Attached files

| file | filename |

|---|---|

| EX-31.01 - EXHIBIT 31.01 - Double-Take Software, Inc. | ex31-01.htm |

| EX-32.01 - EXHIBIT 32.01 - Double-Take Software, Inc. | ex32-01.htm |

| EX-31.01 - EXHIBIT 31.02 - Double-Take Software, Inc. | ex31-02.htm |

| EX-21.01 - EXHIBIT 21.01 - Double-Take Software, Inc. | ex21-01.htm |

| EX-23.01 - EXHIBIT 23.01 - Double-Take Software, Inc. | ex23-01.htm |

| EX-10.46 - EXHIBIT 10.46 - Double-Take Software, Inc. | ex10-46.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

ANNUAL REPORT

PURSUANT TO SECTIONS 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

|

(Mark One)

|

||

|

þ

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

|

For the fiscal year ended December 31, 2009

|

||

|

OR

|

||

|

o

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

|

For the transition period from to

|

||

Commission file number: 001-33184

Double-Take Software, Inc.

(Exact name of registrant as specified in its charter)

|

Delaware

|

20-0230046

|

|

|

(State or other jurisdiction of

|

(I.R.S. Employer

|

|

|

Incorporation or organization)

|

Identification No.)

|

|

|

257 Turnpike Road, Suite 210

|

01772

|

|

|

Southborough, Massachusetts

|

(Zip Code)

|

|

|

(Address of principal executive offices)

|

(877) 335-5674

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

Title of Each Class

|

Name of Each Exchange on Which Registered

|

|

|

Common Stock, $0.001 par value

|

The NASDAQ Stock Exchange

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES o NO þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES o NO þ

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES þ NO o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES o NO o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer o

|

Accelerated filer þ

|

Non-accelerated filer o

(Do not check if a smaller reporting company)

|

Smaller reporting Company o

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) YES o NO þ

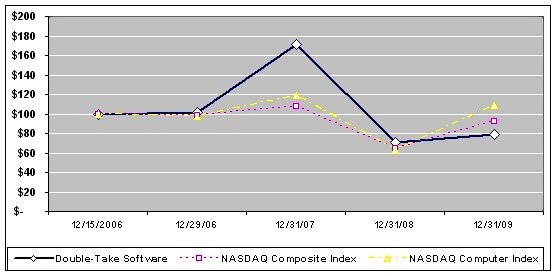

As of June 30, 2009, the last business day of the Registrant’s most recently completed second fiscal quarter, the aggregate market value of the Registrant’s Common Stock held by nonaffiliates was approximately $190.8 million.

The number of shares of Registrant’s Common Stock outstanding as of February 26, 2010 was 21,493,422.

DOCUMENTS INCORPORATED BY REFERENCE

Part III of this Form 10-K incorporates by reference certain portions of the Registrant’s proxy statement for its 2010 Annual Meeting of Shareholders to be filed with the Commission not later than 120 days after the end of the fiscal year covered by this report.

Statements contained in this Form 10-K that are not historical facts may be forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934 (the “Exchange Act”). We intend such forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in Section 21E of the Exchange Act. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date this Form 10-K is filed with the Securities and Exchange Commission (“SEC”).

We may, in some cases, use words such as “project,” “believe,” “anticipate,” “plan,” “expect,” “estimate,” “intend,” “should,” “would,” “could,” “potentially,” “will,” or “may,” or other words that convey uncertainty of future events or outcomes to identify these forward-looking statements. Forward-looking statements in this annual report include statements about:

|

•

|

competition and competitive factors in the markets in which we operate;

|

|

|

•

|

the impact of macro-economic trends on our business;

|

|

|

•

|

demand for our software;

|

|

|

•

|

our ability to transition to a broader focus on software to move, protect and recover workloads;

|

|

|

•

|

the advantages of our technology as compared to others;

|

|

|

•

|

changes in customer preferences and our ability to adapt our product and services offerings;

|

|

|

•

|

our ability to obtain and maintain distribution partners and the terms of these arrangements;

|

|

|

•

|

our plans for future product development;

|

|

|

•

|

the integration of emBoot, Inc. (“emBoot”) and its products into our business;

|

|

|

•

|

our ability to develop and maintain positive relationships with our customers;

|

|

|

•

|

our ability to maintain and establish intellectual property rights;

|

|

|

•

|

our ability to retain and hire necessary employees and appropriately staff our development, marketing, sales and distribution efforts;

|

|

|

•

|

our ability to scale our support efforts;

|

|

|

•

|

our cash needs and expectations regarding cash flow from operations;

|

|

|

•

|

our ability to manage and grow our business and execution of our business strategy;

|

|

|

•

|

our expectations for future revenue; and

|

|

|

•

|

our financial performance.

|

|

The forward-looking statements are based on our beliefs, assumptions and expectations of our future performance, taking into account all information currently available to us. These beliefs, assumptions and expectations can change as a result of many possible events or factors, not all of which are known to us or are within our control. If a change occurs, our business, financial condition and results of operations may vary materially from those expressed in our forward-looking statements. There are a number of important factors that could cause actual results to differ materially from the results anticipated by these forward-looking statements. These important factors include those that we discuss in “Risk Factors,” Management’s Discussion and Analysis of Financial Condition and Results of Operations,” Business and elsewhere in this annual report. You should read these factors and the other cautionary statements made in this annual report as being applicable to all related forward-looking statements wherever they appear in this annual report. If one or more of these factors materialize, or if any underlying assumptions prove incorrect, our actual results, performance or achievements may vary materially from any future results, performance or achievements expressed or implied by these forward-looking statements. We undertake no obligation to publicly update any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

PART I

|

Business.

|

Overview

Double-Take Software develops, sells and supports affordable software that allows IT organizations of all sizes to move, manage, protect and recover workloads across any distance and any combination of physical and virtual server environments. As enterprise IT systems evolve the ability to manage information freely, intelligently and securely becomes critical. Our hardware- and application-independent software benefits these infrastructures by efficiently protecting, moving and recovering data created by any application on almost any type or brand of disk storage on any brand of server running on Microsoft Windows operating systems as well many versions of the Linux operating system. Our newly released Double-Take Cloud product extends these benefits to a broader range of customers by allowing them to provision off-site disaster recovery resources easily in a cost-effective manner. In addition our Double-Take Flex technology offers an alternative to Virtual Desktop Infrastructure, making desktop administration and provisioning easy, and reducing drastically the desktop total cost of ownership. Double-Take Flex enables multiple desktops to run from a centralized shared image stored on any iSCSI storage.

We believe that we are the leading supplier of replication software for Microsoft server environments and that our business is distinguished by our focus on software license and recurring maintenance sales, our productive distribution network and our efficient services infrastructure.

