Attached files

| file | filename |

|---|---|

| EX-99.1 - PRESS RELEASE - PANTRY INC | exhibit99_1.htm |

| 8-K - THE PANTRY, INC. FORM 8-K 03-10-2010 - PANTRY INC | form8k.htm |

Bank of America Merrill Lynch

2010 Consumer Conference

Frank G. Paci, EVP and CFO

March 10, 2010

2010 Consumer Conference

Frank G. Paci, EVP and CFO

March 10, 2010

Safe Harbor Statement

Some of the statements in this presentation constitute “forward-looking

statements” within the meaning of the Private Securities Litigation Reform Act

of 1995. All statements other than those of historical facts included herein,

including those related to the company’s financial outlook, goals, business

strategy, projected plans and objectives of management for future operations

and liquidity, are forward-looking statements. These forward-looking

statements are based on the company’s plans and expectations and involve a

number of risks and uncertainties that could cause actual results to vary

materially from the results and events anticipated or implied by such forward-

looking statements. Please refer to the company’s Annual Report on Form 10-

K and its other filings with the SEC for a discussion of significant risk factors

applicable to the company. In addition, the forward-looking statements

included in this presentation are based on the company’s estimates and plans

as of the date of this presentation. While the company may elect to update

these forward-looking statements at some point in the future, it specifically

disclaims any obligation to do so.

statements” within the meaning of the Private Securities Litigation Reform Act

of 1995. All statements other than those of historical facts included herein,

including those related to the company’s financial outlook, goals, business

strategy, projected plans and objectives of management for future operations

and liquidity, are forward-looking statements. These forward-looking

statements are based on the company’s plans and expectations and involve a

number of risks and uncertainties that could cause actual results to vary

materially from the results and events anticipated or implied by such forward-

looking statements. Please refer to the company’s Annual Report on Form 10-

K and its other filings with the SEC for a discussion of significant risk factors

applicable to the company. In addition, the forward-looking statements

included in this presentation are based on the company’s estimates and plans

as of the date of this presentation. While the company may elect to update

these forward-looking statements at some point in the future, it specifically

disclaims any obligation to do so.

2

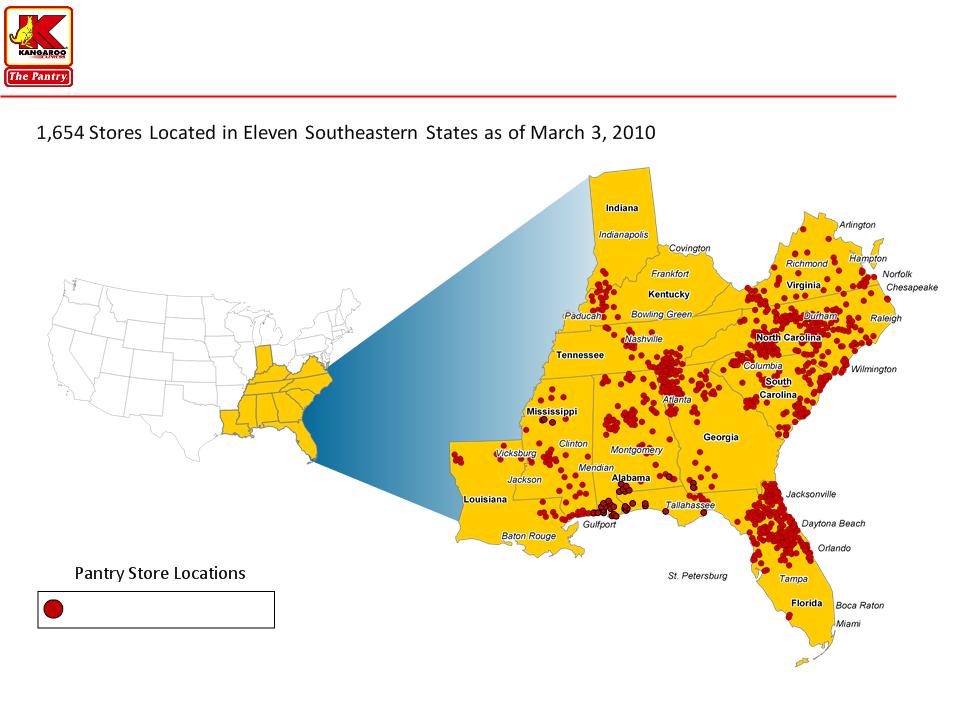

Company Overview

3

n Leading independently operated convenience store retailer in southeastern U.S. and

one of the largest in country

one of the largest in country

} 1,654 stores in 11 states as of March 3, 2010 with primary store brand of

Kangaroo Express®

Kangaroo Express®

} 2009 Financial Results:

