Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2009

Commissions file number 1-14379

CONVERGYS CORPORATION

| An Ohio | I.R.S. Employer | |

| Corporation | No. 31-1598292 |

201 East Fourth Street, Cincinnati, Ohio 45202

Telephone Number (513) 723-7000

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |||

| Common Shares (no par value) | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes X No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes No X

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes X No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (Section 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer X Accelerated filer Non-accelerated filer Smaller reporting company

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes No X

The aggregate market value of the voting shares held by non-affiliates of the registrant was $1,139,860,863, computed by reference to the closing sale price of the stock on the New York Stock Exchange on June 30, 2009, the last business day of the registrant’s most recently completed second fiscal quarter.

At January 31, 2010, there were 123,170,011 common shares outstanding, excluding amounts held in treasury of 60,163,838.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement for the 2010 Annual Meeting of Shareholders to be held on April 20, 2010 are incorporated by reference into Part III of this report.

Table of Contents

Convergys Corporation 2009 Annual Report 1

Table of Contents

Safe Harbor Statement and Part I, Item 1. Business

Private Securities

Litigation Reform Act of 1995

Safe Harbor Cautionary Statement

This report and the documents incorporated by reference contain “forward-looking” statements, as defined in the Private Securities Litigation Reform Act of 1995, that are based on current expectations, estimates and projections. Statements that are not historical facts, including statements about the beliefs and expectations of Convergys Corporation (Company), are forward-looking statements and will contain words such as “believes,” “expects,” “intends,” “could,” “should,” “will,” “plans,” “anticipates” and other similar words. These statements discuss potential risks and uncertainties; and, therefore, actual results may differ materially. You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date on which they were made. The Company has no current intention to update any forward-looking statements, whether as a result of new information, future events or otherwise.

Important factors that may affect these projections or expectations include, but are not limited to: the behavior of financial markets including fluctuations in interest or exchange rates; continued volatility and further deterioration of the capital markets; the impact of regulation and regulatory, investigative, and legal actions; strategic actions, including acquisitions and dispositions; future integration of acquired businesses; future financial performance of major industries which we serve; the loss of a significant client or significant business from a client; difficulties in completing a contract or implementing its provisions; and numerous other matters of national, regional, and global scale including those of the political, economic, business, and competitive nature. These uncertainties may cause our actual future results to be materially different than those expressed in our forward-looking statements. The “Risk Factors” set forth in Part I, Item 1A of this report could also cause actual results to differ materially from the forward-looking statements.

Part I

Overview

Convergys Corporation (the Company or Convergys) is a global leader in relationship management. We provide solutions that drive more value from the relationships our clients have with their customers and employees. Convergys turns these everyday interactions into a source of profit and strategic advantage for our clients. Our unique combination of domain expertise, operational excellence and innovative technologies has delivered process improvement and actionable business insight to clients to enhance their relationships with customers and employees.

The Company maintains an internet website at www.convergys.com. Information about the Company is available on the website, free of charge, including the annual report filed on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as soon as reasonably practicable after we electronically file such material with, or furnish it to, the Securities and Exchange Commission. The Company’s website and the information contained therein are not considered as being incorporated into this Annual Report.

The Company has a Code of Business Conduct that applies to all employees as well as our Board of Directors; a Financial Code of Ethics that applies to our principal executive officer, principal financial and accounting officer and certain other management and senior employees; and Governance Principles for our Board of Directors. The Code of Business Conduct, Financial Code of Ethics and Governance Principles, as well as the charters for the following committees of our Board of Directors; Audit Committee, Finance Committee, Compensation and Benefits Committee and the Governance and Nominating Committee, are posted on our website at www.convergys.com. The Company will post on our website any amendments to, or waivers of, the Code of

2 Convergys Corporation 2009 Annual Report

Table of Contents

Business Conduct and Financial Code of Ethics. Copies of these documents will be provided free of charge upon written request directed to Investor Relations, Convergys Corporation, 201 East Fourth Street, Cincinnati, Ohio 45202.

Business Segments

The Company has three segments: Customer Management, which provides agent-assisted, self-service and intelligent technology care solutions; Information Management, which provides business support system (BSS) solutions; and Human Resources (HR) Management, which provides human resource business process outsourcing (HR BPO) solutions. These segments are consistent with the Company’s management of the business and reflect its internal financial reporting structure and operating focus. The Board of Directors continually monitors the Company’s business and, as appropriate, evaluates various strategies to enhance shareholder value, including by means of strategic transactions involving one or more of its businesses. Any such transactions could occur in the future and could be material, although there can be no assurance that such transactions will occur.

Pursuant to Rule 12b-23 under the Securities Exchange Act of 1934, as amended, the industry segment and geographic information included in Item 8, Note 18 of the Notes to Consolidated Financial Statements, are incorporated by reference in partial response to this Item 1.

Customer Management

Our Customer Management segment partners with clients to deliver customer care solutions that enhance the value of their customer relationships, turning the customer experience into a strategic differentiator. As an end-to-end single-source provider of self-service, agent-assisted and proactive care solutions we combine consulting, innovative technology and agent-assisted services to optimize the customer experience and strengthen customer relationships. Whether contact center operations are on-premises, fully outsourced or blended, we customize our solutions to meet our clients’ needs.

Customer Management solutions are organized into two areas: 1) agent-assisted services, and 2) intelligent technology solutions.

Agent-Assisted Services

Every day our approximately 60,000 contact center employees handle millions of customer service interactions such as account service, billing inquiries and technical support and service in contact centers worldwide. We provide multi-channel customer care using a global service delivery infrastructure that operates 24 hours a day, 365 days a year. Our global delivery model means our clients’ businesses can benefit from workforce advantages around the world including the U.S., Canada, Latin America, Europe, India and the Philippines. We utilize center-based agents as well as work-at-home agents. Our agent-assisted solutions include:

Customer Acquisition Solutions

Customer Acquisition Solutions provide comprehensive sales and order support to identify and secure high-value consumer and business customers, maximize sales conversion rates and increase revenue per customer. In addition, we offer Direct Response Solutions to address the customer support needs of direct response marketers.

Customer Service Solutions

Customer Service Solutions include comprehensive customer care tailored to meet our clients’ specific business needs and designed to provide customers with an optimal service experience. Our agents in this solution commonly handle inquiries on products, account service, billing inquiries and dispute resolution.

Customer Retention Solutions

Customer Retention Solutions leverage analytics to optimize the level of customer satisfaction, build customer loyalty and address customer churn. Our programs are designed to help our clients retain their customers and increase their lifetime value.

Convergys Corporation 2009 Annual Report 3

Table of Contents

Item 1. Business (continued)

Technical Support

Technical Support includes tier-one, tier-two and tier-three advanced services. Either online or by phone, our programs focus on first contact resolution. Our services span from simple “how-to” inquiries from new users to sophisticated trouble-shooting and technical support.

Back Office Solutions

Back Office Solutions combine integrated document management, data entry and transaction processing capabilities with process expertise and workflow management to help meet our clients’ back office needs in customer care, accounts receivable management for early-stage collections, finance and accounting and accounts payable.

Convergys Business-to-Business Solutions

Business-to-Business Solutions include inside sales and account management, marketing campaigns, customer service and self-service programs. Focused on supporting the needs of the business-to-business market, Convergys offers a way to expand the reach of our clients’ sales force and to improve the effectiveness of their channel partnerships. Whether working with current business customers or tapping new and traditionally under-served markets, we become an extension of our clients’ sales force to drive sales and profits higher.

Agent-assisted services are deployed via multi-shore delivery capabilities that have grown to approximately 80 contact centers worldwide with an infrastructure designed to cost-effectively support customer care requirements. Our seamless and integrated network of on-shore and off-shore centers, as well as home agents, provides a high degree of availability and redundancy. Our services include multilingual program support.

