Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2009 Commission file number 000-50552

Asset Acceptance Capital Corp.

(Exact name of registrant as specified in its charter)

| Delaware | 80-0076779 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

28405 Van Dyke Avenue

Warren, Michigan 48093

(Address of principal executive offices)

Registrant’s telephone number, including area code:

(586) 939-9600

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Common Stock, $0.01 par value | The NASDAQ Global Select Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ |

Accelerated filer x | |

| Non-accelerated filer ¨ (Do not check if a smaller reporting company) |

Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the registrant’s Common Stock held by non-affiliates of the registrant on June 30, 2009 (based on the June 30, 2009 closing sales price of $7.69 of the registrant’s Common Stock, as reported on The NASDAQ Global Select Market on such date) was $114,928,880.

Number of shares outstanding of the registrant’s Common Stock, $0.01 par value, at February 26, 2010:

30,603,708 shares of Common Stock, $0.01 par value.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive Proxy Statement for its 2010 Annual Meeting of Stockholders to be held on May 13, 2010 are incorporated by reference into Part III of this Report.

Table of Contents

ASSET ACCEPTANCE CAPITAL CORP.

Annual Report on Form 10-K

TABLE OF CONTENTS

| Page | ||||

| PART I | ||||

| Item 1. |

3 | |||

| Item 1A. |

14 | |||

| Item 1B. |

21 | |||

| Item 2. |

22 | |||

| Item 3. |

22 | |||

| Item 4. |

22 | |||

| Supplemental Item. |

23 | |||

| PART II | ||||

| Item 5. |

25 | |||

| Item 6. |

26 | |||

| Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

29 | ||

| Item 7A. |

52 | |||

| Item 8. |

52 | |||

| Item 9. |

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure |

52 | ||

| Item 9A. |

53 | |||

| Item 9B. |

53 | |||

| PART III | ||||

| Item 10. |

53 | |||

| Item 11. |

54 | |||

| Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

54 | ||

| Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

54 | ||

| Item 14. |

54 | |||

| PART IV | ||||

| Item 15. |

55 | |||

| 58 | ||||

| F-1 | ||||

Annual Report on Form 10-K

We file reports with the Securities and Exchange Commission (“SEC”), which we make available on our website, www.assetacceptance.com, free of charge. These reports include Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to such reports, each of which is provided on our website as soon as reasonably practicable after we electronically file such materials with or furnish them to the SEC.

2

Table of Contents

| Item 1. | Business |

General

We have been purchasing and collecting defaulted or charged-off accounts receivable portfolios from consumer credit originators since the formation of our predecessor company in 1962. Charged-off receivables are the unpaid obligations of individuals to credit originators, such as credit card issuers, consumer finance companies, healthcare providers, retail merchants, telecommunications and other utility providers. Since these receivables are delinquent or past due, we are able to purchase them at a substantial discount. We purchase and collect charged-off consumer receivable portfolios for our own account as we believe this affords us the best opportunity to use long-term strategies to maximize our profits. From January 1, 2000 through December 31, 2009, we purchased 1,090 consumer debt portfolios, with an original charged-off face value of $40.4 billion for an aggregate purchase price of $998.0 million, or 2.47% of face value, net of buybacks.

When considering whether to purchase a portfolio, we conduct a quantitative and qualitative analysis of the portfolio to appropriately price the debt. This analysis includes the use of our proprietary pricing and collection probability model and draws upon our extensive experience in the industry. We have developed experience across a wide range of asset types at various stages of delinquency, having made purchases across more than 20 different asset types from over 160 different debt sellers since 2000. We selectively deploy our capital in the fresh, primary, secondary and tertiary delinquency stages. These stages are typically where the accounts are delinquent and have been charged off and immediately sold or have been placed with between one and four collection agencies who have already attempted to collect on the accounts included in the portfolios we acquired.

We have a long-standing history in the industry, relationships with debt sellers and attention to post-sale service. Unlike some third party collection agencies that typically attempt to collect the debt for a period of only six to twelve months, we generally take a long-term approach to the collection effort as we are the owners of the debt. We apply an approach that encourages cooperation with the debtors to make a lump sum settlement payment in full or to formulate a repayment plan. For those debtors who we believe have the ability to repay the debt, we may proceed with legal remedies to obtain our collections. Through our strategy of holding the debt for the long-term, we have established a methodology of converting debtors into paying customers. In addition, our approach allows us to invest in various collection management and analysis tools that may be too costly for short-term oriented collection agencies, as well as to pursue legal collection strategies as appropriate. In many cases, we continue to receive collections on individual portfolios for more than ten years from the date of purchase.

In addition, the Company finances the sales of consumer product retailers through its Consumer Credit, LLC subsidiary.

3

Table of Contents

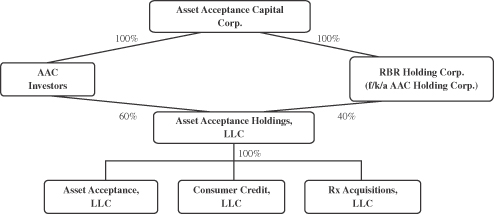

History

Our business originated in 1962 for the purpose of purchasing and collecting charged-off consumer receivables. Set forth below is a diagram depicting our corporate structure as of January 1, 2005:

Acquisition

On April 28, 2006, Asset Acceptance Holdings, LLC completed a stock purchase transaction of Premium Asset Recovery Corporation (“PARC”). Under the terms of the agreement, Asset Acceptance Holdings, LLC acquired 100% of the outstanding shares of PARC.

Currently, Asset Acceptance, LLC purchases and holds portfolios in all asset types except for healthcare. PARC purchases and collects on portfolios primarily in healthcare.

Current Structure and Reorganization

On April 15, 2008, Rx Acquisitions, LLC was merged with and into Asset Acceptance, LLC, with the result that, by operation of law, all assets of Rx Acquisitions, LLC were vested in Asset Acceptance, LLC and all obligations of Rx Acquisitions, LLC were assumed by Asset Acceptance, LLC. Subsequent to the merger, all ownership interests in Asset Acceptance, LLC continue to be owned by Asset Acceptance Holdings, LLC.

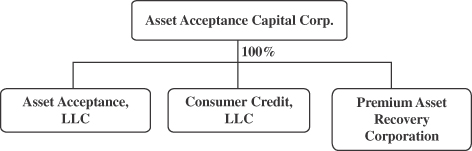

On August 31, 2009, a reorganization was completed that merged AAC Investors, Inc., RBR Holding Corp., and Asset Acceptance Holdings, LLC (“Non-Operating Subsidiaries”) with Asset Acceptance Capital Corp. (“AACC”). All assets of the Non-Operating Subsidiaries vested in AACC and all obligations of the Non-Operating Subsidiaries were assumed by AACC. As a result of this reorganization, Asset Acceptance, LLC, Consumer Credit, LLC and PARC became direct wholly-owned subsidiaries of AACC. The foregoing is referred to herein as the “Reorganization”.

