Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark one)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended December 31, 2009. |

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from to |

Commission file number: 0-21918

FLIR Systems, Inc.

(Exact name of registrant as specified in its charter)

| Oregon | 93-0708501 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

| 27700 SW Parkway Avenue, Wilsonville, Oregon | 97070 | |

| (Address of principal executive offices) | (Zip code) | |

Registrant’s telephone number, including area code: (503) 498-3547

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class |

Name of Each Exchange on Which Registered | |

| Common Stock, $0.01 par value |

NASDAQ Global Select Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or amendment to this Form 10-K. ¨

Indicate by checkmark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one)

Large accelerated filer x Accelerated filer ¨

Non-accelerated filer ¨ Smaller reporting company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

As of June 30, 2009, the aggregate market value of the shares of voting and non-voting stock of the registrant held by non-affiliates was $3,346,287,508.

As of February 12, 2010, there were 152,875,172 shares of the registrant’s common stock, $0.01 par value, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE:

The registrant has incorporated by reference into Part III of this Form 10-K, portions of its Proxy Statement for its 2010 Annual Meeting of Shareholders.

FLIR Systems, Inc.

FORM 10-K

ANNUAL REPORT

TABLE OF CONTENTS

i

Forward-Looking Statements

This Annual Report on Form 10-K (the “Report”), including “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Item 7 contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 regarding future events and the future results of FLIR Systems, Inc. and its consolidated subsidiaries (“FLIR” or the “Company”) that are based on management’s current expectations, estimates, projections and assumptions about the Company’s business. Words such as “expects,” “anticipates,” “intends,” “plans,” “believes,” “sees,” “estimates” and variations of such words and similar expressions are intended to identify such forward-looking statements. These statements are not guarantees of future performance and involve risks, uncertainties and assumptions that are difficult to predict. Therefore, actual outcomes and results may differ materially from what is expressed or forecasted in such forward-looking statements due to numerous factors including, but not limited to, those discussed in “Risk Factors” in Item 1A, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Item 7, and elsewhere in this Report as well as those discussed from time to time in the Company’s other Securities and Exchange Commission filings and reports. In addition, such statements could be affected by general industry, economic and market conditions. Such forward-looking statements speak only as of the date of this Report or, in the case of any document incorporated by reference, the date of that document, and we do not undertake any obligation to update any forward-looking statement to reflect events or circumstances after the date of this Report, or for changes made to this document by wire services or Internet service providers. If we update or correct one or more forward-looking statements, investors and others should not conclude that we will make additional updates or corrections with respect to other forward-looking statements.

PART I

| ITEM 1. | BUSINESS |

General

We are a world leader in the design, manufacture and marketing of thermal imaging systems. Our products are used in a wide variety of applications in commercial, industrial and government markets worldwide. We offer a variety of system configurations to suit specific customer requirements. In 2009, our business was organized into three divisions: Thermography, Commercial Vision Systems and Government Systems.

Thermography products are generally sold for commercial and industrial applications, typically where imaging and temperature measurement together are required. Products range from highly sensitive cameras with extensive analytic capabilities and sophisticated image processing to less expensive cameras offering excellent performance and value for less demanding applications. Our Thermography products range in price from $2,000 for an inexpensive hand-held camera to over $150,000 for our most sophisticated science cameras. Our strategies in this business are to continue to develop products for high-end applications while introducing new products at lower price points, and to capitalize on highly price-elastic demand in numerous emerging markets. Revenue from Thermography has grown at a compound annual rate of 15 percent since 2001 and was $285.5 million or 25 percent of consolidated revenue in 2009.

Commercial Vision Systems (“CVS”) is focused on emerging commercial markets for infrared imaging technology where the primary need is to see at night or in adverse conditions, such as through smoke or light fog. As the cost of infrared technology has declined, demand in large untapped markets such as commercial security, automotive, marine, airborne and first responder markets has grown rapidly. CVS has focused its efforts on expanding distribution, accelerating design cycles, reducing manufacturing costs and providing excellent customer service in these markets. Our infrared sensor business, which sells focal plane arrays and camera cores internally as well as to third parties on an original equipment manufacturer (“OEM”) basis, is also a part of CVS. CVS products range in price from under $1,000 for an OEM imaging core to more than $300,000 for a high definition airborne system. Since 2005, CVS revenue has grown at a compound annual rate of 25 percent. CVS revenue was $206.3 million or 18 percent of our consolidated revenue in 2009.

1

Government Systems (“GS”) is focused on government customers and markets where very high performance is required. Typical applications include surveillance, force protection, drug interdiction, search and rescue, special operations and target designation. We address these markets through either a commercial, off-the-shelf (“COTS”) model or a commercially developed, military qualified (“CDMQ”™) model. Products developed under the COTS model are applicable to a range of government customers and markets, including military applications. CDMQ products are specifically designed to meet military specifications. In both the COTS and CDMQ product development models, we use internally generated funds for research and development, and generally own all rights to the products and their design. We have continued to increase our emphasis on CDMQ as a development strategy, and it is a growing part of our GS business. We also periodically accept government funded design and development contracts. GS products are often customized for specific applications and frequently incorporate additional sensors, including visible light cameras, low light cameras, laser rangefinders, laser illuminators and laser designators. GS products range in price from under $10,000 for certain hand-held and weapon-mounted systems to over $1 million for our most advanced stabilized laser designation systems. Since 2005, GS revenue has grown at a compound annual rate of 28 percent. GS is our largest division with 2009 revenue of $655.3 million, or 57 percent of consolidated revenue in 2009.

On December 10, 2009, we announced that the Company would consolidate its Commercial Vision Systems and Thermography divisions into one unit, the Commercial Systems division, effective January 1, 2010. The new division will continue to focus on the large potential for growth in commercial and industrial markets, and will create value from commonality in distribution, customers and strategic product development focused on uncooled infrared technology. For 2010, however, we will continue to report the financial results of the former Commercial Vision Systems division and Thermography division as we undergo the transition of consolidating these two segments. As we expect Thermography and Commercial Vision Systems to be substantially consolidated by the end of 2010, we expect to report the financial results for Commercial Systems as a single segment in 2011.

For additional information concerning the Company’s three divisions, including revenues from external customers, earnings from operations and total assets by segment, see Note 17 to the Consolidated Financial Statements in Item 8.

FLIR Systems, Inc. is an Oregon corporation and was incorporated in 1978. The Company’s headquarters are located at 27700 SW Parkway Avenue, Wilsonville, Oregon 97070-8238, and the telephone number at this location is (503) 498-3547. Information about the Company is available on our website at www.flir.com.

Infrared Technology Overview

Infrared is a portion of the electro-magnetic spectrum that is adjacent to the visible spectrum, but is invisible to the human eye due to its longer wavelengths. Unlike visible light, infrared radiation (or heat) is emitted directly by all objects above absolute zero in temperature. Thermal imaging systems detect this infrared radiation and convert it into an electronic signal, which is then processed into a video signal and displayed on a video screen. Thermal imaging systems are different than other types of “low light” vision systems, such as visible light intensification used in night vision goggles. Infrared imaging systems are not adversely affected by the presence of visible light, so they can be used day or night, and are not susceptible to rapid changes in visible light levels. Since infrared systems are detecting emitted infrared radiation, they are passive and thus more covert than certain “illuminated” systems. Additionally, thermal imaging systems can measure very small temperature differences, a critical feature for a variety of commercial, industrial and scientific applications.