Intelligent Technology Solutions

Our portfolio of Intelligent Interaction Solutions includes technologies such as voice portals and speech automation, real-time decisioning, web-based service channels, identity verification, mobile services and enhanced analytics.

In September 2008, Convergys purchased Intervoice, Inc. (Intervoice). The purchase was made to augment the Company’s relationship management solutions and to provide a complementary growth platform. Convergys and Intervoice clients understand the importance of driving greater value from customer relationships. Now both have the opportunity to benefit from a wider array of industry-leading, premises-based and hosted technology solutions.

Our intelligent technology-based solutions span the entire interaction lifecycle from proactive service to self-service to assisted service.

Self-Service Solutions deliver an intuitive, intelligent and cost-effective self-service experience. Our solutions support multi-channel formats and include:

Intelligent Self Service

The Convergys Intelligent Self-Service Solution is an integration of Intervoice Voice Portal (IVP) and Convergys Dynamic Decisioning Solution. This solution takes advantage of the power of speech and web-based standards, along with enterprise-wide policy management to enable contact centers to provide a more personalized and relevant experience for their customers, while also reducing costs and increasing revenue opportunities.

Next Generation Messaging

The Convergys Next Generation Messaging is an Internet Protocol (IP) based multimedia messaging solution that provides a suite of text, voice and web-based messaging capabilities. Its features include traditional voicemail, e-mail and facsimile, as well as text-to-speech reading and integrated multimedia messaging.

Proactive Service Solutions deliver personalized outbound notifications via the customer’s preferred method of contact. Another form of proactive service is identity verification that preempts potentially fraudulent transactions or activity. Our specific solutions are:

Intelligent Notification

The Convergys Intelligent Notification Solution is an integration of Advanced Notification Gateway and

4 Convergys Corporation 2009 Annual Report

Table of Contents

Convergys Dynamic Decisioning Solution technologies. This solution turns service strategy from reactive to proactive by delivering real-time notifications to customers via the channel of their choice. The result is greater customer satisfaction, increased revenue and lower operational costs.

On-Demand Voice Authentication

The Convergys On-Demand Voice Authentication Solution is a platform-independent solution that allows companies to easily enroll voice signatures of their customers and employees. Upon enrollment, companies can authenticate transactions more securely than with a traditional ID + PIN authentication. This solution enhances the level of security and protection of personal and confidential information for agent-assisted and self-service interactions and within the phone, interactive voice response (IVR), web and mobile device channels.

Assisted-Service Solutions provide intelligent contact routing and a multi-channel knowledge base to improve the efficiency of live-agent support.

eServices

Convergys eService Solution is an on-demand, web self-service and multi-channel knowledge management solution that complements company websites and agent desktops. eService contains robust web self-service capabilities as well as e-mail, chat and co-browse, all linked with a self-learning knowledge foundation to consistently provide the most relevant information. Live agent phone interactions are supported by the same knowledge foundation thus providing a seamless bridge between the self-service and agent-assisted experience.

Information Management

Information Management provides billing and business support system (BSS) solutions that help our clients configure and deploy mission-critical cost-effective technologies to better understand, sell to and serve their customers. These solutions comprise software, partner products, integration and business consulting services and a strong telecommunication heritage and operational expertise to enable service providers to meet their business goals.

The Information Management Smart Solution portfolio is organized into three functional areas: revenue management, product and order management, and customer care management.

Revenue Management Solutions

Smart Solutions for Revenue Management enable the creation of compelling service bundles to differentiate offers in the marketplace and provide real-time capabilities that enable revenue generation from all customer segments, regardless of payment type. Our Revenue Management solutions and software applications include:

Rating and Billing Manager

Rating and Billing Manager is a highly scalable, reliable and fully convergent real-time charging, rating and billing management system. It supports existing and next-generation services across multiple vertical markets. For the telecommunication market, the solution can be delivered with pre-integrated network control, real-time rating and charging, balance management, payment management, customer self-service and customer service representative (CSR) care. This solution allows service providers to offer and bill consistent product and service bundles, regardless of payment method (pre-/post-paid), from a single database.

Collections Manager

Collections Manager is an automated, in-house collections system that enables service providers to be the sole owners of all collected revenue. It provides out-of-the-box automation that reduces capital expenditures by eliminating custom development and enables faster time-to-market for new treatment schedules.

Convergys Corporation 2009 Annual Report 5

Table of Contents

Item 1. Business (continued)

Active Mediation

Active Mediation seamlessly bridges many protocols and/or data formats to meet convergent mediation business requirements. It is equally suitable for deployment in traditional batch environments and in next-generation networks that require a real-time, bi-directional dialog for end-to-end service delivery.

Infinys/ICOMS

The Infinys Integrated Communications Operations Management System (ICOMS) is designed specifically for the broadband convergent video, high-speed data and telephony markets. It provides an end-to-end billing and subscriber management solution tailored specifically to the demands of today’s converged cable television and broadband telephony service providers.

Product and Order Management Solutions

Smart Solutions for Product and Order Management enable service providers to better manage the increasing complexity associated with managing a growing product and service portfolio. These solutions help clients quickly respond to new market demands, allowing them to launch new segment-specific offers in alignment with their own pre-defined business and service rules. Our Product and Order Management solutions and software applications include:

Product Control Manager

Product Control Manager automates manual and disjointed product management practices, as well as multiple product catalogs, throughout an enterprise. It can coexist with existing product repositories, centralizing and normalizing data and processes.

Shopping and Ordering Solution

Shopping and Ordering Solution enables service providers to manage the complexities of the shopping and order capture process for convergent services.

Service Fulfillment Manager

Service Fulfillment Manager orchestrates and manages order-handling activities for all services. Highly flexible, it accepts product orders from a variety of sources – CSR graphical user interfaces, upstream customer relationship management (CRM) applications, enterprise application integration (EAI) interfaces or self-care portals – then tracks them through to order completion.

Service Activation Manager

Service Activation Manager provides fast, reliable services activation. It is an adaptor platform that activates any service on any network, for any underlying technology. It ensures a smooth hand-off from Service Fulfillment Manager or from any third-party system.

Customer Care Management Solutions

Smart Solutions for Customer Care Management enables service providers to deliver a superior customer experience. These solutions provide significant flexibility for service providers to deliver products and services through any channel the customer chooses and to find the optimal balance of CSR and self-service care to increase customer satisfaction, loyalty and profits. Our Customer Care Management solutions and software applications include:

Customer Service Manager

Customer Service Manager provides automated end-to-end order orchestration and sophisticated human factors engineering to meet and exceed subscriber, order and customer care needs.

Inventory Manager

Inventory Manager provides enterprise-wide functionality to ensure comprehensive, centralized insight into widespread logical and physical inventory items throughout the inventory lifecycle.

Field Service Manager

Field Service Manager enables service providers to predict service demand, then plan, schedule and execute service delivery in a way that maximizes value across their extended enterprise.

6 Convergys Corporation 2009 Annual Report

Table of Contents

Dynamic Decisioning and Customer Intelligence Solution

The Dynamic Decisioning and Customer Intelligence Solution enables service providers to add more personalization to each customer contact, and empower CSRs with real-time decision-making tools. Dynamic Decisioning software includes both a set of tools and a policy engine in order to enable the execution of real-time customer service policies and proactive upsell offers that increase customer retention.

HR Management

Our HR Management segment partners with global HR clients to drive more value from employee relationships, fostering greater organizational effectiveness and lowering costs.

Convergys utilizes best business practices rooted in outsourced HR solutions to help clients automate HR processes and improve service delivery. The result is a greater level of workforce insight that enables our clients to make better decisions and better manage global talent as a strategic asset.

Convergys HR Solutions include the following:

Benefits Administration Solutions

Benefits Administration Solutions manages the complexities of benefits administration, which enables us to predict benefit expenses and provide clients the business intelligence they need to improve benefit-related processes, services and costs. Our service delivery model combines self-service tools and multilingual service centers to provide services to employees, including health and welfare administration services, retirement services and pension administration, absence management, flexible spending account administration, carrier administration and tuition reimbursement.

