Attached files

| file | filename |

|---|---|

| EX-32 - EXHIBIT 32 - HANGER, INC. | a2196899zex-32.htm |

| EX-21 - EXHIBIT 21 - HANGER, INC. | a2196899zex-21.htm |

| EX-23.1 - EXHIBIT 23.1 - HANGER, INC. | a2196899zex-23_1.htm |

| EX-10.(D) - EXHIBIT 10(D) - HANGER, INC. | a2196899zex-10_d.htm |

| EX-31.1 - EXHIBIT 31.1 - HANGER, INC. | a2196899zex-31_1.htm |

| EX-31.2 - EXHIBIT 31.2 - HANGER, INC. | a2196899zex-31_2.htm |

Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO FINANCIAL STATEMENTS

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

ý |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. |

|

For the fiscal year ended December 31, 2009 |

||

OR |

||

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. |

|

For the transition period from to |

||

Commission File Number 1-10670

HANGER ORTHOPEDIC GROUP, INC.

(Exact name of registrant as specified in its charter.)

| Delaware (State or other jurisdiction of incorporation or organization) |

84-0904275 (I.R.S. Employer Identification No.) |

|

Two Bethesda Metro Center (Suite 1200), Bethesda, MD (Address of principal executive offices) |

20814 (Zip Code) |

Registrant's phone number, including area code: (301) 986-0701

Securities registered pursuant to Section 12(b) of the Act:

| Title of class | Name of exchange on which registered | |

|---|---|---|

| Common Stock, par value $0.01 per share | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark whether the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days: Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files. Yes o No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of "accelerated filer and large accelerated filer" in Rule 12b-2 of the Exchange Act. (Check one).

| Large accelerated filer o | Accelerated filer ý | Non-accelerated filer o | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company as defined in Rule 12b-2 of the Exchange Act. Yes o No ý

State the aggregate market value of the registrant's voting and non-voting common equity held by non-affiliates of the registrant computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant's most recently completed second fiscal quarter. $428,417,262

As of February 22, 2010 the registrant had 31,901,708 shares of its Common Stock issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

The information called for by Part III of the Form 10-K is incorporated by reference from the registrant's definitive proxy statement or amendment hereto which will be filed not later than 120 days after the end of the fiscal year covered by this report.

INDEX

2

Business Overview

General

We are the largest owner and operator of orthotic and prosthetic ("O&P") patient-care centers ("patient -care centers") in the United States, accounting for approximately 27% of the estimated $2.6 billion O&P patient-care market. At December 31, 2009, we operated 677 O&P patient-care centers in 45 states and the District of Columbia and employed in excess of 1,000 revenue-generating O&P practitioners ("practitioners"). In addition, through our wholly-owned subsidiary, Southern Prosthetic Supply, Inc. ("SPS"), we are the largest distributor of branded and private label O&P devices and components in the United States, all of which are manufactured by third parties. We also create new products, through our wholly-owned subsidiary, Innovative Neurotronics, Inc. ("IN, Inc.") for patients who have had a loss of mobility due to strokes, multiple sclerosis or other similar conditions. Another subsidiary, Linkia LLC ("Linkia"), develops programs to manage all aspects of O&P patient care for large private payors.

For the years ended December 31, 2009, 2008, and 2007, our net sales were $760.1 million, $703.1 million, and $637.4 million, respectively. We recorded net income of $36.1 million, $26.7 million, and $19.3 million, for the years ended December 31, 2009, 2008, and 2007, respectively.

We conduct our operations in two segments—patient care services and distribution. For the year ended December 31, 2009, net sales attributable to our patient-care services segment and distribution segment were $670.4 and $88.0 million, respectively, and for the year ended December 31, 2008, net sales attributable to our patient-care services segment and distribution segment were $620.0 million and $80.7 million, respectively. See Note P to our consolidated financial statements contained herein elsewhere in this Annual Report on Form 10-K for financial information about our segments.

Industry Overview

We estimate that the O&P patient care market in the United States is approximately $2.6 billion, of which we account for approximately 27%. The O&P patient care services market is highly fragmented and is characterized by local, independent O&P businesses, with the majority generally having a single facility with annual revenues of less than $1.0 million. We do not believe that any of our patient care competitors account for a market share of more than 2% of the country's total estimated O&P patient care services revenue.

The care of O&P patients is part of a continuum of rehabilitation services including diagnosis, treatment and prevention of future injury. This continuum involves the integration of several medical disciplines that begins with the attending physician's diagnosis. A patient's course of treatment is generally determined by an orthopedic surgeon, vascular surgeon or physiatrist, who writes a prescription and refers the patient to an O&P patient care services provider for treatment. A practitioner then, using the prescription, consults with both the referring physician and the patient to formulate the design of an orthotic or prosthetic device to meet the patient's needs.

The O&P industry is characterized by stable, recurring revenues, primarily resulting from the need for periodic replacement and modification of O&P devices. Based on our experience, the average replacement time for orthotic devices is one to three years, while the average replacement time for prosthetic devices is three to five years. There is also an attendant need for continuing O&P patient care services. In addition to the inherent need for periodic replacement and modification of O&P

3

devices and continuing care, we expect the demand for O&P services will continue to grow as a result of several key trends, including:

Aging U.S. Population. The growth rate of the over-65 age group is nearly triple that of the under-65 age group. There is a direct correlation between age and the onset of diabetes and vascular disease, which are the leading causes of amputations. With broader medical insurance coverage, increasing disposable income, longer life expectancy, greater mobility expectations and improved technology of O&P devices, we believe the elderly will increasingly seek orthopedic rehabilitation services and products.

Growing Physical Health Consciousness. The emphasis on physical fitness, leisure sports and conditioning, such as running and aerobics, is growing, which has led to increased injuries requiring orthopedic rehabilitative services and products. These trends are evidenced by the increasing demand for new devices that provide support for injuries, prevent further or new injuries or enhance physical performance.

Increased Efforts to Reduce Healthcare Costs. O&P services and devices have enabled patients to become ambulatory more quickly after receiving medical treatment in the hospital. We believe that significant cost savings can be achieved through the early use of O&P services and products. The provision of O&P services and products in many cases reduces the need for more expensive treatments, thus representing a cost savings to third-party payors.

Advancing Technology. The range and effectiveness of treatment options for patients requiring O&P services have increased in connection with the technological sophistication of O&P devices. Advances in design technology and lighter, stronger and more cosmetically acceptable materials have enabled patients to replace older O&P devices with new O&P products that provide greater comfort, protection and patient acceptability. As a result, treatment can be more effective or of shorter duration, giving the patient greater mobility and a more active lifestyle. Advancing technology has also increased the prevalence and visibility of O&P devices in many sports, including skiing, running and tennis.

