Attached files

| file | filename |

|---|---|

| EX-31.1 - EXHIBIT 31.1 - CONVERSANT, INC. | a2196829zex-31_1.htm |

| EX-32.1 - EXHIBIT 32.1 - CONVERSANT, INC. | a2196829zex-32_1.htm |

| EX-31.2 - EXHIBIT 31.2 - CONVERSANT, INC. | a2196829zex-31_2.htm |

| EX-23.1 - EXHIBIT 23.1 - CONVERSANT, INC. | a2196829zex-23_1.htm |

| EX-21.1 - EXHIBIT 21.1 - CONVERSANT, INC. | a2196829zex-21_1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| (Mark One) | ||

ý |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the Year Ended December 31, 2009 |

||

or |

||

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the transition period from to |

||

Commission file number 000-30135

VALUECLICK, INC.

(Exact name of registrant as specified in its charter)

| Delaware (State or Other Jurisdiction of Incorporation or Organization) |

77-0495335 (I.R.S. Employer Identification No.) |

|

30699 RUSSELL RANCH ROAD, SUITE 250 WESTLAKE VILLAGE, CALIFORNIA 91362 (Address of principal executive offices, including zip code) |

||

Registrant's Telephone Number, Including Area Code: (818) 575-4500 |

||

Securities registered pursuant to Section 12(b) of the Act: |

||

| |

Title of each class | Name of each exchange on which registered | |

|||

|---|---|---|---|---|---|---|

| Common Stock, $0.001 par value | NASDAQ Global Select Market |

Securities registered pursuant to Section 12(g) of the Act:

Series A Junior Participating Preferred Stock Purchase Rights

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files): Yes o No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ý | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

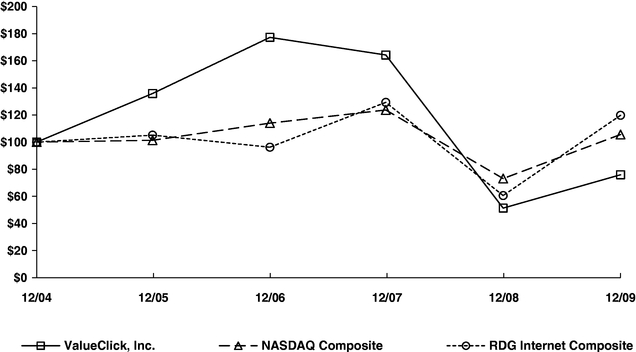

As of June 30, 2009, which was the last business day of the registrant's most recently completed second fiscal quarter, the approximate aggregate market value of voting stock held by non-affiliates of the registrant was $901,062,796 (based upon the closing price for shares of the registrant's Common Stock as reported by the NASDAQ Global Select Market as of that date). As of February 19, 2010, there were 83,529,396 shares of the registrant's Common Stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive Proxy Statement for the 2010 Annual Meeting of the Stockholders (the "Proxy Statement"), to be filed within 120 days of the end of the fiscal year ended December 31, 2009, are incorporated by reference in Part III hereof.

VALUECLICK, INC.

ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

This annual report on Form 10-K ("Report"), including information incorporated herein by reference, contains "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These statements relate to expectations concerning matters that are not historical facts. Words such as "projects," "believes," "anticipates," "will," "estimate," "plans," "expects," "intends," and similar words and expressions are intended to identify forward-looking statements. Although we believe that such forward-looking statements are reasonable, we cannot assure you that such expectations will prove to be correct. Important language regarding factors which could cause actual results to differ materially from such expectations are disclosed in this Report, including without limitation under the caption "Risk Factors" beginning on page 8 of this Report and in the other documents we file, from time to time, with the Securities and Exchange Commission, including our annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K. All forward-looking statements attributable to ValueClick, Inc. are expressly qualified in their entirety by such language. We undertake no obligation to release publicly any revisions to any forward-looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

OVERVIEW

ValueClick is one of the world's largest and most comprehensive online marketing services companies. We sell targeted and measurable online advertising campaigns and programs for advertisers and advertising agency customers, generating qualified customer leads, online sales and increased brand recognition on their behalf with large numbers of online consumers.

Our customers are primarily direct marketers, brand advertisers and the advertising agencies that service these groups. The proposition we offer our customers includes: one of the industry's broadest online marketing services portfolios—including performance-based campaigns and programs where marketers only pay for advertising when it generates a customer lead or product sale; our ability to target campaigns to reach the online consumers our customers are most interested in; and the scale at which we can deliver results for online advertising campaigns. Additionally, our networks of online publishers provide advertisers with a cost-effective and complementary source of online consumers relative to online portals and other large website publishers. Through this approach we have become an industry leader in generating qualified customer leads and online sales for advertisers.

We generate the audiences for our advertisers' campaigns primarily through networks of third-party websites, other online publisher partners and search engines. We aggregate our publisher partners' online advertising inventory into networks, optimize these networks for specific marketing goals, and deliver the campaigns across the appropriate networks' advertising inventory. We are one of the industry's largest online network providers, with: industry expertise and proprietary technology platforms for online advertising inventory aggregation; campaign targeting and optimization, delivery, measurement, and reporting; and, payment settlement and delivery services.

Our publisher partners enjoy efficient and effective monetization of their online advertising inventory through representation by our direct sales teams in major U.S. and European media markets, participation in large-scale advertiser and advertising agency campaigns they may not have access to on their own, enhanced monetization through our proprietary campaign optimization and targeting technology, and settlement services to facilitate payments to publishers for the online inventory utilized by the advertisers. As we do not primarily compete directly with our publisher partners for online consumers, we act as a trusted partner in helping online publishers monetize their online audience and advertising inventory.

We believe that the effectiveness of our online marketing services is dependent on the quality of our networks and our publisher partner relationships. As such, we have established stringent quality standards that include publisher rejection from our networks due to inappropriate content, illegal activity and fraudulent clicking activity, among other criteria. We enforce these quality standards using a combination of manual and automated auditing processes that continually monitor and review both website content and adherence to advertiser campaign specifications.

We derive our revenue from four business segments. These business segments are presented on a worldwide basis and include Media, Affiliate Marketing, Owned & Operated Websites, and Technology, which are described in more detail below. For information regarding the operating performance and total assets of these segments, see Item 7 "Management's Discussion and Analysis of Financial Condition and Results of Operations," and Note 17 to the December 31, 2009 consolidated financial statements included herein.

MEDIA SEGMENT

ValueClick's Media segment provides a comprehensive suite of online marketing services and tailored programs that help marketers create and increase awareness for their products and brands,

1

attract visitors and generate leads and sales through the Internet. We have aggregated thousands of online publishers to provide marketers with access to one of the largest and most reputable display advertising networks in the industry. We partner with third-party website publishers and apply our proprietary technology platform and industry expertise to deliver our customers' display ad campaigns to the appropriate pages of our publisher partners' websites.

With a single buy, marketers can reach targeted online users on a large scale, using a variety of online display ad units across our entire network of publishers, any of 21 standard channels of online content within the network, customized content channels, or a select number of websites where we are authorized to sell inventory on a single-site basis. Audiences can be further targeted based on the demographic and psychographic composition of sites within the network and technical information such as geographic location, browser type, connection speed, ISP or top-level domain (.com, .edu, etc.). In addition, our behavioral targeting capabilities allow marketers to retarget users who have recently visited their sites or to display highly relevant ads based on anonymous profiles we develop based on consumers' recent online behavior such as web browsing and interaction with ads across our network.

