Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2009

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _______ to ________

Commission File Number: 333-134090

Intcomex, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 65-0893400 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

3505 NW 107th Avenue,

Miami, FL 33178

(Address of principal executive offices) (Zip Code)

(305) 477-6230

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class |

Name of Each Exchange on Which Registered | |

| None |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes x No ¨

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ¨ No x

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark if registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The registrant had 100,000 shares of Common Stock, voting, par value $0.01 per share and 29,357 shares of Class B Common Stock, non-voting par value $0.01 per share, outstanding at December 31, 2009. There is no public trading market for the stock.

DOCUMENTS INCORPORATED BY REFERENCE:

None

Table of Contents

| PART I | ||||

| Item 1. |

1 | |||

| Item 1A. |

10 | |||

| Item 1B. |

21 | |||

| Item 2. |

21 | |||

| Item 3. |

22 | |||

| Item 4. |

22 | |||

| PART II | ||||

| Item 5. |

23 | |||

| Item 6. |

23 | |||

| Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

25 | ||

| Item 7A. |

42 | |||

| Item 8. |

43 | |||

| Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

84 | ||

| Item 9A(T). |

84 | |||

| Item 9B. |

85 | |||

| PART III | ||||

| Item 10. |

85 | |||

| Item 11. |

89 | |||

| Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

97 | ||

| Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

99 | ||

| Item 14. |

100 | |||

| PART IV | ||||

| Item 15. |

101 | |||

| SIGNATURES | ||||

Table of Contents

PART I

| Item 1. | Business. |

Company

We believe Intcomex, Inc. and its subsidiaries (“Intcomex,” the “Company”, “we,” “us,” or “our”) is the largest pure play value-added international distributor of computer information technology (“IT”) products focused solely on serving Latin America and the Caribbean (the “Region”). We distribute computer equipment, components, peripherals, software, computer systems, accessories, networking products and digital consumer electronics to more than 50,000 customers in 40 countries. We offer single source purchasing to our customers by providing an in-stock selection of more than 6,100 products from over 173 vendors, including many of the world’s leading IT product manufacturers. We serve the Latin American and Caribbean IT products markets using a dual distribution model as a wholesale aggregator and an in-country distributor:

| • | As a Miami-based wholesale aggregator, we sell primarily to: |

| • | third-party distributors, resellers and retailers of IT products based in countries in Latin America and the Caribbean where we do not have a local presence; |

| • | third-party distributors, resellers and retailers of IT products based in countries in Latin America and the Caribbean where we have a local presence but whose volumes are large enough to enable them to efficiently acquire products directly from United States (“U.S.”)-based wholesale aggregators; |

| • | other Miami-based exporters of IT products to Latin America and the Caribbean; and |

| • | our in-country operations. |

| • | As an in-country distributor in 12 countries, we sell to over 48,000 local reseller and retailer customers, including value-added resellers (companies that sell, install and support IT products and personal computers (“PCs”)), systems builders (companies that specialize in building complete computer systems by combining components from different vendors), smaller distributors and retailers. |

History

Anthony Shalom and Michael Shalom (the “Shaloms”) founded our Company as a small software retailer in South Florida in 1988. In 1989, we started selling IT products from Miami, Florida (“Miami”) to Latin America and moved our headquarters to the Port of Miami and the Miami International Airport vicinity, in order to capitalize on the growing export trade of IT products to Latin America and the Caribbean. We established our first in-country operation in Mexico in 1990, and expanded our presence to Chile and Panama in 1994; Guatemala, Peru and Uruguay in 1997; Costa Rica, Ecuador, El Salvador and Jamaica in 2000; Argentina in 2003; and Colombia in 2004. Our growth into each market has been largely organic, typically in partnership with talented local managers knowledgeable about the IT products distribution business in their respective country.

In 2001, we exchanged our interest in Centel S.A. de C.V. (“Centel”), our then-existing Mexican operations, with Centel’s management, for all of the shares of Intcomex held by Centel’s management. In June 2005, we re-established our presence in Mexico by re-acquiring all of our interest in Centel.

In August 2004, Citigroup Venture Capital International (“CVC International”), a unit of Citigroup Inc. engaged in private equity investments in emerging markets, acquired 52.5% of our voting equity interests. As part of that transaction, we redeemed all of the equity interests in our Company held by our former non-management shareholders and some of the equity interests in our Company held by our management shareholders. We incorporated in the state of Delaware in August 2004. After giving effect to the acquisition and redemptions, Anthony Shalom and Michael Shalom became our second and third largest shareholders after CVC International, with holdings of 23.0% and 9.0%, respectively, of our voting common stock. Our other shareholders, also members of our management, entered into a shareholders agreement providing for, among other things, certain governance arrangements concerning the Company.

In December 2009, certain of our Company’s existing shareholders and their affiliates contributed $20.0 million of new capital in exchange for newly-issued shares of our Class B common stock, non-voting. Following the capital contribution, CVC International maintained 52.5% of our voting equity interests and held 47.6% of our non-voting common stock. Anthony Shalom and Michael Shalom remain our second and third largest shareholders after CVC International, with holdings of 23.0% and 9.0%, respectively, of our voting equity interests and each holds 6.1% of our non-voting common stock.

1

Table of Contents

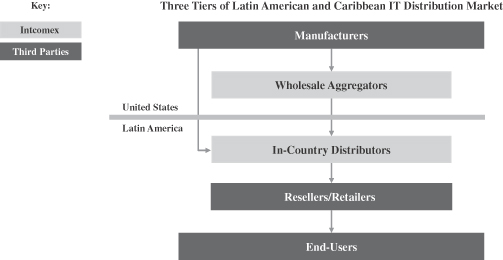

Industry

IT products generally follow a three-tiered distribution system from the manufacturer to end-users in Latin America and the Caribbean:

| • | Wholesale aggregators like our Miami-based operations purchase IT products from vendors and sell them to other Miami-based exporters and in-country distributors. They typically maintain warehouses and sales forces in Miami and do not have substantial operations outside of Miami. |

| • | In-country distributors like our in-country operations purchase IT products from wholesale aggregators and sell them to local resellers and retailers. They typically have a geographic focus limited to one country or cities within one country and a local sales force in direct contact with their customers and local warehousing. In-country distributors’ limited size, capital and geographic reach often prevent them from establishing and maintaining direct relationships with vendors located predominantly in the U.S. and Asia who focus their relationships on IT distributors with broad geographic coverage or large order sizes. In most markets, in-country distributors typically lack sufficient size to benefit from significant economies of scale and are not adequately capitalized to offer a full range of products and services to their customers. |

| • | Resellers typically acquire IT products from the in-country distributors and resell them to end-users, typically individuals, small and medium-sized businesses or governments. Resellers vary greatly in size and type from one-person operations to large retailers. |

The distribution model for IT products in the Latin American and Caribbean markets is distinctly different from more advanced markets where direct sales by IT vendors are common. IT vendors rely extensively on wholesale distribution rather than direct sales. According to International Data Corporation (“IDC”), a market intelligence and advisory firm in the IT and telecommunications industries, IT distributors (including local dealers, resellers, retailers and assemblers) comprised about 69% of PCs sold in Latin America and the Caribbean, while the remaining 31% were sold directly to end-users through the internet and original equipment manufacturer (“OEM”) direct sales forces in 2008.