Competitive Strengths

We believe the combination of the following competitive strengths will help us in growing our business through an increase in our net sales, net income and market share:

- •

- Leading market position, with an approximate 27% share of total industry revenues and operations in 45 states and the

District of Columbia, in an otherwise fragmented industry;

- •

- National scale of operations, which has better enabled us to:

- •

- establish our brand name and generate economies of scale;

- •

- implement best practices throughout the Company;

- •

- utilize shared fabrication facilities;

- •

- contract with national and regional managed care entities;

- •

- identify, test and deploy emerging technology; and

- •

- increase our influence on, and input into, regulatory trends;

- •

- Distribution of, and purchasing power for, O&P components and finished O&P products, which enables us

to:

- •

- negotiate greater purchasing discounts from manufacturers and freight providers;

4

- •

- reduce patient-care center inventory levels and improve inventory turns through centralized purchasing

control;

- •

- quickly access prefabricated and finished O&P products;

- •

- promote the usage by our patient-care centers of clinically appropriate products that also enhance our profit

margins;

- •

- engage in co-marketing and O&P product development programs with suppliers; and

- •

- expand the non-Hanger client base of our distribution segment;

- •

- Development of leading-edge technology to be brought to market through our patient practices and licensed

distributors worldwide;

- •

- Full O&P product offering, with a balanced mix between orthotics services and products and prosthetics services and

products;

- •

- Practitioner compensation plans that financially reward practitioners for their efficient management of accounts

receivable collections, labor, materials, and other costs, and encourage cooperation among our practitioners within the same local market area;

- •

- Proven ability to rapidly incorporate technological advances in the fitting and fabrication of O&P devices;

- •

- History of successful integration of small and medium-sized O&P business acquisitions, including 83 O&P businesses since

1997, representing over 204 patient-care centers;

- •

- Highly trained practitioners, whom we provide with the highest level of continuing education and training through programs

designed to inform them of the latest technological developments in the O&P industry, and our certification program located at the University of Connecticut; and

- •

- Experienced and committed management team; and

- •

- Successful government relations efforts including:

- •

- Supported our patients' efforts to pass "The Prosthetic Parity Act" in 11 states;

- •

- Increased Medicaid reimbursement levels in several states; and

- •

- Created the Hanger Orthopedic Political Action Committee (The Hanger PAC).

Business Strategy

Our goal is to continue to provide superior patient care and to be the most cost-efficient, full service, national O&P operator. The key elements of our strategy to achieve this goal are to:

- •

- Improve our performance by:

- •

- developing and deploying new processes to improve the productivity of our practitioners;

- •

- continuing periodic patient evaluations to gauge patients' device and service satisfaction;

- •

- improving the utilization and efficiency of administrative and corporate support services;

- •

- enhancing margins through continued consolidation of vendors and product offering; and

- •

- leveraging our market share to increase sales and enter into more competitive payor contracts;

5

- •

- Increase our market share and net sales by:

- •

- continued marketing of Linkia to regional and national providers and contracting with national and regional managed care

providers who we believe select us as a preferred O&P provider because of our reputation, national reach, density of our patient-care centers in certain markets and our ability to monitor

quality and outcomes as well as reducing administrative expenses;

- •

- increasing our volume of business through enhanced comprehensive marketing programs aimed at referring physicians and

patients, such as our Patient Evaluation Clinics program, which reminds patients to have their devices serviced or replaced and informs them of technological improvements of which they can take

advantage; and our "People in Motion" program which introduces potential patients to the latest O&P technology;

- •

- expanding the breadth of products being offered out of our patient-care centers; and

- •

- increasing the number of practitioners through our residency program;

- •

- Develop businesses that provide services and products to the broader rehabilitation and post-surgical

healthcare areas;

- •

- Continue to create, license or patent and market devices based on new cutting edge technology. We anticipate bringing new

technology to the market through our IN, Inc. product line. The first new product, the WalkAide System, was released for sale on May 1, 2006;

- •

- Selectively acquire small and medium-sized O&P patient care service businesses and open satellite patient-care

centers primarily to expand our presence within an existing market and secondarily to enter into new markets; and

- •

- Develop new delivery channels for our traditional O&P products; and

- •

- Provide our practitioners with:

- •

- the training necessary to utilize existing technology for different patient service facets, such as the use of our

Insignia scanning system for burns and cranial helmets;

- •

- career development and increased compensation opportunities;

- •

- a wide array of O&P products from which to choose;

- •

- administrative and corporate support services that enable them to focus their time on providing superior patient care; and

- •

- selective application of new technology to improve patient care.

Business Description

Patient Care Services

As of December 31, 2009, we provided O&P patient care services through 677 patient-care centers and over 1,000 practitioners in 45 states and the District of Columbia. Substantially all of our practitioners are certified, or are candidates for formal certification, by the O&P industry certifying boards. One or more practitioners closely manage each of our patient-care centers. Our patient-care centers also employ highly trained technical personnel who assist in the provision of services to patients and who fabricate various O&P devices, as well as office administrators who schedule patient visits, obtain approvals from payors and bill and collect for services rendered.

An attending physician determines a patient's treatment, writes a prescription and refers the patient to one of our patient-care centers. Our practitioners then consult with both the referring

6

physician and the patient with a view toward assisting in the formulation of the prescription for, and design of, an orthotic or prosthetic device to meet the patient's need.

The fitting process often involves several stages in order to successfully achieve desired functional and cosmetic results. The practitioner creates a cast and takes detailed measurements, frequently using our digital imaging system (Insignia), of the patient to ensure an anatomically correct fit. Prosthetic devices are custom fabricated by technicians and fit by skilled practitioners. The majority of the orthotic devices provided by us are custom designed, fabricated and fit; the remainder are prefabricated but custom fit.

Custom devices are fabricated by our skilled technicians using the plaster castings, measurements and designs made by our practitioners as well as utilization of our proprietary Insignia system. The Insignia system replaces plaster casting of a patient's residual limb with the generation of a computer scanned image. Insignia provides a very accurate image, faster turnaround for the patient, and a more professional overall experience. Technicians use advanced materials and technologies to fabricate a custom device under quality assurance guidelines. Custom designed devices that cannot be fabricated at the patient-care centers are fabricated at one of several central fabrication facilities. After final adjustments to the device by the practitioner, the patient is instructed in the use, care and maintenance of the device. Training programs and scheduled follow-up and maintenance visits are used to provide post-fitting treatment, including adjustments or replacements as the patient's physical condition and lifestyle change.

To provide timely service to our patients, we employ technical personnel and maintain laboratories at many of our patient-care centers. We have earned a strong reputation within the O&P industry for the development and use of innovative technology in our products, which has increased patient comfort and capability, and can significantly enhance the rehabilitation process. The quality of our products and the success of our technological advances have generated broad media coverage, building our brand equity among payors, patients and referring physicians.

A substantial portion of our O&P services involves the treatment of a patient in a non-hospital setting, such as our patient-care centers, a physician's office, an out-patient clinic or other facility. In addition, O&P services are increasingly rendered to patients in hospitals, long-term care facilities, rehabilitation centers and other alternate-site healthcare facilities. In a hospital setting, the practitioner works with a physician to provide either orthotic devices or temporary prosthetic devices that are later replaced by permanent prosthetic devices.

Patient-Care Center Administration

We provide all accounting, accounts payable, payroll, sales and marketing, management information systems, real estate, acquisitions and human resources services for our patient-care centers on either a centralized or out-sourced basis. As a result, we are able to provide these services more efficiently and cost-effectively than if these services had to be generated at each patient-care center. Moreover, the centralization or out-sourcing of these services permits our practitioners to allocate a greater portion of their time to patient care activities by reducing their administrative responsibilities.

We also develop and implement programs designed to increase sales and enhance the efficiency of our patient-care centers. These programs include: (i) sales and marketing initiatives to attract new patient referrals by establishing relationships with physicians, therapists, employers, managed care organizations, hospitals, rehabilitation centers, out-patient clinics and insurance companies; (ii) professional management and information systems to improve efficiencies of administrative and operational functions; (iii) professional education programs for practitioners emphasizing new developments in the increasingly sophisticated field of O&P clinical therapy; (iv) the establishment of shared fabrication and centralized purchasing activities, which provide access to component parts and products within two business days at prices that are typically lower than traditional procurement

7

methods; (v) access to virtually every product available at lower cost due to the combined purchasing power of our patient-care centers; and (vi) access to technology, such as Insignia, that is not available to our competitors.