Compensation Solutions

Compensation Solutions help companies improve the clarity and parity of their global compensation plans while assuming global administration to lower overall costs and deliver key analytics. By aligning global compensation with other key HR processes, Convergys can help improve employee understanding of compensation strategies resulting in increased employee engagement.

Human Resource Administration Solutions

Human Resource Administration Solutions help organizations transform the task of managing global employee paperwork and data into a harmonized, automated and highly efficient process. Our solution incorporates process improvements and technology innovations to streamline global HR Administration.

Learning Solutions

Learning Solutions help companies manage the employee life cycle to get more from the talent that they have and develop the talent that they need. By outsourcing select learning functions such as administration, operations and content development and sourcing to us, companies gain better return on investment.

Performance Management Solutions

Convergys Performance Management Solution aligns employee performance with corporate objectives, getting everyone focused on the work that is most critical to an organization’s success. The solutions also drive business results by closing performance gaps and measuring behavior against goals.

Payroll Administration Solution

Payroll Administration Solutions range from end-to-end payroll outsourcing to targeted process management for each point between employee time entry and payroll check production. We can manage the complexities of global payroll, including controls for accuracy and compliance to local regulations.

Recruiting and Resourcing Solution

The global Recruiting and Resourcing Solution can free HR departments from the administrative aspects of finding, hiring and on-boarding employees so that they

Convergys Corporation 2009 Annual Report 7

Table of Contents

Item 1. Business (continued)

can focus on higher-value activities such as staffing strategies and hiring decisions.

Workforce Intelligence Solution

Workforce Intelligence Solutions turn HR information into business insight. Our solutions give our clients the business intelligence it needs to make better decisions and better manage the global workforce.

Strategy

Our strategy is to enable our clients to gain more value from their relationships with their customers and employees. We do this by providing clients comprehensive relationship management solutions (including software, hardware, services and consulting). The value we create drives improved business performance and a sustainable competitive advantage for our clients. Key elements of our strategy include:

Deliver a Differentiated Value Proposition to Clients. As a global leader in relationship management, Convergys provides solutions that drive more value from the relationships our clients have with both their customers and their employees. Convergys turns these everyday interactions into a source of profit and strategic advantage for our clients. Our differentiated solution set includes Customer Solutions, BSS Solutions, HR Solutions and industry-specific solutions. Our Customer Solutions deliver support using live-agents staffed around the world, self-service technology (speech, IVR, web and e-mail) that intelligently automates the handling of interactions, analytics for real-time decisioning and deep customer management process expertise. In addition, we offer a variety of delivery models for our Customer Solutions including outsourced (on-shore, off-shore or home agent) and hosted (on-premise or off-premise). Our BSS solutions address the critical customer care, billing (including real-time rating and charging) and product-related issues that face the communications industry specific to managing customer relationships, revenue management and enterprise product management. Our HR Solutions deliver greater organizational effectiveness through comprehensive HR BPO and integrated talent management strategies. We serve a host of industries with concentration in the telecommunications, technology, financial services, healthcare, government and retail verticals.

Invest in Our Business to Expand our Addressable Markets and Strengthen our Solutions: Our growth strategy is to continue to broaden and deepen our offer portfolio to provide our clients with comprehensive solutions. We will invest in the business as required (e.g., to acquire new capabilities, to expand into new global locations and to employ new personnel with desired talent) to expand our addressable markets. We continue to identify and operate in attractive markets where we can effectively provide differentiated value and deliver superior returns. We intend to expand our capabilities, technology, partners, workforce and operations globally to continually strengthen our ability to successfully serve and satisfy the demands of our multinational clients. We will invest in research and development to deliver unique and innovative solutions.

Expand Our Relationships with Existing Clients. We focus on client satisfaction to maintain and grow our base business. Our intent is to grow by cross-selling new solutions and expanding our relationship management footprint within our client’s organization. Our client renewal rates are very high, reflecting a high degree of satisfaction and stability in our client base.

Aggressively Grow Our Client Base. We believe that the global market for relationship management solutions is large and underserved, and we intend to aggressively pursue this market opportunity. We emphasize a consultative selling approach leveraging our expertise in four critical areas, (1) business and customer strategy development, (2) business and customer analytics, (3) technology enablement, and (4) operational excellence to deliver superior operating performance and further strengthen our leadership by cross-selling other services.

Sustain Our High-Performance Culture to Drive Business Results. We believe that people drive performance and we

8 Convergys Corporation 2009 Annual Report

Table of Contents

are committed to hiring and retaining the best performers worldwide and ensuring that they are committed to the success of our clients. Our competencies include our proven strength in recruiting, training, equipping, deploying and effectively managing very large groups of people with diverse skills on a global basis (people), expertise in operations and cost-effective service delivery (process), and design, development and delivery of innovative, scalable transactions and interaction applications (technology). We adhere to the principles of strategic HR, including emphasizing collaboration, goal alignment, pay for performance, continuous improvement and focus on accountability and results. We believe this approach drives superior execution, enabling us to consistently deliver significant value to our customers.

Clients

Both our Customer Management and Information Management segments derive significant revenues from AT&T Inc. (AT&T), our largest client. Revenues from AT&T were 19.8%, 18.2% and 16.3% of our consolidated revenues for 2009, 2008 and 2007, respectively.

Customer Management

Our Customer Management segment principally focuses on developing long-term strategic outsourcing relationships with large companies in customer-intensive industries and governmental agencies. We focus on these types of clients because of the complexity of services required, the anticipated growth of their market segments and their increasing need for more cost-effective customer management services. In terms of Convergys’ revenues, our largest Customer Management clients during 2009 were AT&T, Comcast Corporation (Comcast), the DirecTV Group, Inc. (DirecTV), General Motors Corporation and Sprint Nextel Corporation (Sprint Nextel). We provide customer management services to Sprint Nextel as a subcontractor to International Business Machines (IBM).

Information Management

Our Information Management segment serves clients principally by providing and managing complex BSS services that address all segments of the communications industry. In terms of Convergys’ revenues, our largest Information Management clients during 2009 were AT&T, Cincinnati Bell, Inc., MetroPCS Communications, Inc., PT Telkomunikasi Seluar (Telkomsel) and Time Warner, Inc.

HR Management

Our HR Management segment primarily focuses on providing HR outsourcing solutions for large companies and governmental agencies. In terms of Convergys’ revenues, our largest HR Management clients during 2009 were Boston Scientific Corporation, E.I. du Pont de Nemours & Co. (DuPont), the State of Florida, Johnson & Johnson and the State of Texas.

Operations

We operate over 80 contact centers averaging approximately 65,000 square feet per center, with approximately 45,000 production workstations with 24 hours a day, 365 days a year availability. Our contact centers are located in various parts of the world including the United States, the Philippines, India, Canada, the U.K. and Costa Rica. New contact centers are established to accommodate anticipated growth in business or in response to a specific customer need. We continue to add contact center capacity in the Philippines and Latin America to accommodate client needs.

Our contact centers employ a broad range of technology including digital switching, intelligent call routing and tracking, proprietary workforce management systems, case management tools, proprietary software systems, computer telephony integration, interactive voice response, advanced speech recognition, web-based tools and relational database management systems. This technology enables us to improve our call, web and e-mail handling and personnel scheduling, thereby increasing our efficiency and enhancing the quality of the services we deliver to our clients and their customers and employees. With this technology, we are able to respond to changes in client call volumes and move call volume traffic based on agent availability. Additionally, we use this technology to collect information concerning the contacts, including number, response time, duration and results of the

Convergys Corporation 2009 Annual Report 9

Table of Contents

Item 1. Business (continued)

contact. This information is reported to the client on a periodic basis for purposes of monitoring quality of service and accuracy of the related billing.

