Attached files

| file | filename |

|---|---|

| EX-21 - SUBSIDIARIES - PRIMEDIA INC | dex21.htm |

| EX-23 - DELOITTE & TOUCHE LLP CONSENT - PRIMEDIA INC | dex23.htm |

| EX-32.1 - CEO 906 CERTIFICATIONS - PRIMEDIA INC | dex321.htm |

| EX-32.2 - CFO 906 CERTIFICATIONS - PRIMEDIA INC | dex322.htm |

| EX-31.2 - CFO 302 CERTIFICATIONS - PRIMEDIA INC | dex312.htm |

| EX-31.1 - CEO 302 CERTIFICATIONS - PRIMEDIA INC | dex311.htm |

Table of Contents

Index to Financial Statements

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended: December 31, 2009

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File number: 1-11106

PRIMEDIA Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 13-3647573 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| 3585 Engineering Drive, Norcross, Georgia | 30092 | |

| (Address of principal executive offices) | (Zip Code) |

(678) 421-3000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class |

Name of Each Exchange on Which Registered | |

| Common Stock, par value $0.01 per share | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company (as defined in Exchange Act Rule 12b-2).

Large accelerated filer ¨ Accelerated filer ¨ Non-accelerated filer ¨ Smaller reporting company x

Indicate by check mark whether the registrant is a shell company Yes ¨ No x

The aggregate market value of the voting common equity of PRIMEDIA Inc. (“PRIMEDIA”) which is held by non-affiliates of PRIMEDIA, computed by reference to the closing price as of the last business day of the registrant’s most recently completed second fiscal quarter, June 30, 2009, was approximately $34.9 million. The registrant has no non-voting common stock.

As of March 1, 2010, 44,146,959 shares of PRIMEDIA’s Common Stock were outstanding.

The following documents are incorporated into this Form 10-K by reference: Part III of this Report on Form 10-K incorporates information by reference from the registrant’s Proxy Statement for its 2010 Annual Meeting of Stockholders to be held on May 19, 2010. The definitive Proxy Statement will be filed within 120 days of the end of the fiscal year ended December 31, 2009.

Table of Contents

Index to Financial Statements

Annual Report on Form 10-K

December 31, 2009

Table of Contents

We include cross references to captions elsewhere in this Annual Report on Form 10-K, which we refer to as this “Report,” where you can find related additional information. The following table of contents tells you where to find these captions.

| Page | ||||

| 1 | ||||

| PART I | ||||

| Item 1. |

1 | |||

| Item 1A. |

7 | |||

| Item 1B. |

12 | |||

| Item 2. |

12 | |||

| Item 3. |

12 | |||

| Item 4. |

12 | |||

| PART II | ||||

| Item 5. |

14 | |||

| Item 6. |

15 | |||

| Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

17 | ||

| Item 7A. |

44 | |||

| Item 8. |

45 | |||

| Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

92 | ||

| Item 9A. |

92 | |||

| Item 9B. |

96 | |||

| PART III | ||||

| Item 10. |

96 | |||

| Item 11. |

96 | |||

| Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

96 | ||

| Item 13. |

Certain Relationships and Related Transactions and Director Independence |

96 | ||

| Item 14. |

96 | |||

| PART IV | ||||

| Item 15. |

97 | |||

| 98 | ||||

| S-1 | ||||

| E-1 | ||||

i

Table of Contents

Index to Financial Statements

IMPORTANT INFORMATION ABOUT THIS REPORT

In this Report, the words “PRIMEDIA,” “Company,” “we,” “us” and “our” mean PRIMEDIA Inc., including its subsidiaries, unless the context otherwise specifies or requires.

This document contains “forward-looking statements”—that is, statements related to future, not past, events. In this context, forward-looking statements often address our expected future business and financial performance and often contain words such as “expects,” “anticipates,” “intends,” “plans,” “believes,” “seeks” or “will.” Forward-looking statements by their nature address matters that are, to different degrees, uncertain. For us, particular uncertainties which could adversely or positively affect our future results include, among others: general economic trends and conditions and, in particular, trends and conditions in the apartment and other rental property and new home sales sectors of the residential real estate industry; changes in technology and competition; implementation and results of our ongoing strategic initiatives; demand by customers for our services; expenses or adverse results of litigation; changes in U.S. federal tax laws; and numerous other matters of national, regional and local market scale, including those of a political, economic, business, competitive and regulatory nature. These uncertainties may cause our actual future results to be materially different than those expressed in our forward-looking statements. We do not undertake to update our forward-looking statements.

| ITEM 1. | BUSINESS |

General

We are a targeted media company that provides consumers with tools and information they need to find a place to live. Our consumer directories are targeted primarily for the apartment and other rental property sectors of the residential real estate industry and are provided free to consumers through online, print and mobile platforms. We derive advertising revenue by providing our advertiser clients – property management companies, private owner/landlords, new home builders and real estate professionals – with products and services that generate measurable results in the form of cost-effective, quality leads.

Our principal digital assets include ApartmentGuide.com, Rentals.com, RentalHouses.com, NewHomeGuide.com and AmericanHomeGuides.com. According to comScore Media Metrix, unique visitors to our websites reached 3.3 million in January 2010, compared with 3.1 million in January 2009. The total number of leads we produce for our advertisers has grown year over year, and leads derived from our online and mobile services now represent more than 75% of the total leads we deliver to our advertiser clients.

We produce printed directories for 75 markets and distribute them through display rack programs, many of which are on an exclusive basis, with large national and regional retail chains, including grocery, drug, convenience, video, fitness and mass merchandise retailers. In 2009, we distributed approximately 14.9 million printed directories to approximately 17,000 advertiser client locations and 28,000 retail and other locations.

Over the past several years, we have aggressively divested assets no longer part of our core businesses. Our continuing operations are currently comprised solely of what we have described historically as our Consumer Guides segment.

Apartments

Our Apartments division comprised approximately 91.7% of our advertising revenue for 2009 and 93.1% of our advertising revenue for fourth quarter 2009.

Apartment Guide

Thirty-five years old, Apartment Guide, our flagship brand and largest business, delivers apartment and apartment community rental information to consumers through a combination of Internet, print and mobile

1

Table of Contents

Index to Financial Statements

products and services. ApartmentGuide.com and RentRentar.com, our Spanish-language edition of ApartmentGuide.com, offer many premium features not available through our printed directories, including flexible search functionality, detailed photos and floorplans, virtual tours, as well as detailed information on metro areas and neighborhoods. Our ApartmentGuide.com mobile platform continues to expand through launches of iPhone and Android applications, which together have generated over 541,000 downloads through January 2010.

We currently produce 77 Apartment Guide printed directories in 75 markets, averaging over 17,000 apartment community listings in print – over 40% more listings than our nearest print competitor within these markets – with a 2009 distribution of approximately 12.0 million copies. Most of our Apartment Guide printed directories are published monthly, though we expect to move to bi-monthly publishing schedules for some of our markets.

We continued to reinforce our commitment to industry-leading innovation in 2009 with the launch of My.ApartmentGuide.com. Feedback from our advertiser clients has confirmed our view that My.ApartmentGuide.com is a valuable, unique ROI-based management tool that enables our clients to measure the cost-effectiveness and other performance metrics of the rental search and lead-generation process. We also released version 2.0 of our iPhone application and launched our initial Android application in 2009.