Latin America and the Caribbean are comprised of more than 45 countries, many unique with respect to their logistical infrastructure, regulatory and legal framework, trade barriers, taxation, currency and language. This fragmentation presents challenges to IT product manufacturers seeking to establish a regional distribution, sales, logistics and service network, because such a network would have to be created separately for each country, with limited economies of scale due to the small size of most markets and barriers to entry associated with cross-border complexities. We believe that our dual distribution model, as well as our extensive geographic presence in the Region, is not only unique, but also valuable to our vendors and customers and difficult to replicate.

The IT products distribution industry is driven by sales to end-users. From 1998 to 2008, spending on IT products (including hardware, packaged software and services) in Latin America and the Caribbean grew at approximately 3.6% per year, from $41.3 billion to $58.7 billion. According to IDC, spending is projected to grow an average of 5.8% per year from 2009 to 2013, to $74.3 billion. While the Latin American and Caribbean population of approximately 568 million people is 86.9% larger than that of the U.S., the market in 2008 for IT products in the Region was only 11.6% of the size of the market for IT products in the U.S.

The growth in IT spending in Latin America and the Caribbean is attributed mainly to increasing PC penetration rates, rapidly increasing Internet penetration rates and increasing access to consumer credit.

2

Table of Contents

Operations

Our Regional Presence

We operate a sales and distribution center in the U.S., 22 sales and distribution centers in Latin America and the Caribbean and a sales office in Brazil. We believe we have the broadest geographical scope of any IT distributor in Latin America and the Caribbean, with in-country operations in 12 countries — Argentina, Chile, Colombia, Costa Rica, Ecuador, El Salvador, Guatemala, Jamaica, Mexico, Panama, Peru and Uruguay (collectively, our “In-country Operations”).

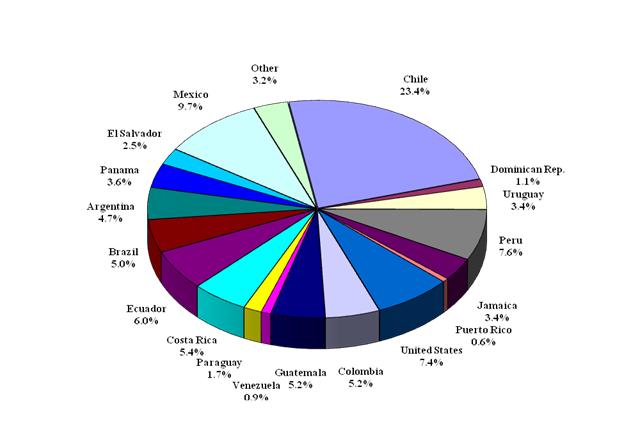

Revenue derived from sales to customers located in Latin America and the Caribbean accounted for almost all of our consolidated revenue for the years ended December 31, 2009, 2008 and 2007. The following chart shows our revenue for the year ended December 31, 2009, by our customers’ country of origin.

2009 Percentage of Revenue by Customers’ Country of Origin

*Other includes 22 other countries, each representing less than 1% of our 2009 revenue.

Our Miami Operations

Our Miami Operations serves as the headquarters for our entire Company (our “Miami Operations”). Our Miami Operations handles purchases from our vendors, and a majority of the products that we acquire from our vendors pass through our Miami warehouse (with the exception of products sourced from Asia, which are usually shipped directly to our In-country Operations). Our Miami Operations supplies our 22 in-country sales and distribution centers and also sells products directly to third parties. Miami third-party customers include U.S., Latin American and Caribbean distributors, resellers and retailers, who in turn, distribute or sell products throughout Latin America and the Caribbean.

Our Miami purchasing department handles most of our vendor relationships and contracts. Our Miami Operations monitors our entire inventory pipeline on an ongoing basis and uses information regarding the levels of inventory, in conjunction with input from the in-country managers regarding our customer demand patterns, to place orders with vendors. The centralization of our purchasing function allows our In-country Operations to focus attention on more country-specific issues such as sales, local marketing, credit control and collections. The centralization of purchasing also allows our Miami Operations to maintain the records with regard to all vendor back-end rebates, promotions and incentives to ensure they are collected and to adjust pricing of products accordingly.

3

Table of Contents

Our Miami distribution center typically ships products to each of our in-country sales and distribution operations twice a week by air and once a week by sea. These frequent shipments facilitate more efficient inventory management and increased inventory turnover. Generally, we do not have long-term contracts with logistics providers, except in Mexico and Chile. Where we do not have long-term contracts, we seek to obtain the best rates and fastest delivery times on a shipment-by-shipment basis. Our Miami Operations coordinates direct shipments to third-party customers and In-country Operations from vendors in Asia.

We have sales and marketing staff located in our Miami headquarters. For a detailed discussion of our sales and marketing staff, see “—Customers, Sales and Marketing.” Other functions performed in our Miami headquarters include human resources, treasury and accounting, strategic planning, consolidated information systems development and maintenance and overall marketing strategy.

As of December 31, 2009, 2008 and 2007, our Miami Operations total assets were $126.4 million, $119.1 million and $185.6 million, respectively. For detailed information of our revenue from our Miami Operations, see Part II, Item 8. Financial Statements and Supplemental Data, of this Annual Report.

Our In-country Operations

Each of our in-country sales and distribution operations has a local sales force and substantial inventory, with the exception of our operations in Brazil, which consist solely of a sales office. Our In-country Operations sells to more than 48,000 customers in 12 countries.

Each of our In-country Operations is critical to meeting the needs of local resellers and retailers which are often small, locally owned companies that lack the size and the knowledge to buy directly from the U.S. or Asia and to handle customs processing, including taxes and duties. By selling directly to resellers and retailers from locally-based facilities, our In-country Operations provides a competitive advantage over other multinational companies that export products into those markets. We believe that we offer our customers some of the shortest product delivery times in the industry by leveraging our capabilities as a Miami-based aggregator and as an in-country distributor. Our local presence also allows us to obtain timely and accurate information with respect to each market’s growth potential and the needs of the customers in each market.

Each of our In-country Operations is responsible for the following functions: sales, human resources, local marketing, extension of credit (in compliance with our corporate credit policies), collections, inventory controls, local accounting and financial controls, shipping to customers when needed and providing local input and data from their IT systems to Miami for purchasing decisions.

As of December 31, 2009, 2008 and 2007, our In-country Operations total assets were $181.7 million, $165.0 million and $177.4 million, respectively. For detailed information of our revenue from In-country Operations, see Part II, Item 8. Financial Statements and Supplemental Data, of this Annual Report.

Products

We offer single source purchasing to our reseller and retailer customers so they can purchase all of their IT product needs from us, including computer products, components and peripherals. We believe that our wide selection of products is a key attraction for resellers and retailers to purchase products from us. The single source purchasing concept is especially important for assemblers of unbranded or “white-box” PCs, who must source all the necessary components before the assembly process begins. White-box PCs typically have lower retail selling prices but higher margins than branded computer systems. According to Gartner, Inc. (“Gartner”), a provider of research and analysis on the global IT industry, in 2008 white-box personal computers comprised about 47.2% of the Latin American and Caribbean personal computer market, by shipments. We do not focus on selling branded desktop PCs other than our own Hurricane operating PCs, Blue Code PC kits and PCs we assemble under our customers’ brands.