We operate two primary data centers, one in Orlando, Florida, and the other in Cincinnati, Ohio, comprising, in total, approximately 170,000 square feet of space. Our technologically advanced data centers provide 24 hours a day, 365 days a year availability (with redundant power and communication feeds and emergency power back-up) and are designed to withstand most natural disasters.

The capacity of our data center and contact center operations, coupled with the scalability of our BSS and customer management solutions, enable us to meet initial and ongoing needs of large-scale and rapidly growing companies and government entities. By employing the scale and efficiencies of common application platforms, we are able to provide client-specific enhancements and modifications without incurring many of the costs of a full custom application. This allows us to be in a position to be a value-added provider of billing, customer and employee support products and services.

Technology, Research and Development

We intend to continue to emphasize the design, development and deployment of scalable billing and customer management systems to increase our market share, both domestically and internationally. During 2009, 2008 and 2007, we spent $74.2 million, $54.9 million and $73.4 million, respectively, for research and development to advance the functionality, flexibility and scalability of our products and services. The majority of this spending has been incurred in Information Management and reflects our commitment to further develop our solutions. We are being selective in our approach to research and development spending, focusing our efforts on only what we consider the highest impact areas. The success of our Customer Management segment depends, in part, on our advanced technology used in the delivery of services to clients. As a result, we continue to invest in the enhancement and development of our contact center technology.

Our intellectual property consists primarily of business methods and software systems. To protect our proprietary rights, we rely primarily on a combination of U.S. and foreign copyright, trade secret and trademark laws, confidentiality agreements with employees and third parties and protective contractual provisions such as those contained in licenses and other agreements with consultants, suppliers, strategic partners and clients.

We own 179 patents, 161 of which relate to Customer Management and HR Management and 18 of which relate to Information Management. Patents protect our technology and business methods that we use both to manage our internal systems and processes effectively and give us competitive advantages in developing innovative technologies to provide customer management, HR management and billing services to our clients. The first of these patents was issued in January 1993, while the most recent patent was granted in November 2009. These patents generally have a life of 17 years, although the life for some patents issued before June 8, 1995 can extend to approximately 20 years in certain instances. Additional applications for U.S. and foreign patents currently are pending.

Our name and logo and the names of our primary software products are protected by their historic use and by trademarks and service marks that are registered or pending in the U.S. Patent and Trademark Office and under the laws of more than 50 foreign countries.

Employees

As of December 31, 2009, we employed approximately 70,000 people, approximately 63,000 of whom work for Customer Management, approximately 3,000 of whom work for Information Management, approximately 3,000 of whom work for HR Management, with the remainder working in various corporate functions.

10 Convergys Corporation 2009 Annual Report

Table of Contents

Items 1. (continued), 1A., 1B. and 2.

Competition

The industries in which we operate are extremely competitive. Our competitors include: (i) other customer management companies, such as Accenture Ltd. (Accenture), APAC Customer Services Inc., IBM, SITEL Corp., Sykes Enterprises Inc., Teleperformance, TeleTech Holdings Inc., West Corporation and Wipro Ltd.; (ii) other HR management companies, such as Accenture, Affiliated Computer Services Inc., ExcellerateHRO, Hewitt Associates Inc., IBM and Tata Consultancy Services; and (iii) other BSS services companies such as Amdocs Ltd., Comverse Technology Inc., CSG Systems International Inc. and Intec Telecom Systems. In addition, niche providers or new entrants could capture a segment of the market by developing new systems or services that could impact our market potential.

Interests in Cellular Partnerships

The Company owns a 33.8% limited partnership interest in the Cincinnati SMSA Limited Partnership, a provider of wireless communications in central and southwestern Ohio and northern Kentucky, and a 45.0% interest in the Cincinnati SMSA Tower Holdings LLC, an operator of cellular tower space (the Cellular Partnerships). We account for our interests in the Cellular Partnerships under the equity method of accounting. Refer to Note 2 of the Notes to Consolidated Financial Statements for more details related to these partnerships.

The information required by Item 1A is included in Item 7 of this Form 10-K.

Item 1B. Unresolved Staff Comments

None.

Our principal executive offices are located at 201 East Fourth Street, Cincinnati, Ohio 45202, and the telephone number at that address is (513) 723-7000. We own our corporate headquarters facility in Cincinnati, Ohio, which is used by the three segments, an office complex in Jacksonville, Florida, which is used predominantly by Customer Management and HR Management, and an office facility in Dallas, Texas, which is used by Customer Management.

We lease space for offices, data centers and contact centers on commercially reasonable terms. Domestic facilities are located in Arizona, California, Colorado, Florida, Georgia, Idaho, Kansas, Kentucky, Louisiana, Missouri, Nebraska, New Mexico, North Carolina, Ohio, Oklahoma, Tennessee, Texas, Utah, Virginia and Wisconsin. International facilities are located in Australia, Brazil, Canada, China, Colombia, Costa Rica, Egypt, England, France, Germany, Hong Kong, Hungary, India, Indonesia, Israel, Malaysia, Mexico, Netherlands, the Philippines, Scotland, Singapore, Spain, Sri Lanka, Taiwan, Thailand and the United Arab Emirates. Customer Management and HR Management use the majority of these facilities. Upon the expiration or termination of any such leases, we believe we could obtain comparable office space. As discussed more fully in Note 12 of Notes to Consolidated Financial Statements, we lease an office complex in Orlando, Florida under an agreement that expires June 2010. Upon termination or expiration, we must either purchase the property from the lessor for $65.0 million or arrange to have the office complex sold to a third party. We are in the process of evaluating whether to purchase or refinance this property.

We also lease some of the computer hardware, computer software and office equipment necessary to conduct our business. In addition, we own computer, communications equipment, software and leasehold improvements. We depreciate these assets using the straight-line method over the estimated useful lives of the assets. Leasehold improvements are depreciated over the shorter of their estimated useful life or the term of the associated lease.

We believe that our facilities and equipment are adequate and have sufficient productive capacity to meet our current needs.

Convergys Corporation 2009 Annual Report 11

Table of Contents

Item 3. and 4.

The information required by Item 3 is included in Note 12 of the Notes to Consolidated Financial Statements of this Form 10-K.

Item 4. Submission of Matters to a Vote of the Security Holders

There were no matters submitted to a vote of security holders during the fourth quarter of 2009.

12 Convergys Corporation 2009 Annual Report

Table of Contents

Executive Officers of the Registrant

The following information responds to the provisions of Part III, Item 10.

As of February 26, 2010, our Executive Officers were:

| Name | Age | Title | ||

| Jeffrey H. Fox (a) | 47 | President and Chief Executive Officer | ||

| Earl C. Shanks | 53 | Chief Financial Officer | ||

| Karen R. Bowman | 46 | Senior Vice President, General Counsel and Corporate Secretary | ||

| Clark D. Handy | 53 | Senior Vice President, Human Resources | ||

| Andre S. Valentine | 46 | Senior Vice President, Finance and Controller | ||

| Andrea J. Ayers | 46 | President, Customer Management | ||

| Michael J. Betzer | 48 | Senior Vice President, Relationship Technology Management | ||

| James P. Boyce | 52 | President, Global Sales and Services | ||

| John B. Gibson | 43 | President, HR Management | ||

| Robert A. Lento | 48 | President, Global Information Management | ||

| (a)Member of the Board of Directors.

| ||||

Officers are appointed annually, but are removable at the discretion of the Board of Directors.

JEFFREY H. FOX, President and Chief Executive Officer since February 9, 2010; Principal, The Circumference Group, LLC, since 2009; Chief Executive Officer, The Circumference Group, LLC, 2009-2010; Chief Operating Officer, Alltel Corporation, 2007–2008; Group President – Shared Service, Alltel Corporation, 2003–2007.

EARL C. SHANKS, Chief Financial Officer since November 13, 2003.

KAREN R. BOWMAN, Senior Vice President, General Counsel and Corporate Secretary since September 1, 2007; President, HR Management, 1999–2007.

