openings. A delay in scheduled openings of production

facilities could delay our receipt of sales revenues from such facilities,

which, when coupled with the increased costs and expenses of our expansion,

could cause a decline in our profits.

Our plans

to finance, develop, and expand our production facilities could be subject to

the many risks inherent in the rapid expansion of a high growth business

enterprise, including unanticipated design, construction, regulatory and

operating problems, and the significant risks commonly associated with

implementing a marketing strategy in changing and expanding markets. These

projects may not become operational within their estimated time frames and

budgets as projected at the time we enter into a particular agreement, or at

all. In addition, we may develop projects as joint ventures in an effort to

reduce our financial commitment to individual projects. The significant

expenditures required to expand our production plants may not ultimately result

in increased profits.

14

When our

future expansion projects become operational, we will be required to add and

train personnel, expand our management information systems and control expenses.

If we do not successfully address our increased management needs or are

otherwise unable to manage our growth effectively, our operating results could

be materially and adversely affected.

We

face the potential risk of product liability associated with food

products.

We face

the risk of liability in connection with the sale and consumption of dairy

products and other products should the consumption of such products cause

injury, illness or death. Such risks may be particularly great in a company

undergoing rapid and significant growth. The successful assertion of product

liability claims against us could result in potentially significant monetary

damages, divert management resources and require us to make significant payments

and incur substantial legal expenses. We do not currently maintain product

liability insurance. Any insurance that we may obtain in the future may be

insufficient to cover potential claims or the level of insurance coverage needed

may be unavailable at a reasonable cost. Even if a product liability claim is

not successfully pursued to judgment by a claimant, we may still incur

substantial legal expenses defending against such a claim and our brand image

and reputation would suffer. Finally, serious product quality concerns could

result in governmental action against us, which, among other things, could

result in mandatory recalls of our products, the suspension of production or

distribution of our products, loss of certain licenses, or other governmental

penalties, including possible criminal liability.

Doing

business in China involves various political and economic risks.

We

conduct substantially all of our operations and generate most of our revenue in

China. Accordingly, our business, financial condition, results of operations and

prospects are affected significantly by economic, political and legal

developments in China. China’s economy differs from the economies of most

developed countries in many respects, including:

|

·

|

the

higher level of government involvement and

regulation;

|

|

·

|

the

early stage of development of the market-oriented sector of the

economy;

|

|

·

|

the

rapid growth rate;

|

|

·

|

the

higher level of control over foreign exchange;

and

|

|

·

|

government

control over the allocation of many

resources.

|

As

China’s economy has been transitioning from a planned economy to a more

market-oriented economy, the government of China has implemented various

measures to encourage economic growth and guide the allocation of resources.

While these measures may benefit the overall economy of China, they may also

have a negative effect on us.

Although

the government of China has in recent years implemented measures emphasizing the

utilization of market forces for economic reform, the PRC government continues

to exercise significant control over economic growth in China through the

allocation of resources, controlling payment of foreign currency-denominated

obligations, setting monetary policy and imposing policies that impact

particular industries or companies in different ways. Any adverse

change in the economic conditions or government conditions or government

policies in China could have a material adverse effect on the overall economic

growth and the level of consumer spending in China, which in turn could lead to

a reduction in demand for our products and consequently have a material adverse

effect on our business and prospects.

15

Extensive

regulation of the food processing and distribution industry in China could

increase our expenses resulting in reduced profits.

We are

subject to extensive regulation by China’s Agricultural Ministry, and by other

provincial and local authorities in jurisdictions in which our products are

processed or sold, regarding the processing, packaging, storage, distribution

and labeling of our products. For instance, in June 2009, regulatory

requirements became effective in China requiring new package labeling for dairy

products, which we believe impacted our sales cycles during the three months

ended June 30, 2009. Additional labeling requirements are scheduled

to become effective on June 10, 2010 for all dairy products, which could have an

adverse impact on our sales, inventory levels, or packing and

distribution.

Other

applicable laws and regulations governing our products may include nutritional

labeling and serving size requirements. Our processing facilities and products

are subject to periodic inspection by national, provincial and local

authorities. We believe that we are currently in substantial compliance with all

material governmental laws and regulations and maintain all material permits and

licenses relating to our operations. Nevertheless, we may fall out of

substantial compliance with current laws and regulations or may be unable to

comply with any future laws and regulations. To the extent that new regulations

are adopted, we will be required, possibly at considerable expense, to adjust

our activities in order to comply with such regulations. Our failure to comply

with applicable laws and regulations could subject us to civil remedies,

including fines, injunctions, recalls or seizures, as well as potential criminal

sanctions, which could have a material adverse effect on our business,

operations and finances.

Regulations

affecting acquisitions of PRC companies by foreign entities may make it more

difficult for us to complete acquisitions and grow our business.