Distribution Services

We distribute O&P components to the O&P market as a whole and to our own patient-care centers through our wholly-owned subsidiary, SPS, which is the nation's largest O&P distributor. We are also a leading manufacturer and distributor of therapeutic footwear for diabetic patients in the podiatric market. For the year ended December 31, 2009, 36.2% or approximately $88.0 million of SPS' distribution sales were to third-party O&P services providers, and the balance of approximately $155.0 million represented intercompany sales to our patient-care centers. SPS maintains in inventory approximately 25,000 O&P related items, all of which are manufactured by other companies. SPS maintains distribution facilities in California, Florida, Georgia, Pennsylvania, and Texas, which allows us to deliver products via ground shipment anywhere in the contiguous United States typically within two business days.

Our distribution business enables us to:

- •

- lower our material costs by negotiating purchasing discounts from manufacturers;

- •

- reduce our patient-care center inventory levels and improve inventory turns through centralized purchasing

control;

- •

- quickly access prefabricated and finished O&P products;

- •

- perform inventory quality control;

- •

- encourage our patient-care centers to use clinically appropriate products that enhance our profit margins; and

- •

- coordinate new product development efforts with key vendor "partners".

This is accomplished at competitive prices as a result of our direct purchases from manufacturers.

Marketing of our distribution services is conducted on a national basis through a dedicated sales force, print and e-commerce catalogues and exhibits at industry and medical meetings and conventions. We direct specialized catalogues to segments of the healthcare industry, such as orthopedic surgeons, physical and occupational therapists, and podiatrists.

Product Development

IN, Inc. specializes in product development principally in the field of functional electrical stimulation. IN, Inc. identifies emerging MyoOrthotics Technologies® developed at research centers and universities throughout the world that use neuromuscular stimulation to improve the functionality of an impaired limb. MyoOrthotics Technologies® represents the merging of orthotic technologies with electrical stimulation. Working with the inventors under licensing and consulting agreements, IN, Inc. commercializes the design, obtains regulatory approvals, develops clinical protocols for the technology, and then introduces the devices to the marketplace through a variety of distribution channels. IN, Inc's. first product, the WalkAide System ("WalkAide"), has received FDA approval, achieved ISO 13485:2004 and ISO 9001:2000 certification, as well as the European CE Mark, which are widely accepted quality management standards for medical devices and related services. Additionally, in September 2007 the WalkAide earned the esteemed da Vinci Award for Adaptive Technologies from the National Multiple Sclerosis Society which honors outstanding engineering achievements in adaptive and assistive technology that provide solutions to accessibility issues for people with disabilities. In November 2008, the Centers for Medicare and Medicaid Services ("CMS") overturned a non-coverage

8

decision and assigned a specific E-code to the WalkAide, which is reimbursable for beneficiaries with foot drop due to incomplete spinal cord injuries. The code was effective January 1, 2009. IN, Inc is pursuing additional coverage for stroke rehabilition which represents the largest potential patient population. CMS has agreed to sponsor additional clinical trials in order to validate the WalkAide's clinical benefits to stroke patients. IN, Inc anticipates that theses trials will be completed in the first half of 2011. In addition to reimbursement from Medicare and Medicaid, IN, Inc has been working with commercial insurance companies and has had limited success in receiving coverage for the WalkAide. The WalkAide is sold in the United States through our patient care centers and SPS. IN, Inc. is also marketing the WalkAide internationally through licensed distributors.

Provider Network Management

Linkia is the first provider network management service company dedicated solely to serving the O&P market. Linkia is dedicated to managing the O&P services of national and regional insurance companies. Linkia partners with healthcare insurance companies by securing a national or regional contract either as a preferred provider or to manage their O&P network of providers. Linkia's network now totals over 1,000 O&P provider locations. As of December 31, 2009, Linkia had 35 contracts with national and regional providers.

Reimbursement

The principal reimbursement sources for our O&P services are:

- •

- private payor/third-party insurer sources, which consist of individuals, private insurance companies, HMOs, PPOs,

hospitals, vocational rehabilitation, workers' compensation programs and similar sources;

- •

- Medicare, a federally funded health insurance program providing health insurance coverage for persons aged 65 or older and

certain disabled persons, which provides reimbursement for O&P products and services based on prices set forth in fee schedules for 10 regional service areas;

- •

- Medicaid, a health insurance program jointly funded by federal and state governments providing health insurance coverage

for certain persons in financial need, regardless of age, which may supplement Medicare benefits for financially needy persons aged 65 or older; and

- •

- the U.S. Department of Veterans Affairs.

We estimate that government reimbursement, comprised of Medicare, Medicaid and the U.S. Department of Veterans Affairs, in the aggregate, accounted for approximately 40.5%, 39.7%, and 40.3% of our net sales in 2009, 2008, and 2007, respectively. These payors have set maximum reimbursement levels for O&P services and products. Medicare prices are adjusted each year based on the Consumer Price Index-Urban ("CPIU") unless congress acts to change or eliminate the adjustment. The Medicare price increases for 2010, 2009, 2008, and 2007 were 0.0%, 5.0%, 2.7%, and 4.3%, respectively. There can be no assurance that future changes will not reduce reimbursements for O&P services and products from these sources.

We enter into contracts with third-party payors that allow us to perform O&P services for a referred patient and be paid under the contract with the third-party payor. These contracts typically have a stated term of one to three years. These contracts generally may be terminated without cause by either party on 60 to 90 days' notice or on 30 days' notice if we have not complied with certain licensing, certification, program standards, Medicare or Medicaid requirements or other regulatory requirements. Reimbursement for services is typically based on a fee schedule negotiated with the third-party payor that reflects various factors, including geographic area and number of persons covered. Renewals can be impacted by competition from small independent O&P providers who from time to time will accept contracts with below market reimbursement in order to gain market share.

9

Through the normal course of business, we receive patient deposits on devices not yet delivered. At December 31, 2009 and 2008, we had received $0.9 million of deposits from our patients.

Suppliers

We purchase prefabricated O&P devices, components and materials that our technicians use to fabricate O&P products from in excess of 400 suppliers across the country. These devices, components and materials are used in the products we offer in our patient-care centers throughout the country. Currently, only four of our third-party suppliers accounted for more than 5% of our total patient care purchases. In addition, four of our purchased products accounted for a significant portion of total purchases from four of our existing suppliers.

Sales and Marketing

The individual practitioners in local patient-care centers historically have conducted our sales and marketing efforts. Due primarily to the fragmented nature of the O&P industry, the success of a particular patient-care center has been largely a function of its local reputation for quality of care, responsiveness and length of service in the local communities. Individual practitioners have relied almost exclusively on referrals from local physicians or physical therapists and typically are not involved in more sophisticated marketing techniques.

We have developed a centralized marketing department the goal of which is to augment the responsibilities of the individual practitioner, enabling the practitioner to focus more of his or her efforts on patient care. Our sales and marketing effort targets the following:

- •

- Marketing and Public Relations. Our objective is to

increase the visibility of the "Hanger" name by building relationships with major referral sources through activities such as co-sponsorship of sporting events and co-branding

of products. We also continue to explore creating alliances with certain vendors to market products and services on a nationwide basis.