CLARK D. HANDY, Senior Vice President, Human Resources since December 11, 2006; Executive Vice President, Human Resources of Teleflex, Inc., 2003–2006.

ANDRE S. VALENTINE, Senior Vice President, Finance and Controller since December 7, 2009; Senior Vice President Group Finance, Customer Management, 2002–2009.

ANDREA J. AYERS, President, Customer Management since April 1, 2008; President, Relationship Technology Management, 2007–2008; President, Government and New Markets, 2005–2007.

MICHAEL J. BETZER, Senior Vice President, Relationship Technology Management since May 1, 2008; Vice President, CRM Siebel/Oracle, 2004–2008.

JAMES P. BOYCE, President, Global Sales and Services since January 1, 2009; President, North America Business Units, 2008; President, Communications, Technology, Media, Entertainment and Canada Groups, 2007; President, AT&T Group, 2005–2006.

JOHN B. GIBSON, President, HR Management since September 1, 2007; Senior Vice President, HR Management Client Services, 2007; Senior Vice President, HR Management Global Operations, 2005–2007.

ROBERT A. LENTO, President, Global Information Management since January 1, 2009; President, Information Management, 2007–2008; President, Communications, Technology, Automotive Group, 2003–2007.

Convergys Corporation 2009 Annual Report 13

Table of Contents

PART II

Item 5. Market for the Registrant’s Common Equity, Related

Stockholder Matters and Issuer Purchases of Equity Securities

Convergys Corporation’s shares of common stock, no par value, are listed on the New York Stock Exchange under the symbol “CVG.” As of January 31, 2010, there were 10,315 holders of record of the 123,170,011 common shares of Convergys, excluding amounts held in Treasury (183,333,849 outstanding common shares of Convergys, of which 60,163,838 were held in Treasury).

The high, low and closing prices of our common shares for each quarter in 2009 and 2008 are listed below:

| Quarter | 1st | 2nd | 3rd | 4th | ||||||||

| 2009 | ||||||||||||

| High | $ | 9.05 | $ | 10.66 | $ | 11.51 | $ | 11.97 | ||||

| Low | $ | 5.49 | $ | 7.91 | $ | 8.26 | $ | 9.35 | ||||

| Close | $ | 8.08 | $ | 9.28 | $ | 9.94 | $ | 10.75 | ||||

| 2008 | ||||||||||||

| High | $ | 16.60 | $ | 16.75 | $ | 16.99 | $ | 14.93 | ||||

| Low | $ | 13.66 | $ | 14.62 | $ | 11.77 | $ | 4.02 | ||||

| Close | $ | 15.06 | $ | 14.86 | $ | 14.78 | $ | 6.41 | ||||

We have not paid any cash dividends on our common stock. Our Board of Directors re-evaluates this policy periodically. There is no current anticipation of paying cash dividends in the future.

We did not repurchase any shares of Convergys common stock during 2009 and purchased 7.7 million shares for $116.6 during 2008. At December 31, 2009, the Company has the authority to purchase an additional 7.1 million common shares. The timing and terms of any future transactions depend on a number of considerations including market conditions and our liquidity.

14 Convergys Corporation 2009 Annual Report

Table of Contents

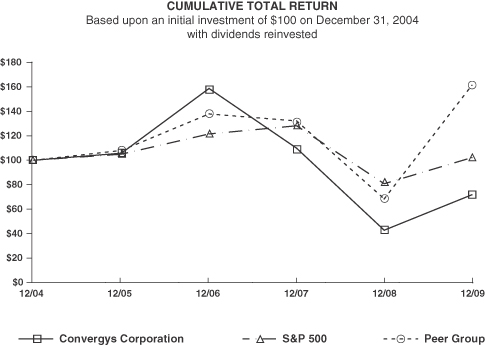

Performance Graph

The following Performance Graph compares, for the period from December 31, 2004 through December 31, 2009, the percentage change of the cumulative total shareholder return on the Company’s shares of common stock with the cumulative total return of the S&P 500 Stock Index and the Peer Group Index, based on an initial investment of $100 on December 31, 2004, with dividends reinvested.

| Dec-04 | Dec-05 | Dec-06 | Dec-07 | Dec-08 | Dec-09 | |||||||

| Convergys Corp. | 100.00 | 105.74 | 158.64 | 109.81 | 42.76 | 71.71 | ||||||

| S&P 500® | 100.00 | 104.91 | 121.48 | 128.16 | 80.74 | 102.11 | ||||||

| Peer Group Index | 100.00 | 107.97 | 137.85 | 132.11 | 68.39 | 161.21 | ||||||

The Peer Group Index consists of Affiliated Computer Services Inc, Amdocs Limited, APAC Customer Services Inc, Comverse Technology Inc, CSG Systems International Inc, Hewitt Associates Inc, ICT Group Inc, Intec Telecom Systems PLC, Sykes Enterprises Inc, Tata Consultancy Services Limited, Teleperformance, Teletech Holdings Inc and Wipro Limited.

Copyright© 2010 Standard & Poor’s, a division of The McGraw-Hill Companies Inc. All rights reserved.

Convergys Corporation 2009 Annual Report 15

Table of Contents

Item 6. Selected Financial Data

| (Amounts in Millions Except Per Share Amounts) | 2009 | 2008 | 2007 | 2006 | 2005 | |||||||||||||||

| Results of Operations | ||||||||||||||||||||

| Revenues (1) | $ | 2,827.2 | $ | 2,785.8 | $ | 2,844.3 | $ | 2,789.8 | $ | 2,582.1 | ||||||||||

| Costs and expenses (2) (3) | 2,940.0 | 2,977.1 | 2,599.5 | 2,536.9 | 2,358.5 | |||||||||||||||

| Operating (loss) income | (112.8 | ) | (191.3 | ) | 244.8 | 252.9 | 223.6 | |||||||||||||

| Equity in earnings of Cellular Partnerships | 41.0 | 35.7 | 14.3 | 11.8 | 12.4 | |||||||||||||||

| Other income (expense), net | (16.9 | ) | 14.3 | 4.0 | 2.7 | (1.4 | ) | |||||||||||||

| Interest expense | (28.9 | ) | (22.6 | ) | (17.5 | ) | (22.8 | ) | (21.2 | ) | ||||||||||

| (Loss) income before income taxes | (117.6 | ) | (163.9 | ) | 245.6 | 244.6 | 213.4 | |||||||||||||

| Income tax (benefit) expense | (40.3 | ) | (71.0 | ) | 76.1 | 78.4 | 90.8 | |||||||||||||

| Net (loss) income | $ | (77.3 | ) | $ | (92.9 | ) | $ | 169.5 | $ | 166.2 | $ | 122.6 | ||||||||

| (Loss) earnings per share: | ||||||||||||||||||||

| Basic |

$ | (0.63 | ) | $ | (0.75 | ) | $ | 1.26 | $ | 1.20 | $ | 0.88 | ||||||||

| Diluted |

$ | (0.63 | ) | $ | (0.75 | ) | $ | 1.23 | $ | 1.17 | $ | 0.86 | ||||||||

| Weighted average common shares outstanding: | ||||||||||||||||||||

| Basic (4) |

122.8 | 123.5 | 134.1 | 138.4 | 140.0 | |||||||||||||||

| Diluted (4) |

122.8 | 123.5 | 137.7 | 141.7 | 142.9 | |||||||||||||||

| Financial Position | ||||||||||||||||||||

| Total assets | $ | 2,613.6 | $ | 2,841.4 | $ | 2,564.2 | $ | 2,540.3 | $ | 2,411.4 | ||||||||||

| Total debt | 469.6 | 665.9 | 259.9 | 343.5 | 432.2 | |||||||||||||||

| Shareholders’ equity | 1,206.4 | 1,150.1 | 1,521.7 | 1,455.1 | 1,355.1 | |||||||||||||||