Our in-country product lines typically include between 1,500 and 2,500 products in stock. Our catalog of products offers a broad selection that demonstrates our focus on responding to market demands, reflecting increasing demand for portable computing devices such as notebook computers and netbooks, bare-bones notebook computers designed specifically for web browsing, multimedia access and gaming, and mobile and ultra portable products. The breadth and diversity of our product lines allows us a key competitive advantage by enhancing our leadership position in the IT distribution industry and mitigating the risks inherent in our strong, competitive market. Based on our estimates, we believe that many of our local competitors have product lines of no more than 200 to 300 products in stock. The following table presents the percentage of our consolidated revenue represented by our product categories in each of the last three years:

4

Table of Contents

| Year Ended December 31, | |||||||||

| Category |

2009 | 2008 | 2007 | ||||||

| Components |

36.9 | % | 40.3 | % | 46.5 | % | |||

| Peripherals |

15.8 | % | 16.7 | % | 16.8 | % | |||

| Software |

6.4 | % | 6.6 | % | 6.8 | % | |||

| Computer systems |

28.0 | % | 24.2 | % | 17.4 | % | |||

| Accessories |

8.4 | % | 6.2 | % | 6.9 | % | |||

| Networking |

2.6 | % | 2.7 | % | 2.5 | % | |||

| Other products |

1.9 | % | 3.3 | % | 3.1 | % | |||

| Total |

100.0 | % | 100.0 | % | 100.0 | % | |||

Our product categories are:

| • | Components. This category consists of the components that are the basic building blocks of a PC and includes motherboards, processors, memory chips, internal hard drives, internal optical drives, cases and monitors. |

| • | Peripherals. This category consists of devices that are used in conjunction with computer systems and includes printers, power protection/backup devices, mice, scanners, external disk drives, storage devices, multimedia peripherals, modems, projectors and digital cameras. |

| • | Software. This category consists of operating system, security and anti-virus software. |

| • | Computer systems. This category consists of self-standing computer systems capable of functioning independently, including notebook computers and netbooks. In most of our operations, we assemble and sell PC and notebook computers under our own brands, under our customers’ brands and in unbranded cases. |

| • | Accessories. This category consists of computer cables, connectors, computer and networking tools, media, media storage, keyboard and mouse accessories, speakers, computer furniture and networking accessories. |

| • | Networking. This category consists of hardware that enables two or more PCs to communicate, and includes adapters, modems, routers, switches, hubs and wireless local area network (“LAN”) access points and interface cards. |

| • | Other products. This category consists of digital consumer electronics and special order products. |

We focus primarily on components, peripherals, software and accessories categories, as these product categories tend to have higher margins than the other product categories. We believe our focus on these product categories and our attention to the vendor price protection policies described below under “—Vendors,” help us reduce the risks associated with inventory obsolescence. We believe that our inventory obsolescence rates of (0.1)%, 0.17% and 0.12% of revenue for the years ended December 31, 2009, 2008 and 2007, respectively, are very low by industry standards. One of our strategies is to maintain our core mix of product categories, in particular, to maintain high levels of sales in the components category as more people in Latin America and the Caribbean become computer users.

Sales in our computer systems product category increased to 28.0% of our consolidated revenue as of December 31, 2009 from 24.2% of our consolidated revenue as of December 31, 2008. We believe this reflects increasing customer demand for portable computing devices such as notebook computers and netbooks, barebones notebook computers designed specifically for web browsing, multimedia access and gaming devices. Notebook computers and netbooks serve as a portable solution for accessing the web’s multimedia alternatives. Due to the increase in market demand for mobile and ultraportable products represented by our computer systems category, the percentage of products in our components product category declined from prior year levels.

Among our growth strategies is the expansion of our offerings in the following product categories or subcategories: enterprise-class networking products (including networking products, servers, storage and software), enterprise IP telephony products (including IP, PBX systems and IP telephones), gaming and “infotainment” products (including video game systems), digital consumer electronics (including digital cameras and plasma displays) and products sold under our proprietary brands (for example, Hurricane). We plan to expand into these product categories or subcategories gradually as demand for these products grows among our customers and end user markets, our existing vendors begin to offer these products and as we initiate relationships with new vendors offering these products.

Vendors

We have established long-term direct relationships with many of the major global manufacturers of branded computer products, including Apple, Dell, Epson, Hewlett Packard, Intel, Kingston, Microsoft, Samsung, Seagate, Toshiba and Western Digital, as well as a number of generic component vendors from the U.S. and Asia. For the years ended December 31, 2009, 2008 and 2007, our top

5

Table of Contents

10 vendors manufactured products that accounted for 66.1%, 65.5% and 64.6%, respectively, of our total revenue and the products of our top vendor accounted for 19.1%, 17.5% and 16.7%, respectively, of our total revenue. We continue to believe in the strategic importance of diversifying our revenues among multiple vendors.

We have entered into written distribution agreements, which provide for nonexclusive distribution rights for specific territories with many of our vendors. The distribution agreements are generally short-term and subject to periodic renewal. We believe it is not common for vendors in our industry to have exclusive relationships with distributors. We also believe our customers are better served by our ability to carry a breadth of competing brands because the IT products market is subject to rapid change and reliant upon product innovation. Our vendors typically extend to us payment terms of between 30 and 60 days. Vendors of branded products often offer to us back-end rebates, promotions and incentives, to drive sales of their products.

Like other IT distributors, we are subject to the risk that the value of our inventory will be affected adversely by vendors’ price reductions or by technological changes affecting the usefulness or desirability of the products comprising our inventory. It is the policy of many vendors of IT products to offer distributors like us, who purchase directly from them, some protection from the loss in value of inventory due to technological change or a vendor’s price reductions. Under many of these agreements, there is only a limited, specified period of time in which the distributor may return products for credit, exchange products for other products or claim price protection credits. We take various actions to maximize our participation in these vendor approved programs and reduce our inventory risk including monitoring our inventory levels, soliciting frequent input from in-country managers about demand projections and controlling the timing of purchases.

Although we do not offer our own rebates or price protection to our customers, we provide some of the benefits of vendor-sponsored rebates. When we sell a product, we issue to our customer a product warranty with the same terms as the vendor’s product warranty issued to us. We track the unique serial numbers of all products passing through each of our distribution facilities which enables us to determine whether specific products under product warranty presented by our customers of our In-country Operations for service or repair benefit from the product warranty issued by us. This tracking system allows us to limit the quantity of unauthorized returns of merchandise and provide fast, high quality return-to-manufacturer authorization (“RMA”) service across Latin America and the Caribbean. We incurred expenses in administering the warranties issued to our customers of $1.7 million, $2.4 million and $1.5 million for the years ended December 31, 2009, 2008 and 2007, respectively.