4

Table of Contents

Set forth below is a diagram depicting our current corporate structure, which reflects the Reorganization:

As used in this Annual Report, all references to us mean AACC, a Delaware corporation, and all wholly-owned subsidiaries (referred to in our financial statements as the “Company”).

Purchasing

Typically, we purchase our portfolios in response to a request to bid received via e-mail or telephone from a prospective seller. In addition to these requests, we have developed a marketing and acquisitions team that contacts and cultivates relationships with known and prospective sellers of portfolios in our core markets and in markets for new asset types. We have purchased portfolios from over 160 different debt sellers since 2000, including many of the largest consumer lenders in the United States. While we have no policy limiting purchases from a single debt seller, we purchase from a diverse set of debt sellers and our purchasing decisions are based upon constantly changing economic and competitive conditions as opposed to long-term relationships with particular debt sellers. Depending on market conditions and opportunities presented by certain debt sellers, we may enter into forward flow contracts. Forward flow contracts commit a debt seller to sell a steady volume of charged-off receivables to us for a fixed percentage of the face value over a specified time period, which typically ranges between three and twelve months.

We purchase our portfolios through a variety of sources, including consumer credit originators, private brokers and occasionally from debt resellers. Debt resellers are debt purchasers that sell accounts at some point in time after purchase. Generally, portfolios are purchased either in competitive bids through a sealed bid process, in some cases, through an on-line process or through privately-negotiated transactions between the credit originator or other holders of consumer debt and us.

Each potential acquisition begins with a quantitative and qualitative analysis of the portfolio. In the initial stages of the due diligence process, we review basic data on the portfolio’s accounts. This data typically includes the account number, the consumer’s name, address, social security number, phone numbers, outstanding balance, date of charge-off, last payment and account origination to the extent the debt sellers provide this data. We analyze this information and summarize it based on certain key metrics, such as, but not limited to, state of debtor’s last known residence, type of debt, and, time remaining on the credit bureaus and time remaining within the statute of limitations. In addition, we request the seller to provide answers to a questionnaire designed to help us understand important qualitative factors relating to the portfolio.

As part of our due diligence, we evaluate the portfolio utilizing our proprietary pricing model. This model uses certain characteristics of the portfolio, historical analysis of similar portfolios, potential portfolio recoveries and collection expense estimates to formulate a bid range. In those circumstances where the type or pricing of the portfolio is unusual, we consult with industry experts and our collections management to help ascertain collectability, potential collection strategies and our ability to integrate the new portfolio into our collection platform.

5

Table of Contents

Once we have compiled and analyzed available data, we consider market conditions and determine an appropriate bid price or bid range. The recommended bid price or bid range, along with a summary of our due diligence, is submitted to our investment committee and, for purchases in excess of a certain dollar threshold, to a designated member of our audit committee for review and approval. After appropriate approvals and acceptance of our offer by the seller of the portfolio, a purchase agreement is negotiated. Buyback provisions are generally incorporated into the purchase agreement for bankrupt, fraudulent, paid prior or deceased accounts and, typically, the credit originator either agrees to repurchase these accounts or replace them with acceptable accounts within certain time frames, generally within 90 to 180 days. Upon execution of the agreement, we receive title to the accounts and the transaction is funded.

The following chart categorizes our purchased receivables portfolios acquired from January 1, 2000 through December 31, 2009 into major asset types, as of December 31, 2009:

| Asset Type |

Face Value of Charged-off Receivables(2) |

% | No. of Accounts |

% | |||||||

| (in thousands) | (in thousands) | ||||||||||

| General Purpose Credit Cards |

$ | 20,312,939 | 51.7 | % | 8,651 | 26.1 | % | ||||

| Private Label Credit Cards |

5,654,938 | 14.4 | 7,827 | 23.6 | |||||||

| Telecommunications/Utility/Gas |

3,094,747 | 7.9 | 7,920 | 23.9 | |||||||

| Healthcare |

2,510,266 | 6.4 | 4,118 | 12.4 | |||||||

| Health Club |

1,562,807 | 4.0 | 1,272 | 3.8 | |||||||

| Auto Deficiency |

1,352,470 | 3.4 | 240 | 0.7 | |||||||

| Other Installment Loans |

1,345,148 | 3.4 | 353 | 1.1 | |||||||

| Other(1) |

3,443,045 | 8.8 | 2,785 | 8.4 | |||||||

| Total |

$ | 39,276,360 | 100.0 | % | 33,166 | 100.0 | % | ||||

| (1) | “Other” includes charged-off receivables of several debt types, including healthcare, student loan, mobile home deficiency and retail mail order. This excludes the purchase of a single portfolio in June 2002 with a face value of $1.2 billion at a cost of $1.2 million (or 0.1% of face value), consisting of approximately 3.8 million accounts. |

| (2) | Face value of charged-off receivables represents the cumulative amount of purchases net of buybacks. The amounts in this table are not adjusted for payments received, settlements or additional accrued interest on any accounts in such portfolios that occur after the purchase date. |

The age of a charged-off consumer receivables portfolio, the time since an account has been charged-off by the credit originator and the number of times a portfolio has been placed with third parties for collection purposes are important factors in determining the price at which we will offer to purchase a portfolio. Generally, there is an inverse relationship between the age of a portfolio and the price at which we will purchase it. This relationship is due to the fact that older receivables are typically more difficult to collect. The consumer debt collection industry places receivables into the following categories depending on the age and number of third parties that have previously attempted to collect on the receivables:

| • | fresh accounts are typically 120 to 180 days past due, have been charged-off by the credit originator and are being sold prior to any post charge-off collection activity. These accounts typically sell for the highest purchase price; |

| • | primary accounts are typically 180 to 360 days past due, have been previously placed with one third party collector and typically receive a lower purchase price; and |

| • | secondary and tertiary accounts are typically more than 360 days past due, have been placed with two or three third party collectors and receive even lower purchase prices. |

We will purchase accounts at any point in the delinquency cycle. We deploy our capital within these delinquency stages based upon the relative values of the available debt portfolios.

6

Table of Contents

The following chart categorizes our purchased receivables portfolios acquired from January 1, 2000 through December 31, 2009 into the major account types, as of December 31, 2009:

| Account Type |

Face Value of Charged-off Receivables(2) |

% | No. of Accounts |

% | |||||||

| (in thousands) | (in thousands) | ||||||||||

| Fresh |

$ | 2,634,805 | 6.7 | % | 1,507 | 4.5 | % | ||||

| Primary |

4,642,472 | 11.8 | 4,530 | 13.7 | |||||||

| Secondary |

9,192,511 | 23.4 | 8,339 | 25.1 | |||||||

| Tertiary(1) |

18,434,537 | 47.0 | 15,642 | 47.2 | |||||||

| Other |

4,372,035 | 11.1 | 3,148 | 9.5 | |||||||

| Total |

$ | 39,276,360 | 100.0 | % | 33,166 | 100.0 | % | ||||

| (1) | Excludes the purchase of a single portfolio in June 2002 with a face value of $1.2 billion at a cost of $1.2 million (or 0.1% of face value), consisting of approximately 3.8 million accounts. |

| (2) | Face value of charged-off receivables represents the cumulative amount of purchases net of buybacks. The amount is not adjusted for payments received, settlements or additional accrued interest on any accounts in such portfolios that occur after the purchase date. |