An infrared detector, which collects or absorbs infrared radiation and converts it into an electronic signal, is the primary component of thermal imaging systems. The two types of infrared detectors we manufacture and use in our systems are often referred to as “cooled” and “uncooled.” Cooled detectors utilize a mechanical micro-cooler to reduce the operating temperature of the infrared sensor to -200° C, and offer high sensitivity and resolution for long-range applications or those requiring high measurement precision. These systems, while more

2

sensitive and thus able to see farther, result in a product that is more expensive, heavier, more complex and uses more power than those using uncooled detectors. Uncooled detectors operate at room temperature and thus do not require a micro-cooler, resulting in products that are lighter, use less power and are less expensive to produce than cooled systems. While the performance of uncooled detectors is improving, uncooled detectors are still less sensitive than cooled detectors. The cost of both types of detectors is declining and we expect to continue reducing costs as volumes rise and the technology improves in the future. We currently expect demand for both types of systems to increase.

Products and Markets

Thermography. The Thermography market has traditionally addressed thermal imaging applications where both imaging and temperature measurement are required. This market has grown in size and breadth as prices have declined, volumes have increased and new applications have emerged. Over the past several years, markets have grown rapidly and expanded beyond the traditional industrial predictive and preventive maintenance segments. We expect new markets to continue to develop in the future. Key end-user markets include:

| Predictive Maintenance |

Thermal imaging systems are used for monitoring the condition of mechanical and electrical equipment. Such monitoring assists our customers in identifying equipment faults (manifested as hot spots) so they can be repaired before they fail. This increases equipment productivity and avoids catastrophic failures or major damage, which reduces operating expenses by lowering repair costs and reducing downtime. Improved functionality of image analysis software, smaller size and weight, and simplicity of system operation are critical factors for this well established market segment. |

| Research & Development |

Infrared’s unique ability to detect very small differences in temperature while detailing complex thermal dynamics and patterns makes Thermography systems a useful tool in a wide variety of research and development applications. Our systems provide the ability to view thermal distribution in real time for products ranging in size from small hybrid integrated circuits to jet engines. Common applications include product development of microelectronics, cell phones, laptop computers, telecommunications equipment, consumer appliances, automotive components and aircraft engines. Systems used in research and development applications typically require very high imaging performance and measurement precision, coupled with extensive analysis and reporting software. We have a complete line of both cooled and uncooled infrared imagers specifically designed for high-end research and development applications. |

| Manufacturing Process Control |

Thermal imaging applications for manufacturing process control include applications where temperature consistency is critical, including monitoring the quality of metal, plastic and glass cast parts, which are highly dependent upon the temperature distribution in the mold; monitoring the quality of paper, which is dependent upon proper and even moisture distribution during the drying process; and monitoring the quality of products such as rubber gloves, which can be thermally examined to locate abnormally warm or cool spots, indicating non-uniform thickness that may result in a quality defect. |

| Building Inspection |

Infrared imagers can detect missing insulation, electrical faults, water intrusion, pest infiltration, gauge energy efficiency, and help detect |

3

| the presence of moisture. Market segments include building diagnostics, energy auditing and home inspection, property and facility management, HVAC and plumbing, and moisture and restoration. This market has grown rapidly as costs have declined and new uses for thermal imaging systems have emerged. Building inspection represents the largest single Thermography market for us in 2009. |

| Gas Detection |

Specially designed infrared systems can detect and image hydrocarbon gas emissions or leaks. Using this technology, we have established a market focused on leak detection at gas production, transmission and storage locations, as well as compliance monitoring by environmental and other regulatory agencies. New applications are emerging for this technology. For example, we now have a system that detects sulfur hexafluoride, a dangerous pollutant and potential fire hazard used as an insulator in electrical transformers. During 2008, the United States Environmental Protection Agency (“EPA”) modified its rules to allow optical gas imaging systems such as ours to be used in place of toxic vapor analyzers for the detection of gas leaks under leak detection programs required by the EPA. |

| Emerging Markets |

Over the past seven years, we have successfully introduced progressively lower priced thermal imaging systems that have enabled us to expand traditional Thermography markets and open new markets for our products. These products, the latest of which is the i-family, have met with strong market acceptance in the lower-end building and electrical inspection markets, and we expect additional market segments for thermal imaging to develop as prices continue to decline. These market segments may include healthcare and screening, food service and distribution, veterinary science, automotive care, aircraft inspection, and maritime vessel inspections. |

| Training |

We offer fee-based training on the principles of thermography and the use of our products through ITC®, our Infrared Training Center, which provides comprehensive instruction, training, certification and applications engineering from several FLIR locations or at the customer’s site. We also license Infrared Training Centers to qualified third parties in certain countries. In 2009, nearly 11,000 people received training at our Infrared Training Centers worldwide. |

Commercial Vision Systems. Commercial Vision Systems is focused on commercial markets where the primary need is to see at night and in adverse conditions. While these markets are broad and growing rapidly, they exhibit low penetration of infrared technology and require distinct distribution channels. As in Thermography, price elasticity of demand is high, and as prices fall further, we expect sales volumes to continue to increase. CVS is focused on expanding its product line and building distribution channels. Significant markets for CVS products today include:

| Security and Surveillance |

Thermal imaging systems have been used for surveillance and perimeter security of government, military and industrial facilities for many years. Over the past few years, we have introduced a series of lower priced, purpose built systems targeted at the commercial security market and are actively expanding distribution in this market. |

4

| Our security products are now being used to protect critical infrastructure, ports, borders, commercial sites, and residential homes. Demand for security systems utilizing thermal imaging technology is growing rapidly across all segments. |

| Automotive Night Vision |

Since 2001, we have worked with Autoliv Electronics, a major supplier of safety equipment to the automotive industry, to offer a night vision system for passenger automobiles. Since late 2005, BMW has offered a night vision system utilizing our camera as an option in their 5-, 6-, and 7-Series automobiles. The system provides drivers with the ability to see at night and through obscurants, such as fog, at distances much further than can be seen with traditional headlights. In late 2008, the second generation of the BMW night vision system, which incorporates significant improvements, including a pedestrian warning system, was introduced on the 7-Series automobiles. In late 2009, both Audi and Rolls Royce introduced night vision systems utilizing this technology. Together with Autoliv, we expect to continue to expand the technology into new makes and models over the next several years. |

| Other Transportation Night Vision |

We are actively promoting our products in other transportation markets, such as trucks, trains, recreational vehicles and first responder vehicles, as well as aftermarket sales in the automotive market. These markets are in the early stages of adoption of infrared technology but we believe they offer significant future growth opportunities. |

| Marine |

In 2006, we introduced the first cost-effective infrared device specifically designed for recreational boating, cruise lines, commercial fishing and merchant marine vessels, ferries, and other maritime markets. Since then we have aggressively expanded distribution through a combination of direct sales and a network of dealers. In 2009, we launched a new line of maritime products that enhances the breadth of our product line. |

| Law Enforcement |

We are a leader in the supply of stabilized airborne thermal imaging systems for federal, state and local law enforcement agencies. Agencies with this type of equipment have the ability to track suspects, locate lost persons and provide situational awareness to officers on the ground. We also offer low cost, hand-held systems to the law enforcement market. These cameras provide a light weight, cost-effective, high performance tool for police officers and other law enforcement professionals to conduct search and rescue, surveillance, or pursuit missions. |

| OEM Markets |

We supply cooled and uncooled camera cores, sensors and readout integrated circuits on an OEM basis for a broad range of applications where customers require a product at a lower level of integration than a fully developed thermal imaging system. Examples of major customers in this segment are Mine Safety Appliances, Inc. (firefighting); Bullard (firefighting); Aerovironment, Inc. (unmanned aerial vehicles); Northrop Grumman Corporation (cooled cores for |