Customers, Sales and Marketing

Customers

We currently sell to over 50,000 distributors, resellers and retailers in 40 countries. Although the end users of our products are mostly individuals and small and medium-sized businesses, we supply these end users through a well-established network of in-country distributors, value-added resellers, system builders and retailers, as well as through U.S.-based distributors selling into the Region. We have always emphasized customer care and long-term customer development. We seek to build customer loyalty not only by having wide product selection and quick delivery times, but also by offering customs and duties payment management, marketing assistance, product training, new product exposure, technical support and local warranty service and by providing trade credit (when the customer is approved under our credit policies). We believe that the extension of payment terms to creditworthy customers is one of our key competitive advantages. Many of our local competitors do not have the financial resources to do so and, as a result, offer products only on a cash-and-carry basis.

For the years ended December 31, 2009, 2008 and 2007, no single customer accounted for more than 2.0% of our consolidated revenue and the top 10 customers by sales volume accounted for less than 10.4%, 9.0% and 9.5%, respectively, of our consolidated revenue. Our strategy is to not rely on any single customer for a large percentage of sales, but to diversify our revenues and maximize sales from a large quantity of individual customers.

Sales

As of December 31, 2009, we maintained a sales force of 342 people in our In-country Operations and 29 employees in our Miami Operations dedicated to serving our third-party customers. Each in-country sales force is managed by a general manager and, in some cases, a sales manager, depending on the size of the operation. The general managers and sales managers are responsible for developing and maintaining relationships with new and existing customers. Our Chief Executive Officer also spends a considerable amount of time visiting customers and our In-country Operations to develop new customer accounts and solidify and improve existing relationships.

We use an incentive-based compensation structure for our sales force that varies from country to country. Generally, the compensation consists of a base salary and variable commission or bonus, based on pre-established sales and performance metrics. The commission is generally calculated as a percentage of collected gross profits and net customer additions.

6

Table of Contents

Marketing

As of December 31, 2009, our marketing department consisted of five employees in Miami and 39 employees throughout Latin America and the Caribbean. The marketing department’s responsibilities include oversight of our corporate identity, preparation of marketing materials, creation and coordination of various types of media activity and development of marketing research studies and specialized reseller-focused events. In addition, the marketing department works with vendors to establish periodic marketing and sales programs to generate vendor brand awareness and product demand, acting as a liaison between our company and our vendors.

Our marketing department uses marketing and business development funds available from vendors of branded IT products for various activities, including the preparation of our annual product catalog and monthly pricing books, customer training, specialized events and trade shows. Our Miami Operations administers a majority of the marketing funds and distributes them as needed to our In-country Operations.

Some of our more notable marketing events include quarterly IT educational and training seminars offered by vendors for our sales executives and channel customers in Latin America and the Caribbean in order to introduce new products and programs, present product roadmaps, launches and promotions and provide strategies aimed at enhancing selling skills.

Promotional Floordays are conducted weekly throughout the Region, in which vendors interact with and showcase products and solutions to reseller customers and sales executives and provide individualized training and test drives of the products. Our regional Intcomex Product Catalog is published semi-annually and includes over 1,500 products in 45 categories.

IntcomExpo is our annual private, regional trade show in which 15 to 30 vendors present their products. These expos are held throughout the year in several of our In-country locations.

I-Blasts and interactive email signatures are used to promote our vendor’s brand directly to our customers. When our sales executives send an email, our vendor’s banner appears under the electronic signature and our customers can access the vendor’s promotions and Intcomex’s Webstore directly by clicking on the banner.

Intcomex Marketing on Hold is a unique method of advertising that allows our vendors to promote their products to our customers on a daily basis. We play an advertisement of the vendor’s products, brand and latest releases on large screen televisions in the Region that customers can view as they await or obtain quotations. Internal communications also showcase vendors’ products on large screen televisions in the Region in the form of slideshows and short movies that run continuously between promotions. The television advertisements are a convenient format for introducing new products and programs to our customers.

Reseller training labs are seminar events designed to introduce new products, provide product and technology information and selling techniques to resellers.

Intcomex WebStore is our e-commerce store located at http://store.intcomex.com which offers our products to our resellers and customers to search products by category, subcategory, name or stock-keeping unit (or SKU), compare product specifications, review product quotations and prices and purchase products.

Credit Risk Management

We extend payment terms, generally up to 30 days, to creditworthy customers of our Miami Operations and most of our In-country Operations, although some higher-volume customers, such as large retailers, receive longer payment terms. In our In-country Operations (most notably Mexico, where sales are primarily on a cash-and-carry basis), we modify our credit policies on a country-by-country basis depending mostly on local macroeconomic conditions, the nature of our customers and local market practices.

We have established standardized credit policies for our Miami Operations and our In-country Operations. Our credit policies include credit analysis, credit database checks, vendor and bank relationship checks and, where necessary, collateralization. In addition, substantially all of our Miami Operations’ foreign accounts receivable (other than accounts receivable owed by affiliates) are insured by Euler Hermes American Credit Indemnity Company (“Euler Hermes ACI”), a worldwide credit insurance company. The policy’s aggregate limit is $20.0 million with an aggregate deductible of $1.5 million; the policy expires on August 31, 2010. Under this insurance, 10% or 20% buyer coinsurance provisions and sub-limits in coverage on a per-buyer and on a per-country basis apply. The policy also covers certain large, local companies that purchase directly from our In-country Operations in Argentina, Costa Rica, El Salvador, Guatemala, Jamaica and Peru. Our In-country operations in Chile insures certain customer accounts with Coface Chile, S.A. credit insurance company; the policy expires on October 31, 2010.

We believe that our relatively low bad debt expenses of 0.5%, 0.4% and 0.2% of net revenues for the years ended December 31, 2009, 2008 and 2007, respectively, are a result of our standardized credit policies, our close and proactive monitoring of accounts receivables and collections by our Miami Operations, our In-country Operations and the diversification of our receivables over a large number of countries and customers. We have become more cautious in extending credit to our customers due to the recent financial

7

Table of Contents

and economic crisis. Most of our larger credit losses relate to customers of our Miami Operations, where we sell to large volume customers, who in some cases, are afforded credit lines in excess of $100,000. Credit losses have been nominal in our In-country Operations where credit lines typically do not exceed $10,000.

Information Systems

In 2009, we continued the process of installing Sentai, our company-wide enterprise resource planning (“ERP”), management and financial reporting system. Sentai is a scalable IT ERP system that enables simultaneous decentralized decision-making by our employees included in sales and purchasing while permitting control of daily operating functions by our senior management. We are also using the Sentai logistics and inventory management system in order to better manage our increasing shipping volumes. The ERP system has been implemented in our Miami Operations and in 11 of our 12 In-country Operations. We completed the implementation of our core ERP system in Chile and some portions of Mexico in 2009 and expect to complete the remaining areas of Mexico in early 2010.

In 2008, we implemented SAP Business Planning and Consolidation (“SAP BPC”), our company-wide management planning, budgeting and forecasting system. SAP BPC is a comprehensive financial management system that enables complete budgeting, forecasting, consolidation and reporting functionality through a single application and user interface.

In 2008, we started the process of implementing our e-commerce sales platform which will help maximize online revenues and reduce costs and risks associated with running our e-commerce operation. The e-commerce infrastructure includes site development and hosting, order management and merchandising, reporting and analytics, product fulfillment and multilingual customer service. Our e-commerce platform is a centralized system and critical solution to serving our Miami and in-country customers through rich functionality to deliver large volume transactions in an integrated environment. We expect to complete implementation in each of our In-country Operations in 2010.