Our success has been driven in large part by our flagship “Double-Take” software technology, which was first released in 1995 and has been enhanced by years of customer feedback and is now called Double-Take Availability. Double-Take Availability, among other things, continuously replicates software and data changes made on a primary operating server to a duplicate server at a different location. Because the duplicate server can commence operating in place of the primary server at almost any time, Double-Take Availability facilitates rapid failover and application recovery in the event of a disaster or other service interruption. During 2009, in addition to Double-Take Availability, we integrated our software offerings under the Double-Take brand by releasing Double-Take Backup, which includes the TimeData, Livewire and Cargo products, Double-Take Flex, which includes the emBoot products and enables multiple desktops to run from a centralized shared image stored on any iSCSI storage, and Double-Take Move, which includes our migration product.

The disaster recovery market has been our primary historical focus, but as a result of acquisitions and internal development, we are expanding into adjacent markets for system migrations, back-up and network booting. With our acquisition of TimeSpring Software Corporation in December 2007, now known as Double-Take Canada, and its TimeData products, now included in Double-Take Backup, we can also recover data from almost any point in time from a repository located on- or off-site. In July 2008, we acquired emBoot, Inc. which is now a part of Double-Take Canada, and which specializes in network booting technology. The technology acquired with emBoot, now included in Double-Take Flex, allows organizations to easily assign and re-assign computing workloads to any available Windows or Linux physical servers or desktops or any virtual machine in their environment. IT organizations can now move those workloads around in a matter of minutes, whether because a disaster has occurred, a data center is moving, the company has decided to virtualize its infrastructure or an application needs more capacity. Double-Take Move, released in April 2009, is a server migration product that can migrate live server workloads across physical and virtual platforms.

We sell our software through multiple channels, including a global distribution network that is supported by an experienced direct sales force. Our distribution partners include leading server manufacturers, such as Dell Computer Corporation and Hewlett-Packard Company, leading distributors, such as Bell Microproducts Inc. and Tech Data Corporation, and over 900 value-added resellers that we believe are generally well-connected with small- and medium-sized enterprises. Our direct sales force augments the revenue generated by our distribution partners and actively supports them in their third-party sales efforts. We have also begun to make some of our products available via on-line purchase, including Double-Take Move and Double-Take Cloud.

Our broad distribution network, coupled with affordable price points, feature-rich proven software, modest implementation costs and dependable support, makes our software accessible and scalable from small enterprises of 20 people to Fortune 500 companies. As of December 31, 2009, our customer base of about 22,000 organizations includes a large number of law firms, financial institutions, hospitals, school districts and government entities. We believe that we have a highly satisfied customer base. Many of our customers provide references that help us to generate new sales opportunities and to shorten sales cycles. Our sales personnel often enlist the assistance of satisfied customers to recommend our software to potential customers in similar industries or that have similar applications or server configurations. The breadth and diversity of our customers frequently allows us to refer to a similar configuration when making a new sale. The satisfaction of our customer base also contributes to reduced support costs.

We expect that future growth in our market will be driven by a number of factors, including the following:

|

•

|

an increased focus on protecting a growing number of business-critical applications, such as email applications, particularly in service-oriented industries;

|

|

|

•

|

a heightened awareness of the potential for natural and man-made disasters;

|

|

|

•

|

a need to move information rapidly within an IT infrastructure for efficiency, virtualization, data center changes, hardware and software upgrades;

|

|

|

•

|

the rapid growth in digital data, driven by increased usage of automated systems;

|

|

|

•

|

the increased acceptance of and reliance on cloud computing for reducing the cost and complexity of managing IT systems;

|

|

|

•

|

government and industry regulations, such as the Health Insurance Portability and Accountability Act of 1996 and the Sarbanes-Oxley Act of 2002, which require data protection and recovery; and

|

|

|

•

|

general improvement of global economic conditions and related increases in information technology spending.

|

|

The matters discussed in this “Business” section should be read in conjunction with the Consolidated Financial Statements found under Item 8 of Part II of this annual report, which include additional financial information about our total assets, revenue and measures of profits and loss and financial information about geographic areas.

Organization; Principal Executive Offices

We were organized as a New Jersey corporation in 1991, and we reincorporated in Delaware in 2003. In July 2006 we changed our name to Double-Take Software, Inc. from NSI Software, Inc. Our principal executive offices are located at 257 Turnpike Road, Suite 210, Southborough, Massachusetts 01772, and our main telephone number at that address is (877) 335-5674. We maintain our general corporate website at www.doubletake.com. The contents of our website, however, are not a part of this annual report.

Our Strategy

Our goal is to provide affordable software that will enable our customers to move, manage, protect and recover workloads across any distance and any combination of physical and virtual server environments. We are also continuing to build on our historical goal of reducing our customers’ downtime for business-critical systems to as close to zero as possible and offering effective protection and recovery for less critical systems. We are pursuing the following key initiatives:

|

•

|

Continue to Innovate. We plan to continue to focus on enhancing our existing software and to develop new, innovative software, in line with our shift from our historical offerings of products focused on the disaster recovery market to our current offerings of products that help customers protect, recover, move their business critical workloads, and provision desktops. For example, in 2007 we introduced new software products and features that protect the full system state of a server, including operating system and application configuration, in 2008 we introduced new software products to provision virtual machines and in 2010 we introduced Double-Take Cloud which is a real-time recovery platform. We believe that software innovations will also help us to expand our addressable market, and we have software in the development pipeline that we expect will help us to scale up to serve larger entities and to scale down to serve even smaller enterprises.

|

|

|

•

|

Expand our Customer Base within our Current Markets. We plan to gain additional customers in the markets we currently serve by expanding our distribution network to reach more customers and by leveraging our existing customer base. We believe our customers are very satisfied and will continue to provide references across multiple industries, multiple configurations and multiple applications. In addition, we plan to continue to offer enhancements to our current software to broaden its appeal. For example, our Double-Take Cloud product (launched in February 2010), provides cost-effective off-site protection and recovery for customers who in the past may not have been able to afford a disaster recovery solution.

|

|

•

|

Cross-sell Existing and New Software to our Customer Base. We plan to sell software for additional applications to our current customers and believe that many of our existing customers will acquire more licenses to the software that they are already using. We also believe that a large number of our customers will renew maintenance in the future because of their need for product upgrades and customer support. We plan to offer new software that complements our existing software and applications and achieves additional customer objectives. We expect that our new offerings will be developed internally, or we may in some instances hire third-party developers to develop software on our behalf or acquire new offerings through strategic transactions. For example, in December 2007 we acquired Montreal-based TimeSpring Software, and in July of 2008 we acquired Toronto based emBoot, now both known as Double-Take Software Canada. Through these acquisitions we obtained elements of our Double-Take Backup and our Double-Take Flex product offerings.

|

|

•

|

Enter New Markets. We plan to enter into new markets and grow our presence in markets where we currently have a small presence. We expect to do this through expansion of our channel by creating or expanding relationships with partners that serve different markets. We also plan to continue to grow our presence in the larger enterprise market by leveraging our supportive customer base. We believe that small- and medium-sized enterprises frequently lead in the adoption of cost effective technology solutions out of necessity and that large institutions follow by replacing more expensive solutions with cost effective solutions. We have seen organizations in the larger enterprise market adopt our software, and we expect this trend to continue. We have developed and acquired new products that we believe will allow us to enter new markets. For example, Double-Take Backup, which includes the combination of our Livewire product (released in late 2008), our Timedata product and our Cargo tiered recovery product, allows us to compete more effectively in the backup market.