With 10,000 active online publisher sites in the U.S. and 16,000 worldwide, our display advertising network reached 171 million unique visitors, or 83% of the U.S. internet audience in December 2009 according to published industry data.

We deliver a variety of display ad units to the Web pages of our online display advertising network publisher partners and track them to evaluate success against the goals of the advertising programs. With traditional banner ads, interstitials, text links, and other online ad units, our technology maximizes the impact of marketing campaigns by identifying the most effective placement for each type of campaign. We also execute a wide variety of rich media applications, including in-stream and in-banner video ads, providing even greater visual and auditory impact for a marketer's online display advertising campaigns.

We began as a performance-based marketing network and we continue to offer multiple pricing models designed around maximizing our customers' return on investment. Our display advertising placements are offered on several pricing models including: cost-per-thousand-impression ("CPM"), whereby our customers pay based on the number of times the target audience is exposed to the advertisement; cost-per-click ("CPC"), whereby payment is triggered only when an interested individual clicks on our customer's advertisement; and cost-per-action ("CPA"); whereby payment is triggered only when a specific, pre-defined action is performed by an online consumer.

The benefits that our customers enjoy in display and other Web advertising include, but are not limited to: flexible pricing models; the ability to target and reach significant numbers of online consumers in a way that complements media buys on portals and other large websites; and the ability to improve online advertising performance while the campaigns are still running by optimizing at site, placement and creative levels, based on both response to ads and the resulting conversions.

Publishers in our display advertising network enjoy efficient and effective monetization of their online advertising inventory, including: representation by our direct sales teams in major U.S. and European media markets; participation in large-scale advertiser and advertising agency campaigns they may not be able to access on their own; enhanced monetization through our campaign optimization technology; and, settlement services to facilitate payments to publishers for the inventory utilized by the advertisers. Through our proprietary publisher interface, publishers can control their participation in campaigns as well as their minimum acceptable level of revenue on an effective-CPM basis.

Lead Generation Marketing & E-commerce

Our Media segment previously included our lead generation marketing and e-commerce businesses. We divested our lead generation marketing business in February 2010 and our e-commerce

2

business in October 2008. These divestitures are discussed more fully in Note 5 to our consolidated financial statements contained in this annual report.

AFFILIATE MARKETING SEGMENT

Our Affiliate Marketing segment services, outlined below, are offered through our wholly-owned subsidiary Commission Junction. Through the combination of: a large-scale pay-for-performance model built on our proprietary technology platforms; marketing expertise; and a large, quality advertising network, our Affiliate Marketing business enables advertisers to develop their own fully-commissioned online sales force comprised of third-party affiliate publishers. We believe we are the largest provider of affiliate marketing services.

In affiliate marketing, a publisher joins an advertiser's affiliate marketing program and agrees to distribute the advertiser's offers in exchange for commissions on leads or sales generated. The publisher places the advertiser's display ads or text links on their website, in email campaigns, or in search listings, and receives a commission from the advertiser only when a visitor takes an agreed-upon action, such as filling out a form or making a purchase on the advertiser's website.

Our Affiliate Marketing services are offered on a hosted basis to enable marketers to execute their own affiliate marketing programs without the expense of building and maintaining their own in-house technical infrastructure and resources.

CJ Marketplace

To facilitate our advertiser customers' recruitment of affiliate publishers, we manage CJ Marketplace, an advertising network dedicated to our affiliate marketing business. Advertisers upload their offers onto CJ Marketplace, making them available for placement by affiliates. Affiliates apply to join the advertiser's program, and upon acceptance, select and place the advertiser's offers on their websites, in email campaigns, or in search listings. These links are served and tracked by Commission Junction. When a visitor clicks on one of the affiliate's links and then makes an online purchase or completes an agreed-upon action on the advertiser's website, that transaction is tracked and recorded by Commission Junction.

CJ Marketplace provides an open environment whereby affiliates can quickly view payment and conversion statistics to assess the effectiveness of every advertiser relationship and advertisement, and advertisers can quickly gauge the quality and potential of every affiliate relationship in the marketplace, allowing them to maximize the performance and scale of their online advertising campaigns.

Affiliate Marketing revenues are principally driven by variable compensation that is based on either a percentage of commissions paid to affiliates or on a percentage of transaction revenue generated from the programs managed with our affiliate marketing platforms.

In addition to the transaction-related revenue streams, we also receive monthly service fees from our advertiser customers who elect to utilize our Program Management service offerings. With these services, we assume full responsibility for all aspects of managing the advertiser's program including planning, affiliate recruitment, program review and management, and program administration.

Search Marketing

Search marketing allows advertisers to find prospective customers who are actively engaged in researching and buying products and services online. Our CJ Search product provides a fully-managed, comprehensive search engine marketing (SEM) solution by combining proprietary technology and expert services to optimize keyword campaigns across major search and shopping engines, and is specifically designed to complement our advertisers' affiliate marketing efforts. We use our technology and processes to create, manage and optimize pay-per-click, paid inclusion and organic search

3

campaigns for our advertiser customers. SEM revenues are driven primarily by a percentage of the revenue we generate for our advertiser customers.

OWNED & OPERATED WEBSITES SEGMENT

Our Owned & Operated Websites segment services are offered through a number of transaction-focused branded websites including Pricerunner, Smarter.com and Couponmountain.com. In 2009, we also launched a limited number of content websites in key online verticals such as healthcare, finance, travel, home and garden, education and business services.

The Pricerunner comparison shopping destination websites operate in the United Kingdom, Sweden, Germany, France, Denmark, and Austria. The Smarter.com and Couponmountain.com websites operate primarily in the United States and, to a lesser extent, Japan and China. The Pricerunner and Smarter.com websites enable consumers to research and compare products from among thousands of online and/or offline merchants using our proprietary technologies. We gather product and merchant data and organize it into comprehensive catalogs on our destination websites, along with relevant consumer and professional reviews. The Couponmountain.com website allows consumers to locate coupons and deals related to products and services that may be of interest to them, and our content websites offer consumers information and reference material across a variety of topics. Our services in these areas are free for consumers, and we generate revenue in one of three ways: on a CPC basis for traffic delivered to the customers' websites from listings on our websites; on a CPA basis when a consumer completes a purchase or other specific event; and on a CPM basis for display advertising shown on our websites.

In addition to our destination websites, Search123, which operates primarily in Europe, is ValueClick's self-service paid search offering that generates its traffic primarily through syndication relationships with other search engines, Web portals and content websites. Search syndication revenues are driven primarily on a CPC basis.

TECHNOLOGY SEGMENT

Our Technology segment provides advertisers, advertising agencies, and other companies with the tools they need to effectively manage their online marketing programs. Our technology products and services are offered through our wholly-owned subsidiary Mediaplex, Inc. Mediaplex is an application services provider ("ASP") offering technology infrastructure tools and consultative services that enable marketers to implement and manage their own online display advertising, SEM and email campaigns. Our Mediaplex products are based on our proprietary MOJO® technology platform, which has the ability, among other attributes, to automatically configure advertisements in response to real-time information from an advertiser's enterprise data system and to provide ongoing campaign optimization and analytics. Mediaplex's products are priced primarily on a CPM or email-delivered basis.