Competition

The IT products distribution industry in Latin America and the Caribbean is highly competitive. The factors on which we compete include:

| • | price; |

| • | availability and quality of products and services; |

| • | terms and conditions of sale; |

| • | availability of credit and payment terms; |

| • | timeliness of delivery; |

| • | flexibility in tailoring specific solutions to customers’ needs; |

| • | effectiveness of marketing and sales programs; |

| • | availability of technical and product information; and |

| • | availability and effectiveness of warranty programs. |

The IT products distribution industry in Latin America and the Caribbean is very fragmented and contains several public multinational companies, which we refer to as our public company competitors, such as Ingram Micro (in-country operations in Brazil, Chile, Mexico, Peru and Argentina), Tech Data (in-country operations in Brazil, Chile, Mexico, Peru and Uruguay), Bell Microproducts (in-country operations in Argentina, Brazil, Chile and Mexico) and SYNNEX (in-country operations in Mexico) and a large number of local companies that operate in a single country, such as Grupo Deltron S.A. in Peru, Airoldi Computación in Argentina and Makro Computo in Colombia. We believe we have the broadest in-country presence in Latin America and the Caribbean in terms of the number of countries served through an in-country presence.

Our principal public company competitors are Ingram Micro and Tech Data, each of which operates local distribution centers in the limited number of markets listed previously. In contrast, we are able to offer our vendors a broader in-country distribution channel in more Latin American and Caribbean markets than these competitors. Additionally, while our product offering is more focused on components for white-box PCs, Ingram Micro and Tech Data are focused on high-end branded equipment, including servers. While these competitors are larger and better capitalized than we are, and, in the case of the Mexican market, have a significantly larger market share than we do, we believe that our multi-country, components-focused business model is better suited to serve our customers located in Latin America and the Caribbean.

Our relatively large size provides us with certain advantages over smaller local distributors, who sometimes have a lower cost structure than we do partially because we believe they may operate in the grey market or “informal” economy. We believe our advantages generally include more developed vendor relationships, broader product offerings, greater product availability and more extensive customer service including credit and technical support.

8

Table of Contents

Our participation at two levels of the distribution chain (Miami and in-country), coupled with our extensive geographic footprint, creates a market presence that we believe is unmatched by any of our public company competitors in terms of the number of countries served through an in-country presence and enables us to generate industry-leading margins among our public company competitors. Our dual distribution approach links a diversified set of vendors, primarily located in the U.S. and Asia, to a fragmented number of customers spread throughout Latin America and the Caribbean, and delivers value to both ends of the supply chain. To our vendors, we provide access to markets and customers that would be costly and inefficient for them to reach directly. To our customers, which are often small local resellers and retailers that lack the scale and access to buy directly from the U.S. and Asia, we provide broad and timely product availability, local staff, multi-vendor single source purchasing, technical support, customs management and local warranty service.

Trademarks and Domain Names

We have registered a number of trademarks and domain names for use in our business. Our registered trademarks include “Intcomex,” “Blue Code,” “CENTEL,” “FORZA,” “Hurricane,” “KLIP,” “KLIP XTREME,” and “NEXXT Solutions” in the U.S. and/or in various Latin American and Caribbean jurisdictions. We also have registered domain names, including “intcomex.com,” “nexxtsolutions.com,” “intcomex.cl,” “intcomex.ec” and “intcomex.com.pe.” We believe that our trademarks help us build name recognition in the region in which we operate.

Market and Industry Data

Market and industry data used throughout this Annual Report on Form 10-K (“Annual Report”) were obtained from our internal surveys, industry publications, unpublished industry data and estimates, discussions with industry sources and currently available information. The sources for this data include IDC and Gartner. Industry publications generally state that the information contained therein has been obtained from sources believed to be reliable, but there can be no assurance as to the accuracy and completeness of such information. Based on our familiarity with the market, we believe that estimates by these third party sources are reliable; however, we have not independently verified such market data. Similarly, while believed by us to be reliable, our internal surveys have not been verified by any independent sources. Accordingly, no assurance can be given that such data will prove to be accurate.

Personnel

As of December 31, 2009, we employed 1,413 people, of which 178 were located at our headquarters in Miami, Florida, and 1,235 were located in our In-country Operations throughout Latin America and the Caribbean. We do not have any collective bargaining agreements with our employees. With the exception of our employees in Mexico and certain employees in Argentina, our In-country Operations are not unionized. We believe that our relations with our employees are generally good.

We have a contract with ADP Total Source, Inc. (“ADP”) to provide certain professional employment services such as health insurance, other employee benefits and payroll services to our Miami personnel. Pursuant to this contract, our Miami personnel became employees of ADP. We lease the services of these employees from ADP, and reimburse ADP for the costs of compensation and benefits. For purposes of this Annual Report, we consider employees of ADP covered by this contract to be employees of our Company.

Website Access to Exchange Act Reports and Available Information

We file periodic reports and other information with the U.S. Securities and Exchange Commission (the “SEC”). A copy of those reports and the exhibits and schedules thereto may be inspected without charge at the public reference room maintained by the SEC located at 100 F Street, N.E., Room 1580, Washington, DC 20549. Copies of those reports and all or any portion of the registration statements and the filings may be obtained from such offices upon payment of prescribed fees. The public may obtain information on the operation of the public reference room by calling the SEC at 1-800-SEC-0330. The SEC maintains a website at www.sec.gov that contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC.

Financial and other information can also be accessed through our website at www.intcomex.com, where we make available, free of charge, copies of our Annual Report, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports filed or furnished, as soon as reasonably practicable after filing such material electronically or otherwise furnishing it to the SEC. Our website and the information contained therein or connected thereto are not incorporated into this Annual Report.

9

Table of Contents

| Item 1A. | Risk Factors. |

The recent global economic downturn and the disruptions in the credit markets could become increasingly worse, may improve in the near future, and could cause a severe disruption in our operations and adversely affect our business and results of operations.

Global financial markets have recently experienced an extreme economic downturn and severe disruption, including, among other things, volatility in securities prices, severely diminished liquidity and credit availability, and rating downgrades of certain investments. If this downturn were to return or worsen, there could be severely negative implications to our business that may exacerbate many other risks described below.

The recent global economic downturn and the associated credit crisis could return resulting in a negative impact on financial institutions and the global financial system, which would, in turn, have a negative impact on us and our creditors. Credit insurers could drop coverage on our customers and increase premiums, deductibles and co-insurance levels on our remaining or prospective coverage. Our suppliers have tightened trade credit already, and could do so further, which could negatively impact our liquidity. We may not be able to borrow additional funds under our existing credit facilities if participating banks become insolvent or their liquidity is limited or impaired. The subsequent tightening of credit in financial markets could also result in a decrease in the demand for IT products. A global recession could adversely affect our vendors’ and customers’ ability to obtain financing for operations and result in continued severe job losses and lower consumer confidence. Certain markets could experience deflation, which would negatively impact our average selling price and revenue.