|

|

|

•

|

Expand Globally. We believe that the market potential outside the United States is at least as large as the market within and offers us significant growth potential. We plan to extend our global reach though the expansion of our direct and channel sales efforts and through strategic acquisitions. For example, in May 2006 we acquired our main European distributor, now known as Double-Take Software S.A.S., or Double-Take EMEA, with offices in France, the United Kingdom and Germany. We also work closely with Hewlett-Packard, which has a strong international presence and is our largest OEM, and we plan to continue our increased focus and sales support on international sales. In August 2006, we established a full time presence in Asia and now have a presence in Singapore and China, including Hong Kong and Shanghai. Additionally, we opened an office in Dubai, United Arab Emirates in the fourth quarter of 2008.

|

|

|

•

|

Expand our Distribution Capabilities. We will make our products easier to buy and more accessible to both our end users and trusted partners. This will allow us to expand the reach of our sales force in a cost-effective way. For example, our Double-Take Move product (released in March 2009), and our Double-Take Cloud product (released in February 2010) are both available for on-line purchase.

|

|

Our Software and Services

In 2008 and 2009, all of our software revenue came from sales of our software applications, compared to 98% of our total software revenue in 2007. Similarly, we derive substantially all of our maintenance and professional services revenue from associated maintenance and customer support of our applications. During 2009, in addition to Double-Take Availability, we integrated our software offerings under the Double-Take brand by releasing Double-Take Backup which includes the TimeData, Livewire and Cargo products, Double-Take Flex, which includes the emBoot products and enables multiple desktops to run from a centralized shared image stored on any iSCSI storage, and Double-Take Move, which includes our migration product.

Our product offerings are:

Double-Take Availability. Our flagship software provides continuous protection of data to reduce or eliminate data loss, as well as the ability to recover rapidly the application and server needed to utilize that data through automatic or manually initiated failover. This combination of data protection with high availability failover provides significantly higher levels of availability than solutions that address only data protection or that provide local failover clustering but that do not provide data redundancy or protection across multiple locations.

Double-Take Availability is easily installed on each protected “source” server as well as on each “target” server that will store copies of the protected data and be prepared to take over for the protected server and its applications. This software-based approach provides several important features and benefits:

|

•

|

Real-time Byte Level Change Capture. Our file system filtering technology monitors all file input and output (I/O) to files selected for protection and captures changes as they occur, without the overhead of additional disk reads to compare file content. This approach captures only the bytes written to the file system, rather than full files or disk blocks, and allows Double-Take Availability to replicate any application data, including open files such as databases, messaging systems or other transactional applications. As a result, data can be protected continuously with very little system impact or overhead.

|

|

|

•

|

Storage Architecture Independence. Double-Take Availability can replicate to or from almost any storage type supported by the host operating system. Not only can replication occur between storage types such as Fibre Channel or iSCSI Storage Area Networks and directly attached disks, but source and target disks that have completely different geometries or multiple source volumes can be consolidated onto a single large capacity target volume. As a result, customers can use their existing storage systems and even replicate between storage systems of different types. Only solutions that run along with the applications and replicate logical file system structures can provide this level of flexibility and performance.

|

|

|

•

|

Integrated Application and Server Availability. Software replicating between servers can easily monitor and failover other functions such as server name, IP addresses or integrated applications between servers. As a result, not only is data protected, but the operating system and applications that use that data to provide services to users can be replicated and activated quickly and automatically, even on different hardware or virtual servers. Double-Take provides application managers for a variety of the business-critical applications that companies rely on to run their businesses.

|

|

|

•

|

Standards-Based IP Networking Support. Double-Take Availability utilizes standard IP networking for data replication, monitoring and failover, allowing data to be protected and servers to be managed remotely over great distances. In addition to capturing the smallest byte level changes possible, our software is optimized for long-distance, wide-area network communications providing built-in data compression and flow control capabilities, as well as leveraging advanced functionality such as encryption, wide area network optimizations and quality of service controls provided by existing IP infrastructure.

|

|

Double-Take Availability Features and Benefits

|

Feature

|

Description

|

Customer Benefit

|

||

|

Continuous, Real-time Data Replication

|

File system changes are captured as they are made on the source server(s) and transmitted immediately according to system policies.

|

Potential for data loss is reduced and sometimes eliminated.

|

||

|

Delta File Replication

|

Only file changes or “deltas” are captured and transmitted across the network.

|

The amount of network bandwidth required to keep a secondary copy of data synchronized is minimized, and data can be replicated to a remote target server across any IP connection.

|

||

|

Replicates Open Files

|

Even open files can be mirrored and changes replicated almost immediately.

|

Applications can be protected while they are in use providing increased availability and reducing potential for data loss.

|

||

|

Many to One Replication

|

Data from many source servers may be replicated to a single target server.

|

Shares the cost of a target server among many source machines, and allows centralized data protection.

|

||

|

Automatic Failover

|

Can stand in for multiple servers simultaneously; the target server assumes the IP addresses and names of failed servers and restarts applications.

|

Users can automatically access data on the target server, reducing down-time associated with a source (production) server failure.

|

||

|

Hardware Independent Failover and Recovery

|

Failover and recovery of entire systems can be done between dissimilar hardware.

|

Enables flexible failover and recovery, without the need for similar hardware.

|

||

|

Virtual Server Provisioning

|

Can automatically provision virtual machines on popular virtualization platforms, for the purpose of failover, recovery and migration.

|

Allows users to easily leverage virtualization for high availability and disaster recovery purposes. Also allows users to migrate from physical to virtual platforms in real-time, with minimal downtime.

|

||

|

Virtual Server Protection

|

Allows protection of entire virtual machines on various platforms, regardless of the guest operating system.

|

Allows users to easily leverage virtualization for high availability and disaster recovery purposes. Also allows users to migrate from physical to virtual platforms in real-time, with minimal downtime.

|

|

System State Recovery

|

Replicates changes, such as patches to operating systems and applications.

|

Enables full server recovery to most recent state, including files, operating systems and applications.

|

||

|

File Selection

|

Users can define which files are to be replicated at a volume, directory, file and wildcard level. The location of data on the target can also be specified.

|

Allows exact control of which files are replicated and where they are stored for maximum flexibility.

|

||

|

Flow Control

|

Automatically queues transactions on the source server if network resources are not available or are restricted by policy.

|

Runs reliably in spite of network disruptions or peak loads, without severely affecting the performance of the source server.

|

||

|

Transmission Limiting

|

The amount of bandwidth available for replication, as well as start and stop conditions, may be defined by the network administrator.

