Attached files

QuickLinks -- Click here to rapidly navigate through this document

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

ý |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2009 |

|

or |

|

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Transition period from to |

|

Commission File Number: 000-26091

TC PipeLines, LP

(Exact name of registrant as specified in its charter)

| Delaware State or other jurisdiction of incorporation or organization |

52-2135448 (I.R.S. Employer Identification No.) |

|

717 Texas Street, Suite 2400 Houston, Texas (Address of principal executive offices) |

77002-2761 (Zip code) |

|

877-290-2772 (Registrant's telephone number, including area code) |

||

Securities registered pursuant to Section 12(b) of the Act: |

||

Common units representing limited partner interests |

NASDAQ Stock Market |

|

| Title of each class | Name of each exchange on which registered | |

Securities registered pursuant to Section 12(g) of the Act: None |

||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer", "accelerated filer" and "small reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ý | Accelerated filer o | Non-accelerated filer o (Do not check if a small reporting company) |

Smaller Reporting Company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No ý

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant as at June 30, 2009 was approximately $839.8 million.

As of February 26, 2010, there were 46,227,766 common units of the registrant outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None

TC PIPELINES, LP

| Page No. | ||||

| PART I | ||||

| Item 1. | Business | 9 | ||

| Item 1A. | Risk Factors | 32 | ||

| Item 1B. | Unresolved Staff Comments | 46 | ||

| Item 2. | Properties | 46 | ||

| Item 3. | Legal Proceedings | 46 | ||

| Item 4. | Submission of Matters to a Vote of Security Holders | 47 | ||

PART II |

||||

| Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 48 | ||

| Item 6. | Selected Financial Data | 49 | ||

| Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 49 | ||

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 73 | ||

| Item 8. | Financial Statements and Supplementary Data | 75 | ||

| Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | 75 | ||

| Item 9A. | Controls and Procedures | 75 | ||

| Item 9B. | Other Information | 76 | ||

PART III |

||||

| Item 10. | Directors, Executive Officers and Corporate Governance | 77 | ||

| Item 11. | Executive Compensation | 80 | ||

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

83 | ||

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | 84 | ||

| Item 14. | Principal Accounting Fees and Services | 89 | ||

PART IV |

||||

| Item 15. | Exhibits, Financial Statement Schedules | 91 | ||

All amounts are stated in United States dollars unless otherwise indicated.

2009 ANNUAL REPORT 5

Glossary

The abbreviations, acronyms, and industry terminology used in this annual report are defined as follows:

| 2007 Credit Agreement | Northern Border's $250.0 million amended and restated revolving credit agreement | |

| Acquisition Agreement | Agreement for Purchase and Sale of Membership Interest | |

| Alberta Hub | The grouping of gas gathering lines, processing, storage facilities in large scale and also a "liquid" pricing point recognized for trading in Alberta, Canada | |

| ASC | Accounting Standards Codification | |

| ANR | ANR Pipeline Company | |

| Bcf | Billion cubic feet | |

| Bcf/d | Billion cubic feet per day | |

| BIA | Bureau of Indian Affairs | |

| Bison | Bison Pipeline LLC | |

| CERCLA | Comprehensive Environmental Response, Compensation and Liability Act | |

| CWA | Clean Water Act | |

| Collar Agreement | Northern Border's interest rate collar agreement | |

| DCF | Discounted cash flow | |

| Delaware Act | Delaware Revised Uniform Limited Partnership Act | |

| Design capacity | Pipeline capacity available to transport natural gas based on system facilities and design conditions | |

| Dth | Dekatherms | |

| Dth/d | Dekatherms per day | |

| EBITDA | Net income plus interest expense, income taxes, depreciation and amortization and all other non-cash charges | |

| El Paso | El Paso Natural Gas Company | |

| EPA | U.S. Environmental Protection Agency | |

| Essar | Essar Steel Minnesota LLC | |

| Exchange Agreement | Agreement with the general partner pursuant to which the Partnership issued new common units to the general partner and provided for Revised IDRs in exchange for the cancellation of the Old IDRs | |

| FERC | Federal Energy Regulatory Commission | |

| GAAP | U.S. generally accepted accounting principles | |

| Gas exiting the WCSB | Net of the supply of and demand for natural gas in the WCSB region that is available for transportation to downstream markets; where supply represents WCSB production adjusted for injections into and withdrawals from WCSB storage | |

| General Partner | TC PipeLines GP, Inc. | |

| GL Cost and Revenue Study | Cost and Revenue study filed by Great Lakes with the FERC in response to the FERC's November 19, 2009 Order | |

| GL Executive Committee | Executive Committee of the Great Lakes Management Committee |

6 TC PIPELINES, LP

| GL Management Committee | Great Lakes Management Committee | |

| GL Rate Proceeding | FERC investigation into Great Lakes' rates pursuant to Section 5 of the NGA | |

| Great Lakes | Great Lakes Gas Transmission Limited Partnership | |

| GTN | Gas Transmission Northwest Corporation | |

| IDRs | Incentive Distribution Rights | |

| INGAA | Interstate Natural Gas Association of America | |

| IRS | Internal Revenue Service | |

| LDCs | Local Distribution Companies | |

| LIBOR | London Interbank Offered Rate | |

| LNG | Liquefied Natural Gas | |

| MBT | Michigan Business Tax | |

| MDth/d | Thousand dekatherms per day | |

| MLP | Master Limited Partnership | |

| MMcf/d | Million cubic feet per day | |

| NEPA | National Environmental Policy Act | |

| NGA | Natural Gas Act | |

| North Baja | North Baja Pipeline, LLC | |

| Northern Border | Northern Border Pipeline Company | |

| NOV | Notice of Violation | |

| November 2009 Order | FERC order issued in FERC Docket No. RP10-149 on November 19, 2009 instituting GL Rate Proceeding | |

| Offering | The sale of 2,609,680 newly issued, unregistered common units representing limited partner interests in the Partnership to TransCan Northern at a price per common unit of $30.042 for an aggregate amount of approximately $78.4 million | |

| Old IDRs | IDRs available to the general partner under the Amended and Restated Agreement of Limited Partnership | |

| ONEOK Partners | ONEOK Partners, L.P. | |

| ONEOK Partners GP | ONEOK Partners GP, LLC | |

| Other Pipes | North Baja and Tuscarora | |

| Our pipeline systems | Great Lakes, Northern Border, North Baja and Tuscarora | |

| Paiute | Paiute Pipeline Company | |

| Partnership | TC PipeLines, LP and its subsidiaries | |

| Partnership Agreement | Second Amended and Restated Agreement of Limited Partnership | |

| RCRA | Resource Conservation and Recovery Act | |

| Revised IDRs | IDRs available to the general partner under the Second Amended and Restated Agreement of Limited Partnership | |

| REX | Rockies Express Pipeline | |

| ROE | Return on equity | |

| Ruby | Ruby Pipeline LLC |

2009 ANNUAL REPORT 7

| SEC | Securities and Exchange Commission | |

| Senior Credit Facility | TC PipeLines' revolving credit and term loan agreement | |

| SFAS | Statement of Financial Accounting Standards | |

| Sierra Pacific Power | Sierra Pacific Power Company, a subsidiary of NV Energy Inc. (formerly known as Sierra Pacific Resources) | |

| TCILP | TC PipeLines Intermediate Limited Partnership, a subsidiary of the Partnership | |

| TransCan Northern | TransCan Northern Ltd. | |

| TransCanada | TransCanada Corporation and its subsidiaries | |

| Tuscarora | Tuscarora Gas Transmission Company | |

| U.S. | United States of America | |

| WCSB | Western Canada Sedimentary Basin | |

| Yuma Lateral | An expansion of the North Baja pipeline from the Mexico/Arizona border to Yuma City, Arizona |

8 TC PIPELINES, LP

PART I

FORWARD-LOOKING STATEMENTS

The statements in this report that are not historical information, including statements concerning plans and objectives of management for future operations, economic performance or related assumptions, are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Exchange Act. Forward-looking statements may include words such as "anticipate," "estimate," "expect," "project," "intend," "plan," "believe," "forecast" and other words and terms of similar meaning. The absence of these words, however, does not mean that the statements are not forward-looking.