| Other Data | ||||||||||||||||||||

| Cash provided (used) by: | ||||||||||||||||||||

| Operating activities |

$ | 264.7 | $ | 192.3 | $ | 209.9 | $ | 353.4 | $ | 232.7 | ||||||||||

| Investing activities |

(38.0 | ) | (365.1 | ) | (74.8 | ) | (127.5 | ) | (138.3 | ) | ||||||||||

| Financing activities |

(135.0 | ) | 292.5 | (250.7 | ) | (186.0 | ) | 43.2 | ||||||||||||

| Free cash flow (5) | 189.8 | 100.2 | 108.6 | 256.9 | 206.8 | |||||||||||||||

| (1) | In 2009, we recognized $122.3 of previously deferred implementation revenue resulting from the agreements reached to eliminate future implementation obligations and liabilities for services not yet operational for two large HR Management contracts. See Note 7 of the Notes to Consolidated Financial Statements in this Form 10-K for additional details. |

| (2) | This includes restructuring charges of $47.0, $34.4, $3.4, $12.5 and $21.2 recorded during 2009, 2008, 2007, 2006 and 2005, respectively. |

| (3) | In 2009 and 2008, we incurred $369.2 and $334.0 of implementation-related, settlement and impairment charges, respectively. The 2009 charge of $369.2 includes (a) $255.6 recorded within the cost of providing services and products sold caption representing the expensing of implementation and settlement costs related to two HR Management contracts and (b) $113.6 for impairment of certain long-lived assets. The 2008 charge of $334.0 consists of (a) $65.4 recorded within the cost of providing services and products sold caption, related to excess implementation costs that were expensed rather than capitalized related to two HR Management contracts in accordance with the Company’s accounting policy and (b) $268.6 for impairment of certain long-lived assets including goodwill related to HR Management. |

| (4) | Basic and diluted common shares outstanding at December 31, 2009 were 123.1. |

| (5) | Free cash flow is not defined under accounting principles generally accepted in United States and is calculated as cash flows from operations excluding the impact of the accounts receivable securitization less capital expenditures (net of proceeds from disposal). The Company uses free cash flow to assess the financial performance of the Company. Convergys’ Management believes that free cash flow is useful to investors because it relates the operating cash flow of the Company to the capital that is spent to continue and improve business operations, such as investment in the Company’s existing businesses. Further, free cash flow facilitates Management’s ability to strengthen the Company’s balance sheet, to repay the Company’s debt obligations and to repurchase the Company’s common shares. Limitations associated with the use of free cash flow include that it does not represent the residual cash flow available for discretionary expenditures as it does not incorporate certain cash payments including payments made on capital lease obligations or cash payments for business acquisitions. Management compensates for these limitations by using both the non-GAAP measure, free cash flow, and the GAAP measure, cash from operating activities, in its evaluation of performance. There are no material purposes for which we use this non-GAAP measure beyond the purposes described above. For more detail and a reconciliation of cash flows from operations to free cash flows, see the “Financial Condition, Liquidity and Capital Resources” section in Part 1, Item 7 of this report. |

16 Convergys Corporation 2009 Annual Report

Table of Contents

Item 7. Management’s Discussion and Analysis

of Financial Condition and Results of Operations

(Amounts in Millions Except Per Share Amounts)

The following information should be read in conjunction with our Consolidated Financial Statements and related notes, included elsewhere in this Annual Report on Form 10-K. In addition to historical information, this discussion and analysis may contain forward-looking statements that involve risks, uncertainties and assumptions, which could cause actual results to differ materially from management’s expectations. Please see additional risks and uncertainties described above in the “Safe Harbor Cautionary Statement,” which appears at the beginning of this report and in Part 1, Item 1A. “Risk Factors.”

Overview

Customer Management

Our Customer Management segment, which accounted for approximately 70% of our consolidated revenues in 2009, partners with clients to deliver customer care solutions that enhance the value of their customer relationships, turning the customer experience into a strategic differentiator. As an end-to-end single-source provider of self-service, agent-assisted and proactive care solutions, we combine consulting, innovative technology and agent-assisted services to optimize the customer experience and strengthen customer relationships. Whether contact center operations are on-premises, fully outsourced or blended, we customize our solutions to meet our clients’ needs.

On September 3, 2008, we acquired 100 percent of the outstanding common shares of Intervoice, Inc. (Intervoice), a developer of automated voice response systems, for cash consideration of $338.8. Intervoice is a market leader in the delivery of personalized, multi-channel automated information solutions that connect people with information, empowering them to control the way they interact with a business. Integration of Intervoice’s speech automation and mobile applications with the Company’s agent-assisted services has enabled us to build upon our leadership position in relationship management solutions. Our solutions result in improved operational efficiencies, new revenue streams and, most importantly, enhanced differentiation in the large and growing automated services market. The operating results of Intervoice have been included within the Customer Management segment from the date of the acquisition.

As more fully described under the heading, “Customer Management,” Customer Management revenue increased 2% from the prior year to $1,986.7. Intervoice revenues were $166.3 and $63.3 for 2009 and 2008, respectively. Customer Management 2009 operating income and operating margin were $133.9 and 6.7%, respectively, compared to $92.6 and 4.7% in 2008. The positive gross margin impact from the Intervoice acquisition and operating efficiency improvements within the live-agent business was partially offset by investments in sales and relationship technology resources. Results for 2009 and 2008 also include restructuring charges of $7.9 and $14.0, respectively, to streamline operations.

Information Management

Our Information Management segment serves clients principally by providing and managing complex business support system (BSS) solutions.

In 2009, Information Management accounted for 15% of our consolidated revenues. License and related support and maintenance fees, which accounted for 37% of Information Management revenues for 2009, are earned under perpetual and term license arrangements. Professional and consulting services for installation, implementation, customization, migration, training and managed services accounted for 37% and data processing services accounted for 26% of Information Management revenues in 2009. As more fully described below under the heading “Information Management,” during 2009, Information Management revenue was $434.3, a 24% decline compared to the same period last year due to the negative impact of North American client migrations as well as international project completions partially offset by revenues from new clients. Information Management operating income and operating margin for 2009 were $21.9 and 5.0%, respectively, compared with $96.4 and 16.9%, respectively, in the prior year period. The decline in operating income during 2009 was due to the decline in

Convergys Corporation 2009 Annual Report 17

Table of Contents

Item 7. Management’s Discussion and Analysis

of Financial Condition and Results of Operations (continued)

(Amounts in Millions Except Per Share Amounts)

revenues as well as restructuring charges of $30.4 compared to $9.7 in 2008.

Information Management continues to face competition as well as consolidation within the communications industry. AT&T, our largest client, has substantially migrated its subscribers from the legacy wireless billing system that we supported through a managed services agreement onto AT&T’s other wireless billing system. In addition, AT&T acquired several other Convergys clients that also migrated to this other billing system. The loss of revenue resulting from the AT&T related migrations was approximately $30 in 2009 compared to our 2008 Information Management revenues. This migration was substantially completed by December 31, 2009. We expect revenue loss resulting from the AT&T related migrations to be approximately $40 in 2010 compared to our 2009 Information Management revenues.

In September 2005, Sprint PCS, a large data processing outsourcing client, completed its acquisition of Nextel Communications. In 2006, Sprint Nextel informed us that it intended to consolidate its billing systems onto a competitor’s system. The migration began in 2006 and was fully completed by December 31, 2009. Revenues from Sprint Nextel were down approximately $50 in 2009 compared to the prior year. We expect revenue from Sprint Nextel to be down by approximately $10 in 2010 compared to our 2009 Information Management revenues.

The impact of these client migrations is included in our 2010 guidance detailed in the “Business Outlook” section.

HR Management

Our HR Management segment provides a full range of HR outsourcing solutions including benefits administration, compensation, HR administration, learning, payroll administration, performance management, recruiting and sourcing services to large companies and governmental entities. We standardize HR processes across departments, business lines, language differences and national borders.