We also review the geographic distribution of accounts within a portfolio because collection laws differ from state to state. The following chart illustrates our purchased receivables portfolios acquired from January 1, 2000 through December 31, 2009 based on geographic location of debtor, as of December 31, 2009:

| Geographic Location |

Face Value of Charged-off Receivables(3)(4) |

% | No. of Accounts(3) |

% | |||||||

| (in thousands) | (in thousands) | ||||||||||

| Texas(1) |

$ | 5,639,291 | 14.4 | % | 5,291 | 15.9 | % | ||||

| California |

4,472,324 | 11.4 | 3,707 | 11.2 | |||||||

| Florida(1) |

3,815,494 | 9.7 | 2,379 | 7.2 | |||||||

| New York |

2,279,597 | 5.8 | 1,398 | 4.2 | |||||||

| Michigan(1) |

2,102,903 | 5.4 | 2,573 | 7.8 | |||||||

| Ohio(1) |

1,848,596 | 4.7 | 2,360 | 7.1 | |||||||

| Illinois(1) |

1,583,502 | 4.0 | 1,754 | 5.3 | |||||||

| Pennsylvania |

1,344,888 | 3.4 | 998 | 3.0 | |||||||

| New Jersey(1) |

1,259,953 | 3.2 | 1,081 | 3.3 | |||||||

| North Carolina |

1,095,588 | 2.8 | 731 | 2.2 | |||||||

| Georgia |

1,094,616 | 2.8 | 895 | 2.7 | |||||||

| Other(2) |

12,739,608 | 32.4 | 9,999 | 30.1 | |||||||

| Total |

$ | 39,276,360 | 100.0 | % | 33,166 | 100.0 | % | ||||

| (1) | Collection site(s) located in this state. |

| (2) | Each state included in “Other” represents less than 2.0% of the face value of total charged-off receivables. |

| (3) | Excludes the purchase of a single portfolio in June 2002 with a face value of $1.2 billion at a cost of $1.2 million (or 0.1% of face value), consisting of approximately 3.8 million accounts. |

| (4) | Face value of charged-off receivables represents the cumulative amount of purchases net of buybacks. The amounts in this table are not adjusted for payments received, settlements or additional accrued interest on any accounts in such portfolios that occur after the purchase date. |

7

Table of Contents

Collection Operations

Our collection operations seek to maximize the recovery of our purchased charged-off receivables in a cost-effective manner. We have organized our collection process into a number of specialized departments, which include collection, legal collection and other collection departments. Other collections is predominantly comprised of third party agencies, bankruptcy and probate collections.

Generally, our efforts begin in our collection department and, if warranted, move to our legal collection department. If an account involves a bankrupt debtor or a deceased debtor, our bankruptcy or probate recovery departments will review and manage the account. If it is determined that an account should be outsourced to a third party collection agency, our agency or legal forwarding departments handle the matter. We utilize a network of data providers to obtain updated data on our purchased charged-off receivables and to assist our account representatives in their ability to collect on these receivables.

Collection Department

Once a portfolio is purchased, we perform a review in order to formulate and apply what we believe to be an effective collection strategy. This review includes a series of data preparation and information acquisition steps to provide the necessary account data to begin collection efforts. Portfolio accounts are assigned, sorted and prioritized based on account status and demographics, balance sizes and various internal and external collectability indicators.

We train our account representatives to be full service account representatives who handle substantially all collection activity related to the accounts they service. Such activities include manual and automated dialer outbound calling activity, inbound call management, skip tracing or debtor location efforts and settlement and payment plan negotiation. Our performance-based collection model is driven by a bonus program that allows account representatives to earn bonuses based on their achievement compared to collection goals. In addition, we monitor our account representatives for compliance with federal and state debt collection laws.

When an initial telephone contact is made with a debtor, the account representative is trained to go through a series of questions in an effort to obtain accurate location and financial information on the debtor, the reason the debtor may have defaulted on the account, the debtor’s willingness to pay and other relevant information that may be helpful in securing satisfactory settlement or payment arrangements. If full payment is not available, the account representative will attempt to negotiate a settlement. In an effort to maximize recoveries, we maintain settlement guidelines that account representatives, supervisors and managers must follow. Exceptions are handled by management on an account-by-account basis. If the debtor is unable to pay the balance in full or settle within allowed guidelines, monthly installment plans are encouraged in order to have the debtor resume a regular payment habit. Our experience has shown that debtors are more likely to respond to this approach, which can result in settlement in full in the future.

If an account representative is unable to establish contact with a debtor, the account representative undertakes skip tracing procedures to locate, initiate contact with and collect from the debtor. Skip tracing efforts are performed individually at the account representative level and by third party information providers in a batch process. Each account representative has access to internal and external information databases that interface with our collection system. In addition, we have several information providers from whom we acquire information that is either systematically or manually validated and used in our efforts to locate debtors. Using these methods, we periodically refresh and supply updated account information to our account representatives to increase contact with debtors.

Legal Collection Department

In the event collection has not been obtained through our collection department and the opportunity for legal action is verified, we pursue a legal judgment against the debtor. Once a judgment is obtained, our legal department pursues various collection strategies to secure payment. Our in-house legal collection department is

8

Table of Contents

comprised of collection attorneys, non-attorney legal account representatives, support staff and skip tracers. Our legal forwarding department is comprised of account representatives, support staff and associates managing activities with outside attorneys.

For accounts in states where we have a local presence, and in some cases adjacent states, we prefer to pursue an in-house legal strategy as it provides us with a greater ability to manage the process. We currently have in-house capability in nine states. In each of these states, we have designed our legal policies and procedures to maintain compliance with state and federal laws while pursuing available legal opportunities. We will pursue selective expansion into different geographic regions if analysis indicates it is favorable to do so.

Our legal forwarding department is organized to address the legal recovery function for accounts principally located in states where we do not have a local or adjacent presence to handle excess capacity and for accounts that we believe can be better served by a third party law firm. To that end, we utilize independent agencies including law firms throughout the country, who work for us on a contingent fee basis. The legal forwarding department actively manages and monitors our legal collection process handled by third parties.

Other Collection Departments

Although we collect the largest portion of our charged-off receivable portfolios through our internal collection operations, in some cases we believe it can be more effective and cost-efficient to outsource collections. We have developed a network of third party collection agencies to service accounts when we believe outsourcing is an appropriate strategy. For example, we may consider outsourcing relatively small balance accounts so that our account representatives can focus on larger balance accounts. In addition, we have an agency agreement with a firm in India which we engaged to collect on our behalf. These varying collection channels allow us to pursue the most effective collection method for each account.

Our bankruptcy and probate recovery departments handle bankruptcy and estate probate processing and collections. The bankruptcy department files proofs of claims for recoveries on receivables, which are included in consumer bankruptcies filed under Chapter 7 (resulting in liquidation and discharge of a debtor’s debts) and Chapter 13 (resulting in repayment plans based on the financial wherewithal of the debtor) of the U.S. Bankruptcy Code. The probate recovery department and our network of third party law firms submit claims against estates involving deceased debtors having assets that may become available to us through a probate claim.