Apartment Guide advertising revenue is generated primarily from property management companies that manage larger apartment communities (generally in excess of 50 units) that experience ongoing vacancies. A majority of our 2009 revenue was derived from contracts at least 12 months in duration, and a majority of these contracts were renewed when they expired. Most of our property management company clients purchase integrated media packages that include online, mobile and print advertising. However, as we continue to pursue enhancements to our product portfolio and market segment expansion to grow our customer count, we are providing more flexibility to clients, based on specific markets and market segments, to purchase more customized mixes of products, product features and services on a stand-alone or package basis.

Apartment Guide’s national competitors include Rent.com (owned by eBay), Apartments.com (owned by Classified Media Ventures), For Rent (published by Dominion Enterprises), Apartment Finder (published by Network Communications Inc.) and, to a lesser extent, Move.com (owned by Move, Inc.) and craigslist.org (owned by craigslist, Inc.).

Rentals.com

Rentals.com is a comprehensive real estate rental site with one of the largest collections of single-unit rental property listings on the Internet. The Rentals.com Network of Sites, which includes Rentals.com and RentalHouses.com, averaging more than 33,000 listings, including approximately 28,000 distribution partner listings, of single-family homes, townhomes, condos and smaller apartment communities, as well as select inventory of apartments from ApartmentGuide.com. Our advertiser clients use Rentals.com and RentalHouses.com to list their rental vacancies, including through the self-provisioning feature of the website we call the “Ad Store,” and peruse the expert advice and tips on managing their rental properties offered on our websites. A majority of our customers are derived from the Ad Store, while a majority of our listings are derived from property management companies.

Advertising revenue is generated primarily from private owner/landlords, investors and property managers that own or manage single-unit rental properties or smaller apartment communities (generally less than 50 units) that experience vacancies intermittently. Listings on the Rentals.com and RentalHouses.com Network of Sites are generally purchased on a monthly basis, though longer-term packages are available for property management company clients. In some of its markets, advertisers purchase basic and premium listings. In all other markets, basic listings are provided free of charge, with premium upgrades available for charges that vary by category and market.

2

Table of Contents

Index to Financial Statements

Competitors of Rentals.com and RentalHouses.com include craigslist.org (owned by craigslist, Inc.), HomeRentals.net (owned by RealEIS, LLC), RentalHomesPlus.com (owned by Classified Ventures LLC), Move.com (owned by Move, Inc.) and, to a lesser extent, traditional newspapers.

New Homes

Our New Homes division, comprising approximately 8.3% of our advertising revenue for 2009 and 6.9% of our advertising revenue for fourth quarter 2009, provides display and classified advertising for new home builders to showcase product and inventory on a national and local basis through a network of home-related websites, including NewHomeGuide.com, AmericanHomeGuides.com, NewHomeDirectory.com, FloridaGuide.com, and many others specific to states and metropolitan areas with significant home building activity. In addition, as of December 31, 2009, New Homes produced 21 printed directories, averaging over 2,100 new home community listings in print, with a combined 2009 distribution of approximately 3.0 million copies. New Homes printed directories generally are published bi-monthly.

New Homes advertising revenue is generated primarily from new home builders and advertising agencies representing new home builders. Most of our clients purchase integrated media packages that include online, mobile and print advertising. However, our products and services are offered nationwide on a stand-alone or package basis.

Our New Homes division competes primarily with national competitors such as Move.com (owned by Move, Inc.), New Home Finder (published by Network Communications, Inc.), Housing Guide of America (owned by a consortium of local and regional magazine publishers), newhomesource.com (owned by Builder Homesite, Inc.) and the iNest real estate brokerage (owned by Lending Tree, LLC).

Distribution

In 2009, our distribution function, DistribuTech, distributed free publications, including PRIMEDIA’s directories and over 1,800 third-party titles, flyers and special piece advertising materials, to more than 28,000 retail locations and 17,000 PRIMEDIA advertiser client locations in 39 states and Washington, D.C. DistribuTech maintains display rack programs, many of which are on an exclusive basis, which we refer to as retail display allowances, or RDAs, with several large national and regional retail chains. The free directories are typically displayed in free-standing, multi-pocket racks located in high-visibility, high-traffic locations at the entrance or exit of these locations.

The primary function of DistribuTech is to ensure priority placement for PRIMEDIA’s directories through RDAs and to reduce our overall distribution costs through revenue from third-party customers who pay DistribuTech for distribution services. Historically, we have paid substantial premiums for the exclusive nature of many of our RDAs, which has contributed to relatively high fixed costs within this function. In addition, over the past three years, we have experienced substantial declines in revenue from third-party DistribuTech customers that have scaled back or ceased operations or are providing an Internet-only product.

Beginning in 2008, we undertook strategic initiatives to significantly reduce the cost structure of our distribution function, including the relatively high costs of RDAs. During 2009, we implemented a plan to further reduce our ongoing distribution costs arising from RDAs that were underperforming, and as a result, our distribution costs decreased from $85.2 million in 2008 to $60.9 million in 2009. We intend to continue aggressively reducing our distribution cost structure.

Our overall distribution strategy is to reduce our print distribution costs as we devote greater resources to opportunities for growth that digital media present and eliminate less effective locations, while focusing our efforts on retaining and servicing locations that produce the best results for PRIMEDIA’s advertisers in terms of leads. We intend to move to a smaller, more efficient distribution model that primarily relies on third-party distribution services, in combination with more limited internal resources, to deliver our directories.

3

Table of Contents

Index to Financial Statements

Technology

We use technology to improve our operations by increasing productivity, improving effectiveness and minimizing costs. With the introduction of mobile technologies, such as wireless data networks and laptop/handheld technologies, the use of technology has expanded within our organization to include customer relationship management activities and business workflow functionality.

We back up critical website data at various times throughout the day and retain it at certified third-party facilities. We have firewalls and switchgear designed to help ensure network security. We rely increasingly on hosted providers for many of our corporate applications. These applications are provided over our network to us and configured to meet our needs, although the software itself is not installed at our locations.

Production and Fulfillment

We provide most of the content for our websites, but we outsource some technology, production and content. All of our printed directories are printed and bound by independent printers. The principal raw material used in our printed directories is paper, which is purchased from merchants. In 2009, paper prices declined as the year progressed. We expect paper costs to increase slightly in 2010, and we expect to offset these costs through adjustment of our production metrics. In the future, our results could be adversely affected by increases in paper prices.

Sales and Marketing

Because our directories are free to users, we compete for audience on the basis of the relevance and usefulness of our search results and the features, availability and ease of use of our tools and information. Our websites are marketed to end users through our printed directories and through search engine optimization, e-mail marketing and online advertising, which we purchase on a non-exclusive basis with companies such as Google, MSN, Yahoo!, Advertising.com and others. We monetize visits to our websites through various advertising revenue formats, such as cost per impression, cost per click, cost per action and flat fees, which comprise the substantial majority of our advertising revenue.

We sell our advertising products and services to our advertiser clients through our direct sales force. Our sales force is comprised currently of approximately 460 sales people. The sales force is generally organized vertically, focusing on specific categories and product lines, and by market. Generally, sales people are responsible for developing new accounts and servicing existing customers. Most of our sales people live in the market they serve. We also maintain an in-house telemarketing sales force, supplemented by local and regional support in the field, which focuses on specific customer segments within markets.

Our marketing personnel conduct a variety of marketing programs designed to raise the general awareness of our businesses, generate leads for the sales organization and promote our various product lines. These programs include participation in trade shows and industry trade groups, public relations, digital/online promotion, advertising and production of collateral literature.

In 2009, more than 74% of our Internet audience was generated through non-paid sources, such as repeat visitation, word-of-mouth, natural search and public relations. We selectively utilize paid-marketing sources, such as search engine marketing, affiliate relationships and co-branded partner deployments.