These statements reflect our current views with respect to future events, based on what we believe are reasonable assumptions. Certain factors that could cause actual results to differ materially from those contemplated in the forward-looking statements include:

- •

- the

ability of Great Lakes Gas Transmission Limited Partnership (Great Lakes) and Northern Border Pipeline Company (Northern Border) to continue to make distributions at

their current levels;

- •

- the

impact of unsold capacity on Great Lakes and Northern Border being greater or less than expected;

- •

- competitive

conditions in our industry and the ability of Great Lakes, Northern Border, North Baja Pipeline, LLC and Tuscarora Gas Transmission Company (together "our

pipeline systems") to market pipeline capacity on favorable terms, which is affected by:

- •

- future

demand for and prices of natural gas;

- •

- level

of natural gas basis differentials;

- •

- competitive

conditions in the overall natural gas and electricity markets;

- •

- availability

and relative cost of supplies of Canadian and United States (U.S.) natural gas, including the recently discovered shale gas resources such as the Horn

River and Montney deposits in Western Canada, along with U.S. Rockies, Mid-Continent, and Marcellus gas developments;

- •

- competitive

developments by U.S. and Canadian natural gas transmission companies;

- •

- the

availability of additional storage capacity and current storage levels;

- •

- the

level of liquefied natural gas imports;

- •

- weather

conditions that impact supply and demand; and

- •

- the

ability of shippers to meet credit worthiness requirements;

- •

- the

impact of current and future laws, rulings and governmental regulations, particularly Federal Energy Regulatory Commission regulations and rate proceedings, and proposed

and pending legislation by Congress and proposed and pending regulations by the U.S. Environmental Protection Agency on us and our pipeline systems;

- •

- changes

in relative cost structures of natural gas producing basins, such as changes in royalty programs, that may prejudice the development of the Western Canada

Sedimentary Basin;

- •

- decisions

by other pipeline companies to advance projects which will affect our pipeline systems and the regulatory, financing and construction risks related to construction

of interstate natural gas pipelines and additional facilities;

- •

- the

ability of our pipeline systems to identify and/or consummate expansion projects which are accretive growth opportunities for the Partnership;

- •

- performance

of contractual obligations by customers of our pipeline systems;

- •

- the

imposition of entity level taxation by states on partnerships;

- •

- operating hazards, natural disasters, weather-related delays, casualty losses and other matters beyond our control;

2009 ANNUAL REPORT 9

- •

- the

Partnership's ability to identify and/or consummate accretive growth opportunities from TransCanada Corporation or others;

- •

- our

ability to control operating costs and the ability of TransCanada to implement its reorganization of U.S. pipeline operations, including the operations of our

pipeline systems, and realize cost savings; and

- •

- general

economic conditions in North America, which impact:

- •

- the

debt and equity capital markets and our ability to access these markets at reasonable costs;

- •

- the

overall demand for natural gas by end users; and

- •

- natural gas prices.

Other factors described elsewhere in this document, or factors that are unknown or unpredictable, could also have material adverse effects on future results. Please also read Item 1A. "Risk Factors". All forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by these factors. These forward-looking statements and information are made only as of the date of the filing of this report, and except as required by applicable law, we undertake no obligation to update these forward-looking statements and information to reflect new information, subsequent events or otherwise.

Item 1. Business

OVERVIEW

We are a publicly traded Delaware limited partnership formed in 1998 by TransCanada PipeLines Limited to acquire, own and participate in the management of energy infrastructure businesses in North America. Our strategic focus is on delivering stable, sustainable cash distributions to our unitholders and finding opportunities to increase cash distributions while maintaining a low risk profile.

TC PipeLines, LP and its subsidiaries are collectively referred to herein as "the Partnership". In this report, references to "we", "us" or "our" refer to the Partnership. TransCanada PipeLines Limited is a wholly-owned subsidiary of TransCanada Corporation (which, together with its subsidiaries, is referred to as TransCanada).

The general partner of the Partnership is TC PipeLines GP, Inc., a wholly-owned subsidiary of TransCanada.

To date, our investments have been in interstate natural gas pipeline systems that transport natural gas to a variety of markets in the United States, Eastern Canada and Mexico.

- •

- We

own a 46.45 per cent general partner interest in Great Lakes Gas Transmission Limited Partnership (Great Lakes). The remaining 53.55 per cent

interest in Great Lakes is held by TransCanada.

- •

- We

own a 50 per cent general partner interest in Northern Border Pipeline Company (Northern Border). The other 50 per cent interest is held by

ONEOK Partners, L.P. (ONEOK Partners), a publicly traded limited partnership that is controlled by ONEOK, Inc.

- •

- We

own 100 per cent of North Baja Pipeline, LLC (North Baja), which we acquired on July 1, 2009 from TransCanada. Please read "Year in

Review – 2009" within this section for additional information regarding the North Baja acquisition.

- •

- We own 100 per cent of Tuscarora Gas Transmission Company (Tuscarora).

We believe our strong financial position, including available unused capacity on our credit facility, gives us the capacity to pursue opportunities to grow in a sustained and disciplined manner for the long-term benefit of our unitholders.

TransCanada operates Great Lakes, Northern Border, North Baja and Tuscarora (collectively, "our pipeline systems"). See Item 13. "Certain Relationships and Related Transactions, and Director Independence".

10 TC PIPELINES, LP

Year in Review – 2009

Partnership

Public Equity Issuance

On November 18, 2009, the Partnership completed a public offering of 5,000,000 common units at a price of $38.00 per unit for net proceeds of approximately $185 million, including the capital contribution of approximately $4 million from our general partner to maintain its two per cent general partner interest. The proceeds were used to repay debt outstanding under our revolving credit facility.

North Baja Acquisition

On July 1, 2009, the Partnership acquired 100 per cent of North Baja from TransCanada for a purchase price of approximately $271 million. The acquisition was financed through a combination of a private equity issuance, a draw on the Partnership's credit facility and cash on hand. The private equity issuance resulted in 2,609,680 common units issued to a wholly-owned subsidiary of TransCanada at $30.042 per common unit.

The Partnership agreed to acquire an expansion of the North Baja pipeline from the Mexico/Arizona border to Yuma City, Arizona (Yuma Lateral) if TransCanada completed the expansion by June 30, 2010. See "Business of North Baja" within this section for an update with respect to the Yuma Lateral.

Incentive Distribution Right (IDR) Restructuring

Concurrent with the acquisition of North Baja, the Partnership entered into an exchange agreement (Exchange Agreement) with its general partner whereby the Partnership issued 3,762,000 new common units to the general partner and provided revised incentive distribution rights (Revised IDRs) in exchange for the cancellation of the incentive distribution rights available to the general partner (Old IDRs) under the Partnership's Amended and Restated Agreement of Limited Partnership.

Under the terms of the Revised IDRs, the distributions to the general partner were reset to two per cent, down from the general partner distribution levels of the Old IDRs at 50 per cent (for combined general partner interest and incentive distribution interest). The incentive distribution levels of the Revised IDRs will result in increased combined distributions to the general partner (for general partner interest and incentive distribution interest) of 15 per cent and a maximum of 25 per cent when quarterly distributions increase to $0.81 and $0.88 per common unit, or $3.24 and $3.52 per common unit on an annualized basis, respectively.

Partnership Agreement Amended and Restated

As part of the Exchange Agreement, the Partnership's Amended and Restated Agreement of Limited Partnership was amended and restated effective July 1, 2009 to reflect the Revised IDRs as described above.