In 2005,

the PRC State Administration of Foreign Exchange, or SAFE, issued a public

notice, known as “Circular 75,” concerning the application of foreign exchange

regulations to mergers and acquisitions involving foreign investment in

China. Among other things, the public notice provides that if an

offshore company controlled by PRC residents intends to acquire a PRC company,

such acquisition will be subject to strict examination by the relevant foreign

exchange authorities. Under Circular 75, if an acquisition of a PRC

company by an offshore company controlled by PRC residents occurred prior to the

issuance of Circular 75, certain PRC residents were required to submit a

registration form to the local SAFE branch to register their ownership interests

in the offshore company before March 31, 2006. Such PRC

residents must also amend the registration form if there is a material event

affecting the offshore company, such as, among other things, a change of the

company’s share capital, a transfer of shares, or if the company is involved in

a merger, an acquisition or a spin-off transaction or uses its assets in China

to guarantee offshore obligations. In the past, we have acquired a

number of assets from, or equity interests in, PRC companies.

There is

still significant uncertainty in China regarding the interpretation and

implementation of Circular 75. Nevertheless, we have requested that

our shareholders who are PRC residents make the necessary applications, filings

and amendments that required under Circular 75 and related

regulations. However, all of our PRC-resident shareholders may not comply with

such requirements. We also cannot predict how these regulations will

affect our future acquisition strategy and business operations. For example, if

we decide to acquire additional PRC companies, we or the owners of such

companies may not be able to complete the filings and registrations, if any,

required by the SAFE notices. Failure to complete Circular 75 registrations may

limit the ability of our PRC subsidiaries to issue dividends to us, limit our

ability to inject additional capital into our subsidiaries, restrict our ability

to implement our acquisition strategy and adversely affect our business and

prospects.

In

addition, in 2006 six PRC regulatory authorities, including the PRC Ministry of

Commerce and the PRC Securities Regulatory Commission, jointly promulgated a

rule entitled “Provisions regarding Mergers and Acquisitions of Domestic

Enterprises by Foreign Investors,” or the New M&A Rules, in

September 2006. The New M&A Rules establish additional procedures and

requirements that could make merger and acquisition activities by foreign

investors more time-consuming and complex, including, in some circumstances,

advance notice to the Ministry of Commerce of any change-of-control transaction

in which a foreign investor takes control of a PRC domestic enterprise.

Compliance with the New M&A Rules, and any related approval processes,

including obtaining approval from the Ministry of Commerce, may delay or inhibit

our ability to complete such transactions, which could affect our ability to

expand our business or maintain our market share.

16

Furthermore,

in August 2008, SAFE issued a notice, known as “Circular 142,” regulating the

conversion by a foreign-invested company of foreign currency into PRC currency,

the Reminbi or RMB, by restricting the uses for the converted RMB. Circular 142

requires that the registered capital of a foreign-invested company denominated

in RMB but converted from a foreign currency may only be used pursuant to the

purposes set forth in the foreign-invested company’s business scope as approved

by the applicable governmental authority. Such registered capital may not be

used for equity investments within the PRC. In addition, SAFE strengthened its

oversight of the flow and use of the registered capital of a foreign-invested

company that was denominated in RMB but converted from foreign currency.

Violations of Circular 142 may result in severe penalties, including significant

fines. As a result, Circular 142 may significantly limit our ability to invest

in or acquire other PRC companies using the RMB-denominated capital of our PRC

subsidiaries.

The

PRC government’s recent measures to curb inflation rates could adversely affect

future results of operations.

China has

faced rising inflation in recent years. The government of China undertook

various measures to alleviate the effects of inflation, especially with respect

to key commodities. In January 2008, the PRC National Development and Reform

Commission announced national price controls on various products, including

milk. Similarly, the government of China may conclude that the prices of infant

formula or other of our products are too high and may institute price controls

that would limit our ability to set prices for our products as we might wish.

The government of China has also encouraged local governments to institute price

controls on similar products. Such price controls could adversely affect our

future results of operations and, accordingly, the price of our common

stock.

The

PRC currency is not a freely convertible currency, which could limit our ability

to obtain sufficient foreign currency to support our business operations in the

future.

The PRC

currency is not a freely convertible currency. We rely on the PRC government’s

foreign currency conversion policies, which may change at any time, in regard to

our currency exchange needs. We receive substantially all of our revenues in

Renminbi, which is not freely convertible into other foreign currencies. In

China, the government has control over Renminbi reserves through, among other

things, direct regulation of the conversion of Renminbi into other foreign

currencies and restrictions on foreign imports. Although foreign currencies that

are required for current account transactions can be bought freely at authorized

PRC banks, the proper procedural requirements prescribed by PRC law must be met.

At the same time, PRC companies are also required to sell their foreign exchange

earnings to authorized PRC banks and the purchase of foreign currencies for

capital account transactions still requires prior approval of the PRC

government. This substantial regulation by the PRC government of foreign

currency exchange may restrict our business operations and a change in any of

these government policies could negatively impact our operations, which could

result in a loss of profits.

In order

for our China subsidiaries to pay dividends to us, a conversion of Renminbi into