If the recent downturn in the global economy returns, it may also further intensify competition, regionally and internationally, which may negatively affect our margins. The impact may be in the form of reduced prices, lower sales or reduced sales growth, loss of market share, lower gross margins, loss of vendor rebates, extended payment terms with customers, increased bad debt risks, shorter payment terms with vendors, increased capital investment and interest costs, increased inventory losses related to obsolescence and/or excess quantities, all of which could adversely affect our results of operations and financial condition. Our vendors and customers may become insolvent and file for bankruptcy, which also would negatively impact our results of operations.

Our business requires significant levels of capital to finance accounts receivable and inventory that is not financed by trade creditors. We believe that our existing sources of liquidity, including cash resources and cash provided by operating activities, supplemented as necessary with funds available under our credit arrangements, will provide sufficient resources to meet our present and future working capital and cash requirements for at least the next 12 months. However, the capital and credit markets have been experiencing unprecedented levels of volatility and disruption. Such market conditions may affect our ability to access the capital markets or the capital we require may not be available on terms acceptable to us, or at all, due to inability of our finance partners to meet their commitments to us. We are unable to predict the likely duration and severity of disruptions to financial markets and adverse economic conditions in the U.S. and other countries and the impact these events may have on our operations and the industry in general.

We operate in a highly competitive environment and, as a result, we may not be able to compete effectively or maintain or increase our sales, market share or margins, particularly if a prolonged global economic downturn persists.

The IT products distribution industry in Latin America and the Caribbean is highly competitive. The factors on which IT distributors compete include:

| • | price; |

| • | availability and quality of products and services; |

| • | terms and conditions of sale; |

| • | availability of credit and payment terms; |

| • | timeliness of delivery; |

| • | flexibility in tailoring specific solutions to customers’ needs; |

| • | effectiveness of marketing and sales programs; |

| • | availability of technical and product information; and |

| • | availability and effectiveness of warranty programs. |

10

Table of Contents

The IT products distribution industry in Latin America and the Caribbean is very fragmented. In certain markets, we compete against large multinational public companies (including Ingram Micro, Tech Data, SYNNEX and Bell Microproducts) that are significantly better capitalized than we are and potentially have greater bargaining power with vendors than we do. In addition, our main competitor in Mexico, Ingram Micro, has a significantly larger market share than we do in that country. In all of our in-country markets, we also compete against a substantial number of locally-based distributors, many of which have a lower cost structure than we do, in some cases because they operate in the gray market and the local “informal” economy. Due to intense competition in our industry, we may not be able to compete effectively against our existing competitors or new entrants to the industry, or maintain or increase our sales, market share or margins.

In addition, overcapacity in our industry and price reductions by our competitors may result in a reduction of our prices and thereby a reduction of our gross margins. We may also, as a result, lose market share, need to offer customers more credit or extended payment terms or need to reduce our prices in order to remain competitive, and any of these measures may result in an increase in our required capital, financing costs, and bad debt expense in the future.

We are dependent on a variety of IT and telecommunications systems and are subject to additional risks, as we are in the process of continuing to implement our company-wide reporting system, and any disruptions in our existing systems or delays in implementing our new system could adversely impact our ability to effectively manage our business and prepare accurate and timely financial information.

We are dependent on a variety of IT and telecommunications systems, including systems for managing our inventories, accounts receivable, accounts payable, order processing, shipping and accounting. In addition, our ability to price products appropriately and the success of our expansion plans depend to a significant degree upon our IT and telecommunications systems. We are in the process of continuing to install Sentai, our company-wide ERP, management and financial reporting system. Sentai is a scalable IT system that enables simultaneous decentralized decision-making by our employees involved in sales and purchasing while permitting control of daily operating functions by our senior management. We are also using the Sentai logistics and inventory management system in order to better adapt to higher shipping volumes. The ERP system has been implemented in our Miami Operations and 11 of our 12 In-country Operations. We completed the implementation of our core ERP system in Chile and some portions of Mexico in 2009 and expect to complete the remaining areas of Mexico in early 2010.

Our experience with this new platform is limited and each new installation requires the training of our local employees. In addition, new installations may require further modifications in order to handle the different accounting requirements in each of the countries in which we operate. Any delay in installation or temporary or long-term failure of these systems, once installed, could adversely impact our ability to effectively manage our business and prepare accurate and timely financial information. Also, our failure to adapt and upgrade our systems to keep pace with our future development and expansion could hurt our results of operations.

If the IT products market in Latin America and the Caribbean does not grow as we expect, we may not be able to maintain or increase our present growth rate and our results of operations and financial condition could be affected.

Historically, the growth of our business has been driven in large part by the growth of the IT products market in Latin America and the Caribbean. In particular, we have benefited from rapid growth in PC and Internet penetration rates. We expect that our future growth will also depend in large part on further growth in the IT market including growth in PC and Internet penetration rates and increasing demand for notebook computers, netbooks, mobile and ultra portable drives. If the IT products market does not grow as quickly and in the manner we expect for any reason, including as a result of economic, political, social or legal developments in Latin America and the Caribbean, we may not be able to maintain or grow our business as expected which could have an impact on our results of operations and financial condition.

Economic, political, social or legal developments in Latin America and the Caribbean could hurt our results of operations and financial condition.

Historically, sales to Latin America and the Caribbean have accounted for almost all of our consolidated revenues. As a result, our financial results are particularly sensitive to the performance of the economies of countries in Latin America and the Caribbean. If local, regional or worldwide developments adversely affect the economies of any of the countries in which we do business, our results of operations and financial condition could be hurt. Our results are also impacted by political and social developments in the countries in which we conduct business and changes in the laws and regulations affecting our business in those regions. Changes in local laws and regulations could, among other things, make it more difficult for us to sell our products in the affected countries, restrict or prevent our receipt of cash from our customers, result in longer payment cycles, impair our collection of accounts receivable and make it more difficult for us to repatriate capital and dividends from our foreign subsidiaries to the ultimate U.S. parent company.

11

Table of Contents

The economic, political, social and legal risks we are subject to in Latin America and the Caribbean include but are not limited to:

| • | deteriorating economic, political or social conditions; |

| • | additional tariffs, import and export controls or other trade barriers that restrict our ability to sell products into countries in Latin America and the Caribbean; |

| • | changes in local tax regimes, including the imposition of significantly increased withholding or other taxes or an increase in value added tax (“VAT”) or sales tax on products we sell; |

| • | changes in laws and other regulatory requirements governing foreign capital transfers and the repatriation of capital and dividends; |

| • | increases in costs for complying with a variety of different local laws, trade customs and practices; |

| • | delays in shipping and delivering products to us or customers across borders for any reason, including more complex and time-consuming customs procedures; and |

| • | fluctuations of local currencies. |

Any adverse economic, political, social or legal developments in the countries in which we do business could harm our results of operations and financial condition.

Fluctuations in foreign currency exchange rates could reduce our gross profit and gross margins and increase our operating expenses in U.S. dollar terms.

We periodically engage in foreign currency forward contracts when available and when doing so is not cost prohibitive. In periods when we do not, foreign currency fluctuations may adversely affect our results of operations, including our gross margins and operating margins.

