Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - CAPSTEAD MORTGAGE CORP | d8k.htm |

CAPSTEAD INVESTOR PRESENTATION February 2, 2010 Exhibit 99.1 |

CAPSTEAD 2 Safe Harbor Statement - Private Securities Litigation Reform Act of 1995 Forward Looking Information This document contains “forward-looking statements” (within the meaning of the Private Securities Litigation Reform Act of 1995) that inherently involve risks and uncertainties. Capstead’s actual results and liquidity can differ materially from those anticipated in these forward-looking

statements because of changes in the level and composition of the

Company’s investments and other factors. As discussed in the

Company’s filings with the Securities and Exchange Commission, these factors may include, but are not limited to, changes in general economic conditions, the availability of suitable

qualifying investments from both an investment return and regulatory

perspective, the availability of new investment capital, the availability of

financing at reasonable levels and terms to support investing on a leveraged basis, fluctuations in interest rates and levels of mortgage prepayments, deterioration in

credit quality and ratings, the effectiveness of risk management strategies,

the impact of differing levels of leverage employed, liquidity of secondary

markets and credit markets, increases in costs and other general competitive

factors. In addition to the above considerations, actual results and liquidity related to investments in loans secured by commercial real estate are affected by borrower

performance under operating and/or development plans, lessee performance

under lease agreements, changes in general as well as local economic

conditions and real estate markets, increases in competition and inflationary pressures, changes in the tax and regulatory environment including zoning and

environmental laws, uninsured losses or losses in excess of insurance limits and the availability of adequate insurance coverage at reasonable costs, among other factors. |

CAPSTEAD 3 Agency-guaranteed residential mortgage securities are considered to have

little, if any, credit risk, particularly given recent federal government support

for Fannie Mae and Freddie Mac As a result, these investments are highly liquid and can be financed with multiple funding providers through standard repurchase arrangements Overview We manage a leveraged portfolio of residential adjustable-rate mortgage,

or ARM, securities issued and guaranteed by Fannie Mae, Freddie Mac or Ginnie Mae that reset to more current interest rates within a relatively short

period of time allowing for: • potential expansion of financing spreads during periods of falling interest rates, • potential recovery of financing spreads diminished during periods of rising interest rates, and • smaller fluctuations in portfolio values from changes in interest rates compared to investments in fixed-rate mortgage securities We are self-managed with low G&A costs and a conservative incentive structure Business Strategy Management Structure Capstead is a Real Estate Investment Trust formed in 1985, headquartered in Dallas,

Texas |

CAPSTEAD 4 Experienced Management Team Andrew F. Jacobs - President and Chief Executive Officer, Director – Has served in various executive positions with us since 1988 – Certified Public Accountant, member of the Board of Governors of the National Association of Real Estate Investment Trusts (“NAREIT”), the Executive Committee of the Chancellors

Council of the University of Texas System, the Executive Council of the

Real Estate Finance and Investment Center at the University of Texas at Austin, the American Institute of Certified Public Accountants (“AICPA”), the

Texas Society of Certified Public Accountants (“TSCPA”), the

National Association of Corporate Directors (“NACD”), and the Financial Executive International (“FEI”). Phillip A. Reinsch – Executive Vice President and Chief Financial Officer, Secretary – Has held various financial accounting and reporting positions with us since 1993

– Formerly employed by Ernst & Young LLP as an audit senior manager focusing on

mortgage banking and asset securitization – CPA, Member AICPA, TSCPA, FEI Robert A. Spears – Executive Vice President, Director of Residential Mortgage Investments – Has served in asset and liability management positions with us since 1994 – Formerly vice president of secondary marketing with NationsBanc Mortgage

Corporation Michael W. Brown – Senior Vice President, Asset and Liability Management, Treasurer – Has served in asset and liability management positions with us since 1994 – MBA, Southern Methodist University, Dallas, Texas Over 80 years of combined mortgage finance industry experience, 67 years at Capstead |