Seasonality

Refer to Part II. Item 7, under the caption “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Seasonality” for the effect of seasonality on our business.

Competition

The consumer debt collection industry is highly competitive and fragmented. We compete with a wide range of other purchasers of charged-off consumer receivables, third party collection agencies, other financial service companies and credit originators that manage their own consumer receivables. Some of these companies may have substantially greater numbers of associates and financial resources and may experience lower account representative turnover rates than we do. Furthermore, some of our competitors may obtain alternative sources of financing, the proceeds from which may be used to fund expansion and to increase their number of charged-off portfolio purchases. Barriers to entry into the consumer debt collection industry are low. Companies with greater financial resources may elect at a future date to enter the consumer debt collection business. Furthermore, current debt sellers may change strategies and cease selling debt portfolios in the future.

Competitive pressures affect the availability and pricing of receivable portfolios, as well as the availability and cost of qualified account representatives. In addition, some of our competitors may have entered into forward

9

Table of Contents

flow contracts under which consumer credit originators have agreed to transfer a steady flow of charged-off receivables to them in the future, which may restrict those credit originators from selling receivables to other purchasers and limit the supply of receivables available to us.

We face bidding competition in our acquisition of charged-off consumer receivables. We believe successful bids generally are predominantly awarded based on price, secondarily based on service and relationships with the individual debt sellers, and the debt buyer’s ability to fund the deal. In addition, there continues to be a consolidation of issuers of credit cards, which have been a principal source of our receivable purchases. This consolidation has decreased the number of sellers in the market and could eventually give the remaining sellers increasing market strength in the price and terms of the sale of charged-off credit card accounts.

Technology Platform

We believe that information technology is critical to our success. Our key systems have been purchased from outside vendors and, with our input, have been tailored to meet our particular business needs. We maintain a full-time staff of technology professionals who monitor and maintain our information technology and communications structure. We utilize a centralized data center model. This leverages economies of scale in providing distributed computing capabilities.

We license our collection software and complementary products from third party providers. The collection software in use today enables us to:

| • | automate the loading of accounts in order to expedite collecting after purchase; |

| • | segment the accounts into dispositions for collection prioritization; |

| • | access several approved service partners including third party letter production and mailing vendors, credit reporting services and information service providers; |

| • | interface with automated dialers to increase the number of contacts with our debtors; |

| • | connect to a document imaging system to allow our associates, with appropriate responsibilities, to view scanned documents on accounts from their workstations while working on an account; |

| • | limit an associate’s ability to work outside of company guidelines; |

| • | query the appropriate database for any purpose which may be used for collection, reporting or other business matters; and |

| • | establish parameters to comply with federal and state laws. |

In 2007, we signed an agreement with a software provider and initiated a project to install a new collection platform. The new collection platform will maintain all crucial functionality of the current platform. We are in the process of installing that platform.

In order to minimize the potential impact of a disaster or other interruption of data or telephone communications that are critical to our business, we have:

| • | a diesel generator sufficient in size to power our entire Warren, Michigan headquarters, including our centralized systems; |

| • | a back-up server sufficient in size to handle our database located in a separate data center from the primary data center; |

| • | replication of data from the primary system to a backup system; |

| • | an ability to have inbound phone calls rerouted to other offices; |

| • | fire suppression systems in our primary and back-up data centers; |

10

Table of Contents

| • | redundant data paths to each of our call center offices and data centers; |

| • | daily back-up of all of our critical applications with the tapes transported offsite to a secure data storage facility; and |

| • | data replication in our primary server to preserve data in the event of a failure of a storage component. |

In addition, we have state-of-the-art dialer systems for incoming and outgoing calls that include call recording and messaging technology.

Regulation and Legal Compliance—Collection Activities

Federal, state and local statutes establish specific guidelines and procedures, which debt collection account representatives must follow when collecting consumer accounts. It is our policy to comply with the provisions of all applicable federal, state and local laws in all of our recovery activities. As such, we have established comprehensive procedures to ensure compliance with applicable federal, state and local collection laws. Failure to comply with these laws could lead to fines, suits and disruption of our collection activities that could have a material adverse effect on us.

Federal, state and local consumer protection, privacy and related laws and regulations extensively regulate the relationship between debt collectors and debtors. Significant federal laws and regulations applicable to our business as a debt collection company include the following:

| • | Fair Debt Collection Practices Act (“FDCPA”). This act imposes obligations and restrictions on the practices of consumer debt collectors, including specific restrictions regarding communications with debtors, including the time, place and manner of the communications. This act also gives consumers certain rights, including the right to dispute the validity of their obligations; |

| • | Fair Credit Reporting Act/Fair and Accurate Credit Transaction Act of 2003. The Fair Credit Reporting Act and its amendment entitled the Fair and Accurate Credit Transaction Act of 2003 (“FACT Act”) place requirements on credit information furnishers regarding verification of the accuracy of information furnished to credit reporting agencies and requires such information furnishers to investigate consumer disputes concerning the accuracy of such information. The FACT Act also requires certain conduct in the cases of identity theft or unauthorized use of a credit card and direct disputes to the creditor. We furnish information concerning our accounts to the three major credit-reporting agencies, and it is our practice to correctly report this information and to investigate credit-reporting disputes in a timely fashion; |

| • | The Financial Privacy Rule. Promulgated under the Gramm-Leach-Bliley Act, this rule requires that financial institutions, including collection agencies, develop policies to protect the privacy of consumers’ private financial information and provide notices to consumers advising them of their privacy policies. It also requires that if private personal information concerning a consumer is shared with another unrelated institution, the consumer must be given an opportunity to opt out of having such information shared. Since we do not share consumer information with non-related entities, except as required by law, or except as allowed by the rule in connection with our collection efforts, our consumers are not entitled to any opt-out rights under this rule. Both this rule and the Safeguards Rule described below are enforced by the Federal Trade Commission, which has retained exclusive jurisdiction over enforcement of them. Consumers do not have a private cause of action for violations of the Gramm-Leach-Bliley Act; |

| • | The Safeguards Rule. Also promulgated under the Gramm-Leach-Bliley Act, this rule specifies that we must safeguard financial information of consumers and have a written security plan setting forth information technology safeguards and the ongoing monitoring of the storage and safeguarding of electronic information; |

| • | Electronic Funds Transfer Act. This act regulates the use of the Automated Clearing House (“ACH”) system to make electronic funds transfers. All ACH transactions must comply with Federal Reserve |

