Attached files

Table of Contents

UNITED STATES SECURITIES AND

EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2009

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

for the transition period from to

| Commission file number 001-14768 | I.R.S. Employer Identification Number 04-3466300 |

NSTAR

(Exact name of registrant as specified in its charter)

| Massachusetts | 800 Boylston Street, Boston, Massachusetts | |

| (State or other jurisdiction of incorporation or organization) | (Address of principal executive offices) | |

| 617-424-2000 | 02199 | |

| (Registrant’s telephone number, including area code) | (Zip code) | |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Common Shares, par value $1 per share | New York Stock Exchange |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

x Yes ¨ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

¨ Yes ¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company, as defined in Rule 12b-2 of the Exchange Act.

| Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨ Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

¨ Yes x No

The aggregate market value of the 106,808,376 shares of voting stock of the registrant held by non-affiliates of the registrant, computed as the average of the high and low market prices of the common shares as reported on the New York Stock Exchange consolidated transaction reporting system for NSTAR Common Shares as of the last business day of the registrant’s most recently completed second fiscal quarter: $3,396,506,000.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date:

| Class |

Outstanding at February 5, 2010 | |

| Common Shares, par value $1 per share | 106,808,376 shares |

Documents Incorporated by Reference

Portions of NSTAR’s Definitive Proxy Statement relating to the Annual Meeting of Shareholders to be held on May 6, 2010 are to be filed with the SEC under Regulation 14A within 120 days after the end of NSTAR’s fiscal year and, upon such filing, to be incorporated by reference into Parts I and III of this Form 10-K.

Table of Contents

NSTAR

Index to Annual Report on Form 10-K

Year Ended December 31, 2009

1

Table of Contents

The following is a glossary of abbreviated names or acronyms frequently used throughout this report.

| NSTAR Companies |

||

| NSTAR |

NSTAR (Holding company), Company or NSTAR and its subsidiaries (as the context requires) | |

| NSTAR Electric |

NSTAR Electric Company | |

| NSTAR Gas |

NSTAR Gas Company | |

| NSTAR Electric & Gas |

NSTAR Electric & Gas Corporation | |

| MATEP |

Medical Area Total Energy Plant, Inc. | |

| AES |

Advanced Energy Systems, Inc. (Parent company of MATEP) | |

| NSTAR Com |

NSTAR Communications, Inc. | |

| Hopkinton |

Hopkinton LNG Corp. | |

| HEEC |

Harbor Electric Energy Company | |

| Unregulated operations |

Represents non-regulated operations of NSTAR Com and Hopkinton | |

| Discontinued operations |

Represents operations of MATEP | |

| Regulatory and Other Authorities |

||

| DOE |

U.S. Department of Energy | |

| DPU |

Massachusetts Department of Public Utilities | |

| FERC |

Federal Energy Regulatory Commission | |

| IRS |

U.S. Internal Revenue Service | |

| ISO-NE |

ISO (Independent System Operator) - New England Inc. | |

| Moody’s |

Moody’s Investors Service | |

| NRC |

U.S. Nuclear Regulatory Commission | |

| NYMEX |

New York Mercantile Exchange | |

| PCAOB |

Public Company Accounting Oversight Board (United States) | |

| SEC |

U.S. Securities and Exchange Commission | |

| S&P |

Standard & Poor’s | |

| Other |

||

| AFUDC |

Allowance for Funds Used During Construction | |

| AOCI |

Accumulated Other Comprehensive Income | |

| ARO |

Asset Retirement Obligation | |

| ARRA |

American Recovery and Reinvestment Act of 2009 | |

| ASC |

Financial Accounting Standards Board (U.S) Accounting Standards Codification | |

| BBtu |

Billions of British thermal units | |

| Bcf |

Billion cubic feet | |

| CAP |

IRS Compliance Assurance Process | |

| CGAC |

Cost of Gas Adjustment Clause | |

| CPSL |

Capital Projects Scheduling List | |

| CY |

Connecticut Yankee Atomic Power Company | |

| DSM |

Demand-Side Management | |

| EEI Index |

Edison Electric Institute Stock Index of U.S. Shareholder - Owned Electric Utilities | |

| EERF |

Energy Efficiency Reconciling Factor | |

| EPS |

Earnings Per Common Share | |

| FCA |

Forward Capacity Auction | |

| FCM |

Forward Capacity Market | |

| GAAP |

Accounting principles generally accepted in the United States of America | |

| GCA |

Massachusetts Green Communities Act of 2007 | |

| GWSA |

Massachusetts Global Warming Solutions Act | |

2

Table of Contents

| ISFSI |

Independent Spent Fuel Storage Installation | |

| kW |

Kilowatt (equal to one thousand watts) | |

| kWh |

Kilowatthour (the basic unit of electric energy equal to one kilowatt of power supplied for one hour) | |

| LDAC |

Local Distribution Adjustment Clause | |

| LNG |

Liquefied Natural Gas | |

| MD&A |

Management’s Discussion and Analysis of Financial Condition and Results of Operations | |

| MGP |

Manufactured Gas Plant | |

| MMbtu |

Millions of British thermal units | |

| MW |

Megawatts | |

| MWh |

Megawatthour (equal to one million watthours) | |

| MY |

Maine Yankee Atomic Power Company | |

| NEH |

New England Hydro-Transmission Electric Company, Inc. | |

| NHH |

New England Hydro-Transmission Corporation | |

| OATT |

Open Access Transmission Tariff | |

| PAM |

Pension and PBOP Rate Adjustment Mechanism | |

| PBOP |

Postretirement Benefit Obligation other than Pensions | |

| PPA |

Pension Protection Act of 2006 | |

| RMR |

Reliability Must Run | |

| ROE |

Return on Equity | |

| RTO |

Regional Transmission Organization | |

| SIP |

Simplified Incentive Plan | |

| SQI |

Service Quality Indicators | |

| SSCM |

Simplified Service Cost Method | |

| WRERA |

Worker, Retiree and Employer Recovery Act of 2008 | |

| YA |

Yankee Atomic Electric Company | |

| N/A |

Not applicable | |

3

Table of Contents

Cautionary Statement Regarding Forward-Looking Information

This Annual Report on Form 10-K contains statements that are considered forward-looking statements within the meaning of the Securities Act of 1933 and the Securities Exchange Act of 1934. These forward-looking statements may also be contained in other filings with the SEC, in press releases, and oral statements. You can identify these statements by the fact that they do not relate strictly to historical or current facts. They use words such as “anticipate,” “estimate,” “expect,” “project,” “intend,” “plan,” “believe,” and other words and terms of similar meaning in connection with any discussion of future operating or financial performance. These statements are based on the current expectations, estimates or projections of management and are not guarantees of future performance. Some or all of these forward-looking statements may not turn out to be what NSTAR expected. Actual results could differ materially from these statements. Therefore, no assurance can be given that the outcomes stated in such forward-looking statements and estimates will be achieved.

Examples of some important factors that could cause our actual results or outcomes to differ materially from those discussed in the forward-looking statements include, but are not limited to, the following:

| • | adverse financial market conditions including changes in interest rates and the availability and cost of capital |

| • | adverse economic conditions |

| • | changes to prevailing local, state, and federal governmental policies and regulatory actions (including those of the DPU and the FERC) with respect to allowed rates of return, rate structure, continued recovery of regulatory assets and energy costs, financings, municipalization, acquisition and disposition of assets, operation and construction of facilities, changes in tax laws and policies, and changes in, and compliance with, environmental and safety laws and policies |

| • | new governmental regulations or changes to existing regulations that impose additional operating requirements or liabilities |

| • | changes in available information and circumstances regarding legal issues and the resulting impact on our estimated litigation costs |

| • | weather conditions that directly influence the demand for electricity and natural gas |

| • | impact of continued cost control processes on operating results |

| • | ability to maintain current credit ratings |

| • | impact of uninsured losses |

| • | impact of adverse union contract negotiations |

| • | damage from major storms |

| • | impact of conservation measures and self-generation by our customers |

| • | changes in financial accounting and reporting standards |

| • | changes in hazardous waste site conditions and the cleanup technology |

| • | prices and availability of operating supplies |

| • | impact of terrorist acts and cyber-attacks, and |

| • | impact of service quality performance measures |

Any forward-looking statement speaks only as of the date of this filing and NSTAR undertakes no obligation to publicly update forward-looking statements, whether as a result of new information, future events, or otherwise. You are advised, however, to consult all further disclosures NSTAR makes in its filings to the SEC. Other factors in addition to those listed here could also adversely affect NSTAR. This Annual Report also describes material contingencies and critical accounting policies and estimates in the accompanying Item 1A, “Risk Factors,” Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and in the accompanying Notes to Consolidated Financial Statements and NSTAR encourages a review of these items.

4

Table of Contents

Part I

| Item 1. | Business |

(a) General Development of Business

NSTAR (or the Company) is a holding company engaged through its subsidiaries in the energy delivery business serving approximately 1.4 million customers in Massachusetts, including approximately 1.1 million electric distribution customers in 81 communities and approximately 300,000 natural gas distribution customers in 51 communities. Utility operations accounted for approximately 99% of consolidated operating revenues from continuing operations in 2009, 2008, and 2007. The remaining revenue is generated from its unregulated operations.

NSTAR’s utility operations derive their operating revenues primarily from electric and natural gas sales, distribution, and transmission services to customers. NSTAR’s earnings are impacted by fluctuations in unit sales of electric kWh and natural gas MMbtu, which directly determine the level of distribution revenues recognized. In accordance with the regulatory rate structure in which NSTAR operates, its recovery of energy and certain energy-related costs are fully reconciled with the level of energy revenues currently recorded and, therefore, do not have an impact on earnings. As a result of this rate structure, any variability in the cost of energy supply purchased will have an impact on the purchased power and transmission and cost of gas sold expenses, but will not affect the Company’s net income as the Company recognizes a corresponding change in revenues.

On December 21, 2009, NSTAR reached an agreement to sell Medical Area Total Energy Plant, Inc. (MATEP), NSTAR’s unregulated district energy operation in Boston’s Longwood Medical Area. MATEP provides chilled water, steam, and electricity to several hospitals, medical research and biotechnology centers, and teaching institutions, and is accounted for as a discontinued operation held for sale in the accompanying consolidated financial statements.

(b) Financial Information about Industry Segments

NSTAR’s principal operating segments or line of regulated utility businesses are electric and natural gas distribution operations that provide energy transmission and delivery services in 107 cities and towns in Massachusetts and its unregulated operations. Refer to Note M, “Segment and Related Information” of the accompanying Notes to Consolidated Financial Statements in Item 8, “Financial Statements and Supplementary Data” for specific financial information related to NSTAR’s electric utility, natural gas utility, and unregulated operations segments.

(c) Narrative Description of Business

Principal Products and Services

NSTAR Electric

NSTAR Electric supplies distribution and transmission electricity service at retail to an area of 1,702 square miles. The territory served is located in Massachusetts and includes the City of Boston and 80 surrounding cities and towns, including Cambridge, New Bedford, Plymouth, and the geographic area comprising Cape Cod and Martha’s Vineyard. The population of this area is approximately 2.4 million.

NSTAR Electric’s operating revenues and sales percentages by customer class for the years 2009, 2008, and 2007 consisted of the following:

| Revenues ($) | Retail Electric Sales (mWh) | |||||||||||||||||

| 2009 | 2008 | 2007 | 2009 | 2008 | 2007 | |||||||||||||

| Retail: |

||||||||||||||||||

| Commercial and industrial |

57 | % | 57 | % | 56 | % | 68 | % | 69 | % | 69 | % | ||||||

| Residential |

42 | % | 42 | % | 43 | % | 31 | % | 30 | % | 30 | % | ||||||

| Other |

1 | % | 1 | % | 1 | % | 1 | % | 1 | % | 1 | % | ||||||

5

Table of Contents

Regulated Electric Distribution Rates

Retail electric delivery rates are established by the DPU and are comprised of:

| • | a distribution charge, which includes a fixed customer charge and a demand and/or energy charge (to collect the costs of building and expanding the infrastructure to deliver power to its destination, as well as ongoing operating costs and certain DPU-approved safety and reliability programs costs), a Pension and PBOP Rate Adjustment Mechanism (PAM) to recover incremental pension and pension benefit costs, a reconciling rate adjustment mechanism to recover costs associated with the residential assistance adjustment clause, and an Energy Efficiency Reconciling Factor (EERF) to recover energy efficiency expenditures in addition to those charges recovered in the energy conservation charge; |

| • | a basic service charge represents the collection of energy costs, including costs related to charge-offs of uncollected energy costs, through DPU-approved rate mechanisms. Electric distribution companies in Massachusetts are required to obtain and resell power to retail customers through Basic Service for those who choose not to buy energy from a competitive energy supplier. Basic Service rates are reset every six months (every three months for large commercial and industrial customers). The price of Basic Service is intended to reflect the average competitive market price for electric power; |

| • | a transition charge represents the collection of costs primarily from previously held investments in generating plants and costs related to existing above-market power contracts, and contract costs related to long-term power contracts buy-outs; |

| • | a transmission charge represents the collection of costs of moving the electricity over high voltage lines from generating plants to substations located within NSTAR’s service area including costs allocated to NSTAR Electric by ISO-NE to maintain the wholesale electric market; |

| • | an energy conservation charge represents a legislatively-mandated charge to collect costs for demand-side management programs and energy efficiency programs; and |

| • | a renewable energy charge represents a legislatively-mandated charge to collect the costs to support the development and promotion of renewable energy projects. |

Rate Settlement Agreement

NSTAR Electric is currently operating under a DPU approved Rate Settlement Agreement (Rate Settlement Agreement) that expires December 31, 2012. From 2007 through 2012, the Rate Settlement Agreement establishes for NSTAR Electric, among other things, annual inflation-adjusted distribution rate adjustments that are generally offset by an equal and corresponding reduction in transition rates. Refer to the “Rate Settlement Agreement” section of the accompanying Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” for more details.

Massachusetts Regulatory Environment

The Secretary of Energy and Environmental Affairs oversees the Commonwealth Utilities Commission, consisting of three commissioners. The Commonwealth Utilities Commission leads the DPU, an agency that has jurisdiction over electric, natural gas, water, and transportation matters. Massachusetts has joined the Regional Greenhouse Gas Initiative, a multi-state group that supports implementation of programs to reduce the production of greenhouse gases by electric power plants.

In July 2008, the Massachusetts Legislature enacted the Green Communities Act (GCA)-energy policy legislation designed: (1) to substantially increase energy efficiency, (2) foster the development of renewable energy resources and (3) provide for a reduction of greenhouse gas emissions in Massachusetts. Refer to the “Massachusetts Regulatory Environment” section of the accompanying Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” for more details.

6

Table of Contents

Rate Decoupling

On July 16, 2008, the DPU issued an order to all Massachusetts’ electric and gas distribution utility companies that requires them to develop plans to decouple their rates/revenues from sales volumes. This action is intended to encourage utility companies to help their customers reduce energy consumption. Decoupling of rates will allow utility companies to carry out the mandates of the GCA and at the same time collect the adequate level of revenues to maintain the quality and reliability of electric and gas services. This order allows companies to file for recovery of lost base revenues caused by incremental energy efficiency spending until their decoupling rate plans are approved. Once decoupled rate plans are approved, revenues will be set at a level designed to recover the utility companies’ incurred costs plus a return on their investment. This revenue level will be reconciled with actual revenues received from decoupled rates on an annual basis and any over or under collection will be refunded to or recovered from customers in the subsequent year. NSTAR Electric and NSTAR Gas have not yet applied for decoupled rate structures. NSTAR Electric currently does not expect to file for fully decoupled electric rates until after the Rate Settlement Agreement expires in 2012. However, NSTAR Gas may file prior to that date.

Sources and Availability of Electric Power Supply

For Basic Service power supply, NSTAR Electric makes periodic market solicitations consistent with DPU regulations. NSTAR Electric enters into short-term power purchase agreements to meet its Basic Service supply obligation, ranging in term from three to twelve months. NSTAR Electric fully recovers its payments to suppliers through DPU-approved rates billed to customers.

The New England Forward Capacity Market (FCM) includes a locational price mechanism to establish separate zones for capacity when transmission constraints are found to exist. FCM allows load-serving entities such as NSTAR Electric to self-supply through contracted resources to meet its capacity obligations without participating in the Forward Capacity Auctions (FCAs). FCAs are auctions designed to procure capacity three or more years into the future with a one-year to five-year commitment period. FCM will begin on June 1, 2010. To date, three FCM auctions have taken place covering the 2010-2011, 2011-2012, and 2012-2013 time periods. NSTAR Electric expects these costs to be fully recoverable.

Market and Transmission Regulation

NSTAR Electric and most other New England electric utilities, generation owners, and marketers are parties to a series of agreements that provide for coordinated planning and operation of the region’s generation and transmission facilities and the rules by which they participate in the wholesale markets and acquire transmission services. Under these arrangements, ISO-New England, a non-profit corporation whose board of directors and staff are independent from all market participants, serves as the regional Transmission Operator (RTO) of the New England Transmission System. ISO-New England works to ensure the reliability of the system, administers the independent system operator tariff subject to FERC approval, oversees the efficient and competitive functioning of the regional wholesale power market and determines which costs of NSTAR’s major transmission facilities are regionalized throughout New England. NSTAR Electric is a New England Transmission Owner subject to FERC regulation and is a member of ISO-New England. Refer to the “FERC Transmission ROE” section of the accompanying Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” for more details.

Transmission Rates

Transmission revenues are based on formula rates that are approved by the FERC. Tariffs are set by FERC and primarily include the Regional Network Service (RNS) and Local Network Service (LNS) rate schedules. The RNS rate, administered by ISO-NE and billed to all New England transmission owners, is reset on June 1 of each year and recovers the revenue requirements associated with transmission facilities that benefit the New England

7

Table of Contents

region. The LNS rate, which NSTAR Electric administers, is reset annually and recovers the revenue requirements for local transmission facilities. The LNS rate calculation recovers total transmission revenue requirements net of revenues received from other sources, thereby ensuring that NSTAR Electric recovers all regional and local revenue requirements as prescribed in the tariffs.

Transmission Capital Improvements

NSTAR Electric continues to evaluate needs for transmission improvements throughout the NSTAR service area. ISO-New England transmission project upgrades maintain transmission system reliability, improve the economic performance of the system, and are fully coordinated with other power regions. Over the next five to ten years, ISO-New England transmission projects are expected to enhance the region’s ability to support a robust, competitive wholesale power market by reliably moving power from various internal and external sources to the region’s load centers.

Additional transmission plans have been developed to further reduce the dependence on certain generating units needed for reliability and the exposure to special load-shedding contingency procedures. At various times, generating units in New England have been in “must-run” situations to maintain area reliability. Transmission improvements placed in-service have reduced costs associated with Reliability Must Run Agreements and second-contingency and voltage-control payments.

The lower Southeastern Massachusetts (SEMA) Projects are examples in which transmission improvements have contributed to the reduction of energy supply costs; further improvements in lower SEMA will significantly reduce the need to commit generation for second-contingency protection. NSTAR Electric’s future lower SEMA Project consists of an expansion and upgrade of existing lines, equipment and substations, and construction of a new 22 mile, 345kV transmission line that will cross the Cape Cod Canal. The project is expected to be in-service in late 2012.

NSTAR Gas

NSTAR Gas distributes natural gas to approximately 300,000 customers in 51 communities in central and eastern Massachusetts covering 1,067 square miles and having an aggregate population of 1.2 million. Twenty-five of these communities are also served with electricity by NSTAR Electric. Some of the larger communities served by NSTAR Gas include the Hyde Park area of Boston, Cambridge, Dedham, Framingham, New Bedford, Plymouth, Somerville, and Worcester.

NSTAR Gas’ operating revenues and sales percentages by customer class for the years 2009, 2008, and 2007, consisted of the following:

| Revenues ($) | Retail Gas Sales (therms) | |||||||||||||||||

| 2009 | 2008 | 2007 | 2009 | 2008 | 2007 | |||||||||||||

| Gas Sales and Transportation: |

||||||||||||||||||

| Residential |

62 | % | 59 | % | 60 | % | 43 | % | 43 | % | 44 | % | ||||||

| Commercial and Industrial |

28 | % | 27 | % | 28 | % | 44 | % | 46 | % | 43 | % | ||||||

| Other |

5 | % | 4 | % | 4 | % | 6 | % | 6 | % | 6 | % | ||||||

| Off-System and Contract sales |

5 | % | 10 | % | 8 | % | 7 | % | 5 | % | 7 | % | ||||||

Gas Rates

NSTAR Gas generates revenues primarily through the sale and/or transportation of natural gas. Gas sales and transportation services are divided into two categories: firm, whereby NSTAR Gas must supply gas and/or transportation services to customers on demand; and interruptible, whereby NSTAR Gas may, generally during colder months, temporarily discontinue service to high volume commercial and industrial customers. Sales and transportation of gas to interruptible customers have no impact on NSTAR Gas’ operating income because a substantial portion of the margin for such service is returned to its firm customers as rate reductions.

8

Table of Contents

Retail gas delivery and supply rates are established by the DPU and are comprised of:

| • | a distribution charge consists of a fixed customer charge and a demand and/or energy charge that collects the costs of building and expanding the gas infrastructure to deliver gas supply to its customers’ destination. This also includes collection of ongoing operating costs; |

| • | a seasonal cost of gas adjustment clause (CGAC) represents the collection of gas supply costs, pipeline and storage capacity, costs related to charge-offs of uncollected energy costs and working capital related costs. The CGAC is reset every six months. In addition, NSTAR Gas is required to file interim changes to its CGAC factor when the actual costs of gas supply vary from projections by more than 5%; and |

| • | a local distribution adjustment clause (LDAC) primarily represents the collection of demand-side management costs, environmental costs, PAM related costs, and costs associated with the residential assistance adjustment clause. The LDAC is reset annually and provides for the recovery of certain costs applicable to both sales and transportation customers. |

NSTAR Gas purchases financial contracts based on NYMEX natural gas futures in order to reduce cash flow variability associated with the purchase price for approximately one-third of its natural gas purchases. This practice attempts to minimize the impact of fluctuations in prices to NSTAR’s firm gas customers. These financial contracts do not procure gas supply. All costs incurred or benefits realized when these contracts are settled are included in the CGAC.

Gas Supply, Transportation and Storage

NSTAR Gas maintains a flexible resource portfolio consisting of natural gas supply contracts, transportation contracts on interstate pipelines, market area storage and peaking services.

NSTAR Gas purchases transportation, storage, and balancing services from Tennessee Gas Pipeline Company and Algonquin Gas Transmission Company, as well as other upstream pipelines that bring gas from major producing regions in the U.S., Gulf of Mexico, and Canada to the final delivery points in the NSTAR Gas service area. NSTAR Gas purchases all of its natural gas supply from third-party vendors. Most of the flowing supplies are purchased under a firm portfolio management contract with a term of one year, which has a maximum quantity of 139,606 MMBtu/day. NSTAR Gas has one multiple year contract, which is used for the purchase of its 4,500 MMbtu/day of Canadian supplies.

In addition to the firm transportation and natural gas supplies mentioned above, NSTAR Gas utilizes contracts for underground storage and LNG facilities to meet its winter peaking demands. The LNG facilities, described below, are located within NSTAR Gas’ distribution system and are used to liquefy and store pipeline gas during the warmer months for vaporization and use during the heating season. During the summer injection season, excess pipeline capacity and supplies are used to deliver and store natural gas in market area underground storage facilities located in the New York and Pennsylvania region. Stored natural gas is withdrawn during the winter season to supplement flowing pipeline supplies in order to meet firm heating demand. NSTAR Gas has firm underground storage contracts and total storage capacity entitlements of approximately 9.3 Bcf.

A portion of the storage of natural gas supply for NSTAR Gas during the winter heating season is provided by Hopkinton, a wholly-owned subsidiary of NSTAR. The facilities consist of an LNG liquefaction and vaporization plant and three above-ground cryogenic storage tanks having an aggregate capacity of 3.5 Bcf of liquefied natural gas.

Based on information currently available regarding projected growth in demand and estimates of availability of future supplies of pipeline natural gas, NSTAR Gas believes that its present sources of natural gas supply are adequate to meet existing load and allow for future growth in sales.

9

Table of Contents

Franchises

Through their charters, which are unlimited in time, NSTAR Electric and NSTAR Gas have the right to engage in the business of delivering and selling electricity and natural gas within their respective service territories, and have powers incidental thereto and are entitled to all the rights and privileges of and subject to the duties imposed upon electric and natural gas companies under Massachusetts laws. The locations in public ways for electric transmission and distribution lines and gas distribution pipelines are obtained from municipal and other state authorities who, in granting these locations, act as agents for the state. In some cases the actions of these authorities are subject to appeal to the DPU. The rights to these locations are not limited in time and are subject to the action of these authorities and the legislature. Under Massachusetts law, no other entity may provide electric or gas delivery service to retail customers within NSTAR’s service territory without the written consent of NSTAR Electric and/or NSTAR Gas. This consent must be filed with the DPU and the municipality so affected.

Unregulated Operations

NSTAR’s unregulated operations include telecommunications and liquefied natural gas service. Telecommunications services are provided through NSTAR Com, which installs, owns, operates, and maintains a wholesale transport network for other telecommunications service providers in the metropolitan Boston area to deliver voice, video, data, and internet services to customers. Revenues earned from NSTAR’s unregulated operations accounted for less than 1% of consolidated operating revenues in 2009, 2008, and 2007.

Discontinued Operations

On December 21, 2009, NSTAR announced an agreement to sell its wholly-owned subsidiary, MATEP. MATEP provides chilled water, steam, and electricity under long-term contracts to several hospitals, medical research and biotechnology centers, and teaching institutions located in Boston’s Longwood Medical Area. Revenues earned by MATEP represented approximately 3% of total consolidated revenues in 2009, 2008, and 2007. Refer to Note B, “Discontinued Operations,” of the accompanying Notes to Consolidated Financial Statements in Item 8, “Financial Statements and Supplementary Data” of this Form 10-K.

Regulation

The Energy Policy Act of 2005 established the Public Utility Holding Company Act of 2005 (PUHCA 2005) that transferred certain regulatory oversight from the SEC to the FERC. NSTAR has been granted an exemption and waiver from certain provisions of PUHCA 2005.

NSTAR Gas, NSTAR Electric and NSTAR Electric’s wholly-owned regulated subsidiary, Harbor Electric Energy Company, operate primarily under the authority of the DPU, whose jurisdiction includes supervision over retail rates for distribution of electricity, natural gas, and financing and investing activities. In addition, the FERC has jurisdiction over various phases of NSTAR Electric and NSTAR Gas utility businesses, conditions under which natural gas is sold at wholesale, facilities used for the transmission or sale of that energy, certain issuances of short-term debt, and regulation of accounting.

These companies are also subject to various other state and municipal regulations with respect to environmental, employment, and general operating matters.

10

Table of Contents

Plant Expenditures and Financings

The most recent estimates of plant expenditures and long-term debt maturities for 2010 and the years 2011-2014 are as follows:

| (in millions) |

2010 | 2011-2014 | ||||

| Plant expenditures: |

||||||

| Electric |

$ | 317 | $ | 1,130 | ||

| Gas |

53 | 170 | ||||

| $ | 370 | $ | 1,300 | |||

| Long-term debt |

$ | 684 | $ | 935 | ||

In the five-year period 2010 through 2014, plant expenditures are forecasted to be used for system reliability and performance improvements, customers service enhancements, and capacity expansion in NSTAR’s service territory. Of the $317 million planned electric expenditures for 2010, approximately $90 million is for transmission system improvements. The amounts stated above exclude expenditures for NSTAR’s proposed transmission investment with Northeast Utilities and Hydro-Quebec as these costs will be incurred by an entity that will be created to hold those assets (further discussed in the “Proposed Transmission Investment” Section in Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations).

Management continuously reviews its capital expenditure and financing programs. These programs and, therefore, the estimates included in this Form 10-K are subject to revision due to changes in regulatory requirements, operating requirements, environmental standards, availability and cost of capital, interest rates and other assumptions. Refer to the accompanying “Cautionary Statement Regarding Forward-Looking Information” preceding Item 1, “Business” and the “Liquidity, Commitments and Capital Resources” section of Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Seasonal Nature of Business

NSTAR Electric’s kilowatt-hour sales and revenues are typically higher in the winter and summer than in the spring and fall as sales tend to vary with weather conditions. NSTAR Gas’ sales are positively impacted by colder weather because a substantial portion of its customer base uses natural gas for space heating purposes. Refer to the accompanying “Selected Quarterly Consolidated Financial Data” section in Item 6, “Selected Consolidated Financial Data” for specific financial information by quarter for 2009 and 2008.

Competitive Conditions

As a rate regulated distribution and transmission utility company, NSTAR is not subject to a significantly competitive business environment. NSTAR Electric and NSTAR Gas have the exclusive right and privilege to engage in the business of delivering energy services within their granted territory. Under Massachusetts law, no other entity may provide electric or natural gas delivery service to retail customers within NSTAR’s service territory without the written consent of NSTAR Electric and/or NSTAR Gas. Refer to the accompanying “Franchises” section of this Item 1 and to Item 1A, “Risk Factors” for a further discussion of NSTAR’s rights and competitive pressures within its service territory.

Environmental Matters

NSTAR’s subsidiaries are subject to numerous federal, state and local standards with respect to the management of wastes and other environmental considerations. NSTAR subsidiaries face possible liabilities as a result of involvement in several multi-party disposal sites, state-regulated sites or third party claims associated with contamination remediation. NSTAR generally expects to have only a small percentage of the total potential

11

Table of Contents

liability for the majority of these sites. Noncompliance with certain standards can, in some cases, also result in the imposition of monetary civil penalties. Refer to the accompanying “Contingencies -Environmental Matters” section in Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and to Notes to Consolidated Financial Statements, Note O, “Commitments and Contingencies,” for more information.

Management believes that its facilities are in substantial compliance with currently applicable statutory and regulatory environmental requirements.

Number of Employees and Employee Relations

Excluding its discontinued operations subsidiary, MATEP, at December 31, 2009, NSTAR has approximately 3,000 employees, including approximately 2,100 who are represented by two labor unions covered by separate collective bargaining contracts.

Substantially all management, engineering, finance and support services are provided to the operating subsidiaries of NSTAR by NSTAR Electric & Gas. NSTAR has the following labor union contracts:

| Union |

Percent of Union to Total NSTAR Employees |

Supports | Contract Expiration Date | |||

| Local 369 of the Utility Workers of America (AFL-CIO) |

61% | Utility Operations | June 1, 2012 | |||

| Local 12004 of the United Steelworkers of America |

8% | Utility Operations | March 31, 2010 |

Management is currently in negotiations with Local 12004 regarding a new contract. Management believes it has satisfactory relations with its employees.

On December 21, 2009, NSTAR announced an agreement to sell its wholly-owned subsidiary, MATEP. MATEP has approximately 85 employees of whom 59 are represented by Local 877 of the International Union of Operating Engineers (AFL-CIO).

(d) Financial Information about Geographic Areas

NSTAR is a holding company engaged through its subsidiaries in the energy delivery business in Massachusetts. None of NSTAR’s subsidiaries have any foreign operations or export sales.

(e) Available Information

NSTAR files its Forms 10-K, 10-Q, and 8-K reports, proxy statements, and other information with the SEC. You may access materials free of charge NSTAR has filed with the SEC on NSTAR’s website at: www.nstar.com: Select “Investor Relations” and “Financial Information” or on the SEC’s website at www.sec.gov. Copies of NSTAR’s SEC filings may also be obtained free of charge by writing to NSTAR’s Investor Relations Department at the address on the cover of this Form 10-K or by calling 781-441-8338.

In addition, NSTAR’s Board of Trustees has several committees, including an Audit, Finance and Risk Management Committee, an Executive Personnel Committee and a Board Governance and Nominating Committee. The Board of Trustees also has a standing Executive Committee. The Board of Trustees has adopted the NSTAR Board of Trustees Guidelines on Significant Corporate Governance Issues, a Code of Ethics for the Principal Executive Officer, General Counsel, and Senior Financial Officers pursuant to Section 406 of the Sarbanes-Oxley Act of 2002, and a Code of Ethics and Business Conduct for Trustees, Officers and Employees

12

Table of Contents

(“Code of Conduct”). NSTAR intends to disclose any amendment to, and any waiver from, a provision of the Code of Ethics that applies to the Chief Executive Officer or Chief Financial Officer or any other executive officer and that relates to any element of the Code of Ethics definition enumerated in Item 406(b) of Regulation S-K, in a press release, on our website or on Form 8-K, within four business days following the date of such amendment or waiver. NSTAR’s Corporate Governance documents, including charters, guidelines and codes, and any amendments to such charters, guidelines and codes that are applicable to NSTAR’s executive officers, senior financial officers or trustees can be accessed free of charge on NSTAR’s website at: www.nstar.com: Select “Investor Relations” and “Company Information.”

The certifications of NSTAR’s Chief Executive Officer and Chief Financial Officer pursuant to Sections 302 and 906 of the Sarbanes-Oxley Act of 2002 are attached to this Annual Report on Form 10-K as Exhibits 31.1, 31.2, 32.1, and 32.2.

| Item 1A. | Risk Factors |

Our future performance is subject to a variety of risks, including those described below. If any of the following risks actually occur, our business could be harmed and the market price of our common shares could decline. In addition to the other information in this Annual Report on Form 10-K, shareholders or prospective investors should carefully consider the following risk factors.

Our electric and gas operations are highly regulated, and any adverse regulatory changes could have a significant impact on the Company’s results of operations and its financial position.

NSTAR’s electric and gas operations, including the rates charged, are regulated by the FERC and the DPU. In addition, NSTAR’s accounting policies are prescribed by GAAP, the FERC, and the DPU. Adverse regulatory changes could have a significant impact on the Company’s results of operations and its financial condition.

Potential municipalization or technological developments may adversely affect our regulated electricity and natural gas businesses.

Under Massachusetts law, no other entity may provide electric or gas delivery service to retail customers within NSTAR’s service territory without the written consent of NSTAR Electric and/or NSTAR Gas. Although not a trend, NSTAR’s operating utility companies could be exposed to municipalization risk, whereby a municipality could acquire the electric or natural gas delivery assets located in that city or town and take over the customer delivery service, thereby reducing NSTAR’s revenues. Any such action would require numerous legal and regulatory consents and approvals. Municipalization would require that NSTAR be compensated for its assets assumed. In addition, there is also the risk that technological developments could lead to distributed generation among NSTAR’s customer base reducing such customers’ use of NSTAR’s utility system.

Changes in environmental laws and regulations affecting our business could increase our costs or curtail our activities.

NSTAR and its subsidiaries are subject to a number of environmental laws and regulations that are currently in effect, including those related to the handling, disposal, and treatment of hazardous materials. Changes in compliance requirements or the interpretation by governmental authorities of existing requirements may impose additional costs, all of which could have an adverse impact on NSTAR’s results of operations.

The Company may be required to conduct environmental remediation activities for power generating sites and other potentially unidentified sites.

NSTAR is subject to actual or potential claims and lawsuits involving environmental remediation activities for power generating sites previously owned and other potentially unidentified sites. NSTAR divested all of its regulated generating assets under terms that generally require the buyer to assume all responsibility

for past and present environmental harm. Based on NSTAR’s current assessment of its environmental

13

Table of Contents

responsibilities, existing legal requirements and regulatory policies, NSTAR does not believe that its known environmental remediation responsibilities will have a material adverse effect on NSTAR’s results of operations, cash flows or financial position. However, discovery of currently unknown conditions at existing sites, identification of additional waste sites or changes in environmental regulation, could have a material adverse impact on NSTAR’s results of operations, cash flows or financial position.

NSTAR is subject to operational risk that could cause us to incur substantial costs and liabilities.

Our business, which involves the transmission and distribution of natural gas and electricity that is used as an energy source by our customers, is subject to various operational risks, including incidents that expose the Company to potential claims for property damages or personal injuries beyond the scope of NSTAR’s insurance coverage, and equipment failures that could result in performance below assumed levels. For example, operational performance below established target benchmark levels could cause NSTAR to incur penalties imposed by the DPU, up to a maximum of two and one-half percent of transmission and distribution revenues, under applicable Service Quality Indicators.

Increases in interest rates due to financial market conditions or changes in our credit ratings, could have an adverse impact on our access to capital markets at favorable rates, or at all, and could otherwise increase our costs of doing business.

NSTAR frequently accesses the capital markets to finance its working capital requirements, capital expenditures and to meet its long-term debt maturity obligations. Increased interest rates, or adverse changes in our credit ratings or further deterioration in the credit markets, would increase our cost of borrowing and other costs that could have an adverse impact on our results of operations and cash flows and ultimately have an adverse impact on the market price of our common shares. In addition, an adverse change in our credit ratings could increase borrowing costs, trigger requirements that we obtain additional security for performance, such as a letter of credit, related to our energy procurement agreements. Refer to the accompanying Item 7A, “Quantitative and Qualitative Disclosures About Market Risk,” for a further discussion.

Our electric and gas businesses are sensitive to variations in weather and have seasonal variations. In addition, severe storm-related disasters could adversely affect the Company.

Sales of electricity and natural gas to residential and commercial customers are influenced by temperature fluctuations. Significant fluctuations in heating or cooling degree days could have a material impact on energy sales for any given period. In addition, extremely severe storms, such as hurricanes and ice storms, could cause damage to our facilities that may require additional costs to repair and have a material adverse impact on the Company’s results of operations, cash flows or financial position. To the extent possible, NSTAR’s rate regulated subsidiaries would seek recovery of these costs through the regulatory process.

An economic downturn, increased costs of energy supply, and customers’ conservation efforts could adversely affect energy consumption and could adversely affect our results of operations.

Energy consumption is significantly impacted by the general level of economic activity and cost of energy supply. Economic downturns or periods of high energy supply costs typically lead to reductions in energy consumption and increased conservation measures. These conditions could adversely impact the level of energy sales and result in less demand for energy delivery. A recession or a prolonged lag of a subsequent recovery could have an adverse effect on NSTAR’s results of operations, cash flows or financial position.

The ability of NSTAR to maintain future cash dividends at the level currently paid to shareholders is dependent upon the ability of its subsidiaries to pay dividends to NSTAR.

As a holding company, NSTAR does not have any operating activity and therefore is substantially dependent on dividends from its subsidiaries and from external borrowings at variable rates of interest to provide the cash

14

Table of Contents

necessary for repayment of debt obligations, to pay administrative costs, to meet contractual obligations that may not be met by our subsidiaries and to pay common share dividends to NSTAR’s shareholders. Regulatory and other legal restrictions may limit our ability to transfer funds freely, either to or from our subsidiaries. These laws and regulations may hinder our ability to access funds that we may need to make payments on our obligations. As the Holding company’s sources of cash are limited to dividends from its subsidiaries and external borrowings, the ability to maintain future cash dividends at the level currently paid to shareholders will be dependent upon cash flows of NSTAR’s subsidiaries.

NSTAR’s subsidiaries do have certain limitations that could impact the payment of dividends to the Holding company. Refer to the “Sources of Additional Capital and Financial Covenant Requirements” section of the accompanying Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” for more information.

Our electric and gas operations may be impacted if generation supply or its transportation or transmission availability is limited or unreliable.

Our electric and natural gas delivery businesses are reliant on transportation and transmission facilities that we do not own or control. Our ability to provide energy delivery services depends on the operations and facilities of third parties, including the independent system operator, electric generators that supply our customers’ energy requirements and natural gas pipeline operators from which we receive delivery of our natural gas supply. Should our ability to receive electric or natural gas supply be disrupted due either to operational issues or to inadequacy of transmission capacity, it could impact our ability to serve our customers. It could also force us to secure alternative supply at significantly higher costs.

Financial market performance and other changes may decrease the Company’s pension and postretirement benefit plans’ assets and could require additional funding beyond historic levels.

A sustained decline in the global financial markets may have a material adverse effect on the value of our pension and postretirement benefit plans’ assets. This situation may increase our benefit plans’ funding requirements.

| Item 1B. | Unresolved Staff Comments |

None

| Item 2. | Properties |

NSTAR Electric properties include an integrated system of transmission and distribution lines and substations, an interest in a jointly owned administration office building and other structures such as garages and service centers that are located in eastern Massachusetts. NSTAR’s high-voltage transmission lines are generally located on land either owned or subject to perpetual and exclusive easements in its favor. Its low-voltage distribution lines are located principally on public property under permits granted by municipal and other state authorities.

At December 31, 2009, NSTAR Electric’s primary and secondary transmission and distribution system consisted of approximately 21,980 circuit miles of overhead lines, approximately 13,020 circuit miles of underground lines, 256 substation facilities and approximately 1,173,500 active customer meters.

NSTAR Gas’ principal natural gas properties consist of distribution mains, services and meters necessary to maintain reliable service to customers. In addition, it shares an interest in a jointly owned administration office and service building, three district office buildings and owns several natural gas receiving and take stations. As of December 31, 2009, the gas system included approximately 3,130 miles of gas distribution lines, approximately 188,800 services and approximately 277,900 customer meters together with the necessary

15

Table of Contents

measuring and regulating equipment. In addition, Hopkinton owns a liquefaction and vaporization plant, a satellite vaporization plant and above ground cryogenic storage tanks having an aggregate storage capacity equivalent to 3.5 Bcf of natural gas.

NSTAR Com owns approximately 240 miles of fiber optic network that represents approximately 79,000 fiber miles of network.

Assets of discontinued operations held for sale primarily consist of district energy operations, a cogeneration facility located in the Longwood Medical Area of Boston. MATEP provides steam, chilled water and electricity to over 9 million square feet of medical and teaching facilities. NSTAR anticipates the final sale of MATEP towards the end of the first quarter or early second quarter of 2010.

| Item 3. | Legal Proceedings |

In the normal course of its business, NSTAR and its subsidiaries are involved in certain legal matters, including civil litigation. Management is unable to fully determine a range of reasonably possible court-ordered damages, settlement amounts, and related litigation costs (legal liabilities) that would be in excess of amounts accrued and amounts covered by insurance. Based on the information currently available, NSTAR does not believe that it is probable that any such legal liabilities will have a material impact on its consolidated financial position. However, it is reasonably possible that additional legal liabilities that may result from changes in circumstances could have a material impact on its results of operations, financial condition and cash flows.

| Item 4. | Submission of Matters to a Vote of Security Holders |

There were no matters submitted to a vote of security holders during the fourth quarter of 2009.

| Item 4A. | Executive Officers of Registrant |

Identification of Executive Officers

| Name of Officer |

Position and Business Experience |

Years in Current Position |

Years as an Officer |

Age at December 31, 2009 | ||||

| Thomas J. May |

Chairman, President and Chief Executive Officer and an NSTAR Trustee | 15 | 23 | 62 | ||||

| James J. Judge |

Senior Vice President and Chief Financial Officer | 14 | 14 | 53 | ||||

| Douglas S. Horan |

Senior Vice President - Strategy, Law and Policy, Secretary and General Counsel | 14 | 14 | 60 | ||||

| Joseph R. Nolan, Jr. |

Senior Vice President - Customer & Corporate Relations | 9 | 9 | 46 | ||||

| Werner J. Schweiger |

Senior Vice President - Operations | 8 | 8 | 50 | ||||

| Christine M. Carmody |

Senior Vice President - Human Resources Previously Vice President of Organizational Effectiveness for 2 years and Director, Learning and Performance for 3 years | 2 | 2 | 46 | ||||

| Robert J. Weafer, Jr. |

Vice President, Controller and Chief Accounting Officer | 21 | 21 | 62 | ||||

16

Table of Contents

PART II

| Item 5. | Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

(a) Market Information and (c) Dividends

The NSTAR Common Shares, $1 par value, are listed on the New York Stock Exchange under the symbol “NST.” NSTAR’s Common Shares closing market prices at December 31, 2009 and 2008 were $36.80 and $36.49 per share, respectively.

The NSTAR Common Shares high and low market prices per common share as reported by the New York Stock Exchange composite transaction reporting system and dividends declared per common share for each of the quarters in 2009 and 2008 were as follows:

| 2009 | 2008 | |||||||||||||||||

| Market Prices | Dividends Declared |

Market Prices | Dividends Declared | |||||||||||||||

| High | Low | High | Low | |||||||||||||||

| First quarter |

$ | 36.80 | $ | 27.49 | $ | 0.375 | $ | 36.70 | $ | 29.36 | $ | 0.350 | ||||||

| Second quarter |

$ | 34.68 | $ | 28.54 | $ | 0.375 | $ | 35.36 | $ | 30.41 | $ | 0.350 | ||||||

| Third quarter |

$ | 32.91 | $ | 30.10 | $ | 0.375 | $ | 40.00 | $ | 31.17 | $ | 0.350 | ||||||

| Fourth quarter |

$ | 37.75 | $ | 30.76 | $ | 0.400 | $ | 36.94 | $ | 25.67 | $ | 0.375 | ||||||

NSTAR paid common share dividends to shareholders of $160.2 million and $149.5 million in 2009 and 2008, respectively.

(b) Holders

As of December 31, 2009, there were 19,566 registered holders of NSTAR Common Shares.

(d) Securities authorized for issuance under equity compensation plans

The following table provides information about NSTAR’s equity compensation plans as of December 31, 2009.

| Plan Category |

Number of securities to be issued upon exercise of outstanding options, warrants and rights |

Weighted average exercise price of outstanding options, warrants and rights |

Number of securities remaining available for future issuance under equity compensation plans | ||||||

| Equity compensation plans approved by shareholders |

2,855,535 | (1) | $ | 29.63 | (2) | 1,928,263 | |||

| Equity compensation plans not approved by shareholders |

N/A | N/A | N/A | ||||||

| Total |

2,855,535 | $ | 29.63 | 1,928,263 | |||||

| (1) | Includes 2,454,367 common shares to be issued upon the exercise of options and 401,168 common shares for distribution of deferred shares and performance units pursuant to the terms of our Incentive Plan |

| (2) | The weighted-average exercise price in Column (b) does not take into account deferred shares or performance units, which have no exercise price. |

17

Table of Contents

The NSTAR 2007 Long Term Incentive Plan (the 2007 Plan) permits a variety of stock and stock-based awards, including stock options, deferred stock awards, and performance share units granted to key employees. The aggregate number of common shares that are available for award under the 2007 Plan is 3.5 million. The Plan limits the terms of awards to ten years and prohibits the granting of awards beyond ten years after its effective date. In general, stock options and stock awards vest over a three-year period from date of grants. The Executive Personnel Committee (EPC) of the Board of Trustees approves stock-based awards for all executives and other key employees. However, the Chief Executive Officer’s (CEO) award must also be approved by the independent members of the Board of Trustees. The EPC and Board of Trustees established that the date of grant for annual stock-based awards under the Plan is the date each year on which the Board of Trustees approves the CEO’s stock award. This date is when all participants are notified of their awards. Options are granted at the full market price of the common shares on the date of grant.

(e) Purchases of equity securities

Common Shares of NSTAR issued under the NSTAR Dividend Reinvestment and Direct Common Shares Purchase Plan, the Long Term Incentive Plan and the NSTAR Savings Plan may consist of newly issued shares from the Company or shares purchased in the open market by the Company or an independent agent. During the three-month period ended December 31, 2009, the shares listed below were acquired in the open market.

| Total Number of Common Shares Purchased |

Average Price Paid Per Share | ||||

| October |

114,429 | $ | 31.36 | ||

| November |

128,765 | $ | 31.20 | ||

| December |

31,014 | $ | 35.86 | ||

| Total Fourth Quarter |

274,208 | $ | 31.79 | ||

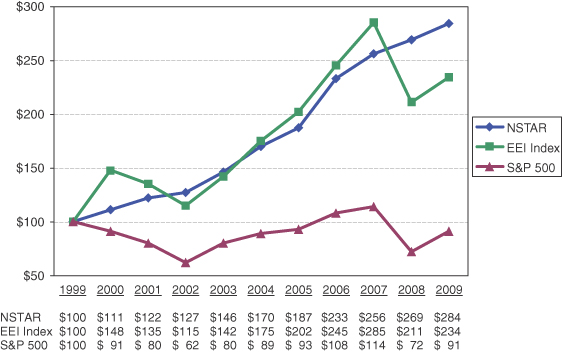

(f) Stock Performance Graphs

The following Stock Performance Graphs and related information shall not be deemed “soliciting material” or “as filed” with the SEC, nor shall such information be incorporated by reference into any future filing under the Securities Act of 1933 or Securities Exchange Act of 1934, each as amended, except to the extent that the Company specifically incorporates it by reference into such filing.

18

Table of Contents

The stock performance graph presentations set forth below compare cumulative five-year and ten-year shareholder returns with the Standard & Poor’s 500 Index (S&P 500) and the Edison Electric Institute Index (EEI Index), a recognized industry index of 58 investor-owned utility companies. Pursuant to the SEC’s regulations, the graphs below depict the investment of $100 at the commencement of the measurement periods, with dividends reinvested.

Five-Year Performance Graph

Ten-Year Performance Graph

19

Table of Contents

| Item 6. | Selected Consolidated Financial Data |

The following table summarizes five years of selected consolidated financial data.

| (in thousands, except per share data) |

2009 | 2008 | 2007 | 2006 | 2005 | ||||||||||

| Operating revenues (a) |

$ | 3,050,044 | $ | 3,208,321 | $ | 3,136,085 | $ | 3,441,505 | $ | 3,135,219 | |||||

| Net income: from continuing operations (b) |

$ | 244,015 | $ | 225,996 | $ | 213,056 | $ | 191,917 | $ | 192,209 | |||||

| Net income: from discontinued operations |

$ | 9,233 | $ | 11,551 | $ | 8,459 | $ | 14,857 | $ | 3,926 | |||||

| Net income: attributable to common shareholders |

$ | 253,248 | $ | 237,547 | $ | 221,515 | $ | 206,774 | $ | 196,135 | |||||

| Per common share: |

|||||||||||||||

| Basic earnings - |

|||||||||||||||

| Continuing operations |

$ | 2.28 | $ | 2.11 | $ | 1.99 | $ | 1.80 | $ | 1.80 | |||||

| Discontinued operations |

0.09 | 0.11 | 0.08 | 0.14 | 0.04 | ||||||||||

| Total earnings |

$ | 2.37 | $ | 2.22 | $ | 2.07 | $ | 1.94 | $ | 1.84 | |||||

| Diluted earnings - |

|||||||||||||||

| Continuing operations |

$ | 2.28 | $ | 2.11 | $ | 1.99 | $ | 1.79 | $ | 1.79 | |||||

| Discontinued operations |

0.09 | 0.11 | 0.08 | 0.14 | 0.04 | ||||||||||

| Total earnings |

$ | 2.37 | $ | 2.22 | $ | 2.07 | $ | 1.93 | $ | 1.83 | |||||

| Cash dividends declared (c) |

$ | 1.525 | $ | 1.425 | $ | 1.325 | $ | 1.535 | $ | 0.87 | |||||

| Assets from continuing operations |

$ | 7,976,929 | $ | 8,093,996 | $ | 7,588,570 | $ | 7,602,680 | $ | 7,480,285 | |||||

| Assets held for sale |

$ | 167,857 | $ | 175,493 | $ | 170,975 | $ | 166,715 | $ | 158,047 | |||||

| Long-term debt (a)(d) |

$ | 1,754,236 | $ | 1,928,708 | $ | 1,929,348 | $ | 1,631,474 | $ | 1,518,651 | |||||

| Transition property securitization (d) |

$ | 212,205 | $ | 331,209 | $ | 483,961 | $ | 637,217 | $ | 787,966 | |||||

| Preferred stock of subsidiary |

$ | 43,000 | $ | 43,000 | $ | 43,000 | $ | 43,000 | $ | 43,000 | |||||

| (a) | On December 21, 2009, NSTAR announced the sale of its wholly-owned subsidiary, MATEP. The assets of MATEP were considered to be held for sale as of December 21, 2009 and the subsidiary operations were classified as discontinued operations. Operating revenues and long-term debt amounts of MATEP have been excluded from the selected financial data presented. |

| (b) | Includes impact of preferred stock dividends of subsidiary to the noncontrolling interest |

| (c) | As a result of a change in NSTAR’s Board of Trustees’ meetings schedule in 2005, the fourth quarter dividend that typically would have been declared in December 2005, was approved on January 26, 2006 at $0.3025 per share, and therefore dividends declared during 2006 include the fourth quarter of 2005. The dividend payment schedule remained unchanged. |

| (d) | Excludes the current portion and debt obligation related to discontinued operations. |

Selected Quarterly Consolidated Financial Data (Unaudited) (a)

| (in thousands, except earnings per share) |

|||||||||||||||

| Operating Revenues (c) |

Operating Income (c) |

Net Income (d) |

Earnings Per Share (b) | ||||||||||||

| Basic | Diluted | ||||||||||||||

| 2009 |

|||||||||||||||

| First quarter |

$ | 908,638 | $ | 123,971 | $ | 61,036 | $ | 0.57 | $ | 0.57 | |||||

| Second quarter |

$ | 683,235 | $ | 114,495 | $ | 56,934 | $ | 0.53 | $ | 0.53 | |||||

| Third quarter |

$ | 745,626 | $ | 170,226 | $ | 87,638 | $ | 0.82 | $ | 0.82 | |||||

| Fourth quarter |

$ | 712,545 | $ | 107,410 | $ | 47,640 | $ | 0.45 | $ | 0.45 | |||||

| 2008 |

|||||||||||||||

| First quarter |

$ | 857,366 | $ | 122,081 | $ | 59,236 | $ | 0.55 | $ | 0.55 | |||||

| Second quarter |

$ | 711,774 | $ | 113,475 | $ | 50,369 | $ | 0.47 | $ | 0.47 | |||||

| Third quarter |

$ | 857,709 | $ | 170,949 | $ | 85,820 | $ | 0.80 | $ | 0.80 | |||||

| Fourth quarter |

$ | 781,472 | $ | 98,624 | $ | 42,122 | $ | 0.39 | $ | 0.39 | |||||

| (a) | This information has been provided in accordance with Regulation S-K, Item 302(a). |

| (b) | The sum of the quarters may not equal annual basic and diluted earnings per share due to rounding. |

20

Table of Contents

| (c) | On December 21, 2009, NSTAR announced an agreement to sell its wholly-owned subsidiary, MATEP. The results of operations of MATEP have been classified as discontinued operations as of December 31, 2009. Operating revenues and Operating income attributable to MATEP have been excluded from the selected data presented. |

| (d) | Net income attributable to common shareholders. |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations (MD&A) |

Overview

NSTAR (or the Company) is a holding company engaged through its subsidiaries in the energy delivery business serving approximately 1.4 million customers in Massachusetts, including approximately 1.1 million electric distribution customers in 81 communities and approximately 300,000 natural gas distribution customers in 51 communities. NSTAR’s retail electric transmission and distribution utility subsidiaries are NSTAR Electric and NSTAR Gas, respectively. Harbor Electric Energy Company, a wholly-owned subsidiary of NSTAR Electric, provides distribution service and ongoing support to its only customer, the Massachusetts Water Resources Authority. NSTAR’s nonutility, unregulated operations include telecommunications operations (NSTAR Com) and a liquefied natural gas service company (Hopkinton). Utility operations accounted for approximately 99% of consolidated operating revenues of continuing operations in 2009, 2008, and 2007.

NSTAR consolidates three wholly-owned special purpose subsidiaries, BEC Funding LLC, BEC Funding II, LLC and CEC Funding, LLC. These entities were created to complete the sale of electric rate reduction certificates to a special purpose trust created by two Massachusetts state agencies. These financing transactions securitized the costs incurred related to the divestiture of generation assets and long-term power contracts.

NSTAR derives its operating revenues primarily from the sale of energy, distribution, transmission, and energy efficiency services to customers. NSTAR’s earnings are impacted by fluctuations in unit sales of electric kWh and natural gas MMbtu, which have an effect on the level of distribution and transmission revenues recognized. In accordance with the regulatory rate structure in which NSTAR operates, its recovery of energy costs are fully reconciled with the level of energy revenues currently recorded and, therefore, do not have an impact on earnings. As a result of this rate structure, any variability in the cost of energy supply purchased will have an impact on purchased power and transmission and cost of gas sold expenses, but will not affect the Company’s net income as the Company recognizes a corresponding change in revenues.

Discontinued Operations

On December 21, 2009, NSTAR announced an agreement to sell its wholly-owned subsidiary, Medical Area Total Energy Plant, Inc. (MATEP). MATEP provides steam, chilled water service, and electricity under long-term contracts to several hospitals, medical research and biotechnology centers, and teaching institutions in the Longwood Medical Area of Boston. The sale is at a price of approximately $320 million in cash and is subject to certain federal and local regulatory approvals. The purchase price is subject to certain closing adjustments related to changes in working capital, interest, and other adjustments. In connection with the sale, NSTAR will retire MATEP’s debt.

MATEP’s principal asset is a cogeneration plant that produces electricity, steam and chilled water, and a distribution system that delivers these products to its customers. MATEP has approximately 85 employees.

The sale is expected to close towards the end of the first quarter or early part of the second quarter of 2010. Net proceeds from the transaction are anticipated to be used to reduce NSTAR’s capitalization.

Critical Accounting Policies and Estimates

NSTAR’s discussion and analysis of its financial condition, results of operations and cash flows are based on the accompanying Consolidated Financial Statements, which have been prepared in accordance with GAAP. The

21

Table of Contents

preparation of these Consolidated Financial Statements required management to make estimates and judgments that affect the reported amount of assets and liabilities, revenues and expenses, and related disclosure of contingent assets and liabilities at the date of the Consolidated Financial Statements. Actual results may differ from these estimates under different assumptions or conditions.

Critical accounting policies and estimates are defined as those that require significant judgment and uncertainties, and potentially may result in materially different outcomes under different assumptions and conditions. The accounting policies and estimates that are most critical to the reported results of operations, cash flows and financial position are described below.

a. Revenue Recognition

Electric and gas revenues are based on rates approved by the DPU and the FERC. Revenues related to the sale, transmission and distribution of energy delivery service are generally recorded when service is rendered or energy is delivered to customers. However, the determination of the sales to individual customers is based on systematic meter readings throughout a month. Meters that are not read during a given month are estimated and trued-up to actual use in a future period. At the end of each month, aggregate amounts of energy delivered to customers since the date of their last meter reading are estimated and the corresponding unbilled revenue is recorded. Unbilled electric revenue is estimated each month based on daily territory load (customer energy requirements), estimated line losses and applicable customer rates. Unbilled natural gas revenues are estimated based on estimated purchased gas volumes, estimated gas losses and applicable customer rates. Accrued unbilled revenues recorded in the accompanying Consolidated Balance Sheets as of December 31, 2009 and 2008 were $67 million and $62 million, respectively.

The level of revenues is subject to seasonal weather conditions. Electric sales volumes are typically higher in the winter and summer than in the spring or fall. Gas sales volumes are impacted by colder weather since a substantial portion of NSTAR Gas’ customer base uses natural gas for heating purposes. As a result, NSTAR records a higher level of revenue during the seasonal periods mentioned above.

NSTAR’s nonutility revenues are recognized when services are rendered. Revenues are based, for the most part, on long-term contractual rates.

b. Regulatory Accounting

NSTAR follows accounting policies prescribed by GAAP, the FERC, and the DPU. In addition, NSTAR and its subsidiaries are subject to the accounting and reporting requirements of the SEC. As rate-regulated companies, NSTAR’s utility subsidiaries are subject to the application of an accounting standard for rate-regulated entities, ASC 980, Regulated Operations, that considers the effects of regulation resulting from differences in the timing of their recognition of certain revenues and expenses from those of other businesses and industries. NSTAR’s distribution and transmission businesses are subject to rate-regulation that is based on cost recovery and meets the criteria for application of ASC 980. This ratemaking process results in the recording of regulatory assets or a regulatory liability (including cost of removal) based on the probability of current and future cash flows. Regulatory assets represent incurred or accrued costs that have been deferred because they are probable of future recovery from customers. Regulatory liabilities may represent collections from customers that have been deferred because they will be expended in the future or they may relate to the future cost of removal of assets. (Refer to the accompanying “Asset Retirement Obligations and Cost of Removal” section of Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”) As of December 31, 2009 and 2008, NSTAR has recorded regulatory assets of $2.6 billion and $2.9 billion, and regulatory liabilities of $270 million and $265 million, respectively. NSTAR continuously reviews these regulatory assets to assess their ultimate recoverability within the approved regulatory guidelines. NSTAR expects to fully recover these regulatory assets in its rates. If future recovery of any deferred costs ceases to be probable, NSTAR would be required to charge such deferred amounts to earnings. Impairment risk associated with these assets relates to potentially adverse legislative, judicial or regulatory actions in the future.

22

Table of Contents

c. Pension and Other Postretirement Benefits

NSTAR’s annual pension and other postretirement benefits costs are dependent upon several factors and assumptions, such as but not limited to, employee demographics, plan design, the level of cash contributions made to the plans, the discount rate, the expected long-term rate of return on the plans’ assets and health care cost trends.

Changes in pension and PBOP assets and liabilities associated with these factors are not immediately recognized as pension and PBOP costs in the statements of income, but generally are recognized in future years over the remaining average service period of the plans’ participants. However, these factors could have a significant impact on pension and postretirement assets or liabilities recognized.

NSTAR’s Pension Plan and PBOP Plan assets, which partially consist of equity investments, have been affected by recent trends in the overall global equity markets. Fluctuations in the fair value of the Pension Plan and PBOP Plan assets impact the funded status, accounting costs, and cash funding requirements of these Plans. The earnings impact of increased Pension and PBOP costs is substantially mitigated by NSTAR’s DPU-approved pension and PBOP rate adjustment mechanism. Under the PAM, NSTAR recovers its pension and PBOP expense through a reconciling rate mechanism. The PAM removes the volatility in earnings that could result from fluctuations in market conditions and plan experience.

There were no significant changes to NSTAR’s pension and PBOP benefits in 2009, 2008, and 2007. As further described in Note H, “Pension and Other Postretirement Benefits,” in the accompanying Notes to the Consolidated Financial Statements, NSTAR’s discount rate for the Pension Plan obligation was 5.85% and 6.25% at December 31, 2009 and 2008, respectively. NSTAR’s discount rate for the PBOP obligation was 6.00% and 6.10% at December 31, 2009 and 2008, respectively. These discount rates align with market conditions and the anticipated cash flow characteristics of NSTAR’s pension and PBOP obligations. The expected long-term rate of return on both pension plan and PBOP assets for 2009 remained at 9.0%, the same as 2008 and 2007. Changes in these assumptions have an impact on reported pension and PBOP costs and obligations.