A significant portion of our revenues from our In-country Operations is invoiced in currencies other than the U.S. dollar, and a significant amount of our in-country operating expenses are denominated in currencies other than U.S. dollars. In markets where we invoice in local currency, including Argentina, Chile, Colombia, Costa Rica, Guatemala, Jamaica, Mexico, Peru and Uruguay, the appreciation of a local currency could have an impact on our gross profit and gross margins in U.S. dollar terms. In markets where our books and records are prepared in currencies other than the U.S. dollar, the appreciation of the local currency will increase our operating expenses and decrease our operating margins in U.S. dollar terms.

Large and sustained devaluations of local currencies, like those that occurred in Brazil in 2000 and Argentina in 2001, can make many of our products more expensive in local currencies. This could result in our customers having difficulty paying those invoices and, in turn, result in decreases in revenue. Moreover, such devaluations may adversely impact demand for our products because our customers may be unable to afford them. For example, during 2009, our foreign exchange gain amounted to $3.1 million primarily due to the appreciation of the Chilean, Colombian and Uruguayan Pesos. The Chilean Peso strengthened by 19.9%, to 519 pesos per U.S. dollar as of December 31, 2009, from 648 pesos per U.S. dollar as of December 31, 2008. The Colombian Peso strengthened by 8.3%, to 2,065 pesos per U.S. dollar as of December 31, 2009, from 2,252 pesos per U.S. dollar as of December 31, 2008. The Uruguayan Peso also strengthened by 19.8%, to 20 pesos per U.S. dollar as of December 31, 2009, from 25 pesos per U.S. dollar as of December 31, 2008. For a more detailed discussion of the effect of foreign currency fluctuations on our results of operations, see Part II—Item 7A. Quantitative and Qualitative Disclosures About Market Risk—Foreign exchange risk, of this Annual Report.

We are exposed to market risk and credit exposure and loss as we engage in foreign currency exchange forward contracts to hedge foreign currency denominated payables for inventory purchases, in a currency other than the currency in which the products are sold.

We are exposed to fluctuations in foreign exchange rates and reduce our exposure to the fluctuations by sometimes using derivative financial instruments, particularly foreign currency forward contracts. We use these contracts to hedge foreign currency denominated payables for inventory purchases in the normal course of business, in a currency other than the currency in which the products are sold. Derivative financial instruments potentially subject our Company to risk. Volatile foreign currency exchange rates increase our risk related to products purchased in a currency other than the currency in which the products are sold in the normal course of business. We did not have any foreign currency forward contracts outstanding as of December 31, 2009. Our foreign currency forward contract with a notional amount of $11.8 million as of December 31, 2008, had a fair value of ($31,000).

12

Table of Contents

We are exposed to market risk related to volatility in foreign currency exchange rates, including devaluation and revaluation of local currencies. The market risk related to the forward contracts is offset by changes in the valuation of the underlying foreign currencies being hedged. We are also exposed to credit loss in the event of nonperformance by our counterparties to foreign exchange forward contracts and we may not be able to adequately mitigate all foreign currency related risks. We manage our exposure to fluctuations in the value of currencies and interest rates using foreign currency forward contracts with creditworthy financial institution counterparties. We monitor our exposures and the creditworthiness of our financial institution counterparties. Credit exposure for derivative financial instruments is limited to the amounts, if any, by which the counterparties’ obligations under the contracts exceed the obligations of our Company to the counterparties. We manage the potential risk of credit loss through careful evaluation of counterparty credit standing, selection of counterparties from a limited group of financial institutions and other contract provisions.

We maintain a policy to protect against fluctuation in currency exchange rates, which may result in a loss. We do not use derivative financial instruments for trading or speculative purposes. The realization of any or all of these risks could have a significant adverse effect on our financial results and statement of operations.

Our management and financial reporting systems, internal and disclosure controls and finance and accounting personnel may not be sufficient to meet our management and reporting needs.

We rely on a variety of management and financial reporting systems and internal and disclosure controls to provide management with accurate and timely information about our business and operations. This information is important because it enables management to capitalize on business opportunities and identify unfavorable developments and risks at an early stage. We also rely on these management and financial reporting systems and internal and disclosure controls to enable us to prepare accurate and timely financial information for our investors.

The challenge of establishing and maintaining sufficient systems and controls and hiring, training and retaining sufficient accounting and finance personnel has intensified as our business has grown rapidly in recent years and expanded into new geographic markets. As a result, we have identified the need to expand our finance and accounting staff and enhance internal controls at both the corporate and in-country levels and enhance the training of in-country management personnel regarding internal controls and management reporting to meet our current needs. This process is ongoing. For example, although we expect Sentai, our company-wide ERP, management and financial reporting system, to enhance the control of daily operating functions by our senior management, Sentai has yet to be fully implemented in Mexico, the last operation not entirely on Sentai. The ERP system has been implemented in our Miami Operations and 11 of our 12 In-country Operations. We completed the implementation of our core ERP system in Chile and some portions of Mexico in 2009 and expect to complete the remaining areas of Mexico in early 2010.

As of the end of 2009, we determined the need to make certain enhancements to access controls within our IT systems to limit unauthorized access and user functionality in our financial reporting systems and ensure proper segregation of duties. We intend to develop additional controls that ensure authorized personnel have access only to the areas of our financial reporting systems necessary to effectively perform their particular job functions.

In 2008, we hired a new director of internal audit, vice president of human resources, a director of finance for our subsidiary in El Salvador and controllers for each of our subsidiaries in Jamaica and Mexico. In 2009, we hired a new director of finance for each of our subsidiaries in Guatemala, Chile and Colombia. In addition, we are continuously seeking to add personnel to our finance and accounting staff, institute new controls and enhance existing controls at our consolidated and subsidiary operating levels.

Although we believe our current management and financial reporting systems, internal and disclosure controls and finance and accounting personnel are sufficient to enable us to effectively manage our business, identify unfavorable developments and risks at an early stage and produce financial information in an accurate and timely manner, we cannot be sure this will be the case. For example, management identified a material weakness in one of our foreign operations control environment during 2008, which included the following: (i) a failure to perform proper management oversight of the local operations and monitor and test controls to detect the override of established controls and policies; (ii) failure to institute all elements of an effective program to detect and prevent personnel (considered to be employees performing functions under a services agreement in the ordinary course of business for our Company under the laws of the jurisdiction in which the foreign entity operates) from improperly claiming tax withholding exemptions as non-employees; and (iii) failure to establish and maintain an effective control environment surrounding the payroll process and the disbursement process, including the failure to verify the existence of complete and accurate procedures to support a three-way matching process comparing the original purchase order, invoice and receipt records of the purchased products to support the approval and payment for services rendered or products purchased. This material weakness resulted in increased payroll tax and VAT in the amount estimated to be approximately $0.4 million in the second quarter of 2008.

Although management undertook corrective actions to remediate the failed controls surrounding the foreign operating entity’s purchase and receipt of products, such actions may prove to be ineffective or inadequate and may expose our Company to risk of misstatements in our financial statements. In such circumstances, investors and other users of our financial statement may lose confidence in the reliability of our financial information, and we could fail to comply with certain covenants in our debt agreements.

13

Table of Contents

No matter how well designed and operated, a control system can provide only reasonable, not absolute, assurance that its objectives are met. Its inherent limitations include the realities that judgments in decision-making can be faulty and failures can occur due to simple mistakes. Moreover, controls can be circumvented by the acts of an individual, collusion of two or a group of people or by management’s decision to override the existing controls.