11

Table of Contents

| Regulation E and the rules of the Electronic Payments Association, formerly the National Automated Check Clearing House Association (“NACHA”). This act, Regulation E and the NACHA regulations give the consumer, among other things, certain privacy rights with respect to the transactions, the right to stop payments on a pre-approved fund transfer, and the right to receive certain documentation of the transaction; |

| • | Telephone Consumer Protection Act. In the process of collecting on accounts, we use automated dialers to place calls to consumers. This act and similar state laws place certain restrictions on users of automated dialing equipment who place telephone calls to consumers; |

| • | Health Insurance Portability and Accountability Act (“HIPAA”)/Health Information Technology for Economical and Clinical Health Act (“HITECH”). HIPAA requires that healthcare institutions provide safeguards to protect the privacy of consumers’ healthcare information. As a debt buyer collecting on healthcare debt, we are considered a business associate to the healthcare institutions and are required to abide by HIPAA. HITECH increased HIPAA requirements relating to electronic security as well as consumer and public notification of security breaches; and |

| • | U.S. Bankruptcy Code. In order to prevent any collection activity with bankrupt debtors by creditors and collection agencies, the U.S. Bankruptcy Code provides for an automatic stay, which prohibits certain contact with consumers after the filing of bankruptcy petitions. |

Additionally, there are state and local statutes and regulations comparable to the above federal laws and other state and local-specific licensing requirements which affect our operations. State laws may also limit interest rates and fees, methods of collections, as well as the time frame in which judicial actions may be initiated to enforce the collection of consumer accounts. Court rulings in various jurisdictions also may impact our ability to collect.

Although we are not generally a credit originator, the following laws, which apply typically to credit originators, may occasionally affect our operations because our receivables were originated through credit transactions:

| • | Truth in Lending Act; |

| • | Fair Credit Billing Act; |

| • | Equal Credit Opportunity Act; |

| • | Retail Installment Sales Act; and |

| • | Credit Card Accountability Responsibility and Disclosure Act of 2009. |

Federal laws which regulate credit originators require, among other things, that credit card issuers disclose to consumers the interest rates, fees, grace periods and balance calculation methods associated with their credit card accounts. Consumers are entitled under current laws to have payments and credits applied to their accounts promptly, to receive prescribed notices, and to require billing errors to be resolved promptly. Some laws prohibit discriminatory practices in connection with the extension of credit. Federal statutes further provide that, in some cases, consumers cannot be held liable for, or their liability is limited with respect to, charges to the credit card account that were a result of an unauthorized use of the credit card. These laws, among others may limit our ability to recover amounts due on an account, whether or not we committed any wrongful act or omission in connection with the account. If the credit originator fails to comply with applicable statutes, rules and regulations, it could create claims and rights for consumers that could reduce or eliminate their obligations to repay the account, and have a possible material adverse effect on us. Accordingly, when we acquire charged-off consumer receivables, we typically require credit originators to represent and warrant that the receivables were originated and serviced in compliance with applicable laws, and indemnify us against certain losses that may result from their failure to comply with applicable statutes, rules and regulations relating to the receivables before they are sold to us.

12

Table of Contents

There are federal and state statues concerning identity theft or unauthorized use of a credit card. Some of these provisions place restrictions on our ability to report information concerning receivables, which may be subject to identity theft or unauthorized use of a credit card, to consumer credit reporting agencies. Additional consumer protection and privacy protection laws may be enacted that would impose additional requirements on the recovery of consumer credit card or installment accounts. Any new laws, rules or regulations that may be adopted, as well as existing consumer protection and privacy protection laws, may adversely affect our ability to collect on our charged-off consumer receivable portfolios. In addition, our failure to comply with these requirements could adversely affect our ability to recover the receivables and increase our costs.

It is possible that some of the receivables were established as a result of identity theft or unauthorized use. In such cases, we would not be able to recover the amount of the charged-off consumer receivables. As a purchaser of charged-off consumer receivables, we may acquire receivables subject to legitimate defenses on the part of the consumer. Most of our account purchase contracts allow us to return to the credit originators (within an agreed upon amount of time) certain charged-off consumer receivables that may not be collectible at the time of purchase, due to these and other circumstances. Upon return, the credit originators or debt sellers are required to replace the receivables with similar receivables or repurchase the receivables. These provisions limit, to some extent, our losses on such accounts.

Associates

As of December 31, 2009, we employed 1,758 associates, including 1,701 associates on a full-time basis and 57 associates on a part-time basis.

Training

We provide a comprehensive development training program for our new account representatives and continuing education opportunities for all associates via the Company’s learning center. Our training includes several learning approaches, including classroom interactive activities, computer-based training and on-the-job training. We also use our e-mail system and intranet to address on-going training issues.

New collection account representatives are required to complete an eight-week training program. The program is divided into two four-week modules. The initial four-week module has weekly objectives using various learning activities. The first week includes structured learning of our collection software and information technology tools, federal, state and local collection laws (with particular emphasis on the FDCPA and the FACT Act), telephone collection techniques and core company policies, procedures and practices. The second week continues the structured learning and is supplemented by supervised telephone collection calls. During weeks three and four, the new hires form a collection team, with a trainer as supervisor. Collection goals are established and collection calls are made and supervised. Instruction and guidance is shared with the new associates to improve productivity. Training includes discussion of challenges faced by associates and debriefing of the activities performed. Interactive activities are used to enhance collection and organization skills.

The second four-week training module transitions the collection team to the collection floor, where they are assigned productivity goals and work under the direction of a supervisor. This team of new hires continues to receive closely monitored training and reviews key elements from the first session.

New legal account representatives are required to complete a four-week training program. The first week of training is the same for legal account representatives as it is for collection account representatives. The second week of training focuses on legal processes and procedures and also includes supervised collection calls. Weeks three and four include closely supervised implementation of assigned duties.

All account representatives are tested annually on their knowledge of the FDCPA and other applicable laws. Account representatives not achieving our minimum standards are required to complete a FDCPA review session and are then retested. In addition, annual supplemental instruction in the FDCPA and collection techniques is provided to all our account representatives.

13

Table of Contents

| Item 1A. | Risk Factors |

This Report includes forward-looking statements as defined in the Private Securities Litigation Reform Act of 1995. In addition, we may make other written and oral communications from time to time that contain forward-looking statements. All statements regarding our expected financial position, strategies and growth prospects and general economic conditions we expect to exist in the future are forward-looking statements. The words “anticipates,” “believes,” “feels,” “expects,” “estimates,” “seeks,” “strives,” “plans,” “intends,” “outlook,” “forecast,” “position,” “target,” “mission,” “assume,” “achievable,” “potential,” “strategy,” “goal,” “aspiration,” “outcome,” “continue,” “remain,” “maintain,” “trend,” “objective,” and variations of such words and similar expressions, or future or conditional verbs such as “will,” “would,” “should,” “could,” “might,” “can,” “may” or similar expressions, as they relate to us or our management, are intended to identify forward-looking statements.

We caution that forward-looking statements are subject to numerous assumptions, risks and uncertainties, which change over time. Forward-looking statements speak only as of the date the statement is made, and we do not undertake to update forward-looking statements to reflect facts, circumstances, assumptions or events that occur after the date the forward-looking statements are made. Actual results could differ materially from those anticipated in forward-looking statements and future results could differ materially from historical performance.