- •

- Business Development. We have dedicated personnel in most

of our regions of operation who are responsible for arranging seminars, clinics and forums to educate and consult with patients and to increase the individual communities' awareness of the "Hanger"

name. These business development managers ("BDM") also meet with local referral and contract sources to help our practitioners develop new relationships in their markets.

- •

- Insurance Contracts. Linkia is actively seeking contracts

with national insurance companies to manage their network. We also have regional contract managers who negotiate with hospitals and regional payors.

- •

- Other Initiatives. We are constantly seeking and developing new technology and products to enable us to provide the highest quality patient-oriented care. We continue to use our Insignia laser scanning system, which enables our practitioners to create and modify a computer-based scan of patients' limbs to create more comprehensive patient records and a better prosthetic fit. Due to the improvement Insignia offers to our patient care, it has been an effective marketing tool for our practitioners. During 2006, the Company launched the WalkAide system for treatment of a condition commonly referred to as dropfoot. Management believes the product can broaden our traditional customer base and through distribution agreements will allow the Company to enter international markets.

Acquisitions

In 2009, we acquired seven O&P companies and related businesses, operating a total of 23 patient care centers and one fabrication facility, located in California, Iowa, Nebraska, New York, Pennsylvania, Washington, and Wyoming. The aggregate purchase price for these O&P businesses was $16.6 million.

10

In 2008, we acquired 13 O&P companies and related businesses, operating a total of 19 patient care centers, located in California, Colorado, Florida, Louisiana, Maine, New York, Ohio, and Washington. The aggregate purchase price for these O&P businesses, excluding potential contingent consideration provisions, was $13.5 million.

Competition

The O&P services industry is highly fragmented, consisting mainly of local O&P patient-care centers. The business of providing O&P patient care services is highly competitive in the markets in which we operate. We compete with numerous small independent O&P providers for referrals from physicians, therapists, employers, HMOs, PPOs, hospitals, rehabilitation centers, out-patient clinics and insurance companies on both a local and regional basis. We compete with other patient care service providers, including device manufacturers that have independent sales forces, on the basis of quality and timeliness of patient care, location of patient-care centers and pricing for services.

We also compete with independent O&P providers for the retention and recruitment of qualified practitioners. In certain markets, the demand for practitioners exceeds the supply of qualified personnel.

Government Regulation

We are subject to a variety of federal, state and local governmental regulations. We make every effort to comply with all applicable regulations through compliance programs, policies and procedures, manuals, and personnel training. Despite these efforts, we cannot guarantee that we will be in absolute compliance with all regulations at all times. Failure to comply with applicable governmental regulations may result in significant penalties, including exclusion from the Medicare and Medicaid programs, which would have a material adverse effect on our business.

Medical Device Regulation. We distribute products that are subject to regulation as medical devices by the U.S. Food and Drug Administration ("FDA") under the Federal Food, Drug and Cosmetic Act ("FDCA") and accompanying regulations. With the exception of two products which have been cleared for marketing as prescription medical devices under section 510(k) of the FDCA, we believe that the products we distribute, including O&P medical devices, accessories and components, are exempt from the FDA's regulations for pre-market clearance or approval requirements and from requirements relating to quality system regulation (except for certain recordkeeping and complaint handling requirements). We are required to adhere to regulations regarding adverse event reporting, establishment registration, and product listing; and we are subject to inspection by the FDA for compliance with all applicable requirements. Labeling and promotional materials also are subject to scrutiny by the FDA and, in certain circumstances, by the Federal Trade Commission. Our medical device operations are subject to inspection by the FDA for compliance with applicable FDA requirements, and the FDA has raised compliance concerns in connection with these investigations. We believe we have addressed these concerns and are in compliance with applicable FDA requirements, but we cannot assure that we will be found to be in compliance at all times. Non-compliance could result in a variety of civil and/or criminal enforcement actions, which could have a material adverse effect on our business and results of operations.

Fraud and Abuse. Violations of fraud and abuse laws are punishable by criminal and/or civil sanctions, including, in some instances, imprisonment and exclusion from participation in federal healthcare programs, including Medicare, Medicaid, U.S. Department of Veterans Affairs health programs and the Department of Defense's TRICARE program, formerly known as CHAMPUS. These laws, which include but are not limited to, antikickback laws, false claims laws, physician self-referral laws, and federal criminal healthcare fraud laws, are discussed in further detail below. We believe our billing practices, operations, and compensation and financial arrangements with referral sources and

11

others materially comply with applicable federal and state requirements. However, we cannot assure that such requirements will not be interpreted by a governmental authority in a manner inconsistent with our interpretation and application. The failure to comply, even if inadvertent, with any of these requirements could require us to alter our operations and/or refund payments to the government. Such refunds could be significant and could also lead to the imposition of significant penalties. Even if we successfully defend against any action against us for violation of these laws or regulations, we would likely be forced to incur significant legal expenses and divert our management's attention from the operation of our business. Any of these actions, individually or in the aggregate, could have a material adverse effect on our business and financial results.

Antikickback Laws. Our operations are subject to federal and state antikickback laws. The federal Antikickback Statute (Section 1128B(b) of the Social Security Act) prohibits persons or entities from knowingly and willfully soliciting, offering, receiving, or paying any remuneration in return for, or to induce, the referral of persons eligible for benefits under a federal healthcare program (including Medicare, Medicaid, the U.S. Department of Veterans Affairs health programs and TRICARE), or the ordering, purchasing, leasing, or arranging for, or the recommendation of purchasing, leasing or ordering of, items or services that may be paid for, in whole or in part, by a federal healthcare program. Courts have held that the statute may be violated when even one purpose (as opposed to a primary or sole purpose) of the renumeration is to induce referrals or other business.

Recognizing that the Antikickback Statute is broad and may technically prohibit beneficial arrangements, the Office of Inspector General of the Department of Health and Human Services has developed regulations addressing certain business arrangements that will offer protection from scrutiny under the Antikickback Statute. These "Safe Harbors" describe activities which may be protected from prosecution under the Antikickback Statute, provided that they meet all of the requirements of the applicable Safe Harbor. For example, the Safe Harbors cover activities such as offering discounts to healthcare providers and contracting with physicians or other individuals or entities that have the potential to refer business to us that would ultimately be billed to a federal healthcare program. Failure to qualify for Safe Harbor protection does not mean that an arrangement is illegal. Rather, the arrangement must be analyzed under the Antikickback Statute to determine whether there is an intent to pay or receive remuneration in return for referrals. Conduct and business arrangements that do not fully satisfy one of the Safe Harbors may result in increased scrutiny by government enforcement authorities. In addition, some states have antikickback laws that vary in scope and may apply regardless of whether a federal healthcare program is involved.

Our operations and business arrangements include, for example, discount programs or other financial arrangements with individuals and entities, such as lease arrangements with hospitals and certain participation agreements. Therefore, our operations and business arrangements are required to comply with the antikickback laws. Although our business arrangements and operations may not always satisfy all the criteria of a Safe Harbor, we believe that our operations are in material compliance with federal and state antikickback statutes.

HIPAA Violations. The Health Insurance Portability and Accountability Act ("HIPAA") provides criminal penalties for, among other offenses: health care fraud; theft or embezzlement with respect to a health care benefit program; false statements in connection with the delivery of or payment for health care benefits, items or services; and obstruction of criminal investigation of health care offenses. Unlike other federal laws, these offenses are not limited to Federal health care programs.