5

| military applications); Hologic (readout integrated circuits for digital X-ray); and various makers of security systems worldwide. |

Government Systems. Government Systems focuses on providing enhanced vision capabilities to a wide variety of military, paramilitary, law enforcement, public safety and other government customers. Our systems typically provide the capability to see over long distances, day or night, through adverse weather conditions and from a wide variety of vehicle, man portable and fixed installation platforms. Currently, the majority of our infrared imaging systems use cooled technology to identify objects from long distances; however, uncooled thermal imaging systems are growing rapidly in certain markets such as weapon sights, hand-held monoculars/binoculars, military vehicles and unmanned aerial vehicles. Many of our markets require systems that operate in demanding environments such as extreme climatic conditions, battlefield and military environments or maritime conditions. Systems are often installed onto larger platforms and must be able to integrate with such other systems as aircraft avionics, radars, laser systems and large, broad-based security networks.

Government Systems offers a very wide array of products across multiple markets. For airborne applications, we have developed highly stabilized platforms, known as gimbals, which typically contain multiple payloads in addition to the infrared imaging system, as well as sophisticated software and analytic capabilities. For land applications, we manufacture three types of products: hand-held products, platform mounted products and targeting products. Platform mounted units are typically housed in a weather-tight enclosure and feature remote control capabilities and multi-sensor integration capability (e.g., closed circuit TV, laser rangefinder, compass or global positioning system). Hand-held ground products are ruggedized and have optional lenses and target location capabilities. Ground-based targeting products are designed to attach to existing daylight sights to provide bore-sighted, nighttime capabilities. For maritime applications, we manufacture shipborne products which are similar to our airborne gimbals, but are inverted and customized for the marine environment.

The Government Systems market primarily consists of the following end-user market segments:

| Search and Rescue |

Thermal imaging systems are used in airborne and shipborne search and rescue missions to rescue individuals in danger or distress on boats or vehicles, or lost in adverse conditions. Such systems are in use today by organizations such as the United States Coast Guard, the United States Marine Corps, the United States Air National Guard and the United Kingdom Ministry of Defense. |

| Force Protection |

In instances where military or other personnel are deployed in hostile areas, thermal imaging systems mounted on towers or other platforms are deployed to identify and defeat potential threats at an early stage. Our systems are deployed for this purpose by the United States Army, United States Marine Corps and others worldwide. |

| Border and Maritime Patrol |

Thermal imaging systems are used in airborne, shipborne, hand-held and fixed installation applications for border and maritime surveillance, particularly at night, to enforce borders and coastal waters, to monitor national fishing boundaries and to prevent smuggling. Our cameras are currently deployed along numerous borders worldwide, including in the United States, Europe and the Middle East. |

| Surveillance and Reconnaissance |

Thermal imaging systems are used in surveillance and reconnaissance applications for the precise positioning of objects or people from substantial distances and for enhanced situational awareness, particularly at night or in conditions of reduced or obscured visibility. |

6

| These systems are installed on fixed platforms, manned mobile platforms, and unmanned aerial vehicles. |

| Targeting |

We offer several products that provide precise target location and designation capabilities in this application ranging from a clip-on rifle scope device to high-precision, stabilized, airborne laser designator systems. |

| Federal Drug Interdiction |

Thermal imaging systems enable government agencies to expand their drug interdiction and support activities by allowing greater surveillance and detection capabilities. Our systems are in use by the United States Customs Service, the United States Drug Enforcement Agency and the United States Federal Bureau of Investigation, as well as by international government agencies. |

Our Government Systems contracts and subcontracts are subject to certain risks related to doing business with the United States government and may be subject to termination, reduction and/or amendment at the election of the United States government. For a discussion of these risks, see sections “We depend on the United States government for a material portion of our business and changes in government spending could adversely affect our business” and “As a United States government contractor, we are subject to a number of procurement rules and regulations” in Item 1A “Risk Factors.”

Mergers and Acquisitions

Since 2003, we have made a total of eleven acquisitions. Most recently, we acquired Salvador Imaging, Inc. (“Salvador”) in June 2009, OmniTech Partners, Inc. (“OmniTech”) in October 2009, and Directed Perception, Inc. (“Directed Perception”) in December 2009. The Salvador acquisition expands our capabilities to include low-light electron multiplying charge coupled device cameras which can be integrated into many of our multi-sensor systems for government applications, and has significant potential for stand-alone applications. The OmniTech acquisition adds image intensified capability to our product line, and creates the opportunity to leverage our capabilities to expand in the growing market for fused image intensified/thermal imagers. The Directed Perception acquisition enhances and differentiates our pan-tilt-zoom camera systems for both commercial and military markets through lower cost, improved functionality, and ease-of-use.

We are selective in our acquisition strategy, seeking to make acquisitions that are strategically important and generally add to our technology, distribution network or product portfolio. We are continuously evaluating opportunities for additional acquisitions, but cannot predict the timing, size or nature of any future activity.

Technology and Core Competencies

We use our expertise in product design, infrared imagers, optics, lasers, image processing, systems integration and other technologies, to develop and produce sophisticated thermal and multi-sensor imaging systems. We integrate the following capabilities and disciplines into our manufacturing processes:

| System Design and Integration |

We have developed extensive competencies in the design and integration of numerous capabilities and payloads into integrated systems or sub-systems. Competencies such as stabilization, packaging and systems integration allow us to effectively combine a wide variety of technologies and payloads to design and manufacture complex systems to suit our customers’ needs. |