One of our individual advertisers comprised 1.5% of our total revenue in 2009, while another comprised 1.3%. All of our other individual advertisers comprised less than 1.0% of our total revenue in 2009.

Employees

During 2009, our overall headcount declined by approximately 9.0%, primarily due to the elimination of certain administrative and support positions as a result of automation and consolidation of functions. Our sales force

4

Table of Contents

Index to Financial Statements

headcount also declined by 7.9%. As of December 31, 2009, we had approximately 900 employees, of which approximately 20 were part-time, compared to approximately 1,000 employees at the end of 2008, of which approximately 20 were part-time. Our employees are not represented by any collective bargaining agreements. We consider our relations with our employees to be good.

Intellectual Property

We own various registered trademarks, including Apartment Guide, and have service mark applications pending for others. We also have the right to use a number of unregistered service marks in connection with our businesses. So long as these marks remain in continuous use in connection with similar goods and services, their terms can be perpetual, subject, with respect to registered trademarks, to the timely renewal of such registrations in the United States Patent and Trademark Office. Most of our content and databases are copyrighted, as are certain of our software and user manuals. The absence of a registration does not waive copyright protection.

5

Table of Contents

Index to Financial Statements

Discontinued Operations

Over the past several years, we have aggressively sought to divest assets no longer part of our current core businesses. Details about our divestitures during the years ended December 31, 2008 and 2007 are as follows:

| Consideration |

Pre-tax Gain or Loss on Disposition Recognized During the Years Ended December 31, |

|||||||||||||||||

| Segment, Group or Division |

Year of |

Basis for |

Year of |

Form |

Amount | 2008 | 2007(1) | |||||||||||

| (Dollars in thousands) | ||||||||||||||||||

| Outdoors group (part of Enthusiast Media (“PEM”) segment), primarily hunting, fishing and shooting titles |

2006 | Agreement to sell | 2007 | Cash | $ | 170,000 | $ | — | $ | 57,547 | ||||||||

| Channel One (part of Education segment), proprietary network for secondary schools |

2006 | Announcement of intent to sell segment | 2007 | Assumption by the acquirer of net liabilities | 8,600 | — | (7,050 | ) | ||||||||||

| Films Media Group (part of Education segment), a source of educational video |

2006 | Announcement of active pursuit of sale of segment | 2007 | Cash | 11,000 | — | 170 | |||||||||||

| PRIMEDIA Healthcare (part of Education segment), a medical education business(2) |

2006 | Announcement of active pursuit of sale of segment | 2008 | Cash | 200 | 132 | — | |||||||||||

| Enthusiast Media segment(3)(4) |

2007 | Sale of segment | 2007 | Cash | 1,177,900 | — | 460,988 | |||||||||||

| Auto Guides division(5) |

2007 | Announcement of intent to sell or shut down operations of division | 2008 | Cash | 2,100 | 42 | — | |||||||||||

| (1) | Loss related to final adjustments for disposition in previous years was approximately $0.7 million in 2007. |

| (2) | Remaining operations were shut down, resulting in a loss of approximately $0.4 million. |

| (3) | Proceeds were used to pay down debt |

| (4) | Gain related to final adjustments was approximately $0.7 million in 2008 and resulted in payment of approximately $4.4 million to acquirer. |

| (5) | Remaining operations were shut down, resulting in a loss of approximately $0.8 million. |

6

Table of Contents

Index to Financial Statements

There was no pre-tax gain or loss on disposition recognized during the year ended December 31, 2009.

As of December 31, 2009 and 2008, there were no assets or liabilities of businesses held for sale.

The financial results for all divestitures are reported as discontinued operations in the consolidated statement of operations for all periods presented and are more fully discussed in Item 7—“Management’s Discussion and Analysis of Financial Condition and Results of Operations,” of this Report.

Company Organization

PRIMEDIA Inc. was incorporated on November 22, 1991 in the State of Delaware as K-III Communications Corporation, and in 1997, we changed our name to PRIMEDIA Inc. Our principal executive offices are located at 3585 Engineering Drive, Norcross, Georgia 30092, and our telephone number is (678) 421-3000.

Available Information

We maintain a website located at www.primedia.com on which, among other things, we make available, free of charge, various corporate governance materials and reports that we file or furnish to the United States Securities and Exchange Commission (“SEC”). Our Corporate Governance Guidelines, Code of Ethics, and charters for each of the Audit Committee, Compensation Committee and Nominating and Corporate Governance Committee, are all provided on this website. We will post any waivers of our Code of Ethics granted to any of our directors or executive officers on the “Investor Relations” portion of this website. Our reports and other filings, including, without limitation, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements and all other documents, including amendments thereto, filed with or furnished to the SEC, are made available as soon as practicable after their receipt by the SEC. We are not incorporating the information on our website into this Report, and our website and the information appearing on our website are not included in, and are not part of, this Report.

| ITEM 1A. | RISK FACTORS |

Below, we have described our present view of certain important risk factors. This discussion of risk factors contains “forward-looking statements,” as discussed on page 1 of this Report. These risk factors may be important to understanding any statement in this Report or elsewhere. The following information should be read in conjunction with Management’s Discussion and Analysis of Financial Condition and Results of Operations and the consolidated financial statements and related notes contained elsewhere in this Report.

Deterioration in general economic conditions, and in the specific industries in which we operate, have adversely affected and are expected to continue to adversely affect advertising revenue.

National and local market economic conditions affect the overall levels of advertising revenue. Negative economic conditions, including a U.S. recession and the nationwide and local downturn in the housing markets, have adversely affected and are expected to continue to adversely affect our overall level of advertising revenue, and a failure of economic conditions to improve in our markets could adversely affect our future business, financial condition and results of operations.

We depend on large property management companies in the apartment leasing sector of the residential real estate industry for a majority of our revenue, and any economic or industry developments that adversely affect the number and value of leasing transactions generated could adversely impact our financial results.

The return on investment for our large property management company advertisers depends upon the comparison of how many leases we are generating for the managed communities in a particular local market, and the value of such leases, to the amount charged for our advertising. Many of the factors affecting the number and value of lease transactions are beyond our control. In markets where occupancy levels are extraordinarily high or

7

Table of Contents

Index to Financial Statements

extraordinarily low, the management company’s return on investment can be adversely affected, and the management company may choose to decrease the level of advertising, which could adversely affect our revenue. The effects of occupancy rates can be mitigated or exacerbated by effective rent levels, which are essentially average rent amounts after giving effect to free months of rent and other incentives.

Our new home directories and related websites depend on the new home sales sector of the residential real estate industry, which is cyclical.

Approximately 8.3% of our 2009 advertising revenue was generated from sales of advertising products to new home builders in the residential real estate industry. This sector, which is cyclical, directly affects the success of our New Homes division. The return on investment for our new home builder advertisers depends on the success rate of actual sales that are closed in comparison to the advertising expenses paid. If our advertisers experience lower return on investment because actual sales decline for reasons beyond our control, they tend to decrease their advertising budget, which adversely affects our revenue.

The United States economy is currently experiencing its worst downturn in the residential real estate industry in over 50 years. The duration of this downturn, as is true of most trends in the real estate industry, is unpredictable, and as a result, our prospects in this area are also unpredictable. An economic recession, unfavorable taxation laws and regulations, higher credit standards, unavailability of mortgage loans, increased interest rates, increased unemployment, lower consumer confidence or lower wages can cause consumers to reduce their activity in the residential real estate industry, thus negatively impacting local new home sales markets.