HR Management accounted for 15% of our consolidated revenues in 2009 and increased 57% to $406.2 from the prior year. This increase includes accelerated recognition of deferred implementation revenue of $122.3 in 2009 related to two large HR Management contracts. HR Management operating loss for 2009 was $246.1 compared to a loss of $358.8 in the prior year. In addition to the $122.3 of implementation revenue described above, operating results include implementation-related, settlement and impairment charges of $366.1 and $334.0 in 2009 and 2008, respectively. These charges were primarily driven by two large HR Management contracts. The Company restructured both of those large HR Management contracts during 2009 to eliminate future implementation obligations related to services not operational to continue providing services already operational. As a result, all of the capitalized implementation costs related to these contracts were written-off and a portion of implementation revenue, as referenced above, was recognized. Completing the contract restructurings has stabilized the HR Management business and has eliminated the future implementation risk on services not yet operational.

We have undertaken a series of actions intended to improve the future earnings in HR Management. Actions include not signing any new HR Management outsourcing business with significant implementation risk, streamlining existing operations by continuing to use additional automation, standardization and leveraging of off-shore labor, and using partners to implement projects.

18 Convergys Corporation 2009 Annual Report

Table of Contents

Results of Operations

Consolidated Results

| 2009 | 2008 | % Change 09 vs. 08 |

2007 | % Change 08 vs. 07 |

||||||||||||||

| Revenues | $ | 2,827.2 | $ | 2,785.8 | 1 | $ | 2,844.3 | (2 | ) | |||||||||

| Costs and Expenses: | ||||||||||||||||||

| Cost of providing services and products sold (1) | 1,925.8 | 1,892.9 | 2 | 1,837.9 | 3 | |||||||||||||

| Selling, general and administrative expenses | 648.8 | 593.8 | 9 | 554.9 | 7 | |||||||||||||

| Research and development costs |

74.2 | 54.9 | 35 | 73.4 | (25 | ) | ||||||||||||

| Depreciation | 118.9 | 119.0 | — | 115.4 | 3 | |||||||||||||

| Amortization | 11.7 | 13.5 | (13 | ) | 9.0 | 50 | ||||||||||||

| Restructuring charges | 47.0 | 34.4 | 37 | 3.4 | — | |||||||||||||

| Asset impairment | 113.6 | 268.6 | (58 | ) | 5.5 | — | ||||||||||||

| Total costs and expenses |

2,940.0 | 2,977.1 | (1 | ) | 2,599.5 | 15 | ||||||||||||

| Operating (Loss) Income | (112.8 | ) | (191.3 | ) | (41 | ) | 244.8 | — | ||||||||||

| Equity in earnings of Cellular Partnerships | 41.0 | 35.7 | 15 | 14.3 | — | |||||||||||||

| Other income (expense), net | (16.9 | ) | 14.3 | — | 4.0 | — | ||||||||||||

| Interest expense | (28.9 | ) | (22.6 | ) | 28 | (17.5 | ) | 29 | ||||||||||

| (Loss) Income Before Income Taxes | (117.6 | ) | (163.9 | ) | (28 | ) | 245.6 | — | ||||||||||

| Income tax (benefit) expense | (40.3 | ) | (71.0 | ) | (43 | ) | 76.1 | — | ||||||||||

| Net (Loss) Income | $ | (77.3 | ) | $ | (92.9 | ) | (17 | ) | $ | 169.5 | — | |||||||

| Diluted (Loss) Earnings Per Common Share | $ | (0.63 | ) | $ | (0.75 | ) | (16 | ) | $ | 1.23 | — | |||||||

| (1) | Exclusive of depreciation and amortization, with the exception of amortization of deferred charges as disclosed in Note 7 of Notes to Consolidated Financial Statements. |

2009 vs. 2008

Consolidated revenues for 2009 were $2,827.2, up 1% compared to $2,785.8 in the prior year. Growth in revenues from HR Management and Customer Management was partially offset by revenue declines at Information Management. As described more fully under the “HR Management” section below, revenue for 2009 includes $122.3 of previously deferred implementation revenue related to two large HR Management contracts. Customer Management revenues for 2009 and 2008 include $166.3 and $63.3, respectively, from the Intervoice acquisition that closed on September 3, 2008.

Operating loss for 2009 was $112.8 compared to an operating loss of $191.3 in the prior year. As described more fully under the “HR Management” section, the operating results for 2009 include the impact of the $122.3 of HR Management related implementation revenue and the impact of implementation-related, settlement and impairment charges in 2009 and 2008 of $366.1 and $334.0, respectively. The implementation-related, settlement and impairment charges noted above that were recorded both during 2009 and 2008 were primarily driven by two large HR Management contracts. Operating results for 2009 and 2008 also include restructuring charges of $47.0 and $34.4, respectively to streamline operations across the businesses. Excluding the impact of items discussed above, operating income increased slightly in 2009 compared to the prior year.

As a percentage of revenues, the cost of providing services and products sold was 68.1%, compared to 67.9% in the prior year. Decreases in the cost of providing services and products sold as a percentage of revenues both at Customer Management and Information Management were offset by increases at HR Management. The increase in cost of providing services and products sold at HR Management was due to the implementation-related and settlement charges of $255.6 and $65.4 recorded during 2009 and 2008, respectively as described under the “HR Management” section. Selling, general and administrative expenses of $648.8 increased 9% compared to the prior year. The increase was due to higher selling, general and administrative expenses at Customer Management, reflecting higher sales and marketing costs to service the expanded client base and extensive global channel partnerships obtained through the Intervoice acquisition.

Convergys Corporation 2009 Annual Report 19

Table of Contents

Item 7. Management’s Discussion and Analysis

of Financial Condition and Results of Operations (continued)

(Amounts in Millions Except Per Share Amounts)

As a percentage of revenues, selling, general and administrative expenses were 22.9% compared to 21.3% in the prior year. The 35% increase in research and development costs largely reflects our investments in the automated self-care and technology solutions related to the acquired Intervoice platforms.

As discussed more fully under the heading “Restructuring Charges,” we recorded restructuring charges of $47.0 in 2009 versus $34.4 in 2008, largely to streamline operations across the business. In 2009, we recorded equity income in the Cellular Partnerships of $41.0 compared to $35.7 recorded in 2008. Interest expense of $28.9 increased from $22.6 in the prior year reflecting a higher level of debt outstanding during the course of the year. The $16.9 other expense, net was due to higher foreign exchange transaction losses and a $2.3 loss on extinguishment of debt. The prior year income of $14.3 was the result of foreign exchange transaction gains and a $6.0 gain from the termination of treasury lock derivative instruments discussed in more detail in Note 13 of the Notes to Consolidated Financial Statements. The foreign exchange transaction gains and losses arise from transactions denominated in a currency other than the functional currency. As discussed in further detail in the section titled “Market Risk,” we periodically enter into forward exchange contracts to protect the Company against these foreign currency exposures. The gains and losses from these forward exchange contracts are reported within the other income (expense), net caption in the consolidated results of operations. Our effective tax benefit rate was 34.3% for 2009 compared to an effective tax benefit rate of 43.3% in the prior year. The lower tax benefit rate for 2009 is due primarily to the 2009 change of the reinvestment assertion related to certain foreign unremitted earnings, adjustments to income tax reserves and the geographic mix of world-wide income. See Note 15 of the Notes to Consolidated Financial Statements for further discussion related to effective tax rates.

As a result of the factors above, the 2009 net loss and diluted loss per share was $77.3 and $0.63, respectively, compared to net loss and diluted loss per share of $92.9 and $0.75, respectively, in the prior year.