In addition to factors mentioned elsewhere in this Report or previously disclosed in our SEC reports (accessible on the SEC’s website at www.sec.gov or on our website at www.assetacceptance.com), the factors contained below, among others, could cause actual results to differ materially from forward-looking statements, and future results could differ materially from historical performance.

Instability in the financial markets and a prolonged economic recession may affect our access to capital and our ability to purchase and collect receivables. High unemployment rates may negatively affect our collections of charged-off consumer receivables.

Our success depends on our continued ability to purchase and collect charged-off consumer receivables. The unemployment rate in the United States is the highest it has been since the 1980’s. In addition, the residential real estate market in the United States has experienced a significant downturn due to declining real estate values, precipitating credit market dislocations and a significant contraction in available liquidity. Individual consumers are experiencing high delinquency rates on various consumer loans and defaults on indebtedness of all kinds have increased compared to historical levels. We have been experiencing the impact of these economic factors on our collections. Continued depression or further declines in real estate values, continued high levels of unemployment and continuing credit and liquidity concerns could further reduce our ability to collect on our purchased consumer receivable portfolios and would adversely affect their value. In addition, continued or further credit market dislocations or sustained market downturns may reduce the ability of lenders to originate new credit, limiting our ability to purchase consumer receivable portfolios in the future. Financial pressure on the distressed consumer may lead to regulatory restrictions on our collections and increased litigation filed against us. We may be unable to predict the likely duration or severity of the adverse economic conditions and the effects they may have on our business, financial condition, results of operations, and cash flows.

Our access to capital through our credit agreement is critical to our ability to continue to grow. If our available credit is materially reduced or the credit agreement is terminated and we are unable to replace it on favorable terms or at all, our ability to purchase charged-off receivables and our results of operations may be materially and adversely affected.

We believe that access to capital through our credit agreement has been critical to our ability to maintain our operations. We have a $100.0 million revolving line of credit that expires June 5, 2012 and a $150.0 million term loan facility that matures on June 5, 2013. If our available credit is materially reduced or the credit agreement is terminated as a result of noncompliance with a covenant or other event of default and if we are unable to replace it on relatively favorable terms or at all, our ability to purchase charged-off receivables to generate revenue and cash flow and our results of operations may be materially and adversely affected.

14

Table of Contents

All of our receivable portfolios are pledged to secure amounts owed to our lenders under our credit agreement. In addition, our credit agreement imposes a number of restrictive covenants on how we operate our business. These include financial covenants. As of December 31, 2009, we had the ability to borrow approximately an additional $25.9 million under the most restrictive of these financial covenants. Our ability to meet these financial covenants is predicated on our ability to continue to generate revenues and other financial results at levels sufficient to satisfy the requirements of our credit agreement. Failure to satisfy any one of these covenants could result in all or any of the following consequences, each of which could have a material adverse effect on our ability to conduct business:

| • | acceleration of outstanding indebtedness; |

| • | our inability to continue to purchase charged-off receivables needed to operate our business; or |

| • | our inability to secure alternative financing on favorable terms, if at all. |

In addition, our credit agreement contains limitations and restrictions as to our ability to seek additional credit from other lenders, and requires that a portion of proceeds from issuance of our stock be used to pay down our term loan facility.

Negative attention and news regarding the debt collection industry and individual debt collectors may have a negative impact on a debtor’s willingness to pay the debt we acquire.

The following factors may cause consumers to be more reluctant to pay their debts or to pursue legal actions against us:

| • | Annually the Federal Trade Commission submits a report to Congress, which summarizes the complaints it has received regarding debt collection practices. The report contains the total number of complaints filed, the percentage of increases or decreases from the previous year in addition to an outline of key types of complaints. |

| • | Print and television media, from time to time, may publish stories about the debt collection industry which may cite specific examples of abusive collection practices. These stories are also published on websites, which can lead to the rapid dissemination of the story adding to the level of exposure to negative publicity about us or the industry. |

| • | The Internet has websites where consumers list their concerns about the activities of debt collectors and seek guidance from other website posters on how to handle various situations. |

| • | Advertisements by “anti-collections” attorneys and credit counseling centers are becoming more common and add to the negative attention given to our industry. |

As a result of this negative publicity, debtors may be more reluctant to pay their debts or could pursue legal action against us regardless of whether those actions are warranted. These actions could impact our ability to collect on the receivables we acquire and impact our ability to operate profitably.

Our ability to recover on our charged-off consumer receivables may be limited under federal, state and local laws.

Federal and state consumer protection, privacy and related laws and regulations extensively regulate the relationship between debt collectors and debtors. Federal and state laws may limit our ability to recover on our charged-off consumer receivables regardless of any act or omission on our part. Some laws and regulations applicable to credit card issuers may preclude us from collecting on charged-off consumer receivables we purchase if the credit card issuer previously failed to comply with applicable law in generating or servicing those receivables. Additional consumer protection and privacy protection laws may be enacted that would impose additional or more stringent requirements on the enforcement of and collection on consumer receivables.

15

Table of Contents

New federal, state or local laws or regulations, or changes in the ways these rules or laws are interpreted or enforced, could limit our activities in the future or significantly increase the cost of regulatory compliance. Any new laws, rules or regulations that may be adopted, as well as existing consumer protection and privacy protection laws, may adversely affect our ability to collect on our charged-off consumer receivable portfolios and may have a material adverse effect on our business and results of operations. In addition, federal and state governmental bodies are considering, and may consider in the future, other legislative proposals that would regulate the collection of consumer receivables. The Federal Trade Commission has proposed amendments to the Fair Debt Collection Practices Act that, if enacted, may adversely affect our business and results of operations. Although we cannot predict if or how any future legislation would impact our business, our failure to comply with any current or future laws or regulations applicable to us could limit our ability to collect on our charged-off consumer receivable portfolios, which could reduce our profitability and harm our business.

In addition to the possibility of new laws being enacted, it is possible that regulators and litigants may attempt to extend debtors’ rights beyond the current interpretations placed on existing statutes. These attempts could cause us to (i) expend significant financial and human resources in either litigating these new interpretations or (ii) alter our existing methods of conducting business to comply with these interpretations, either of which could reduce our profitability and harm our business.

Failure to comply with government regulation could result in the suspension or termination of our ability to conduct business and the imposition of financial penalties.

The collections industry is regulated under various federal and state laws and regulations. Many states and several cities require that we be licensed as a debt collection company. The Federal Trade Commission, state Attorneys General and other regulatory bodies have the ability to investigate consumer complaints against debt collection companies and to recommend enforcement actions and seek monetary penalties. If we fail to comply with applicable laws and regulations, it could result in significant penalties or the suspension or termination of our ability to conduct collection operations, which could materially adversely affect us.

A significant portion of our collections relies upon our success in individual lawsuits brought against consumers and our ability to collect on judgments in our favor.

We generate a significant portion of our revenue by collecting on judgments that are granted by courts in lawsuits filed against debtors. A decrease in the willingness of courts to grant such judgments, a change in the requirements for filing such cases or obtaining such judgments, or a decrease in our ability to collect on such judgments could have a material and adverse effect on our results of operations. As we increase our use of the legal channel for collections, our short-term margins may decrease as a result of an increase in upfront court costs and costs related to counter claims. We may not be able to collect on certain aged accounts because of applicable statues of limitations and we may be subject to adverse effects of regulatory changes that we cannot predict.

