Attached files

| file | filename |

|---|---|

| EX-31.2 - EXHIBIT 31.2 - OTELCO INC. | ex31-2.htm |

| EX-32.2 - EXHIBIT 32.2 - OTELCO INC. | ex32-2.htm |

| EX-21.1 - EXHIBIT 21.1 - OTELCO INC. | ex21-1.htm |

| EX-12.1 - EXHIBIT 12.1 - OTELCO INC. | ex12-1.htm |

| EX-32.1 - EXHIBIT 32.1 - OTELCO INC. | ex32-1.htm |

| EX-31.1 - EXHIBIT 31.1 - OTELCO INC. | ex31-1.htm |

| EX-10.13 - EXHIBIT 10.13 - OTELCO INC. | ex10-13.htm |

| EX-10.14 - EXHIBIT 10.14 - OTELCO INC. | ex10-14.htm |

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

Form

10-K

|

x

|

ANNUAL

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

|

|

For

the Fiscal Year Ended December 31, 2009

|

|

|

OR

|

|

|

o

|

TRANSITION

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT

OF 1934

|

For

the Transition Period from to

Commission

File Number: 1-32362

|

OTELCO

INC.

(Exact

Name of Registrant as Specified in Its Charter)

|

||

|

Delaware

|

52-2126395

|

|

|

(State

or Other Jurisdiction of

Incorporation

or Organization)

|

(I.R.S.

Employer

Identification

No.)

|

|

|

505

Third Avenue East, Oneonta, Alabama

|

35121

|

|

|

(Address

of Principal Executive Offices)

|

(Zip

Code)

|

|

|

205-625-3574

|

||

|

(Registrant’s

Telephone Number, Including Area Code)

|

||

|

Securities

registered pursuant to Section 12(b) of the Act:

|

||

|

Title

of Each Class

|

Name

of Each Exchange on Which Registered

|

|

|

Income

Deposit Securities, each representing shares of

Class

A Common Stock and Senior Subordinated

Notes

due 2019

|

The

NASDAQ Stock Market LLC

|

|

Securities registered pursuant to Section 12(g) of

the Act: None

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in

Rule 405 of the Securities Act. Yes o No

x

Indicate

by check mark if the registrant is not required to file reports pursuant to

Section 13 or Section 15(d) of the Act. Yes o No

x

Indicate

by check mark whether the registrant (1) has filed all reports required to be

filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the

preceding 12 months (or for such shorter period that the registrant was required

to file such reports), and (2) has been subject to such filing requirements for

the past 90 days. Yes x No

o

Indicate

by check mark whether the registrant has submitted electronically and posted on

its corporate Web site, if any, every Interactive Data File required to be

submitted and posted pursuant to Rule 405 of Regulation S-T during the

preceding 12 months (or for such shorter period that the registrant was

required to submit and post such files). Yes o No

o

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K is not contained herein, and will not be contained, to the best

of registrant’s knowledge, in definitive proxy or information statements

incorporated by reference in Part III of this Form 10-K or any amendment to this

Form 10-K. x

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer, or a smaller reporting company. See

the definitions of “large accelerated filer,” “accelerated filer” and “smaller

reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large

accelerated filer o

|

Accelerated

filer x

|

Non-accelerated

filer o

|

Smaller

reporting company o

|

|

|

(Do

not check if a smaller reporting company)

|

Indicate

by check mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Exchange Act). Yes o No

x

As

of June 30, 2009, the aggregate market value of the registrant’s Income Deposit

Securities (IDSs) held by non-affiliates of the registrant was $139.3 million

based on the closing sale price as reported on NASDAQ. Each IDS represents one

share of Class A Common Stock, par value $0.01 per share, and $7.50 principal

amount of senior subordinated notes due 2019. In determining the market value of

the registrant’s IDSs held by non-affiliates, IDSs beneficially owned by

directors, officers and holders of more than 10% of the registrant’s IDSs have

been excluded. This determination of affiliate status is not necessarily a

conclusive determination for other purposes.

As

of March 8, 2010, the registrant had 12,676,733 shares of Class A Common Stock,

par value $0.01 per share, and 544,671 shares of Class B Common Stock, par value

$0.01 per share, outstanding.

DOCUMENTS

INCORPORATED BY REFERENCE

Certain

information required in Part III of this report is incorporated by reference

from the registrant’s proxy statement to be filed pursuant to Regulation 14A

with respect to the registrant’s 2010 annual meeting of

stockholders.

OTELCO

INC.

TABLE

OF CONTENTS

i

Unless

the context otherwise requires, the words “we”, “us”, “our”, the “Company” and

“Otelco” refer to Otelco Inc., a Delaware corporation.

FORWARD-LOOKING

STATEMENTS

The

report contains forward-looking statements that are subject to risks and

uncertainties. Forward-looking statements give our current expectations relating

to our financial condition, results of operations, plans, objectives, future

performance and business. These statements may include words such as

“anticipate,” “estimate,” “expect,” “project,” “plan,” “intend,” “believe” and

other words and terms of similar meaning in connection with any discussion of

the timing or nature of future operating or financial performance or other

events. These forward-looking statements are based on assumptions that we have

made in light of our experience in the industry in which we operate, as well as

our perceptions of historical trends, current conditions, expected future

developments and other factors we believe are appropriate under the

circumstances. Although we believe that these forward-looking statements are

based on reasonable assumptions, you should be aware that many factors could

affect our actual financial condition or results of operations and cause actual

results to differ materially from those in the forward-looking statements. These

factors include, among other things, those discussed under the caption “Risk

Factors” in Item 1A.

History

We were

formed in Delaware in 1998 for the purpose of operating and acquiring rural

local exchange carriers, or RLECs. Since 1999, we have acquired ten RLEC

businesses, four of which serve contiguous territories in north central Alabama;

three of which serve territories adjacent to either Portland or Bangor, Maine;

one each which serve a portion of central Missouri, southern West Virginia and

western Massachusetts. We provide competitive services through several

subsidiaries in these territories. In addition, we acquired three facilities

based competitive local exchange carriers, or CLECs, which offer services as a

single entity in Maine and New Hampshire. The Company completed an initial

public offering of income deposit securities, or IDSs, in December 2004 at which

time it converted from a Delaware limited liability company into a Delaware

corporation and changed its name to Otelco Inc. In July 2007, the Company

completed an additional offering of 3,000,000 IDS units.

The

following table shows the aggregate number of our voice and data access lines

(which together are access line equivalents) and other services we offer such as

wholesale network connections, television, and other Internet customers as of

December 31, 2009:

|

Voice

and data access line equivalents

|

100,356 | |||

|

Wholesale

network connections

|

132,324 | |||

|

Cable

television customers

|

4,195 | |||

|

Other

Internet customers

|

9,116 |

The RLEC

companies we acquired can trace their history as local communications providers

to the introduction of telecommunications services in the areas they serve. We

are able to leverage our long-standing relationship with our local service

customers by offering them a broad suite of telecommunications and information

services, such as long distance, Internet/data access and, in some areas, cable

or satellite television, thereby increasing customer loyalty and revenue per

access line.