2008 vs. 2007

Consolidated revenues for 2008 were $2,785.8, down 2% from 2007. Growth in revenues from Customer Management and HR Management partially offset by a decline in Information Management. Customer Management revenues for 2008 include revenue of $63.3 from the Intervoice acquisition that closed on September 3, 2008. The operating loss of $191.3 in 2008 was driven by the $334.0 of asset impairment and implementation charges recorded at HR Management as well as a 48% operating income decline at Customer Management and a 26% operating income decline at Information Management. The $334.0 of charges, as more fully described under the heading “HR Management,” reflect challenges with complex implementations, which caused an increase in overall implementation and delivery costs and an assessment of capitalized implementation expenses and goodwill. The 48% Customer Management operating income decline was due to the negative foreign exchange impact as well as higher costs related to investments in consulting and relationship technology resources and infrastructure partially offset by contribution from the Intervoice acquisition. The 26% Information Management operating income decline was driven by revenue declines resulting from North American client migrations as well as project completions. Operating income included restructuring charges of $34.4 and $3.4 during 2008 and 2007, respectively.

As a percentage of revenues, cost of providing services and products sold was 67.9% compared to 64.6% in 2007. The increase was primarily due to increases in cost of providing services and products sold at HR Management, reflecting expensing of the $65.4 of implementation costs as more fully described below under the heading “HR Management.” Selling, general and administrative expenses of $593.8 increased 7% compared to 2007. As a percentage of revenues, selling, general and administrative expenses were 21.3% compared to 19.5% in

20 Convergys Corporation 2009 Annual Report

Table of Contents

2007. The increase was due to higher selling, general and administrative expenses at Customer Management, reflecting additional investments in consulting and relationship technology resources and infrastructure costs. This increase was partially offset by lower selling, general and administrative expenses both at Information Management and HR Management, largely reflecting the benefits from cost saving initiatives. The 25% decrease in research and development costs largely reflects reduced spending at Information Management reflecting our selective approach to research and development spending, focusing our efforts on only what we consider the highest impact areas.

As discussed more fully under the heading, “Restructuring Charges,” we recorded net restructuring charges of $34.4 in 2008 versus $3.4 in 2007. In 2008, we recorded equity income in the Cellular Partnerships of $35.7 compared to $14.3 recorded in 2007. Interest expense of $22.6 increased from $17.5 in 2007 reflecting a higher level of debt resulting from the Intervoice acquisition. The $10.3 increase in other income, net, was primarily due to an increase in our foreign exchange transaction gains. Other income, net also includes a $6.0 gain from termination of treasury lock instruments that was offset by lower interest income in 2008. Our effective tax benefit rate was 43.3% for 2008 compared to an effective tax expense rate of 31.0% for 2007. This relatively high effective tax benefit rate was driven by the asset impairment and implementation charges at HR Management of which a significant portion was not tax deductible, a favorable impact from the resolution of uncertain tax positions (including resolution of tax audits and expiration of statutes of limitations during 2008), and the impact from the higher mix of non-U.S. income that is taxed at lower effective rates.

As a result of the above, net loss and diluted loss per share for 2008 were $92.9 and $0.75, respectively, compared with net income and diluted earnings per share of $169.5 and $1.23, respectively, in 2007.

Customer Management

| 2009 | 2008 | % Change 09 vs. 08 |

2007 | % Change 08 vs. 07 |

||||||||||||||

| Revenues: | ||||||||||||||||||

| Communications | $ | 1,176.0 | $ | 1,140.2 | 3 | $ | 1,075.0 | 6 | ||||||||||

| Technology | 153.9 | 159.5 | (4 | ) | 155.2 | 3 | ||||||||||||

| Financial services | 288.1 | 250.8 | 15 | 259.0 | (3 | ) | ||||||||||||

| Other | 368.7 | 404.3 | (9 | ) | 376.9 | 7 | ||||||||||||

| Total revenues |

1,986.7 | 1,954.8 | 2 | 1,866.1 | 5 | |||||||||||||

| Costs and Expenses: | ||||||||||||||||||

| Cost of providing services and products sold | 1,240.7 | 1,319.4 | (6 | ) | 1,244.1 | 6 | ||||||||||||

| Selling, general and administrative expenses | 507.8 | 454.7 | 12 | 380.7 | 19 | |||||||||||||

| Research and development costs |

22.2 | 8.4 | — | 4.6 | 83 | |||||||||||||

| Depreciation | 66.9 | 61.4 | 9 | 55.9 | 10 | |||||||||||||

| Amortization | 7.3 | 4.3 | 70 | 2.7 | 59 | |||||||||||||

| Restructuring charges | 7.9 | 14.0 | (44 | ) | — | — | ||||||||||||

| Asset impairment | — | — | — | 1.4 | (100 | ) | ||||||||||||

| Total costs and expenses |

1,852.8 | 1,862.2 | (1 | ) | 1,689.4 | 10 | ||||||||||||

| Operating Income | $ | 133.9 | $ | 92.6 | 45 | $ | 176.7 | (48 | ) | |||||||||

| Operating Margin |

6.7 | % | 4.7 | % | 9.5 | % | ||||||||||||

2009 vs. 2008

Revenues

Customer Management revenues for 2009 were $1,986.7, up 2% from 2008. This includes $166.3 and $63.3 in 2009 and 2008, respectively, in revenue from the Intervoice acquisition that closed on September 3, 2008.

Revenues from the communications vertical increased 3% from the prior year. Growth with our largest communications client and from the Intervoice acquisition was partially offset by a reduction in spending with a few communications clients largely due to the decline in their volumes, as well as a shift in our revenue mix for several of our clients from North America to off-shore locations.

Convergys Corporation 2009 Annual Report 21

Table of Contents

Item 7. Management’s Discussion and Analysis

of Financial Condition and Results of Operations (continued)

(Amounts in Millions Except Per Share Amounts)

Revenues from the financial services vertical increased 15%, primarily reflecting growth from the Intervoice acquisition as well as from new collections programs in the current year. Other revenues, which are comprised of clients outside of Customer Management’s largest industries, decreased 9% from the prior year. A decline in revenues from several retail and automotive clients as a result of the softness in the current economic environment were partially offset by growth from the Intervoice acquisition.

Costs and Expenses

Customer Management total costs and expenses were $1,852.8, a 1% decrease from the prior year. Customer Management cost of providing services and products sold decreased 6% to $1,240.7 from the prior year. As a percentage of revenues, cost of providing services and products sold was 62.5% for 2009, down 500 basis points from 67.5% in the prior year, due to effective live-agent workforce management, as well as positive contributions from the Intervoice acquisition. Selling, general and administrative expenses of $507.8 increased 12% compared to the prior year. This largely reflects higher sales and marketing costs to service the expanded client base and extensive global channel partnerships obtained through the Intervoice acquisition. As a percentage of revenues, selling, general and administrative expenses were 25.6% for 2009 compared to 23.3% in the prior year. The $13.8 increase in research and development costs reflects investments in the automated self-care and technology solutions related to the acquired Intervoice platforms. Compared to the prior year, the 9% increase in depreciation expense and the 70% increase in amortization expense reflect depreciation and amortization of the assets acquired through the Intervoice acquisition. As discussed more fully under the heading, “Restructuring Charges,” we recorded restructuring charges of $7.9 and $14.0 during 2009 and 2008, respectively, to better align cost structure to future business needs.

Operating results also include a favorable foreign currency impact of approximately 30 basis points. Customer Management serves a number of its U.S.-based clients using contact center capacity in the Philippines, India and Canada. Although the contracts with these clients are typically priced in U.S. dollars, a substantial portion of the costs incurred to operate these non-U.S. contact centers is denominated in Philippine pesos, Indian rupees or Canadian dollars, which represents a foreign exchange exposure. As discussed in further detail in the section titled “Market Risk,” we hedge this exposure by entering into foreign currency forward contracts and options to limit potential foreign currency exposure. We enter into these derivative instruments on a periodic basis over time and, therefore, the 2009 earnings impact is determined based on the difference in the extent of our hedged exposures as well as changes in foreign exchange rates between 2009 and 2008.

Operating Income