Our Technology segment also included our Mediaplex Systems subsidiary prior to October 2008. We divested the operations of this subsidiary in October 2008. Please refer to Note 5 to our consolidated financial statements contained in this annual report on Form 10-K for further information about this divestiture.

INTERNATIONAL OPERATIONS

We currently conduct international operations through wholly-owned subsidiaries throughout Europe as well as China and Japan.

In August 1999, we commenced operations in the European market with ValueClick Europe Ltd., a wholly-owned subsidiary of ValueClick, Inc., based in the United Kingdom. Since then we have expanded in Europe by opening wholly-owned subsidiaries in Paris, France; Munich, Germany; Madrid, Spain; and Dublin, Ireland. In August 2004, we acquired Pricerunner AB, a leading provider of online

4

comparison shopping services in Europe, based in Sweden. In July 2007, we acquired MeziMedia, which has operations in the United States, China and Japan. Employees in our international subsidiaries totaled 400 as of December 31, 2009. For additional information regarding our international operations, see Note 17 to our consolidated financial statements contained in this annual report on Form 10-K.

TECHNOLOGY PLATFORMS

Our proprietary applications are constructed from established, readily available technologies. Some of the basic components that our products are built on come from leading software and hardware providers such as Oracle, Sybase, Sun, Dell, EMC, NetApp, and Cisco while some components are constructed from leading Open Source initiatives such as Apache Web Server, MySQL, Java, Perl, PHP, and Linux. By striking the proper balance between using commercially available software and Open Source software, our technology expenditures are directed toward enhancing and maintaining our technology platforms while minimizing our technology costs.

We build high-performance, availability and reliability into our product offerings. We safeguard against the potential for service interruptions by engineering fail-safe controls into our critical software components. ValueClick delivers its solutions from a variety of geographic locations within the United States, Europe and China. ValueClick applications are monitored 24 hours a day, 365 days a year by specialized monitoring systems that aggregate alarms to a human-staffed network operations center.

SALES, MARKETING AND CUSTOMER SERVICE

We market our products and services primarily through direct marketing, print advertising and online advertising throughout the year. We also market them through the ValueClick properties' websites, trade show participation and other media events. In addition, we actively pursue public relations programs to promote our brands, products and services to potential network publishers and advertiser customers, as well as to industry analysts.

Customers

We sell our products and services to a variety of advertisers, advertising agencies and traffic distribution partners. Our Media and Affiliate Marketing segment revenues are generated from thousands of customers, and there are no significant customer concentrations in these segments. Our Owned & Operated Websites and Technology segment each have a significant customer that comprises a large portion of each segment's respective revenues. A loss of, or reduction of revenue from, these significant customers could have a significant negative impact on the revenue of these segments.

Competition

We face intense competition in the Internet advertising market. We expect that this competition will continue to intensify in the future as a result of industry consolidation, the continuing maturation of the industry and low barriers to entry. We compete with a diverse and large pool of advertising, media and Internet companies.

Our ability to compete depends upon several factors, including the following:

- •

- our continued ability to aggregate large networks of quality publishers efficiently;

- •

- the timing and market acceptance of new solutions and enhancements to existing solutions developed by us;

- •

- our customer service and support efforts;

- •

- our sales and marketing efforts;

- •

- the ease of use, performance, price, and reliability of solutions provided by us; and

5

- •

- our ability to remain price competitive while maintaining our operating margins.

Additional competitive factors include, but are not limited to, our: reputation, knowledge of the advertising market, financial controls, geographical coverage, relationships with customers, technological capability, and quality and breadth of products and services. For additional information regarding our competitors, see "If we fail to compete effectively against other Internet advertising companies, we could lose customers or advertising inventory and our revenue and results of operations could decline" in the Item 1A Risk Factors discussion in this annual report on Form 10-K.

Seasonality and Cyclicality

We believe that our business is subject to seasonal fluctuations with the calendar fourth quarter generally being our strongest. Expenditures by advertisers and advertising agencies vary in cycles and tend to reflect the overall economic conditions, as well as budgeting and buying patterns.

INTELLECTUAL PROPERTY RIGHTS

We currently rely on a combination of copyright, trademark and trade secret laws and restrictions on disclosure to protect our intellectual property rights. Our success depends on the protection of the proprietary aspects of our technology as well as our ability to operate without infringing on the proprietary rights of others. We also enter into proprietary information and confidentiality agreements with our employees, consultants and commercial partners and control access to, and distribution of, our software documentation and other proprietary information. We have registered the trademark "ValueClick" in the United States and the European Union. We currently have nine pending U.S. patent applications. In addition, we have been granted ten U.S. patents. We do not know if our current patent applications or any future patent application will result in a patent being issued within the scope of the claims we seek, if at all, or whether any patents we may have or may receive will be challenged or invalidated. Although patents are only one component of the protection of intellectual property rights, if our patent applications are denied, it may result in increased competition and the development of products substantially similar to our own. In addition, it is difficult to monitor unauthorized use of technology, particularly in foreign countries where the laws may not protect our proprietary rights as fully as in the United States, and our competitors may independently develop technology similar to our own. We will continue to assess appropriate occasions for seeking patent and other intellectual property protections for those aspects of our technology that we believe constitute innovations providing significant competitive advantages.

CORPORATE HISTORY AND RECENT ACQUISITIONS

We commenced operations as ValueClick, LLC, a California limited liability company, on May 1, 1998. Prior to the formation of ValueClick, LLC, the ValueClick Internet advertising business began in July 1997 as a line of business within Web-Ignite Corporation, a company wholly owned by the founding member of ValueClick, LLC. The reorganization and formation of ValueClick, LLC was affected by the transfer of the Internet advertising business of Web-Ignite to ValueClick, LLC. On December 31, 1998, ValueClick, LLC reorganized as ValueClick, Inc., a Delaware corporation. On March 30, 2000, we completed our initial public offering of common stock. Our common stock is publicly traded and is reported on the NASDAQ Global Select Market under the symbol "VCLK." We have acquired 14 companies since our inception, the most recent of which was MeziMedia in July 2007.

PRIVACY

We may collect personally identifiable information on a permitted basis. We store this personally identifiable data securely and do not use the data without the permission of the Web user. In addition, we use anonymous and non-personally identifiable information, in accordance with our privacy policies, for purposes that include, without limitation, tailoring advertisements and website content to a Web

6

user's interests. We use "cookies," along with other technologies, as set forth in our privacy policies, for purposes that include, without limitation, improving the experience Web users have when they see Web advertisements, advertising campaign reporting, and website reporting.

Please refer to the section entitled "Government Enforcement Actions, Changes in Government Regulation and Industry Standards, Including, But Not Limited To Spyware, Privacy and Email Matters, Could Decrease Demand For Our Products and Services and Increase Our Costs of Doing Business" in Item 1A "Risk Factors" of this annual report on Form 10-K for further details about our compliance with privacy regulations.

EMPLOYEES

As of December 31, 2009, we had 686 employees in the U.S. and 400 employees in our international locations. None of these employees are covered by collective bargaining agreements. Management believes that our relations with our employees are good.

EXECUTIVE OFFICERS

See Part III, Item 10 "Directors and Executive Officers of the Registrant" of this annual report on Form 10-K for information about executive officers of the registrant.