} $1.66B merchandise revenue

} 2.08B retail gas gallons sold under multiple brands

} $169M in operating cash flow

n 234 Quick Service Restaurants in 224 locations as of March 3, 2010

Key Investment Highlights

4

Strong Cash Flow Generation allows us to invest in Growing

Our Business and De-lever Our Balance Sheet

Our Business and De-lever Our Balance Sheet

n Leading market positions in attractive Southeastern markets

n Significant scale advantages versus primary competitors

n Attractive sector consolidation potential

n Strong cash flow generation

n Investing in information systems and food service initiatives to

drive growth

drive growth

Leading Convenience Store Retailer Concentrated in the

Southeastern United States

Southeastern United States

5

_____________________

Note: Map is illustrative as of March 3, 2010.

High Degree of Fragmentation Provides Continued

Consolidation Opportunities

Consolidation Opportunities

6

More than 50% of the stores in key markets are single store operators

Florida

(7,246 stores)

North Carolina

(5,350 stores)

South Carolina

(2,888 stores)

Markets Fragmentation(1)(2)

Tennessee

(3,657 stores)

Mississippi

(2,503 stores)

Alabama

(3,756 stores)

(1) Source: U.S. Convenience 2008 Store Count (Gas Only) from NACS/TDLinx.

(2) Pantry store counts as of March 3, 2010.

Pantry

1 Store

Operators

2-50 Store

Operators

Operators

>50 Store

Operators

Operators

Pantry

1 Store

Operators

2-50 Store

Operators

Operators

>50 Store

Operators

Operators

Pantry

1 Store

Operators

2-50 Store

Operators

Operators

>50 Store

Operators

Operators

Pantry

1 Store

Operators

2-50 Store

Operators

Operators

>50 Store

Operators

Operators

Pantry

1 Store

Operators

2-50 Store

Operators

Operators

>50 Store

Operators

Operators

Pantry

1 Store

Operators

2-50 Store

Operators

Operators

>50 Store

Operators

Operators

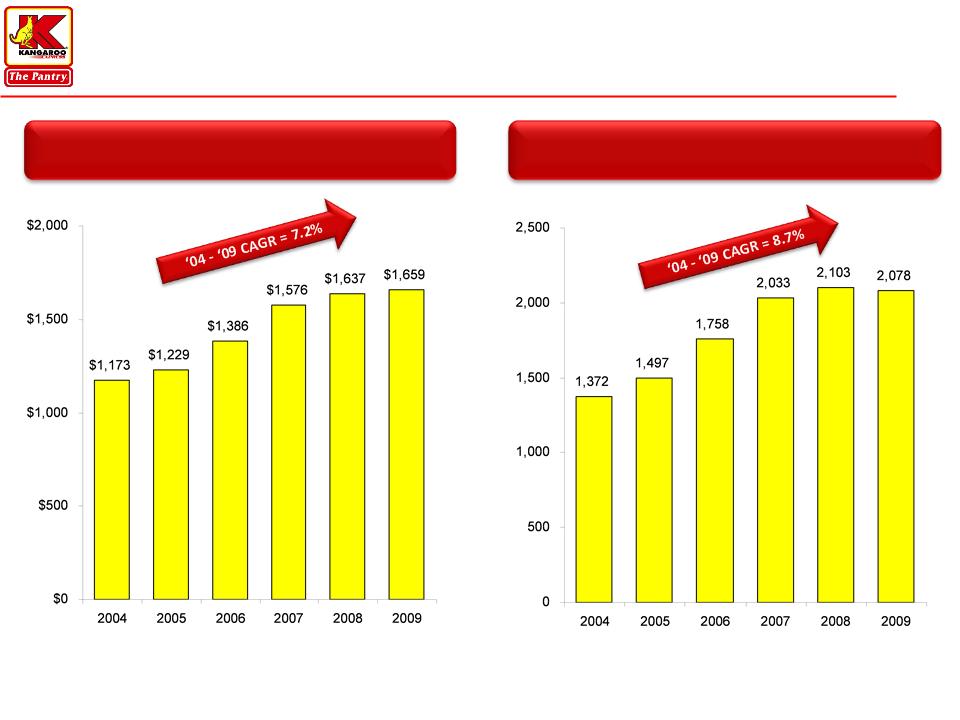

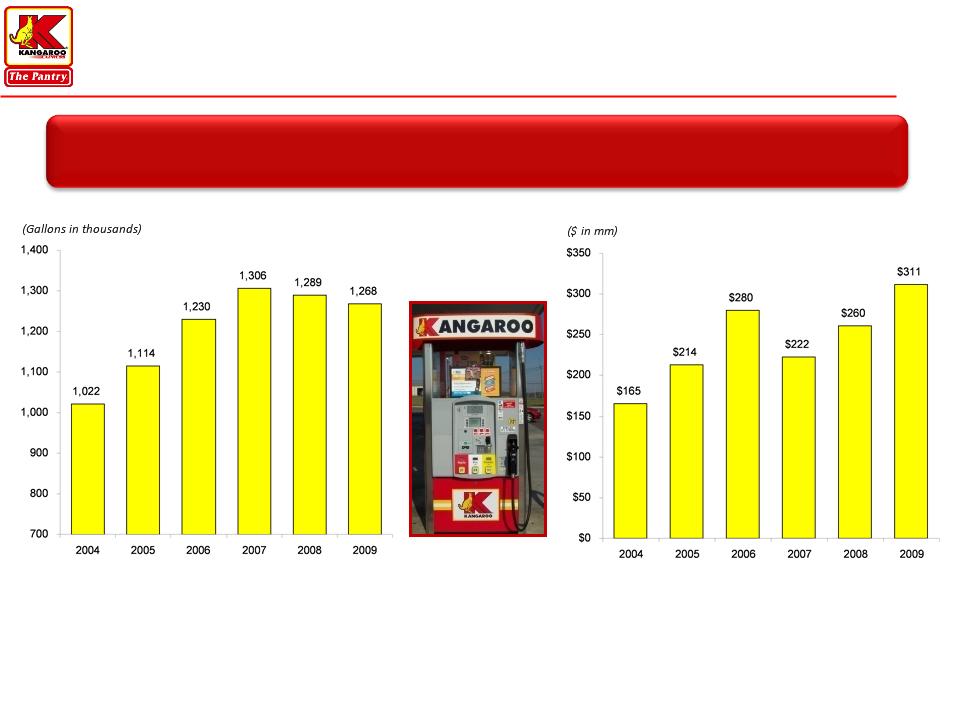

Strong Track Record of Growth…

7

Merchandise Revenue

Fiscal Year

Retail Gas Gallons Sold

Fiscal Year

($ in mm)

(Gallons in mm)

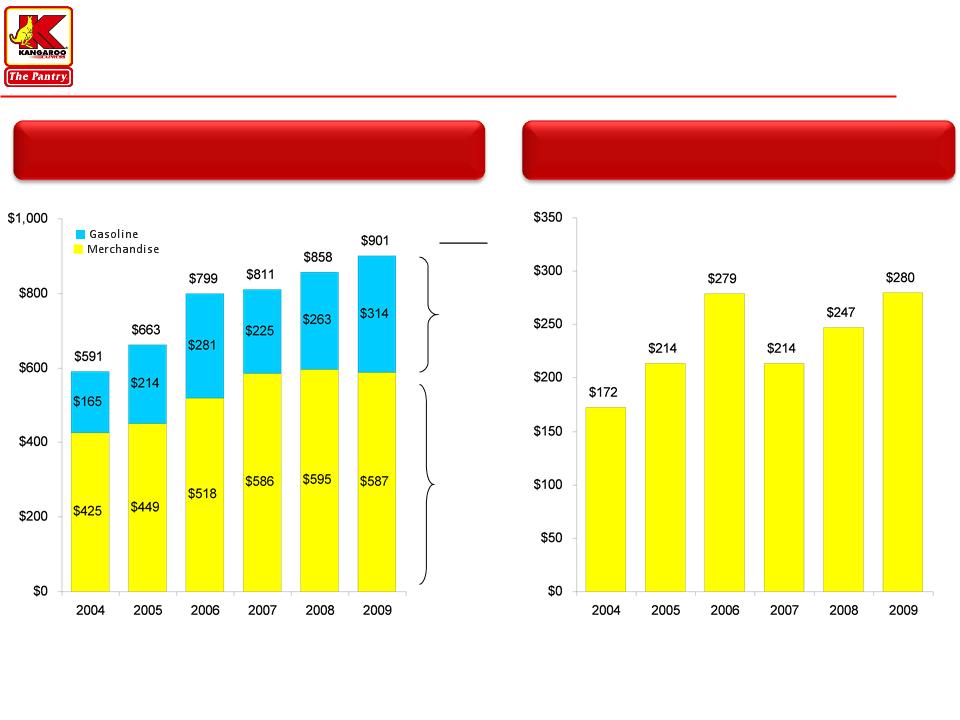

…Substantial EBITDA Generation…

8

Gross Profit

Fiscal Year

Reported EBITDA

Fiscal Year

’04-’09

CAGR

13.7%

6.7%

($ in mm)

($ in mm)

…And Significant Operating Cash Flow

9

($ in mm)

Fiscal Year

Operating Cash Flow

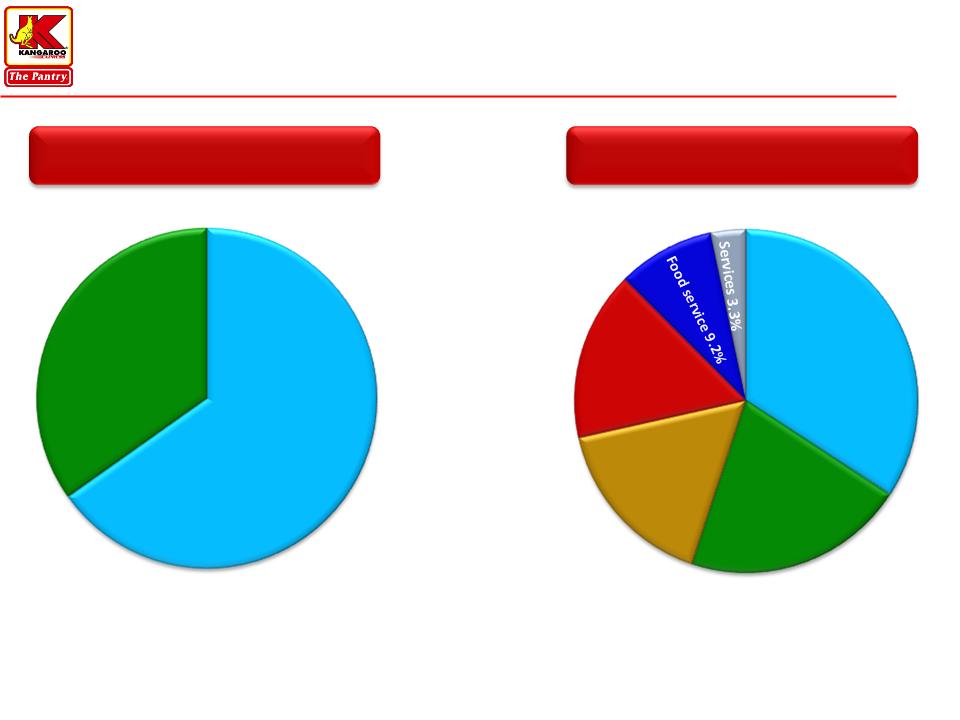

Merchandise Margin is the Primary Contributor of Our

Gross Profit

Gross Profit

10

Fiscal 2009 Gross Profit Mix

Fiscal 2009 Merchandise Sales Mix2

_____________________

(1) 2009 CPG (net of credit card fees and repairs and maintenance) was $0.150.

(2) Category sales mix estimates based on merchandise purchase and sales information.

(3) Includes Other Tobacco Products and Cigarettes.

Gas1

35%

Merchandise

65%

Tobacco products3

34.2%

Packaged

beverages

16.4%

Beer & wine

16.0%

Grocery

20.9%

Capturing the Food Service Opportunity

11

_____________________

(1) Pantry Food Service includes Fast Food Service, Self-Service Fast Foods and Beverages and is for FY2009.

(2) Industry Data is for Calendar Year 2008 and Industry source is NACS.

Industry2

Pantry1

Food Service Mix of Total Inside Sales

17%

9%

Core Store Food Service Offering

Lunch

Breakfast

Snacks

Expansion Opportunities

n Re-Image Stores

n Day Part Focus

} Breakfast, Lunch and Snacks

n Fresh and Healthier Offerings

Branded Food Service

13

_____________________

Note: Grill & Chill picture not a Pantry location.

(1) QSR Count as of March 3, 2010.

n Anticipate 25 new nationally branded food service locations in FY2010

n Current portfolio1

} Subway - 126 locations

} Dairy Queen - 8 locations

} Proprietary Chicken - 63 locations

Gasoline Strategy Maximizes Fuel Gross Profit Dollars

14

We Balance Average Gallons Sold per Store and Gasoline Margin to

Maximize Overall Gross Profit Dollars

Maximize Overall Gross Profit Dollars

_____________________

(1) Net of credit card fees and repairs and maintenance.

Average Gallons Sold per Store

Fiscal Year

Comps

2.0%

-3.3%

-4.4%

1.0%

3.1%

4.7%

Retail Gasoline Gross Profit $

Fiscal Year

CPG

(1)

(1)

12.0¢

15.0¢

12.4¢

10.9¢

15.9¢

14.3¢

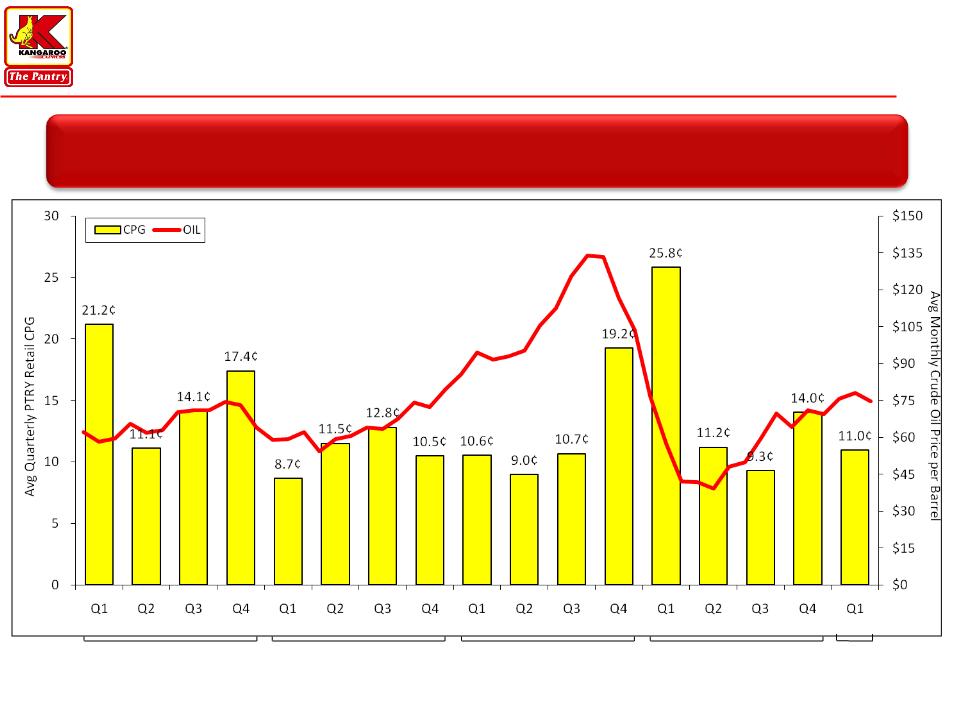

Oil Price Changes Drive Volatility in Quarterly Retail

Gasoline Cents per Gallon…

Gasoline Cents per Gallon…

Energy Market Volatility Impacts Margin

15

FY2006

FY2007

FY2008

FY2009

Source: Energy Information Administration. Data represents daily average futures contract price per barrel of light sweet crude (contract 1) and CPG is net of credit card fees and repairs and

maintenance.

maintenance.

FY2010

¢

¢

¢

¢

¢

¢

¢

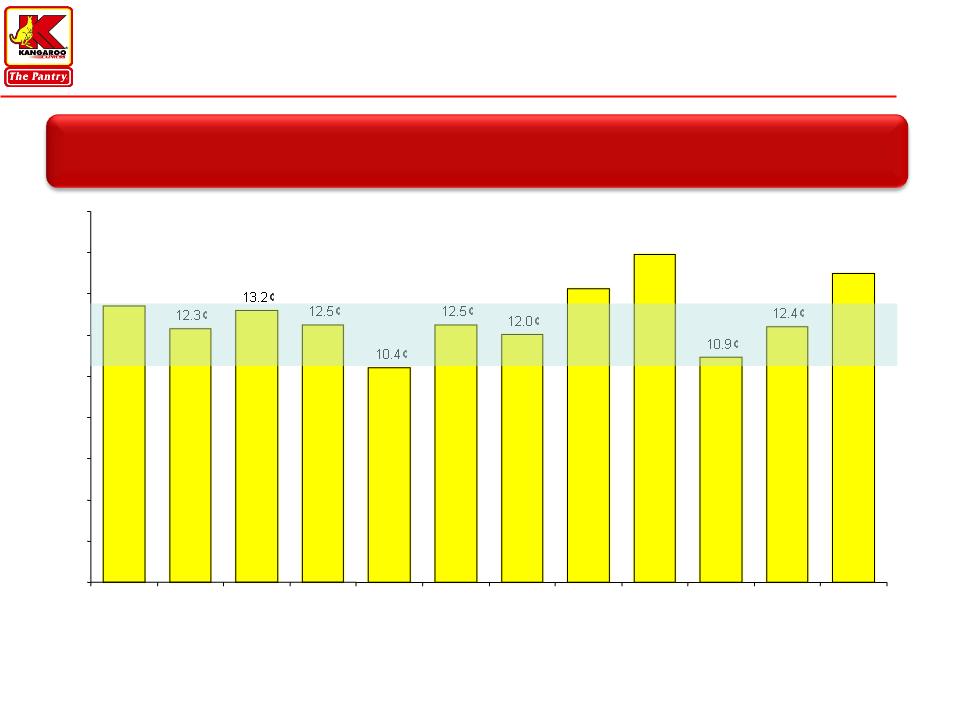

… But Annual CPG Tends to Remain Relatively Stable

16

Fiscal Year

_____________________

Note: Shaded area represents average historical CPG range and CPG is net of credit card fees and repairs and maintenance.

Annual Net CPG Margins Typically Range from 10.5¢ to 13.5¢

13.4¢

14.3¢

15.9¢

15.0¢

0¢

2¢

4¢

6¢

8¢

10¢

12¢

14¢

16¢

18¢

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Key Initiatives Targeted to Leverage Our Competitive Advantages

17

n Focus on specific meal occasions such as breakfast, lunch and snacks

n Accelerate nationally branded food service locations

n Develop store reimaging concepts that feature broader food service offerings

n Established the position of Chief Information Officer

n Build business intelligence capabilities

n Upgrade POS and implement WAN across the store base

n Evaluate investment opportunities with a more disciplined focus

n Balance between store additions and investment in existing stores

n Weigh growth investment versus debt reduction

“On-The-Go” Meals

Information Systems

Return Optimization

We believe these actions will better position us to

drive growth when the market environment improves

drive growth when the market environment improves

Financial Flexibility

18

n Meaningful liquidity

} $180 million in cash-on-hand

} $225 million revolver - $0 drawn, approximately $142 million

available after LOCs

available after LOCs

n Long-term debt profile; earliest maturity is the convertible debt in

November 2012

November 2012

n Covenant-light bank facility(1)

} 6.25x Adj. Net Debt / EBITDAR Leverage - Currently 5.65x

} 2.25x Interest Coverage - Currently 2.69x

_____________________

Note: Balance Sheet data as of December 24, 2009.

(1) Per credit facility covenant calculations (8x rent methodology) for TTM as of December 24, 2009.

Key Investment Highlights

19

Strong Cash Flow Generation allows us to invest in Growing

Our Business and De-lever Our Balance Sheet

Our Business and De-lever Our Balance Sheet

n Leading market positions in attractive Southeastern markets

n Significant scale advantages versus primary competitors

n Attractive sector consolidation potential

n Strong cash flow generation

n Investing in information systems and food service initiatives to

drive growth

drive growth

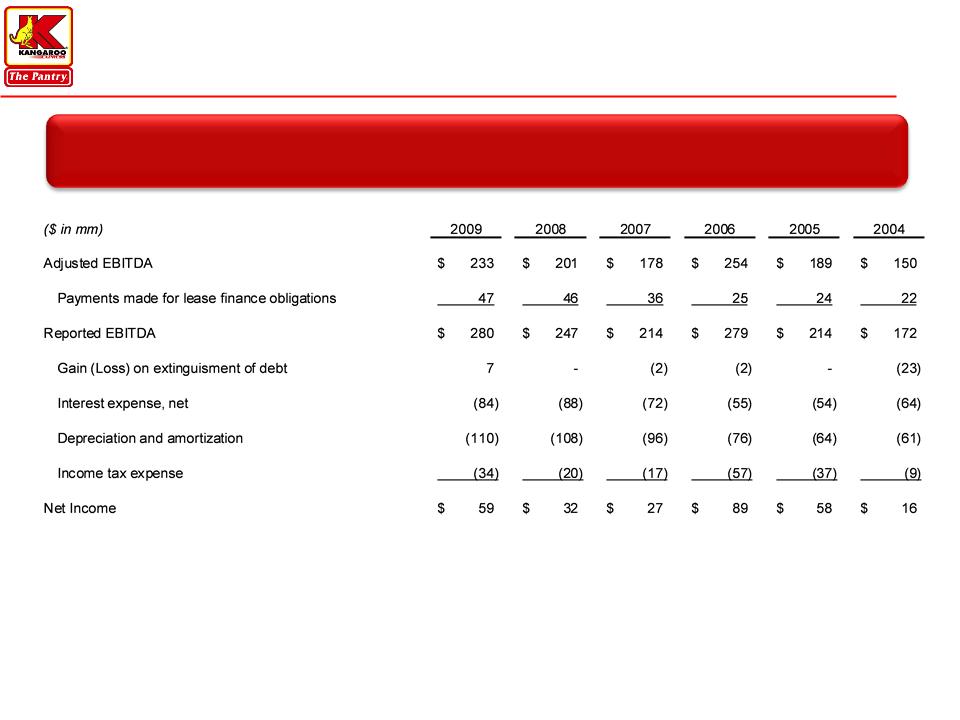

Reconciliation of Non-GAAP Measures

20

Adjusted EBITDA & EBITDA Reconciled to Net Income

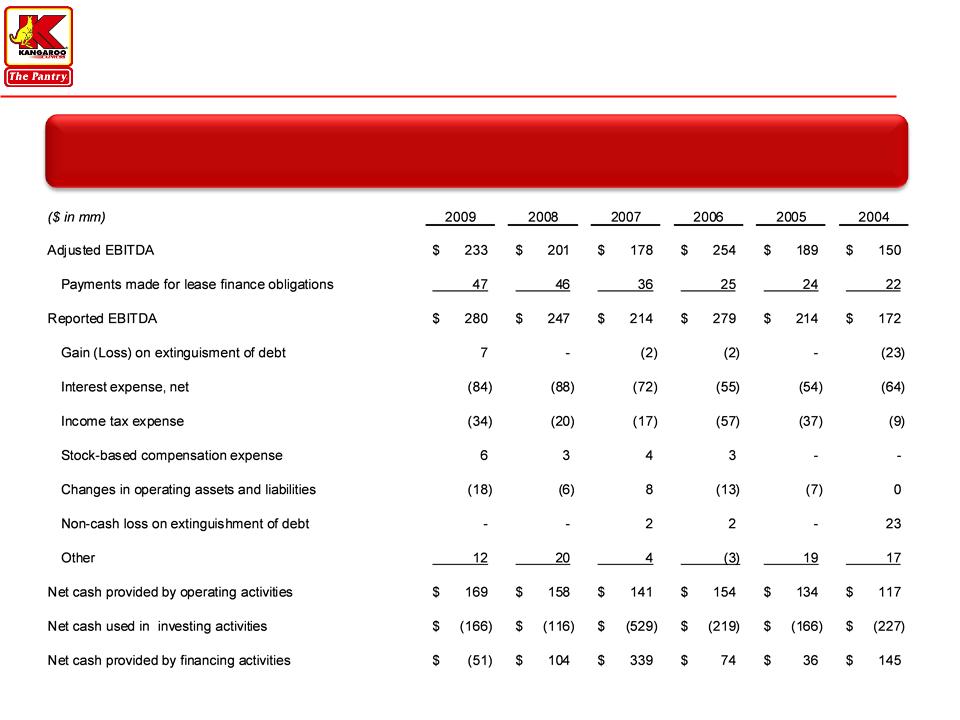

Reconciliation of Non-GAAP Measures

21

Adjusted EBITDA & EBITDA Reconciled to Cash Flows