The market for our products and services is highly competitive.

The markets for our products and services are disbursed throughout the United States. Generally, other online and print apartment and new home-targeted resources for the consumer represent our main competitors. To a lesser extent, we also compete with traditional newspapers and yellow pages.

Competition for advertising is generally based on audience or traffic levels and demographics, price, service and advertising results. Competition from all relevant media and services affects our ability to attract and retain consumers and advertisers and to maintain or increase our advertising rates. This competition has intensified as a result of the continued developments of digital media technologies. Distribution of advertising over the Internet, as well as through mobile phones and other devices, continues to increase in popularity. As a result, a shift from print advertising to online alternatives has contributed to significant declines in print advertising.

The majority of our current product offerings are built upon integrated media packages that feature online, mobile and print components. However, we are continuing to aggressively develop and market our online products and services, and we could experience a decline in advertising revenue if we are unable to migrate print advertising to our website offerings in volumes or at rates sufficient to offset declines in print advertising.

If we are not successful in growing our digital products and services, our business, financial condition and prospects will be adversely affected.

Our growth depends, to a significant degree, upon the development of our digital products and services. Accordingly, our ability to grow and succeed over the long term depends on various factors, including, among other things:

| • | increasing our online traffic and attracting and retaining visitors to our websites, which may be adversely affected by search engines (including Google, the primary search engine directing traffic to our websites) changing the algorithms responsible for directing search queries to web pages; |

| • | attracting advertisers to our websites, which depends partly on our ability to generate online traffic and partly on the rate at which users engage in lease or sale transactions with advertisers using our websites; |

8

Table of Contents

Index to Financial Statements

| • | maintaining or increasing advertising rates on our websites, which will depend, in part, on the market position of our brands; |

| • | exploiting new and existing technologies to distinguish our products and services from those of our competitors and developing new content, products and services, which may move in unanticipated directions due to the development of competitive alternatives, rapid technological change, regulatory changes and shifting market preferences; |

| • | investing funds and resources in online opportunities, in which some of our existing competitors and possible additional entrants may have greater operational, financial and other resources than we do or may be better positioned to compete for certain opportunities; and |

| • | attracting and retaining talent for critical positions. |

Even if we continue to develop our digital products and services, we may not be successful in generating or increasing revenue from these products or services due to increasing competition and economic conditions. If we are not successful in maintaining or growing revenue from our digital products and services to offset current and anticipated declines in revenue from print products, our business, financial condition and prospects will be adversely affected.

If we are unable to meet rapid changes in technology, our services and technology and systems may become obsolete.

The Internet and e-commerce are constantly changing. Due to the costs and management time required to introduce new services and enhancements, we may not be able to respond in a timely manner to competitive innovations. To remain competitive, we must continue to enhance and improve the functionality and features of our online businesses. Further, to remain competitive, we must meet the challenges of the introduction by our competitors of new services using new technologies or the introduction of new industry standards and practices. In addition, the vendors we use to support our technology may not provide the level of service we expect or may not continue to provide their product or services on commercially reasonable terms or at all. If we fail to meet any of these potential changes, or our vendors fail to provide the necessary support to our technology, our results of operations and financial condition could be negatively impacted.

Our success and growth depend, to a significant degree, upon the protection of our intellectual property rights.

As a media company, we have a significant intellectual property portfolio, especially copyrights and trademarks, and have allocated considerable resources toward intellectual property maintenance, prosecution and enforcement. For example, we hold and maintain or have pending applications for numerous copyrights and trademarks in connection with our various products and services, such as Apartment Guide. In addition, we also continuously develop and create proprietary software to enhance our ability to effectively and efficiently update the listings in our online and print directories. We may be unable to deter infringement or misappropriation of our data and other proprietary information, detect unauthorized use or take appropriate steps to enforce our intellectual property rights. Any unauthorized use of our intellectual property could make it more expensive for us to do business and consequently harm our business.

Kohlberg Kravis Roberts & Co. L.P. (“KKR”) has control of a majority of our outstanding common stock and has the power to elect all the members of our Board of Directors and to approve any action requiring stockholder approval.

As of March 1, 2010, approximately 58.9% of the outstanding shares of our common stock were held by investment partnerships of which KKR Associates, L.P. and KKR GP 1996 LLC are the general partners. KKR Associates and KKR GP 1996 have sole voting and investment power with respect to these shares.

Consequently, KKR Associates, L.P. and KKR GP 1996 LLC and their respective general partners and members, two of whom are also on our Board of Directors, control us and have the power to elect all of our directors and

9

Table of Contents

Index to Financial Statements

approve any action requiring stockholder approval, including adopting amendments to our certificate of incorporation and approving mergers or sales of all or substantially all of our assets. KKR Associates, L.P. and KKR GP 1996 LLC will also be able to prevent or cause a change of control at any time.

Our stock price is volatile.

Our common stock price has experienced substantial volatility in the past and may remain volatile in the future. Volatility can arise as a result of a number of the factors discussed in this “Risk Factors” section, as well as divergence between our actual or anticipated financial results and published expectations of analysts; announcements that we, our competitors or our customers may make; and the relatively small portion of our outstanding shares that is in the hands of public investors, as opposed to our officers, directors and controlling-interest investors.

We may be unable to realize the benefits of our net operating loss carryforwards (“NOLs”), and, as a result, lose our future tax savings, which could have a negative impact on our liquidity and financial position.

NOLs may be utilized to offset federal and state taxable income in future years and reduce income taxes otherwise payable on such taxable income, subject to certain adjustments. The Internal Revenue Service (“IRS”) or state taxing authorities could challenge the amount of the NOLs, which could result in increases in future income tax liabilities. Based on current federal and state corporate income tax rates, our NOLs could provide a benefit to us, if fully utilized, of significant future tax savings. However, if we do not have sufficient taxable income in future years to use the tax benefits before they expire, we will lose the benefit of these NOLs permanently. Our inability to utilize available NOLs, if any, could require us to pay substantial additional federal and state taxes and interest, which may adversely affect our liquidity and financial position.

Future legislation may result in our inability to realize the tax benefits of our NOLs.

It is possible that legislation or regulations will be adopted that would limit our ability to use the tax benefits associated with our NOLs. However, we are not currently aware of any proposed changes in the tax laws or regulations that would materially and adversely impact our ability to use available NOLs, if any.

Our use of NOL carryforwards could be limited by ownership changes.

In addition to the general limitations on the carryback and carryforward of NOLs under Section 172 of the Internal Revenue Code (the “Code”), Section 382 of the Code imposes further limitations on the utilization of NOLs by a corporation following various types of ownership changes, generally resulting in more than a 50 percentage point change in ownership of a corporation within a three year period. Therefore, the future utilization of our NOLs may be subject to limitation for regular federal income tax purposes.

We cannot be certain that the limitations of Section 382 will not limit or deny in full our future utilization of available NOLs, if any. Such limitation or denial could require us to pay substantial additional federal and state taxes and interest. Moreover, we cannot be certain that future ownership changes will not limit or deny in full our future utilization of all available NOLs. If we cannot utilize available NOLs, if any, we may be required to pay substantial additional federal and state taxes and interest. Such tax and interest liabilities may adversely affect our liquidity and financial position.

If we are unable to meet continued listing requirements of the New York Stock Exchange, Inc. (“NYSE”), the NYSE may delist our common stock, which could negatively affect the price of the common stock and your ability to sell the common stock.