In addition, HIPAA authorizes the imposition of civil monetary penalties where a person offers or pays remuneration to any individual eligible for benefits under a federal healthcare program that such person knows or should know is likely to influence the individual to order or receive covered items or services from a particular provider, practitioner or supplier. Excluded from the definition of "remuneration" are incentives given to individuals to promote the delivery of preventive care (excluding

12

cash or cash equivalents), incentives of nominal value and certain differentials in or waivers of coinsurance and deductible amounts.

These laws may apply to certain of our operations. As noted above, we have established various types of discount programs and other financial arrangements with individuals and entities. We also bill third-party payors and other entities for items and services provided at our patient-care centers. While we endeavor to ensure that our discount programs and other financial arrangements, and billing practices comply with applicable laws, such programs, arrangements and billing practices could be subject to scrutiny and challenge under HIPAA.

False Claims Laws. We are also subject to federal and state laws prohibiting individuals or entities from knowingly presenting, or causing to be presented, claims for payment to third-party payors (including Medicare and Medicaid) that are false or fraudulent, are for items or services not provided as claimed, or otherwise contain misleading information. Each of our patient-care centers is responsible for the preparation and submission of reimbursement claims to third-party payors for items and services furnished to patients. In addition, our personnel may, in some instances, provide advice on billing and reimbursement to purchasers of our products. While we endeavor to assure that our billing practices comply with applicable laws, if claims submitted to payors are deemed to be false, fraudulent, or for items or services not provided as claimed, we may face liability for presenting or causing to be presented such claims.

Physician Self-Referral Laws. We are also subject to federal and state physician self-referral laws. With certain exceptions, the federal Medicare physician self-referral law (the "Stark Law") (Section 1877 of the Social Security Act) prohibits a physician from referring Medicare beneficiaries to an entity for "designated health services"—including prosthetic and orthotic devices and supplies—if the physician or the physician's immediate family member has a financial relationship with the entity. A financial relationship includes both ownership or investment interests and compensation arrangements. An entity that furnishes designated health services pursuant to a prohibited referral may not present or cause to be presented a claim or bill for such designated health services. Penalties for violating the Stark Law include denial of payment for the service, an obligation to refund any payments received, civil monetary penalties, and the possibility of being excluded from the Medicare or Medicaid programs.

With respect to ownership/investment interests, there is an exception under the Stark Law for referrals made to a publicly traded entity in which the physician or the physician's immediate family member has an investment interest if the entity's shares are generally available to the public at the time of the designated health service referral, and are traded on certain exchanges, including the New York Stock Exchange, and the entity had shareholders' equity exceeding $75.0 million for its most recent fiscal year or as an average during the three previous fiscal years. We meet these tests and, therefore, believe that referrals from physicians who have ownership interests in our stock, or whose immediate family members have ownership interests in our stock, should not result in liability under the Stark Law.

With respect to compensation arrangements, there are exceptions under the Stark Law that permit physicians to maintain certain business arrangements, such as personal service contracts and equipment or space leases, with healthcare entities to which they refer patients for designated health services. Unlike the Antikickback Statute, all of the elements of a Stark Law exception must be met in order for the exception to apply. We believe that our compensation arrangements with physicians comply with the Stark Law, either because the physician's relationship fits fully within a Stark Law exception or because the physician does not generate prohibited referrals. If, however, we receive a prohibited referral, our submission of a bill for services rendered pursuant to such a referral could subject us to sanctions under the Stark Law and applicable state self-referral laws. State self-referral laws may extend the prohibitions of the Stark Law to Medicaid beneficiaries.

13

Certification and Licensure. Our practitioners and/or certain operating units may be subject to certification or licensure requirements under the laws of some states. Most states do not require separate licensure for practitioners. However, several states currently require practitioners to be certified by an organization such as the American Board for Certification. The American Board for Certification conducts a certification program for practitioners and an accreditation program for patient-care centers. The minimum requirements for a certified practitioner are a college degree, completion of an accredited academic program, one to four years of residency at a patient-care center under the supervision of a certified practitioner and successful completion of certain examinations. Minimum requirements for an accredited patient-care center include the presence of a certified practitioner and specific plant and equipment requirements.

Some states may require licensure or registration of facilities that dispense or distribute prescription medical devices within or from outside of the state. In addition, some states may require a license or registration to provide services such as those offered by Linkia. We are in the process of meeting these requirements.

While we endeavor to comply with all state licensure requirements, we cannot assure that we will be in compliance at all times with these requirements. Failure to comply with state licensure requirements could result in suspension or termination of licensure, civil penalties, termination of our Medicare and Medicaid agreements, and repayment of amounts received from Medicare and Medicaid for services and supplies furnished by an unlicensed individual or entity.

Confidentiality and Privacy Laws. The Administrative Simplification Provisions of HIPAA, and their implementing regulations, set forth privacy standards and implementation specifications concerning the use and disclosure of individually identifiable health information (referred to as "protected health information") by health plans, healthcare clearinghouses and healthcare providers that transmit health information electronically in connection with certain standard transactions ("Covered Entities"). HIPAA further requires Covered Entities to protect the confidentiality of health information by meeting certain security standards and implementation specifications. In addition, under HIPAA, Covered Entities that electronically transmit certain administrative and financial transactions must utilize standardized formats and data elements ("the transactions/code sets standards"). HIPAA imposes civil monetary penalties for non-compliance, and, with respect to knowing violations of the privacy standards, or violations of such standards committed under false pretenses or with the intent to sell, transfer or use individually identifiable health information for commercial advantage, criminal penalties. We believe that we are subject to the Administrative Simplification Provisions of HIPAA and are taking steps to meet applicable standards and implementation specifications. The new requirements have had a significant effect on the manner in which we handle health data and communicate with payors. Our billing system, OPS, was designed to meet these requirements.

In addition, state confidentiality and privacy laws may impose civil and/or criminal penalties for certain unauthorized or other uses or disclosures of individually identifiable health information. We are also subject to these laws. While we endeavor to assure that our operations comply with applicable laws governing the confidentiality and privacy of health information, we could face liability in the event of a use or disclosure of health information in violation of one or more of these laws.

Personnel and Training

None of our employees are subject to a collective-bargaining agreement. We believe that we have satisfactory relationships with our employees and strive to maintain these relationships by offering competitive benefit packages, training programs and opportunities for advancement. During the year

14

ended December 31, 2009, we had an average of 3,636 employees. The following table summarizes our average number of employees for the year:

| |

Practitioners | Residents | Technicians | Administrative | Distribution | Corporate and Shared Services |

|||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Hanger Prosthetics & Orthotics, Inc. |

1,106 | 90 | 563 | 1,359 | — | — | |||||||||||||

Southern Prosthetic Supply, Inc. |

— | — | — | — | 201 | — | |||||||||||||

Hanger Orthopedic Group, Inc. |

— | — | — | — | — | 317 | |||||||||||||

We have established an affiliation with the University of Hartford pursuant to which we own and operate a school at the Newington, Connecticut campus that offers a certificate in orthotics and/or prosthetics after the completion of a nine-month course. We believe there are only nine schools of this kind in the United States. The program director is a Hanger employee, and our practitioners teach most of the courses. After completion of the nine-month course, graduates receive a certificate and go on to complete a residency in their area of specialty. After their residency is complete, graduates can choose to complete a course of study in another area of specialty. Most graduates will then sit for a certification exam to either become a certified prosthetist or certified orthotist. We offer exam preparation courses for graduates who agree to become our practitioners to help them prepare for those exams.