|

Allows replication to share a network link with other applications, preserving bandwidth for other applications.

|

||

|

Data Compression

|

Data transmitted between the source and target may be compressed, using various industry-standard algorithms.

|

Allows user to minimize the amount of network bandwidth used to protect data, especially in wide area network configurations.

|

||

|

Centralized Enterprise Management

|

A graphical management interface is provided which can be run from anywhere on the network and allows the user to control all of the servers running our software in their environment.

|

Allows user to monitor a large number of servers running our software from a single central location, minimizing management costs.

|

||

|

Geographically dispersed clustering

|

An extension to Microsoft Clustering support which allows clusters to be extended to multiple geographic locations.

|

Provides remote clustering and the elimination of shared storage as a single point of failure within a cluster.

|

||

|

Extensive Reporting/ Verification

|

An extensive collection of events, alerts and statistics are made available through standard mechanisms, including SNMP, Log Files and Windows NT/ 2000 Event Viewer/ Performance Monitor.

|

Prevents silent failures by confirming that your data protection systems are working properly.

|

||

|

Application Awareness

|

Setup of protection for key applications such as Exchange, SQL, Share Point and Blackberry Enterprise Server are automated for the user.

|

Eases the process of configuring protection for critical application, and minimizes configuration errors.

|

Double-Take Backup. In December 2007, we completed the acquisition of TimeSpring Software Corporation, now Double-Take Canada, which was a Montreal-based software company with software that provided the ability to recover copies of protected data from any point-in-time. The product acquired was “TimeData”, which allows customers to recover from operational problems such as files or e-mails that were erroneously deleted, file corruption due to viruses or other malfunctions, or malicious attacks on data files. In the second quarter of 2008 we began to market this software under the Double-Take company name to our new and existing customers. In the fourth quarter of 2009 the TimeData product, our Livewire product and our Cargo tiered recovery product were included in the product offering we call Double-Take Backup.

Double-Take Backup Features and Benefits

|

Feature

|

Description

|

Customer Benefit

|

||

|

Continuous, Real-time Data Protection

|

File system changes are captured as they are made on the data server(s) and transmitted immediately according to system policies.

|

Potential for data loss is reduced and sometimes eliminated.

|

||

|

Delta File Replication

|

Only file changes or “deltas” are captured and transmitted across the network.

|

The amount of network bandwidth required to keep a secondary copy of data synchronized is minimized.

|

||

|

Replicates Open Files

|

Even open files can be mirrored and changes replicated almost immediately.

|

Applications can be protected while they are in use providing increased availability and reducing potential for data loss.

|

||

|

Many to One Replication

|

Data from many source servers may be replicated to a single target server.

|

Shares the cost of a target server among many source machines, and allows centralized data protection.

|

||

|

Any point-in-time Recovery

|

File changes are maintained in time sequence order, and can be replayed on the repository server to give the user a view of any file at any point-in-time.

|

Users can rollback to previous versions of files in the event of an operational error such as a deleted file, virus, or other file system error.

|

||

|

Consistency Points

|

Software detects when protected data is in a good state, and allows users to select those points in time when recovering data.

|

Allows user to easily recover to a point-in-time at which the protected data is in a known, good state.

|

||

Double-Take Flex. In July 2008, through Double-Take Canada, we completed the acquisition of emBoot Inc., a Toronto, Ontario -based software company. The technology acquired provides the ability to boot servers, workstations and virtual machines from iSCSI storage using standard Ethernet technologies. The software product acquired was netBoot/i which enables organizations to utilize their iSCSI based storage area networks, or SANs, by enabling IT administrators to affordably provision, centralize and maintain virtual desktop infrastructures that are secure and easy to manage.. In the first quarter of 2009, the emBoot product was included in the product offering Double-Take Flex.

Double-Take Flex Features and Benefits

|

Feature

|

Description

|

Customer Benefit

|

||

|

Hardware Independent

|

The same iSCSI OS boot image can be booted from any x86/64 systems, physical or virtual servers, and virtually any storage hardware.

|

There are fewer images to maintain, and it allows for the flexible use of infrastructure.

|

||

|

Enterprise Management Console

|

One console allows you to centrally and easily manage network boot configurations for machines throughout an enterprise. You can also easily browse the network and add new boot from SAN clients.

|

Managing operating system boot images is simpler and users have centralized administration and control of workloads and hardware infrastructure.

|

||

|

Rapid Provisioning

|

Client and iSCSI Target configurations can be cloned for rapid setup of similar client configurations.

|

Allows users to quickly re-purpose existing infrastructure and optimize workloads.

|

||

|

Shared Boot Images

|

Single boot images can be shared among multiple clients, in read-only

or read/write states.

|

Ensures standard environment, avoid storing duplicate boot image data.

|

||

|

Software-based iSCSI Target

|

Turns any Windows-based server into an iSCSI storage host.

|

Provides iSCSI storage and boot image storage using existing hardware. Minimizes cost and complexity to implement a Flex network-boot configuration.

|

||

Double-Take Move. This software product provides real-time data movement and hardware-independent conversion technology that make workloads simple for administrators to move – and minimizes the impact on user productivity. Operating systems, applications and data are easily moved from one make, model and server configuration to another. Because Double-Take Move is hardware independent, it can also be used for any combination of virtual or physical servers. Double-Take Move continuously captures byte-level changes to a server's OS, applications and data and replicates those changes to new physical or virtual hardware at any location, locally or globally. By moving only the bytes that change, the software uses the minimum bandwidth required.

Double-Take Move Features and Benefits

|

Feature

|

Description

|

Customer Benefit

|

||

|

Low-impact Migration

|

Mirrors data from the source machine to the new target, even if they are separated by a low-bandwidth WAN.

|

Data can be compressed for transmission and bandwidth usage can be defined to ensure quality of service during migration.

|

||

|

Push Install

|

The migration console pushes the product to the new server, if necessary.

|

Eliminates the need to have the software pre-installed on the new server thus saving time.

|

||

|

Seamless Switchover

|

Switching to the new server can be executed manually or set up to be fully automated.

|

Allows the user to choose the best switchover method for their system.

|

||

|

Support for Hyper-V and ESX Server

|

Virtualize servers to VMware ESX or Microsoft Hyper-V platforms and automatically provision new virtual machines as needed.

|

Allows users to easily convert physical machines to virtual machines; or to convert virtual machines from one format to another.

|

||

|

X2X Migration

|

The entire system can be migrated. Migration can happen from physical serer to virtual server or a virtual machine from one virtualization platform to another.

|

Allows flexibility for users.

|

||

Double-Take Cloud. Double-Take Cloud was released in February 2010 and leverages Amazon Elastic Compute Cloud (Amazon EC2), a product offered by Amazon Web Service, LLC, to create a real-time workload recovery platform. Double-Take Cloud uses Double-Take Software’s system state replication engine, allowing customers to recover their data, applications, and operating systems, and rapidly recover a workload into an automatically provisioned Amazon virtual machine.