In November 2008, the NYSE notified us that we were considered “below criteria” specifically because our average total market capitalization was less than $75 million over a consecutive 30 trading-day period. This

10

Table of Contents

Index to Financial Statements

required us to submit a plan that demonstrated our ability to achieve compliance with the continued listing standards within 18 months of receipt of the notice. In February 2009, the NYSE notified us that it had accepted our proposed plan for continued listing on the NYSE, subject to quarterly reviews by the NYSE’s Listing and Compliance Committee to ensure progress against the plan. In June 2009, the NYSE lowered its minimum total market capitalization requirement to $50 million and subsequently notified us that we were considered in compliance and that no quarterly reviews would be required.

In the future, we may not be able to meet the continued listing requirements of the NYSE. If we are unable to satisfy the NYSE criteria for continued listing, our common stock would be subject to delisting. Trading, if any, in our common stock would thereafter be conducted on another exchange or quotation system. As a consequence of any such delisting, a stockholder would likely find it more difficult to dispose of, or to obtain accurate quotations as to the prices for our common stock.

The soundness of financial institutions could adversely affect us.

We have relationships with several financial institutions as lenders under our credit facility and engage in transactions with other counterparties in the financial services industry. Defaults by, or even rumors or questions about, financial institutions or the financial services industry generally, could result in losses or defaults by these institutions. As a result of Lehman Brothers, Inc. ceasing to be a participating lender in our credit facility, the total capacity under our revolving credit facility was reduced by $12.0 million to $88.0 million. In the event that the volatility of the financial markets further adversely affects financial institutions that are lenders under our credit facility, we may be unable to access our credit facility or complete financing transactions as intended, which could adversely affect our revenue and results of operations.

Our credit agreement limits our business flexibility by imposing operating and financial restrictions on our operations.

Our credit agreement imposes specific operating and financial restrictions on us. These restrictions impose conditions or limitations on our ability to, among other things: change the nature of our business; incur additional indebtedness; create liens on our assets; sell assets; issue stock; engage in mergers, consolidations or transactions with our affiliates; make investments in or loans to specific subsidiaries; make guarantees or specific restricted payments; and declare or make dividend payments on our common stock.

Our failure to comply with the terms and covenants in our credit agreement could lead to a default under the terms of such agreement, which would entitle the lenders to accelerate the indebtedness and declare all amounts owed due and payable. If that occurred, we might not be able to refinance or otherwise satisfy our debt obligations, which could have a substantial adverse effect on our ability to continue as a going concern. We may not be able to comply with these restrictions in the future, or, in order to comply with these restrictions, we may have to forego opportunities that might otherwise be beneficial to us.

Our accounting policies and methods are key to how we report our financial condition and results of operations and may require management to make estimates about matters that are uncertain.

Accounting policies and methods are fundamental to how we record and report our financial condition and results of operations. Management must exercise judgment in selecting and applying many of these accounting policies and methods so they comply with accounting principles generally accepted in the United States of America (“GAAP”).

Management has identified certain accounting policies and estimates as being critical because they require management’s judgment to ascertain the valuations of assets, liabilities, commitments and contingencies. A variety of factors could affect the ultimate value that is obtained either when earning income, recognizing an expense, recovering an asset or reducing a liability. We have established detailed policies and control procedures

11

Table of Contents

Index to Financial Statements

that are intended to ensure these critical accounting estimates and judgments are well controlled and applied consistently. In addition, the policies and procedures are intended to ensure that the process for changing methodologies occurs in an appropriate manner. Because of the uncertainty of estimates about these matters, we cannot guarantee that we will not be required to adjust accounting policies or restate prior period financial statements. See Item 7—“Management’s Discussion and Analysis of Financial Condition and Results of Operations—Critical Accounting Policies and Estimates” and Note 2, “Summary of Significant Accounting Policies,” to the consolidated financial statements contained elsewhere in this Report for more information.

| ITEM 1B. | UNRESOLVED STAFF COMMENTS |

None.

| ITEM 2. | PROPERTIES |

The following table sets forth certain information with respect to our principal locations as of December 31, 2009. These properties were leased by us initially for use in our operations, but as a result of divestitures and consolidations, certain of these properties are now subleased to third-party tenants; only the Norcross location is used in our current operations. Of the total of approximately 1.1 million rentable square feet currently under lease, approximately 0.3 million rentable square feet are fully subleased to third parties. We consider the locations presently used by us for our operations to be adequate for our present needs. If we are forced for any reason to vacate any of our facilities due to lease expirations or any other reasons, we believe that equally suitable alternative locations are available on equally favorable terms in all of the locations where we do business.

| Principal Locations |

Principal Use |

Approximate Rentable Square Feet (“RSF”) |

Type of Ownership Expiration Date of Lease | |||

| Norcross, GA 3585 Engineering Drive |

Executive and administrative offices | 86,600 | Lease expires in 2016 | |||

| Carrollton, TX 4101 International Parkway |

Sublease | 201,180 | Lease expires in 2014; 62,825 RSF sublet as of December 31, 2009 | |||

| New York, NY 1440 Broadway |

Sublease | 170,700 | Lease expires in 2015; fully sublet as of December 31, 2009 | |||

| New York, NY 261 Madison |

Sublease | 72,100 | Lease expires in 2017; 47,333 RSF sublet as of December 31, 2009 | |||

| ITEM 3. | LEGAL PROCEEDINGS |

As is more fully discussed in Note 20, “Commitments and Contingencies,” to the consolidated financial statements contained elsewhere in the Report, we are involved in lawsuits and claims, both actual and potential, including some that we have asserted against others, in which substantial monetary damages are sought. Although the result of any future litigation of such lawsuits and claims is inherently unpredictable, management believes that, in the aggregate, the outcome of all such lawsuits and claims will not have a material effect on our long-term consolidated financial position or liquidity; however, any such outcome could be material to the results of operations of any particular period in which costs, if any, are recognized.

| ITEM 4. | RESERVED |

12

Table of Contents

Index to Financial Statements

EXECUTIVE OFFICERS OF THE REGISTRANT

Our current executive officers are:

| Corporate Officers | ||

| Dean B. Nelson Chairman of the Board Age: 51 |

Mr. Nelson became Chairman of the Board in April 2003 and also served as President and Chief Executive Officer from October 2005 to September 2007. He has served as the Chief Executive Officer of Capstone Consulting LLC, a strategic consulting firm, since March 2000. | |

| Charles J. Stubbs President and Chief Executive Officer Age: 37 |

Mr. Stubbs has served as President and Chief Executive Officer since May 2008. From November 2004 to May 2008, he was the President and CEO of YellowPages.com. Prior to that time, Mr. Stubbs served as President of BellSouth IntelliVentures, the electronic media division of BellSouth Advertising and Publishing Group. Before joining BellSouth, Mr. Stubbs was Executive Vice President of Infospace, a Bellevue, Washington-based entity that develops and markets Internet and wireless solutions for wireless operators and content sites. | |

| Kim R. Payne Senior Vice President and Chief Financial Officer Age: 41 |

Ms. Payne has served as Chief Financial Officer since August 2007. Previously, she had served as Chief Financial Officer of our operating subsidiary since August 2006. She joined us as an accountant in 1991 and during her tenure has served in various finance management roles at our operating subsidiary, including Financial Analyst, Director of Analysis and Planning, and Vice President of Finance. | |

| J. Michael Barber Senior Vice President and Chief Accounting Officer Age: 43 |

Mr. Barber has served as Chief Accounting Officer since May 2008. Prior to joining us in October 2007, Mr. Barber served as Executive Vice President and Chief Accounting Officer of HomeBanc Corp. from September 2004 through October 2007. From 2001 to August 2004, he served as Senior Vice President/Manager of Accounting Policy and Reporting with Union Planters Corp., a bank holding company. Prior to 2001, Mr. Barber worked with PricewaterhouseCoopers LLP, where he was a Senior Manager in that organization’s banking practice. Mr. Barber is a certified public accountant. | |

| Arlene Mayfield Senior Vice President and President, Apartment Guide and New Home Guide Age: 47 |