7

| Radiometry |

Our ability to produce thermal imaging systems that can accurately measure temperature is critical in many of our Thermography markets. We have demonstrated know-how in designing and producing systems that can measure temperature to within very precise tolerances while maintaining accuracy and stability over time and over a wide range of ambient temperatures. We believe our skills in this area, known as radiometry, offer an important competitive advantage over many of our competitors. |

| Mechanical Engineering |

Our design and production of thermal imaging systems involves highly sophisticated mechanical engineering techniques, particularly in the design and assembly of the supporting structures for system components such as detector arrays, coolers, scanners and optics. We also have expertise in designing stabilized assemblies used in our gimbal mounted products utilizing electro-mechanical control, gyroscopes and electronic stabilization, and specialized control mechanisms. |

| Infrared Detector Design and Manufacturing |

We design and manufacture both cooled and uncooled infrared detector arrays, in high volumes and at low cost. We believe our uncooled vanadium oxide microbolometers and cooled detectors using indium antimonide and indium gallium arsenide are among the highest performing infrared detectors of their type available in the world. Internal design and manufacturing of detectors provides significant cost and engineering advantages compared with the use of third-party detectors. |

| Integrated Circuits and Electronic Design |

We have significant electronic design capabilities across several specialized areas, including readout integrated circuit design, signal processing, image processing and electronics integration. Our design expertise lies in the areas of reliability, low power consumption and extreme environmental survivability. |

| Software Development |

Software is an increasingly important aspect of our overall engineering and design activity. We offer networking capability, video analytics and other software and middleware inside many of our camera systems, and such applications are growing in importance. Our systems are also able to interface with many standard external software protocols. |

| Motion Control Systems |

Our recent acquisition of Directed Perception added significantly to our motion control system design and manufacturing capabilities. In addition to highly accurate stabilized gimbaled systems for airborne and other applications, we also offer a line of high precision, repeatable pan and tilt systems for use with a wide variety of payloads. |

| Optical Design, Fabrication and Coating |

We design and manufacture sophisticated infrared optics using materials such as silicon and germanium that are required to produce a thermal imaging system. This capability allows us to rapidly develop optics optimized for use with our cameras and avoid costs and delays associated with reliance on third-party optics suppliers. |

8

| We also have the ability to apply custom vapor deposited coatings to improve the transmission of the unique lens materials that are used in infrared systems. |

| Micro-Coolers |

We manufacture the industry’s smallest, lightest and lowest power micro-coolers for use in cooling infrared detectors. Our coolers are especially effective in hand-held applications, where light weight and long battery life are essential. |

| Lasers and Laser Components |

Many of our more sophisticated systems are increasingly being offered with various types of laser payloads, including pointers, illuminators, rangefinders and designators. We design and manufacture purpose-built laser rangefinders and designators for inclusion in some of our gimbaled systems. We also manufacture certain laser-related components for customers. |

Internally funded research and development expenses were $91.3 million in 2009, $90.0 million in 2008 and $72.5 million in 2007. We anticipate that we will continue to have significant internal research and development expenses in the future to provide a continuing flow of innovative and high quality products to maintain and enhance our competitive position in each of our business segments.

Proprietary Rights

We have numerous patents, trademarks, trade secrets and other intellectual property that are important for our success. We rely on a combination of patent, trademark and trade secret laws, confidentiality agreements and contractual provisions to protect our proprietary rights. Our intellectual property provides important competitive advantages, and we are increasing our efforts to document and protect our intellectual property from misappropriation. We cannot, however, be certain or give any assurance that we can maintain our competitive advantage in the thermal imaging industry or that competitors will not develop similar or superior capabilities.

Customers

The primary customers for our products vary substantially by division. Typical Thermography customers include research and development facilities, universities, industrial companies, utility companies, building inspectors, electrical contractors, thermography consultants, damage restoration contractors and numerous commercial enterprises. Commercial Vision Systems serves customers such as OEMs, automotive suppliers, aircraft manufacturers and dealers, marine electronics dealers, major integrators of security systems and news gathering agencies. Government Systems customers generally consist of United States and international government agencies, including military, paramilitary and police forces, as well as defense contractors and aircraft manufacturers. Our customers in each segment are located around the world and are serviced by a global distribution and service organization.

A substantial portion of our revenue is derived from sales to United States and international government agencies and our business will continue to be substantially dependent upon such sales. Aggregate sales to United States government agencies accounted for 43 percent of our revenue in 2009, 41 percent in 2008 and 39 percent in 2007.

Sales to customers outside the United States accounted for 41 percent of our revenue in 2009, 38 percent in 2008 and 39 percent in 2007. We expect revenue outside the United States to continue to account for a significant portion of our total revenue. Further information about geographic operations and customers appears in Note 17 to the Consolidated Financial Statements in Item 8.

9

Sales and Distribution

We believe our sales and distribution organization is among the largest in the industry and effectively covers the world with a combination of direct sales, independent representatives and distributors, dealers, application engineers, and service and training centers. Our sales personnel, including third-party distributors, undergo a comprehensive training program on each product’s technical specifications, functions and applications. We also continuously update our training programs to incorporate technological and competitive shifts and changes. We sell in many distinct markets and have established specific sales channels for each market.

We sell our Thermography products worldwide through a direct sales staff and a network of distributors and representatives. Our Thermography business continues to expand distribution, particularly in Asia and Latin America. At the end of 2009, our Thermography division employed over 190 direct sales personnel and utilized approximately 500 distributors. In November 2007, we acquired Extech Instruments Corporation, a distributor of hand-held test equipment. We are utilizing its distribution channels, particularly into catalogs and retailers to expand our distribution in the United States. In January 2008, we acquired Cedip Infrared Systems (“Cedip”) which has provided additional distribution capability, particularly in international markets.

Commercial Vision Systems is also actively expanding its distribution network by hiring additional direct sales personnel and expanding third-party distribution networks in specific markets. At the end of 2009, our Commercial Vision Systems sales organization employed approximately 70 direct sales personnel as well as a worldwide network of dealers across many distinct markets. In certain markets, CVS has chosen to supply camera cores on an OEM basis to companies with well established distribution networks. Examples include firefighting, where we supply cores to Mine Safety Appliances, Inc. and Bullard, and automotive, where we are partnered with Autoliv Electronics.

Our Government Systems business has a direct sales staff of approximately 80 individuals and a network of independent representatives and distributors covering major government markets worldwide. Included in this total are technical and customer support staff in the United States and Europe who provide application development, technical training and operational assistance to direct and indirect sales personnel as well as to customers.

Marketing

With our further expansion into the low cost segment of the commercial markets, we have developed greater competencies in market research, electronic marketing, marketing communications and business development. Our ability to identify new markets, adapt our product solutions to meet unique market needs, quickly develop marketing communications that highlight these unique features, and leverage existing and new distribution channels to develop incremental business are important aspects of our marketing and communications efforts.

We focus our product marketing activities on internet promotion, advertising, direct mail, press tours, technical articles for publications and participation in most major trade shows in our industry. These activities give us the opportunity to educate potential customers about the key features and attributes of our products and how they may be used to address specific customer needs.

Customer Service

We maintain service facilities at most of our facilities worldwide. Each of our service facilities has the capability to perform the complex calibrations required to service thermal imaging systems. We also maintain field service capabilities under the direction of our independent representatives or distributors in five locations outside the United States.

10

Manufacturing

We manufacture many of the critical components for our products, including infrared detectors, gimbals, pan-tilts, optics and coatings, laser sub-systems and micro-coolers, and develop much of the necessary software and middleware for our systems. This vertical integration minimizes lead times, facilitates prompt delivery of our products, controls costs and ensures that these components satisfy our quality standards. We purchase other parts pre-assembled, including certain detectors, certain coolers and optics, circuit boards, cables and wire harnesses. These purchased and manufactured components are then assembled into finished systems and tested at one of our primary production facilities located in Wilsonville, Oregon; North Billerica, Massachusetts; Goleta, California; Danderyd, Sweden; Croissy-Beaubourg, France; Tallinn, Estonia; Bozeman, Montana; Colorado Springs, Colorado; Freeport, Pennsylvania; and Burlingame, California.