WEBSITE ACCESS TO OUR PERIODIC SEC REPORTS

Our primary Internet address is www.valueclick.com. We make our Securities and Exchange Commission ("SEC") periodic reports (Forms 10-Q and Forms 10-K) and current reports (Forms 8-K), and amendments to these reports, available free of charge through our website as soon as reasonably practicable after they are filed electronically with the SEC. We may from time to time provide important disclosures to investors by posting them in the investor relations section of our website, as allowed by SEC rules.

Materials we file with the SEC may be read and copied at the SEC's Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. Information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. The SEC also maintains an Internet website at www.sec.gov that contains reports, proxy and information statements, and other information regarding our Company that we file electronically with the SEC.

CODE OF ETHICS AND BUSINESS CONDUCT

We have adopted a Code of Ethics and Business Conduct (the "Code") for our principal executive, financial and accounting, and other officers, and our directors, employees, agents, and consultants. The Code is publicly available on our website at www.valueclick.com under the heading "About Us." Among other things, the Code addresses such issues as conflicts of interest, corporate opportunities, confidentiality, fair dealing, protection and proper use of Company assets, compliance with applicable laws (including insider trading laws), and reporting of illegal or unethical behavior.

Within the Code, ValueClick has established an accounting ethics complaint procedure for all of its employees. The complaint procedure is for employees who may have concerns regarding accounting, internal accounting controls and auditing matters. We treat all complaints confidentially and with the utmost professionalism. If an employee desires, he or she may submit any concerns or complaints on an anonymous basis, and his or her concerns or complaints will be addressed in the same manner as any other complaints. We do not, and will not, condone any retaliation of any kind against an employee who comes forward with an ethical concern or complaint.

7

You should carefully consider the following risks before you decide to buy shares of our common stock. The risks and uncertainties described below are not the only ones facing us. Additional risks and uncertainties, including those risks set forth in "Management's Discussion and Analysis of Financial Condition and Results of Operations" below, may also adversely impact and impair our business. If any of the following risks actually occur, our business, results of operations or financial condition would likely suffer. In such case, the trading price of our common stock could decline, and you may lose all or part of the money you paid to buy our stock.

This annual report on Form 10-K contains forward-looking statements based on the current expectations, assumptions, estimates, and projections about us and our industry. These forward-looking statements involve risks and uncertainties. Our actual results could differ materially from those discussed in these forward-looking statements as a result of certain factors, as more fully described in this section and elsewhere in this annual report on Form 10-K. We undertake no obligation to release publicly any revisions to any forward-looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

DETERIORATING MACROECONOMIC CONDITIONS IN THE UNITED STATES HAVE NEGATIVELY IMPACTED OUR BUSINESS AND FURTHER WEAKENING OF MACROECONOMIC CONDITIONS MAY HAVE ADDITIONAL NEGATIVE IMPACTS ON OUR BUSINESS.

In 2008, we began experiencing weakness across most of our business segments in connection with deteriorating macroeconomic conditions in the United States and Europe. Our consolidated full year 2009 revenue and cash generated from operations decreased as compared to the prior year amounts. We are not able to predict whether general macroeconomic conditions, or conditions in the online advertising industry specifically, will worsen or improve, or the timing of such developments. If macroeconomic conditions worsen, we are not able to predict the impact such worsening conditions will have on the online marketing industry in general, and our results of operations specifically. Further, when macroeconomic conditions do improve, there can be no assurances that we will be able to regain the levels of revenue, profitability and positive cash flow that we achieved prior to the macroeconomic downturn.

OUR PROFITABILITY MAY NOT REMAIN AT CURRENT LEVELS

We face risks that could prevent us from achieving our current profitability levels in future periods. These risks include, but are not limited to, our ability to:

- •

- adapt our products, services and cost structure to changing macroeconomic conditions;

- •

- maintain and increase our inventory of advertising space on publisher websites and with email list owners and newsletter

publishers;

- •

- maintain and increase the number of advertisers that use our products and services;

- •

- continue to expand the number of products and services we offer and the capacity of our systems;

- •

- adapt to changes in Web advertisers' promotional needs and policies, and the technologies used to generate Web

advertisements;

- •

- respond to challenges presented by the large and increasing number of competitors in the industry;

- •

- respond to challenges presented by the continuing consolidation within our industry;

8

- •

- adapt to changes in legislation, taxation or regulation regarding Internet usage, advertising and e-commerce;

- •

- adapt to changes in technology related to online advertising filtering software; and

- •

- adapt to changes in the competitive landscape.

If we are unsuccessful in addressing these or other risks and uncertainties, our business, results of operations and financial condition could be materially and adversely affected.

IF ADVERTISING ON THE INTERNET LOSES ITS APPEAL, OUR REVENUE COULD DECLINE.

Our business models may not continue to be effective in the future for a number of reasons, including the following: click and conversion rates have always been low and may decline as the number of advertisements and ad formats on the Web increases; Web users can install "filter" software programs which allow them to prevent advertisements from appearing on their computer screens or in their email boxes; Internet advertisements are, by their nature, limited in content relative to other media; companies may be reluctant or slow to adopt online advertising that replaces, limits or competes with their existing direct marketing efforts; companies may prefer other forms of Internet advertising we do not offer, including certain forms of search engine placements; companies may not utilize online advertising due to concerns of "click-fraud", particularly related to search engine placements; and regulatory actions may negatively impact certain business practices that we currently rely on to generate a portion of our revenue and profitability. If the number of companies who purchase online advertising from us does not grow, we may experience difficulty in attracting publishers, and our revenue could decline.

OUR REVENUE COULD DECLINE IF WE FAIL TO EFFECTIVELY MANAGE OUR EXISTING ADVERTISING SPACE AND OUR GROWTH COULD BE IMPEDED IF WE FAIL TO ACQUIRE NEW ADVERTISING SPACE.

Our success depends in part on our ability to effectively manage our existing advertising space. The Web publishers and email list owners that list their unsold advertising space with us are not bound by long-term contracts that ensure us a consistent supply of advertising space, which we refer to as inventory. In addition, Web publishers or email list owners can change the amount of inventory they make available to us at any time. If a Web publisher or email list owner decides not to make advertising space from its websites, newsletters or email lists available to us, we may not be able to replace this advertising space with advertising space from other Web publishers or email list owners that have comparable traffic patterns and user demographics quickly enough to fulfill our advertisers' requests. This would result in lost revenue.

We expect that our advertiser customers' requirements will become more sophisticated as the Web continues to mature as an advertising medium. If we fail to manage our existing advertising space effectively to meet our advertiser customers' changing requirements, our revenue could decline. Our growth depends, in part, on our ability to expand our advertising inventory within our networks and to have access to new sources of advertising inventory such as ad exchange. To attract new customers, we must maintain a consistent supply of attractive advertising space. Our success relies in part on expanding our advertising inventory by selectively adding new Web publishers and email list owners to our networks that offer attractive demographics, innovative and quality content and growing Web user traffic and email volume. Our ability to attract new Web publishers and email list owners to our networks and to retain Web publishers and email list owners currently in our networks will depend on various factors, some of which are beyond our control. These factors include, but are not limited to: our ability to introduce new and innovative products and services, our ability to efficiently manage our existing advertising inventory, our pricing policies, and the cost-efficiency to Web publishers and email list owners of outsourcing their advertising sales. In addition, the number of competing intermediaries

9

that purchase advertising inventory from Web publishers and email list owners continues to increase. We cannot assure you that the size of our advertising inventory will increase or remain constant in the future.

OUR OWNED & OPERATED WEBSITES SEGMENT REVENUE IS SUBJECT TO CUSTOMER CONCENTRATION RISKS. THE LOSS OF ONE OR MORE OF THE MAJOR CUSTOMERS IN OUR OWNED & OPERATED WEBSITES SEGMENT COULD SIGNIFICANTLY AND NEGATIVELY IMPACT THE REVENUE AND PROFITABILITY LEVELS OF THIS SEGMENT.

Our Owned & Operated Websites business generates revenue through a combination of: sponsored search listings placed on our destination websites, merchant relationships, affiliate marketing networks and display advertising on our destination websites. A large portion of the revenue in our Owned & Operated Websites segment is generated via sponsored search listings from major search engines. Factors that could cause these relationships to cease or become significantly reduced in scale include, but are not limited to: the non-renewal of our distribution agreement with one or more of the major search engines; the determination by one or more of the major search engines that consumer traffic received from us does not meet their quality standards (in other words, the traffic is not converting at appropriate rates); and changes in the competitive environment, such as industry consolidation. If our relationships with one or more of the major search engines were to cease or become significantly reduced in scale, our revenue and profitability levels could be significantly and negatively impacted. In the fourth quarter of 2009, our largest customer in our Owned & Operated Websites segment made changes that negatively impacted the amount of traffic that we could monetize with them. This change had a significant negative impact on the revenue levels of this segment beginning in the fourth quarter of 2009. As a result of this change, we expect our revenue from the Owned & Operated Websites segment in 2010 to be lower than it was in 2009.

CHANGES IN HOW WE GENERATE ONLINE CONSUMER TRAFFIC FOR OUR DESTINATION WEBSITES COULD NEGATIVELY IMPACT OUR ABILITY TO MAINTAIN OR GROW THE REVENUE AND PROFITABILITY LEVELS OF OUR OWNED & OPERATED WEBSITES SEGMENT.

We generate online consumer traffic for our destination websites using various methods, including: organic traffic, offline marketing campaigns, distribution agreements, search engine marketing (SEM) and search engine optimization (SEO). The current revenue and profitability levels of our Owned & Operated Websites segment are dependent upon our continued ability to use a combination of these methods to generate online consumer traffic to our websites in a cost-efficient manner. Our SEM and SEO techniques have been developed to work with the existing search algorithms utilized by the major search engines. The major search engines frequently modify their search algorithms. Future changes in these search algorithms could change the mix of the methods we use to generate online consumer traffic for our destination websites and could negatively impact our ability to generate such traffic in a cost-efficient manner, which could result in a significant reduction to the revenue and profitability of our Owned & Operated Websites segment. There can be no assurances that we will be able to maintain the current mix of online consumer traffic sources for our destination websites or that we will be able to modify our SEM and SEO techniques to address any future search algorithm changes made by the major search engines.

WE MAY FACE INTELLECTUAL PROPERTY ACTIONS THAT ARE COSTLY OR COULD HINDER OR PREVENT OUR ABILITY TO DELIVER OUR PRODUCTS AND SERVICES.

We may be subject to legal actions alleging intellectual property infringement (including patent infringement), unfair competition or similar claims against us. Companies may apply for or be awarded patents or have other intellectual property rights covering aspects of our technologies or businesses. We

10

are currently involved in two patent disputes with subsidiaries of AOL, Inc. On July, 15, 2008, we filed a complaint against Tacoda, Inc., a Company which was subsequently acquired by AOL, Inc., in the United States District Court for the for the Central District of California for patent infringement of U.S. patent numbers 5,848,396 and 5,991,735. In March of 2009, Netscape, Inc. a subsidiary of AOL, Inc., filed a complaint in the United States District Court for the Eastern District of Virginia against ValueClick, Inc., Mediaplex, Inc., Commission Junction, Inc., MeziMedia, Inc. Web Clients, Inc., and Fastclick, Inc. for alleged patent infringement of U.S. patent number 5,774,670. If Netscape is successful in its patent lawsuit against us, it could result in a large monetary reward against us. If Netscape obtains an injunction from the Court against us, it could require us to change our business practices, could potentially hinder or prevent our ability to deliver our products and services and could divert management's attention.

IF THE TECHNOLOGY THAT WE CURRENTLY USE TO TARGET THE DELIVERY OF ONLINE ADVERTISEMENTS AND TO PREVENT FRAUD ON OUR NETWORKS IS RESTRICTED OR BECOMES SUBJECT TO REGULATION, OUR EXPENSES COULD INCREASE AND WE COULD LOSE CUSTOMERS OR ADVERTISING INVENTORY.

Websites typically place small files of non-personalized (or "anonymous") information, commonly known as cookies, on an Internet user's hard drive. Cookies generally collect information about users on a non-personalized basis to enable websites to provide users with a more customized experience. Cookie information is passed to the website through an Internet user's browser software. We currently use cookies to track an Internet user's movement through our advertiser customer's websites and to monitor and prevent fraudulent activity on our networks. Most currently available Internet browsers allow Internet users to modify their browser settings to prevent cookies from being stored on their hard drive, and some users currently do so. Internet users can also delete cookies from their hard drives at any time. Some Internet commentators and privacy advocates have suggested limiting or eliminating the use of cookies, and legislation has been introduced in some jurisdictions to regulate the use of cookie technology. The effectiveness of our technology could be limited by any reduction or limitation in the use of cookies. If the use or effectiveness of cookies were limited, we expect that we would need to switch to other technologies to gather demographic and behavioral information. While such technologies currently exist, they may be less effective than cookies. We also expect that we would need to develop or acquire other technology to monitor and prevent fraudulent activity on our networks. Replacement of cookies could require reengineering time and resources, might not be completed in time to avoid losing customers or advertising inventory, and might not be commercially feasible. Our use of cookie technology or any other technologies designed to collect Internet usage information may subject us to litigation or investigations in the future. Any litigation or government action against us could be costly and time consuming, could require us to change our business practices and could divert management's attention.

IF WE FAIL TO COMPETE EFFECTIVELY AGAINST OTHER INTERNET ADVERTISING COMPANIES, WE COULD LOSE CUSTOMERS OR ADVERTISING INVENTORY AND OUR REVENUE AND RESULTS OF OPERATIONS COULD DECLINE.

The Internet advertising markets are characterized by rapidly changing technologies, evolving industry standards, frequent new product and service introductions, and changing customer demands. The introduction of new products and services embodying new technologies and the emergence of new industry standards and practices could render our existing products and services obsolete and unmarketable or require unanticipated technology or other investments. Our failure to adapt successfully to these changes could harm our business, results of operations and financial condition.

The market for Internet advertising and related products and services is highly competitive. We expect this competition to continue to increase, in part because there are no significant barriers to

11

entry to our industry. Increased competition may result in price reductions for advertising space, reduced margins and loss of market share. Our principal competitors include other companies that provide advertisers with Internet advertising solutions and companies that offer pay-per-click search services. We compete in the performance-based marketing segment with CPL and CPA performance-based companies, such as Platform-A (owned by AOL), Google Affiliate Network, Trade Doubler, and Linkshare (owned by Rakuten), and we compete with other large Internet display advertising networks. In addition, we compete in the online comparison shopping market with focused comparison shopping websites such as Shopping.com (owned by eBay), Kelkoo, NexTag, Shopzilla (owned by EW Scripps), and Pricegrabber (owned by Experian), and with search engines and portals such as Yahoo!, Google and MSN, and with online retailers such as Amazon.com and eBay. Large websites with brand recognition, such as Yahoo!, Google, AOL and MSN, have direct sales personnel and substantial proprietary online advertising inventory that may provide competitive advantages compared to our networks, and they have a significant impact on pricing for online advertising overall. These companies have longer operating histories, greater name recognition and have greater financial, technical, sales, and marketing resources than we have. Further, Google, Yahoo! and Microsoft have made acquisitions to put them in direct competition with a number of our offerings.

Competition for advertising placements among current and future suppliers of Internet navigational and informational services, high-traffic websites and Internet service providers ("ISPs"), as well as competition with other media for advertising placements, could result in significant price competition, declining margins and reductions in advertising revenue. In addition, as we continue our efforts to expand the scope of our Web services, we may compete with a greater number of Web publishers and other media companies across an increasing range of different Web services, including in vertical markets where competitors may have advantages in expertise, brand recognition and other areas. If existing or future competitors develop or offer products or services that provide significant performance, price, creative or other advantages over those offered by us, our business, results of operations and financial condition could be negatively affected. We also compete with traditional advertising media, such as direct mail, television, radio, cable, and print, for a share of advertisers' total advertising budgets. Many current and potential competitors enjoy competitive advantages over us, such as longer operating histories, greater name recognition, larger customer bases, greater access to advertising space on high-traffic websites, and significantly greater financial, technical, sales, and marketing resources. As a result, we may not be able to compete successfully. If we fail to compete successfully, we could lose customers or advertising inventory and our revenue and results of operations could decline.

WE DEPEND ON KEY PERSONNEL, THE LOSS OF WHOM COULD HARM OUR BUSINESS.

Our success depends in part on the retention of personnel critical to our combined business operations due to, for example, unique technical skills, management expertise or key business relationships. We may be unable to retain existing management, finance, engineering, sales, customer support, and operations personnel that are critical to the success of the Company, which may result in disruption of operations, loss of key business relationships, information, expertise or know-how, unanticipated additional recruitment and training costs, and diminished anticipated benefits of acquisitions, including loss of revenue and profitability.

Our future success is substantially dependent on the continued service of our key senior management. Our employment agreements with our key personnel are short-term and on an at-will basis. We do not have key-person insurance on any of our employees. The loss of the services of any member of our senior management team, or of any other key employees, could divert management's time and attention, increase our expenses and adversely affect our ability to conduct our business efficiently. Our future success also depends on our continuing ability to attract, retain and motivate highly skilled employees. We may be unable to retain our key employees or attract, retain and motivate

12

other highly qualified employees in the future. We have experienced difficulty from time to time in attracting or retaining the personnel necessary to support the growth of our business, and may experience similar difficulties in the future.

DELAWARE LAW AND OUR STOCKHOLDER RIGHTS PLAN CONTAIN ANTI-TAKEOVER PROVISIONS THAT COULD DETER TAKEOVER ATTEMPTS THAT COULD BE BENEFICIAL TO OUR STOCKHOLDERS.

Provisions of Delaware law could make it more difficult for a third-party to acquire us, even if doing so would be beneficial to our stockholders. Section 203 of the Delaware General Corporation Law may make the acquisition of our company and the removal of incumbent officers and directors more difficult by prohibiting stockholders holding 15% or more of our outstanding voting stock from acquiring us, without our board of directors' consent, for at least three years from the date they first hold 15% or more of the voting stock. In addition, our Stockholder Rights Plan has significant anti-takeover effects by causing substantial dilution to a person or group that attempts to acquire us on terms not approved by our board of directors.

SYSTEM FAILURES COULD SIGNIFICANTLY DISRUPT OUR OPERATIONS, WHICH COULD CAUSE US TO LOSE CUSTOMERS OR ADVERTISING INVENTORY.

Our success depends on the continuing and uninterrupted performance of our systems. Sustained or repeated system failures that interrupt our ability to provide services to customers, including failures affecting our ability to deliver advertisements quickly and accurately and to process visitors' responses to advertisements, would reduce significantly the attractiveness of our solutions to advertisers and Web publishers. Our business, results of operations and financial condition could also be materially and adversely affected by any systems damage or failure that impacts data integrity or interrupts or delays our operations. Our computer systems are vulnerable to damage from a variety of sources, including telecommunications failures, power outages, malicious or accidental human acts, and natural disasters. We lease data center space in various locations in northern and southern California; Stockholm, Sweden; and Shanghai, China. Therefore, any of the above factors affecting any of these areas could substantially harm our business. Moreover, despite network security measures, our servers are potentially vulnerable to physical or electronic break-ins, computer viruses and similar disruptive problems in part because we cannot control the maintenance and operation of our third-party data centers. Despite the precautions taken, unanticipated problems affecting our systems could cause interruptions in the delivery of our solutions in the future and our ability to provide a record of past transactions. Our data centers and systems incorporate varying degrees of redundancy. All data centers and systems may not automatically switch over to their redundant counterpart. Our insurance policies may not adequately compensate us for any losses that may occur due to any failures in our systems.

IT MAY BE DIFFICULT TO PREDICT OUR FINANCIAL PERFORMANCE BECAUSE OUR QUARTERLY OPERATING RESULTS MAY FLUCTUATE.

Our revenue and operating results may vary significantly from quarter to quarter due to a variety of factors, many of which are beyond our control. You should not rely on period-to-period comparisons of our results of operations as an indication of our future performance. Our results of operations have fallen below the expectations of market analysts and our own forecasts in the past and may also do so in some future periods. If this happens, the market price of our common stock may fall significantly. The factors that may affect our quarterly operating results include, but are not limited to, the following:

- •

- macroeconomic conditions in the United States and Europe;

- •

- fluctuations in demand for our advertising solutions or changes in customer contracts;

- •

- fluctuations in click, lead, action, impression, and conversion rates;

13

- •

- fluctuations in the amount of available advertising space, or views, on our networks;

- •

- the timing and amount of sales and marketing expenses incurred to attract new advertisers;

- •

- fluctuations in sales of different types of advertising; for example, the amount of advertising sold at higher rates

rather than lower rates;

- •

- fluctuations in the cost of online advertising;

- •

- seasonal patterns in Internet advertisers' spending;

- •

- fluctuations in our stock price which may impact the amount of stock-based compensation we are required to record;

- •

- changes in our pricing and publisher compensation policies, the pricing and publisher compensation policies of our

competitors, the pricing and publisher compensation policies of our advertiser customers, or the pricing policies for advertising on the Internet generally;

- •

- changes in the regulatory environment, including regulation of advertising on the Internet, that may negatively impact our

marketing practices;

- •

- possible impairments of the recorded amounts of goodwill, intangible assets, or other long-lived assets;

- •

- the timing and amount of expenses associated with litigation, regulatory investigations or restructuring activities,

including settlement costs and regulatory penalties assessed related to government enforcement actions;

- •

- the adoption of new accounting pronouncements, or new interpretations of existing accounting pronouncements, that impact

the manner in which we account for, measure or disclose our results of operations, financial position or other financial measures;

- •

- the loss of, or a significant reduction in business from, large customers resulting from, among other factors, the

exercise of a cancellation clause within a contract, the non-renewal of a contract or an advertising insertion order, or shifting business to a competitor when the lack of an exclusivity

clause exists;

- •

- fluctuations in levels of professional services fees or the incurrence of non-recurring costs;

- •

- deterioration in the credit quality of our accounts receivable and an increase in the related provision;

- •

- impairments on our marketable securities due to, among other factors, issuer-specific difficulties or dislocations in the

credit markets in the United States;

- •

- changes in tax laws or our interpretation of tax laws, changes in our effective income tax rate or the settlement of

certain tax positions with tax authorities as a result of a tax audit; and

- •

- costs related to acquisitions of technologies or businesses.

Expenditures by advertisers also tend to be cyclical, reflecting overall economic conditions as well as budgeting and buying patterns. Any decline in the economic prospects of advertisers or the economy generally may alter advertisers' current or prospective spending priorities, or may increase the time it takes us to close sales with advertisers, and could materially and adversely affect our business, results of operations and financial condition.

14

OUR EXPANDING INTERNATIONAL OPERATIONS SUBJECT US TO ADDITIONAL RISKS AND UNCERTAINTIES AND WE MAY NOT BE SUCCESSFUL WITH OUR STRATEGY TO CONTINUE TO EXPAND SUCH OPERATIONS.

We initiated operations, through wholly-owned subsidiaries or divisions, in the United Kingdom in 1999, France and Germany in 2000, Sweden in 2004, Japan and China in 2007, and Spain and Ireland in 2008. Our international expansion and the integration of international operations present unique challenges and risks to our company, and require management attention. Compliance with complex foreign and U.S. laws and regulations that apply to our international operations increases our cost of doing business in international jurisdictions and could interfere with our ability to offer our products and services to one or more countries or expose us or our employees to fines and penalties. These laws and regulations include, but are not limited to, content requirements, tax laws, data privacy and filtering requirements, U.S. laws such as the Foreign Corrupt Practices Act, and local laws prohibiting corrupt payments to governmental officials. Violations of these laws and regulations could result in monetary damages, criminal sanctions against us, our officers, or our employees, and prohibitions on the conduct of our business. Our continued international expansion also subjects us to additional foreign currency exchange rate risks and will require additional management attention and resources. We cannot assure you that we will be successful in our international expansion. Our international operations and expansion subject us to other inherent risks, including, but not limited to:

- •

- the impact of recessions in economies outside of the United States;

- •

- changes in and differences between regulatory requirements between countries;

- •

- U.S. and foreign export restrictions, including export controls relating to encryption technologies;

- •

- reduced protection for and enforcement of intellectual property rights in some countries;

- •

- potentially adverse tax consequences;

- •

- difficulties and costs of staffing and managing foreign operations;

- •

- political and economic instability;

- •

- tariffs and other trade barriers; and

- •

- seasonal reductions in business activity.

Our failure to address these risks adequately could materially and adversely affect our business, revenue, results of operations and financial condition.

WE MAY NOT BE ABLE TO PROTECT OUR INTELLECTUAL PROPERTY FROM UNAUTHORIZED USE, WHICH COULD DIMINISH THE VALUE OF OUR PRODUCTS AND SERVICES, WEAKEN OUR COMPETITIVE POSITION AND REDUCE OUR REVENUE.

Our success depends in large part on our proprietary technologies, including tracking management software, our affiliate marketing technologies, our display advertising technologies, our lead generation technologies, our technology, including SEM technology that runs our owned and operated websites, and our MOJO platform. In addition, we believe that our trademarks are key to identifying and differentiating our products and services from those of our competitors. We may be required to spend significant resources to monitor and police our intellectual property rights. If we fail to successfully enforce our intellectual property rights, the value of our products and services could be diminished and our competitive position may suffer.

15

We rely on a combination of copyright, trademark and trade secret laws, confidentiality procedures and licensing arrangements to establish and protect our proprietary rights. Third-party software providers could copy or otherwise obtain and use our technologies without authorization or develop similar technologies independently, which may infringe upon our proprietary rights. We may not be able to detect infringement and may lose competitive position in the market before we do so. In addition, competitors may design around our technologies or develop competing technologies. Intellectual property protection may also be unavailable or limited in some foreign countries.

We generally enter into confidentiality or license agreements with our employees, consultants, vendors, customers, and corporate partners, and generally control access to and distribution of our technologies, documentation and other proprietary information. Despite these efforts, unauthorized parties may attempt to disclose, obtain or use our products and services or technologies. Our precautions may not prevent misappropriation of our products, services or technologies, particularly in foreign countries where laws or law enforcement practices may not protect our proprietary rights as fully as in the United States.

GOVERNMENT ENFORCEMENT ACTIONS, CHANGES IN GOVERNMENT REGULATION AND INDUSTRY STANDARDS, INCLUDING, BUT NOT LIMITED TO SPYWARE, PRIVACY AND EMAIL MATTERS, COULD DECREASE DEMAND FOR OUR PRODUCTS AND SERVICES AND INCREASE OUR COSTS OF DOING BUSINESS.

Laws and regulations that apply to Internet communications, commerce and advertising are becoming more prevalent. These regulations could affect the costs of communicating on the Web and could adversely affect the demand for our advertising solutions or otherwise harm our business, results of operations and financial condition. The United States Congress has enacted Internet legislation regarding children's privacy, copyrights, sending of commercial email (e.g., the Federal CAN-SPAM Act of 2003), and taxation. The United States Congress has passed legislation regarding spyware (i.e., H.R. 964, the "Spy Act of 2007") and the New York Attorney General's office has also pursued enforcement actions against companies in this industry. The Federal Trade Commission ("FTC") conducted an investigation in 2007 into certain ValueClick websites which promise consumers a free gift of substantial value, and the manner in which they drive traffic to such websites, in particular through email. In the first quarter of 2008, we agreed to a stipulated injunction with the FTC resolving this matter. The injunction made clear that it constituted no finding of any impermissible conduct by us in the past under preexisting FTC regulations then in effect. But the injunction also imposed new FTC guidelines for promotional lead generation activities, consistent with the approach that the agency applied to our competitors. In addition, the FTC issued a report and a revised set of "Self-Regulatory Principles for Online Behavioral Advertising" which promotes principles designed to encourage meaningful self-regulation with regard to online behavioral advertising within the industry, however its message strongly encourages that industry participants come up with more meaningful and rigorous self-regulation or invite legislation by states, Congress or a more regulatory approach by the FTC. Such legislation or increased regulatory approach, including legislation by Congress or guidelines by the FTC that may require consumers to "opt-in" before any data is collected about their web viewing behavior, may adversely affect our ability to grow our company and our behavioral targeting platform. Other laws and regulations have been adopted and may be adopted in the future, and may address issues such as user privacy, spyware, "do not email" lists, pricing, intellectual property ownership and infringement, copyright, trademark, trade secret, export of encryption technology, click-fraud, acceptable content, search terms, lead generation, behavioral targeting, taxation, and quality of products and services. This legislation could hinder growth in the use of the Web generally and adversely affect our business. Moreover, it could decrease the acceptance of the Web as a communications, commercial and advertising medium. We do not use any form of spam or spyware and has policies to prohibit abusive Internet behavior, including prohibiting the use of spam and spyware by our Web publisher partners.