Ms. Mayfield has served as Senior Vice President since December 2007 and President of the Apartment Guide and New Home Guide businesses since October 2005 and November 2008, respectively. Previously, she had served as Vice President of the New Home Guide from September 2003 through October 2005. She began her career with us in 1993 as the Publisher of the Albuquerque Apartment Guide. Ms. Mayfield was promoted to Publisher of the Orlando Apartment Guide in 1997 and subsequently to Regional Director for the Eastern Region in 1999. | |

| Keith L. Belknap, Jr. Senior Vice President, General Counsel and Secretary Age: 52 |

Mr. Belknap has served as Senior Vice President, General Counsel and Secretary since September 2007 and of our operating subsidiary since March 2007. Mr. Belknap is responsible for oversight of our legal and corporate and business development functions. From February 2006 to March 2007, he served as Assistant General Counsel of PPG Industries, Inc. From April 2003 to February 2006, he served as a Principal Counsel to Georgia-Pacific Corporation. Prior to April 2003, Mr. Belknap was Counsel at Skadden, Arps, Slate, Meagher & Flom LLP. | |

| Business Executive | ||

| Jamison M. Clymer President, Rentals.com Age: 35 |

Mr. Clymer has served as President of Rentals.com since January 2008. Prior to joining us, Mr. Clymer served as Vice President and General Manager of Homes.com at Dominion Enterprises from January 2005 through December 2007. From October 2003 through December 2004, he served as General Manager of Employmentguide.com at Dominion, and from July 2001 through September 2003 he served as District Manager of Employmentguide.com. | |

13

Table of Contents

Index to Financial Statements

| ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Market Information

Our common stock is listed on the NYSE under the ticker symbol “PRM.” As of March 1, 2010, there were 636 holders of record of our common stock. The following table sets forth, for the quarterly periods indicated, the high, low and closing sales prices per share of our common stock as quoted on the NYSE at the end of regular trading, as well as the cash dividends declared per share of common stock:

| Stock Prices | Cash Dividends Declared per Share | |||||||||||

| 2009 Quarters Ended |

High | Low | Close | |||||||||

| March 31 |

$ | 3.00 | $ | 1.60 | $ | 2.47 | $ | 0.07 | ||||

| June 30 |

4.05 | 1.80 | 2.01 | 0.07 | ||||||||

| September 30 |

3.25 | 1.72 | 2.52 | 0.07 | ||||||||

| December 31 |

4.29 | 2.36 | 3.61 | 0.07 | ||||||||

| Stock Prices | Cash Dividends Declared per Share | |||||||||||

| 2008 Quarters Ended |

High | Low | Close | |||||||||

| March 31 |

$ | 9.18 | $ | 5.69 | $ | 7.35 | $ | 0.07 | ||||

| June 30 |

7.54 | 4.65 | 4.66 | 0.07 | ||||||||

| September 30 |

4.74 | 2.20 | 2.43 | 0.07 | ||||||||

| December 31 |

2.51 | 0.69 | 2.17 | 0.07 | ||||||||

Dividends

Our bank credit facilities impose certain limitations on the amount of dividends permitted to be paid on our common stock. See Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity, Capital and Other Resources—Financing Arrangements.”

We announced on March 4, 2010 that our Board of Directors had authorized a regular quarterly cash dividend of $0.07 per share of common stock, payable on or about March 24, 2010, to stockholders of record on March 15, 2010. We currently expect that we will continue to pay a regular quarterly dividend, at the discretion of our Board of Directors.

Equity Compensation Plan Information

Information required by this item with respect to our equity compensation plans is incorporated by reference to our Proxy Statement for our 2010 Annual Meeting of Stockholders. The definitive Proxy Statement will be filed within 120 days of the end of the fiscal year ended December 31, 2009.

Recent Sales of Unregistered Securities

There have been no recent sales of unregistered securities.

Issuer Purchases of Equity Securities

Our Board of Directors has authorized a program (the “Repurchase Program”) to repurchase up to $5.0 million of our common stock through December 31, 2010. Under the terms of the Repurchase Program, we may repurchase shares in open market purchases or through privately negotiated transactions. We expect to use cash on hand to fund any repurchases of our common stock. As of December 31, 2008, we had not repurchased any shares under the Repurchase Program. During the three months ended March 31, 2009, we repurchased 0.2 million shares of our common stock for approximately $0.4 million at a weighted-average price (including brokerage commissions) of $1.79 per share. We did not repurchase any additional shares of our common stock during the year ended December 31, 2009 beyond those discussed above. The reacquired shares have been designated as treasury shares. As of December 31, 2009, we had $4.6 million available under the Repurchase Program for further share repurchases, which we may make.

14

Table of Contents

Index to Financial Statements

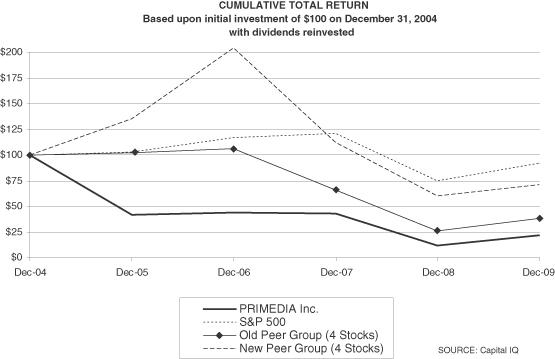

Performance Graph

The stock performance graph is not and shall not be deemed incorporated by reference by any general statement incorporating by reference this Report into any filing under the Securities Act of 1933 or the Securities Exchange Act of 1934, (collectively, the “Acts”) except to the extent that we specifically incorporate this information by reference, and shall not otherwise be deemed filed under such Acts.

The graph below compares the cumulative total stockholder return of our Common Stock with the cumulative total return of the S&P 500 Index and two different customized peer groups, the “Old Peer Group” and the “New Peer Group,” for the period commencing December 31, 2004 and ending December 31, 2009. The Old Peer Group is comprised of Autobytel Inc., Martha Stewart Living Omnimedia, Inc., Meredith Corp. and Move, Inc. The New Peer Group is comprised of Move, Inc., Martha Stewart Living Omnimedia, Inc., The Knot, Inc. and Market Leader, Inc. We elected to change our peer group because we believe the companies reflected in the New Peer Group provide a more relevant comparison to our business model and industry than the Old Peer Group. The graph assumes that $100 was invested in our Common Stock, in the index and in each of the peer groups on December 31, 2004 and that all dividends were reinvested on a quarterly basis.

| Dec-04 | Dec-05 | Dec-06 | Dec-07 | Dec-08 | Dec-09 | |||||||||||||

| PRIMEDIA Inc. |

$ | 100 | $ | 42 | $ | 44 | $ | 43 | $ | 12 | $ | 22 | ||||||

| S&P © 500 |

100 | 103 | 117 | 121 | 75 | 92 | ||||||||||||

| Old Peer Group (4 Stocks) |

100 | 102 | 106 | 66 | 26 | 38 | ||||||||||||

| New Peer Group (4 Stocks) |

100 | 135 | 204 | 112 | 60 | 71 | ||||||||||||

| ITEM 6. | SELECTED FINANCIAL DATA |

The selected consolidated financial data were derived from the audited consolidated financial statements. The data should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and the related notes thereto included elsewhere in this Report.