We also provide a series of ongoing training programs to improve the professional knowledge of our practitioners. For example, we have an annual Education Fair which is attended by over 750 of our practitioners and consists of lectures and seminars covering many clinical topics including the latest technology and process improvements, basic accounting and business courses and other courses which allow the practitioners to fulfill their ongoing continuing education requirements.

Insurance

We currently maintain insurance coverage for malpractice liability, product liability, workers' compensation, executive protection and property damage. Our general liability insurance coverage is $1.0 million per incident, with a $25.0 million umbrella insurance policy. The coverage for malpractice, product and workers' compensation is self-insured with both individual specific claim and aggregate stop-loss policies to protect us from either significant individual claims or dramatic changes in our loss experience. Based on our experience and prevailing industry practices, we believe our coverage is adequate as to risks and amount. We have not incurred a material amount of expenses in the past as a result of uninsured O&P claims.

Special Note On Forward-Looking Statements

Some of the statements contained in this report discuss our plans and strategies for our business or make other forward-looking statements, as this term is defined in the Private Securities Litigation Reform Act. The words "anticipates," "believes," "estimates," "expects," "plans," "intends" and similar expressions are intended to identify these forward-looking statements, but are not the exclusive means of identifying them. These forward-looking statements reflect the current views of our management; however, various risks, uncertainties and contingencies could cause our actual results, performance or achievements to differ materially from those expressed in, or implied by, these statements, including the following:

- •

- the demand for our orthotic and prosthetic services and products;

15

- •

- our ability to integrate effectively the operations of businesses that we have acquired and plan to acquire in the future;

- •

- our ability to enter into national contracts;

- •

- our ability to maintain the benefits of our performance improvement plans;

- •

- our ability to attract and retain qualified orthotic and prosthetic practitioners;

- •

- changes in federal Medicare reimbursement levels and other governmental policies affecting orthotic and prosthetic

operations;

- •

- our indebtedness, the impact of changes in prevailing interest rates and the availability of favorable terms of equity and

debt financing to fund the anticipated growth of our business;

- •

- changes in, or failure to comply with, federal, state and/or local governmental regulations; and

- •

- liabilities relating to orthotic and prosthetic services and products and other claims asserted against us.

For a discussion of important risk factors affecting our business, including factors that could cause actual results to differ materially from results referred to in the forward-looking statements, see "Item 1A-Risk Factors" and "Management's Discussion and Analysis of Financial Condition and Results of Operations" below. We do not have any obligation to publicly update any forward-looking statements, whether as a result of new information, future events or otherwise.

Changes in government reimbursement levels could adversely affect our net sales, cash flows and profitability.

We derived 40.5%, 39.7%, and 40.3% of our net sales for the years ended December 31, 2009, 2008, and 2007, respectively, from reimbursements for O&P services and products from programs administered by Medicare, Medicaid and the U.S. Department of Veterans Affairs. Each of these programs sets maximum reimbursement levels for O&P services and products. If these agencies reduce reimbursement levels for O&P services and products in the future, our net sales could substantially decline. In addition, the percentage of our net sales derived from these sources may increase as the portion of the U.S. population over age 65 continues to grow, making us more vulnerable to maximum reimbursement level reductions by these organizations. Reduced government reimbursement levels could result in reduced private payor reimbursement levels because fee schedules of certain third-party payors are indexed to Medicare. Furthermore, the healthcare industry is experiencing a trend towards cost containment as government and other third-party payors seek to impose lower reimbursement rates and negotiate reduced contract rates with service providers. This trend could adversely affect our net sales. Medicare provides for reimbursement for O&P products and services based on prices set forth in fee schedules for ten regional service areas. Medicare prices are adjusted each year based on the Consumer Price Index- Urban ("CPIU") unless Congress acts to change or eliminate the adjustment. The Medicare price increases for 2010, 2009, 2008, and 2007 were 0.0%, 5.0%, 2.7%, and 4.3%, respectively. If the U.S. Congress were to legislate additional modifications to the Medicare fee schedules, our net sales from Medicare and other payors could be adversely and materially affected. We cannot predict whether any such modifications to the fee schedules will be enacted or what the final form of any modifications might be.

Changes in payor reimbursements could negatively affect our net sales volume.

Recent years have seen a consolidation of healthcare companies coupled with certain payors terminating contracts, imposing caps or reducing reimbursement for O&P products. Additionally, employers are increasingly pushing healthcare costs down to their employees. These trends could result in decreased O&P revenue.

16

We face periodic reviews, audits and investigations under our contracts with federal and state government agencies, and these audits could have adverse findings that may negatively impact our business.

We contract with various federal and state governmental agencies to provide O&P services. Pursuant to these contracts, we are subject to various governmental reviews, audits and investigations to verify our compliance with the contracts and applicable laws and regulations. Any adverse review, audit or investigation could result in:

- •

- refunding of amounts we have been paid pursuant to our government contracts;

- •

- imposition of fines, penalties and other sanctions on us;

- •

- loss of our right to participate in various federal programs;

- •

- damage to our reputation in various markets; or

- •

- material and/or adverse effects on our business, financial condition and results of operations.

We are subject to numerous federal, state and local governmental regulations, noncompliance with which could result in significant penalties that could have a material adverse effect on our business.

A failure by us to comply with the numerous federal, state and/or local healthcare and other governmental regulations to which we are subject, including the regulations discussed under "Government Regulation" in Item 1 above, could result in significant penalties and adverse consequences, including exclusion from the Medicare and Medicaid programs, which could have a material adverse effect on our business.

If the non-competition agreements we have with our key executive officers and key practitioners were found by a court to be unenforceable, we could experience increased competition resulting in a decrease in our net sales.

We generally enter into employment agreements with our executive officers and a significant number of our practitioners which contain non-compete and other provisions. The laws of each state differ concerning the enforceability of non-competition agreements. State courts will examine all of the facts and circumstances at the time a party seeks to enforce a non-compete covenant. We cannot predict with certainty whether or not a court will enforce a non-compete covenant in any given situation based on the facts and circumstances at that time. If one or more of our key executive officers and/or a significant number of our practitioners were to leave us and the courts refused to enforce the non-compete covenant, we might be subject to increased competition, which could materially and adversely affect our business, financial condition and results of operations.

Funds associated with certain of our auction rate securities are not currently accessible and our auction rate securities have experienced other than temporary decline in value, which could adversely affect our income.

Our investments include an auction rate security ("ARS"), classified as other long term assets, and reported at an aggregate fair value of $1.4 million and an aggregate cost of $1.7 million, as of December 31, 2009. ARS are securities that are structured with short-term interest rate reset dates which generally occur every 28 days, but with contractual maturities that can be well in excess of ten years. At the end of each reset period, investors can attempt to sell via auction or continue to hold the securities at par. The auctions for all of the ARS held by us were unsuccessful as of December 31, 2009. The funds associated with these will not be accessible until a successful auction occurs, a buyer is found outside of the auction process or the underlying securities have matured.

17

Our Website

Our website is http://www.hanger.com. We make available free of charge, on or through our website, our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, Section 16 filings (i.e. Forms 3, 4 and 5), proxy statements, and other documents as required by applicable law and regulations as soon as reasonably practicable after electronically filing such reports with the Securities and Exchange Commission at http://www.sec.gov. The public may read and copy any materials that we file with the SEC at the SEC's Public Reference Room at 100 F Street N.E., Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330 (1800-732-0330). The SEC maintains an Internet site (http://www.sec.gov) that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC. Our website also contains the charters of the Audit Committee, Corporate Governance and Nominating Committee, Compensation Committee and Quality and Technology Committee of our Board of Directors; our Code of Business Conduct and Ethics for Directors and Employees, which includes our principal executive, financial and accounting officers; as well as our Corporate Governance Guidelines. Information contained on our website is not part of this report.

ITEM 1B. UNRESOLVED STAFF COMMENTS.

None.

As of December 31, 2009, we operated 677 patient-care centers and facilities in 45 states and the District of Columbia. We own 16 buildings that house a patient-care center. The remaining centers are occupied under leases expiring between the years of 2010 and 2019. We believe our leased or owned centers are adequate for carrying on our current O&P operations at our existing locations, as well as our anticipated future needs at those locations. We believe we will be able to renew such leases as they expire or find comparable or additional space on commercially suitable terms.

The following table sets forth the number of our patient-care centers located in each state as of December 31, 2009:

| State | Patient- Care Centers |

State | Patient- Care Centers |

State | Patient- Care Centers |

|||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Alabama |

12 | Louisiana | 15 | North Carolina | 13 | |||||||||

Arizona |

37 | Maine | 5 | North Dakota | 2 | |||||||||

Arkansas |

5 | Maryland | 10 | Ohio | 35 | |||||||||

California |

73 | Massachusetts | 9 | Oklahoma | 11 | |||||||||

Colorado |

25 | Michigan | 6 | Oregon | 11 | |||||||||

Connecticut |

10 | Minnesota | 6 | Pennsylvania | 30 | |||||||||

Delaware |

1 | Mississippi | 10 | South Carolina | 13 | |||||||||

District of Columbia |

1 | Missouri | 21 | South Dakota | 1 | |||||||||

Florida |

50 | Montana | 5 | Tennessee | 15 | |||||||||

Georgia |

32 | Nebraska | 8 | Texas | 30 | |||||||||

Illinois |

23 | Nevada | 6 | Utah | 3 | |||||||||

Indiana |

11 | New Hampshire | 2 | Virginia | 9 | |||||||||

Iowa |

8 | New Jersey | 8 | Washington | 18 | |||||||||

Kansas |

14 | New Mexico | 7 | West Virginia | 7 | |||||||||

Kentucky |

10 | New York | 33 | Wisconsin | 13 | |||||||||

|

Wyoming | 3 | ||||||||||||

18

We also lease distribution facilities in Texas, California, Georgia, Florida, and Pennsylvania. We lease our corporate headquarters in Bethesda, Maryland. In January 2010, we signed a lease agreement and will relocate our corporate headquarters to Austin, TX. Substantially all of our owned properties are pledged to collateralize bank indebtedness. See Note G to our Consolidated Financial Statements.

The Company is subject to legal proceedings and claims which arise in the ordinary course of its business, including additional payments under business purchase agreements. In the opinion of management, the amount of ultimate liability, if any, with respect to these actions will not have a materially adverse effect on the financial position, liquidity or results of operations of the Company.

The Company is in a highly regulated industry and receives regulatory agency inquiries from time to time in the ordinary course of its business, including inquiries relating to the Company's billing activities. To date these inquiries have not resulted in material liabilities, but no assurance can be given that future regulatory agencies' inquiries will be consistent with the results to date or that any discrepancies identified during a regulatory review will not have a material adverse effect on the Company's consolidated financial statements.

The United States Attorney's Office for the Eastern District of New York (the "US Attorney's Office") initiated an investigation in June 2004 regarding allegations of billing discrepancies at the Company's West Hempstead, New York patient-care center. Based upon communications with the US Attorney's Office, it is the Company's understanding that the US Attorney's Office will not file any criminal charges or pursue any False Claims Act remedies against the Company related to the alleged billing discrepancies.

ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS.

[Reserved]

EXECUTIVE OFFICERS OF THE REGISTRANT.

The following table sets forth information regarding current executive officers of the Company and certain of its subsidiaries:

Name

|

Age | Office with the Company | |||

|---|---|---|---|---|---|

Ivan R. Sabel, CPO |

64 | Chairman of the Board | |||

Thomas F. Kirk |

64 | President and Chief Executive Officer | |||

Richmond L. Taylor |

61 | Executive Vice President, President and Chief Operating Officer of Hanger Prosthetics & Orthotics, Inc. | |||

Ron N. May |

63 | Executive Vice President, President and Chief Operating Officer of Southern Prosthetic Supply, Inc. | |||

George E. McHenry |

57 | Executive Vice President, Secretary, and Chief Financial Officer | |||

Vinit K. Asar |

43 | Executive Vice President and Chief Growth Officer | |||

Thomas E. Hartman |

47 | Vice President and General Counsel | |||

Thomas C. Hofmeister |

43 | Vice President and Chief Accounting Officer | |||

Marion L. Mullauer |

57 | Vice President and Chief Information Officer | |||

Sam Reimer |

40 | Vice President and Treasurer | |||

Brian A. Wheeler |

49 | Vice President, Human Resources | |||

19

Ivan R. Sabel, CPO has been our Chairman of the Board of Directors since August 1995 and was our Chief Executive Officer from August 1995 until March 2008. Mr. Sabel was our President from November 1987 to January 2002. Mr. Sabel also served as the Chief Operating Officer from November 1987 until August 1995. Prior to that time, Mr. Sabel had been Vice President, Corporate Development from September 1986 to November 1987. Mr. Sabel was the founder, owner and President of Capital Orthopedics, Inc. from 1968 until that company was acquired by us in 1986. Mr. Sabel is a Certified Prosthetist and Orthotist ("CPO"), a former clinical instructor in orthopedics at the Georgetown University Medical School in Washington, D.C., a member of the Government Relations Committee of the American Orthotic and Prosthetic Association ("AOPA"), a former Chairman of the National Commission for Health Certifying Agencies, a former member of the Strategic Planning Committee, a current member of the U.S. Department of Veterans Affairs Committee of AOPA and a former President of the American Board for Certification in Orthotics and Prosthetics. Mr. Sabel also serves as a member of the Medical Advisory Board of DJ Orthopedics, Inc., a manufacturer of knee braces. Mr. Sabel has been a director since 1986. Mr. Sabel holds a B.S. in Prosthetics and Orthotics from New York University.

Thomas F. Kirk has been our President and Chief Executive Officer since March 2008. Mr. Kirk also served as our Chief Operating Officer from January 2002 until March 2008. From September 1998 to January 2002, Mr. Kirk was a principal with AlixPartners, LLC (formerly Jay Alix & Associates, Inc.), a management consulting company retained by Hanger to facilitate its reengineering process. From May 1997 to August 1998, Mr. Kirk served as Vice President, Planning, Development and Quality for FPL Group, a full service energy provider located in Florida. From April 1996 to April 1997, he served as Vice President and Chief Financial Officer for Quaker Chemical Corporation in Pennsylvania. From December 1987 to March 1996, he served as Senior Vice President and Chief Financial Officer for Rhone-Poulenc, S.A. in Princeton, New Jersey and Paris, France. From March 1977 to November 1987, he was employed by St. Joe Minerals Corp., a division of Fluor Corporation. Prior to this he held positions in sales, commercial development, and engineering with Koppers Co., Inc. Mr. Kirk holds a Ph.D. degree in strategic planning/marketing, and an M.B.A. degree in finance, from the University of Pittsburgh. He also holds a Bachelor of Science degree in mechanical engineering from Carnegie Mellon University. He is a registered professional engineer and a member of the Financial Executives Institute.