Our RLECs

have historically experienced relatively stable operating results and strong

cash flows and operate in supportive regulatory environments. Each RLEC

qualifies as a rural telephone company under the Federal Communications Act of

1934, or the Communications Act, so we are currently exempt from certain costly

interconnection requirements imposed on incumbent or historical local telephone

companies, or incumbent local exchange carriers, by the Communications Act.

While this exemption helps us maintain our strong competitive position, we do

have direct competition in portions of our RLEC market, primarily where another

cable provider also serves the same market. The cost of operations and capital

investment requirements for new entrants is high, discouraging such

investments.

In Maine

and New Hampshire, our facilities based CLEC serves primarily business

customers, utilizing our 296 mile fiber backbone network. In eleven years of

operations, the CLEC has grown to provide more than 32,000 voice and data access

lines.

Otelco

Telephone. On January 5, 1999, through Otelco Telephone LLC,

or Otelco Telephone, we acquired certain telecommunications businesses from

Oneonta Telephone Company, Inc., a rural local exchange carrier that serves a

portion of Blount county in Alabama. In connection with the transaction, we

acquired 8,127 voice and data access lines.

Hopper. On

September 30, 1999, we acquired Hopper Telecommunications Company, Inc., or

Hopper, a rural local exchange carrier that serves portions of Blount and Etowah

counties in Alabama. In connection with the transaction, we acquired 3,827 voice

and data access lines.

Brindlee

Mountain. On July 19, 2000, we acquired Brindlee Mountain

Telephone Company, or Brindlee, a rural local exchange carrier that serves

portions of Marshall, Morgan, Blount and Cullman counties in Alabama. In

connection with the transaction, we acquired 14,013 voice and data access

lines.

Blountsville. On

June 30, 2003, we acquired Blountsville Telephone Company, Inc., or

Blountsville, a rural local exchange carrier that serves a portion of Blount

county in Alabama. In connection with the transaction, we acquired 4,080 access

lines.

2

Mid-Missouri. On

December 21, 2004, we acquired Mid-Missouri Telephone Company, or Mid-Missouri,

a rural local exchange carrier that serves portions of Cooper, Moniteau, Morgan,

Pettis and Saline counties in central Missouri. In connection with the

transaction, we acquired approximately 4,585 voice and data access lines. In

addition, we provide Internet services in areas surrounding our

territory.

Mid-Maine. On July

3, 2006, we acquired Mid-Maine Communications, Inc., or Mid-Maine, a rural local

exchange carrier that serves portions of Penobscot, Somerset and Piscataquis

counties adjacent to Bangor, Maine and a competitive local exchange carrier,

serving customers adjacent to its fiber network along the I-95 corridor in

Maine. In connection with the transaction, we acquired approximately 22,413

voice and data access lines. In addition, we provide dial-up Internet services

throughout Maine.

Country Road. On

October 31, 2008, we acquired Pine Tree Holdings, Inc., Granby Holdings, Inc.

and War Holdings, Inc., which we collectively refer to as the CR Companies, from

Country Road Communications LLC. The three holding companies had four RLEC

operating subsidiaries: War Acquisition Corp., or War, serves areas in and

around War, West Virginia; The Granby Telephone and Telegraph Co. of Mass., or

Granby, serves areas in and around Granby, Massachusetts; and Saco River

Telegraph and Telephone Company, or Saco River, and The Pine Tree Telephone and

Telegraph Company, or Pine Tree, which collectively serve areas in and around

Buxton, Hollis, Waterboro, Gray and New Gloucester, Maine (adjacent to

Portland). There are also two CLEC subsidiaries providing services primarily to

business customers in Maine and New Hampshire – CRC Communications of Maine,

Inc. and Communications Design Acquisition Corporation, which we collectively

refer to as Pine Tree Networks. In connection with the transaction, we acquired

approximately 29,112 voice and data access lines and 93,994 wholesale network

connections.

The

following table reflects the percentage of total revenues derived from each of

our service offerings for the year ended December 31, 2009:

Revenue

Mix

|

Source

of Revenue

|

||||

|

Local

services

|

46.7 | % | ||

|

Network

access

|

32.1 | |||

|

Cable

television

|

2.4 | |||

|

Internet

|

13.5 | |||

|

Transport

services

|

5.3 | |||

|

Total

|

100.0 | % | ||

Local

Services

We are

the sole provider of wireline telephone services in seven of the ten RLEC

territories we serve. In the remaining three territories, the incumbent cable

provider also offers local services. Local services enable customers to

originate and receive telephone calls. The amount that we can charge a customer

for certain basic services in Alabama, Maine, Massachusetts, Missouri and West

Virginia is regulated by the Alabama Public Service Commission, or APSC; the

Maine Public Utilities Commission, or MPUC; the Massachusetts Department of

Telecommunications and Cable, or MDTC; the Missouri Public Service Commission,

or MPSC; and the West Virginia Public Service Commission, or WVPSC. We also have

authority to provide service in New Hampshire from the New Hampshire Public

Utilities Commission, or NHPUC. The regulatory involvement in pricing varies by

state and by type of service. Increasingly, bundled services involve less

regulation.

Revenue

derived from local services includes monthly recurring charges for voice access

lines providing local dial tone and calling features, including caller

identification, call waiting, call forwarding and voicemail. We also receive

revenue for providing long distance services to our customers, billing and

collection services for other carriers under contract, and directory

advertising. We provide local services on a retail basis to residential and

business customers. With the high level of acceptance of local service bundles,

a growing percentage of our customers receive a broad range of services,

including long distance, for a single, fixed monthly price.

We also

offer long distance telephone services to our local telephone customers who do

not purchase a local service bundle. We resell long distance services purchased

from various long distance providers. At December 31, 2009, customers

representing approximately 60% of our regulated access lines subscribed to our

long distance services. We intend to continue to expand our long distance

business within our rural local exchange carrier territories, principally

through bundling services for our local telephone customers.

3

In Maine and New Hampshire, our CLEC

provides communications services tailored to business customers, including

specialized data and voice network configurations, to support their unique

business requirements. Our fiber network in Maine allows us to offer our

customers affordable and reliable voice and data solutions to support their

business requirements and applications, which is a significant differentiator

for our Company in the competitive local exchange carrier environment in which

it operates. In connection with the acquisition of the CR Companies, the Company

acquired a multi-year contract with a large multiple system operator (“MSO”) for

the provision of wholesale network connections to the MSO’s customers in Maine

and New Hampshire. Various terms of the agreement were amended at the time of

the acquisition, including extending the contract through 2012. The customer

represented approximately 9.1% of the consolidated revenue for

2009.

We derive

revenue from other telephone related services, including leasing, selling,

installing, and maintaining customer premise telecommunications equipment and

the publication of local telephone directories in certain of our rural local

exchange carrier territories. We also provide billing and collection services

for interexchange carriers through negotiated billing and collection agreements

for certain types of toll calls placed by our local customers.