15

Table of Contents

Index to Financial Statements

PRIMEDIA INC. AND SUBSIDIARIES

| As of and for the Years Ended December 31, | |||||||||||||||||||

| 2009 | 2008 | 2007 | 2006 | 2005 | |||||||||||||||

| (Dollars in thousands, except per share amounts) | |||||||||||||||||||

| Operating Data: |

|||||||||||||||||||

| Revenue, net |

$ | 257,931 | $ | 304,105 | $ | 314,800 | $ | 307,929 | $ | 307,187 | |||||||||

| Depreciation and amortization of property and equipment |

13,256 | 14,475 | 12,612 | 11,501 | 10,410 | ||||||||||||||

| Amortization of intangible assets |

2,970 | 2,870 | 3,492 | 3,286 | 3,140 | ||||||||||||||

| Interest expense |

15,670 | 19,338 | 77,660 | 126,940 | 128,980 | ||||||||||||||

| Income (loss) from continuing operations |

$ | 4,540 | $ | 49,027 | $ | (55,678 | ) | $ | (65,114 | ) | $ | (101,306 | ) | ||||||

| Discontinued operations, net of tax |

(1,052 | ) | 10,441 | 547,123 | 103,344 | 665,924 | |||||||||||||

| Cumulative effect of change in accounting principle, net of tax(1) |

— | — | — | 22 | — | ||||||||||||||

| Net income |

3,488 | 59,468 | 491,445 | 38,252 | 564,618 | ||||||||||||||

| Income applicable to common stockholders |

$ | 3,488 | $ | 59,468 | $ | 491,445 | $ | 38,252 | $ | 564,618 | |||||||||

| Basic and diluted income (loss) applicable to common stockholders per common share(2): |

|||||||||||||||||||

| Income (loss) from continuing operations |

$ | 0.10 | $ | 1.11 | $ | (1.26 | ) | $ | (1.48 | ) | $ | (2.31 | ) | ||||||

| Discontinued operations |

(0.02 | ) | 0.24 | 12.40 | 2.35 | 15.19 | |||||||||||||

| Cumulative effect of change in accounting principle(1) |

— | — | — | 0.00 | — | ||||||||||||||

| Income applicable to common stockholders |

$ | 0.08 | $ | 1.35 | $ | 11.14 | $ | 0.87 | $ | 12.88 | |||||||||

| Dividends declared per share of common stock |

$ | 0.28 | $ | 0.28 | $ | 2.15 | $ | — | $ | — | |||||||||

| Basic common shares outstanding (weighted-average)(2) |

44,124,538 | 44,176,398 | 44,118,943 | 43,997,665 | 43,838,591 | ||||||||||||||

| Diluted common shares outstanding (weighted-average)(2) |

44,214,003 | 44,197,590 | 44,118,943 | 43,997,665 | 43,838,591 | ||||||||||||||

| Balance Sheet Data: |

|||||||||||||||||||

| Goodwill and intangible assets, net |

$ | 149,972 | $ | 152,942 | $ | 155,712 | $ | 862,025 | $ | 994,581 | |||||||||

| Total assets |

239,729 | 286,154 | 256,864 | 1,254,329 | 1,389,468 | ||||||||||||||

| Long-term debt(3) |

222,349 | 245,531 | 247,575 | 1,316,959 | 1,456,770 | ||||||||||||||

Notes to Selected Financial Data

| (1) | Effective January 1, 2006, we adopted GAAP related to the accounting for share-based payments, using the modified prospective method. Prior to the adoption of this statement, we expensed the fair value of stock-based compensation for all grants, modifications or settlements made on or after January 1, 2003 in accordance with GAAP, which was adopted on January 1, 2003 using the prospective method. Upon adoption, we were also required to expense the fair value of any awards that were granted prior to January 1, 2003 and that were not fully vested as of January 1, 2006. The cumulative effect of adopting this change in accounting principle was less than $0.1 million, which is included in the results of operations for the year ended December 31, 2006. |

| (2) | Income (loss) per common share has been determined based on income (loss) applicable to common stockholders, divided by the weighted-average number of common shares outstanding for all years presented. |

16

Table of Contents

Index to Financial Statements

The securities that could potentially dilute basic earnings per share in the future consist of 1.6 million warrants at December 31, 2009, 2008, 2007, 2006 and 2005; and an aggregate of 2.1 million, 3.1 million, 3.2 million, 3.4 million and 3.6 million stock options and shares of restricted stock as of December 31, 2009, 2008, 2007, 2006 and 2005, respectively. For the year ended December 31, 2009, potentially dilutive securities, including 2.5 million stock options and 1.6 million warrants to purchase common stock, were not included in the weighted-average number of common shares outstanding used in the computation of diluted income per common share because their strike price was greater than the average market price of our common stock during the period, and their inclusion would be anti-dilutive. An additional 0.4 million shares of restricted stock were excluded from the weighted-average number of common shares outstanding used in the computation of diluted earnings per share for the year ended December 31, 2009 because either they did not vest and were forfeited or the calculation under the treasury stock method resulted in no additional dilutive shares.

For the year ended December 31, 2008, potentially dilutive securities, including 2.7 million stock options and 1.6 million warrants to purchase common stock, were not included in the weighted-average number of common shares outstanding used in the computation of diluted income per common share because their strike price was greater than the average market price of our common stock during the period, and their inclusion would be anti-dilutive. An additional 0.4 million shares of restricted stock were excluded from the weighted-average number of common shares outstanding used in the computation of diluted earnings per share for the year ended December 31, 2008 because either the performance goals were not met at the end of the period or the calculation under the treasury stock method resulted in no additional dilutive shares.

For the years ended December 31, 2007, 2006 and 2005, potentially dilutive securities were not included in the weighted-average number of common shares outstanding used in the computation of diluted income (loss) per common share because the effect of their inclusion, as measured against loss from continuing operations, would be anti-dilutive.

| (3) | Excludes current maturities of long-term debt. |

| Item 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

Introduction

The following discussion and analysis summarizes our financial condition and operating performance and should be read in conjunction with our historical consolidated financial statements and notes thereto included elsewhere in this Report.

Executive Summary

Our Company

We are a targeted media company that provides consumers with tools and information they need to find a place to live. Our consumer directories are targeted primarily for the apartment and other rental property sectors of the residential real estate industry and are provided free to consumers through a combination of online, print and mobile platforms. We derive advertising revenue by providing our advertiser clients – property management companies, private owner/landlords, new home builders and real estate professionals – with products and services that generate measurable results in the form of cost-effective, quality leads.

Our principal digital assets include ApartmentGuide.com, Rentals.com, RentalHouses.com, NewHomeGuide.com and AmericanHomeGuides.com. According to comScore Media Metrix, unique visitors to our websites reached 3.3 million in January 2010, compared with 3.1 million in January 2009. The total number of leads we produce for our advertisers has grown year over year, and leads derived from our online and mobile services now represent more than 75% of the total leads we deliver to our advertiser clients.

17

Table of Contents

Index to Financial Statements

We produce printed directories for 75 markets and distribute them through display rack programs, many of which are on an exclusive basis, with large national and regional retail chains, including grocery, drug, convenience, video, fitness and mass merchandise retailers. In 2009, we distributed approximately 14.9 million printed directories to approximately 17,000 advertiser client locations and 28,000 retail and other locations.