Our manufacturing operations are, from time to time, audited by certain OEM customers, which include several major aircraft manufacturers, and have been certified as meeting their quality standards. Our facilities in Wilsonville, North Billerica, Goleta, Danderyd, Croissy-Beaubourg, Tallinn, Bozeman and West Malling, UK are ISO 9001:2000 certified. Our facilities in Colorado Springs and Freeport are ISO 9001:2008 certified.

Backlog

At December 31, 2009 and 2008, we had a total order backlog of $563 million and $663 million, respectively. Government Systems typically has the highest backlog of our divisions relative to revenue and in absolute terms. At December 31, 2009, Government Systems backlog totaled $433 million, compared with $552 million at December 31, 2008. The decline in Government Systems backlog is primarily due to significant deliveries in 2009 on the United States Army and Marine Corps BETTS-C program. Commercial Vision Systems carries backlog in certain markets, but is less backlog dependent than Government Systems. Commercial Vision Systems backlog at year end 2009 was $103 million, compared with $91 million a year earlier. Thermography is our least backlog intensive business, and typically ships products within a few weeks of receipt of orders. At December 31, 2009, Thermography backlog was $27 million, compared with $20 million a year earlier. Backlog is defined as orders received for products or services for which a sales agreement is in place and delivery is expected within twelve months.

Competition

Competition in the market for thermal imaging equipment is significant. We believe that the principal competitive factors in our market are product performance, price, customer service and training, product reputation, and effective marketing and sales efforts. Our competitors are different in each market segment. In the Thermography market, principal competitors include Fluke (a division of Danaher Corporation) and NEC San-Ei. Competitors in Commercial Vision Systems vary market by market, but include L-3 Communications, ULIS, Axsys Technologies (a General Dynamics company) and numerous smaller companies. In the Government Systems market, our competitors include Raytheon Corporation, BAE Systems, L-3 Communications, DRS Corporation (a Finmecanica Company), Lockheed Martin Corporation, El-Op, Sagem, Tamam and Thales. Many of these competitors have substantially greater financial, technical and marketing resources than we do.

Employees

As of December 31, 2009, we had 2,079 employees of which 1,360 were located in the United States and 719 were located outside of the United States. We have generally been successful in attracting highly skilled technical, marketing and management personnel. None of our employees in the United States is represented by a union or other bargaining group. Certain employees in Sweden are represented by unions whose contracts are subject to periodic renegotiations. We believe our relationships with our employees and unions are good.

11

Available Information

Our internet website address is www.flir.com. This Report, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 and other required filings are available through our internet website as soon as reasonably practicable after we electronically file such material with, or furnish it to, the Securities and Exchange Commission. Our internet website and the information contained therein or connected thereto are not intended to be incorporated into this Report.

| ITEM 1A. | RISK FACTORS |

The following are important factors that could cause actual results or events to differ materially from those contained in any forward-looking statements made by or on behalf of the Company. In addition, the risks and uncertainties described below are not the only ones we face. Unforeseen risks could arise and problems or issues that we now view as minor could become more significant. If we are unable to adequately respond to these risks and uncertainties, our business, financial condition and results of operations could be materially adversely affected. Additionally, we cannot be certain or give any assurance that any actions taken to reduce known risks and uncertainties will be effective.

General economic conditions may adversely affect our business, operating results and financial condition

Our operations and performance depend significantly on worldwide economic conditions and their impact on levels of capital investment and consumer spending and the recent worldwide recession has negatively impacted demand in many of our markets. These markets may remain weak, or be subject to further deterioration. Economic factors that could adversely influence demand for the Company’s products include continued uncertainty about current global economic conditions leading to reduced levels of investment, changes in government spending priorities, the size and availability of government budgets, customers’ and suppliers’ access to credit, consumer confidence and other macroeconomic factors affecting government, industrial or consumer spending behavior.

Our primary markets are volatile and unpredictable

Our business depends on the demand for our thermal imaging systems in a variety of commercial, industrial and government markets. In the past, the demand for our products in these markets has fluctuated due to a variety of factors, some of which are beyond our control, including:

| • | the timing, number and size of orders from, and shipments to, our customers, as well as the relative mix of those orders; |

| • | variations in the volume of orders for a particular product or product line in a particular quarter; |

| • | the size and timing of new contract awards; |

| • | the timing of the release of government funds for procurement of our products; and |

| • | the timing of orders and shipments within a given fiscal quarter. |

Seasonal fluctuations in our operating results, particularly the increase in sales we generally experience in the fourth quarter, result from:

| • | the seasonal pattern of contracting by the United States government and certain foreign governments; |

| • | the frequent requirement of international customers to take delivery of equipment prior to January due to funding considerations; and |

| • | the tendency of commercial enterprises to fully utilize annual capital budgets prior to expiration. |

12

We depend on the United States government for a material portion of our business and changes in government spending could adversely affect our business

We derive significant revenue from contracts or subcontracts with United States government agencies. A significant reduction in the purchase of our products by these agencies would have an adverse effect on our business. For the fiscal years ended December 31, 2009, 2008 and 2007, approximately 43 percent, 41 percent and 39 percent, respectively, of our revenues were derived directly or indirectly from contracts with the United States government and its agencies. Recently, a higher percentage of our contracts have been larger Indefinite Delivery, Indefinite Quantity (“IDIQ”) contracts. The funding of contracts awarded to us depends on the overall United States government budget and appropriation process, which is beyond our control. In addition, at its discretion, the United States government may change its spending priorities and/or terminate, reduce or modify contracts.

As a United States government contractor, we are subject to a number of procurement rules and regulations

Government contractors must comply with specific procurement regulations and other requirements and are subject to routine audits and investigations by United States government agencies. If we fail to comply with these rules and regulations, the results could include: reductions in the value of contracts; contract modifications or termination; the assessment of penalties and fines; and/or suspension or debarment from government contracting or subcontracting for a period of time or permanently.

Our future success will depend on our ability to respond to the rapid technological change in the markets in which we compete, our ability to introduce new or enhanced products and enter into new markets

The markets in which we compete, including the thermal imaging industry, are characterized by rapid technological developments and frequent new product introductions, enhancements and modifications. Our ability to develop new products and technologies that anticipate changing customer requirements, reduce costs and otherwise retain or enhance our competitive position in existing and new markets will be an important factor in our future results from operations. We will continue to make substantial capital expenditures and incur significant research and development costs to improve our manufacturing capability, reduce costs, and develop and introduce new products and enhancements. If we fail to develop and introduce new products and technologies in a timely manner, our business, financial condition and results of operations would be adversely affected. In addition, we cannot be certain that our new products and technologies will be successful or that customers will accept any of our new products.