We are subject to ongoing risks of litigation, including individual and class actions under consumer credit, collections, and other laws.

We operate in an extremely litigious industry and currently are, and may in the future, be named as defendants in litigation, including individual and class actions under consumer credit, collections, and other laws.

Our operations could suffer from telecommunications or technology downtime or from not responding to changes in technology. We are converting our legacy debt collection platform to a different software system. A failure to convert our debt collection platform successfully could materially impair our ability to conduct our business.

Our success depends in large part on sophisticated telecommunications and computer systems. The temporary or permanent loss of our computer and telecommunications equipment and software systems, through

16

Table of Contents

casualty or operating malfunction (including outside influences such as computer viruses), could disrupt our operations. In the normal course of our business, we must record and process significant amounts of data quickly and accurately. Any failure of our information systems or software and their backup systems would interrupt our operations and harm our business. In addition, we rely significantly on various outside vendors for the software used in operating our current collections platform. Our business operations would be disrupted and our results of operations may be harmed if they were to cease operations or significantly reduce their support to us. We endeavor to deploy state-of-the-art technology across our infrastructure and, as warranted, will upgrade that technology over time.

We are in the process of converting our legacy debt collection platform to a different software system, supported by a different third party vendor. Failure to execute successfully the conversion to and implementation of that new debt collection platform will exacerbate the risks identified above and could materially impair our ability to collect our receivables and otherwise conduct our business. During times of transition, risk exists in decommissioning existing applications and hardware and the implementation of new applications and hardware. Failure to accurately identify and mitigate that risk could have a significant impact on our operational capabilities.

We are subject to examinations and challenges by tax authorities.

Our industry is relatively new and unique and, as a result, there is not a set of well defined laws, regulations or case law for us to follow that match our particular facts and circumstances for some tax positions. Therefore, certain tax positions we take are based on industry practice, tax advice and drawing similarities of our facts and circumstances to those in case law relating to other industries. These tax positions may relate to tax compliance, sales and use, franchise, gross receipts, payroll, property and income tax issues, including tax base and apportionment. Challenges made by tax authorities to our application of tax rules may result in adjustments to the timing or amount of taxable income or deductions or the allocation of income among tax jurisdictions, as well as, inconsistent positions between different jurisdictions on similar matters. If any such challenges are made and are not resolved in our favor, they could have an adverse effect on our financial condition and result of operations.

We are dependent on our management team for the adoption and implementation of our strategies and the loss of their services could have a material adverse effect on our business.

Our future success depends on the continued ability to recruit, hire, retain and motivate highly skilled management. The continued growth and success of our business is particularly dependent upon the continued services of our executive officers, including our Chief Executive Officer and our Chief Acquisitions Officer, each of whom is integral to the development of our business. Our performance also depends on our ability to retain and motivate our other executives. The loss of the services of one or more of our executive officers or other key associates could disrupt our operations and impair our ability to continue to acquire or collect on portfolios of charged-off consumer receivables and to manage and expand our business. We have employment agreements with each of our Chief Executive Officer, Chief Acquisitions Officer and Chief Financial Officer. However, these agreements do not and will not assure the continued services of these officers. On January 8, 2010, our Chief Financial Officer provided notice of resignation and has agreed to continue in his role as an officer and associate while we work towards identifying and retaining a successor. We do not maintain key person life insurance policies for our executive officers or key associates.

If we are not able to purchase charged-off consumer receivables at appropriate prices or in sufficient amounts, the resulting decrease in our inventory of purchased portfolios of receivables could adversely affect our ability to generate cash collections and income.

If we are unable to purchase charged-off consumer receivables from credit originators in sufficient face value amounts at appropriate prices, our business may be harmed. The availability of portfolios of consumer

17

Table of Contents

receivables at prices which generate an appropriate return on our investment depends on a number of factors, both within and outside of our control, including:

| • | our ability to borrow to fund purchases; |

| • | the absence of significant contraction in the levels of credit being extended by credit originators; |

| • | the absence of significant contraction in the levels of consumer obligations; |

| • | charge-off rates; |

| • | continued growth in the number of industries selling charged-off consumer receivable portfolios; |

| • | continued sales of charged-off consumer receivable portfolios by credit originators; |

| • | competitive factors affecting potential purchasers and credit originators of charged-off receivables, including the number of firms engaged in the collection business and the capitalization of those firms, as well as new entrants seeking returns, that may cause an increase in the price we are willing to pay for portfolios of charged-off consumer receivables or cause us to overpay for portfolios of charged-off consumer receivables. |

In addition, we believe that credit originators and debt sellers are utilizing more sophisticated collection methodologies that result in lower quality portfolios available for purchase, which may render the portfolios available for sale less collectible.

Because of the length of time involved in collecting charged-off consumer receivables on acquired portfolios and the volatility in the timing of our collections, we may not be able to identify trends and make changes in our purchasing or collection strategies in a timely manner.

We generally account for purchased receivable revenues using the interest method of accounting in accordance with generally accepted accounting principles, which requires making reasonable estimates of the timing and amount of future cash collections. If the timing is delayed or the actual amount recovered by us is materially different from our estimates, it could cause us to recognize impairments and negatively impact our earnings.

The estimates used in the interest method (“Interest Method”) to calculate the projected internal rate of return (“IRR”) on our portfolios are primarily based on historical cash collections and payer dynamics. If actual future cash collections are materially different in amount or timing than the remaining collections estimate, earnings could be affected, either positively or negatively. Higher collection amounts or cash collections that occur sooner than projected will have a favorable impact on reversal of impairments or an increase in yields and revenues. Higher than projected collections could also have a short term impact of increased amortization, which results in lower net income. Lower collection amounts or cash collections that occur later than projected will have an unfavorable impact and result in an impairment of the purchased receivable balance. Impairments may cause reduced earnings or volatility in earnings which could have the effect of depressing the price per share of our common stock and reducing our Consolidated Tangible Net Worth and put pressure on the financial covenants in our Credit Facilities. Refer to “Critical Accounting Policies—Revenue Recognition” on page 50 for further information regarding the Interest Method and estimates.

We may not be able to collect sufficient amounts on our charged-off consumer receivables, which would adversely affect our results of operations, our ability to satisfy debt obligations, our purchase of new portfolios and our future growth.

Our business consists of acquiring and collecting receivables that consumers have failed to pay and that the credit originator has deemed uncollectible and has charged-off. The credit originators or other debt sellers generally have attempted to recover on their charged-off consumer receivables before we purchase such

18

Table of Contents

receivables, often using a combination of in-house recovery and third party collection efforts. Since there generally have been multiple efforts to collect on these portfolios of charged-off consumer receivables before we attempt to collect on them (three or more efforts on more than 50% of the face value of our portfolios), our attempts to collect on these portfolios may not be successful. Therefore, we may not collect a sufficient amount to cover our investment associated with purchasing the charged-off consumer receivable portfolios and the costs of running our business, which would adversely affect our results of operations. In addition, if cash flows from operations are less than anticipated, our ability to satisfy our debt obligations, purchase new portfolios and our future growth and profitability may be materially and adversely affected.