We believe that we need to continue to expand our finance and accounting staff, enhance internal controls at both the corporate and in-country levels and enhance the training of in-country management personnel regarding internal controls and management reporting to meet our future needs, as a result of our anticipated or future growth. We cannot be sure that we will be able to take all necessary actions in a timely manner to keep pace with our anticipated growth.

Although we believe our controls were effective as of year end, if we fail to maintain sufficient management and financial reporting systems and internal and disclosure controls, hire, retain and train sufficient accounting and finance personnel, and enhance the training of in-country management personnel regarding internal controls and management reporting, our ability to prepare accurate and timely financial information could be impaired, hinder our growth and have a material adverse effect on our current or future business, results of operations and financial condition.

We could experience difficulties in staffing and managing our foreign operations, which could result in reduced revenues and difficulties in realizing our growth strategy.

We have many sales and distribution centers in multiple countries, which require us to attract managers of our business in each of those locations. In establishing and developing many of our in-country sales and distribution operations, we have relied in large part on the local market knowledge and entrepreneurial skills of a limited number of local managers in those markets. We have no employment agreements with any of our in-country managers. The loss of the services of any of these managers could adversely impact our results of operations in the market in which the manager is located. Further, it may prove difficult to find and attract new talent, including accounting and finance personnel, in our existing markets or any new markets we enter in Latin America and the Caribbean who possess the expertise required to successfully manage and operate our in-country sales and distribution operations. In 2009, we hired a new general manager and a director of finance for our operations in Colombia, each of whom we believe has the appropriate knowledge and management skills to oversee our operations. If we fail to recruit highly qualified candidates, we may experience greater difficulty realizing our growth strategy, which could hurt our results of operations.

If we lose the services of our key executive officers, we may not succeed in implementing our business strategy.

We are currently managed by certain key executive officers, including both of our founders, Anthony Shalom and Michael Shalom. These individuals have extensive experience and knowledge of our industry and the many local markets in which we operate. They also have been integral in establishing and expanding some of our most significant customer relationships and building our unique distribution platform. The loss of the services of these key executive officers could adversely affect our ability to implement our business strategy, and new members of management may not be able to successfully replace them. With the exception of an employment agreement with our Chief Financial Officer, we have no employment agreements with any of our key executive officers.

We are exposed to increased costs associated with complying with the Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act”) and other corporate governance and disclosure standards. Compliance efforts could divert management time from revenue-generating activities to compliance activities. Failures to comply could cause reputational harm and additional costs to remedy shortcomings.

The Sarbanes-Oxley Act and the rules promulgated by the SEC require us to adopt various corporate governance practices and implement various internal controls. Our efforts to comply with evolving laws, regulations and standards applicable to public companies have resulted in, and are likely to continue to result in, increased expenses and a diversion of management time from revenue-generating activities to compliance activities.

In particular, Section 404 of the Sarbanes-Oxley Act (“Section 404”) requires our management to annually review and evaluate our internal controls over financial reporting and attest to the effectiveness of these controls, beginning with our fiscal year ended December 31, 2007. The Sarbanes-Oxley Act requires our independent registered public accounting firm to attest to the effectiveness of internal control over financial reporting, beginning with our fiscal year ended December 31, 2010. To date, our ongoing efforts to comply with Section 404 have required the commitment of significant financial and managerial resources. In the event that our Chief Executive Officer, Chief Financial Officer or independent registered public accounting firm determines that our controls over financial reporting are not effective as required by Section 404 at any time in the future, investor perceptions of us and our reputation may be adversely affected and we may incur significant additional costs to remedy shortcomings in our internal controls.

14

Table of Contents

We may be required to recognize further impairments of our goodwill, identifiable intangible assets or other long-lived assets or to establish further valuation allowances against our deferred income tax assets, which could adversely affect our results of operations or financial condition.

In the fourth quarter of 2008, consistent with the severe decline in the global capital markets, we experienced a similar decline in the market value of our goodwill and other intangible assets. As a result, our fair value of goodwill was significantly lower than book value. We perform our impairment test of our goodwill and other intangible assets on an annual basis. As a result of this evaluation, we recognized a charge of $18.8 million against the carrying value of our goodwill for the year ended December 31, 2008. This non-cash charge materially impacted our equity and results of operations in 2008, but did not impact our ongoing business operations, liquidity or cash flow. We did not recognize a charge against the carrying value of our goodwill, identifiable intangible assets or other long-lived assets as of December 31, 2009.

As part of our 2009 impairment analysis of goodwill, we noted that our operations in Centel reflected a fair value that exceeded its carrying value by approximately 3.4%. The fair value was determined using management’s projections giving the recent economic contraction in Mexico’s gross domestic product, or GDP, and our independent valuation experts’ estimate of fair value. As of December 31, 2009, we have $2.9 million of goodwill attributable to our operations in Mexico, which represents approximately 11.2% of Centel’s carrying value and less than 1.0% of our total assets. An extended period of economic contraction could result in a further impairment to the carrying value of the goodwill attributable to our operations in Mexico.

Deferred income tax represents the tax effect of the differences between the book and tax bases of assets and liabilities. Deferred tax assets, which also include net operating loss carryforwards for entities that have generated or continue to generate operating losses, are assessed periodically by management to determine if their future benefit will be fully realized. Factors in management’s determination include the performance of the business and the feasibility of ongoing tax planning strategies. If available information indicates that it is more likely than not that the deferred income tax asset will not be realized then a valuation allowance must be established with a corresponding charge to net (loss) income. Such charges could have a material adverse effect on our results of operations or financial condition. As a result of our evaluation, we established a valuation allowance against the carrying value of our long-term deferred tax assets of $6.4 million and $4.8 million, respectively, as of December 31, 2009 and 2008.

Our future results of operations may be impacted by a prolonged weakness in the global economic environment that may result in a further impairment of any existing goodwill or goodwill recorded in the future and/or other long-lived assets or further valuation allowances on our deferred tax assets, which could adversely affect our results of operations or financial condition.

The indenture governing our 13 1/4% Second Priority Senior Secured Notes due December 15, 2014 (the “13 1/4% Senior Notes”) and the credit agreement governing Software Brokers of America, Inc. (“SBA”)’s Senior Secured Revolving Credit Facility imposes significant operating and financial restrictions on our Company and our subsidiaries, which may prevent us from capitalizing on business opportunities.

The indenture governing our 13 1/4% Senior Notes imposes significant operating and financial restrictions on us. These restrictive covenants limit our ability, among other things to:

| • | incur additional indebtedness or enter into sale and leaseback obligations; |

| • | pay certain dividends or make certain distributions on our capital stock or repurchase our capital stock; |

| • | make certain investments or other restricted payments; |

| • | place restrictions on the ability of subsidiaries to pay dividends or make other payments to us; |

| • | engage in transactions with shareholders or affiliates; |

| • | sell certain assets or merge with or into other companies; |

| • | guarantee indebtedness; and |

| • | create liens. |

The Senior Secured Revolving Credit Facility limits SBA’s ability, among other things, to:

| • | incur additional indebtedness; |

| • | make certain capital expenditures; |

15

Table of Contents

| • | guarantee certain obligations, other than SBA’s guarantee of our 13 1/4% Senior Notes; |