We must successfully manage an increasingly complex global organization

As the Company has grown, the size and scope of the Company’s worldwide operations have also increased substantially. Worldwide operations have grown to accommodate the design, manufacture and marketing of numerous product lines across all of our divisions in a vertically integrated manufacturing environment. Significant management time and effort is required to effectively manage the increased complexity of the business. In December 2009, we announced a reorganization whereby we would consolidate the Thermography Division and the Commercial Systems Division into one division, called Commercial Systems, effective January 1, 2010. Our failure to successfully manage the global operations and integration of the two divisions could have a material adverse effect on our business, financial condition and results of operations. In addition, we manufacture our products at various facilities as described in Item 2. Our inability to continue to manufacture our products at one or more of our facilities as a result of, for example, a prolonged power outage, earthquake, fire or other natural disaster, or labor or political unrest, could prevent us from supplying products to our customers and could have a material adverse effect on our business, financial condition and results of operations.

We face risks from international sales and business activities

We market and sell our products worldwide and international sales have accounted for, and are expected to continue to account for, a significant portion of our revenue. For the years ended December 31, 2009, 2008 and

13

2007, international sales accounted for 41 percent, 38 percent and 39 percent, respectively, of our total revenue. We also manufacture certain products and subassemblies in Europe. Our international business activities are subject to a number of risks, including:

| • | the imposition of and changes to governmental controls; |

| • | restrictions on the export of critical technology; |

| • | trade restrictions; |

| • | difficulty in collecting receivables; |

| • | inadequate protection of intellectual property; |

| • | labor union activities; |

| • | changes in tariffs and taxes; |

| • | restriction on the importation and exportation of goods and services; |

| • | compliance with anti-bribery and anti-corruption laws; |

| • | difficulties in staffing and managing international operations; and |

| • | political and economic instability. |

No assurance can be given that these factors will not have a material adverse effect on our future international sales and operations and, consequently, on our business, financial condition and results of operations.

Operating margins may be negatively impacted by a downturn in sales

Our expense levels are based, in part, on our expectations regarding future sales and these expenses are largely fixed in the short term. Some expenses, such as those related to research and development activities, would likely be maintained in the event of a sales downturn in order to maintain and enhance the long-term competitiveness of the Company. In addition, to enable us to promptly fill orders, we maintain inventories of finished goods, components and raw materials. As a result, we commit to considerable costs in advance of anticipated sales. Accordingly, we may not be able to reduce our costs in a timely manner to compensate for any unexpected shortfall between forecasted and actual sales. Any significant shortfall of sales may result in us carrying higher levels of inventories of finished goods, components and raw materials thereby increasing our risk of inventory obsolescence and corresponding inventory write-downs and write-offs.

Competition in our markets is intense and our failure to compete effectively could adversely affect our business

Competition in the markets for our products is intense. The speed with which companies can identify new applications for thermal imaging, develop products to meet those needs and supply commercial quantities at low prices to the market are important competitive factors. We believe the principal competitive factors in our markets are product performance, price, customer service and training, product reputation, and effective marketing and sales efforts. Many of our competitors have greater financial, technical, research and development, and marketing resources than we do. All of these factors, as well as the potential for increased competition from new competitors, require us to continue to invest in, and focus on, research and development and new product innovation. No assurance can be given that we will be able to compete effectively in the future and a failure to do so could have a material adverse effect on our business, financial condition and results of operations.

14

Dependence on sole source and limited source suppliers of components for our products exposes us to risks that could result in delays in satisfying customer demand, increased costs and loss of revenue

We currently rely on a number of sole source and limited source suppliers to provide certain key components for our products. We have increased our internal sources of supply for certain critical components, in particular, cooled and uncooled infrared detectors, optics and optical coatings, and laser components, but we rely on sole or limited source third-party suppliers for other key components including laser rangefinders, certain machined parts, optics, motors and electronic components. Many of these suppliers are small and we are often one of their most important customers. Our business, financial condition and results of operations could be materially and adversely affected in the event that we are unable to source certain of these components on a timely basis or if such components are defective or they do not otherwise meet our performance standards.

Based on past experience, we expect to occasionally receive late deliveries or to experience inadequate supplies of certain components. If critical components provided by any significant supplier become unavailable, our manufacturing operations could be disrupted. Unless we have sufficient lead-time and are otherwise able to identify and qualify acceptable replacement components or redesign our products with different components, we might not be able to obtain necessary components on a timely basis or at acceptable prices. Any extended interruption in the supply of sole or limited source components could have a material adverse effect on our business, financial condition and results of operations.

Our future success depends in part on attracting and retaining key senior management and qualified technical, sales and other personnel

Our future success depends in part on the efforts and continued services of our key executives and our ability to attract and retain qualified technical, sales and other personnel. Significant competition exists for such personnel and we cannot assure the retention of our key executives, technical and sales personnel or our ability to attract, integrate and retain other such personnel that may be required in the future. We cannot assure that employees will not leave and subsequently compete against us. If we are unable to attract and retain key personnel, our business, financial condition and results of operations could be adversely affected.

We may be unable to successfully integrate recent or future acquisitions into our operations, thereby disrupting our business and harming our financial condition and results of operations

We have made several acquisitions of various sizes during our history, including eleven in the past seven years. Our most recent acquisitions include Salvador, OmniTech, and Directed Perception in 2009. The integration of businesses, personnel, product lines and technologies can be difficult, time consuming and subject to significant risks. For example, we could lose key personnel from companies that we acquire, incur unanticipated costs, lose major sources of revenue, fail to integrate critical technologies, suffer business disruptions, fail to capture anticipated synergies, fail to establish satisfactory internal controls, or incur unanticipated liabilities. Any of these difficulties could disrupt our ongoing business, distract our management and employees, increase our expenses and decrease our revenue.

We frequently evaluate strategic opportunities available to us and it is likely that we will make additional acquisitions in the future. Such acquisitions may vary in size and complexity. Any future acquisitions are subject to the risks described above. Furthermore, we might assume or incur additional debt or issue additional equity securities to pay for future acquisitions. Additional debt may negatively impact our results and increase our financial risk, and the issuance of any additional equity securities could dilute our then existing shareholders’ ownership. No assurance can be given that we will realize anticipated benefits of any future acquisitions, or that any such acquisition or investment will not have a material adverse effect on our business, financial condition and results of operations.

15

We may experience impairment in the value of our tangible and intangible assets

Our industry is subject to rapid changes in technology, which may result in unexpected obsolescence or impairment of our assets. As of December 31, 2009, our intangible assets, including goodwill, totaled $321.5 million and represented 22 percent of our total assets. Most of these intangibles are the result of acquisitions in which the purchase price exceeded the value of the tangible assets acquired. We amortize certain of these intangibles over their anticipated useful life and review goodwill for impairment annually or more frequently if warranted by events. To date we have not experienced any impairment of our intangible assets, but there can be no assurance that we will not experience such impairment in the future. In addition, certain of our tangible assets such as inventory and machinery and equipment may experience impairment in their value as a result of such events as the introduction of new products, changes in technology or changes in customer demand patterns. We depreciate our machinery and equipment at levels we believe are adequate; however, there can be no assurance that there will not be a future impairment that may have a material impact on our business, financial condition and results of operations.