Double-Take Cloud Features and Benefits

|

Feature

|

Description

|

Customer Benefit

|

||

|

Low Startup Costs

|

Customers can provision new image servers on the fly, without purchasing expense hardware or securing an off-site recovery location.

|

Customer does not have to incur large capital expenses to establish an effective off-site recovery plan.

|

||

|

Rapid Deployment

|

Protection and recovery of a production server can be completed within a matter of minutes from signing up for the service.

|

Customer can be up and running with off-site protection and recovery with extensive planning and investment.

|

||

|

Pay-as-you-go Resources

|

Customers pay for Double-Take and Amazon services on a monthly basis, and no long-term commitment is required.

|

Customer is not locked in to a long-term commitment, thereby reducing risk and cost.

|

||

|

Recover to the Cloud

|

Production servers can be recovered to the cloud so they can be accessed from anywhere in the event of a disaster.

|

Production servers can be recovered quickly, without copying recovery data from the cloud to a local production facility.

|

|

Local Recovery

|

Production servers can be recovered to their original location, as well as to other recovery facilities.

|

Customer has flexibility in where they recover their production data. After a site failure, they can resume running workloads in a local environment.

|

||

|

Unlimited Scalability

|

Additional repository servers and storage capacity can be added easily without infrastructure changes.

|

Customer does not have to buy excess capacity or infrastructure up front in order to account for future growth. As storage and compute requirements grow, the solution will scale with them.

|

||

|

Real-time System State Protection

|

The entire state of a production server is protected, including the operating system, applications and user data.

|

Customer can recover an entire production server easily, without going through the process of reloading and configuring applications, applying patches, etc…

|

||

|

Lower Management Costs

|

Ongoing costs such as power, cooling and general server management are significantly reduced.

|

Customer can focus IT management resources on other areas.

|

Software Editions. Our product offerings have the features and benefits that are described above and are offered in versions that are aligned to operating system capabilities. Additional versions of our product offerings include those that have been specifically crafted to run within virtual systems and to perform replication only. Some versions are also available from OEM partners under different brand names.

Customer Support Services. We provide comprehensive customer support, which we consider to be both a critical asset and a source of competitive advantage. We have developed our support organization to be a key differentiator for our company and our customers. Unlike the increasing number of software companies that seek to cut costs attributable to customer support, we have chosen to invest in the customer support experience and take pride in our personal interaction with our customers. We view our customer support function as a means to drive renewals, increase licenses with existing customers and acquire new customers. As part of our focus on customer support, we staff our front line support team with senior technicians with the goal of solving customer issues within the first call. We aim to provide an exceptional post-sales product experience for each customer. We believe this support effort will be scalable as our customer base continues to grow.

Product support is offered on an annual basis and can be either purchased in advance or at annual renewal points based on the date of initial software purchase. We have support centers in Bracknell, United Kingdom, Worcester, United Kingdom, and Indianapolis, Indiana. In addition to our support organization, primary product support for channel and OEM customers is sometimes provided directly by our partners, and we provide escalated engineering support for those partners when needed.

Deployment Services. We have a professional services organization to help our customers with deployments. These offerings give our customers access to our best-practices and knowledge of the surrounding infrastructure to ensure a clean implementation. However, we do not consider our professional services to be strategic to our overall direction, and we try to design and build our software with the idea that it should be simple to install and operate without the need for extensive training or associated services. For those clients that meet the scale and complexity requirements, our professional services offerings consist of assessment and design services and implementation and deployment services.

Training. We provide a series of training courses. Training is provided both on-site and off-site to fit the wide variety of needs of our customers and partners. The training courses include both instructor-led as well as computer-based class formats.

Our Customers

As of December 31, 2009, we had about 22,000 customers in a variety of industries, including a large number of law firms, financial institutions, hospitals, school districts and government entities. Our customers use our software for a variety of purposes in terms of the applications they protect and the configuration of their servers. Our customers deploy our software in installations ranging from two servers to several hundred servers.

Our Technology

The Double-Take Availability software is based on flexible and efficient file system replication technology and advanced server and application failover technology. Most server applications have not been designed to provide for data redundancy or application failover to a different server or a different geographic location. Consequently, we had to develop solutions outside of standard application frameworks, utilizing different approaches to ensure that business-critical applications can be moved and restarted in different locations in a way that is as fast and transparent to users as possible. Many years of experience across a large installed base have given us a mature base of data protection and availability technologies that we believe represent a significant competitive advantage.

The software’s functionality is built into the user-mode components (source and target) of the software, which remain largely consistent across operating systems. The driver component is responsible for intercepting file system modifications, determining if the modifications are selected for replication and passing this information to the source component. The driver has been optimized to produce high-throughput with minimal resource requirements and to minimize file system latency to the end user.

The source component packages these transactions and transmits them to one or more target machines. The source component queues transactions when the target server or network is either slow or unavailable and uses patented compression techniques to minimize the system overhead required for this queuing. The source component also controls transmission and initial mirroring, as well as verification, replication set maintenance and connection management.

File system transactions are transmitted to the target machine using standard networking mechanisms to provide high-throughput. The target component then receives replication transactions from the source component and applies these transactions to the target file system. The target component is multi-threaded to handle efficiently simultaneous transactions from multiple source servers to multiple target files. The target component also monitors the source server’s health and performs server failover (via name, network address and share/mount point aliasing) when the source is unavailable.

Our full server failover technology applies the system state from a protected system to the backup system during the failover process, allowing the backup system to take over the full identity of the protected system. This includes operating system and application configuration, which is maintained on the backup system in real-time as changes are made on the protected system. This failover process takes into account hardware differences between the protected and backup systems, and allows failover to occur even if the systems have different processors, network interface cards, memory, or other hardware.

Management of our software is supported through various client interfaces, including graphical interfaces, a COM based application programming interface (API), and a command-line interface. All client platforms are based on the same set of common application interface commands, and these functions are available to third-party developers. Our cluster capabilities combines our core replication technology with the application failover capabilities of Microsoft Cluster Services (MSCS). Our cluster capabilities eliminate the need for clustered nodes to share access to the same physical disk, providing data redundancy and allowing cluster nodes to be placed at different locations, providing geographic redundancy for the cluster nodes as well as the data. With cluster capabilities, business critical data is stored on each cluster node’s local drives and then replicated to the other nodes in the cluster using our real-time replication. Our cluster capabilities can also provide quorum capability, acting as an arbitrator for the cluster in the event that the cluster nodes are running but cannot communicate.

Our Double-Take Backup product is a combination of our former products TimeData, Livewire and Cargo, along with several other technologies. This product continuously replicates changes to data, applications, and the operating system, protecting one or more production servers to a centralized repository server. At the time of recovery, Double-Take Backup allows the end user to configure and perform full-server recovery quickly to physically dissimilar hardware or virtual servers, with added validation steps. Validation compares the image of the source server to the actual recovery server then alerts the end user of potential problems. Double-Take Backup can also be used to migrate a server to different hardware, allowing the end user to use licenses for disaster recovery. When recovering to a virtual platform, Double-Take Backup automatically provisions virtual machines to match the original source machine.

In addition to maintaining a live copy of each production server’s data, Double-Take Backup also maintains a history of changes to the production server’s data so it can be recovered at any point in time. Our Double-Take Backup product captures file system changes that are replicated to the repository server, and stores those in a database in time sequence. A target file system interface allows Double-Take Backup and other applications to access the protected file system data at various points in time by presenting a view of the file system at that time.

Management of the Double-Take Backup technology is done via a management console that can be run from any computer within the customer’s network that has connectivity to the source and repository servers. This console is designed to allow centralized management of a customer’s environment from one convenient location.

Our Double-Take Cloud product leverages the Double-Take real-time replication engine to protect customer’s servers to the cloud. This product currently leverages Amazon’s Web Services (AWS) to provide off-site compute and storage resources, though it is planned that this offering will be extended to other cloud vendors in the future. The Double-Take Cloud product is bundled in an Amazon Machine Image (AMI), which can be deployed by any customer subscribing to the Double-Take Cloud service, which allows them easily provision a new repository server to host protected data. We also provide AMIs for the recovery process, which allows customers to quickly and easily provision and recover their workloads in the cloud in the event of a local disaster. In addition, customer’s can use Double-Take cloud to recover their protected data back to their original production site, or to a new location. Virtual Private Networking (VPN) software is provided to secure communication between a customer’s production site and the cloud, both for protection and recovery.

Our Double-Take Flex technology leverages the iSCSI storage standard and standard Ethernet network interface cards that support PXE (Preboot Execution Environment) to allow physical and virtual servers and workstations to boot directly from iSCSI storage systems. In addition, Double-Take Flex allows the assignment of boot images to physical and virtual systems to be centrally controlled and changed in order to simplify provisioning, migration and system re-purposing. To allow the greatest flexibility, Double-Take Flex makes the boot images for most current operating systems hardware independent, allowing a workload to be moved from one brand of server hardware to another or between physical and virtual systems and back. For customers that do not have existing iSCSI storage, Double-Take Flex also provides software-based iSCSI target functionality, which allows any Windows-based server to be used as an iSCSI storage device.

Our Double-Take Move product allows operating systems, applications and data to be easily moved from one make, model and server configuration to another. Because Double-Take Move is hardware independent, it can also be used for any combination of virtual or physical servers. Double-Take Move does not require servers to be offline during migration; data is mirrored from the old server to the new server without interruption to users. Changes that users make during migration are captured and replicated to the new server in real time. When the mirror is complete and all changes are replicated to the new server, cutover can occur with little to no downtime. Double-Take Move continuously captures byte-level changes to a server's OS, applications and data and replicates those changes to new physical or virtual hardware at any location, locally or globally. By moving only the bytes that change, Double-Take Move uses the minimum bandwidth required.

Marketing and Sales

We market and sell our software primarily to or through distributors, value-added resellers and OEMs, supported by an inside and field-based direct sales force located in the United States, Asia and Europe. Our selling model is based on building a strong distribution network through which customers can purchase the software. To date, we believe that this selling model has created an advantage for us. We currently have about 900 selling partners within our distribution and value-added reseller program, and we are adding more to this group to meet regional and technology related needs. To support our partners in our sales channels, our sales group has been organized in an overlay format so that our sales teams are working with our partners to pursue sales jointly.

In addition, our marketing partners complement our sales campaigns through seminars, trade shows and joint advertising. We leverage our customers and partners to provide references and recommendations that we use in our various promotional and sales activities. These partners include Dell Computer Corporation, Microsoft Corporation, Hewlett-Packard Company and VMware, Inc.

The goal of our marketing effort is to develop sales opportunities by increasing the awareness of our software’s functionality and business need within our target markets and segments. We plan to continue to invest in building greater Double-Take brand recognition in the United States and internationally through expansion of the use of our brand, public relations programs, interactions with industry analysts, trade shows, web search optimization, regional seminars and speaking engagements.

In 2009, we received approximately 17% of our total sales from sales of software and services to Dell Computer Corporation, which is the largest reseller of our software and services and approximately 10% of our total sales from sales of software and services through Sunbelt Software, Inc. (formerly Sunbelt Software Distribution, Inc.), which is a reseller of our software and services. No other resellers or distributors and no customer accounted for 10% or more of our total sales in 2009.

Our software revenue generally experiences some seasonality. Many organizations make the bulk of their information technology purchases, including software in the third and fourth quarters of the year. We believe this generally has resulted in higher revenue generated by software sales during these quarters. In 2009, software revenue increased from the first quarter to the second quarter. Software revenue decreased from the second quarter to the third quarter and then increased from the third quarter to the fourth quarter. Due to the effects of the current economic downturn, our quarterly revenue predictability has decreased significantly. As a result, future quarterly revenue may trend differently than it has historically. While the economic downturn continues to make predicting the quarterly revenue trending difficult, we believe that in line with our historical seasonality, the first quarter of 2010 should be the weakest quarter of the year.

Competition

The markets in which we compete are competitive and rapidly changing. Our primary competitors for Double-Take Availability include EMC (Legato), Neverfail, Symantec (Veritas) and CA, Inc. (XOsoft). All of our competitors offer a variety of data protection and recovery solutions, some of which may offer features that we do not offer or have more attractive pricing. Our primary competitors for Double-Take Backup include Symantec (Backup Exec), EMC (Avamar), Commvault (Simpana Backup and Recovery), Acronis (Acronis Backup and Recovery), and Microsoft Data Protection Manager. Our primary competitors for Double-Take Flex include Citrix (Citrix Provisioning Server) and Virtual Desktop Infrastructure (VDI) solutions from vendors such as VMWware. Our primary competitors for Double-Take Move are Platespin (Migrate), VMWare (VMWare Converter), Visoncore (vConverter) and Microsoft (Virtual Machine Manager).

The principal competitive factors in our industry include:

|

•

|

technology;

|

|

|

•

|

price;

|

|

|

•

|

product functionality and effectiveness;

|

|

|

•

|

product reliability;

|

|

|

•

|

product integration;

|

|

|

•

|

sales support;

|

|

|

•

|

scope and quality of customer support;

|

|

|

•

|

relationships with OEMs; and

|

|

|

•

|

reputation.

|

|

Our Double-Take software products also compete with alternative approaches for data protection and recovery. Alternative approaches include the following technologies:

|

•

|

Tape Backup. Tape backup solutions run on a scheduled basis, usually nightly or weekly, backing up all files to tape or scanning for files that have changed since the last backup and copying those files to tape. Full recovery from tape usually requires that the operating system and recovery software first be re-installed and re-configured on identical hardware before the data recovery component can begin. Examples of companies and products in this category include Symantec NetBackup and Backup Exec, IBM Tivoli Storage Manager, CA Brightstor Enterprise Backup, Legato Networker and CommVault Galaxy.

|

|

|

•

|

Snapshots. Hardware array based and operating system provided snapshots are tools that can reduce the time for recovering data, applications and servers. Snapshots operate on a disk volume basis by copying disk blocks that are about to be overwritten by changes before allowing new blocks to be written to disk. Because many snapshots are just differences from one point in time to another and not full copies of the volume, they are dependent on the survival of the original volume and exist in the same geographic location as the original volume. Therefore snapshots alone do not provide a complete solution, but can be used in conjunction with continuous data replication solutions like Double-Take to address many of the above limitations. Snapshot functionality is usually specific to a particular operating system volume manager or disk storage array. Examples of companies and products in this category include Microsoft Volume Shadow Copy Service, EMC TimeFinder and Snapview.

|

|

|

•

|

Clustering. Server clustering can improve the availability of data by providing one or more additional servers to resume processing in the event of a hardware or software failure. These systems are expensive, requiring matched server hardware and certified shared disk subsystems. In addition, server clusters are generally restricted to very short distances, making offsite disaster protection difficult. Shared disk clustering systems continue to have a single point of failure in the shared disk subsystem. Examples of companies and products in this category include Microsoft Cluster Service, Symantec Cluster Server, Steeleye LifeKeeper and Legato AutoStart.

|

|

|

•

|

Remote Disk Mirroring. Disk mirroring is typically implemented as software within a proprietary storage array or as a software driver or appliance between the server and the primary data storage. Changes are captured at the disk block level, with entire blocks of data being mirrored for any size change and any physical changes to the disk such as temporary files or defragmentation causing replication traffic. Typically, an operating system must boot and then “mount” the remotely mirrored drive in order to make the data accessible, which requires the operating system and applications to be installed and correctly configured to use the replicated volume, as well as extensive integrity checks. Examples of companies and products in this category include EMC SRDF and Mirrorview, Symantec Volume Replicator, FalconStorIPStor, DataCore SANmelody and Hitachi TrueCopy.

|

|

|

•

|

On-line Backup. On-line Backup solutions provide periodic backup of a user’s user data to an off-site location via a network connection. These solutions allow users to store copies of their data at a different location without purchasing or managing storage hardware. This data can be recovered back to the user’s site (or another site) in the event of a disaster. These systems generally do not provide real-time protection, and only protect user and application data vs. the entire contents of a server. While these types of systems are usually inexpensive, they do not allow users to recover their data directly at the off-site location and access it immediately. A lengthy recovery process is typically required to recover data. Examples of companies and products in this area include: ZManda Cloud Backup, Carbonite Pro, Mozy Pro, Commvault Simpana, Symantec Protection Network for servers and Computer Associates Instant Recovery On-Demand.

|

|

Some of our competitors have greater financial, technical, sales, marketing and other resources than we do, as well as greater name recognition and a larger overall customer base for their products. Additionally, some of these competitors have research and development capabilities that may allow them to develop new or improved products that may compete with our software. As this market continues to develop, a number of companies with greater resources than ours could attempt to enter the market or increase their presence in this market by acquiring or forming strategic alliances with our competitors or business partners or by introducing their own competing products.

Our success will depend on our ability to adapt to these competing forces, to develop more advanced products more rapidly and less expensively than our competitors, to continue to develop a global sales and support network and to educate potential customers about the benefits of using our software rather than our competitors’ products. Our competitors could introduce products with superior features, scalability and functionality at lower prices than our software. In addition, some of our customers and potential customers may buy other software or services from our competitors, and to the extent that they prefer to consolidate their software purchasing from fewer vendors, may choose not to continue to purchase our software and support services.

We expect additional competition from other established and emerging companies. Increased competition could result in price reductions, reduced gross margins and loss of market share, any of which could harm our business.

Research and Development

We have made a significant investment in developing and improving our software. Our research and development expenditures were $11.9 million, or approximately 14% of our total revenue, for 2007, $16.5 million, or approximately 17% of our total revenue, for 2008 and $15.3 million, or approximately 18%, for 2009. Our development team has specific core competencies in Windows development including drivers, file systems, storage, clustering, networking and applications such as Exchange, SQL Server, Oracle Database and SharePoint server. Our engineering organization, located in Indianapolis, Montreal, and Toronto is responsible for product development, quality assurance, product management and documentation.

Intellectual Property

Our success as a company depends upon our ability to protect our core technology and intellectual property. To accomplish this, we rely on a combination of intellectual property rights, including patents, trade secrets, copyrights and trademarks, as well as customary contractual protections.

We have been granted two United States patents relating to our Real Time Backup System which is a component of all of our Double-Take products. The granted United States patents will expire in October 2015. As part of our acquisition of TimeSpring, we acquired seven United States patents which will expire at various dates from 2015 to 2020. These patents and, to the extent any future patents are issued, may be contested, circumvented or invalidated over the course of our business, and we may not be able to prevent third-parties from infringing these patents. Therefore, the exact effect of having patents cannot be predicted with certainty.

Furthermore, we have registered Double-Take®, Double-Take Flex®, Double-Take Move®, Double-Take for Virtual Systems®, TimeData®, and netBoot/i® product trademarks in the United States and have applied for registration for a variety of other trademarks including Double-Take Availability tm, Double-Take Backup tm and Double-Take Cloud tm. A third party may contest the registration of our trademark applications or may bring a claim for infringement of any of our registered or non-registered trademarks.

Employees

As of February 26, 2010, we had 387 employees in offices across the United States, Europe, Canada and Asia. None of our employees are represented by labor unions, and we consider our current employee relations to be good.

The following table sets forth information with respect to our executive officers:

|

Name

|

Age

|

Position

|

||||

|

Dean Goodermote

|

56

|

President, Chief Executive Officer and Chairman of the Board of Directors

|

||||

|

Robert L. Beeler

|

44

|

Vice President of Engineering

|

||||

|

David J. Demlow

|

42

|

Chief Technology Officer

|

||||

|

S. Craig Huke

|

48

|

Chief Financial Officer

|

||||

|

Daniel M. Jones

|

42

|

Vice President of Worldwide Sales

|

||||

|

Michael Lesh

|

65

|

Vice President of Professional Services and Support

|

||||

|

Jo Murciano

|

58

|

Vice President of EMEA; President of Double-Take EMEA

|

Dean Goodermote joined Double-Take Software in March 2005 as President, Chief Executive Officer and Chairman of the board of directors. Since July 2004 he has also served as Chief Executive Officer of Grid-Analytics LLC, a concept-stage company he founded focused on aggregated research. From September 2001 to March 2005, Mr. Goodermote served as a Venture Partner of ABS Capital Partners. From September 2000 to August 2001, Mr. Goodermote was Chairman and Chief Executive Officer of Clinsoft Corporation, a developer of software for clinical research. From 1997 to August 2001, Mr. Goodermote was Chairman and President of Domain Solutions Corporation, a software developer for enterprise applications and the parent of Clinsoft. From May 2000 until December 2001, Mr. Goodermote founded and was Chief Executive Officer and then the Chairman of IPWorks, Inc., a developer of internet address management software. From August 1996 to May 2000, Mr. Goodermote was Chief Executive Officer and President of Process Software Corporation, a developer of Internetworking software. From August 1986 to February 1997, Mr. Goodermote served in various positions, including eventually President and Chairman, of Project Software and Development Corporation, later known as MRO Software, Inc., a provider of software-based asset and service management solutions.

Robert L. Beeler joined Double-Take Software in July 1995 as Vice President of Engineering. From 1996 to 2001, Mr. Beeler served as a member of our board of directors. From July 1991 to July 1995, Mr. Beeler served as Project Manager, Project Engineer and System/Software Engineer at the Naval Air Warfare Center, where he supervised and provided technical leadership to a development team in support of the Navy Airborne Electronic Warfare Platform. From 1988 to 1991, Mr. Beeler served as a Software Developer for National Field Service Inc.

David J. Demlow joined Double-Take Software in 1997 as Vice President of Product Management and, since January 2005, has served as our Chief Technology Officer. From 1991 to 1997, Mr. Demlow held the following positions at Seagate Software: 1994 to 1997, Senior Product Manager, Enterprise Storage Management; 1993 to 1994, Systems Engineer, Sales and Channel Support; 1991 to 1993, Account Rep, Direct and Channel Sales. From 1990 to 1991, Mr. Demlow served as a Sales Manager at Business Technology Associates, Inc.

S. Craig Huke joined Double-Take Software in June 2003 as Chief Financial Officer. From May 2001 to May 2003, Mr. Huke served as Chief Financial Officer for Apogee Networks Systems and Consulting LLC, Inc., a privately held software company specializing in network cost visibility and containment. From April 1999 to May 2001, Mr. Huke served as Chief Financial Officer at Bluestone Software, Inc., an Internet infrastructure software company. From

April 1998 to April 1999, Mr. Huke served as Vice President, Finance at Metronet Communications Corp., a communications company. From November 1994 to April 1998, Mr. Huke held the following positions at Seer Technologies, Inc., a software development company: September 1997 to April 1998, Vice President & Corporate Controller; November 1996 to September 1997, Corporate Controller; November 1995 to November 1996, Director of Financial Reporting and Analysis; and November 1994 to November 1995, Manager of Financial Reporting and Analysis.

Daniel M. Jones joined Double-Take Software in October 2001 as Eastern Region Sales Director and, since May 2005, has served as our Vice President of Sales and Marketing. In January 2010 Mr. Jones became our Vice President of Worldwide Sales. From January 2000 to October 2001, Mr. Jones served as National Director of Sales at StorageNetworks, a provider of data storage software services to major and global businesses. From January 1998 to January 2000, Mr. Jones served as Vice President of North American Sales of Net-tel Inc., a provider of internet protocol data and voice services. From June 1996 to December 1997, Mr. Jones served as Director of Sales at MidCom Communications Inc., a facility-based telecommunications company. From February 1991 to June 1996, Mr. Jones held the following positions at ALLNET/Frontier Communications: May 1993 to June 1996, Area Manager, July 1992 to May 1993, District Manager; and July 1991 to July 1992, Sales Representative.

Michael Lesh joined Double-Take Software in June 2001 as Vice President of Professional Services and Support. From October 2000 to June 2001, Mr. Lesh served as Director, Professional Services at Openpages, Inc., a provider of enterprise compliance management software. From February 1973 to October 2000, Mr. Lesh held the following positions at Data General, a division of EMC Corporation: January 1998 to October 2000, Director, Professional Services; February 1996 to January 1998, Director, Eastern Operations Professional Services; March 1995 to February 1996, Director, Technology Deployment Services; March 1990 to March 1995, Manager, Northeast Professional Services; and May 1984 to March 1990, Manager, Regional Systems Engineering.

Jo Murciano joined Double-Take Software in May 2006 as Vice President of EMEA and President of Double-Take EMEA, and from January 2008 through December 2009 served as our Vice President of International. Mr. Murciano is also Chief Executive Officer and a director of Sunbelt Software, Inc. (formerly Sunbelt Software Distribution, Inc.), one of our resellers, which he joined in 1994. From October 1983 to May 2006, Mr. Murciano served as Chairman of Sunbelt System Software S.A.S., a software distributor that he founded in 1983 and which we acquired in May 2006. From September 1982 to October 2000, Mr. Murciano served as Chief Executive Officer of RMH Group, a provider of development and communication tools for the IBM AS/400 market that Mr. Murciano founded in 1982.

Available Information

For more information about us, visit our web site at www.doubletake.com. Our electronic filings with the SEC (including our annual report on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K, and any amendments to these reports) are available free of charge through our web site as soon as reasonably practicable after we electronically file with or furnish them to the SEC.

|

Risk Factors.

|

An investment in our stock involves a high degree of risk. You should carefully consider the following risks and all of the other information set forth in this annual report before deciding to invest in shares of our common stock. If any of the events or developments described below occur, our business, financial condition or results of operations could be negatively affected. In that case, the trading price of our common stock could decline, and you could lose all or part of your investment in our common stock.

Risks Related to Our Business

A continued downturn in the global economy could adversely impact our continued growth, results of operations and our ability to forecast future business.

Beginning in 2008 and continuing through 2009, there has been a downturn in the global economy, resulting in slower economic activity, decreased consumer confidence, reduced corporate profits and capital spending, adverse business conditions and liquidity concerns. There has also been increased volatility in foreign exchange markets. We believe that our sales and results of operations were impacted by these economic factors. These factors make it difficult for our customers, our vendors and us to accurately forecast and plan future business activities, and they could cause customers to slow or defer spending on our products, which would delay and lengthen sales cycles, hurt our growth and negatively affect our results of operations. We cannot predict the timing or duration of any economic slowdown or the timing or strength of a subsequent economic recovery, worldwide or in our industry.

Intense competition in our industry may hinder our ability to generate revenue and may adversely affect our margins.

The market for our software is intensely competitive. Our primary competitors for Double-Take Availability include EMC Corporation (Legato), Neverfail Group, Ltd., Symantec Corporation (Veritas) and CA, Inc. (XOsoft Inc.). In addition to direct competitors, other technologies such as SAN-based replication are available that solve some of the same problems that our software solves. These technologies may be viewed as a competitive alternative to our products by customers. We also have competitors for our other products. Some of the companies we have identified and many of our other current and potential competitors have longer operating histories and substantially greater financial, technical, sales, marketing and other resources than we do, as well as larger installed customer bases and greater name recognition. Our competitors may be able to devote greater resources to the development, marketing, distribution, sale and support of their products than we can and some may have the ability to bundle their data replication offerings with their other products. The extensive relationships that these competitors have with existing customers may make it increasingly difficult for us to increase our market share. The resources of these competitors also may enable them to respond more rapidly to new or emerging technologies and changes in customer requirements and to reduce prices to win new customers.