Fiscal 2009 Fourth Quarter Results

| Fourth Quarters Ended December 31, |

$ Change Favorable/ (Unfavorable) |

% Change Favorable/ (Unfavorable) |

|||||||||||||

| 2009 | 2008 | ||||||||||||||

| (Dollars in thousands) | |||||||||||||||

| Revenues, net |

$ | 61,253 | $ | 73,409 | $ | (12,156 | ) | (16.6 | )% | ||||||

| (Provision) benefit for income taxes |

(3,535 | ) | 29,401 | (32,936 | ) | (112.0 | ) | ||||||||

| Income from continuing operations |

$ | 7,469 | $ | 34,691 | $ | (27,222 | ) | (78.5 | )% | ||||||

| Discontinued operations, net of tax |

3,679 | (2,710 | ) | 6,389 | 235.8 | ||||||||||

| Net income |

$ | 11,148 | $ | 31,981 | $ | (20,833 | ) | (65.1 | ) | ||||||

The decrease in revenue, net was primarily attributable to a decrease in New Homes advertising revenue and distribution revenue. The decrease in New Homes advertising revenue was due to a 39.1% decrease in revenue per community served driven by the continued weaknesses in the new home sales sector and a 21.2% decrease in new home communities served. The decrease in distribution revenue was due to a 23.6% decrease in the average revenue per pocket due to softness in demand and a 24.2% decrease in the number of pockets sold in our display racks due largely to the reduction in retail locations serviced.

Income from continuing operations decreased primarily due to lower revenue of $12.2 million and the release in 2008 of $29.3 million in deferred tax asset valuation allowance, partially offset by decreases in 2009 in distribution and circulation of $8.2 million, cost of goods sold of $2.2 million, and general and administrative of $2.0 million.

Net income decreased due to the factors above, partially offset by a $6.4 million increase in income from discontinued operations, net of tax, which was the result of a benefit recorded from our estimated liability for certain tax-related contingencies of approximately $6.0 million, primarily due to the lapsing of the statutes of limitations.

2009 Summary Consolidated Results

In 2009, revenue was $257.9 million, down 15.2% as compared to $304.1 million in 2008. In 2009, costs and expenses were $251.3 million, down 10.9% compared to $282.1 million in 2008.

In 2009, income from continuing operations was $4.5 million, compared to $49.0 million in 2008.

Net income was $3.5 million in 2009 compared to $59.5 million in 2008, which included gain on sale of businesses, net of tax, of $2.0 million.

Business Trends and Outlook

The continuing and deepening deterioration in the economy generally and in the conditions in the residential real estate industry in particular have resulted in relatively low occupancy and effective rent levels on a national basis. Though local market conditions vary, our advertisers generally have responded to these conditions with shifts in marketing strategies and budget cuts, which have depressed and may continue to depress our advertising

18

Table of Contents

Index to Financial Statements

revenue. As we look ahead, we believe advertisers will continue to be cautious with their budgets, focusing more on total advertising spend than on ROI, and advertising revenue is likely to continue to be challenged in 2010.

Also contributing to shifts in marketing strategies of our advertisers is the continuing increase in popularity of online advertising, including through mobile phones and other devices. The broad shift from print advertising to online alternatives has contributed to significant declines in print advertising across traditional media products and services. Most of our current offerings are built upon integrated media packages that include online, print and mobile components. However, we have seen the effects of this trend in revenue declines attributable to our premium print products, as well as increasing advertiser focus on our online and mobile offerings.

The targeted nature of our ROI-based print products is why they continue to deliver substantial value to our advertisers, even though the greater portion of the value we now deliver (in the form of leads) on a national basis has shifted to our digital products and services. The mix of advertising results, and therefore value, as between our digital and print products and services is highly market-specific, with consumers in some markets favoring print products, while those in other markets favor our Internet or mobile services.

Overall, we expect our advertisers to increasingly favor digital media choices in their advertising budgets, and we are continuing to aggressively develop and market our online and mobile offerings. However, at least in the shorter term, we anticipate continuing decreases in revenue per community served as we increase apartment communities served. We believe that our growth will depend, to a significant degree, upon the value of our online products and services and our ability to monetize this value.

During 2010, we intend to continue to grow our client count and market share in our largest business, Apartment Guide, and pursue enhancements to our product portfolio and market and market segment expansion. We also intend to grow our Rentals.com business by focusing on improving site engineering and performance, while increasing traffic, primarily through search engine optimization. Our visibility around 2010 revenue for Apartments is extremely limited, given general economic and market conditions, though we currently expect to see a 5% to 6% year-over-year decline in first quarter 2010 Apartments revenue, similar to the percentage decline experienced in fourth quarter 2009.

We anticipate continued pressure on our New Homes business during 2010, and we remain focused on managing costs for this business in accordance with anticipated levels of revenue and managing our client relationships to best position us for opportunities as macroeconomic conditions improve. We currently expect a 40% to 50% year-over-year decline in New Homes revenue in first quarter 2010.

We anticipate that DistribuTech will continue to be impacted by lower revenue from customers that publish free publications and are scaling back or ceasing operations or providing an Internet-only product and by further reductions in retail locations serviced. Since 2008, we have undertaken strategic initiatives to substantially reduce the cost structure of our distribution function. As a result, distribution costs decreased from $85.2 million in 2008 to $60.9 million in 2009. We intend to continue aggressively reducing our distribution cost structure and expect to incur restructuring charges related to our RDAs of between $5.0 million and $7.0 million in 2010. We currently expect a 35% to 40% year-over-year decline in DistribuTech revenue in first quarter 2010.

Our overall distribution strategy is to reduce our overall print distribution costs as we devote greater resources to opportunities for growth that digital media present and eliminate less effective locations, while focusing our efforts on retaining and servicing locations that produce the best results for PRIMEDIA advertisers in terms of leads. We intend to move to a smaller, more efficient distribution model that primarily relies on third-party distribution services, in combination with more limited internal resources, to deliver our directories.

Transition Plan

We have relocated our corporate headquarters from New York to Norcross, Georgia. We continued to utilize certain of our New York-based functions through the first half of 2008 and to incur their associated costs.

19

Table of Contents

Index to Financial Statements

Critical Accounting Policies and Estimates

Management’s discussion and analysis of our financial condition and results of operations is based upon the amounts reported in our consolidated financial statements, which have been prepared in accordance with GAAP. The preparation of these financial statements requires the use of estimates, judgments and assumptions that affect the reported amounts. The significant accounting policies, outlined in Note 2, “Summary of Significant Accounting Policies,” to the consolidated financial statements contained elsewhere in this Report, are integral to an understanding of management’s discussion and analysis. The accounting policies and estimates that we believe are the most critical to an understanding of the results of operations and financial condition are those that require complex management judgment regarding matters that are highly uncertain at the time policies were applied and estimates were made. These accounting policies and estimates are discussed below. We base some of our estimates on historical experience and on various other assumptions that we believe are reasonable under the circumstances. Additionally, GAAP allows or requires many assets and liabilities to be accounted for at fair value, which is defined to be the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. GAAP also requires that certain assets be assessed for impairment based on fair value. In cases where active markets do not exist, as discussed below, modeling or other techniques may be required to estimate fair value. Different estimates reasonably could have been used in the current period that would have had a material effect on these financial statements, and changes in these estimates are likely to occur from period to period in the future.

We have discussed the development and selection of these critical accounting policies and estimates with the Audit Committee of the Board of Directors, and the Audit Committee has reviewed our disclosures relating to them in this Management’s Discussion and Analysis.