We are exposed to worldwide financial markets

Financial markets are volatile. Changes in the availability of credit and the perceived and actual market risk of financial instruments can have numerous potential adverse effects, including the inability of customers to obtain credit to finance purchases of our products, the insolvency of customers resulting in reduced sales and bad debts, and the insolvency of key suppliers resulting in product development and production delays. We invest our cash and cash equivalents in instruments that may be exposed to credit and market risk, including default, the failure of financial institutions and market illiquidity.

We face risks from currency fluctuations

Historically, currency fluctuations have affected our operating results. Changes in the value of foreign currencies in which our sales or costs incurred are denominated have in the past caused, and could in the future cause, fluctuations in our operating results. We seek to reduce our exposure to currency fluctuations by denominating, where possible, our international sales in United States dollars, and by undertaking limited hedging of forecasted currency exposures. With respect to international sales denominated in United States dollars, a decrease in the value of foreign currencies relative to the United States dollar could make our products less price competitive.

Our inability to protect our intellectual property and proprietary rights and avoid infringing the rights of others could harm our competitive position and our business

Our ability to compete successfully and achieve future revenue growth depends, in part, on our ability to protect our proprietary technology and operate without infringing the rights of others. To accomplish this, we rely on a combination of patent, trademark, copyright and trade secret laws, confidentiality agreements and contractual provisions to protect our proprietary rights. Many of our proprietary rights are held in confidence as trade secrets and are not covered by patents, making them more difficult to protect. Although we currently hold United States patents covering certain aspects of our technologies and products, and we are actively pursuing additional patents, we cannot be certain that we will obtain additional patents or trademarks on our technology, products and trade names. Furthermore, we cannot be certain that our patents or trademarks will not be challenged or circumvented by our competitors or that measures taken by us to protect our proprietary rights will adequately deter their misappropriation or disclosure. Any failure by us to meaningfully protect our intellectual property could have a material adverse effect on our business, financial condition and results of operations. Moreover, because intellectual property does not necessarily prevent our competitors from entering the thermal imaging industry, there can be no assurance that we will be able to maintain our competitive advantage or that our competitors will not develop capabilities equal or superior to ours.

16

Litigation over patents and other intellectual property is common in our industry. We have been the subject of patent and other intellectual property litigation in the past and cannot be sure that we will not be subject to such litigation in the future. Similarly, there exists the possibility we will assert claims in litigation to protect our intellectual property. Lawsuits defending or prosecuting intellectual property claims and related legal and administrative proceedings could result in substantial expense to us and significant diversion of effort of our personnel. An adverse determination in a patent suit or in any other proceeding in which we are a party could subject us to significant liabilities, result in the loss of intellectual property rights we claim or impact our competitive position. Additionally, an adverse determination could require us to seek licenses from third parties. If such licenses are not available on commercially reasonable terms or at all, our business, financial condition and results of operations could be adversely affected.

We may not be successful in obtaining the necessary export licenses to conduct operations abroad and the United States government may prevent proposed sales to foreign governments

Export licenses are required from United States government agencies under the Export Administration Act, the Trading with the Enemy Act of 1917 and the Arms Export Control Act of 1976 for export of many of our products. We can give no assurance that we will be successful in obtaining these licenses. Recently, heightened government scrutiny of export licenses for products in our markets has resulted in lengthened review periods for our license applications. Failure to obtain or delays in obtaining these licenses would prevent or delay us from selling our products outside the United States and could have a material adverse effect on our business, financial condition and results of operations.

Our products may suffer from defects or errors leading to substantial damage or warranty claims

We include complex system designs and components in our products that may contain errors or defects, particularly when we incorporate new technology into our products or release new versions. If any of our products are defective, we might be required to redesign or recall those products or pay substantial damages or warranty claims. Such an event could result in significant expenses including expenses arising from product liability and warranty claims, disrupt sales and affect our reputation and that of our products, which could have a material adverse effect on our business, financial condition and results of operations. We maintain product liability insurance but cannot be certain that it is adequate or will remain available on acceptable terms.

We have indebtedness as a result of the sale of our convertible notes and are subject to certain restrictive covenants under our credit facility which may limit our operational and financial flexibility

In June 2003, we issued $210 million of 3.0 percent senior convertible notes due in 2023 in a private offering pursuant to Rule 144A under the Securities Act of 1933, as amended, of which as of December 31, 2009, approximately $58.8 million aggregate principal amount of convertible notes were outstanding.

Additionally, we have a $300 million revolving credit agreement. The credit agreement contains financial covenants that require the maintenance of certain leverage ratios, in addition to minimum levels of EBITDA and consolidated net worth, a maximum level of capital expenditures and, commencing December 31, 2009, a minimum level of liquidity comprised of cash and undrawn/unutilized availability under the credit agreement. The credit agreement is collateralized by substantially all assets of the Company. As of December 31, 2009, there were no amounts borrowed and outstanding under the credit agreement. The credit agreement expires on October 6, 2011.

Our ability to meet our debt service obligations and comply with the financial covenants under our credit facility will be dependent upon our future performance, which will be subject to financial, business and other factors affecting our operations, many of which are beyond our control. Our inability to comply with the required financial covenants could result in a default under the credit agreement. In the event of any such default, the lenders under our credit facility could elect to declare all outstanding debt, accrued interest and fees under the

17

facility to be due and immediately payable. If we are unable to repay any of this debt when due, the lenders under our credit facility could foreclose on our assets pledged to them as security.

Changes in our effective income tax rate may have an adverse effect on our results of operations

Our future effective tax rate may be adversely affected by a number of factors including:

| • | the jurisdictions in which profits are determined to be earned and taxed; |

| • | the resolution of issues arising from tax audits with various tax authorities; |

| • | changes in the valuation of our deferred tax assets and liabilities; |

| • | adjustments to estimated taxes upon finalization of various tax returns; |

| • | increases in expenses not deductible for tax purposes; |

| • | changes in available tax credits; |

| • | changes in share-based compensation expense; |

| • | changes in tax laws or the interpretation of such tax laws and changes in generally accepted accounting principles; and/or |

| • | the repatriation of earnings from outside the United States for which we have not previously provided for United States taxes. |

Any significant increase in our future effective tax rates could adversely impact net income for future periods. In addition, the United States Internal Revenue Service (“IRS”) and other tax authorities regularly examine our income tax returns. Our financial condition and results of operations could be adversely impacted if any assessments resulting from the examination of our income tax returns by the IRS or other taxing authorities are not resolved in our favor.

Oregon law and our charter documents contain provisions that could discourage or prevent a potential takeover, even if the transaction would benefit our shareholders

Other companies may seek to acquire or merge with us. An acquisition or merger of our Company could result in benefits to our shareholders, including an increase in the value of our common stock. Some provisions of our Articles of Incorporation and Bylaws, including our ability to issue preferred stock without further action by our shareholders, as well as provisions of Oregon law, may discourage, delay or prevent a merger or acquisition that a shareholder may consider favorable.

| ITEM 1B. | UNRESOLVED STAFF COMMENTS |

None.