Our Pipeline Systems

Great Lakes Rate Proceeding

On November 19, 2009, the Federal Energy Regulatory Commission (FERC) instituted proceedings under Section 5 of the Natural Gas Act to review the tariff rates of Great Lakes. As directed under the November 2009 FERC Order, Great Lakes filed a cost and revenue study on February 4, 2010. See "Regulatory Environment, Government Regulation" within this section and also Item 7 "Management's Discussion and Analysis of Financial Condition and Results of Operations" for more information with respect to this proceeding.

Great Lakes Contract Renewal

On November 3, 2009, Great Lakes and TransCanada extended contracts until October 31, 2011 for 470 thousand dekatherms per day (MDth/d) of long haul capacity, which would have expired on October 31, 2010. Great Lakes has 486 MDth/d of long haul capacity and an additional 110 MDth/d of short haul capacity under contracts expiring on October 31, 2010. See "Contracting" within this section for more information with respect to Great Lakes' contracting position.

2009 ANNUAL REPORT 11

Northern Border Des Plaines Project

Northern Border's Des Plaines compressor station and interconnect facilities project went into service in March 2009, with a final cost to Northern Border of approximately $17 million.

Business Strategies

Our strategic focus is on delivering stable, sustainable cash distributions to our unitholders and finding opportunities to increase cash distributions while maintaining a low risk profile.

We seek opportunities to undertake accretive acquisitions and pursue organic growth projects through our pipeline systems to maximize the value of our existing portfolio of investments. Working with our partners in our pipeline systems, we seek to pursue policies that:

- •

- maximize

the utilization of our pipeline systems;

- •

- expand

our pipeline systems to meet market demand and increase supply diversity; and

- •

- promote safe and efficient operations.

We intend to support the execution of our business strategies by:

- •

- maintaining

a strong and balanced financial position to:

- •

- maintain

a prudent level of available cash for distribution to unitholders;

- •

- fund

future growth; and

- •

- broaden

our asset base in a disciplined and focused manner;

- •

- investing

in energy infrastructure businesses in North America that are underpinned by strong business fundamentals and provide stable cash flows; and

- •

- maximizing the benefits of our relationship with TransCanada.

Competitive Strengths

We believe that we are well positioned to execute our business strategies successfully because of the following competitive strengths:

- •

- Our

pipeline systems hold strategic market positions and, except for North Baja, comprise critical links for the transportation of natural gas from the Alberta Hub in Canada

to U.S. markets. The Alberta Hub is one of the largest natural gas hubs in North America. Additional natural gas supply from the Alberta Hub is expected to be available in the future when new

pipeline projects associated with the Montney and Horn River shale deposits in Western Canada are constructed, or if the longer-term potential associated with the proposed development of

the Mackenzie Delta in Northern Canada and the North Slope in Alaska is realized;

- •

- With

TransCanada as operator of our pipeline systems, we believe our pipeline systems are well positioned to continue to operate as trusted and experienced transportation

service providers; and

- •

- The senior management team and the board of directors of our general partner have extensive industry experience and include some of the most senior officers of TransCanada. The management team plays a significant role in developing the strategic direction of our pipeline systems and their associated operations, and we believe our ability to execute our business strategies is enhanced by our affiliation with TransCanada.

12 TC PIPELINES, LP

Our Relationship with TransCanada

One of our principal strengths is our relationship with TransCanada. TransCanada, a Canadian corporation, was founded in 1951 with the objective of transporting natural gas from Alberta, Canada to distant markets. Today, TransCanada is a major North American energy infrastructure company engaged in numerous aspects of the energy industry but is primarily focused on natural gas and oil transmission and power generation services. TransCanada owns, including assets that are under construction or in development, approximately 37,300 miles of wholly-owned natural gas pipelines and interests in an additional 5,500 miles of natural gas pipelines, along with approximately 380 billion cubic feet (Bcf) of storage capacity and, including facilities that are under construction or in development, also owns, operates, and/or controls over 11,700 megawatts of power generation. TransCanada is also constructing the Keystone oil pipeline which will be approximately 3,800 miles in length.

TransCanada provides access to a significant pool of management talent and strong relationships throughout the energy industry. We expect to pursue strategic acquisitions in a disciplined manner and to have the opportunity to participate jointly with TransCanada in reviewing potential acquisitions, including transactions that we would be unable to pursue on our own. Additionally, we may have the opportunity to make acquisitions directly from TransCanada. TransCanada, however, is under no obligation to allow us to participate in any of its pipeline or energy infrastructure acquisitions, nor is TransCanada required to offer any of its assets to us.

See Item 5. "Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities" for more information regarding TransCanada's ownership in us.

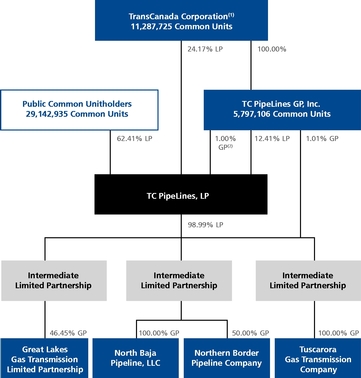

Our Partnership Structure

The following chart depicts our organizational and ownership structure.

- (1)

- Through

subsidiary companies.

- (2)

- Effective aggregate economic interest.

2009 ANNUAL REPORT 13

Our Pipeline Systems

All of our pipeline systems are regulated by the FERC. Operating revenue is derived from the transportation of natural gas. The maximum transportation rates that our pipeline systems may charge are approved by the FERC, and in most cases, established in a FERC proceeding known as a rate case. During a rate case, a determination is reached by the FERC, either through a hearing or a settlement, on the maximum rates permissible for transportation service on a pipeline system that include the recovery of cost-based investment, operating expenses and a reasonable return for its investors. Once maximum rates are set, the pipeline system is not permitted to adjust the maximum rates to reflect changes in costs or contract demand until new rates are approved by the FERC, usually after a rate case has been filed. The FERC also governs the general terms and conditions for natural gas transportation service on interstate natural gas pipelines. The tariff also allows for services to be provided under negotiated and discounted rates. As a result, earnings and cash flow of each pipeline system depend on costs incurred; contracted capacity and transportation path; the volume of gas transported; and the ability of each system to sell capacity at acceptable rates.

Transportation Services

Our pipeline systems' transportation contracts include specifications regarding the receipt and delivery of natural gas at points along the pipeline system. The transportation services provided by our pipeline systems are generally categorized as firm or interruptible. The type of transportation contract, either for firm or interruptible service, determines the basis upon which each customer is charged.

14 TC PIPELINES, LP

Customers with firm service transportation agreements pay a fee known as a reservation charge to reserve pipeline capacity, regardless of use, for the term of their contracts. On the Great Lakes, Northern Border and North Baja systems, firm service transportation customers also pay a variable usage fee known as a commodity charge (or utilization fee) that is generally based on distance and the volume of natural gas they transport.

Customers with interruptible service transportation agreements may utilize available capacity on a pipeline system after firm service transportation requests are satisfied. Interruptible service customers are assessed commodity charges (or utilization fees) based on distance and the volume of natural gas they transport. On the Great Lakes and Tuscarora systems, interruptible revenues are generally subject to a sharing mechanism whereby 90 per cent of the revenue is refunded to firm shippers paying maximum tariff rates. Our Northern Border and North Baja pipeline systems are not subject to sharing mechanisms with their shippers on their interruptible revenues.

Variable usage fees for Northern Border include a compressor usage surcharge to recover the cost of the electric compression and fuel use tax which relates to both firm and interruptible transportation services.

The table below provides information with respect to tariff revenue composition for each of our investments for the year ended December 31, 2009. It is provided to indicate the extent to which the revenue for our pipeline systems is dependent upon fixed versus variable fees.

| |

|

2009 Tariff Revenue Composition |

|

||||||

|---|---|---|---|---|---|---|---|---|---|

| |

|

Firm Contracts |

|

|

|||||

| |

Our Ownership Interest |

Capacity Reservation Charges |

Variable Usage Fees |

Interruptible Contracts & Other Services |

|

||||

| Great Lakes | 46.45% | 97% | 2% | 1% | |||||

| Northern Border | 50% | 85% | 10% | 5% | |||||

| North Baja | 100% | 97% | 2% | 1% | |||||

| Tuscarora | 100% | 100% | 0% | 0% | |||||

Business of Great Lakes

Great Lakes is a Delaware limited partnership formed in 1990. The Partnership acquired its 46.45 per cent general partner interest in Great Lakes in February 2007.

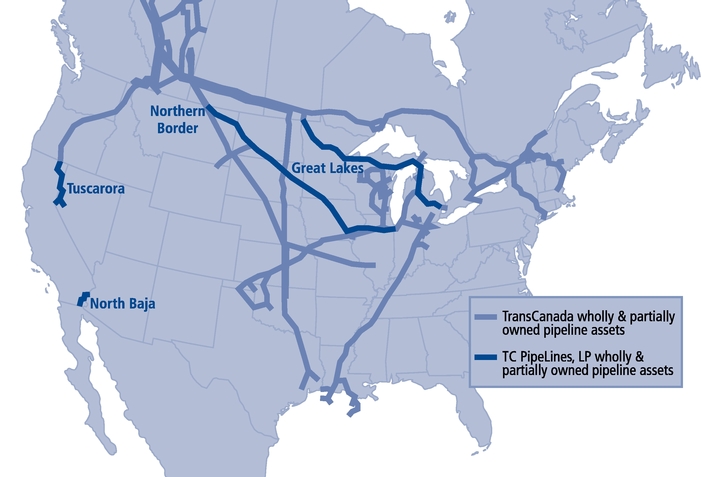

Great Lakes receives natural gas from an interconnection with the TransCanada Mainline system at the Canadian border near Emerson, Manitoba, Canada and extends across Minnesota, Northern Wisconsin and Michigan, and redelivers gas to TransCanada at the Canadian border near Sault Ste. Marie, Ontario, Canada and St. Clair, Ontario, Canada. Great Lakes also connects to storage centers in Michigan and interconnects with other interstate natural gas pipelines.

The pipeline system consists of approximately 2,115 miles of pipeline with diameters ranging from 10 inches to 36 inches and a design capacity of 2,500 million cubic feet per day (MMcf/d) during the winter and 2,300 MMcf/d during the summer. Annual capacity is determined by the summer design capacity. Great Lakes has 14 compressor stations with a total of 438,000 horsepower and measurement facilities to support the 58 receipt and delivery points on the system.

The original construction of the Great Lakes system occurred in 1967 and 1968. Numerous capacity system expansions have occurred since its original construction, the last one completed in 1998.

The major policies of Great Lakes are established by the management committee of Great Lakes (GL Management Committee). The current GL Management Committee consists of four appointed members, two of whom are designated by us and two of whom are designated by TransCanada. All decisions by the GL Management Committee

2009 ANNUAL REPORT 15

require unanimous consent. For the day to day management of Great Lakes' business, the GL Management Committee established an executive committee (GL Executive Committee). The GL Executive Committee currently consists of two appointed members: one Partnership GL Management Committee member, and one TransCanada GL Management Committee member, who also serves as the president of Great Lakes. The GL Executive Committee has all of the powers of the GL Management Committee in the management of Great Lakes' business.

Business of Northern Border

Northern Border is a Texas general partnership formed in 1978. The Partnership had a 30 per cent general partner interest in Northern Border at its initial public offering and acquired an additional 20 per cent general partner interest in April 2006.

Northern Border transports natural gas from the Canadian border near Port of Morgan, Montana to a terminus near North Hayden, Indiana. Additionally, Northern Border transports natural gas produced in the Williston Basin of Montana and North Dakota, and the Powder River Basin of Wyoming and Montana, as well as synthetic gas produced at the Dakota Gasification plant in North Dakota.

The pipeline system consists of 1,249 miles of pipeline with diameters ranging from 30 to 42 inches and a design capacity on the largest segment of the pipeline of 2,374 MMcf/d. Northern Border has 18 compressor stations with a total of approximately 517,000 horsepower, measurement facilities to support the 65 receipt and delivery points on the system.

Construction of Northern Border's system was initially completed in 1982, followed by expansions or extensions in 1991, 1992, 1998, 2001 and 2006.

Northern Border is managed by a management committee that consists of four members. Each partner designates two members, and the Partnership designates one of our members as Chairman. Each partner holds a 50 per cent voting interest on the management committee.

Des Plaines Project – The compressor station and interconnect facilities project went into service in March 2009, with a final cost to Northern Border of approximately $17 million. The project is fully subscribed under a 10 year compression and transportation contract. The new contract generates approximately $3 million in annual revenue for Northern Border.

Business of North Baja

North Baja is a Delaware limited liability company formed in 2000. The Partnership acquired 100 per cent of North Baja on July 1, 2009 from TransCanada.

North Baja transports natural gas between an interconnection with El Paso Natural Gas Company (El Paso) near Ehrenberg, Arizona and an interconnection near Ogilby, California on the California/Mexico border with the Gasoducto Bajanorte natural gas pipeline system which is owned by Sempra Energy International. North Baja is a bi-directional system which allows it to accept receipts and make deliveries of natural gas at both interconnection points with connecting pipelines.

The pipeline system consists of 80 miles of pipeline with diameters of 30 and 36 inches and a FERC licensed capacity of 500 MMcf/d for southbound transportation and a design capacity of 600 MMcf/d for northbound transportation. There is one compressor station at the north end of the pipeline with a limit of 21,600 horsepower. The metering points at both ends of the pipeline act as either receipt or delivery points depending on the direction of flow.

The North Baja pipeline system was initially placed into service in 2002. An expansion was completed in April 2008 to allow for bi-directional gas flow. To date, all gas flows have been southbound.

16 TC PIPELINES, LP

Yuma Lateral Project – At the time of our acquisition of North Baja, TransCanada had begun an expansion project of the North Baja pipeline from the Mexico/Arizona border to Yuma City, Arizona. We agreed to acquire the expansion facilities and contracts for an additional sum up to $10 million, if TransCanada completed the project by June 30, 2010. The Yuma Lateral project is currently under construction and is expected to be completed in March 2010. The purchase price has yet to be determined.

Business of Tuscarora

Tuscarora is a Nevada general partnership formed in 1993. The Partnership acquired 49 per cent of Tuscarora in September 2000, followed by an additional 49 per cent in December 2006, and the final two per cent in December 2007.

Tuscarora originates at an interconnection point with existing facilities of Gas Transmission Northwest Corporation (GTN), a wholly-owned subsidiary of TransCanada, near Malin, Oregon and runs southeast through Northeastern California and Northwestern Nevada. Tuscarora's pipeline system terminates near Wadsworth, Nevada. Along its route, deliveries are made in Oregon, Northern California and Northwestern Nevada.

The pipeline system consists of 240 miles of pipeline with a diameter of 20 inches and a design capacity of approximately 230 MMcf/d. Tuscarora has three compressor stations with a total of over 17,100 horsepower, and measurement facilities at one receipt point and 16 delivery points.

The Tuscarora pipeline system was initially placed into service in 1995, followed by expansions or extensions in 2001, 2002, 2005 and 2008.

NATURAL GAS INDUSTRY OVERVIEW

North American Natural Gas Flows

Natural gas is transported from producing regions and Liquefied Natural Gas (LNG) import facilities to market hubs for distribution to natural gas consumers. The main producing regions in North America are the Gulf of Mexico, Western Canada Sedimentary Basin (WCSB), Mid-Continent, Rockies, Permian basin, and San Juan basin. The largest consuming regions are the Northeastern U.S. and the Midwest. Recent increases in the development of unconventional and shale gas have resulted in increases in overall North American natural gas production and increased reserves. Over the past two years, significant new pipeline infrastructure has been added to move gas from producing regions to market areas, including the Rockies Express Pipeline (REX) which transports gas from the Rockies to Ohio. New interstate natural gas pipelines sourcing supply basins in the Mid-Continent, along with the completion of REX, have increased the supply of natural gas into Eastern markets. As a result, the level of competition in these market regions from alternate sources of supply has increased and caused a general reduction in basis differential between producing and market regions. This impacts the transportation value on pipelines, including our pipeline systems. Additional pipeline projects have been proposed, including projects to move additional gas supply into western market regions, which are expected to continue to impact overall North American natural gas flows. Additionally, development of new producing regions, such as the Marcellus shale in the eastern U.S., will also impact North American natural gas flows.

2009 ANNUAL REPORT 17

Demand

North America

Demand for natural gas transportation service on a pipeline system is directly related to demand for natural gas in the markets served by that system. Factors that may impact demand for natural gas include:

- •

- weather

conditions;

- •

- economic

conditions;

- •

- government

regulation;

- •

- the

availability and price of alternative energy sources versus availability and price of natural gas;

- •

- natural

gas storage inventories for the markets served;

- •

- fuel

conservation measures; and

- •

- technological advances in fuel economy and energy generation devices.

Some of the factors have an immediate impact on natural gas demand, while others are longer term. Natural gas demand fluctuates from year to year, as well as seasonally, as a result of the factors described above. North American demand for natural gas declined in 2009 with the economic downturn. We expect that demand in 2010 will be relatively unchanged but will increase in the long term as economic growth returns. The relative environmental merits of natural gas versus other carbon based forms of energy are also expected to increase the demand for natural gas. The impact of natural gas demand on the demand for natural gas transportation service on any one pipeline system will depend upon changes in demand for natural gas in the market areas which that pipeline serves.

Other factors that may impact demand for natural gas transportation service on any one system include:

- •

- the

availability of natural gas supply at the pipeline system's receipt points;

- •

- the

ability and willingness of natural gas shippers to utilize that pipeline system over alternative pipelines;

- •

- the

relative transportation rates; and

- •

- the volume of natural gas delivered to the markets supplied by that system from other supply sources and storage facilities.

These factors, and the impact on our pipeline systems, are discussed further under "Supply" and "Customers, Competition, and Contracting".

Our pipeline systems are exposed to risk when marketing available capacity. This occurs when existing transportation contracts expire and when there is available capacity on the pipeline system. Customers with expiring contracts can, depending on the market, either extend their contract commitments, renegotiate for shorter terms and/or discounted rates, or they may choose not to renew their contract. Customers with competitive alternatives analyze the market price spread, or basis differential, between receipt and delivery points along the pipeline to determine their expected gross margin. The anticipated margin and its variability are important determinants of the transportation rate customers are willing to pay and the transportation routes they choose to ship their gas. Depending on supply and market conditions, a customer can contract for long-term firm transportation, short-term firm transportation, or interruptible transportation services.

Our Pipeline Systems

Contracted capacity and system throughput are measures of demand for natural gas transportation services. The trend in the amount of design capacity that is contracted gives an indication of the trend in revenue generation. The trend in system throughput generally gives an indication of the extent to which design capacity is being utilized. The table

18 TC PIPELINES, LP

below provides historical information on the average throughput and contracted capacity as a percentage of design capacity for our pipeline systems from the past three years:

| Year Ended December 31 | 2009 | 2008 | 2007 | |||||

| Contracted Capacity(a) | ||||||||

| Average Throughput (MMcf/d) | ||||||||

Great Lakes(b) |

100% |

100% |

100% |

|||||

| 1,992 | 2,143 | 2,270 | ||||||

Northern Border |

68% |

90% |

97% |

|||||

| 1,708 | 2,041 | 2,247 | ||||||

| North Baja(c) | ||||||||

| Southbound | 79% | 88% | 95% | |||||

| Northbound | 64% | 53% | n/a | |||||

| 257 | 278 | 247 | ||||||

Tuscarora |

99% |

98% |

96% |

|||||

| 93 | 82 | 77 | ||||||

- (a)

- Contracted

capacity percentage is calculated based upon contracted capacity compared to design capacity for Northern Border, North Baja northbound

transportation and Tuscarora, compared to average design capacity for Great Lakes, and compared to FERC licensed capacity for North Baja southbound transportation.

- (b)

- The

average throughput for Great Lakes includes periods prior to the February 22, 2007 acquisition by us of a 46.45 per cent general

partner interest in Great Lakes.

- (c)

- Due to North Baja's bi-directional nature, it can contract for both southbound and northbound capacity separately. North Baja's ability to provide northbound transportation services commenced April 2008, but as there have been no northbound gas flows to date, average throughput reflects only southbound deliveries.The average throughput for North Baja includes periods prior to the July 1, 2009 acquisition by us of a 100 per cent interest in North Baja.

Great Lakes provides transportation services to Midwest and Northeast U.S. markets, as well as Eastern Canadian markets. The transportation services provided by Great Lakes are principally related to storage injection and withdrawal activity from storage centers in Michigan and Ontario as Great Lakes provides a critical link between these storage centers and consuming markets. Demand for natural gas in the markets served by Great Lakes declined in 2009 due to the economic environment's negative impact on industrial and electric generation demand. However, this demand is expected to recover slowly in the near term and grow over the long term, primarily due to the anticipated growth in demand for natural gas fired power generation. Demand for transportation services on Great Lakes remained relatively constant until 2009 when high storage levels and the economic recession dampened demand for Great Lakes transportation services. Underutilization of contracts reflected the reduced demand for transportation from Canadian supply sources during 2009. This is discussed further under "Customers, Competition and Contracting".

Northern Border provides transportation services to Midwest U.S. markets directly and through major interconnections with other interstate natural gas pipelines at Ventura and Harper, Iowa and the Chicago market hub. Demand for natural gas in the markets served by Northern Border was negatively impacted by the economic environment in 2009 and although these impacts may continue into 2010, overall demand for natural gas is expected to grow over the long term. Demand for transportation on Northern Border decreased in 2008 as a result of new volumes of natural gas being delivered to its Ventura market area from the Rockies basin by a competing pipeline. The new supply volumes moved from the Ventura market area further east with the completion of REX in 2009 and natural gas prices at Ventura improved, which improved market conditions for Northern Border at Ventura. Additional supply into Eastern markets from new pipeline projects which went into service in 2009, including the completion of REX, resulted in other supplies being displaced into the Chicago market. Demand for WCSB natural gas supply in the Chicago market has

2009 ANNUAL REPORT 19

subsequently declined, resulting in reduced demand for transportation to Chicago on the eastern leg of Northern Border's system in 2009. This is discussed further under "Customers, Competition and Contracting".

North Baja was initially constructed to provide transportation services to markets in northern Baja California, Mexico through its interconnection with Gasoducto Bajanorte. Demand for natural gas in this market has been relatively flat over the past three years but is expected to grow over the long term. Demand for transportation services on North Baja is expected to grow slowly over time as new loads develop in Mexico that prefer to be served by U.S sourced gas. The facility modifications (bi-directional capability) that were completed in April 2008 enable North Baja to serve natural gas demand in the southwestern U.S. through northbound transportation services when the Energia Costa Azul LNG terminal receives LNG cargos. Although long-term contracts for northbound and southbound transportation services do not fully contract the pipeline capacity, the bi-directional capabilities of the system result in a continued high demand for transportation services on the North Baja pipeline system.

Tuscarora provides transportation services to markets in Oregon, Northern California and Northern Nevada. Demand for natural gas in these markets has grown over the last three years due primarily to increased demand from electric generation companies and local distribution companies (LDCs). The major shippers on Tuscarora's system require transportation capacity to meet their obligations to their customers but are not necessarily required to flow any gas through the system. As a result, Tuscarora's throughput is not indicative of its revenue generation. This is discussed further under "Customers, Competition and Contracting".

Seasonality

North America

North American demand for natural gas is seasonal. In general, demand tends to be higher in the winter months for heating requirements and in the summer for power generation demand to meet increased air conditioning or cooling requirements. The winter season is considered to be November through March, and the peak summer season is considered to be July through September. Weather conditions throughout North America can significantly impact regional natural gas supply and demand. Moderate winter and summer temperatures can lead to a decline in the demand for transportation service due to reduced demand for natural gas.

The North American natural gas industry uses natural gas storage to balance the impacts of relatively steady natural gas supply with the seasonality of demand for natural gas. In the spring and fall, when there is less demand for heating and cooling requirements, gas continues to be shipped through pipelines and is put into storage near market areas and in producing regions for future use. Available storage capacity combined with price spreads between current and future pricing during certain periods of the year may make it more profitable to store the gas for use in the future when the price for natural gas may be more favorable.

Gas in storage in producing regions, such as the WCSB, may impact the supply of natural gas for transportation to market areas. During periods of storage injection, there will be less supply available for transportation to market areas. Conversely, storage withdrawal provides additional supplies of natural gas for transportation to markets.

Gas in storage near market areas also impacts the demand for transportation services. Transportation services are required to transport the natural gas from producing regions to the market area. When the natural gas is in storage near the market area, the transportation required to meet market demand is reduced.

Levels of natural gas in storage in North America have been growing over the past three years and were at five year highs at the end of 2009. As inventory levels in storage fields approach maximum capacity, the demand for additional natural gas and associated transportation services is reduced. Market areas are less dependent upon supply from producing regions to meet short-term demand when there is adequate natural gas stored nearby.

The revenue associated with capacity that is contracted under long-term firm contracts is not impacted by seasonal throughput variations. The amount of uncontracted (or available) transportation capacity as well as transportation

20 TC PIPELINES, LP

capacity under short-term contracts on a pipeline system determines the extent to which seasonal demand will impact a pipeline system's revenue. Revenues for pipeline systems that have a higher ratio of long-term contracts (contracts with a duration of at least one year) will be impacted less by seasonal demand. Conversely, for those pipeline systems with more available capacity, or operating under short-term contracts, fluctuations in demand between seasons can impact revenue. Additionally, a pipeline can generate revenue with interruptible or daily sales of available capacity if a firm transportation customer does not utilize all of their contracted capacity. Pipeline systems which have a tariff that includes seasonal rates for short-term service may be able to mitigate the potential negative impact of seasonal fluctuations in demand.

Our Pipeline Systems

Great Lakes – Great Lakes' design day capacity at the receipt point near Emerson, Manitoba is approximately 2.5 billion cubic feet per day (Bcf/day) during the winter due to the ability to increase flow through gas turbine driven compressors during periods of low ambient temperatures and 2.3 Bcf/day during the summer when ambient temperatures are higher.

The transportation value across the Great Lakes pipeline system is normally at its highest in conjunction with storage fill requirements and electric power generation demand. Great Lakes is connected to approximately 880 Bcf of working gas storage located at the Eastern end of the Great Lakes system in Michigan and Ontario, Canada. The demand for Great Lakes' long haul transportation service is normally at its highest when natural gas is being delivered to storage areas. The high demand period usually begins in the spring and extends through most of the summer. High levels of natural gas in storage throughout 2009 reduced the demand for Great Lakes' transportation services to fill market storage.

During the winter, there is also strong demand for Great Lakes' services to meet the peak winter heating demand requirements of Northern Minnesota, Northern Wisconsin and Michigan. These deliveries are met through Great Lakes' short haul, long haul, and backhaul transportation services from storage fields in Michigan and Ontario, Canada.

Great Lakes experiences significant winter volatility in the utilization of its long haul transportation contracts due to downstream constraints on the Union Gas Limited and TransCanada pipeline systems. When there are increases in natural gas withdrawn from the Eastern Michigan and Ontario, Canada storage fields to serve U.S. Northeast and Eastern Canadian markets, constraints increase on downstream pipelines. These constraints may reduce shippers' ability to use Great Lakes' transportation services to serve Eastern markets and may reduce demand for Great Lakes' transportation services during certain peak winter periods.

Approximately 90 per cent of Great Lakes' average design capacity was contracted on a long-term firm basis in 2009, compared to 89 per cent in 2008. As a result, Great Lakes had limited exposure to fluctuations in revenue due to seasonality. Reductions in the level of capacity under long-term contracts will increase exposure to fluctuations in revenue from seasonal and short-term demand for transportation services. See further discussion under "Contracting" in this section for changes to Great Lakes' contracting profile.

Northern Border – Demand for Northern Border's transportation services has traditionally been the strongest during peak winter months to serve heating demand and peak summer months to serve electric cooling demand and storage injection.

Approximately 42 per cent of Northern Border's design capacity was contracted on a long-term firm basis in 2009, compared to 65 per cent in 2008. As a result, Northern Border has increased exposure to fluctuations in revenue due to seasonal demand factors.

Some of Northern Border's exposure may be mitigated by its seasonal rate structure for short-term service that provides for higher maximum rates during anticipated peak usage periods and lower maximum rates during anticipated periods of reduced demand. Approximately 27 per cent of Northern Border's design capacity was contracted on a short-term basis in 2009 compared to 24 per cent in 2008.

2009 ANNUAL REPORT 21

North Baja and Tuscarora – Seasonal fluctuations in revenue are minimal for these pipeline systems because their capacity is contracted on a long-term basis. See further discussion under "Contracting" in this section.

Supply

North America

The primary source of natural gas transported by our pipeline systems, except North Baja, is the WCSB. For this reason, the continuous supply of Canadian natural gas is crucial to the long-term financial condition of our pipeline systems.

The WCSB has remaining discovered natural gas reserves of approximately 61 trillion cubic feet and a reserves-to-production ratio of approximately 11 years at current levels of production. Supply from the WCSB has declined in recent years due to reduced drilling activity in the basin related to lower natural gas prices, higher supply costs, including higher royalties, and competition for capital from other North American gas production basins that have lower exploration costs. Drilling in the WCSB is expected to recover in the ensuing years assuming that gas prices stabilize and that exploration and development costs become more economical.

The net amount of natural gas exiting the WCSB is a significant factor affecting the volume of natural gas transported by our pipeline systems, except North Baja. "Gas exiting the WCSB" is the term we use to represent the net of the supply of and demand for natural gas in the WCSB region. WCSB supply is made up of WCSB production with injections into WCSB storage reducing net supply, and withdrawals from WCSB storage increasing supply. Gas exiting the WCSB is determined by:

- •

- WCSB

natural gas production levels;

- •

- Western

Canadian demand for WCSB natural gas; and

- •

- Western Canadian storage capacity for WCSB natural gas and demand for storage injection.

The extent to which gas exiting the WCSB will be transported on each pipeline system is affected by:

- •

- demand

for WCSB natural gas in various U.S. consumer markets;

- •

- available

transportation capacity and related market pricing options on our competitors' pipelines;

- •

- natural

gas from other supply sources that can be transported to our customer markets;

- •

- the

natural gas market price spread between the Alberta Hub in Canada and the applicable downstream market which reflects the relative supply of and demand for WCSB natural

gas in Canada and in the U.S.; and

- •

- storage capacity in the U.S. and Canada and the related demand for storage injection or withdrawal.

Our Pipeline Systems

Great Lakes receives natural gas primarily from its interconnection with the TransCanada Mainline pipeline system. Gas received from the interconnection with the TransCanada Mainline pipeline system near Emerson, Manitoba, Canada is WCSB supply. Great Lakes also transports natural gas from its interconnection with TransCanada's ANR pipeline system (ANR) and from storage facilities. ANR is interconnected with numerous other pipelines, primarily sourcing gas from the Gulf of Mexico and Mid-Continent regions. The gas received from Great Lakes' interconnection with ANR accounted for approximately 12 per cent of the natural gas Great Lakes transported in 2009.

Northern Border receives natural gas primarily from its interconnection with one of TransCanada's pipelines at the Canadian border near Port of Morgan, Montana. Gas received from this interconnection is WCSB supply. Northern Border also transports natural gas produced in the Williston Basin of Montana and North Dakota and the Powder River Basin of Wyoming and Montana, which accounted for approximately 11 per cent of the natural gas Northern Border transported in 2009. Synthetic gas produced at the Dakota Gasification plant in North Dakota accounted for another approximately eight per cent of the natural gas transported by Northern Border in 2009.

22 TC PIPELINES, LP

TransCanada is pursuing the Bison Pipeline Project, which is a proposed new interstate natural gas pipeline extending from the Powder River Basin producing region in Wyoming to an interconnection with the Northern Border system in Morton County, North Dakota. The FERC issued a Final Environmental Impact Statement in December 2009 and the project is in the final stages of the regulatory process. Pending these approvals, TransCanada expects to commence construction in May 2010 and expects to place the project into service in late 2010. If completed, this project would bring approximately 407 MMcf/d of additional supply from the Powder River Basin to Northern Border, which would increase Northern Border's supply diversity.

North Baja receives natural gas from its interconnections with El Paso, which is primarily gas originating from the West Texas or Southern Rocky Mountain supply regions, and Gasoducto Bajanorte, which would originate from the Costa Azul LNG facility in Mexico. To date, no gas has been transported on North Baja from its interconnection with Gasoducto Bajanorte.

Tuscarora receives natural gas from its interconnection with GTN. GTN is interconnected with WCSB supply as well as natural gas from the Rockies and other U.S. basins. A second interstate pipeline with the potential to interconnect to Tuscarora, Ruby Pipeline LLC (Ruby), is currently under development. If Ruby is constructed, it will increase Tuscarora's access to natural gas from the Rockies and other U.S. basins.

CUSTOMERS, COMPETITION AND CONTRACTING

Customers

Our pipeline systems transport natural gas for a variety of customers including other natural gas pipelines, LDCs, industrial companies, electric power generation companies, natural gas producers, and natural gas marketers. Each type of customer has a different reason for using certain natural gas transportation services and routes. LDCs, industrial companies and electric power generation companies typically require a secure and reliable supply of natural gas over a sustained period of time to meet the needs of their customers. These types of shippers typically enter into long-term firm transportation contracts to ensure a ready supply of natural gas and sufficient transportation capacity to meet their obligations to their customers over the life of their contracts with their customers. Natural gas producers typically enter into firm transportation contracts to ensure that they will have sufficient capacity to deliver their product to market centers. Natural gas marketers typically use transportation services to capitalize on natural gas price volatility and therefore tend to contract for shorter terms to increase their flexibility.

Great Lakes – The largest customer for Great Lakes' capacity is TransCanada, through its Canadian mainline pipeline system. This capacity is used by TransCanada customers to transport WCSB gas to Eastern Canadian and U.S. markets. TransCanada's ANR pipeline system also holds capacity on Great Lakes to integrate its Michigan storage locations with its Wisconsin pipeline segments. Great Lakes customers also include various LDCs, natural gas marketers and producers. Great Lakes' customer profile is becoming more heavily weighted towards natural gas marketers and less towards producers and end users, such as industrial customers and LDCs.

For the year ended December 31, 2009, contracts with TransCanada and its affiliates represented approximately 49 per cent of Great Lakes' revenue. Great Lakes did not have any other customers contributing more than 10 per cent of its 2009 revenues. TransCanada has elected to turn back contracts for 361 MDth/d of capacity as of October 31, 2010. This is discussed further under "Contracting".

Northern Border – Northern Border's main customers are natural gas producers and marketers. Other customers include industrial facilities, LDCs and electric power generating companies.

For the year ended December 31, 2009, contracts with BP Canada Energy Marketing Corp. and Tenaska Marketing Ventures represented approximately 17 per cent and 11 per cent, respectively, of Northern Border's revenue. Northern Border did not have any other customers contributing more than 10 per cent of its 2009 revenues.

2009 ANNUAL REPORT 23

North Baja – North Baja's main customers are electric power generating companies and natural gas marketers.

North Baja's revenues are dependent upon a relatively small group of customers. For the year ended December 31, 2009, the following shippers had contracts which contributed revenues in excess of 10 per cent of North Baja's overall revenues (including the period prior to the Partnership's July 1, 2009 acquisition of North Baja):

| • Sempra LNG Marketing Corp. | 32% | ||

• Shell Energy North America |

19% |

||

• Energia Azteca |

15% |

||

• Gasoducto Rosarito |

12% |

||

• Termoelectrical de Mexicali |

11% |

Tuscarora – Tuscarora's main customers are a power generation company and an LDC, along with a variety of industrial, commercial, and other companies.

For the year ended December 31, 2009, contracts with Sierra Pacific Power Company and Southwest Gas Corporation contributed approximately 76 per cent and 11 per cent, respectively, of Tuscarora's revenue. Tuscarora did not have any other customers contributing more than 10 per cent of its 2009 revenues.

Competition

Competition among natural gas pipelines is based primarily on transportation rates and proximity to natural gas supply areas and markets. Our pipeline systems face competition at both the supply and market ends of their pipeline systems. At the supply end, other pipelines access the WCSB and provide alternative routes for shippers to access markets served by our systems or take gas to markets not served by our pipeline systems. Competition at the market end comes from WCSB natural gas which may be transported through alternative pipeline systems as well as from natural gas sourced from other U.S. supply basins, including shale gas, which can be transported by other pipelines into our pipeline systems' market areas. Our North Baja pipeline system is not connected to the WCSB and therefore is not sensitive to WCSB competitive factors.

Reductions in gas exiting the WCSB over recent years have resulted in excess pipeline capacity serving the WCSB. As a result, there has been an increase in competition for gas exiting the WCSB. We anticipate there will be excess natural gas pipeline capacity serving the WCSB for the foreseeable future and therefore competition for gas exiting the WCSB will continue. Commencing January 1, 2010, one of the main pipelines accessing the WCSB, the TransCanada Mainline pipeline system, increased its rates for firm transportation services by 40 per cent. This may improve the relative competitive position of the other pipelines accessing the WCSB, including our Great Lakes and Northern Border pipeline systems.

New natural gas supplies from unconventional sources, such as shale, and new pipeline projects in the U.S. moving additional natural gas supply from the Rockies basin and from the Barnett Shale have increased the supply competition in the markets served by our pipeline systems. This additional supply delivered to Midwest and Eastern markets is displacing traditional supply in the markets served by our pipeline systems.

Great Lakes – Great Lakes' principal business comes from its position as a link in the chain of pipelines that facilitate the transportation of natural gas from WCSB to Midwest and Northeast U.S. markets and Eastern Canadian markets. Natural gas is transported by TransCanada from Western Canada to near Emerson, Manitoba, Canada. Great Lakes provides transportation from Emerson to the TransCanada system at St. Clair, Ontario. TransCanada transports the gas received at St. Clair to Dawn, Ontario, Canada and points further east. The primary competition for Great Lakes is the alternate route from Western Canada to Dawn on TransCanada's Mainline. Other routes from Western Canada to Ontario, Canada, are the Foothills Pipeline to Northern Border to Vector Pipeline route, or the Alliance Pipeline which

24 TC PIPELINES, LP

also interconnects with the Vector Pipeline. In addition, gas can be delivered to the markets served by Great Lakes by competing pipelines that have access to alternate sources of supply from the Rockies, Mid-Continent and Gulf Coast.

Northern Border – Northern Border's system competes for natural gas supply with other pipelines that transport WCSB natural gas to markets in the West, Midwest and East in North America. The pipeline systems that offer primary competition in these markets include Alliance Pipeline, Great Lakes, GTN, and other pipelines that interconnect with the TransCanada Mainline for WCSB supply. Northern Border also has competition in its market areas from other pipelines that have access to natural gas storage facilities, and alternate sources of supply from the Rockies, Mid-Continent, Permian Basin and Gulf Coast, as well as LNG. The pipeline systems that deliver natural gas from competing supply sources include Northern Natural Gas Company in Northern Border's Ventura, Iowa market area and ANR, Midwestern Gas Transmission Company and Natural Gas Pipeline of America in the Chicago market region.

Increased competition in the Chicago market can impact the Ventura market. In the face of this competition, Northern Border customers with firm service to the Chicago market may increase deliveries to the Ventura market, thereby reducing Northern Border's ability to capture additional transportation revenues to Ventura.

The combination of growing supply from the Rockies and shale developments reaching the Chicago market region through new and available pipeline capacity, and reductions in demand resulting from the current economic environment has negatively impacted Northern Border's ability to contract available capacity to Ventura and Harper. The impact of these competitive factors is expected to continue in 2010. Northern Border's contracting position is discussed further under "Contracting".

North Baja – North Baja's southbound deliveries into Mexico will compete with LNG deliveries from the Energia Costa Azul terminal when supply is received at that terminal. Shippers retain contracts on North Baja to be able to provide service to several power plants in Baja California, Mexico at times when LNG sourced gas from the Costa Azul terminal is unavailable. As well, North Baja provides a critical path for LNG from the Energia Costa Azul terminal to reach markets in the southwestern United States, once cargos of LNG are received at this terminal.

Tuscarora – Tuscarora's primary competition in the Northern Nevada natural gas transportation market is with Paiute Pipeline Company (Paiute), owned by Southwest Gas Co. Paiute interconnects with Northwest Pipeline Corp. at the Nevada-Idaho border and transports natural gas from British Columbia, Canada and from the Rockies to the Northern Nevada market.

Contracting

Transportation contracts mature at varying times and for varying amounts of throughput capacity. As existing contracts on our pipeline systems approach their expiration dates, efforts are made to extend and/or renew the contracts. The ability to extend and/or renew expiring contracts will depend upon competitive alternatives, the regulatory environment, and market and supply factors. The length of new or renegotiated contracts will be affected by current market price spreads, transportation rates, competitive conditions, levels of available pipeline capacity, and judgments concerning future market trends and volatility. Customer liquidity and capital constraints can also impact the length of contracts. If market conditions are not favorable at the time of renewal, transportation capacity may remain available until market conditions become more favorable. Subject to regulatory requirements, our pipeline systems attempt to recontract or remarket their capacity at the maximum rates allowed under their tariffs. However, a pipeline system may discount capacity under certain circumstances in order to maximize revenue.

Increased competition within the North American natural gas industry has resulted in a trend towards shorter term contracting as customers assess and choose the markets which optimize their netback prices.

2009 ANNUAL REPORT 25

Great Lakes – For the year ended December 31, 2009, Great Lakes' average contracted capacity compared to average design capacity was 100 per cent. Great Lakes had long-term firm transportation contracts for 89 per cent of its average design capacity with a weighted average remaining contract life of 2.0 years, as at January 31, 2010. On November 1, 2010, the per cent of average design capacity contracted on a firm basis decreases to 68 per cent.

Great Lakes had approximately 990 MDth/d of long haul capacity expiring on October 31, 2010, of which 831 MDth/d, representing 36 per cent of Great Lakes' average design capacity, was contracted with TransCanada. On November 3, 2009, Great Lakes and TransCanada renewed contracts through October 31, 2011 for 470 MDth/d of capacity, or 20 per cent of average design capacity, some at a slightly discounted rate, and agreed that Great Lakes would provide other transportation services. TransCanada elected to turn back 361 MDth/d, or 16 per cent of average design capacity, as of October 31, 2010. Of the remaining long haul capacity expiring on October 31, 2010, 125 MDth/d was turned back.

In addition to the long haul capacity expiries, Great Lakes has an additional 110 MDth/d of short haul capacity under contract expiring on October 31, 2010. The cost and revenue study filed by Great Lakes with the FERC on February 4, 2010 reflects the increased risk of de-contracting on the Great Lakes system. Great Lakes is discounting transportation capacity as needed to optimize revenue. Refer to Item 7. "Management's Discussion and Analysis of Financial Condition and Results of Operations" for further discussion.

Northern Border – For the year ended December 31, 2009, Northern Border's average contracted capacity compared to design capacity was 68 per cent. Some of this capacity was sold at a discount to maximize overall revenue on the Port of Morgan, Montana to the Ventura and Harper, Iowa portions of the pipeline. As of January 31, 2010, Northern Border had long-term firm transportation contracts for 69 per cent of its design capacity in the first quarter of 2010, decreasing to 36 per cent beginning in the second quarter of 2010 following contract maturities. The weighted average remaining contract life at January 31, 2010 was 1.9 years. Northern Border expects to continue to discount transportation capacity as needed to optimize revenue. Refer to Item 7. "Management's Discussion and Analysis of Financial Condition and Results of Operations" for further discussion.

Shippers on the Bison Pipeline project, a project sponsored by TransCanada, have executed 10 year contracts for approximately 407 MMcf/d of capacity on the Northern Border system from Port of Morgan, Montana to Ventura, Iowa, commencing on the in-service date of the Bison Pipeline project. If the Bison Pipeline project is completed, this would increase Northern Border's average contracted capacity and weighted average contract life.

North Baja – Due to North Baja's bi-directional nature, it has the ability to accept receipts at both ends of its system. North Baja's average contracted capacity for the year ended December 31, 2009 was 79 per cent of southbound capacity and 64 per cent of northbound capacity. As at January 31, 2010, North Baja had long-term firm transportation contracts for 79 per cent of its capacity for southbound receipts and 64 per cent of its capacity for northbound receipts, with a combined weighted average remaining life of the contracts of 16.7 years.

Tuscarora – Tuscarora's average contracted capacity for the year ended December 31, 2009 was 99 per cent. Tuscarora had long-term firm transportation contracts for approximately 97 per cent of its design capacity with a weighted average remaining contract life of 10.6 years, as at January 31, 2010.

REGULATORY ENVIRONMENT

Government Regulation

Great Lakes, Northern Border, North Baja and Tuscarora are regulated under the Natural Gas Act of 1938, Natural Gas Policy Act of 1978, and Energy Policy Act of 2005, which give the FERC jurisdiction to regulate virtually all aspects of their businesses, including:

26 TC PIPELINES, LP

- •

- transportation

of natural gas;

- •

- rates

and charges;

- •

- terms

of service and service contracts with customers, including creditworthiness requirements;

- •

- certification

and construction of new facilities;

- •

- extension

or abandonment of service and facilities;

- •

- accounts

and records;

- •

- depreciation

and amortization policies;

- •

- acquisition

and disposition of facilities;

- •

- initiation

and discontinuation of services; and

- •

- standards of conduct for business relations with certain affiliates.

Rate Proceeding, Great Lakes – On November 19, 2009, the FERC issued an order in FERC Docket No. RP10-149 (November 2009 Order) instituting an investigation pursuant to Section 5 of the Natural Gas Act (GL Rate Proceeding). The FERC alleged, based on a review of certain historical information, that Great Lakes' revenues might substantially exceed Great Lakes' actual cost of service and therefore may be unjust and unreasonable. On February 4, 2010, Great Lakes filed a cost and revenue study (GL Cost and Revenue Study) in response to the November 2009 Order. The GL Cost and Revenue Study supports Great Lakes' current rates, and shows that if Great Lakes filed to reset its rates, these rates should be above Great Lakes' current rates. The GL Cost and Revenue Study reflects the increased risk of de-contracting on the Great Lakes system which may result in decreases to overall long-term, daily and short-term firm transportation revenues, and interruptible transportation revenues, as compared to prior periods.