CAPSTEAD 5 Market Snapshot (in thousands, except percentages and per share amounts) Perpetual Preferred Trust Total Long-Term Common Series A Series B Preferred Investment Capital NYSE Stock Ticker CMO CMOPRA CMOPRB Shares outstanding (a) 69,319 188 15,819 Preferred dividend rate (annualized) $1.60 $1.26 Cost of preferred capital (annualized) 11.44% 11.28% 8.49% 10.28% Price as of January 27, 2010 $13.49 $21.72 $14.41 Book value per common share (a) $11.99 Price as a multiple of book value 113% Recorded value (a) $834,608 $2,630 $176,703 $99,978 $1,113,919 Market cap as of January 27, 2010 (b) $935,113 $4,083 $227,952 $99,978 $1,267,126 (a) As of December 31, 2009 (b) Excludes any shares issued subsequent to year-end.

|

CAPSTEAD 6 (a) See pages 15 and 16 for discussion of use of Core Earnings and Core Earnings per

diluted common share, non-GAAP financial measures. (b) See page 14 for

discussion of use of financing spread on mortgage assets, a non-GAAP financial measure. Fourth Quarter Highlights Core Earnings (a) of $43 million or $0.54 per diluted common share GAAP earnings of $3 million or a loss of $0.04 per diluted common share, after $40 million in charges which nearly eliminates exposure to commercial real estate loans Book value ended year at $11.99 per common share Portfolio increased to $8.1 billion Portfolio leverage ended year at 6.67 times long-term investment capital Total financing spreads averaged 2.21% while financing spreads on mortgage assets averaged 2.40 % (b) |

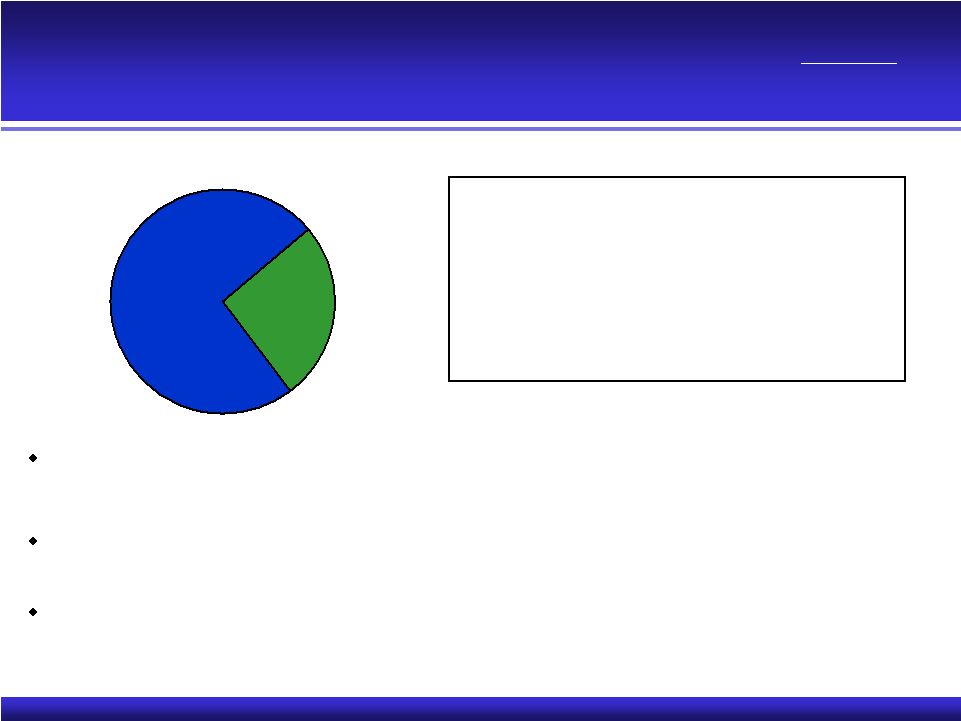

CAPSTEAD 7 Low Risk Agency-guaranteed Residential ARM Securities Investment Strategy Current-Reset ARMs ($6.14 billion) Longer-to-Reset ARMs ($1.74 billion) (investment basis as of December 31, 2009) Over 99% of the securities in our portfolio are backed by well-seasoned mortgage loans with coupon interest rates that reset at least annually or begin

doing so after an initial fixed-rate period of five years or less Capstead has long-term relationships with most of its 20 active lending counterparties and is constantly seeking to expand counterparty relationships The duration of our assets and liabilities was approximately 8½ months and 5¼ months, respectively, for a net duration gap of approximately 3¼ months 78% 22% Financed primarily with 30- to 90-day “repo” borrowings Interest rate risk mitigated on macro basis with two-year swap agreements ($2.8 billion at 1.83%, 13 month average maturity as of December 31, 2009) or longer-term repo, if available at attractive rates and terms |

CAPSTEAD 8 Financing Spreads Fed Funds vs. One-Month Libor Our portfolio is currently earning above market rates (3.59% during 4 Qtr vs. 2.71% on 4 Qtr purchases) – if current conditions persist, portfolio yields will drift lower as the underlying mortgages reset to more current rates and as new acquisitions are made Rates on our borrowings will continue declining in this environment as older,

higher-rate swap positions terminate and are replaced with a combination

of 30-day borrowings (currently at less than 25 bps) and new swap

positions (2-year swaps currently pricing in the 110’s) Under these

conditions, we anticipate that the impact on financing spreads from declining portfolio yields will be muted by declining borrowing rates Yields on Mortgage Assets vs. Borrowing Rates 0.0% 2.0% 4.0% 6.0% 8.0% Yields Borrowing Rate Financing spreads on mortgage assets* 4th Qtr 2009: 2.40% High:

3.71% Low:

(.16) Average:

1.56 0.00% 1.00% 2.00% 3.00% 4.00% 5.00% 6.00% 7.00% Fed Funds 1-Month LIBOR th th * See page 14 for discussion of use of financing spread on mortgage assets, a non-GAAP financial

measure. |

CAPSTEAD A P P E N D I X 9 |

CAPSTEAD 10 Comparative Balance Sheet (in thousands, except per share amounts) December 31, 2008 December 31, 2007 (unaudited) Assets Mortgage securities and similar investments 8,091,103 $ 7,499,249 $ 7,108,438 $ ($7.86 billion pledged under repurchase arrangements) Cash collateral receivable from interest rate swap counterparties 30,485 53,676 1,800 Interest rate swap agreements at fair value 1,758 - - Cash and cash equivalents 409,623 96,839 6,653 Receivables and other assets 92,817 76,481 88,918 Investments in unconsolidated affiliates 3,117 3,117 3,117 8,628,903 $ 7,729,362 $ 7,208,926 $ Liabilities Repurchase arrangements and similar borrowings 7,435,256 $ 6,751,500 $ 6,500,362 $ Unsecured borrowings 103,095 103,095 103,095 Interest rate swap agreements at fair value 9,218 46,679 2,384 Common stock dividend payable 37,432 22,728 9,786 Accounts payable and accrued expenses 29,961 44,910 32,382 7,614,962 6,968,912 6,648,009 Stockholders' Equity Perpetual preferred stock 179,333 179,460 179,533 Common stock 661,724 618,369 344,423 Accumulated other comprehensive income (loss) 172,884 (37,379) 36,961 1,013,941 760,450 560,917 8,628,903 $ 7,729,362 $ 7,208,926 $ Long-term investment capital unsecured borrowings, net of related investments in statutory trusts) (unaudited) $1,113,919 $860,428 $660,895 Portfolio leverage divided by long-term investment capital) (unaudited) 6.67:1 7.85:1 9.84:1 Book value per common share liquidation preferences for the Series A and B preferred stock) (unaudited) $11.99 $9.14 $9.25 December 31, 2009 (stockholders’ equity and (borrowings under repurchase arrangements (calculated assuming |

CAPSTEAD 11 Comparative Income Statement (in thousands, except per share amounts) (unaudited) Quarter Ended December September June March December 2009 2009 2009 2009 2008 Interest income: Mortgage securities and similar investments $ 70,458 $ 74,695 $ 81,062 $ 87,884 $ 95,397 Other 76 69 133 217 272 70,534 74,764 81,195 88,101 95,669 Interest expense: Repurchase arrangements and similar borrowings (21,697) (26,802) (31,626) (39,957) (65,349) Unsecured borrowings (2,187) (2,186) (2,187) (2,187) (2,187) (23,884) (28,988) (33,813) (42,144) (67,536) 46,650 45,776 47,382 45,957 28,133 Other revenue (expense): Impairment and related charges associated with commercial real estate loan investments (39,673) – – – – Miscellaneous other revenue (expense) (75) 16 (804) (105) (124) Incentive compensation expense (1,334) (1,058) (1,243) (1,134) (1,180) General and administrative expense (3,038) (2,713) (2,893) (2,707) (2,592) (44,120) (3,755) (4,940) (3,946) (3,896) Income before equity in earnings of unconsolidated affiliates 2,530 42,021 42,442 42,011 24,237 Equity in earnings of unconsolidated affiliates 65 64 65 65 65 Net income Net i ncome per diluted common share $(0.04) $0.56 $0.58 $0.58 $0.32 Core Earnings (a) $ 42,908 $ 42,677 $ 43,745 $ 42,367 $ 23,545 Core Earnings per diluted common share (a) $ 0.54 $0.56 $0.60 $0.58 $0.30 Average balance on mortgage assets $ 7,801,412 $7,564,203 $7,481,914 $7,517,220 $7,747,643 Average financing spread on mortgage assets (b) 2.40% 2.40% 2.47% 2.33% 1.28% Average financing spread on all interest - earning assets 2.21% 2.25% 2.31% 2.16% 1.17% Investment premium amortization $ 8,994 $ 8,311 $ 6,618 $ 5,523 $ 6,141 (a) See pages 15 and 16 for discussion of use of Core Earnings and Core Earnings per diluted common share, non GAAP financial

measures. (b) See page 14 for discussion of use of financing spread on mortgage assets, a non-GAAP financial

measure. $ 2,595 $ 42,085 $ 42,507 $ 42,076 $ 24,302 |

CAPSTEAD 12 Yield / Cost Analysis (dollars in thousands) * See page 14 for discussion of use of financing spread on mortgage assets, a non-GAAP

financial measure. Basis Yield/Cost Runoff Basis Yield/Cost Runoff Agency-guaranteed securities: Fannie Mae/Freddie Mac: Fixed-rate $ 7,323 6.47% 26.9% $ 7,713 6.47% 23.2% ARMs 7,420,397 3.59 21.1 7,130,322 3.96 21.8 Ginnie Mae ARMs 357,911 3.68 21.3 357,716 4.06 20.2 7,785,631 3.60 21.1 7,495,751 3.96 21.7 Unsecuritized residential mortgage loans: Fixed-rate 3,717 6.93 5.7 4,321 6.67 44.7 ARMs 8,434 4.26 19.4 8,630 4.57 6.2 12,151 5.08 15.9 12,951 5.27 23.9 Commercial real estate loans 40,190 - - 44,267 - - Commercial loans 10,060 9.63 - 7,576 9.59 - 3,630 8.54 3.0 3,658 5.84 14.8 7,851,662 3.59 20.9 7,564,203 3.95 21.6 Other interest-earning assets 218,195 0.14 111,733 0.25 8,069,857 3.50 7,675,936 3.90 30-day to 90-day interest rates 7,126,672 1.19 6,527,919 1.40 Greater than 90-day interest rates - - 253,259 5.15 Structured financings 3,630 8.54 3,658 5.84 7,130,302 1.19 6,784,836 1.55 Unsecured borrowings 103,095 8.49 103,095 8.49 7,233,397 1.29 6,887,931 1.65 Capital employed/ Total financing spread $ 836,460 2.21 $ 788,005 2.25 Financing spread on mortgage assets * 2.40 2.40 Third Quarter Average Secured borrowings based on: Fourth Quarter Average Collateral for structured financings |

CAPSTEAD 13 Residential ARM Securities Portfolio Statistics (as of December 31, 2009) Fully Indexed Average Average Average Months Principal Cost Basis Net Net Net Periodic Lifetime To Balance Premiums $ % WAC WAC* Margins Caps Caps Roll Current-reset ARMs: Agency Securities: Fannie/Freddie ARM securities $ 5,696,174 $ 81,651 $ 5,777,825 101.43 3.44% 2.55% 1.82% 3.26% 10.41% 5.3 Ginnie Mae ARM securities 354,611 2,210 356,821 100.62 3.94 2.03 1.53 1.00 10.08 5.5 Residential mortgage loans 7,974 67 8,041 100.84 3.93 2.50 2.06 1.56 11.12 5.5 6,058,759 83,928 6,142,687 101.39 3.47 2.52 1.80 3.13 10.40 5.3 Longer-to-reset ARMs: Agency Securities: Fannie/Freddie ARM securities 1,719,442 25,415 1,744,857 101.48 6.13 2.39 1.66 1.90 11.55 27.2 Total ARM securities $ 7,778,201 $ 109,343 $ 7,887,544 101.41 4.06 2.49 1.77 2.86 10.65 10.1 * Fully indexed net WAC represents the coupon upon one or more resets using interest rates indices as of

