Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended December 31, 2009

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number 000-25032

UNIVERSAL STAINLESS & ALLOY PRODUCTS, INC.

(Exact name of Registrant as specified in its charter)

| DELAWARE | 25-1724540 | |

| (State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification No.) |

| 600 MAYER STREET, BRIDGEVILLE, PA 15017 | (412) 257-7600 | |

| (Address of principal executive offices, including zip code) | (Registrant’s telephone number, including area code) |

Securities registered pursuant to Section 12(b) of the Act: [None]

Securities registered pursuant to Section 12(g) of the Act:

Title of Class

Common Stock, par value $.001 per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data file required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definitions of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check One)

| Large accelerated filer | ¨ | Accelerated filer | x | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the voting stock held by non-affiliates of the registrant on June 30, 2009, based on the closing price of $16.27 per share on that date, was $74,758,000. For the purposes of this disclosure only, the registrant has assumed that its directors, executive officers, and beneficial owners of 5% or more of the registrant’s Common Stock are the affiliates of the registrant. The registrant has made no determination that such persons are “affiliates” within the meaning of Rule 405 under the Securities Act of 1933.

As of February 26, 2010, there were 6,773,104 shares of the Registrant’s Common Stock issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Part III of this Form 10-K incorporates by reference portions of the Company’s definitive Proxy Statement for the Annual Meeting of Stockholders scheduled to be held May 19, 2010.

Table of Contents

2

Table of Contents

| ITEM 1. | BUSINESS |

GENERAL

Universal Stainless & Alloy Products, Inc. and its wholly-owned subsidiaries (the “Company”), which was incorporated in 1994, manufactures and markets semi-finished and finished specialty steel products, including stainless steel, tool steel and certain other alloyed steels. The Company’s manufacturing process involves melting, remelting, heat treating, hot and cold rolling, machining and cold drawing of semi-finished and finished specialty steels. The Company’s products are sold to rerollers, forgers, service centers, original equipment manufacturers (“OEMs”) and wire redrawers. The Company’s customers further process its products for use in a variety of industries, including the aerospace, power generation, petrochemical and heavy equipment manufacturing industries. The Company also performs conversion services on materials supplied by customers that lack certain of the Company’s production facilities or that are subject to their own capacity constraints.

The Company is comprised of three operating locations and one corporate headquarters. For segment reporting, the Bridgeville and Titusville facilities have been aggregated into one reportable segment, Universal Stainless & Alloy Products. Dunkirk Specialty Steel represents the second reportable segment.

The Company’s products are manufactured in a wide variety of grades, widths and gauges in response to customer specifications. At its Bridgeville facility, the Company produces specialty steel products in the form of long products (ingots, blooms, billets and bars) and flat rolled products (slabs and plates). Certain grades requiring vacuum-arc remelting (“VAR”) may be transported to the Titusville facility to complete that process and then be transported back to the Bridgeville facility for further processing. The semi-finished long products are primarily used by the Company’s Dunkirk facility and certain customers to produce finished bar, rod and wire products, and the semi-finished flat rolled products are used by customers to produce light-gauge plate, sheet and strip products. The finished bar products manufactured by the Company are primarily used by OEMs and by service center customers for distribution to a variety of end users. The Company also produces customized shapes primarily for OEMs that are cold rolled from purchased coiled strip, flat bar or extruded bar at its Precision Rolled Products department (“PRP”), located at its Titusville facility.

INDUSTRY OVERVIEW

The specialty steel industry is a relatively small but distinct segment of the overall steel industry. Specialty steels include stainless steels, high-speed and tool steels, electrical steels, high-temperature alloys, magnetic alloys and electronic alloys. Specialty steels are made with a high alloy content, which enables their use in environments that demand exceptional hardness, toughness, strength and resistance to heat, corrosion or abrasion, or combinations thereof. Specialty steels generally must conform to more demanding customer specifications for consistency, straightness and surface finish than carbon steels. According to the Specialty Steel Industry of North America (“SSINA”), annual domestic consumption of specialty steels approximated 2.3 million tons in 2008. Of this amount, approximately 1.6 million tons of specialty steels consumed domestically represented stainless steel sheet and strip and electrical alloy products which the Company does not produce. Also, according to SSINA data through October 31, 2009, U.S. consumption of total specialty steel products in 2009 decreased 36% from 2008 levels. The consumption of those products in the Company’s addressable market, comprising stainless steel bar, rod and wire products, decreased by 38.9%, 47.2% and 42.2%, respectively.

The Company primarily manufactures its products within the following product lines and, generally, in response to customer orders:

Stainless Steel. Stainless steel, which represents the largest part of the specialty steel market, contains elements such as nickel, chrome and molybdenum that give it the unique qualities of high strength, good wear characteristics, natural attractiveness, ease of maintenance and resistance to rust, corrosion and heat. Stainless steel is used, among other applications, in the automotive, aerospace and power generation industries, as well as

3

Table of Contents

in the manufacture of food handling, health and medical, chemical processing and pollution control equipment. The increased number of applications for stainless steel has resulted in the development of a greater variety of stainless steel metallurgical grades than carbon steel.

Tool Steel. Tool steels contain elements of manganese, silicon, chrome and molybdenum to produce specific hardness characteristics that enable tool steels to form, cut, shape and shear other materials in the manufacturing process. Heating and cooling at precise rates in the heat-treating process bring out these hardness characteristics. Tool steels are utilized in the manufacturing of metals, plastics, paper and aluminum extrusions, pharmaceuticals, electronics and optics.

High-Temperature Alloy Steel. These steels are designed to meet critical requirements of heat resistance and structural integrity. They generally have very high nickel content relative to other types of specialty steels. High-temperature alloy steels are manufactured for use generally in the aerospace industry.

High-Strength Low Alloy Steel. High-strength low alloy steel is a relative term that refers to those steels that maintain alloying elements that range in versatility. The alloy element of nickel, chrome and molybdenum in such steels typically exceeds the alloy element of carbon steels but not that of high-temperature alloy steel. High-strength low alloy steels are manufactured for use generally in the aerospace industry.

Net sales by principal product line were as follows:

| For the years ended December 31, |

2009 | 2008 | 2007 | ||||||

| (dollars in thousands) | |||||||||

| Stainless steel |

$ | 98,069 | $ | 172,222 | $ | 164,228 | |||

| Tool steel |

9,413 | 39,046 | 28,119 | ||||||

| High-strength low alloy steel |

9,235 | 11,936 | 25,892 | ||||||

| High-temperature alloy steel |

5,567 | 7,931 | 9,317 | ||||||

| Conversion service |

1,203 | 1,941 | 2,011 | ||||||

| Other |

1,420 | 2,030 | 369 | ||||||

| Total net sales |

$ | 124,907 | $ | 235,106 | $ | 229,936 | |||

RAW MATERIALS

The Company’s Bridgeville facility depends on the delivery of key raw materials for its day-to-day operations. These key raw materials are ferrous and non-ferrous scrap metal and alloys, primarily consisting of nickel, chrome, molybdenum and copper. Scrap metal is primarily generated by industrial sources and is purchased through a number of scrap brokers and dealers. Alloys are generally purchased from domestic agents and originate in Australia, Canada, China, Russia and South Africa. Political disruptions in countries such as these could cause supply interruptions and affect the availability and price of the raw materials purchased by the Company.

The Bridgeville facility supplies semi-finished specialty steel products as starting materials to the Company’s Titusville and Dunkirk facilities. Semi-finished specialty steel starting materials, not capable of being produced by the Company at a competitive cost, are purchased from other suppliers. The Company generally purchases these starting materials from steel strip coil suppliers, extruders, flat rolled producers and service centers. The Company believes that adequate supplies of starting material will continue to be available.

The cost of raw materials represents more than 50% of the Company’s total cost of products sold in 2009 and 2008. Raw material costs can be impacted by significant price changes. Raw material prices vary based on numerous factors, including quality, and are subject to frequent market fluctuations. Future raw material prices can not be predicted with any degree of certainty. Therefore, the Company does not maintain any long-term written agreements with any of its raw material suppliers.