18

| ITEM 2. | PROPERTIES |

We maintain our corporate headquarters in Wilsonville, Oregon. The location, approximate size and type of facility of our principal properties are as follows:

| Location |

Square Feet |

Type of Facility | ||

| Wilsonville (Portland), Oregon(1) |

154,000 | Corporate headquarters, manufacturing, sales and service | ||

| Danderyd (Stockholm), Sweden(2) |

165,000 | Manufacturing, sales and service | ||

| North Billerica (Boston), Massachusetts(1) |

133,000 | Manufacturing, sales and service | ||

| Goleta (Santa Barbara), California(2) |

137,000 | Manufacturing, sales and service | ||

| Orlando, Florida (1) |

82,000 | Research and development | ||

| Bozeman, Montana(2) |

32,000 | Manufacturing and sales | ||

| Waltham (Boston), Massachusetts(2) |

26,000 | Sales and distribution | ||

| Freeport, Pennsylvania(2) |

16,000 | Manufacturing, sales and service | ||

| West Malling (London), United Kingdom(2) |

15,000 | Sales and service | ||

| Tallinn, Estonia(2) |

15,000 | Manufacturing | ||

| Croissy-Beaubourg (Paris), France(2) |

14,000 | Manufacturing, sales and service | ||

| Colorado Springs, Colorado(2) |

14,000 | Manufacturing, sales and service |

| (1) | Owned property |

| (2) | Leased property |

The owned properties in Wilsonville and Orlando, and the leased facilities in Bozeman are used by the Government Systems business. The leased facilities in Waltham, Tallinn and Croissy-Beaubourg are locations for the Thermography business. The leased facilities in Goleta are used by the Commercial Vision Systems business. The leased facilities in Danderyd and West Malling and the owned property in North Billerica are used jointly by both the Thermography and Government Systems businesses.

Additionally, the Thermography business has leased sales and service facilities in Antwerp, Belgium; Frankfurt, Germany; Toronto, Canada; Paris, France; Milan, Italy; Hong Kong; Shanghai, China; Tokyo, Japan; Seoul, South Korea; and Melbourne, Australia; and owns a sales and service facility in Sao Paulo, Brazil. The Government Systems business has a leased sales and service office in Dubai, United Arab Emirates. The Commercial Vision Systems business owns a sales office in Breda, Netherlands, and leases an engineering office in Madrid, Spain, and a manufacturing, sales and service facility in Burlingame, California.

We believe our properties are suitable for their intended use, adequate for our business needs and in good condition.

19

| ITEM 3. | LEGAL PROCEEDINGS |

The Company and its subsidiary, Indigo Systems Corporation (now known as FLIR Commercial Systems, Inc.) (together, the “FLIR Parties”), were named in a lawsuit filed by Raytheon Company on March 2, 2007, in the United States District Court for the Eastern District of Texas. On August 11, 2008, Raytheon Company was granted leave to file a second amended complaint. The complaint, as amended, asserted claims for tortious interference, patent infringement, trade secret misappropriation, unfair competition, breach of contract and fraudulent concealment. The FLIR Parties filed an answer to the second amended complaint and counterclaims on September 2, 2008, in which they denied all material allegations. On August 31, 2009, the court entered an order granting the FLIR Parties’ motion for summary judgment on Raytheon’s trade secret misappropriation claim based on the FLIR Parties’ statute of limitations defense. Raytheon has abandoned all of its other claims except its patent claims which are currently set for trial to commence on April 19, 2010. The Company intends to vigorously defend itself in this matter and is unable to estimate the amount or range of potential loss, if any, which might result if the outcome in this matter is unfavorable.

We are also subject to other legal proceedings, claims and litigation arising in the ordinary course of business. We make a provision for a liability when it is both probable that a liability has been incurred and the amount of loss can be reasonably estimated. We believe we have recorded adequate provisions for any probable and estimable losses. While the outcome of such matters is currently not determinable, we do not expect that the ultimate costs to resolve these matters will have a material adverse effect on our financial position, results of operations or cash flows.

| ITEM 4. | SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS |

No matters were submitted to a vote of security holders during the quarter ended December 31, 2009.

20

PART II

| ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

The common stock of the Company has been traded on the NASDAQ Global Market since June 22, 1993, under the symbol “FLIR.” The following table sets forth, for the quarters indicated, the high and low closing sales price for our common stock as reported on the NASDAQ Global Select Market, a segment of the NASDAQ Global Market.

| 2009 | 2008 | |||||||||||

| High | Low | High | Low | |||||||||

| First Quarter |

$ | 31.76 | $ | 18.87 | $ | 33.15 | $ | 23.69 | ||||

| Second Quarter |

26.55 | 20.70 | 41.38 | 28.72 | ||||||||

| Third Quarter |

28.64 | 20.71 | 45.10 | 33.29 | ||||||||

| Fourth Quarter |

33.19 | 26.73 | 39.21 | 24.63 | ||||||||

At December 31, 2009, there were approximately 135 holders of record of our common stock and 152,826,045 shares outstanding. We have never paid cash dividends on our common stock. We intend to retain earnings for use in our business and, therefore, do not anticipate paying cash dividends in the foreseeable future.

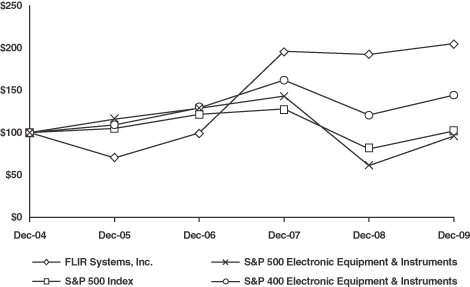

The graph below shows a comparison of the five-year cumulative total shareholder return for the Company’s common stock with the cumulative total returns on the Standard & Poor’s (“S&P”) 500 Index, the S&P 400 Electronic Equipment & Instruments Index and the S&P 500 Electronic Equipment & Instruments Index for the same five-year period. The data used for this graph assumes that $100 was invested in the Company and in each index on December 31, 2004, and that all dividends were reinvested.

21

The stock performance graph was plotted using the following data:

| Dec 04 | Dec 05 | Dec 06 | Dec 07 | Dec 08 | Dec 09 | |||||||||||||

| FLIR Systems, Inc. |

$ | 100.00 | $ | 70.01 | $ | 99.80 | $ | 196.27 | $ | 192.38 | $ | 205.24 | ||||||

| S&P 500 Index |

100.00 | 104.91 | 121.48 | 128.16 | 80.74 | 102.11 | ||||||||||||

| S&P 400 Electronic Equipment & Instruments Index |

100.00 | 109.24 | 129.20 | 162.26 | 120.83 | 144.39 | ||||||||||||

| S&P 500 Electronic Equipment & Instruments Index |

100.00 | 116.03 | 128.75 | 143.38 | 61.00 | 96.09 | ||||||||||||

During 2009, the Company was moved from the S&P 400 Electronic Equipment & Instruments Index to the S&P 500 Electronic Equipment & Instruments Index. In accordance with Securities and Exchange Commission rules, the Company is showing in the above graph the performance of both these indices.

The Company has also been included in the NASDAQ-100 Index since 2008.

The following table summarizes our 2009 common stock repurchases: