Attached files

| file | filename |

|---|---|

| EX-23.2 - EXHIBIT 23.2 - INDUS REALTY TRUST, INC. | a2196315zex-23_2.htm |

| EX-21 - EXHIBIT 21 - INDUS REALTY TRUST, INC. | a2196315zex-21.htm |

| EX-23.1 - EXHIBIT 23.1 - INDUS REALTY TRUST, INC. | a2196315zex-23_1.htm |

| EX-31.2 - EXHIBIT 31.2 - INDUS REALTY TRUST, INC. | a2196315zex-31_2.htm |

| EX-32.1 - EXHIBIT 32.1 - INDUS REALTY TRUST, INC. | a2196315zex-32_1.htm |

| EX-32.2 - EXHIBIT 32.2 - INDUS REALTY TRUST, INC. | a2196315zex-32_2.htm |

| EX-31.1 - EXHIBIT 31.1 - INDUS REALTY TRUST, INC. | a2196315zex-31_1.htm |

QuickLinks -- Click here to rapidly navigate through this document

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

ý |

ANNUAL REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the fiscal year ended November 28, 2009 |

||

OR |

||

o |

TRANSITION REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

Commission file number 1-12879

GRIFFIN LAND & NURSERIES, INC.

(Exact name of registrant as specified in its charter)

| Delaware (State or Other Jurisdiction of Incorporation or Organization) |

06-0868496 (I.R.S. Employer Identification No.) |

|

One Rockefeller Plaza New York, New York (Address of principal executive offices) |

10020 (Zip Code) |

|

(212) 218-7910 (Registrant's telephone number, including area code) |

||

SECURITIES REGISTERED PURSUANT TO SECTION 12(B) OF THE ACT:

| Title of Each Class | Name of Each Exchange on Which Registered | |

|---|---|---|

| Common Stock $0.01 par value | The NASDAQ Stock Market LLC |

SECURITIES REGISTERED PURSUANT TO SECTION 12(G) OF THE ACT: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined by Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer," and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer ý | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No ý

The aggregate market value of the Common Stock held by non-affiliates of the registrant, was approximately $69,612,000 based on the closing sales price on The NASDAQ Stock Market LLC on May 29, 2009, the last business day of the registrant's most recently completed second quarter. Shares of Common Stock held by each executive officer, director and persons or entities known to the registrant to be affiliates of the foregoing have been excluded in that such persons may be deemed to be affiliates. This assumption regarding affiliate status is not necessarily a conclusive determination for other purposes.

As of February 1, 2010, 5,102,436 shares of common stock were outstanding.

Griffin Land & Nurseries, Inc. ("Griffin") and its subsidiaries comprise principally a real estate business and a landscape nursery business. Griffin is engaged in two lines of business: (1) the real estate business comprised of (a) the ownership, construction, leasing and management of commercial and industrial properties and (b) the development of residential subdivisions on real estate owned by Griffin in Connecticut and Massachusetts; and (2) the landscape nursery business comprised of the growing of containerized plants for sale principally to independent retail garden centers, rewholesalers, whose main customers are landscape contractors, and mass merchandisers.

Griffin also owns an approximate 4% interest in Centaur Media plc ("Centaur Media"), a publicly held magazine and information services publisher based in the United Kingdom, and an approximate 14% interest in Shemin Nurseries Holding Corp. ("SNHC"), a private company that operates a landscape nursery distribution business through its subsidiary, Shemin Nurseries, Inc. ("Shemin Nurseries").

Griffin was incorporated as Culbro Realty and Development Corporation in 1970 and was a wholly owned subsidiary of Culbro Corporation ("Culbro") through July 3, 1997. On July 3, 1997, Culbro distributed to its shareholders the common stock of Griffin in a tax-free distribution (the "Distribution"). In early 1997, prior to the Distribution, the Company's name was changed to Griffin Land & Nurseries, Inc.

Griffin does not maintain a corporate website. Griffin's annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and the proxy statement for Griffin's Annual Meeting of Stockholders can be accessed through the SEC website at www.sec.gov.

Real Estate Business

Griffin's real estate division, Griffin Land, is directly engaged in the real estate development business on parts of its land in Connecticut and Massachusetts. Griffin Land's buildings and land holdings are located primarily in the Hartford, Connecticut area particularly the north submarket of Hartford. Griffin Land develops portions of its properties for industrial, commercial and residential use and expects to continue to sell some of its land holdings either before or after obtaining development approvals. Griffin Land also will seek to acquire and develop properties not presently owned, including land and buildings outside the Hartford area. Generally any properties acquired in areas in which Griffin Land does not presently own property are expected to be within a few hours driving time from Hartford, Connecticut. Recently, Griffin Land purchased an approximately 120,000 square foot warehouse in Pennsylvania which is fully leased and contracted to purchase undeveloped land, also in Pennsylvania. The headquarters for Griffin Land is in Bloomfield, Connecticut.

As of November 28, 2009, Griffin Land's real estate portfolio consisted of twenty-nine buildings totaling 2.4 million square feet, including industrial, office and flex facilities and approximately 3,000 acres of undeveloped land. Activity for the leasing of industrial and office space in the Hartford market was slow in 2009, as the weak economy has depressed the rental markets over the past eighteen to twenty-four months. The north submarket of Hartford continues to have the highest vacancy percentage and the lowest rental rates for office space of all of Hartford's submarkets. The number of inquiries received by Griffin Land from prospective tenants declined in 2009 from the prior year. In the past four years, several warehouse and light industrial buildings, competitive with Griffin Land's industrial buildings, have been built in the greater Hartford area. These facilities compete with Griffin Land's properties in the leasing of new industrial space in the north submarket of Hartford. Additional capacity in the industrial market could adversely affect Griffin Land's operating results from its leasing business by potentially resulting in longer times to lease vacant space, eroding lease rates in Griffin

1

Land's properties or hindering renewals by existing tenants. In the last year, however, there was practically no new development of industrial space in the north submarket of Hartford other than Griffin Land's development of a pre-leased warehouse for Tire Rack, Inc. ("Tire Rack"). There can be no assurance as to the direction of the real estate market in this region in the near future.

The decline in the residential real estate market and tightening of credit availability during the past two years has adversely affected Griffin Land's real estate development activities. In 2008, Griffin Land's agreement with the local home builder that had previously purchased the first twenty-five lots of Griffin Land's fifty lot residential subdivision known as Stratton Farms, in Suffield, Connecticut, expired because the home-builder did not exercise its option to purchase the next phase of lots (see below). The softening of the residential real estate market could result in lower selling prices for Griffin Land's undeveloped land intended for residential use or delay the sale of such land. The continued tightening of the credit markets could also adversely impact future financing of Griffin Land's office and industrial facilities and adversely impact the financing of potential acquisitions of real estate assets.

In fiscal 2009, Griffin Land leased approximately 298,000 square feet, comprised of approximately 257,000 square feet of warehouse/light industrial space and approximately 40,000 square feet of single story office/flex space. The leasing of warehouse/light industrial space reflected the space leased in a new approximately 304,000 square foot build-to-suit building in New England Tradeport ("Tradeport"), Griffin Land's industrial park in Windsor and East Granby, Connecticut. The lease of approximately 40,000 square feet in a single story office/flex building reflects leasing to a single tenant an entire building in Griffin Center South that had been vacant. In fiscal 2009, leases aggregating approximately 89,000 square feet expired and were not renewed.

In fiscal 2008, Griffin Land leased approximately 388,000 square feet, almost all of which was warehouse/light industrial space. Of the newly leased space in fiscal 2008, approximately 308,000 square feet was to an affiliate of Raymour & Flanigan, a regional furniture retailer, which leased Griffin Land's entire warehouse facility in Manchester, Connecticut. In addition, Griffin Land leased approximately 58,000 square feet in an industrial building built in 2008. The tenant in that building previously occupied approximately 22,000 square feet in one of Griffin Land's other industrial buildings. Griffin Land also entered into several smaller leases in fiscal 2008 for warehouse, flex and office space. Two small leases for office space expired in fiscal 2008 and were not renewed.

There were no property sales in fiscal 2009. Property sales revenue in fiscal 2008 included the sale of approximately 75 acres of undeveloped land in Simsbury, Connecticut, which was sold to the Town of Simsbury for open space as part of the settlement of litigation related to Meadowood, Griffin Land's proposed residential development (see Item 3 Legal Proceedings). Griffin received $0.5 million in cash at the closing, and will receive an additional $2.2 million in four installments through 2012 ($0.5 million of which was received in fiscal 2009). Also in fiscal 2008, Griffin Land recognized the remaining amounts of revenue and profit that had been deferred from the land sale to Walgreen Co. ("Walgreen") that closed in fiscal 2006. Although all of the cash proceeds from that sale were received in fiscal 2006, because that transaction was accounted for using the percentage of completion method, a portion of the revenue and profit from that sale was initially deferred and recognized in subsequent periods as the required road improvements were made. As of November 29, 2008, all of the required road improvements were completed.

In fiscal 2007, Griffin Land completed several property sales, generating cash proceeds of $13.3 million. Included in those transactions were the sale of approximately 73 acres of undeveloped land in Griffin Center in Windsor, Connecticut, the sale of approximately 103 acres of undeveloped land in South Windsor, Connecticut, the sale of the second phase of residential lots of Stratton Farms, and the sale of a small parcel of undeveloped land near the central business district of Tampa, Florida. Also in fiscal 2007, Griffin Land purchased approximately 24 acres of land that included an approximate 31,000 square foot warehouse. The land parcel acquired abuts a significant parcel of

2

undeveloped land held by Griffin Land. The terms of that acquisition included a ten-year lease of the warehouse to the seller. That acquisition was made using a portion of the proceeds from a land sale earlier in that year as part of a Section 1031 exchange for income tax purposes, which resulted in the deferral of a portion of the income taxes related to the prior land sale.

Griffin Land's development of its land is affected by regulatory and other constraints. Subdivision and other residential development issues may also be affected by the potential adoption of initiatives meant to limit or concentrate residential growth. Commercial and industrial development activities for Griffin Land's undeveloped land may also be affected by traffic considerations, potential environmental issues and other restrictions to development imposed by governmental agencies.

Commercial and Industrial Developments

New England Tradeport

The major portion of Griffin Land's current commercial and industrial development effort is focused on Tradeport, the 600 acre industrial park near Bradley International Airport and Interstate 91, located in Windsor and East Granby, Connecticut. Within Tradeport, Griffin Land built and owns approximately 1,465,000 square feet of warehouse and light manufacturing space in thirteen buildings, of which approximately 75% was leased as of November 28, 2009. Tradeport also contains a large distribution facility recently built by Walgreen on land purchased from Griffin Land in fiscal 2006 (see below) and a bottling and distribution plant built by the Pepsi Bottling Group ("Pepsi") on land sold to Pepsi by Griffin Land in the early 1990s.

In fiscal 2009, Griffin Land completed a build-to-suit warehouse and light manufacturing building in Tradeport of approximately 304,000 square feet. Construction of this new facility commenced upon Griffin Land entering into a ten-year lease with Tire Rack, a private company that will use this facility as its northeast distribution center. Tire Rack currently pays rent on 257,000 square feet of the building but pays for the operating expenses of the entire building. No later than the beginning of the sixth year of the lease, August 2014, Tire Rack is required to pay rent on the entire building. The lease also contains provisions for a potential expansion that would increase the size of the building up to approximately 450,000 square feet.

In fiscal 2008, Griffin Land built an approximate 100,000 square foot warehouse and light manufacturing building in Tradeport. Approximately 58,000 square feet of this building was leased at the time the building was placed in service to a tenant that consolidated several of its locations into that space, including approximately 22,000 square feet of space previously leased in one of Griffin Land's other Tradeport buildings.

As of November 28, 2009, $66.2 million was invested (net book value) in buildings owned by Griffin Land that are located in Tradeport and $4.0 million was invested (net book value) by Griffin Land in the undeveloped land there.

As of November 28, 2009, ten of Griffin Land's Tradeport buildings were mortgaged for an aggregate of approximately $47.8 million. Two Tradeport buildings built in fiscal 2007 and an older Tradeport building, aggregating approximately 373,000 square feet, are currently not mortgaged. A summary of Griffin Land's square footage owned and leased in Tradeport at the end of each of the

3

past three fiscal years and leases in Tradeport scheduled to expire during each of the next three fiscal years are as follows:

| |

Square Footage Owned |

Square Footage Leased |

Percentage Leased |

|||||||

|---|---|---|---|---|---|---|---|---|---|---|

November 2007 |

1,061,000 | 848,000 | 80 | % | ||||||

November 2008 |

1,161,000 | 893,000 | 77 | % | ||||||

November 2009* |

1,465,000 | 1,104,000 | 75 | % | ||||||

| |

2010 | 2011 | 2012 | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

Square footage of leases expiring |

187,000 | 189,000 | 59,000 | |||||||

Percentage of currently leased space |

17% | 17% | 5% | |||||||

- *

- The square footage leased as of November 2009 does not include 47,000 square feet of space on which Tire Rack pays operating expenses and is required to occupy no later than August 2014, the beginning of the sixth year of its lease.

In fiscal 2006, Griffin Land sold approximately 130 acres of undeveloped land in Tradeport to Walgreen for their construction of a distribution center. The sale generated cash proceeds of $13.0 million, before transaction expenses. As provided under the terms of the sale contract and as required under a revised State Traffic Commission certificate (the "STC Certificate") covering the area in Tradeport located in Windsor, certain improvements to existing roads were required. The cost of these improvements was the responsibility of Griffin Land, however, a portion of the costs were borne by the town of Windsor and Walgreen. Accordingly, Griffin Land recognized revenue of $11.0 million and profit of $8.6 million through fiscal 2007. This sale was accounted for using the percentage of completion method because of Griffin Land's responsibility to make certain road improvements. In fiscal 2008, the required road improvements were completed, and Griffin Land recognized the balance of the previously deferred revenue of approximately $2.0 million and profit of approximately $1.5 million.

In connection with the fiscal 2006 land sale to Walgreen, the State Traffic Commission of Connecticut (the "STC") approved a revised STC Certificate that allowed Griffin Land to construct an additional approximate 1.1 million square feet of light manufacturing and warehouse space on certain parcels in Tradeport. In fiscal 2009, the STC Certificate for the Windsor land in Tradeport was amended to permit an additional 350,000 square feet to be built (resulting in a total of 1.45 million approved square feet) in connection with granting approval for the approximately 304,000 square foot build-to-suit building that Griffin Land built in fiscal 2009 for Tire Rack's occupancy. As a result of receiving the amended STC Certificate, Griffin Land received approval to build this new building in addition to all of the square footage allowed under the previous certificate. Through the end of fiscal 2009, Griffin Land has built approximately 679,000 square feet of the 1.45 million approved square feet. The balance of the space that has been approved is expected to be built over time as demand warrants. Upon construction of all of the additional square footage permitted under the STC Certificate, there will remain for future development an additional approximately 152 acres of undeveloped Tradeport land in Windsor and a 36 acre undeveloped parcel of contiguous land in East Granby. There are no STC or other approvals (other than zoning in the case of Windsor) for the development of this additional land currently in place, and Griffin Land believes that infrastructure improvements, which may be significant, may be required to obtain approvals to develop this land.

Griffin Land intends to continue to direct its primary efforts in the industrial properties portion of its real estate business with construction and leasing of its warehouse and light manufacturing facilities at Tradeport. Griffin Land currently owns some other nearby land not part of Tradeport that may be appropriate for such development over a longer term and that will require substantial additional preparation and zoning approvals.

4

Griffin Center and Griffin Center South

Griffin's other substantial commercial development is the combination of its buildings in Griffin Center in Windsor and Bloomfield, Connecticut and Griffin Center South in Bloomfield. Together these master planned developments comprise approximately 600 acres and as of November 28, 2009, approximately 63% has been developed with approximately 2,165,000 square feet of office and industrial space. Griffin Land owns approximately 617,000 of the 2,165,000 square feet of developed space. In fiscal 2007, Griffin Land sold approximately 73 acres of undeveloped land in Griffin Center to The Hartford Insurance Company ("The Hartford"), which built an approximately 460,000 square foot office building.

Griffin Center currently includes eleven office buildings (including the building built by The Hartford), a light manufacturing building and a small restaurant, five of which are owned by Griffin Land. Griffin Land currently owns two multi-story office buildings that have an aggregate of approximately 161,000 square feet, a single story office building of approximately 48,000 square feet, a 165,000 square foot light manufacturing building used principally as office, data center and call center space and the small restaurant building. As of November 28, 2009, $19.2 million was invested (net book value) in Griffin Land's buildings in Griffin Center and $1.2 million was invested by Griffin Land in the undeveloped land there. Griffin Land's two multi-story office buildings and its light manufacturing building in Griffin Center are separately mortgaged for an aggregate of approximately $12.2 million, and Griffin Land's single story office building is included as collateral under Griffin's $10 million Revolving Line of Credit.

There were no new leases in Griffin Land's Griffin Center properties in fiscal 2009, and leases aggregating approximately 42,000 square feet expired and were not renewed, including a lease for approximately 37,000 square feet to The Hartford, which relocated into its new facility (see above). As of November 28, 2009, approximately 274,000 square feet of Griffin Land's buildings was leased, comprising approximately 72% of Griffin Land's total space in Griffin Center. A summary of Griffin Land's square footage owned and leased in Griffin Center at the end of each of the past three fiscal years and leases in Griffin Center scheduled to expire during each of the next three fiscal years are as follows:

| |

Square Footage Owned |

Square Footage Leased |

Percentage Leased |

|||||||

|---|---|---|---|---|---|---|---|---|---|---|

November 2007 |

382,000 | 318,000 | 83 | % | ||||||

November 2008 |

382,000 | 316,000 | 83 | % | ||||||

November 2009 |

382,000 | 274,000 | 72 | % | ||||||

| |

2010 | 2011 | 2012 | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

Square footage of leases expiring |

3,000 | — | 42,000 | |||||||

Percentage of currently leased space |

1% | — | 15% | |||||||

Griffin Center South is a 130 acre tract with sixteen buildings of single story office, flex and storage space. Griffin Land currently owns nine buildings in Griffin Center South with an aggregate of approximately 235,000 square feet, of which approximately 217,000 square feet is single story office and flex space and 18,000 square feet is storage space. The only new lease completed in fiscal 2009 was a ten-year lease of an entire approximate 40,000 square foot single story office/flex building that had been vacant. As of November 28, 2009, $8.9 million was invested (net book value) in Griffin Land's buildings in Griffin Center South and $0.4 million was invested by Griffin Land in the undeveloped land there. As of November 28, 2009, eight of Griffin Land's nine properties in Griffin Center South, aggregating approximately 195,000 square feet, are included as collateral under Griffin's $10 million Revolving Line of Credit. Undeveloped land remaining in Griffin Center South is sufficient to build at least two additional buildings aggregating approximately 175,000 square feet.

5

As of November 28, 2009, approximately 177,000 square feet of space in the Griffin Center South buildings owned by Griffin Land was leased, comprising 75% of Griffin Land's total space in Griffin Center South. A summary of Griffin Land's square footage owned and leased in Griffin Center South at the end of each of the past three fiscal years and leases in Griffin Center South scheduled to expire during each of the next three fiscal years are as follows:

| |

Square Footage Owned |

Square Footage Leased |

Percentage Leased |

|||||||

|---|---|---|---|---|---|---|---|---|---|---|

November 2007 |

235,000 | 125,000 | 53 | % | ||||||

November 2008 |

235,000 | 136,000 | 58 | % | ||||||

November 2009 |

235,000 | 177,000 | 75 | % | ||||||

| |

2010 | 2011 | 2012 | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

Square footage of leases expiring |

13,000 | 41,000 | 27,000 | |||||||

Percentage of currently leased space |

8% | 23% | 15% | |||||||

Subsequent to the end of fiscal 2009, Griffin Land entered into a lease for approximately 19,000 square feet in one of its buildings in Griffin Center South.

Other Industrial Properties

As of November 28, 2009, Griffin Land's two industrial buildings aggregating approximately 338,000 square feet that are not located within one of its office and industrial parks were fully leased, and $15.0 million was invested (net book value) in these two buildings as of that date. There are no mortgages on these properties. The larger of the two buildings, a 308,000 square foot warehouse in Manchester, Connecticut, has been leased since September 2008 to an affiliate of Raymour & Flanigan. Previously, that building had been vacant since it was acquired in fiscal 2006 as part of a Section 1031 exchange whereby income taxes related to the gain on the June 2006 land sale to Walgreen and a smaller 2006 land sale were deferred. In addition to other customary terms, the lease agreement with Raymour & Flanigan includes an option, with certain conditions, exercisable by Griffin Land, for Griffin Land to sell the property to the lessee, and another option, exercisable by the lessee, to purchase the property from Griffin Land, during different periods during the lease term at a price that has been agreed upon.

In fiscal 2007, Griffin Land completed the sale of approximately 103 acres of undeveloped land in South Windsor, Connecticut to a food distributor for construction of a distribution facility. This transaction generated cash proceeds of approximately $2.5 million to Griffin Land for its share of the sales price. Also in fiscal 2007, Griffin Land acquired approximately 24 acres of land and an approximate 31,000 square foot warehouse facility in Bloomfield, Connecticut from General Cigar Company, Inc. ("General Cigar"). The purchase price of $2.7 million was paid in cash at closing. The purchase of this warehouse facility was also part of a Section 1031 exchange whereby a portion of the income taxes related to the gain on the land sale to The Hartford were deferred. As part of this transaction, Griffin Land entered into a ten-year lease for the entire building with General Cigar. The land acquired abuts approximately 244 acres of undeveloped land held by Griffin Land. Griffin Land is currently in the process of obtaining approvals for roadwork that would connect the acquired land to its existing parcel for future development purposes.

Griffin Land may seek to acquire additional developed and/or undeveloped land parcels both in Connecticut and elsewhere to expand the industrial/warehouse portion of its real estate business. Over the past two years, Griffin Land has examined several sites in New York and Pennsylvania for potential acquisition, and on January 8, 2010, Griffin Land closed on the acquisition of an approximate 120,000 square foot industrial building in Breinigsville, Pennsylvania. The building was purchased through an

6

auction held by the Trustee of the bankruptcy estate of the sole owner of the building. The purchase price was $6.4 million plus acquisition expenses. The building is located in a major industrial area of Pennsylvania's Lehigh Valley and is under a full building lease to Olympus Corporation of the Americas ("Olympus"). Subsequent to the purchase of this building, Griffin Land completed a lease amendment with Olympus that extends the lease term through 2025. On January 29, 2010, Griffin closed on a $4.3 million nonrecourse mortgage on this building from New Alliance Bank. This is Griffin Land's first real estate acquisition outside of the Hartford, Connecticut, market.

Griffin Land also has entered into an agreement to acquire approximately 51 acres of undeveloped land in Lower Nazareth, Pennsylvania. The opportunity to acquire this land was also obtained through an auction held by the Trustee of the bankruptcy estate of the owner of the building recently acquired. The purchase price for the land is approximately $1.8 million plus acquisition expenses. The undeveloped land is also located in a major industrial area of the Lehigh Valley and is expected to support the development of two industrial buildings totaling approximately 530,000 square feet. Closing of this acquisition is subject to several conditions, including completion of due diligence by Griffin Land and obtaining certain municipal approvals. There is no guarantee that this transaction will be completed under its current terms, or at all.

Management expects to continue to seek industrial buildings and/or sites suitable for industrial development in markets outside of the Hartford, Connecticut area.

Residential Developments

Simsbury

In November 1999, Griffin Land filed plans for the creation of a residential community of 640 homes, called Meadowood, on a 363 acre site in Simsbury, Connecticut. One quarter of these homes were to be deed restricted under Connecticut statutes for affordable housing. The public hearings before Simsbury's land use commissions on this proposed residential development focused on the density of the proposed development, as well as sewer, wetlands and soil contamination issues arising from prior use of the land for farming, as a result of which certain pesticides remain in the upper portion of the soil. After the conclusion of the public hearings, Griffin Land amended its plans and reduced the number of proposed homes to 371. Simsbury's land use commissions rejected the amended plans, and Griffin Land filed several separate but related actions appealing the denials of the land use commissions. At the time the original application for Meadowood was filed, Griffin Land's proposal included a method (which has received support from the Connecticut Department of Environmental Protection) of remediating the soils of the residual pesticides. However, subsequent soil testing conducted by Griffin Land indicated that the residual pesticides that remain in the soil on much of the Meadowood site are below levels that would require remediation.

In December 2002, the trial court for two cases related to Meadowood ruled in favor of Griffin Land. Simsbury appealed those decisions, one of which was affirmed and the other, relating to planning, was reversed in part, due to the failure to have obtained a sewer connection approval for Meadowood, which was subsequently obtained. Those decisions could have required compliance with other court decisions on wetlands conservation and placement of septic systems within the sewer district that could have affected the proposed development. Griffin Land appealed an adverse decision on wetlands issues to the Connecticut Supreme Court, which reversed the decision and remanded the case to the trial level court for further consideration. In November 2003, Griffin Land filed a second amendment to its plans for Meadowood, which reduced the density to 298 homes, with certain land reserved for future development, and eliminated most activities in the wetlands and wetland upland areas. Simsbury's Conservation and Inland Wetlands Commission, which has jurisdiction of wetland issues, denied that application. That denial was appealed.

7

In early 2007, Griffin Land and the Town of Simsbury jointly filed a motion in the Appellate Court to have the appeal remanded to the Superior Court in anticipation of the parties potentially presenting a settlement proposal to the court for its review and approval. Also in 2007, Simsbury's Planning, Zoning and Inland Wetlands Commissions approved resolutions for settlement agreements. The settlement terms included, among other things, approval for up to 299 homes, certain remediation measures to be performed by Griffin Land and the purchase by the Town, subject to approvals, of a portion of the Meadowood land for Town open space. In February 2008, the Simsbury Planning Commission approved a resolution recommending that the Town acquire the portion of the Meadowood municipal open space. In March 2008, Griffin Land and Simsbury executed settlement agreements under the terms described above. The settlement agreements were subsequently approved by the Connecticut Superior Court, thus concluding the litigation on this matter with no further appeals possible. In May 2008, the Town of Simsbury approved the purchase of a portion of the Meadowood land for town open space. The sale of that land closed in the 2008 fourth quarter. Development of Meadowood remains subject to receiving certain environmental approvals from government agencies, including the Army Corps of Engineers and the Connecticut Department of Environmental Protection, which Griffin Land is seeking to obtain.

As of November 28, 2009, the book value of the land for this proposed development, including design, development and legal costs, was $4.7 million. Management believes that the costs for Meadowood that have been expended to date will be recovered.

Griffin Land owns another approximate 500 acres in Simsbury, portions of which are zoned for residential use and other portions of which are zoned for industrial use. Not all of this land is developable. The land currently zoned for industrial use is probably more suited to commercial or mixed use development. Griffin Land may seek to develop or sell such lands if approvals can be obtained.

Suffield

In 2003, Griffin Land received approval from the Planning and Zoning Commission of Suffield, Connecticut for the subdivision of 97 acres of contiguous land into a development of 50 homes called Stratton Farms. Griffin Land completed construction of the infrastructure for this residential development in fiscal 2005. In fiscal 2006, Griffin Land entered into a contract with a local homebuilder to sell the fifty residential lots over a three-year time period. The first sale, ten residential lots, was completed in fiscal 2006, and the second sale, fifteen residential lots, was completed in fiscal 2007. In fiscal 2008, the homebuilder did not exercise its option to purchase the next phase of residential lots, thereby canceling the option to acquire the remaining Stratton Farms lots. In fiscal 2008, Griffin Land recognized revenue of $125,000 attributed to the expiration of this option. The homebuilder's decision not to purchase any lots after 2007 was attributed to the weakening of the residential real estate market. In 2009, the homebuilder that purchased the twenty-five Stratton Farms lots entered into bankruptcy proceedings, and the remaining unsold lots held by the homebuilder were foreclosed on and sold by a local bank to a regional homebuilder.

Other

In fiscal 2009, Griffin Land leased approximately 690 acres of undeveloped land in Connecticut and Massachusetts to local farmers. Much of this land had previously been leased to General Cigar under a ten-year lease agreement that terminated in fiscal 2007. That lease was entered into when Griffin and General Cigar were wholly owned subsidiaries of Culbro Corporation. The revenue generated from the leasing of farmland is not material to Griffin Land's total revenue.

8

Griffin Land is evaluating its other properties for development or sale in the future. Griffin Land anticipates that obtaining subdivision approvals in many of the towns where it holds land appropriate for residential subdivision will be an extended process.

Landscape Nursery Business

The landscape nursery business of Griffin is operated by its wholly owned subsidiary, Imperial Nurseries, Inc. ("Imperial"). Imperial grows containerized landscape nursery plants for sale to independent garden centers, rewholesalers, whose main customers are landscape contractors, and mass merchandisers. Imperial's major markets are in the Northeast and mid-Atlantic areas of the United States. The landscape nursery industry is extremely fragmented, and after the shutdown of its Quincy, Florida farm in the 2009 third quarter (see below), Imperial believes it is one of the larger regional growers of landscape nursery products in the Northeast.

Through the 2009 third quarter, Imperial had two growing operations, its farm in Granby and East Granby, Connecticut on land owned by Griffin (approximately 445 acres currently used) and a farm in Quincy, Florida on land owned by Imperial (approximately 490 acres used). Substantially all of the useable contiguous acreage suitable for the container-growing operations in Connecticut is used, and a large portion of such acreage in northern Florida was used in the growing operations prior to the shutdown of the Florida farm. Imperial also uses approximately 45 acres of land in Connecticut to grow liners (starter plants) in the field for transplanting into containers. Imperial is in the process of relocating its field liner growing operation to other land owned by Griffin.

Imperial's sales are extremely seasonal, peaking in spring. They are strongly affected by weather conditions, particularly in the spring planting season, and are also affected by commercial and residential building activity. The slowdown in new housing starts during the past two years and the weak economy have adversely impacted Imperial's results. Imperial expects 2010 sales to be hampered by continued weakness in the economy and increased competition, as other growers of landscape nursery stock seek to liquidate inventories that were not sold in 2009. Imperial's sales are made to a large variety of customers, no single one of which represented more than 10% of Imperial's total sales in fiscal 2009, fiscal 2008 or fiscal 2007. However, aggregate net sales to Imperial's ten largest customers, including mass merchandisers, accounted for 24% of Imperial's total sales in fiscal 2009, 21% of Imperial's total net sales in fiscal 2008 and 25% of Imperial's total net sales in fiscal 2007. A significant amount of sales to independent garden centers are made through cooperative buying organizations. Approximately 19% of Imperial's total net sales in fiscal 2009 were made through buying cooperatives with 13% of Imperial's total net sales made through one buying cooperative.

Imperial's inventories consist principally of container-grown plants. The largest volume products of Imperial are evergreens, including rhododendron, flowering shrubs and perennials. Container-grown product is held principally from one to five years before it is sold. Several years ago, Imperial started selling some perennials and several other products as one of several licensed growers under the "Novalis" trade name. Imperial has entered into additional licensing agreements that enable it to grow and sell certain branded products available only to a limited number of growers. These programs are directed toward increasing Imperial's sales to independent garden centers. Over the past three years, Imperial has increased the percentage of its product sold to independent garden centers and reduced its sales to mass merchant customers. Sales to independent garden centers generally have more favorable gross margins as compared with sales to other customer segments.

In the 2009 third quarter, as previously approved by Griffin's Board of Directors, Imperial shut down its Quincy, Florida farm, which represented all of Imperial's growing operations in Florida. Imperial continues to operate its farm in Granby, Connecticut. The shutdown of the Florida farm reflected the difficulties that the farm encountered in delivering product to most of Imperial's major markets, which are located in the Northeast and Mid-Atlantic areas of the United States. Imperial was

9

unable to develop sufficient volume in southern markets that are closer to its Florida farm to reduce that farm's dependence on shipping product substantial distances. The closure of the Florida farm enables Imperial to focus as a regional grower with most of its major markets within close proximity of its Connecticut farm. Griffin reported charges totaling $8.9 million in connection with the restructuring of its landscape nursery business in its fiscal 2008 consolidated statement of operations as a result of the shutdown of Imperial's Florida farm. Of this amount, $7.2 million related to the writedown of inventories and was included in costs of landscape nursery sales and $1.7 million reflected the writeoff of fixed assets and severance payments and was reported as a restructuring charge on the consolidated statement of operations. The closing of the Florida farm increases the portion of the overhead of Imperial that will need to be covered by Connecticut farm operations. In fiscal 2009, costs of landscape nursery sales included a credit of $0.2 million for the difference between the amount estimated to be recovered from the sale of the remaining Florida inventories and actual results. Because the majority of the charge for the shutdown of the Florida farm was a non-cash charge that reflected the disposition of inventories below their carrying values at the time of sale, the closing of the Florida farm resulted in approximately $3.5 million of cash flow.

In the 2009 third quarter, Imperial entered into a six-year lease of its Florida farm to Tri-B Nursery, Inc. ("Tri-B"), a private company. The lease agreement with Tri-B includes an option for Tri-B to purchase the Florida farm at any time during the lease period at an agreed upon price.

Imperial continues to review ways to improve its operating results, including cost reductions for its remaining growing operations in Connecticut, changes in the relative quantities of some products currently grown, increasing sales to customer segments that are more profitable for Imperial and possible changes in the potting and growing cycles for some of its containerized production. In response to the difficult industry conditions, Imperial reduced its production of new plants in 2009 and expects to continue to reduce production levels in 2010. These changes are expected to result in a reduction in inventory levels over the next few years. Any changes to improve operating results, if successful, taking into account the growing cycles of the related plants, will take a substantial period of time to be reflected in Imperial's results of operations to any material extent.

In fiscal 2009, Imperial's cost of goods sold includes $2.1 million for inventory losses. The inventory losses reflect a higher than expected level of disposals of unsaleable product, increases to inventory reserves because the carrying costs of certain inventories exceed their net realizable values and the writeoff of certain inventories that will no longer be sold due to changes in product mix. The charges for unsaleable inventories and net realizable value issues were $1.1 million in fiscal 2008 and $0.7 million in fiscal 2007. The amount for fiscal 2008 is in addition to the inventory writedown recorded in connection with the shutdown of Imperial's Florida farm.

Shipping capacity and shipping expense are major cost concerns. Over the past several years, costs of shipping have increased significantly as the result of higher fuel costs and the need to arrange for the return of portable shelving units for subsequent shipments. Two years ago, Imperial increased its number of trucking vendors, improved the routing of shipments and purchased additional portable shelving units in order to better control its cost of shipping product to customers.

Investments

Centaur Media plc

In fiscal 2004, Griffin sold its holdings in Centaur Communications Ltd. ("Centaur Communications") and, in addition to the cash proceeds of $68.9 million, received 6,477,150 shares of common stock of Centaur Holdings plc ("Centaur Holdings"), approximately 4% of the outstanding common stock of Centaur Holdings at the time of the transaction. In June 2006, Centaur Holdings changed its name to Centaur Media plc ("Centaur Media"). Centaur Media is a publicly traded

10

company listed on the London Stock Exchange. In fiscal 2007, Griffin sold 1,200,000 shares of its Centaur Media common stock for proceeds of approximately $3.5 million, which resulted in a pretax gain of $2.9 million. Griffin has not sold any of its remaining Centaur Media stock since that time. Griffin accounts for its remaining investment in Centaur Media as an available-for-sale security. Accordingly, changes in the market value of Griffin's remaining investment in Centaur Media, including both changes in the stock price and changes in the foreign currency exchange rate, are not included in Griffin's net income but are included in Griffin's other comprehensive income.

Shemin Nurseries Holding Corp.

In fiscal 2001, Griffin sold the portion of Imperial's business that operated wholesale sales and service centers and received cash proceeds of $18.4 million and approximately 14% of the outstanding common stock of Shemin Acquisition Corp. ("Shemin Acquisition"), a privately held company that operated a landscape nursery distribution business and an irrigation supply business through its subsidiaries. Griffin accounted for its investment in Shemin Acquisition under the cost method of accounting for investments. In fiscal 2004, Griffin invested an additional $143,000 in Shemin Acquisition and maintained its approximate 14% ownership interest. In fiscal 2005, Griffin exchanged a portion of its holdings in Shemin Acquisition for common stock in Shemin Nurseries Holding Corp. ("SNHC"), which operates a landscape nursery distribution business through its subsidiary that previously was a wholly-owned subsidiary of Shemin Acquisition. Griffin then completed the sale of its remaining stock in Shemin Acquisition for cash proceeds of $5.7 million. Also in fiscal 2005, Griffin received a cash distribution of $1.7 million from SNHC. In fiscal 2007, Griffin received cash of $1.8 million from SNHC, which included dividend income of $1.6 million and a $0.2 million return of investment. Griffin did not receive any dividends or distributions from SNHC in fiscal 2008 or fiscal 2009. Griffin continues to hold its investment in SNHC and accounts for this investment under the cost method of accounting for investments.

Financial Information Regarding Industry Segments

See Note 2 to the consolidated financial statements of Griffin for certain financial information regarding the real estate business and the landscape nursery business.

Employees

As of November 28, 2009, Griffin employed 117 people on a full-time basis, including 90 in its landscape nursery business and 21 in its real estate business. Presently, none of Griffin's employees are represented by a union. Griffin believes that its relations with its employees are satisfactory.

Competition

Numerous real estate developers operate in the portions of Connecticut and Massachusetts in which Griffin's real estate holdings are concentrated and in the area of Pennsylvania where Griffin recently acquired a building and is under contract to acquire a parcel of undeveloped land. Some of these businesses may have greater financial resources than Griffin. Griffin's real estate business competes on the bases of location, price, availability of space, convenience and amenities.

The landscape nursery business is competitive, and Imperial competes against a number of other companies, including national, regional and local landscape nursery businesses. Some of Imperial's competitors in the landscape nursery industry are larger than Imperial. Growers of landscape nursery products compete on the bases of price, product quality, service and product availability.

11

Regulation: Environmental Matters

Under various federal, state and local laws, ordinances and regulations, an owner or operator of real estate may be required to investigate and clean up hazardous or toxic substances or petroleum product releases at such property and may be held liable to a governmental entity or to third parties for property damage and for investigation and clean-up costs incurred by such parties in connection with contamination. The cost of investigation, remediation or removal of such substances may be substantial, and the presence of such substances, or the failure to remediate properly such substances, may adversely affect the owner's ability to sell or rent such property or to borrow using such property as collateral. In connection with the ownership (direct or indirect), operation, management and development of real estate properties, Griffin Land may be considered an owner or operator of such properties or as having arranged for the disposal or treatment of hazardous or toxic substances and, therefore, potentially liable for removal or remediation costs, as well as certain other related costs, including governmental fines and injuries to persons and property. The value of Griffin's land may be affected by the presence of chlordane and dieldrin, arising from the prior use of the land for farming on a portion of the land that is intended for residential use. In the event that Griffin Land is unable to remediate adequately any of its land intended for residential use, Griffin Land's ability to develop such property for its intended purposes would be materially affected.

Griffin Land periodically reviews its properties for the purpose of evaluating such properties' compliance with applicable state and federal environmental laws. At this time, Griffin Land does not anticipate experiencing, in the next twelve months, any material expense in complying with such laws. Griffin Land may incur certain remediation costs in the future in connection with its development operations. Griffin Land is in the process of satisfying the Connecticut Department of Environmental Protection's requirements regarding potential remediation agreements on property purchased in fiscal 2006 in Manchester, Connecticut. Such costs are not expected to be significant as compared to expected proceeds from development projects or property sales.

Griffin's real estate and landscape nursery businesses have a number of risk factors. The risk factors discussed below are the ones that management deems to be material, but they may not be the only risks facing Griffin's businesses. Additional risks not currently known or currently deemed not to be material may also impact Griffin's businesses.

Adverse Economic Conditions and Credit Markets

Griffin Land's real estate business may be affected by market conditions and economic challenges experienced by the U.S. economy as a whole or by local economic conditions in the market in which its properties are located. The current conditions in the credit markets, or similar conditions existing in the future, may adversely affect Griffin's results of operations, financial condition or ability to expand as a result of the following:

- •

- The financial condition of Griffin Land's tenants may be adversely affected, which may result in tenant defaults under

leases due to bankruptcy, lack of liquidity, operational failures or for other reasons;

- •

- Significant job losses may occur, which may decrease demand for Griffin Land's office and industrial space, causing market

rental rates and property values to be negatively impacted;

- •

- Griffin's ability to borrow on terms and conditions that it finds acceptable, or at all, may be limited, which could reduce its ability to pursue acquisition and development opportunities, refinance existing debt, and/or increase future interest expense;

12

- •

- Reduced values of Griffin Land's properties may limit its ability to obtain debt financing collateralized by its properties or may limit the proceeds from such potential financings.

Imperial's landscape nursery business may also be affected by the weakness in the U.S. economy. Landscape nursery products are a discretionary purchase, and the softening of demand for such products at the retail level may result in the reduction of orders by Imperial's independent garden center customers. Weakness in demand would also result in lower pricing, as other growers of landscape nursery products seek to liquidate inventories before product becomes unsaleable.

Downturn in the Residential Real Estate Market

The decline in the residential real estate market may adversely affect Griffin Land's real estate development activities, including delaying the development and/or sale of Griffin Land's undeveloped land intended for residential use. The slowdown in new housing starts may also adversely affect Imperial's future results. Although Imperial only has minimal sales of product to home builders, they are the ultimate users of a portion of the product sold to Imperial's rewholesaler customer segment, which accounted for approximately 43% of Imperial's sales in fiscal 2009.

Risks Associated with Concentration of Real Estate Holdings

Griffin Land's real estate operations are concentrated in the Hartford, Connecticut area. Adverse changes in the local economy or real estate market could impact Griffin Land's real estate operations, including the market's ability to absorb newly constructed space and Griffin Land's ability to retenant vacant space.

Risks Associated with Entering New Real Estate Markets

Griffin Land recently closed on the acquisition of an approximate 120,000 square foot industrial building in Breinigsville, Pennsylvania, and Griffin Land entered into a contract to purchase approximately 51 acres of undeveloped land in Lower Nazareth, Pennsylvania. These acquisitions are Griffin's Land's first purchases of properties outside of the Hartford, Connecticut market where Griffin Land's core real estate holdings are located. Griffin Land expects to continue to seek to acquire properties outside of the Hartford, Connecticut market. Operating in a real estate market that is new for Griffin Land creates additional risks and uncertainties to Griffin's operations as Griffin Land becomes familiar with the local real estate market.

Potential Environmental Liabilities

Griffin Land has extensive land holdings in Connecticut and Massachusetts. Under federal, state and local environmental laws, ordinances and regulations, Griffin Land may be required to investigate and clean up the effects of releases of hazardous substances or petroleum products at its properties because of its current or past ownership or operation of the real estate. If previously unidentified environmental problems arise, Griffin Land may have to make substantial payments, which could adversely affect its cash flow. As an owner or operator of properties, Griffin Land may have to pay for property damage and for investigation and clean-up costs incurred in connection with the contamination. The law typically imposes clean-up responsibility and liability regardless of whether the owner or operator knew of or caused the contamination.

Competition and Governmental Regulations

Griffin Land's real estate operations compete with other properties in Griffin Land's area of operation. The construction of new facilities by competitors would increase capacity in the marketplace, which could result in Griffin Land experiencing longer times to lease vacant space, eroding lease rates or hindering renewals by existing tenants. Griffin Land's real estate operations are subject to

13

governmental regulations that affect real estate development, such as local zoning ordinances. Any changes in such regulations may impact the ability of Griffin Land to develop its properties.

Insurance Coverage Does Not Include All Potential Losses in the Real Estate Business

Griffin Land carries comprehensive insurance coverage, including property, fire, terrorism and loss of rental revenue. The insurance coverage contains policy specifications and insured limits. Griffin Land believes its properties are adequately insured. However, there are certain losses that are not generally insured against or that are not fully insured against. If an uninsured loss or a loss in excess of insured limits occurs with respect to one or more of Griffin Land's properties, Griffin Land could experience a significant loss of capital invested and potential revenue from the properties affected.

Risks of Agricultural and Environmental Factors

Imperial's production of plants may be adversely affected by agricultural and environmental factors beyond its control, such as extreme cold during the winter months or severe drought conditions. While management believes that Imperial's Connecticut farm has sufficient water supplies available, a severe drought could impact Imperial's ability to maintain adequately its inventory. In addition, a severe drought in Imperial's major sales markets could substantially impact Imperial's sales.

Other agricultural or environmental factors that could materially impact Imperial's growing operations are plant diseases, pests and the improper use of herbicides and pesticides. The occurrence of any one of these factors could materially affect Imperial's growing operations and result in a portion of Imperial's inventory becoming unsaleable.

Concentration of Customers

Although no single customer of Imperial accounted for more than 10% of Imperial's total net sales in fiscal 2009, Imperial's ten largest customers, including two mass merchandisers, accounted for approximately 24% of Imperial's total net sales in fiscal 2009. Management expects that a small number of customers will continue to account for a significant portion of Imperial's net sales over the next several years. Imperial has one customer with which it has a sales contract. Total revenue under that sales contract was approximately $0.3 million in fiscal 2009. Sales to independent garden centers made through buying cooperatives accounted for 19% of Imperial's total net sales in fiscal 2009, with sales through one buying cooperative accounting for 13% of Imperial's total net sales. The loss of one of Imperial's larger customers or the inability to collect accounts receivable from one of the buying cooperatives could have an adverse effect on Imperial.

None of Griffin Land's tenants accounted for 10% or more of its total rental revenue in fiscal 2009.

Shutdown of Imperial's Florida Farm

In fiscal 2009, Imperial completed the shutdown of operations on its farm located in Quincy, Florida. Starting in fiscal 2010, Imperial will grow and ship plants only from its Granby, Connecticut farm, which Imperial continues to operate. The closure of the Florida farm reduces the breadth of Imperial's product offerings which could cause Imperial's customers to reduce their purchases of Imperial's products and seek alternative suppliers who are able to supply a broader range of customers' requirements.

Regulatory Risks

Imperial's operations are subject to various laws and environmental regulations. The failure to comply with such laws and environmental regulations could result in liabilities being incurred for

14

Imperial's actions. Recently, there has been an increase in legislation regarding the sale and transportation of plant varieties considered to be "invasive" by state governments. The continuation of such legislation could adversely impact Imperial's operations by reducing the area where inventories of plants considered to be invasive may be sold or transported.

Risks Associated with the Cost of Raw Materials and Energy Costs

Imperial's operations could be adversely affected by increases in the cost of growing plants, the costs of certain materials and energy costs. Prices of certain petroleum based materials, such as plant containers and plastics used in protecting inventory during the winter, have increased as overall petroleum prices have increased. In addition, increases in energy costs and the lack of availability of energy could also adversely impact Imperial's operations which uses heat generated from natural gas and propane to maintain certain parts of its inventory during the winter.

Griffin Land's construction activities could be adversely affected by increases in raw materials or energy costs. As petroleum and other energy costs increase, products used in the construction of Griffin Land's facilities, such as steel, masonry, asphalt, cement and building products may increase. The cost of such items increased in 2008 but have subsequently returned to lower levels. An increase in the cost of building new facilities would negatively impact Griffin Land's future operating results through increased depreciation expense. An increase in construction costs would also require increased investment in Griffin Land's real estate assets, which may lower the return on investment in new facilities in the real estate business.

Availability of Transportation Vendors to Deliver Product

Substantially all of Imperial's sales are delivered to customers' locations using independent contractors for trucking services. The ability to ship products timely, especially during the peak spring shipping season, could be adversely impacted by shortages in available trucking capacity. Significant increases in transportation costs could have a material adverse effect on Imperial's business, as customers may choose to purchase product from local growers or Imperial may not be able to pass along such increases to customers.

Availability of Labor

Labor costs comprise a substantial portion of Imperial's production costs. Imperial is subject to the Fair Labor Standards Act as well as various federal, state and local regulations that govern matters such as minimum wage requirements, working conditions and worker regulations. As a significant amount of Imperial's seasonal employees are paid at slightly above minimum wage rates, any increase in such minimum wage rates could adversely impact Imperial's results. In addition, Imperial depends on a significant amount of seasonal labor, particularly during its peak shipping period in the spring. Changes in immigration laws could make it more difficult for Imperial to meet its seasonal labor requirements, which could adversely affect Imperial's operations.

Risks of Loss in the Landscape Nursery Business Not Covered by Insurance

Imperial carries comprehensive insurance coverage, including property, liability, fire and terrorism on its production facilities and its inventories. The insurance contains policy specifications and insured limits, and does not cover all possible losses that Imperial could incur.

Investment in Foreign Company

Griffin has an investment in Centaur Media plc, a public company based in the United Kingdom. The ultimate liquidation of that investment and conversion of proceeds into United States currency is subject to future foreign currency exchange rates.

15

Litigation

Griffin is involved, as a defendant, in various litigation matters arising in the ordinary course of business. In the opinion of management, based on the advice of legal counsel, the ultimate liability, if any, with respect to these matters will not be material, individually or in the aggregate, to Griffin's consolidated financial position, results of operations or cash flows.

The Concentrated Ownership of Griffin Common Stock by Members of the Cullman and Ernst Families

Members of the Cullman and Ernst families (the "Cullman and Ernst Group"), which include Edgar M. Cullman and David M. Danziger, directors of Griffin, Frederick M. Danziger, director and Griffin's President and Chief Executive Officer, and Michael S. Gamzon, a Vice President of Griffin, members of their families and trusts for their benefit, partnerships in which they own substantial interests and charitable foundations on whose boards of directors they sit, owned, directly or indirectly, approximately 49.2% of the outstanding common stock of Griffin as of November 28, 2009. There is an informal understanding that the persons and entities included in the Cullman and Ernst Group will vote together the shares owned by each of them. As a result, the Cullman and Ernst Group may effectively control the determination of Griffin's corporate and management policies and may limit other Griffin stockholders' ability to influence Griffin's corporate and management policies.

16

ITEM 1B. UNRESOLVED STAFF COMMENTS

Not applicable.

Land Holdings

Griffin is a major landholder in the State of Connecticut, owning approximately 3,560 acres, and also owns approximately 440 acres of land in Massachusetts. In addition, Griffin owns approximately 1,070 acres in northern Florida, most of the useable portion of which was used for Imperial's growing operations or was contiguous to such operations. In fiscal 2009, Imperial shut down its Florida growing operations and entered into a six-year lease of the Florida farm to another grower. The lessee of the Florida farm also has an option to purchase that farm at any time during the lease term.

At November 28, 2009, the book value of undeveloped land holdings, including land improvements, owned by Griffin, principally in the Hartford, Connecticut area, was approximately $16.4 million. Griffin believes the fair market value of such land is substantially in excess of its book value, including land improvements.

Listings of the locations of Griffin's land holdings, a portion of which, principally in Bloomfield, East Granby and Windsor, Connecticut have been developed, and nursery real estate, are as follows:

Location

|

Land Area (in acres) | ||||

|---|---|---|---|---|---|

Connecticut |

|||||

Bloomfield |

325 | ||||

East Granby |

150 | ||||

East Windsor |

115 | ||||

Granby |

106 | ||||

Manchester |

30 | ||||

Simsbury |

785 | ||||

Suffield |

299 | ||||

Windsor |

969 | ||||

Massachusetts |

|||||

Southwick |

436 | ||||

Location

|

Land Area (in acres) | ||||

|---|---|---|---|---|---|

Florida |

|||||

Quincy (currently leased to another grower) |

1,066 | ||||

Connecticut |

|||||

East Granby |

424 | ||||

Granby |

305 | ||||

Windsor |

45 | ||||

Simsbury |

10 | ||||

17

As of November 28, 2009, Griffin Land owned twenty-eight industrial, flex and office buildings and a small restaurant building. A listing of those facilities is as follows:

Griffin Center |

|||||||

1985 Blue Hills Avenue, Bloomfield, CT* |

Industrial building | 165,000 sq. ft. | |||||

5 Waterside Crossing, Windsor, CT* |

Office building | 80,500 sq. ft. | |||||

7 Waterside Crossing, Windsor, CT* |

Office building | 80,500 sq. ft. | |||||

21 Griffin Road North, Windsor, CT* |

Office building | 48,300 sq. ft. | |||||

1936 Blue Hills Avenue, Windsor, CT |

Restaurant building | 7,200 sq. ft. | |||||

Griffin Center South |

|||||||

29-35 Griffin Road South, Bloomfield, CT* |

Flex building | 57,500 sq. ft. | |||||

55 Griffin Road South, Bloomfield, CT |

Office/flex building | 40,300 sq. ft. | |||||

340 West Newberry Road, Bloomfield, CT* |

Office/flex building | 39,000 sq. ft. | |||||

206 West Newberry Road, Bloomfield, CT* |

Office/flex building | 23,200 sq. ft. | |||||

204 West Newberry Road, Bloomfield, CT* |

Office/flex building | 22,300 sq. ft. | |||||

210 West Newberry Road, Bloomfield, CT* |

Warehouse building | 18,400 sq. ft. | |||||

330 West Newberry Road, Bloomfield, CT* |

Office/flex building | 11,900 sq. ft. | |||||

310 West Newberry Road, Bloomfield, CT* |

Office/flex building | 11,400 sq. ft. | |||||

320 West Newberry Road, Bloomfield, CT* |

Office/flex building | 11,100 sq. ft. | |||||

New England Tradeport |

|||||||

100 International Drive, Windsor, CT* |

Industrial building | 304,200 sq. ft. | |||||

755 Rainbow Road, Windsor, CT |

Industrial building | 148,500 sq. ft. | |||||

758 Rainbow Road, Windsor, CT* |

Industrial building | 137,000 sq. ft. | |||||

754 Rainbow Road, Windsor, CT* |

Industrial building | 136,900 sq. ft. | |||||

759 Rainbow Road, Windsor, CT |

Industrial building | 126,900 sq. ft. | |||||

75 International Drive, Windsor, CT* |

Industrial building | 117,000 sq. ft. | |||||

20 International Drive, Windsor, CT* |

Industrial building | 99,800 sq. ft. | |||||

40 International Drive, Windsor, CT* |

Industrial building | 99,800 sq. ft. | |||||

35 International Drive, Windsor, CT |

Industrial building | 97,600 sq. ft. | |||||

16 International Drive, Windsor, CT* |

Industrial building | 58,400 sq. ft. | |||||

25 International Drive, Windsor, CT* |

Industrial building | 57,200 sq. ft. | |||||

15 International Drive, Windsor, CT* |

Industrial building | 41,600 sq. ft. | |||||

14 International Drive, Windsor, CT* |

Industrial building | 40,100 sq. ft. | |||||

Other Properties |

|||||||

61 Chapel Road, Manchester, CT |

Industrial building | 307,700 sq. ft. | |||||

1370 Blue Hills Avenue, Bloomfield, CT |

Industrial building | 30,700 sq. ft. | |||||

* Included as collateral under one of Griffin's nonrecourse mortgages or Griffin's revolving line of credit.

Griffin leases approximately 2,200 square feet in New York City for its executive offices.

As with many companies engaged in real estate investment and development, Griffin holds its real estate portfolio subject to mortgage debt. See Note 10 to Griffin's consolidated financial statements for information concerning the mortgage debt associated with Griffin's properties.

18

As discussed in Item 1, certain parts of Griffin's property in Simsbury, Connecticut, are affected by the presence of residual pesticides from the prior use of such land for farming. Although various federal, state and local agencies may have an interest in the matter, there are no proceedings known by Griffin to be contemplated by any of these agencies with respect to the residual pesticides.

In 1999, Griffin Land filed land use applications with the land use commissions of Simsbury, Connecticut for Meadowood, a proposed residential development on approximately 363 acres of land. In 2000, Simsbury's land use commissions issued denials of Griffin Land's Meadowood application. As a result of those denials, Griffin brought several separate, but related, suits appealing those decisions. In 2002, the trial court upheld two of Griffin Land's appeals and ordered the town's Planning and Zoning Commissions to approve the Meadowood application. The Town appealed those decisions. In 2004, the Connecticut Supreme Court ordered the Zoning Commission to approve the zoning regulations proposed by Griffin Land for Meadowood. The Connecticut Supreme Court also ruled that the denial of the Meadowood application by the Planning Commission can be upheld because Griffin Land had not obtained the required sewer usage permits at the time the application was made to the Planning Commission. The required sewer usage permits for Meadowood were subsequently obtained. Also in 2004, the Connecticut Supreme Court reversed a lower court decision that had denied Griffin Land a wetlands permit, and remanded the case to Superior Court for further proceedings to determine if a wetlands permit must be issued. In 2005, the Superior Court ruled that Griffin Land must again apply to the Town's Conservation and Inland Wetlands Commission for a wetlands permit for its proposed Meadowood development.

In early 2007, Griffin Land and the Town of Simsbury jointly filed a motion in the Appellate Court to have the appeal remanded to the Superior Court in anticipation of the parties potentially presenting a settlement proposal to the court for its review and approval. Also in 2007, the Town's Planning, Zoning and Inland Wetlands Commissions approved resolutions for settlement agreements. The settlement terms included, among other things, approval for up to 299 homes, certain remediation measures to be performed by Griffin Land and the purchase by the Town, subject to approvals, of a portion of the Meadowood land for town open space. In February 2008, the Simsbury Planning Commission approved a resolution recommending that the Town acquire the portion of the Meadowood land as outlined in the settlement agreements if such land is substantially clean and suitable for use as municipal open space. In March 2008, Griffin Land and Simsbury executed settlement agreements under the terms described above. The settlement agreements were approved by the Connecticut Superior Court on April 18, 2008 and April 28, 2008, thus concluding the litigation on this matter with no further appeals possible. In May 2008, the Town of Simsbury approved the purchase of a portion of the Meadowood land for town open space. The sale of that land closed in November 2008. Development of Meadowood remains subject to receiving certain environmental approvals from government agencies, including the Army Corps of Engineers and the Connecticut Department of Environmental Protection, which Griffin Land is seeking to obtain.

Griffin is involved, as a defendant, in various litigation matters arising in the ordinary course of business. In the opinion of management, based on the advice of legal counsel, the ultimate liability, if any, with respect to these matters will not be material to Griffin's financial position, results of operations or cash flows.

ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

None.

19

ITEM 5. MARKET FOR THE REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER

MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

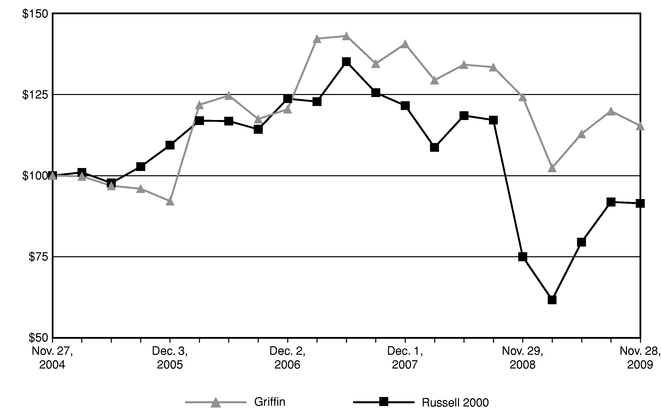

The following are the high and low prices of common shares of Griffin Land & Nurseries, Inc. as traded on the NASDAQ Stock Market LLC:

| |

1st Quarter | 2nd Quarter | 3rd Quarter | 4th Quarter | |||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

High | Low | High | Low | High | Low | High | Low | |||||||||||||||||

2009 |

$ | 37.44 | $ | 23.84 | $ | 36.91 | $ | 21.50 | $ | 34.23 | $ | 25.30 | $ | 33.22 | $ | 27.36 | |||||||||

2008 |

$ | 37.00 | $ | 31.60 | $ | 36.93 | $ | 31.50 | $ | 37.00 | $ | 30.54 | $ | 41.50 | $ | 22.73 | |||||||||

On February 1, 2010, the number of record holders of common stock of Griffin was approximately 329, which does not include beneficial owners whose shares are held of record in the names of brokers or nominees. The closing market price as quoted on the NASDAQ Stock Market LLC on such date was $27.69 per share.

Issuer Purchases of Equity Securities

On January 30, 2007, Griffin's Board of Directors authorized the repurchase of up to 150,000 shares of Griffin's outstanding common stock through private transactions. The program to repurchase did not obligate Griffin to repurchase any specific number of shares, and could have been suspended at any time at management's discretion. In November 2007, the Board of Directors increased by 100,000 shares the number of shares authorized for repurchase under the program and extended the program through December 31, 2008. There were no share repurchases from November 29, 2008 through December 31, 2008, when the share repurchase program expired and was not renewed.

From the time Griffin became a public company in 1997 through the third quarter of fiscal 2007, Griffin did not pay dividends to its stockholders. In the 2007 fourth quarter, Griffin declared a quarterly cash dividend of $0.10 per share on its common stock. In fiscal 2008 and fiscal 2009, Griffin declared a cash dividend of $0.10 per share for each quarter. Griffin expects to pay quarterly dividends to its shareholders in future quarters subject to the Board of Directors' evaluation of other uses for Griffin's cash and of Griffin's liquidity.

Securities Authorized For Issuance Under Equity Compensation Plans

Plan Category

|

Number of securities to be issued upon exercise of outstanding options (a) |

Weighted average exercise price of outstanding options (b) |

Number of securities remaining available for future issuance under the equity compensation plan (excluding securities reflected in column(a)) (c) |

|||||||

|---|---|---|---|---|---|---|---|---|---|---|

Equity compensation plan approved by security holders |

172,510 | $ | 26.56 | 382,197 | ||||||

Note: There are no equity compensation plans that were not approved by security holders.

20