4

Table of Contents

The Company has implemented a sales price surcharge mechanism on its products to help offset the impact of raw material price fluctuations. For substantially all stainless semi-finished products, the surcharge is calculated at the time of order entry, based on current raw material prices. For substantially all finished products and tool steel plate, the surcharge is calculated based on the monthly average raw material prices two months prior to the promised ship date. While the material surcharge mechanism is designed to offset modest fluctuations in raw material prices, it cannot immediately absorb significant spikes in raw material prices. A material change in raw material prices within a short period of time could have a material effect on the financial results of the Company, and there can be no assurance that the raw material surcharge mechanism will completely offset immediate changes in the Company’s raw material costs.

ENERGY AGREEMENTS

The production of specialty steel requires the ready availability of substantial amounts of electricity and natural gas for which the Company negotiates competitive agreements for the supply of electricity and natural gas. While the Company believes that its energy agreements allow it to compete effectively within the specialty steel industry, the potential of curtailments exists as a result of decreased supplies during periods of increased demand for electricity and natural gas. These interruptions not only can adversely affect the operating performance of the Company, but also can lead to increased costs. The Company has a sales price surcharge mechanism on its products to help offset the impact of natural gas price fluctuations.

CUSTOMERS

The Company’s customer base increased from 545 customers at December 31, 2008 to 568 customers at December 31, 2009. The Company’s five largest customers in the aggregate accounted for approximately 38% and 45% of sales for the years ended December 31, 2009 and 2008, respectively. Sales to Fry Steel Company accounted for 10.8%, 10.7% and 13.8% of the Company’s sales for the years ended December 31, 2009, 2008 and 2007, respectively, and 7%, 4% and 1% of total accounts receivable at December 31, 2009, 2008 and 2007, respectively. For 2008 and 2007, Carpenter Technology Corporation (“CRS”) accounted for 15.3% and 13.2%, respectively, of sales and 9% and 16%, respectively of accounts receivable. For 2007, Reliance Steel and Aluminum Co. accounted for 10.5% of sales and 4% of accounts receivable. No other customers accounted for more than 10% of the Company’s sales for those years. Sales outside of the United States approximated 10% of 2009 sales and 4% of both 2008 and 2007 sales. In 2009, sales to Mexico approximated 6% of sales.

BACKLOG

The Company primarily manufactures products to meet specific customer requirements. The Company’s backlog of orders on hand, considered to be firm, as of December 31, 2009 was approximately $36 million as compared to approximately $75 million at the same time in 2008. The decrease in the backlog is primarily due to reduced demand primarily caused by deteriorating economic and credit conditions which started to impact order entry levels during the fourth quarter of 2008. Customer orders are generally subject to cancellation with the payment of a penalty charge prior to delivery. Less than 10% of the December 31, 2009 backlog has promise dates beyond year 2010. The Company’s backlog may not be indicative of actual sales because certain surcharges are not determinable until the order is shipped to the customer and therefore should not be used as a direct measure of future revenue.

COMPETITION

Competition in the Company’s markets is based upon product quality, delivery capability, customer service and price. Maintaining high standards of product quality, while responding quickly to customer needs and keeping production costs at competitive levels, is essential to the Company’s ability to compete in its markets.

Annual domestic U.S. consumption of specialty steel products of the type manufactured by the Company approximates 600,000 tons. The Company chooses to restrict its participation in this market by limiting the volume of commodity stainless steel products it markets because of the highly competitive nature of the commodity business.

5

Table of Contents

The Company believes that ten companies that manufacture one or more similar specialty steel products are significant competitors. There are many smaller producing companies and material converters that are also considered to be competitors of the Company.

High import penetration of specialty steel products, especially stainless and tool steels, also impacts the competitive nature within the United States. Unfair pricing practices by foreign producers have resulted in high import penetration into the U.S. markets in which the Company participates. According to SSINA, import penetration for the years ended December 31, 2008 and 2007 was 53% and 54%, respectively, for stainless bar, and 49% and 48%, respectively, for stainless rod. Import penetration during the first ten months of 2009 for stainless bar and rod was 50% and 38%, respectively, according to SSINA.

The Continued Dumping and Subsidy Offset Act of 2000 (the “CDSOA”) provides for payment of import duties collected by the U.S. Treasury to domestic companies injured by unfair foreign trade practices. The assets purchased for the operations of Dunkirk Specialty Steel were previously owned and operated by AL Tech Specialty Steel, Inc. and Empire Specialty Steel, Inc. During their ownership, both organizations participated in several anti-dumping lawsuits with other domestic specialty steel producers. The Company has joined other domestic producers in the filing of trade actions against foreign producers.

In December 2009, the Company received an import duty net payment of $551,000, and, in December 2008, the Company received a net payment of $599,000. Benefits awarded from the CDSOA expired on September 30, 2007. Future benefits are dependent on the amount of undistributed import duties collected as of September 30, 2007 and the relationship of Dunkirk Specialty Steel’s claim in relation to claims filed by other domestic specialty steel producers.

EMPLOYEE RELATIONS

The Company considers the maintenance of good relations with its employees to be important to the successful conduct of its business. The Company has profit-sharing plans for certain salaried employees and for all of its employees represented by United Steelworkers (the “USW”) and has equity ownership programs for all of its eligible employees, in an effort to forge an alliance between its employees’ interests and those of the Company’s stockholders. At December 31, 2009, the Company had 244 employees at its Bridgeville facility, 28 employees at its Titusville facility and 142 employees at its Dunkirk facility, of which 190, 22 and 120 were USW members, respectively.

Collective Bargaining Agreements

The Company recognizes the USW as the exclusive representative for the Company’s hourly employees with respect to the terms and conditions of their employment. The Company has entered into the following collective bargaining agreements:

| Facility |

Commencement Date |

Expiration Date | ||

| Titusville |

October 2005 | September 2010 | ||

| Dunkirk |

November 2007 | October 2012 | ||

| Bridgeville |

September 2008 | August 2013 |

The Company believes a critical component of its collective bargaining agreements is the inclusion of a profit sharing plan. Under the plan, the hourly employees are entitled to receive 8.5% of their respective facilities’ annual pretax profits in excess of $1.0 million at Bridgeville and Dunkirk, and in excess of $500,000 at Titusville.

6

Table of Contents

Employee Benefit Plans

The Company provides group life and health insurance plans for its hourly and salaried employees. The Company also maintains a 401(k) retirement plan for its hourly and salaried employees. Pursuant to the 401(k) plan, participants may elect to make pre-tax and after-tax contributions, subject to certain limitations imposed under the Internal Revenue Code of 1986, as amended. In addition, the Company makes periodic contributions to the 401(k) plans based on service, except as described below.

The Company also participates in the Steelworkers Pension Trust (the “Trust”), a multi-employer defined-benefit pension plan that is open to all hourly and salaried employees associated with the Bridgeville facility. The Company makes periodic contributions to the Trust based on hours worked at a fixed rate for each hourly employee and a fixed monthly contribution on behalf of each salaried employee. The hourly employees may continue their contributions to the 401(k) retirement plan even if the Company contributions cease. The amount of the contribution for salaried employees will be dependent upon their contribution to the 401(k) retirement plan.

Employee Stock Purchase Plan

Under the 1996 Employee Stock Purchase Plan, as amended (the “Plan”), the Company is authorized to issue up to 150,000 shares of Common Stock to its full-time employees, nearly all of whom are eligible to participate. Under the terms of the Plan, employees can choose as of January 1 and July 1 of each year to have up to 10% of their total earnings withheld to purchase up to 100 shares of the Company’s Common Stock each six-month period. The purchase price of the stock is 85% of the lower of its beginning-of-the-period or end-of-the-period market prices. At December 31, 2009, the Company had issued 113,067 shares of Common Stock since the plan’s inception.

ENVIRONMENTAL

The Company is subject to federal, state and local environmental laws and regulations (collectively, “Environmental Laws”), including those governing discharges of pollutants into the air and water, and the generation, handling and disposal of hazardous and non-hazardous substances. The Company monitors its compliance with Environmental Laws applicable to it and, accordingly, believes that it is currently in compliance with all laws and regulations in all material respects. The Company is subject periodically to environmental compliance reviews by various regulatory offices. The Company may be liable for the remediation of contamination associated with generation, handling and disposal activities. Environmental costs could be incurred, which may be significant, related to environmental compliance, at any time or from time to time in the future.

EXECUTIVE OFFICERS

The following table sets forth, as of February 28, 2010, certain information with respect to the executive officers of the Company:

| NAME (AGE) |

EXECUTIVE OFFICER SINCE |

POSITION | ||

| Dennis M. Oates (57) |

2008 | President and Chief Executive Officer | ||

| William W. Beible, Jr. (58) |

2009 | Senior Vice President of Operations | ||

| Paul McGrath (58) |

1996 | Vice President of Administration, General Counsel and Secretary | ||

| Richard M. Ubinger (50) |

1994 | Vice President of Finance, Chief Financial Officer and Treasurer | ||

7

Table of Contents

Dennis M. Oates has been President and Chief Executive Officer of the Company since January 2008. Mr. Oates was named to the Company’s Board of Directors in October 2007. Mr. Oates previously served as Senior Vice President of the Specialty Alloys Operations of CRS from 2003 to July 2007. Mr. Oates also served as President and Chief Executive Officer of TW Metals, Inc. from 1998 to 2003. On February 22, 2010, the Company announced that its Board of Directors intends to elect Mr. Oates to the additional position of Chairman upon the May 2010 retirement of the current Chairman.

William W. Beible, Jr. has been Senior Vice President of Operations of the Company since February 2009. Mr. Beible was employed by CRS from 2006 to 2008 and served in several positions, including Vice President of Manufacturing—Specialty Alloys Operations. Mr. Beible also served as Vice President of Business Improvement and of Information Technology at P.H. Glatfelter Company, a global supplier of specialty papers and engineered products, from 2003 to 2005.

Paul A. McGrath has been Vice President of Administration of the Company since January 2007, General Counsel since 1995 and was appointed Secretary in 1996. Mr. McGrath served as Vice President of Operations from 2001 to December 2006. Previously, he was employed by Westinghouse Electric Corporation for approximately 24 years in various management positions.

Richard M. Ubinger has been Vice President of Finance of the Company since 2001, Chief Financial Officer and Principal Accounting Officer since 1994 and was appointed Treasurer in 1996. From 1981 to 1994, Mr. Ubinger was employed by Price Waterhouse LLP. Mr. Ubinger is a Certified Public Accountant.

PATENTS AND TRADEMARKS

The Company does not consider its business to be materially dependent on patent or trademark protection, and believes it owns or maintains effective licenses covering all the intellectual property used in its business. The Company seeks to protect its proprietary information by use of confidentiality and non-competition agreements with certain employees.

AVAILABLE INFORMATION

Copies of the Company’s Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, current reports on Form 8-K, and any amendments to those reports, as well as proxy and information statements that we file with the Securities and Exchange Commission (the “SEC”), are available free of charge on the Company’s website at www.univstainless.com as soon as reasonably practicable after such reports are filed with the SEC. The contents of our website are not part of this Form 10-K. You also may read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. You may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet site at www.sec.gov that contains reports, proxy and information statements and other information regarding issuers, like the Company, that file electronically with the SEC.

| ITEM 1A. | RISK FACTORS |

The Company’s business and results of operations are subject to a wide range of substantial business and economic factors including, but not limited to, the factors discussed below, many of which are not within the Company’s control. Other factors of which the Company is unaware or which the Company does not consider to be material at this time also may impact the Company’s business and results of operations. See the information under the heading “Forward-Looking Information Safe Harbor” in Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, of this Annual Report on Form 10-K.

8

Table of Contents

SIGNIFICANT CUSTOMERS AND CONCENTRATED CUSTOMER BASE

Net sales to the Company’s largest customer accounted for 10.8% of total 2009 sales and 10.7% of total 2008 sales. The accounts receivable balances from this customer comprised approximately 7% and 4% of total accounts receivable at December 31, 2009 and 2008, respectively. For 2008, a second customer accounted for 15.3% of net sales and 9% of accounts receivable. An adverse change in, or termination of, the Company’s relationship with one or more of its major customers or one or more of its market segments could have a material adverse effect upon the Company. See the information under the heading “Customers” in Item 1, Business, of this Annual Report on Form 10-K.

COMPETITION

The Company competes with domestic and foreign sources of specialty steel products. In addition, many of the finished products sold by the Company’s customers are in direct competition with finished products manufactured by foreign sources, which may affect the demand for those customers’ products. Any competitive factors that adversely affect the market for finished products manufactured by the Company or its customers could indirectly adversely affect the demand for the Company’s semi-finished products. Additionally, the Company’s products compete with products fashioned from alternative materials such as aluminum, composites and plastics, the production of which includes domestic and foreign enterprises. Competition in the Company’s field is intense and is expected to continue to be so in the foreseeable future. There can be no assurance that the Company will be able to compete successfully in the future. See the information under the heading “Competition” in Item 1, Business, of this Annual Report on Form 10-K.

AEROSPACE MARKET

Approximately 39% of the Company’s sales and 30% of tons shipped represent products sold to customers in the aerospace market in 2009. The aerospace market is historically cyclical due to both external and internal market factors. These factors include general economic conditions, diminished credit availability, airline profitability, demand for air travel, age of fleets, varying fuel and labor costs, price competition, and international and domestic political conditions such as military conflict and the threat of terrorism. The length and degree of cyclical fluctuation can be influenced by any one or a combination of these factors and therefore are difficult to predict with certainty. A downturn in the aerospace industry would adversely affect the demand for products and/or the prices at which the Company is able to sell its products, and its results of operations, business and financial condition could be materially adversely affected.

SUPPLY OF RAW MATERIALS AND COST OF RAW MATERIALS

The Company purchases scrap metal and alloy additives, principally nickel, chrome and molybdenum, for its melting operation. A substantial portion of the alloy additives is available only from foreign sources, some of which are located in countries that may be subject to unstable political and economic conditions. Those conditions might disrupt supplies or affect the prices of the raw materials used by the Company. The Company maintains sales price surcharges to help offset the impact of raw material price fluctuations.

The Company does not maintain long-term supply agreements with any of its raw material suppliers. If its supply of raw materials were interrupted, the Company might not be able to obtain sufficient quantities of raw materials, or obtain sufficient quantities of such materials at satisfactory prices, which, in either case, could adversely affect the Company’s results of operations. In addition, significant volatility in the price of the Company’s principal raw materials could adversely affect the Company’s financial results and there can be no assurance that the raw material surcharge mechanism employed by the Company will completely offset immediate changes in the Company’s raw material costs. See the information under the headings “Raw Materials” in Item 1, Business, and “Liquidity and Capital Resources” and “Future Outlook” in Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, of this Annual Report on Form 10-K.

9

Table of Contents

CURRENT GLOBAL ECONOMIC AND MARKET FACTORS

Our results of operations are affected directly by the level of business activity of our customers, which in turn is affected by global economic and market factors impacting the industries and markets that they serve. As has been widely reported, the financial markets and overall economies in the United States and abroad are currently undergoing a period of significant uncertainty and volatility. Economic slowdowns in certain markets or an extension of the current credit crisis to additional industries, particularly in the United States, may adversely impact overall demand for our products, which could have a negative effect on our revenues. Further, there can be no assurance that any governmental responses to recent disruptions in the financial markets ultimately will stabilize the markets or increase our customers’ liquidity or the availability of credit to our customers. The global financial crisis also may have an impact on our business and financial condition in ways that we currently cannot predict. As a result, there can be no assurance that global economic and market conditions will not adversely impact our results of operations, cash flow or financial position in the future.

RELIANCE ON ENERGY AGREEMENTS

The manufacturing of specialty steels is an energy-intensive industry. While the Company believes that its energy agreements allow it to compete effectively within the specialty steel industry, the Company is subjected to curtailments as a result of decreased supplies and increased demand for electricity and natural gas. These interruptions not only can adversely affect the operating performance of the Company, but also can lead to increased costs for energy. See the information under the heading “Energy Agreements” in Item 1, Business, of this Annual Report on Form 10-K.

LABOR MATTERS

The Company has 332 employees out of a total of 414 who are covered under collective bargaining agreements. The collective bargaining agreement for the Titusville hourly employees will expire in September 2010. There can be no assurance that the Company will succeed in timely concluding collective bargaining agreements with the USW to replace the ones that expire.

RELIANCE ON CRITICAL MANUFACTURING EQUIPMENT

The Company’s manufacturing processes are dependent upon certain critical pieces of specialty steel making equipment, such as the Company’s 50-ton electric-arc furnace and AOD (Argon Oxygen Decarburization) vessel, its ESR (Electro Slag Remelt) and VAR furnaces, and its universal rolling mill. In the event a critical piece of equipment should become inoperative as a result of unexpected equipment failure, there can be no assurance that the Company’s operations would not be substantially curtailed, which may have a negative effect on the Company’s financial results. See Item 2, Properties.

| ITEM 1B. | UNRESOLVED STAFF COMMENTS |

None.

| ITEM 2. | PROPERTIES |

The Company owns its Bridgeville facility, which consists of approximately 760,000 square feet of floor space and the Company’s executive offices on approximately 74 acres. The Bridgeville facility contains melting, remelting, conditioning, rolling, annealing and various other processing equipment. Substantially all products shipped from the Bridgeville facility are processed through its melt shop and universal rolling mill operations.

The Company owns its Titusville facility, which consists of seven buildings on approximately 10 acres, including two principal buildings of approximately 265,000 square feet in total area. The Titusville facility contains five VAR furnaces and various rolling and finishing equipment.

10

Table of Contents

The Company owns its Dunkirk facility, which consists of approximately 680,000 square feet of floor space on approximately 81 acres. The Dunkirk facility processes semi-finished billet and bar stock through one or more of its four rolling mills, a high temperature annealing facility and/or a round bar facility. The products are then finished and shipped as finished bar, rod and wire products.

Specialty steel production is a capital-intensive industry. The Company believes that its facilities and equipment are suitable for its present needs. The Company believes, however, that it will continue to require capital from time to time to add new equipment and to repair or replace existing equipment to remain competitive and to enable it to manufacture quality products and provide delivery and other support service assurances to its customers.

| ITEM 3. | LEGAL PROCEEDINGS |

From time to time, various lawsuits and claims have been or may be asserted against the Company relating to the conduct of its business, including routine litigation relating to commercial and employment matters. The ultimate cost and outcome of any litigation or claim cannot be predicted with certainty. Management believes, based on information presently available, that the likelihood that the ultimate outcome of any such pending matter will have a material adverse effect on its financial condition, or liquidity or a material impact to our results of operations is remote, although the resolution of one or more of these matters may have a material adverse effect on its results of operations for the period in which the resolution occurs.

| ITEM 4. | SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS |

No matters were submitted to a vote of security holders during the fourth quarter of 2009.

| ITEM 5. | MARKET FOR THE REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

At December 31, 2009, a total of 7,043,899 shares of the Company’s Common Stock, par value $.001 per share, were issued and held by approximately 164 holders of record. There were 270,795 shares of the issued Common Stock of the Company held in treasury at December 31, 2009.

Certain holders of Common Stock and the Company are party to a stockholder agreement. That agreement maintains in effect certain registration rights granted to non-management stockholders and provides to them two demand registration rights exercisable at any time upon written request for the registration of shares of Common Stock having an aggregate net offering price of at least $5.0 million.

PRICE RANGE OF COMMON STOCK

The Common Stock is listed on the NASDAQ Global Market under the symbol “USAP.” The following table sets forth the range of high and low sale prices per share of Common Stock, for the periods indicated below:

| 2009 | 2008 | |||||||||||

| High | Low | High | Low | |||||||||

| First quarter |

$ | 16.32 | $ | 7.98 | $ | 34.80 | $ | 24.05 | ||||

| Second quarter |

$ | 16.86 | $ | 9.48 | $ | 41.50 | $ | 30.00 | ||||

| Third quarter |

$ | 21.23 | $ | 14.68 | $ | 38.50 | $ | 25.55 | ||||

| Fourth quarter |

$ | 19.41 | $ | 14.48 | $ | 24.23 | $ | 8.85 | ||||

11

Table of Contents

EQUITY COMPENSATION PLAN INFORMATION

Securities authorized for issuance under equity compensation plans at December 31, 2009 are as follows:

| Plan Category |

Number of shares to be issued upon exercise of outstanding options |

Weighted-average exercise price of outstanding options |

Number of shares remaining available for future issuance under equity compensation plans A | ||||

| Equity compensation plans approved by security holders |

561,300 | $ | 20.04 | 176,101 | |||

| Equity compensation plans not approved by security holders |

— | — | — | ||||

| Total |

561,300 | $ | 20.04 | 176,101 | |||

| A | Includes 139,168 shares of Common Stock on stock options not issued under the Stock Incentive Plan and 36,933 available under the 1996 Employee Stock Purchase Plan, as amended. |

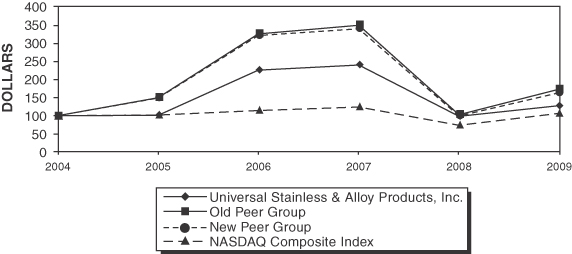

PERFORMANCE GRAPH

The performance graph below compares the cumulative total shareholder return on the Company’s stock with the cumulative total return on the equity securities of NASDAQ Composite Index and a peer group selected by the Company. The new peer group consists of domestic specialty steel producers: Allegheny Technologies, Inc. (“ATI”); Brush Engineered Materials Inc.; Carpenter Technology Corp.; Haynes International Inc.; and RTI International Metals, Inc. The old peer group consisted of only ATI and CRS. The graph assumes an investment of $100 on December 31, 2004 reinvestment of dividends, if any, on the date of dividend payment and the peer group is weighted by each company’s market capitalization. The performance graph represents past performance and should not be considered to be an indication of future performance.

Comparison of 5-Year Cumulative Total Shareholder Return among Universal Stainless & Alloy Products, Inc., the NASDAQ Composite Index an Old Peer Group and a New Peer Group

| Company/Peer/Market |

Fiscal Year Ending December 31, | |||||||||||||||||

| 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | |||||||||||||

| Universal Stainless & Alloy Products, Inc. |

$ | 100.00 | $ | 101.00 | $ | 225.42 | $ | 239.50 | $ | 97.56 | $ | 126.99 | ||||||

| Old Peer Group |

100.00 | 149.41 | 324.86 | 349.05 | 102.55 | 172.11 | ||||||||||||

| New Peer Group |

100.00 | 148.24 | 320.15 | 339.34 | 98.62 | 162.54 | ||||||||||||

| NASDAQ Composite Index |

100.00 | 101.41 | 114.05 | 123.94 | 73.43 | 105.89 | ||||||||||||

12

Table of Contents

PREFERRED STOCK

The Company’s Certificate of Incorporation provides that the Company may, by vote of its Board of Directors, issue up to 1,980,000 shares of Preferred Stock. The Preferred Stock may have rights, preferences, privileges and restrictions thereon, including dividend rights, dividend rates, conversion rights, voting rights, terms of redemption, redemption prices, liquidation preferences and the number of shares constituting any series or designation of such series, without further vote or action by the stockholders. The issuance of Preferred Stock may have the effect of delaying, deferring or preventing a change in control of the Company without further action by the stockholders and may adversely affect the voting and other rights of the holders of Common Stock. The issuance of Preferred Stock with voting and conversion rights may adversely affect the voting power of the holders of Common Stock, including the loss of voting control to others. The Company has no outstanding Preferred Stock and has no current plans to issue any of the authorized Preferred Stock.

DIVIDENDS

The Company has never paid a cash dividend on its Common Stock. The Company’s Credit Agreement with PNC Bank, National Association (“PNC Bank”) currently limits the payment of cash dividends payable on its Common Stock to 50% of the Company’s excess cash flow per fiscal year. Excess cash flow represents the amount of the Company’s earnings before interest, taxes, depreciation and amortization that is greater than the sum of the Company’s payments for interest, income taxes, the principal portion of long-term debt and capital lease obligations, and capital expenditures.

| ITEM 6. | SELECTED FINANCIAL DATA |

| For the years ended December 31, |

2009 | 2008 | 2007 | 2006 | 2005 | |||||||||||

| (dollars in thousands, except per share amounts) | ||||||||||||||||

| SUMMARY OF OPERATIONS |

||||||||||||||||

| Net sales |

$ | 124,907 | $ | 235,106 | $ | 229,936 | $ | 203,873 | $ | 170,022 | ||||||

| Operating income (loss) |

(4,657 | ) | 19,092 | 33,407 | 32,359 | 20,145 | ||||||||||

| Net income (loss) |

(2,958 | ) | 13,950 | 22,504 | 20,590 | 12,758 | ||||||||||

| FINANCIAL POSITION AT YEAR-END |

||||||||||||||||

| Cash and cash equivalents |

$ | 42,349 | $ | 14,812 | $ | 10,648 | $ | 2,909 | $ | 620 | ||||||

| Total assets |

181,714 | 182,944 | 164,296 | 155,287 | 129,239 | |||||||||||

| Long-term debt |

10,823 | 1,046 | 1,453 | 17,228 | 17,317 | |||||||||||

| Stockholders’ equity |

144,226 | 145,700 | 129,602 | 104,654 | 81,134 | |||||||||||

| COMMON SHARE DATA |

||||||||||||||||

| Basic earnings (loss) per share |

$ | (0.44 | ) | $ | 2.08 | $ | 3.39 | $ | 3.19 | $ | 2.00 | |||||

| Diluted earnings (loss) per share |

(0.44 | ) | 2.05 | 3.32 | 3.11 | 1.97 | ||||||||||

13

Table of Contents

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

RESULTS OF OPERATIONS

Universal Stainless & Alloy Products, Inc., headquartered in Bridgeville, Pa., manufactures and markets a broad line of semi-finished and finished specialty steels, including stainless steel, tool steel and certain other alloyed steels. The Company’s products are sold to rerollers, forgers, service centers, OEMs and wire redrawers.

The Company recorded a net loss of $3.0 million for the year ended December 31, 2009. These results include a $542,000 negative tax adjustment primarily for the reconciliation of tax balances to the 2008 tax returns and the following unusual charges (totaling $6.0 million pre-tax) recorded during the three-month period ended March 31, 2009, primarily due to the deepening recession and economic uncertainty:

| • | $1.9 million increase to the bad debt reserve due to the inability of a customer to pay amounts owed on 2008 business and a related $0.5 million increase to inventory reserves; |

| • | $1.5 million due to a decline in raw material values and the consumption of high cost material during the quarter; |

| • | $1.0 million write-down of stock inventory; |

| • | $0.9 million attributed to the reduction of operating levels; and |

| • | $0.2 million resulting from a 20% reduction in salaried employees. |

An analysis of the Company’s operations is as follows:

| For the years ended December 31, |

2009 | 2008 | 2007 | ||||||||||||||||

| Amount | % | Amount | % | Amount | % | ||||||||||||||

| (dollars in thousands; percentages are of total net sales) | |||||||||||||||||||

| NET SALES |

|||||||||||||||||||

| Stainless steel |

$ | 98,069 | 78.5 | % | $ | 172,222 | 73.2 | % | $ | 164,228 | 71.4 | % | |||||||

| Tool steel |

9,413 | 7.5 | 39,046 | 16.6 | 28,119 | 12.2 | |||||||||||||

| High-strength low alloy steel |

9,235 | 7.4 | 11,936 | 5.1 | 25,892 | 11.3 | |||||||||||||

| High-temperature alloy steel |

5,567 | 4.5 | 7,931 | 3.4 | 9,317 | 4.0 | |||||||||||||

| Conversion services |

1,203 | 1.0 | 1,941 | 0.8 | 2,011 | 0.9 | |||||||||||||

| Other |

1,420 | 1.1 | 2,030 | 0.9 | 369 | 0.2 | |||||||||||||

| Total net sales |

124,907 | 100.0 | 235,106 | 100.0 | 229,936 | 100.0 | |||||||||||||

| Total cost of products sold |

117,901 | 94.4 | 204,929 | 87.2 | 184,491 | 80.3 | |||||||||||||

| Selling and administrative expenses |

11,663 | 9.3 | 11,085 | 4.7 | 12,038 | 5.2 | |||||||||||||

| Operating income (loss) |

$ | (4,657 | ) | (3.7 | )% | $ | 19,092 | 8.1 | % | $ | 33,407 | 14.5 | % | ||||||

Net sales by market segment are as follows:

| For the years ended December 31, |

2009 | 2008 | 2007 | |||||||||||||||

| Amount | % | Amount | % | Amount | % | |||||||||||||

| (dollars in thousands; percentages are of total net sales) | ||||||||||||||||||

| Service centers |

$ | 50,355 | 40.3 | % | $ | 110,889 | 47.2 | % | $ | 119,736 | 52.1 | % | ||||||

| Forgers |

39,821 | 31.9 | 52,551 | 22.4 | 47,711 | 20.7 | ||||||||||||

| Original equipment manufacturers |

16,089 | 12.9 | 18,955 | 8.1 | 18,287 | 8.0 | ||||||||||||

| Rerollers |

12,174 | 9.7 | 41,660 | 17.7 | 35,006 | 15.2 | ||||||||||||

| Wire redrawers |

3,845 | 3.1 | 7,129 | 3.0 | 6,843 | 3.0 | ||||||||||||

| Conversion services |

1,203 | 1.0 | 1,941 | 0.8 | 2,011 | 0.9 | ||||||||||||

| Miscellaneous |

1,420 | 1.1 | 1,981 | 0.8 | 342 | 0.1 | ||||||||||||

| Net sales |

$ | 124,907 | 100.0 | % | $ | 235,106 | 100.0 | % | $ | 229,936 | 100.0 | % | ||||||

| Tons shipped |

28,182 | 45,679 | 43,644 | |||||||||||||||

14

Table of Contents

2009 Results as Compared to 2008: The decrease in net sales in 2009 is primarily due to a 38% decline in tonnage shipped and lower raw material surcharges, partially offset by base price increases realized in 2009. Shipments of service center plate products, petrochemical products, aerospace products and power generation products decreased 64%, 40%, 32% and 16%, respectively, compared to 2008. The lower demand for the Company’s products was primarily a result of an oversupply of product within the service center industry resulting from deteriorating economic and credit conditions which started to impact order entry levels during the fourth quarter of 2008. The assessment of lower surcharges is primarily due to a decline in the average cost of nickel, chrome, molybdenum and carbon scrap in 2009 in comparison to 2008.

Cost of products sold, as a percentage of net sales, increased in 2009 as compared to 2008. Cost of products sold for 2009 include $3.9 million of the unusual charges outlined above, representing 3.1% of net sales. The remaining increase is primarily due to higher operation costs resulting from lower production volumes.

Selling and administrative expenses increased in 2009 to $11.7 million, or 9.3% of net sales from $11.1 million, or 4.7% of net sales in 2008. The increased cost in 2009 relates to $2.1 million of the unusual charges outlined above. These costs were partially offset by an $867,000 decrease in labor costs, primarily resulting from a 20% workforce reduction implemented in March 2009 and a reduction in the accrual for incentive compensation. In addition, other discretionary expenditures were curtailed as a result of lower production volumes.

Interest expense and other financing costs decreased from $105,000 in 2008 to $89,000 in 2009. The decrease is primarily due to recognizing lower interest expense associated with the funding of scheduled payments on existing term debt of the Company. In February 2009, the Company entered into a new unsecured credit agreement with PNC Bank which provides for a $12.0 million term loan to assist in the funding of a major capital expenditure project at the Company’s melt shop. Interest charges of $454,000 were capitalized as part of the project costs in 2009. $7.0 million of the project costs have been allocated to assets placed in service as of December 31, 2009 and future interest charges related to those assets will be expensed in 2010.

Other income, net decreased from $911,000 in 2008 to $695,000 in 2009. This decrease is primarily attributed to a $213,000 reduction in interest income earned from excess cash invested during 2009 due to lower interest rates. In addition, the Company received funds under the CDSOA of $551,000 and $599,000 in 2009 and 2008, respectively.

The effective income tax rates for the years ended December 31, 2009 and 2008 were 27.0% and 29.9%, respectively. The change in the effective rate is primarily due to a $742,000 negative tax adjustment primarily for the reconciliation of tax balances at June 30, 2009 to the tax returns. Approximately $200,000 of this adjustment is the cumulative adjustment related to the reduction of the estimated annual effective income tax rate utilized in the three-month period ended March 31, 2009 from 40.3% to 37.2% at June 30, 2009. In addition, the Company has determined that $370,000 of this adjustment relates to prior periods and is not considered material to any prior period or the current year to require the restatement of prior period financial statements. The effective income tax rate in the current period reflects a projected net operating loss and benefits related to federal and state loss carry backs and carry forwards, whereas the prior year had taxable income and benefited from the domestic manufacturing deduction and investment tax credits generated from capital improvements made at the Dunkirk facility in 2008.

15

Table of Contents

2008 Results as Compared to 2007: The increase in net sales in 2008 is primarily due to a 5% increase in tonnage shipped, partially offset by product mix changes and lower raw material surcharges. Shipments of tool steel plate products, petrochemical products and power generation products increased 22%, 15% and 16%, respectively, compared to 2007. These increases were mostly offset by a 17% decrease in aerospace product shipments. The reduced demand for aerospace products was partially due to the Boeing work stoppage during 2008 and by conservative service center purchasing practices in anticipation of lower surcharges due to falling commodity prices. The assessment of lower surcharges is primarily due to a decline in the average cost of nickel from $16.89 in 2007 to $9.58 in 2008 partially offset by increase costs of chrome and carbon scrap. In addition, miscellaneous sales benefited from the $1.1 million sale of excess scrap in June 2008.

Cost of products sold, as a percentage of net sales, increased in 2008 as compared to 2007. This increase is primarily due to the shift in sales from service centers to forgers and rerollers, timing of raw material purchases and the assessment of the related surcharges, and operation cost increases. A significant portion of the raw material timing issue occurred during the 2008 fourth quarter. From September 2008 to December 2008, the average cost of nickel and chrome declined 46%, while molybdenum declined 70% and carbon scrap declined 56%. These declines resulted in the Company increasing its inventory reserves by $1.0 million in 2008. Operation costs were negatively impacted by a $1.6 million increase in natural gas costs, resulting from rate increases of approximately 25% at the Bridgeville facility, and a $2.8 million increase in labor costs. In addition, the Company expensed $834,000 related to the relocation of the Company’s round bar finishing line from Bridgeville to Dunkirk in 2008.

Selling and administrative expenses decreased from $12.0 million, or 5.2% of net sales to $11.1 million, or 4.7% of net sales, primarily due to the 2007 settlement of a lawsuit between the Company and Teledyne Technologies Incorporated (“Teledyne”). Management continuously monitors its selling and administrative expenses in relation to net sales.

Interest expense and other financing costs decreased from $731,000 in 2007 to $105,000 in 2008. The decrease is primarily due to the December 2007 retirement of the $7.5 million outstanding balance on the Company’s term loan with PNC Bank.

Other income, net increased to $911,000 in 2008 from $776,000 in 2007. This increase is primarily attributed to additional interest income of $91,000 earned from excess cash invested during 2008. In addition, the Company received funds under the CDSOA of $599,000 and $586,000 in 2008 and 2007, respectively.

The effective income tax rates for the years ended December 31, 2008 and 2007 were 29.9% and 32.7%, respectively. The change in the effective income tax rate is primarily due to the impact of the lower income level on the Company’s permanent tax deductions and favorable adjustments to state income provisions.

Business Segment Results

The Company is comprised of three operating locations and one corporate headquarters. For segment reporting, the Bridgeville and Titusville facilities have been aggregated into one reportable segment, Universal Stainless & Alloy Products, because of the management reporting structure in place. The Universal Stainless & Alloy Products manufacturing process involves melting, remelting, treating and hot and cold rolling of semi-finished and finished specialty steels. Dunkirk Specialty Steel’s manufacturing process involves hot rolling and finishing specialty steel bar, rod and wire products.

16

Table of Contents

UNIVERSAL STAINLESS & ALLOY PRODUCTS SEGMENT

An analysis of the segment’s operations is as follows:

| For the years ended December 31, |

2009 | 2008 | 2007 | ||||||||||||||||

| Amount | % | Amount | % | Amount | % | ||||||||||||||

| (dollars in thousands; percentages are of total net sales) | |||||||||||||||||||

| NET SALES |

|||||||||||||||||||

| Stainless steel |

$ | 71,670 | 66.2 | % | $ | 121,612 | 58.9 | % | $ | 108,535 | 53.6 | % | |||||||

| Tool steel |

9,146 | 8.4 | 37,631 | 18.2 | 25,638 | 12.7 | |||||||||||||

| High-strength low alloy steel |

3,017 | 2.8 | 3,881 | 1.9 | 12,764 | 6.3 | |||||||||||||

| High-temperature alloy steel |

1,988 | 1.8 | 2,977 | 1.4 | 4,067 | 2.0 | |||||||||||||

| Conversion service |

763 | 0.7 | 1,278 | 0.6 | 1,405 | 0.7 | |||||||||||||

| Other |

1,391 | 1.3 | 1,875 | 0.9 | 295 | 0.1 | |||||||||||||

| 87,975 | 81.2 | 169,254 | 81.9 | 152,704 | 75.4 | ||||||||||||||

| Intersegment |

20,344 | 18.8 | 37,384 | 18.1 | 49,858 | 24.6 | |||||||||||||

| Total net sales |

108,319 | 100.0 | 206,638 | 100.0 | 202,562 | 100.0 | |||||||||||||

| Material cost of sales |

49,592 | 45.8 | 114,930 | 55.6 | 106,456 | 52.6 | |||||||||||||

| Operation cost of sales |

52,656 | 48.6 | 68,415 | 33.1 | 67,286 | 33.2 | |||||||||||||

| Selling and administrative expenses |

8,467 | 7.8 | 7,613 | 3.7 | 8,345 | 4.1 | |||||||||||||

| Operating income (loss) |

$ | (2,396 | ) | (2.2 | )% | $ | 15,680 | 7.6 | % | $ | 20,475 | 10.1 | % | ||||||

Net sales for the year ended December 31, 2009 decreased by $98.3 million, or 47.6%, in comparison to the year ended December 31, 2008 primarily due to a 37% decline in tonnage shipped and lower raw material surcharges, partially offset by base price increases realized in 2009. Shipments of service center plate products, petrochemical products, aerospace products and power generation products decreased 64%, 43%, 29% and 14%, respectively, over 2008. Operating income for the year ended December 31, 2009 decreased by $18.1 million primarily due to the impact of the unusual charges and lower production volumes. The 2009 results include $5.0 million of the unusual charges outlined above, representing 4.6% of net sales. Excluding the impact of the unusual charges, material costs, as a percentage of sales, dropped from 55.6% to 43.7% reflecting a better alignment of material costs and related surcharges assessed and yield improvements recognized on 2009 shipments of semi-finished products.

Net sales for the year ended December 31, 2008 increased $4.1 million, or 2%, in comparison to the year ended December 31, 2007 primarily due to a 2% increase in tonnage shipped and by product mix changes, partially offset by lower raw material surcharges discussed above. Shipments of tool steel plate products, petrochemical products and power generation products increased 20%, 17% and 15%, respectively, over 2007. These increases were mostly offset by a 20% decrease in aerospace product shipments. In addition, other sales benefited from the $1.1 million sale of excess scrap in 2008. Operating income for the year ended December 31, 2008 decreased $4.8 million, primarily due the decline in aerospace sales, and the timing of raw material purchases that resulted in the material cost of sales increasing from 52.6% to 55.6%.

17

Table of Contents

DUNKIRK SPECIALTY STEEL SEGMENT

An analysis of the segment’s operations is as follows:

| For the years ended December 31, |

2009 | 2008 | 2007 | ||||||||||||||||

| Amount | % | Amount | % | Amount | % | ||||||||||||||

| (dollars in thousands; percentages are of total net sales) | |||||||||||||||||||

| NET SALES |

|||||||||||||||||||

| Stainless steel |

$ | 26,399 | 68.4 | % | $ | 50,610 | 72.8 | % | $ | 55,693 | 68.2 | % | |||||||

| High-strength low alloy steel |

6,218 | 16.1 | 8,055 | 11.6 | 13,128 | 16.1 | |||||||||||||

| High-temperature alloy steel |

3,579 | 9.3 | 4,954 | 7.1 | 5,250 | 6.4 | |||||||||||||

| Tool steel |

267 | 0.7 | 1,415 | 2.0 | 2,481 | 3.0 | |||||||||||||

| Conversion services |

440 | 1.1 | 663 | 1.0 | 606 | 0.7 | |||||||||||||

| Other |

29 | 0.1 | 155 | 0.2 | 74 | 0.1 | |||||||||||||

| 36,932 | 95.7 | 65,852 | 94.7 | 77,232 | 94.5 | ||||||||||||||

| Intersegment |

1,659 | 4.3 | 3,712 | 5.3 | 4,493 | 5.5 | |||||||||||||

| Total net sales |

38,591 | 100.0 | 69,564 | 100.0 | 81,725 | 100.0 | |||||||||||||

| Material cost of sales |

24,567 | 63.7 | 44,215 | 63.6 | 47,905 | 58.6 | |||||||||||||

| Operation cost of sales |

13,089 | 33.9 | 18,465 | 26.5 | 17,404 | 21.3 | |||||||||||||

| Selling and administrative expense |

3,196 | 8.3 | 3,472 | 5.0 | 3,693 | 4.5 | |||||||||||||

| Operating income (loss) |

$ | (2,261 | ) | (5.9 | )% | $ | 3,412 | 4.9 | % | $ | 12,723 | 15.6 | % | ||||||

Net sales for the year ended December 31, 2009 decreased by $31.0 million, or 44.5%, in comparison to the year ended December 31, 2008 primarily due to a 26% decline in tonnage shipped and lower raw material surcharges, partially offset by base price increases realized in 2009. Shipments of general industrial products, petrochemical products and aerospace products decreased 34%, 31% and 19%, respectively, over 2008. Operating income for the year ended December 31, 2009 decreased by $5.7 million primarily due to the impact of the unusual charges and lower production volumes. The 2009 results include $1.0 million of the unusual charges outlined above, representing 2.5% of net sales.

Net sales for the year ended December 31, 2008 decreased $12.2 million, or 15%, in comparison to the year ended December 31, 2007 primarily due to a 10% decrease in shipments as well as the impact of lower raw material surcharges. Shipments of aerospace products and commodity grade products decreased 23% and 24%, respectively, which were partially offset by a 33% increase in petrochemical products. Operating income for the year ended December 31, 2008 decreased $9.3 million primarily due to the decline in aerospace sales and the timing of raw material purchases that resulted in the material cost of sales increasing from 58.6% to 63.6% and higher operation costs due to $834,000 of costs related to relocation of the round bar finishing line from Bridgeville to Dunkirk.

18

Table of Contents

Liquidity and Capital Resources

The Company generated cash from operations of $27.7 million, $17.7 million and $33.6 million in the years ended December 31, 2009, 2008 and 2007, respectively. Cash received from sales of $139.5 million, $228.7 million and $235.9 million for the years ended December 31, 2009, 2008 and 2007, respectively, represent the primary source of cash from operations. An analysis of the primary uses of cash is as follows:

| For the years ended December 31, |

2009 | 2008 | 2007 | |||||||||||||||

| Amount | % | Amount | % | Amount | % | |||||||||||||

| (dollars in thousands; percentages are of total uses of cash) | ||||||||||||||||||

| Raw material purchases |

$ | 40,699 | 36.4 | % | $ | 111,212 | 52.7 | % | $ | 100,504 | 49.7 | % | ||||||

| Employment costs |

28,899 | 25.9 | 38,380 | 18.2 | 36,103 | 17.8 | ||||||||||||

| Utilities |

14,891 | 13.3 | 19,915 | 9.4 | 18,657 | 9.2 | ||||||||||||

| Other |

27,275 | 24.4 | 41,547 | 19.7 | 47,057 | 23.3 | ||||||||||||

| Total uses of cash |

$ | 111,764 | 100.0 | % | $ | 211,054 | 100.0 | % | $ | 202,321 | 100.0 | % | ||||||

Cash used for raw material purchases decreased in 2009 in comparison to 2008 and 2007 primarily due to decreased production and lower transaction prices. The Company continuously monitors market price fluctuations of its key raw materials.

The following table reflects the average market values per pound for key raw materials for selected months during the last three-year period.

| December 2009 |

June 2009 |

December 2008 |

June 2008 |

December 2007 |

June 2007 | |||||||||||||

| Nickel |

$ | 7.74 | $ | 6.79 | $ | 4.39 | $ | 10.23 | $ | 11.79 | $ | 18.92 | ||||||

| Chrome |

$ | 0.89 | $ | 0.78 | $ | 0.96 | $ | 2.19 | $ | 1.66 | $ | 1.27 | ||||||

| Molybdenum |

$ | 11.47 | $ | 10.34 | $ | 9.85 | $ | 33.22 | $ | 32.54 | $ | 32.65 | ||||||

| Carbon Scrap |

$ | 0.15 | $ | 0.10 | $ | 0.11 | $ | 0.34 | $ | 0.14 | $ | 0.13 | ||||||

The monthly average price of nickel increased from $15.68 in December 2006 to a high of $23.67 in May 2007. The significant rise was believed to be due to increased demand from foreign (primarily Chinese) and domestic sources coupled with supply volatility. The sharp increase had a material negative impact on the operating margins of the Universal Stainless & Alloy Product Segment and a material positive impact on the operating margins of the Dunkirk Specialty Steel Segment. The monthly average nickel prices declined from its record level in May 2007 to $12.54 in August 2007 and to $11.79 in December 2007. The sharp decline resulted from decreased demand for nickel while supplies continued to increase during the second half of 2007. The sharp decline also had a material negative impact on the operating margins of both business segments through the recognition of increased inventory reserves. Inventory reserves increased from 2.3% of the consolidated inventory balance at December 31, 2006 to 3.3% at December 31, 2007.

During the first nine months of 2008, the monthly average prices of nickel and molybdenum remained stable while chrome and carbon scrap experienced significant increases. From September 2008 to December 2008, the average cost of nickel and chrome declined 46%, while molybdenum declined 70% and carbon scrap declined 56%. The sharp decline also had a material negative impact on the operating margins of both business segments through the recognition of increased inventory reserves. In 2009, material prices increased modestly throughout the year. Inventory reserves increased from 3.3% of the consolidated inventory balance at December 31, 2007 to 5.1% at December 31, 2008 and then decreased to 2.8% at December 31, 2009. While the material surcharge mechanism is designed to offset modest fluctuations in raw material prices, it cannot immediately absorb significant spikes in raw material prices. There can be no assurance that the raw material surcharge mechanism will completely offset immediate changes in the Company’s raw material costs. A material decline in raw material prices within a short period of time could have a material adverse effect on the financial results of the Company.

19

Table of Contents

Decreases in both employment and utility costs are primarily due to lower production volumes. In addition, lower payouts under the Company’s profit-sharing plans were partially offset by higher wage and benefit rates. The decrease in utility costs also resulted from a 56% decrease in average monthly natural gas settlement prices, which largely benefited the Bridgeville facility.

Other uses of cash decreased between 2007 and 2009. 2007 included payments made to settle the Teledyne lawsuit and an EPA violation. Maintenance expenses in 2009 decreased by $3.7 million in comparison to 2008 and 2007. In addition, payments for federal and state income taxes, net of refunds received, decreased from $11.3 million in 2007 to $6.4 million in 2007 to a net refund of $1.4 million in 2008.

At December 31, 2009, working capital approximated $97.6 million, as compared to $94.8 million at December 31, 2008. The increase is attributable to a $27.5 million increase in cash, and decreases in managed working capital, comprised of accounts receivable, inventory and accounts payable, of $26.3 million and a $2.6 million reduction in accrued employment costs. The managed working capital days sales outstanding increased to 146 days at December 31, 2009 from 118 days at December 31, 2008.

Capital Expenditures and Investments. The Company’s capital expenditures were approximately $12.4 million and $12.9 million in 2009 and 2008, respectively. The 2009 expenditures were primarily made in connection with the Bridgeville melt shop project and the addition of annealing and finishing equipment.

In January 2009, the Company announced that it would invest $13 million in its Bridgeville melt shop. The investment includes major upgrades in equipment, automation and plant layout designed to: cut production cycle times and customer lead times; improve on-time delivery performance; increase material yields; reduce operating costs and enhance working capital management. The equipment and infrastructure spending is substantially complete, and the automation investment will be completed in the second-half of 2010. Once fully implemented and when the normal economic cycle resumes, the investment is expected to yield cost savings of more than $7.5 million per year. The Company expects to fund substantially all of the investment with the Term Loan.

Capital expenditures are expected to approximate $12.0 million in 2010, of which $3.0 million is specifically for the Bridgeville melt shop.

Capital Resources Including Off-Balance Sheet Arrangements. The Company does not maintain off-balance sheet arrangements nor does it participate in non-exchange traded contracts requiring fair value accounting treatment or material related-party transaction arrangements.

PNC Credit Agreement. The Company entered into a new unsecured credit agreement with PNC Bank (the “PNC Credit Agreement”), which provided a $12.0 million term loan scheduled to mature on February 28, 2014 (“Term Loan”) and a $15.0 million revolving credit facility with a term expiring on June 30, 2012 (the “PNC Line”). The Company also executed an interest rate swap to convert the LIBOR floating rate Term Loan to a fixed interest rate for the life of the loan. At December 31, 2009, the Company had its $15.0 million revolving line of credit with PNC Bank available for borrowings.

The Company pays a commitment fee on the unused portion of the PNC Line of 0.25%, provided it maintains certain financial ratios. Interest on borrowings under the PNC Line is based on short-term market rates, which may be further adjusted, based upon the Company maintaining certain financial ratios. The Company is required to be in compliance with three financial covenants: a minimum leverage ratio of 2.5:1.0 or less; a minimum debt service ratio of 2.5:1.0 or greater; and a minimum tangible net worth of $135.6 million as of December 31, 2009. In May 2009, PNC Bank agreed to exclude $3.0 million of the unusual charges described above from the 2009 covenant calculations. The Company was in compliance with all financial ratios and restrictive covenants it is required to maintain under the credit agreement at December 31, 2009. The Company believes it will maintain compliance with the financial covenants in effect throughout 2010.

20

Table of Contents

Government Financing Programs. The Company maintains two loan agreements with the Commonwealth of Pennsylvania’s Department of Commerce, originally aggregating $600,000. A $200,000 15-year loan bears interest at 5% per annum with the term ending in 2011, and a $400,000 20-year loan bears interest at 6% per annum with the term ending in 2016. In 2002, Dunkirk Specialty Steel issued two ten-year, 5% interest-bearing notes payable to the New York Job Development Authority for the combined amount of $3.0 million. As of December 31, 2009, the total principal balance of all government-financed debt instruments is $1.0 million.

Share-based Financing Activity. The Company issued 40,820 and 72,785 shares of its Common Stock for the years ended December 31, 2009 and 2008, respectively, through its two share-based compensation plans. In 2009, 32,000 stock options issued under the Stock Incentive Plan were exercised for $253,000 plus related tax benefits of $86,000. In 2008, 64,850 stock options were issued for $625,000 plus related tax benefits of $529,000. The remaining shares were issued to participants of the Employee Stock Purchase Plan.

In October 1998, the Company initiated a stock repurchase program to repurchase up to 315,000 shares of its outstanding Common Stock in open market transactions at market prices. The Company repurchased no shares in 2009 or 2008 and 326 shares in 2007. The Company is authorized to repurchase 44,205 remaining shares of Common Stock under this program as of December 31, 2009.

Short- and Long-Term Liquidity. The Company expects to meet substantially all of its short-term liquidity requirements resulting from operations and current capital investment plans with internally generated funds and borrowings under the PNC Credit Agreement. At December 31, 2009, the Company had $42.3 million in cash and $15.0 million available under the PNC Line. In addition, the ratio of current assets to current liabilities at December 31, 2009 was 8.8:1 compared with 4.9:1 at December 31, 2008, and the debt to total capitalization ratio was 8.3% compared with 1.0%, respectively.

The Company’s long-term liquidity depends upon its ability to obtain additional orders from its existing customers, attract new customers and control costs. Additional sources of financing may be required to fund growth initiatives identified by the Company.

Contractual Obligations. At December 31, 2009, the Company had the following contractual principal and interest obligations:

| (dollars in thousands) | Total | Payments Due by Period | |||||||||||||

| Less than 1 Year |

1–3 Years |

3–5 Years |

More than 5 Years | ||||||||||||

| Long-term debt |

$ | 14,694 | $ | 2,797 | $ | 7,041 | $ | 4,816 | $ | 40 | |||||

| Operating lease obligations |

99 | 31 | 55 | 13 | — | ||||||||||

| Purchase obligations |

4,198 | 4,198 | — | — | — | ||||||||||

| Total contractual obligations |

$ | 18,991 | $ | 7,026 | $ | 7,096 | $ | 4,829 | $ | 40 | |||||

Long-term debt does not include any outstanding balance on the PNC Line, currently due to expire on June 30, 2012, since there was no outstanding balance on December 31, 2009. Purchase obligations include the value of all open purchase orders with established quantities and purchase prices as well as minimum purchase commitments.

21

Table of Contents

Import Protections. The CDSOA provides for payment of import duties collected by the U.S. Treasury Department to domestic companies injured by unfair foreign trade practices. The assets purchased by Dunkirk Specialty Steel were previously owned and operated by AL Tech Specialty Steel, Inc. and Empire Specialty Steel, Inc. During their ownership, both organizations participated in several anti-dumping lawsuits with other domestic specialty steel producers. In accordance with the CDSOA, which expired September 30, 2007, the Company filed claims to receive their appropriate share of the import duties collected and received a net payment of $551,000 in 2009. Future benefits are dependent on the amount of undistributed import duties collected as of September 30, 2007 and the relationship of Dunkirk Specialty Steel’s claim in relation to claims filed by other domestic specialty steel producers. The Company expects minimal distributions in the future.

EFFECTS OF INFLATION

Despite modest inflation in recent years, rising costs, in particular increasing wage and benefit rates, continue to affect operations. The Company strives to mitigate the effects of inflation through cost containment, productivity improvements and sales price increases.

CONTINGENT ITEMS

Product Claims. The Company is subject to various claims and legal actions that arise in the normal course of conducting business. At December 31, 2009, the Company had established a reserve of $154,000 for potential commercial product-claims.

Environmental Matters. The Company, as well as other steel companies, is subject to demanding environmental standards imposed by federal, state and local environmental laws and regulations. The Company is not aware of any environmental condition that currently exists at any of its facilities that are probable or reasonably possible of having a material impact on the Company’s results of operations or liquidity.

The Company is aware of energy usage concerns relating to climate change, however, the Company is not aware of any pending regulations that are expected to have a material impact on the Company’s results of operations or liquidity.

Legal Matters. From time to time, various lawsuits and claims have been or may be asserted against the Company relating to the conduct of our business, including routine litigation relating to commercial and employment matters. The ultimate cost and outcome of any litigation or claim cannot be predicted with certainty. Management believes, based on information presently available, that the likelihood that the ultimate outcome of any such pending matter will have a material adverse effect on its financial condition, or liquidity or a material impact to our results of operations is remote, although the resolution of one or more of these matters may have a material adverse effect on its results of operations for the period in which the resolution occurs.

CRITICAL ACCOUNTING POLICIES AND NEW ACCOUNTING PRONOUNCEMENTS

Critical Accounting Policies. Revenue recognition is the most critical accounting policy of the Company. Revenue from the sale of products is recognized when both risk of loss and title have transferred to the customer, which in most cases coincides with shipment of the related products, and collection is reasonably assured. The Company manufactures specialty steel product to customer purchase order specifications and in recognition of requirements for product acceptance. Material certification forms are executed, indicating compliance with the customer purchase orders, before the specialty steel products are packed and shipped to the customer.

Revenue from conversion services is recognized when the performance of the service is complete. Invoiced shipping and handling costs are also accounted for as revenue. Customer claims, which are not material, are accounted for primarily as a reduction to gross sales after the matter has been researched and an acceptable resolution has been reached.

22

Table of Contents

In addition, management constantly monitors the ability to collect its unpaid sales invoices and the valuation of its inventory. The allowance for doubtful accounts includes specific reserves for the value of outstanding invoices issued to customers currently operating under the protection of the federal bankruptcy law and other amounts that are deemed potentially not collectible with a reserve equal to 15% of 90-day or older balances. However, the total allowance will not be less than 1% of total accounts receivable.