16

Due to the global nature of the Web, it is possible that, although our transmissions originate in California, Sweden and China, the governments of other states or foreign countries might attempt to regulate our transmissions or levy sales or other taxes relating to our activities. In addition, the growth and development of the market for Internet commerce may prompt calls for more stringent consumer protection laws, both in the United States and abroad, that may impose additional burdens on companies conducting business over the Internet. The laws governing the Internet remain largely unsettled, even in areas where there has been some legislative action. It may take years to determine how existing laws, including those governing intellectual property, privacy, libel and taxation, apply to the Internet and Internet advertising. Our business, results of operations and financial condition could be materially and adversely affected by the adoption or modification of industry standards, laws or regulations relating to the Internet, or the application of existing laws to the Internet or Internet-based advertising.

WE COULD BE SUBJECT TO LEGAL CLAIMS, GOVERNMENT ENFORCEMENT ACTIONS AND DAMAGE TO OUR REPUTATION AND HELD LIABLE FOR OUR OR OUR CUSTOMERS' FAILURE TO COMPLY WITH FEDERAL, STATE AND FOREIGN LAWS, REGULATIONS OR POLICIES GOVERNING CONSUMER PRIVACY, WHICH COULD MATERIALLY HARM OUR BUSINESS.

Recent growing public concern regarding privacy and the collection, distribution and use of information about Internet users has led to increased federal, state and foreign scrutiny and legislative and regulatory activity concerning data collection and use practices. The United States Congress currently has pending legislation regarding privacy and data security measures (e.g., S. 495, the "Personal Data Privacy and Security Act of 2007"). Any failure by us to comply with applicable federal, state and foreign laws and the requirements of regulatory authorities may result in, among other things, indemnification liability to our customers and the advertising agencies we work with, administrative enforcement actions and fines, class action lawsuits, cease and desist orders, and civil and criminal liability. Recently, class action lawsuits have been filed alleging violations of privacy laws by ISPs. The European Union's directive addressing data privacy limits our ability to collect and use information regarding Internet users. These restrictions may limit our ability to target advertising in most European countries. Our failure to comply with these or other federal, state or foreign laws could result in liability and materially harm our business.

In addition to government activity, privacy advocacy groups and the technology and direct marketing industries are considering various new, additional or different self-regulatory standards. This focus, and any legislation, regulations or standards promulgated, may impact us adversely. Governments, trade associations and industry self-regulatory groups may enact more burdensome laws, regulations and guidelines, including consumer privacy laws, affecting our customers and us. Since many of the proposed laws or regulations are just being developed, and a consensus on privacy and data usage has not been reached, we cannot yet determine the impact these proposed laws or regulations may have on our business. However, if the gathering of profiling information were to be curtailed, Internet advertising would be less effective, which would reduce demand for Internet advertising and harm our business.

Third parties may bring class action lawsuits against us relating to online privacy and data collection. We disclose our information collection and dissemination policies, and we may be subject to claims if we act or are perceived to act inconsistently with these published policies. Any claims or inquiries could be costly and divert management's attention, and the outcome of such claims could harm our reputation and our business.

Our customers are also subject to various federal and state laws concerning the collection and use of information regarding individuals. These laws include the Children's Online Privacy Protection Act, the Federal Drivers Privacy Protection Act of 1994, the privacy provisions of the Gramm-Leach-Bliley

17

Act, the Federal CAN-SPAM Act of 2003, as well as other laws that govern the collection and use of consumer credit information. We cannot assure you that our customers are currently in compliance, or will remain in compliance, with these laws and their own privacy policies. We may be held liable if our customers use our technologies in a manner that is not in compliance with these laws or their own stated privacy policies.

OUR STOCK PRICE IS LIKELY TO BE VOLATILE AND COULD DROP UNEXPECTEDLY.

Our common stock has been publicly traded since March 30, 2000. The market price of our common stock has been subject to significant fluctuations since the date of our initial public offering.

The stock market has from time to time experienced significant price and volume fluctuations that have affected the market prices of securities, particularly securities of technology companies. As a result, the market price of our common stock may materially decline, regardless of our operating performance. In the past, following periods of volatility in the market price of a particular company's securities, securities class action litigation has often been brought against that company. We were involved in this type of litigation, which arose shortly after our stock price dropped significantly during the third quarter of 2007. Litigation of this type is often expensive and diverts management's attention and resources.

SEVERAL STATES HAVE IMPLEMENTED OR PROPOSED REGULATIONS THAT IMPOSE SALES TAX ON CERTAIN ECOMMERCE TRANSACTIONS INVOLVING THE USE OF AFFILIATE MARKETING PROGRAMS.

In 2008, the state of New York implemented regulations that require advertisers to collect and remit sales taxes on sales made to residents of New York if the affiliate/publisher that facilitated that sale is a New York-based entity. In addition, several other states, including California, have proposed similar regulations, although most of the regulations proposed by these other states have not passed. While the New York sales tax requirement has not had a material impact on our Affiliate Marketing segment results of operations, we are unable to determine the impact on our Affiliate Marketing business if other states adopt similar requirements.

WE MAY BE REQUIRED TO RECORD A SIGNIFICANT CHARGE TO EARNINGS IF OUR GOODWILL OR AMORTIZABLE INTANGIBLE ASSETS BECOME IMPAIRED.

As disclosed in this Annual Report on Form 10-K, we recorded an impairment charge as of December 31, 2008 related to our goodwill and amortizable intangible assets totaling $269.5 million. As of December 31, 2009, we have $157.1 million and $38.7 million of goodwill and amortizable intangible assets, respectively, remaining.

We perform our annual impairment analysis of goodwill as of December 31 of each year, or sooner if we determine there are indicators of impairment, in accordance with accounting principles generally accepted in the United States of America ("GAAP"). Under GAAP, the impairment analysis of goodwill must be based on estimated fair values. The determination of fair values requires assumptions and estimates of many critical factors, including, but not limited to: expected operating results; macroeconomic conditions; our stock price; earnings multiples implied in acquisitions in the online marketing industry; industry analyst expectations; and the discount rates used in the discounted cash flow analysis. We are required to perform our next goodwill impairment analysis at December 31, 2010. If macroeconomic conditions deteriorate further in 2010 or our stock price experiences further declines, we may be required to record additional impairment charges in the future.

We are also required under GAAP to review our amortizable intangible assets for impairment whenever events and circumstances indicate that the carrying value of such assets may not be

18

recoverable. We may be required to record a significant charge to earnings in a period in which any impairment of our goodwill or amortizable intangible assets is determined.

WE MAY INCUR LIABILITIES TO TAX AUTHORITIES IN EXCESS OF AMOUNTS THAT HAVE BEEN ACCRUED WHICH MAY ADVERSELY IMPACT OUR RESULTS OF OPERATIONS AND FINANCIAL CONDITION.

As more fully described in Note 9 to our consolidated financial statements, we have recorded significant income tax liabilities. The preparation of our consolidated financial statements requires estimates of the amount of income tax that will become payable in each of the jurisdictions in which we operate. We may be challenged by the taxing authorities in these jurisdictions and, in the event that we are not able to successfully defend our position, we may incur significant additional income tax liabilities and related interest and penalties which may have an adverse impact on our results of operations and financial condition.

IF WE FAIL TO MAINTAIN AN EFFECTIVE SYSTEM OF INTERNAL CONTROLS, WE MAY NOT BE ABLE TO ACCURATELY REPORT OUR FINANCIAL RESULTS OR PREVENT FRAUD AND OUR BUSINESS MAY BE HARMED AND OUR STOCK PRICE MAY BE ADVERSELY IMPACTED.