There can be no assurance that our success in generating collections in the past will be indicative of our ability to be successful in generating collections in the future.

We are highly dependent on revenues generated from our purchased receivable collection activities. Entry into new markets or other attempts to diversify our business model may not be successful.

Substantially all our operating revenues are generated from collections on charged-off purchased receivables. Although we use multiple collection approaches, changing economic factors or collection laws, for example, may impact our ability to collect regardless of the collection approach we pursue. Although, management may seek opportunities to diversify, we may not be successful.

We experience high turnover rates for our account representatives. We may not be able to hire and retain enough sufficiently trained account representatives to support our operations.

Our ability to collect on new and existing portfolios and to acquire new portfolios is substantially dependent on our ability to hire and retain qualified associates. The consumer accounts receivables management industry is labor intensive and, similar to other companies in our industry, we experience a high rate of associate turnover. For 2009, our annual turnover rate was 45.4% and our collection department associate turnover rate was 60.6%. Based on our experience, account representatives who have been with us for more than one year are generally more productive than account representatives who have been with us for less than one year. In 2009, our turnover rate for all associates employed by us for at least one year was 29.4% and 38.5% for collection department associates. We compete for qualified associates with companies in our industry and in other industries. Our operations require that we continually hire, train and, in particular, retain account representatives. In addition, we believe the level of training we provide to our associates makes them attractive to other collection companies, which may attempt to recruit them. A higher turnover rate among our account representatives will increase our recruiting and training costs, may require us to increase associate compensation levels and will limit the number of experienced collection associates available to service our charged-off consumer receivables. If this were to occur, we may not be able to service our charged-off consumer receivables effectively, which could reduce our ability to operate profitably.

Significant increases in interest rates could adversely impact our financial position, results of operations and cash flows.

Our credit agreement bears interest at 150 to 250 basis points over prime or 250 to 350 basis points over the London Inter Bank Offer Rate. Although a portion of our outstanding borrowings have a fixed rate of interest resulting from a swap agreement, a portion is not fixed. In addition, in the future, we may amend our credit agreement, which could significantly impact the rates of interest we pay. As a result of these factors, fluctuations in interest rates may adversely impact our financial position, results of operations and cash flows.

We face intense competition that could impair our ability achieve our goals.

The consumer debt collection industry is highly competitive and fragmented. We compete with a wide range of other purchasers of charged-off consumer receivables, third party collection agencies, other financial service companies and credit originators and other owners of debt that manage their own charged-off consumer

19

Table of Contents

receivables. Some of these companies may have substantially greater numbers of associates and financial resources and may experience lower account representative turnover rates than we do. Furthermore, some of our competitors may obtain alternative sources of financing, the proceeds from which may be used to fund expansion and to increase their number of charged-off portfolio purchases. Barriers to entry into the consumer debt collection industry are low. Companies with greater financial resources than we have may elect at a future date to enter the consumer debt collection business. Competitive pressures affect the availability and pricing of receivable portfolios as well as the availability and cost of qualified debt collection account representatives. In addition, some of our competitors have signed forward flow contracts under which consumer credit originators have agreed to transfer a steady flow of charged-off receivables to them in the future, which could restrict those credit originators from selling receivables to us.

We face bidding competition in our acquisition of charged-off consumer receivable portfolios. We believe successful bids generally are awarded based predominantly on price and to a lesser extent based on service and relationships with the debt sellers. Some of our current competitors, and possible new competitors, may have more effective pricing and collection models, greater adaptability to changing market needs and more established relationships in our industry than we have. Moreover, our competitors may elect to pay prices for portfolios that we determine are not reasonable and, in that event, our volume of portfolio purchases may be diminished. There can be no assurance that our existing or potential sources will continue to sell their charged-off consumer receivables at recent levels or at all, or that we will continue to offer competitive bids for charged-off consumer receivable portfolios. In addition, there continues to be a consolidation of issuers of credit cards, which have been a principal source of our receivable purchases. This consolidation has decreased the number of sellers in the market and, consequently, could over time, give the remaining sellers increasing market strength in the price and terms of the sale of charged-off credit card accounts and could cause us to accept lower returns on our investment in that paper than we have historically achieved.

If we are unable to develop and expand our business or adapt to changing market needs as well as our current or future competitors, we may experience reduced access to portfolios of charged-off consumer receivables in sufficient face-value amounts at appropriate prices. As a result, we may experience reduced profitability which, in turn, may impair our ability to achieve our goals.

Our strategy includes acquiring charged-off receivable portfolios in industries in which we may have little or no experience. If we do not successfully acquire and collect on these portfolios, revenue may decline and our results of operations may be materially and adversely affected.

We may acquire portfolios of charged-off consumer receivables in industries in which we have limited experience. Some of these industries may have specific regulatory restrictions with which we have no experience. Our limited experience in these industries may impair our ability to effectively and efficiently collect on these portfolios. Furthermore, we need to develop appropriate pricing models for these markets, and there is no assurance that we will do so effectively. When pricing charged-off consumer receivables for industries in which we have limited experience, we attempt to adjust our models for expected or known differences from our traditional models. However, our pricing models are primarily based on historical data for industries in which we do have experience. This may cause us to overpay for these portfolios, and consequently, our profitability may suffer as a result of these portfolio acquisitions.

Our operating results and cash collections may vary from quarter to quarter.

Our business depends on the ability to collect on our portfolios of charged-off consumer receivables. Collections within portfolios tend to be seasonally higher in the first and second quarters of the year, due to consumers’ receipt of tax refunds and other factors. Conversely, collections within portfolios tend to be lower in the third and fourth quarters of the year, due to consumers’ spending in connection with summer vacations, the holiday season and other factors. Operating expenses are seasonally higher during the first and second quarters of the year due to expenses necessary to process the increase in cash collections. However, revenue recognized is

20

Table of Contents

relatively level due to our application of the Interest Method for revenue recognition. In addition, our operating results may be affected to a lesser extent by the timing of purchases of portfolios of charged-off consumer receivables due to the initial costs associated with purchasing and integrating these receivables into our system. Consequently, income and margins may fluctuate from quarter to quarter.

Our collections may decrease if bankruptcy filings increase or if bankruptcy laws change.

During times of economic recession, the amount of charged-off consumer receivables generally increases, which contributes to an increase in the number of personal bankruptcy filings. Under certain bankruptcy filings, a debtor’s assets are sold to repay creditors, but since the charged-off consumer receivables we are attempting to collect are generally unsecured or secured on a second or third priority basis, we often would not be able to collect on those receivables. Our collections may decline with an increase in bankruptcy filings or if the bankruptcy laws change in a manner adverse to our business, in which case, our financial condition and results of operations could be materially adversely affected.

Our common stock trades at a relatively low average daily volume. Consequently, sales of our common stock by one or more of our larger shareholders could depress the price of our common stock.