Network

Access

Network

access revenue relates primarily to services provided by us to long distance

carriers (also referred to as interexchange carriers) in connection with their

use of our facilities to originate and terminate interstate and intrastate long

distance, or toll, telephone calls. As toll calls are generally billed to the

customer originating the call, network access charges are applied in order to

compensate each telecommunications company providing services relating to the

call. Network access charges apply to both interstate and intrastate calls. Our

network access revenues also include revenues we receive from wireless carriers

for terminating their calls on our networks pursuant to our interconnection

agreements with those wireless carriers. Blountsville, Hopper, Mid-Maine,

Mid-Missouri, Pine Tree and War also receive Universal Service Fund High Cost

Loop, or USF HCL, revenue which is included in our reported network access

revenue.

Intrastate Access

Charges. We generate intrastate access revenue when a long

distance call involving a long distance carrier is originated and terminated

within the same state. The interexchange carrier pays us an intrastate access

payment for either terminating or originating the call. We record the details of

the call through our carrier access billing system. Our access charges for our

intrastate access services are set by the APSC, the MPUC, the MDTC, the MPSC,

the NHPUC, and the WVPSC for Alabama, Maine, Massachusetts, Missouri, New

Hampshire and West Virginia, respectively.

Interstate Access

Charges. We generate interstate access revenue when a long

distance call originates from an area served by one of our local exchange

carriers and terminates outside of that state, or vice versa. We bill interstate

access charges in a manner similar to intrastate access charges. Our RLEC

interstate access charges are regulated by the Federal Communications

Commission, or FCC, through our participation in tariffs filed by the National

Exchange Carriers Association, or NECA. The FCC regulates the prices local

exchange carriers charge for access services in two ways: price caps and

rate-of-return. All of our rural local exchange carriers are rate-of-return

carriers for purposes of interstate network access regulation. Interstate access

revenue for rate-of-return carriers is based on an FCC regulated rate-of-return

currently authorized up to 11.25% on investment and recovery of operating

expenses and taxes, in each case solely to the extent related to interstate

access.

Federal Universal Service Fund High

Cost Loop Revenue. Blountsville, Hopper, Mid-Maine,

Mid-Missouri, Pine Tree and War recover a portion of their costs through the USF

HCL, which is regulated by the FCC and administered by the Universal Service

Administrative Company, or USAC, a non-profit organization. Based on historic

and other information, a nationwide average cost per loop is determined by USAC.

Any incumbent local exchange carrier whose individual cost per loop exceeds the

nationwide average by more than 15% qualifies for USF HCL support. Although all

of our rural local exchange carriers have been designated as eligible

telecommunications carriers, or ETCs, Otelco Telephone, Brindlee, Granby and

Saco River do not receive USF HCL support because their cost per loop does not

exceed the national average by more than fifteen percent. The USF HCL, which is

funded by assessments on all United States telecommunications carriers as a

percentage of their revenue from end-users of interstate and international

service, distributes funds to our participating RLECs based upon their

respective costs for providing local services. USF HCL payments are received

monthly.

Transition Service Fund

Revenue. Otelco Telephone, Hopper, Brindlee, and Blountsville

recover a portion of their costs through the Transition Service Fund, or TSF,

which is administered by the APSC. All interexchange carriers originating or

completing calls in Alabama contribute to the TSF on a monthly basis, with the

amount of each carrier’s contribution calculated based upon its relative

originating and terminating minutes of use compared to the aggregate originating

and terminating minutes of use for all telecommunications carriers participating

in the TSF. The TSF reduces the vulnerability of our Alabama rural local

exchange carriers to a loss of access and interconnection revenue. TSF payments

are received monthly.

4

Maine Universal Service

Fund. Mid-Maine recovers a portion of its costs through the

Maine Universal Service Fund, or MUSF, which is administered by the

MPUC. All local and interexchange carriers in Maine contribute to the

MUSF on a monthly basis, with the amount of each carrier’s contribution

calculated based upon a percentage of retail intrastate revenues. The

MUSF was created to support RLEC universal service goals in response to

legislative mandates to reduce intrastate access rates.

Cable

Television Services

We

provide cable television services over networks with 750 MHz of transmission

capacity in the towns of Bunceton and Pilot Grove in Missouri, and in portions

of Blount and Etowah counties in Alabama. Our cable television packages offer

from 17 to 191 channels, depending upon the location in which the services are

offered. In December 2007, we upgraded our Alabama system to provide high

definition and digital video recording capability to our subscribers. In

December 2008, we completed the first phase of an Internet Protocol TV (IPTV)

expansion of our service in Alabama, offering a full set of programs to a

portion of the Blountsville service area. During 2009, we added three

communities within our Alabama service area. We are a licensed installer of

satellite television and have deployed these services to customers in our

Missouri territory.

Internet

Services

We

provide three forms of Internet access data lines to our customers: bulk

broadband data access to support large corporate users; digital high-speed data

lines in varying capacity speeds for business and residential use; and

residential dial-up connectivity. Digital high-speed Internet access is provided

via digital subscriber line, or DSL, cable modems or wireless broadband,

depending upon the location in which the service is offered and via dedicated

fiber connectivity to larger business customers. We charge our Internet

customers a flat rate for unlimited Internet usage and a premium for higher

speed Internet services. We are able to provide digital high-speed Internet data

lines to over 90% of our RLEC access lines and all of our CLEC lines. We intend

to expand the availability of our high-speed Internet services as warranted by

customer demand by installing additional DSL equipment at certain switching

locations. In Maine and Missouri, we provide dial-up Internet services

throughout the state.

Transport

Services

Our CLECs

receive monthly recurring revenues for the rental of fiber to transport data and

other telecommunications services in Maine from businesses and

telecommunications carriers along their fiber route. In 2009, we expanded this

network to over 296 miles.

Network

Assets

Our

telephone networks include carrier grade advanced switching capabilities

provided by traditional digital as well as software based switches; fiber rings

and routes; and network software supporting specialized business applications,

all of which meet industry standards for service integrity, redundancy,

reliability and flexibility. Our networks enable us to provide switched wireline

telephone services and other calling features; long distance services; digital

Internet access services through DSL and cable modems and dedicated circuits;

and specialized customer specific applications.

Our cable

television networks in Alabama and Missouri have been upgraded to a transmission

capacity of 750 MHz. Our cable television system in Alabama was upgraded in 2007

to deliver digital signals, high-definition program content and digital video

recording capability. IPTV capability was added in 2008 and its coverage

expanded to additional communities in 2009.

Sales,

Marketing & Customer Service

In Maine

and New Hampshire, our CLEC competes with the incumbent carriers throughout each

state, utilizing both an employee and agent sales force. Service configurations

are tailored to meet specific customer requirements, utilizing customer designed

voice and data telecommunications configurations. Increased service monitoring

for business customers is provided through a state of the art network operations

center and serves as a differentiator for our offers. Currently, we plan to

introduce the Otelco Inc. brand to replace the existing Mid-Maine and Pine Tree

brand names in our markets in 2010.

5

Our RLEC

marketing approach emphasizes locally managed, customer-oriented sales,

marketing and service. We believe that we are able to differentiate ourselves

from any competition by providing a superior level of service in our

territories. Each of our RLECs has a long history in the communities it serves,

which has helped to enhance our reputation among local residents by fostering

familiarity with our products and level of service. To demonstrate our

commitment to the markets we serve, we maintain local offices in most of the

population centers within our service territories. While customers have the

option of paying their bills by mail, credit card or automatic withdrawal from

their bank account, many elect to pay their monthly bill in person at the local

office. This provides us with an opportunity to directly market our services to

our existing customers. These offices typically are staffed by local residents

and provide sales and customer support services in the community. Local offices

facilitate a direct connection to the community, which we believe improves

customer satisfaction and enhances our reputation with local residents. We also

build upon our strong reputation by participating in local activities, such as

local fund raising and charitable events for schools and community organizations

and by airing local interest programs on our local access community cable

channels.

In order

to capitalize on the strong branding of each of our rural local exchange

carriers, while simultaneously establishing and reinforcing the “Otelco” brand

name across our service territories, we identify both the historical name of the

RLEC and Otelco on our marketing materials and other customer communications.

Part of our strategy is to increase customer loyalty and strengthen our brand

name by deploying new technologies and by offering comprehensive bundling of

services, including digital high-speed Internet access, cable and satellite

television, long distance and a full array of calling features. In addition, our

ability to provide our customers with a single, unified bill for all of our

services is a major competitive advantage and helps to enhance customer

loyalty.

Competition

Local

Services

We

believe that many of the competitive threats now confronting larger telephone

companies are not as significant in our RLEC service areas. The demographic

characteristics of rural telecommunications markets generally require

significant capital investment to offer competitive wireline telephone services

with low potential revenues. For instance, the per minute cost of operating both

telephone switches and interoffice facilities is higher in rural areas than in

urban areas, because rural local exchange carriers typically have fewer, more

geographically dispersed customers and lower calling volumes. Furthermore, the

distance from the telephone switch to the customer is typically longer in rural

areas, which results in increased distribution facilities costs that tend to

discourage wireline telephone competitors from entering territories serviced by

rural local exchange carriers. As a result, rural local exchange carriers

generally do not face the threat of significant wireline telephone competition

except in markets where a cable company provides existing services. We face

current or future direct competition from cable providers in portions of four of

our ten RLEC territories. New market entrants, such as providers of satellite

broadband or voice over electric lines and indirect competition such as voice

over Internet protocol, or VoIP, may gain traction in the future.

We

currently qualify for the rural exemption from certain interconnection

obligations which support industry competition, including obligations to provide

services for resale at discounted wholesale prices and to offer unbundled

network elements. If the APSC, MPUC, MDTC, NHPUC, MPSC or WVPSC terminates this

exemption for our rural local exchange carriers, we may face competition from

resellers and other wireline carriers.

In our

markets, we face competition from wireless carriers. We have experienced a

decrease in access lines as a result of customers switching their residential

wireline telephone service to a wireless service. We have also experienced an

increase in network access revenue associated with terminating wireless calls on

our telephone network. The introduction of residential bundled offerings

including unlimited calling appears to have shifted additional minutes back from

wireless. A portion of the wireless technology threat to our business is reduced

due in part to the topography of our telephone territories and current

inconsistent wireless coverage. However, as wireless carriers continue to employ

new technologies, we may experience increased competition from these

carriers.

The long

distance market remains competitive in all of our rural local exchange carrier

territories. We compete with major national and regional interexchange carriers,

including AT&T and Verizon, as well as wireless carriers, and other service

providers. However, we believe that our position as the rural local exchange

carrier in our territories, our long-standing local presence in our territories

and our ability to provide a single, unified bill for all of our services, are

major competitive advantages. At December 31, 2009, more than 60% of our

regulated access lines subscribed to our long distance services. The majority of

our CLEC customers have also selected us for their long distance services as

part of their overall package of services.

6

In

addition, under the Communications Act, a competitor can obtain USF HCL support

if a state public service commission (or the FCC in certain instances)

determines that it would be in the public interest and designates such

competitor as an ETC. While access to USF HCL support by our competitors

currently would not reduce our current USF HCL revenue, such economic support

could facilitate competition in our RLEC territories, particularly from wireless

carriers. The FCC is currently considering ways to reform USF HCL which could

impact amounts paid to and received from, as well as eligibility for payments

from, USF HCL.

In Maine

and New Hampshire, we operate as a facilities based competitive local exchange

carrier in a number of the larger metropolitan areas primarily currently served

by FairPoint Communications as the incumbent local exchange carrier. There are

other competitors who serve these markets today as both facilities based and

resale carriers. Our focus has been on the small to medium size business

customer with multiple locations and enterprise telecommunications requirements,

where we offer a combination of knowledge, experience and competitive pricing to

meet their specialized needs.

Cable

Television Services

We offer

cable television services in select areas of our territories and are a licensed

agent for a satellite provider. In 2008, we installed IPTV capability in the

Alabama territory not currently served by our cable operations. No provider has

overbuilt cable facilities in the areas we currently serve. In our Alabama

territory, Charter Communications, Inc. provides cable service, passing about

30% of our subscribers. In Maine, Time Warner Cable provides cable service,

passing approximately 60% of our RLEC subscribers. In addition, in all of our

cable television territories, we compete against digital broadcast satellite

providers including Dish Network and DirecTV.

Internet

Services

Competition

in the provision of RLEC data lines and Internet services currently comes from

alternative digital high-speed Internet service providers. Competitors vary on a

market-to-market basis and include Charter Communications, Inc., Time Warner

Cable, and a number of small, local competitors. At December 31, 2009, we

provided data access lines to approximately 41% of our rural access lines. In

Maine and Missouri, we also provide high-speed data lines and dial-up Internet

services to approximately 9,100 subscribers outside of our rural telephone

services territory. Our CLEC customers are provided a variety of data access

options, based on their individual requirements.

Transport

Services

Other

local telephone companies, long distance carriers, cable providers, utilities,

governments, and industry associations deploy and sell fiber capacity to users.

Existing and newly deployed capacity could be made available, impacting market

pricing. Multi-year contracts generally protect existing relationships and

provide revenue stability. The cost of and time required for deploying new fiber

can be a deterrent to adding capacity. We have expanded our fiber network in

Maine to reach additional locations and serve incremental

customers.

Information

Technology and Support Systems

We have

integrated software systems that function as operational support and customer

care/billing systems. One system serves our Alabama and Missouri local exchange

subscribers, one serves our additional Internet subscribers in Missouri, and one

serves our Maine, Massachusetts, New Hampshire and West Virginia subscribers.

The systems include automated provisioning and service activation, mechanized

line records and trouble reporting. These services are provided through the use

of licensed third-party software. By utilizing integrated software systems, we

are able to reduce individual company costs and standardize functions resulting

in greater efficiencies and profitability.

Each

system allows us to provide a single, unified bill for all our services which we

believe is a significant competitive advantage. Additionally, the systems

provide us an extensive database that enables us to gather detailed marketing

information in our service territories. This capability allows us to market new

services as they become available to particular customers. The Company has

implemented all currently established safeguards to Customer Proprietary Network

Information (CPNI) as established by the FCC for telecommunications providers

and is compliant with the “red flag” provisions of the Fair and Accurate Credit

Transactions Act.

Environment

We are

subject to various federal, state and local laws relating to the protection of

the environment. We believe that we are in compliance in all material respects

with all such laws. The environmental compliance costs incurred by us to date

have not been material, and we currently have no reason to believe that such

costs will become material in the foreseeable future.

7

Employees

As of

December 31, 2009, we employed 292 full-time and 7 part-time employees. None of

our employees are members of, or are represented by, any labor union or other

collective bargaining unit. We consider our relations with our employees to be

good.

Available

Information

Under the

Securities Exchange Act of 1934, we are required to file with or furnish to the

Securities and Exchange Commission, or SEC, annual, quarterly and current

reports, proxy and information statements and other information. You may read

and copy any document we file with or furnish to the SEC at the SEC’s Public

Reference Room at 100 F Street, N.E., Washington, D.C. 20549. Please call the

SEC at 1-800-SEC-0330 for further information about the Public Reference Room.

The SEC maintains a web site at http://www.sec.gov that

contains reports, proxy and information statements, and other information

regarding issuers that file electronically with the SEC. We file electronically

with the SEC.

We make

available, free of charge, through the investor relations section of our web

site, our reports on Forms 10-K, 10-Q and 8-K, and amendments to those reports,

as soon as reasonably practicable after they are filed with the SEC. The address

for our web site is

http://www.OtelcoInc.com.

Our Code

of Ethics applies to all of our employees, officers and directors, including our

chief executive officer and our chief financial officer and principal accounting

officer. The full text of the Code of Ethics is available at the investor

relations section of our web site, http://www.OtelcoInc.com. We

intend to disclose any amendment to, or waiver from, a provision of the Code of

Ethics that applies to our chief executive officer or chief financial officer

and principal accounting officer in the investor relations section of our web

site.

The

information contained on our web site is not part of, and is not incorporated

in, this or any other report we file with or furnish to the SEC.

In

evaluating our business, every investor should carefully consider the following

risks. Our business, financial condition or results of operation could be

materially adversely affected by any of the following risks.

Our

Business is Geographically Concentrated and Dependent on Regional Economic

Conditions.

Our

business is conducted primarily in north central Alabama, Maine, New Hampshire,

western Massachusetts, central Missouri and southern West Virginia and,

accordingly, our business is dependent upon the general economic conditions of

these regions. There can be no assurance that future economic conditions in

these regions, including the current global economic recession, will not impact

demand for our services or cause residents to relocate to other regions, which

may adversely impact our business, revenue and cash flow.

The

Telecommunications Industry has Experienced Increased Competition.

Although

we have historically experienced limited wireline telephone competition in many

of our RLEC territories, the market for telecommunications services is highly

competitive. Certain competitors benefit from brand recognition and financial,

personnel, marketing and other resources that are significantly greater than

ours. We cannot predict the number of competitors that will emerge, especially

as a result of existing or new federal and state regulatory or legislative

actions. Increased competition from existing and new entities could have an

adverse effect on our business, revenue and cash flow.

In all of

our markets, we face competition from wireless carriers, including the potential

for customers to export existing wireline telephone numbers to wireless service.

Our unlimited calling bundles provide our customers with an alternative to using

cell phones. As wireless carriers continue to build-out their networks and add

products and services aimed at the fixed wireless market, we may experience

increased competition, which could have an adverse effect on our business,

revenue and cash flow.

The

current and potential competitors in our RLEC territories include cable

television companies; competitive local exchange carriers and other providers of

telecommunications and data services, including Internet and VoIP service

providers; wireless carriers; satellite television companies; alternate access

providers; neighboring incumbent local exchange carriers; long distance

companies and electric utilities that may provide services competitive with

those products and services that we provide or intend to provide.

8

In Maine

and New Hampshire, our competitive local exchange carrier operations may

encounter a change in the competitive landscape that would impact its continued

ability to grow and/or retain customers, sustain current pricing plans, and

control the cost of access to incumbent carrier customers.

Although

our long distance operations have historically been modest in relation to our

competitors, we have expanded our long distance business within our territories,

primarily through bundling long distance with other local services and providing

a single bill for these services. Our existing long distance competitors,

including those with significantly greater resources than us, could respond to

such initiatives and new competitors may enter the market with attractive

offerings. There can be no assurance that our local services revenue, including

long distance services, will not decrease in the future as competition and/or

the cost of providing services increase.

We

May Not be Able to Integrate New Technologies and Provide New Services in a

Cost-Efficient Manner.

The

telecommunications industry is subject to rapid and significant changes in

technology, frequent new service introductions and evolving industry standards.

We cannot predict the effect of these changes on our competitive position, our

capital expenditure requirements, our profitability or the industry generally.

Technological developments may reduce the competitiveness of our networks and

require additional capital expenditures or the procurement of additional

products that could be expensive and time consuming. In addition, new products

and services arising out of technological developments may reduce the

attractiveness of our services. If we fail to adapt successfully to

technological advances or fail to obtain access to new technologies, we could

lose customers and be limited in our ability to attract new customers and/or

sell new services to our existing customers. In addition, delivery of new

services in a cost-efficient manner depends upon many factors, and we may not

generate the revenue anticipated from such services.

Disruptions

in Our Networks and Infrastructure May Cause Us to Lose Customers and Incur

Additional Expenses.

To be

successful, we will need to continue to provide our customers with reliable and

timely service over our networks. We face the following risks to our networks

and infrastructure:

|

●

|

our

territories could have significant weather events which physically damage

access lines;

|

|

●

|

our

rural geography creates the risk of security breaches, break-ins and

sabotage;

|

|

●

|

power

surges and outages, computer viruses or hacking, and software or hardware

defects which are beyond our control;

and

|

|

●

|

unusual

spikes in demand or capacity limitations in our or our suppliers’

networks.

|

Disruptions

may cause interruptions in service or reduced capacity for customers, either of

which could cause us to lose customers and/or incur expenses, and thereby

adversely affect our business, revenue and cash flow. In addition, the APSC,

MPUC, MDTC, MPSC, NHPUC and/or WVPSC could require us to issue credits on

customer bills for such service interruptions, further impacting revenue and

cash. Wholesale network contracts could impose service level penalties for

service disruptions.

Our

Success Depends on a Small Number of Key Personnel.

Our

success depends on the personal efforts of a small group of skilled employees

and senior management. The rural nature of our service area provides for a

smaller pool of skilled telephone employees and increases the challenge of

hiring employees. The loss of key personnel could have a material adverse effect

on our financial performance.

We

Provide Services to Our Customers Over Access Lines, and if We Lose Access

Lines, Our Business and Results of Operations May Be Adversely

Affected.

Our

business generates revenue by delivering voice and data services over access

lines. We have experienced net voice access line loss in our RLEC territories

due to challenging economic conditions, wireless substitution, loss of second

lines when we sell data access lines for Internet and increased competition.

RLEC voice access lines declined by approximately 6.4% during 2009. We expect to

continue to experience net voice access line loss in our rural markets, which

will be partially offset by increases in data access lines. If voice access line

losses are not substantially offset by data access line gains, it could

adversely affect our business and results of operations.

9

Our

Performance Is Subject to a Number of Other Economic and Non-Economic Factors,

Which We May Not Be Able to Predict Accurately.

There are

factors that may be beyond our control that could affect our operations and

business. Such factors include adverse changes in the conditions in the specific

markets for our products and services, the conditions in the broader market for

telecommunications services and the conditions in the domestic and global

economies, generally.

Although

our performance is affected by the general condition of the economy, not all of

our services are affected equally. Voice access revenue is generally linked to

relatively consistent variables such as population changes, housing starts and

general economic activity levels in the areas served. Data access and cable

television revenue is generally related to more variable factors such as

changing levels of discretionary spending on entertainment, the adoption of

e-commerce and other on-line activities by our current or prospective customers.

It is not possible for management to accurately predict all of these factors and

the impact of such factors on our performance.

Changes

in the competitive, technological and regulatory environments may also impact

our ability to increase revenue and/or earnings from the provision of local

wireline services. We may therefore have to place increased emphasis on

developing and realizing revenue through the provision of new and enhanced

services with higher growth potential. In such a case, there is a risk that

these revenue sources as well as our cost savings efforts through further

efficiency gains will not grow or develop at a fast enough pace to offset

slowing growth in local services. It is also possible that as we invest in new

technologies and services, demand for those new services may not develop. There

can be no assurance that we will be able to successfully expand our service

offerings through the development of new services, and our efforts to do so may

have a material adverse effect on our financial performance.

Changes

in the Regulation of the Telecommunications Industry Could Adversely Affect Our

Business, Revenue or Cash Flow.

We

operate in an industry that is regulated at the federal, state and local level.

The majority of our revenue has historically been supported by and subject to

regulation. Certain federal and state regulations and local franchise

requirements have been, are currently, and may in the future be, the subject of

judicial proceedings, legislative hearings and administrative proposals. Such

proceedings may relate to, among other things, the rates we may charge for our

local, network access and other services, the manner in which we offer and

bundle our services, the terms and conditions of interconnection, federal and

state universal service funds (including USF HCL), unbundled network elements

and resale rates, and could change the manner in which telecommunications

companies operate. We cannot predict the outcome of these proceedings or the

impact they will have on our business, revenue and cash flow.

Governmental

Authorities Could Decrease Network Access Charges or Rates for Local Services,

Which Would Adversely Affect Our Revenue.

Approximately

10.8% of our revenue for the year ended December 31, 2009 was derived from

interstate network access charges paid by long distance carriers for use of our

facilities to originate and terminate interstate and intrastate telephone calls.

The interstate network access rates that we can charge are regulated by the FCC,

and the intrastate network access rates that we can charge are regulated by the

regulatory commissions in each state in which we operate. Those rates may change

from time to time. The FCC has reformed and continues to reform the federal

network access charge system. It is unknown at this time what additional

changes, if any, the FCC or state regulatory commissions may adopt. Such

regulatory developments could adversely affect our business, revenue and cash

flow.

The local

services rates and intrastate access fees charged by our rural local exchange

carriers are regulated by state regulatory commissions which have the power to

grant and revoke authorization to companies to provide telecommunications

services and to impose other conditions and penalties. If we fail to comply with

regulations set forth by the state regulatory commissions, we may face

revocation of our authorizations in a state or other conditions and penalties.

It is possible that new plans would require us to reduce our rates, forego

future rate increases, provide greater features as part of our basic service

plan or limit our rates for certain offerings. We cannot predict the ultimate

impact, if any, of such changes on our business, revenue and cash

flow.

Our RLECs

operating in Maine, Missouri and West Virginia charge rates for local services

and intrastate access service based in part upon a rate-of-return authorized by

the state regulatory commissions. These authorized rates are subject to audit at

any time and may be reduced if the regulatory commission finds them excessive.

If any company is ordered to reduce its rates or if its applications to increase

rates are denied or delayed, our business, revenue and cash flow may be

negatively impacted.

10

NECA may

file revisions to its average schedule formula each year which are subject to

FCC approval. Five of our companies participate in average schedule rates. The

level of funding and future changes in the average schedule settlement rates are

not currently known with certainty and could be higher or lower.

A

Reduction in Universal Service Fund High Cost Loop Support Would Adversely

Affect Our Business, Revenue and Cash Flow.

Six of

our RLECs receive federal USF HCL revenue to support their high cost of

operations. Such support payments represented approximately 7.4% of our revenue

for the year ended December 31, 2009, and were based upon each participating

rural local exchange carrier’s average cost per loop as compared to the national

average cost per loop. These support payments fluctuate based upon the

historical costs of our participating rural local exchange carriers as compared

to the national average cost per loop. Each year, the average cost per loop has

increased, putting pressure on the USF HCL funds received by our companies to

the extent that our costs do not increase at the same rate. If our participating

rural local exchange carriers are unable to receive support from the USF HCL, or

if such support is reduced, our business, revenue and cash flow would be

negatively affected.

On May

16, 2006, the FCC released an order extending the current high-cost universal

support rules until the FCC adopts changes, if any, to these rules. The outcome

of any future FCC proceedings and other regulatory or legislative changes could

affect the amount of USF HCL support that we receive, and could have an adverse

effect on our business, revenue and cash flow. If a wireless or other

telecommunications carrier receives ETC status in our service areas or even

outside of our service areas, the amount of support we receive from the USF HCL

could decline under current rules, and under some proposed USF HCL rule changes,

could be significantly reduced.

USAC

serves as the administrative agent to collect data and distribute funds for USF.

In 2006, it began conducting High Cost Beneficiary audits, designed to ensure

compliance with FCC rules and program requirements and to assist in program

compliance. Carriers are chosen from a random sample of each type of ETC,

including average schedule and cost companies, incumbents and competitors, rural

and non-rural, from various states. Audits are designed to ensure proper

designation of a carrier as ETC, accuracy of data submissions, documentation of

accounting procedures, physical inventory of assets, true-up of projected data,

and samples of detailed documentation (e.g., invoices, continuing property

records). Audits of Blountsville, Hopper, Otelco Telephone and Brindlee Mountain

Telephone, during 2007 and 2008, have been completed and no material action is

pending. Granby was selected for audit in January 2008. The audit firm

subsequently withdrew from the audit and USAC has not replaced the auditor.

These audits are being conducted widely across our industry as directed by the

FCC. Currently, there is no guidance on the likelihood of the continuation of

the audit process currently available.

If

We Were to Lose Our Protected Status Under Interconnection Rules, We Would Incur

Additional Administrative and Regulatory Expenses and Face More

Competition.

As a

“rural telephone company” under the Communications Act, each of our RLECs is

exempt from the obligation to lease its unbundled facilities to competitive

local exchange carriers, to offer retail services at wholesale prices for

resale, to permit competitive co-location at its facilities and to comply with

certain other requirements applicable to larger incumbent local exchange

carriers. However, we eventually may be required to comply with these

requirements in some or all of our service areas if: (i) we receive a bona fide

request from a telecommunications carrier; and (ii) the state regulatory

commissions, as applicable, determine that it is in the public interest to

impose such requirements. In addition, we may be required to comply with some or

all of these requirements in order to achieve greater pricing flexibility from

state regulators. If we are required to comply

with these requirements, we could incur additional administrative and regulatory

expenses and face more competition which could adversely affect our business,

revenue and cash flow.

Our

Current Dividend Policy May Negatively Impact Our Ability to Maintain or Expand

Our Network Infrastructure and Finance Capital Expenditures or

Operations.

Our board

of directors has adopted a dividend policy pursuant to which substantially all

of the cash generated by our business in excess of operating needs, interest and

principal payments on indebtedness, and capital expenditures sufficient to

maintain our network infrastructure, would in general be distributed as regular

quarterly cash dividends to the holders of our Class A common stock and not

retained by us. As a result, we may not have a sufficient amount of cash to fund

our operations in the event of a significant business downturn, finance growth

of our network or unanticipated capital expenditure needs. We may have to forego

growth opportunities or capital expenditures that would otherwise be necessary

or desirable if we do not find alternative sources of financing or if we do not

modify our dividend policy. If we do not have sufficient cash for these

purposes, our financial condition and our business will suffer or our board of

directors may change our dividend policy. Our Class B common stockholders have

notified us of their intent to exchange their Class B shares for income deposit

securities during 2010, which will increase the number of Class A shares with a

resultant increase in dividend cost within the current policy.

11

We

Are Subject to Restrictive Debt Covenants That Limit Our Business Flexibility By

Imposing Operating and Financial Restrictions on Our Operations.

The

agreements governing our indebtedness impose significant operating and financial

restrictions on us. These restrictions prohibit or limit, among other

things:

|

●

|

the

incurrence of additional indebtedness and the issuance of preferred stock

and certain redeemable capital

stock;

|

|

●

|

the

making of certain types of restricted payments, including investments and

acquisitions;

|

|

●

|

specified

sales of assets;

|

|

●

|

specified

transactions with affiliates;

|

|

●

|

the

creation of a number of liens;

|

|

●

|

consolidations,

mergers and transfers of all or substantially all of our assets;

and

|

|

●

|

our

ability to change the nature of our

business.

|

None.

Our

property consists primarily of land and buildings; central office, Internet and

cable equipment; computer software; telephone lines; and related equipment. Our

telephone lines include aerial and underground cable, conduit, poles and wires.

Our central office equipment includes digital and software defined switches,

Internet and other servers and related peripheral equipment. We own

substantially all our real property in Alabama and Missouri, including our

corporate office. We primarily lease property in Maine, Massachusetts and West

Virginia, including our primary office locations in Bangor, New Gloucester and

Portland, Maine; Granby, Massachusetts; and War, West Virginia. We also lease

certain other real property, including land in Oneonta, Alabama, pursuant to a

long-term, renewable lease. A small portion of our Alabama cable television

service equipment is located on this leased property. As of December 31, 2009,

our property and equipment consisted of the following:

|

(In

Thousands)

|

||||

|

Land

|

$ | 1,105 | ||

|

Buildings

and improvements

|

11,354 | |||

|

Telephone

equipment

|

205,839 | |||

|

Cable

television equipment

|

9,628 | |||

|

Furniture

and equipment

|

2,889 | |||

|

Vehicles

|

5,554 | |||

|

Computer

software and equipment

|

13,315 | |||

|

Internet

equipment

|

3,426 | |||

|

Total

property and equipment

|

253,110 | |||

|

Accumulated

depreciation

|

(184,081 | ) | ||

|

Net

property and equipment

|

$ | 69,029 | ||

12

Our

senior credit facility is secured by substantially all of the assets of our

subsidiaries that are guarantors of the senior credit facility. As of December

31, 2009, the subsidiary guarantors represent $57.8 million of the $69.0 million

in net property and equipment.

From time

to time, we may be involved in various claims, legal actions and regulatory

proceedings incidental to and in the ordinary course of business, including

administrative hearings of the APSC, MPUC, MDTC, MPSC, NHPUC, and WVPSC relating

primarily to rate making and customer service requirements. Currently, none of

the legal proceedings are expected to have a material adverse effect on our

business.

The

following table sets forth the names and positions of our executive officers and

certain other officers, and their ages as of December 31, 2009.

|

Name

|

Age

|

Position

|

||

|

Michael

D. Weaver

|

57

|

President,

Chief Executive Officer and Director

|

||

|

Curtis

L. Garner, Jr.

|

62

|

Chief

Financial Officer

|

||

|

Dennis

Andrews

|

53

|

Senior

Vice President and General Manager, Alabama

|

||

|

Jerry

C. Boles

|

57

|

Vice

President and Controller

|

||

|

Gary

B. Romig

|

59

|

Vice

President and General Manager, Missouri

|

||

|

Nicholas

A. Winchester

|

40

|

Senior

Vice President and General Manager, New England

|

||

|

Robert

J. Souza

|

56

|

Vice

President of Operations, New

England

|

Michael D. Weaver has served

as our President, Chief Executive Officer and a Director since January 1999.

Prior to this time, he spent 10 years with Oneonta Telephone Co., Inc., the

predecessor to Otelco Telephone, serving as Chief Financial Officer from 1990 to

1998 and General Manager from January 1998 to January 1999.

Curtis L. Garner, Jr. has

served as our Chief Financial Officer since February 2004. Prior to this

position, he provided consulting services to a number of businesses and

not-for-profit organizations from October 2002. He served PTEK

Holdings, Inc. from November 1997 through September 2002 (including one year as

a consultant), first as President of one of its divisions, and later as Chief

Administrative Officer for another division. Prior thereto, he spent 26 years at

AT&T Corp., retiring in 1997 as the Chief Financial Officer of the Southern

and Southwestern Regions of AT&T Corp.’s consumer long distance

business.

Dennis Andrews was appointed

Senior Vice President and General Manager of our Alabama division in August

2006. He served as our Vice President and General Manager, Brindlee and

Blountsville since November 2005 and Vice President — Regulatory

Affairs since July 2000. Prior to this position, he spent 21 years at Brindlee

where he held several positions, including Vice President — Finance,

General Manager, Operations Manager and Accounting Department

Manager.

Jerry C. Boles has served as

our Vice President and Controller since he joined the Company in January 1999.

Prior to joining Otelco, he was controller for McPherson Oil Company for 14

years. He also worked in public accounting for 10 years, is licensed as a CPA by

the state of Alabama, and is a member in good standing of the American Institute

of Certified Public Accountants.

Gary B. Romig has served as

our Vice President and General Manager of our Missouri division since its

acquisition in December 2004. He served as Co-President of Mid-Missouri for five

years prior to the acquisition by Otelco. He joined Mid-Missouri in May 1973 and

has been involved in all aspects of the outside plant operation.

Nicholas A. Winchester joined

Otelco in July 2006 as the Senior Vice President and General Manager of our New

England division (previously known as our Maine division). He served as the

President of Mid-Maine when it was acquired by Otelco. From 1998 through 2005,

he served in various leadership positions in the sales organization, building

the successful competitive sales team for Mid-Maine.

13

Robert J. Souza joined Otelco

in October 2008 as the Vice President of Operations for New England. He served

as President for the CR Companies from 2001 until they were acquired by Otelco

in October 2008. Prior to that role, he served as Operations Manager for Saco

River, having joined that company in 1983. His 34 years experience in the

industry includes three years with Ooltewah-Collegedale Telephone Company in

Tennessee and five years with New England Telephone in Maine.

Officers

are not elected for a fixed term of office but hold their position until a

successor is named.

14

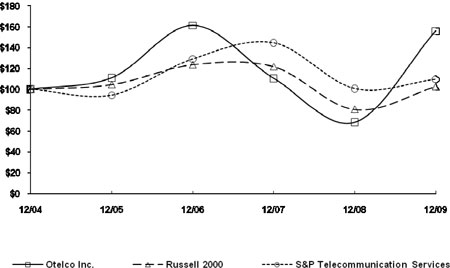

Market

Information

We have

outstanding two separate classes of common stock, our Class A common stock, par

value $0.01 per share, and our Class B common stock, par value $0.01 per

share.

Our IDSs,

each representing one share of Class A common stock and $7.50 principal amount

of senior subordinated notes due 2019, began trading on the American Stock

Exchange, or AMEX, under the symbol “OTT” and on the Toronto Stock Exchange, or

TSX, under the symbol “OTT.un” on December 16, 2004. On June 30, 2008, the

Company voluntarily withdrew its listing on the AMEX and began trading on the

NASDAQ Global Market, or NASDAQ, continuing to use the symbol “OTT”. During this

period, our IDSs continued to trade on the TSX. The high and low for the IDSs on

the AMEX and NASDAQ, as applicable, during the quarters indicated are as

follows:

|

High

($US)

|

Low

($US)

|

|||||||

|

2009

|

||||||||

|

Fourth

Quarter

|

$ | 15.76 | $ | 12.74 | ||||

|

Third

Quarter

|

$ | 13.34 | $ | 10.90 | ||||

|

Second

Quarter

|

$ | 13.24 | $ | 9.41 | ||||

|

First

Quarter

|

$ | 9.55 | $ | 7.70 | ||||

|

2008

|

||||||||

|

Fourth

Quarter

|

$ | 14.27 | $ | 6.79 | ||||

|

Third

Quarter

|

$ | 16.50 | $ | 12.50 | ||||

|

Second

Quarter

|

$ | 17.23 | $ | 13.61 | ||||

|

First

Quarter

|

$ | 18.20 | $ | 14.00 | ||||

There is

no established trading market for our Class B common stock. The Class B common

stock became exchangeable for IDS units on a one-for-one basis without a

financial test after December 21, 2009. On December 30, 2009, the holders of the

Class B shares notified the Company of their desire to exchange their Class B

shares for IDS units in accordance with the Investor Rights Agreement dated as

of December 21, 2004.

Holders

As of

March 8, 2010, there were approximately 14,500 record holders of our IDSs.

Holders of our IDSs have the right to separate the IDSs into the shares of Class

A common stock and senior subordinated notes represented thereby. As of the date

of this report, no holder has elected to separate the IDSs.

As of

March 8, 2010, there were approximately 10 record holders of our Class B common

stock.

Dividends

The board

of directors declared and the Company paid dividends of $0.17625 per Class A

common share each quarter in 2007, 2008 and 2009 for a total of $0.705 per share

for each year. The dividend in the fourth quarter of 2006 was paid on January 2,

2007. For 2007, $0.02 of the dividend was considered qualified for holder tax

purposes and the balance was considered a non-taxable return of capital. For

2008 and 2009, all of the dividends were considered a non-taxable return of

capital. The Company has paid dividends each quarter since the completion of its

initial public offering in December 2004.

The

payment of dividends on our Class B common stock is prohibited by our

certificate of incorporation. As such, we have never declared or paid cash

dividends on our Class B common stock, nor do we intend to declare or pay cash

dividends on our Class B common stock. Class B stockholders have requested that

their Class B shares be exchanged for IDS units during 2010.

15

Our board

of directors has adopted a dividend policy for our Class A common stock pursuant

to which, in the event and to the extent we have any available cash for

distribution to the holders of shares of our Class A common stock and subject to

applicable law and the terms of our credit facility, the indenture governing our

senior subordinated notes and any other then outstanding indebtedness of ours,

our board of directors will declare cash dividends on our Class A common stock.

Our dividend policy reflects a basic judgment that our stockholders would be

better served by distributing available cash in the form of dividends rather

than retaining it. Under this dividend policy, cash generated by our business in

excess of operating needs, interest and principal payments on indebtedness,

capital expenditures and income taxes, if any, would in general be distributed

as regular quarterly dividends to the holders of our Class A common stock rather

than retained by us as cash on our consolidated balance sheet. In determining

our expected dividend levels, we review and analyze, among other things, our

operating and financial performance; the anticipated cash requirements

associated with our capital structure; our anticipated capital expenditure

requirements; our expected other cash needs; the terms of our debt instruments,

including our credit facility; other potential sources of liquidity; and various

other aspects of our business. If these factors change, the board would need to

reassess our dividend policy.

As

described more fully below, holders of our Class A common stock may not receive

any dividends as a result of the following factors:

|

●

|

nothing

requires us to pay dividends;

|

|

●

|

while

our current dividend policy contemplates the distribution of our available

cash, this policy could be modified or revoked at any

time;

|

|

●

|

even

if our dividend policy were not modified or revoked, the actual amount of

dividends distributed under the policy and the decision to make any

distribution is entirely at the discretion of our board of

directors;

|

|

●

|

the

amount of dividends distributed is subject to covenant restrictions in our

indenture and our credit facility;

|

|

●

|

the

amount of dividends distributed is subject to state law

restrictions;

|

|

●

|

our

stockholders have no contractual or other legal right to dividends;

and

|

|

●

|

we

may not have enough cash to pay dividends due to changes to our operating

earnings, working capital requirements and anticipated cash

needs.

|

Dividends

on our Class A common stock will not be cumulative. Consequently, if dividends

on our Class A common stock are not declared and/or paid at the targeted levels,

our stockholders will not be entitled to receive such payments in the

future.

If we

have any remaining cash after the payment of dividends as contemplated above,

our board of directors will, in its sole discretion, decide to use that cash to

fund capital expenditures or acquisitions, repay indebtedness, pay additional

dividends or for general corporate purposes.

Restrictions

on Payment of Dividends

The

indenture governing our senior subordinated notes restricts our ability to

declare and pay dividends on our common stock as follows:

|

●

|

we

may only pay dividends in any given fiscal quarter equal to 100% of our

excess cash for the period from and including the first fiscal quarter

beginning after the date of the indenture to the end of our most recently

ended fiscal quarter for which internal financial statements are available

at the time of such payment. “Excess Cash” means with respect to any

period, Adjusted EBITDA, as defined in the indenture, minus the sum of (i)

cash interest expense, (ii) capital expenditures and (iii) cash income tax

expense, in each case, for such

period;

|

|

●

|

we

may not pay dividends if our interest coverage ratio, which is defined as

Adjusted EBITDA divided by consolidated interest expense, is below 1.4

times;

|

|

●

|

we

may not pay any dividends if not permitted under any of our senior

indebtedness;

|

16

|

●

|

we

may not pay any dividends while interest on the senior subordinated notes

is being deferred or, after the end of any interest deferral, so long as

any deferred interest has not been paid in full;

and

|

|