Richmond L. Taylor is our Executive Vice President, and the President and Chief Operating Officer of Hanger Prosthetics & Orthotics, Inc. and HPO, Inc., our two wholly-owned subsidiaries which operate all of our patient-care centers. Previously, Mr. Taylor served as the Chief Operating Officer of NovaCare O&P from June 1996 until July 1999, and held the positions of Region Vice-President and Region President of NovaCare O&P for the West Region from 1989 to June 1996. Prior to joining NovaCare O&P, Mr. Taylor spent 20 years in the healthcare industry in a variety of management positions including Regional Manager at American Hospital Supply Corporation, Vice President of Operations at Medtech, Vice President of Sales at Foster Medical Corporation and Vice President of Sales at Integrated Medical Systems.

Ron N. May has been the President and Chief Operating Officer of Southern Prosthetic Supply, Inc., our wholly-owned subsidiary that distributes orthotic and prosthetic products, since December 1998. From January 1984 to December 1998, Mr. May was Executive Vice President of the distribution division of J.E. Hanger, Inc. of Georgia until that company was acquired by us in November 1996. Mr. May also currently serves as a Board Member of the O&P Athletic Fund.

George E. McHenry has been our Executive Vice President and Chief Financial Officer since October 2001. From 1987 until he joined us in October 2001, Mr. McHenry served as Executive Vice President, Chief Financial Officer and Secretary of U.S. Vision, Inc., an optical company with 600 locations in 47 states. Prior to joining U.S. Vision, Inc., he was employed principally as a Senior Manager by the firms of Touche Ross & Co. (now Deloitte & Touche) and Main Hurdman (now

20

KPMG LLP) from 1974 to 1987. Mr. McHenry is a Certified Public Accountant and received a Bachelor of Science degree in accounting from St. Joseph's University.

Vinit K. Asar joined us as our Executive Vice President and Chief Growth Officer in December 2008. Mr. Asar comes to Hanger from the Medical Device & Diagnostic sector at Johnson and Johnson, having worked at the Ethicon, Ethicon-Endo-Surgery, Cordis and Biosense Webster franchises. During his 18 year career at Johnson and Johnson, Mr. Asar held various roles of increasing responsibility in Finance, Product Development, Manufacturing, Marketing and Sales in the US and in Europe. Prior to joining Hanger, Mr. Asar was the Worldwide Vice-President at Biosense Webster, the Electrophysiology division of Johnson and Johnson, responsible for the Worldwide Sales, Marketing and Services organizations. Mr. Asar has a B.S.B.A from Aquinas College and an M.B.A. from Lehigh University.

Thomas E. Hartman has been our Vice President & General Counsel since June 2009. Mr. Hartman joined Hanger from Foley & Lardner, LLP where he was a partner in Foley's Business Law Department. Mr. Hartman's practice at Foley was focused on securities transactions, securities law compliance, mergers and acquisitions, and corporate governance. Prior to joining Foley in 1995, Mr. Hartman was a business law associate at Jones Day. Mr. Hartman received his J.D. from the University of Wisconsin in Madison, and a Bachelor of Science in Engineering (Industrial & Operations Engineering) from the University of Michigan in Ann Arbor.

Thomas C. Hofmeister joined us in October of 2004 as our Vice President of Finance and Chief Accounting Officer and was previously employed as the Chief Financial Officer of Woodhaven Health Services from October 2002 through October 2004. Prior to that, Mr. Hofmeister served as Senior Vice President and Chief Accounting Officer of Magellan Health Services, Inc. from 1999 to 2002; Controller of London Fog Industries, Inc. from 1998 to 1999 and Vice President and Controller of Pharmerica, Inc. from 1995 to 1998. Mr. Hofmeister was also employed as a senior manager at KPMG Peat Marwick from 1988 to 1995. Mr. Hofmeister holds a B.S. degree in accounting from Mount Saint Mary's College.

Marion L. Mullauer has been our Vice President and Chief Information Officer since August 2005. She is an experienced CIO, having previously held that position at the American Chemical Society and Lippincott Williams & Wilkins, Inc., a leading publisher of health care information. She has over 25 years of experience in information technology in senior management positions, much of it with healthcare companies. Ms. Mullauer holds a B.S. degree in Business Administration from Towson University and a Masters in Business Administration from Loyola College.

Sam Reimer has been our Vice President & Treasurer since October 2009 and a Vice President with Hanger since May 2008. Prior to Hanger, Mr. Reimer was with Sprint Nextel from 2003 to 2007, most recently as a Corporate Vice President in Finance and Corporate Development. At Sprint Nextel, he also held additional positions in Operations Finance and Merger Integration. From 2000 to 2003, Mr. Reimer was Director of Corporate Finance with webMethods, Inc. Prior to webMethods, Mr. Reimer held various accounting and finance positions with companies in the software and telecommunications industries. Mr. Reimer received his CPA certificate from the state of Virginia and his Bachelor of Science in Accounting degree from Virginia Tech.

Brian A. Wheeler has been our Vice President, Human Resources since November 2002. Prior to joining Hanger, he was the Vice President of Human Resources for Rhodia Inc., a wholly-owned U.S. subsidiary of the French Specialty Chemicals Company. Mr. Wheeler holds a B.A. degree in Political Science from the University of Florida.

21

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES.

Market Information

Our common stock has been listed and traded on the New York Stock Exchange since December 15, 1998, under the symbol "HGR." The following table sets forth the high and low closing sale prices for the common stock for the periods indicated as reported on the New York Stock Exchange:

Year Ended December 31, 2009

|

High | Low | |||||

|---|---|---|---|---|---|---|---|

First Quarter |

$ | 16.08 | $ | 11.32 | |||

Second Quarter |

15.37 | 11.14 | |||||

Third Quarter |

14.95 | 12.28 | |||||

Fourth Quarter |

14.63 | 13.27 | |||||

Year Ended December 31, 2008

|

High | Low | |||||

|---|---|---|---|---|---|---|---|

First Quarter |

$ | 11.92 | $ | 9.27 | |||

Second Quarter |

16.49 | 10.00 | |||||

Third Quarter |

19.76 | 15.06 | |||||

Fourth Quarter |

17.64 | 12.26 | |||||

Holders

At February 22, 2010, there were approximately 311 holders of record of 31,901,708 shares of our outstanding common stock.

Dividend Policy

We have never paid cash dividends on our common stock and intend to continue this policy for the foreseeable future. We plan to retain earnings for use in our business. The terms of our agreements with our financing sources and certain other agreements limit the payment of dividends on our common stock and such agreements will continue to limit the payment of dividends in the future.

Any future determination to pay cash dividends will be at the discretion of our Board of Directors and will be dependent on our results of operations, financial condition, contractual and legal restrictions and any other factors deemed to be relevant.

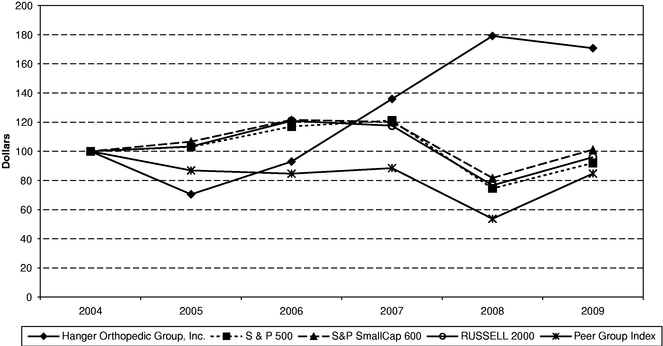

Equity Compensation Plans