September 30, 2009 and the applicable net margin. |

CAPSTEAD 14 Use of Financial Spread on Mortgage Assets, a Non-GAAP Financial Measure Fourth Quarter 2009 (dollars in thousands) Total Financing Spread, a Financing Spread on Mortgage Assets, a GAAP Measure Non-GAAP Financial Measure Interest Income (Expense) Yield/Cost Difference Interest Income (Expense) Yield/Cost Correspondin Third Quarter 2009 Yield/Cost Interest income: Mortgage assets $ 70,458 3.59% $ – $ 70,458 3.59% 3.95% Other interest-earning assets 76 0.14 (76) – – – 70,534 3.50 (76) 70,458 3.59 3.95 Interest expense: Secured borrowings (borrowings under repurchase agreements) (21,697) 1.19 – (21,697) 1.19 1.55 Unsecured borrowings (2,187) 8.49 2,187 – – – (23,884) 1.29 2,187 (21,697) 1.19 1.55 Net interest margin/financing spread $ 46,650 2.21 $ 2,111 $ 48,761 2.40 2.40 (a) (b) Other interest-earning assets consist of overnight investments and cash collateral receivable from

interest rate swap counterparties. (c) Unsecured borrowings consist of junior

subordinated notes with original terms of 30 years issued in 2005 and 2006 by Capstead to

statutory trusts formed to issue $3.1 million of the trusts’ common securities to Capstead and to privately place $100.0 million of preferred securities to unrelated third party investors. Capstead reflects its investment in the

trusts as unconsolidated affiliates and considers the unsecured borrowings, net of these

affiliates, a component of its long-term investment capital. (b) (c) (a) Net interest margin on mortgage assets and Financing spread on mortgage assets are non-GAAP financial measures (based solely on interest income and yields on the Company’s portfolio of mortgage securities,

net of borrowings under repurchase agreements). These measures are

similar to the all-inclusive GAAP measures, Total net interest margin and Total financing spread (based on all interest-earning assets and all interest-bearing liabilities).

|

CAPSTEAD 15 Use of Core Earnings, a Non-GAAP Financial Measure (in thousands) (unaudited) Year Ended Quarter Ended December December September June March December 2009 2008 2009 2009 2009 2009 2008 Net income (a GAAP financial measure) $ 129,263 $ 125,923 $ 2,595 $ 42,085 $ 42,507 $ 42,076 $ 24,302 Reclassify financial results associated with non-core investments in commercial real estate loans: Net interest margin – (3,556) – – – – (926) Impairment charge on Nevis investment 39,249 – 39,249 – – – – Impairment charge and loss on consolidation of townhome 1,174 – 424 – 750 – – development loans Townhome development operating 36 – 36 – – – – expenses, net Legal and other related expenses 1,975 642 604 592 488 291 169 42,434 (2,914) 40,313 592 1,238 291 (757) Core Earnings (a non-GAAP financial measure) Core Earnings and Core Earnings per diluted common share are non-GAAP financial

performance measures closely associated with GAAP net income and net income

(loss) per diluted common share. The Company defines Core Earnings as GAAP net income excluding financial results associated with non-core investments in

commercial real estate loans. The use of these non- GAAP

financial measures allows management and investors to evaluate the performance of the Company's core residential mortgage portfolio by removing commercial real estate lending activity that currently is

limited to two nonperforming investments. Core Earnings and Core Earnings per diluted common share are not substitutes for GAAP net income and net income (loss) per diluted common share as measures of our financial performance and should be not

considered to be any measure of liquidity. In addition, the Company's

definition of Core Earnings and Core Earnings per diluted common share may not be comparable to similarly-titled non-GAAP financial measures used by other companies. The

table above and on the next page reconciles these non-GAAP financial

measures to their associated GAAP financial measures. $ 171,697 $ 123,009 $ 42,908 $ 42,677 $ 43,745 $ 42,367 $ 23,545 |

CAPSTEAD 16 Use of Core Earnings, a Non-GAAP Financial Measure (in thousands, except per share amounts) (unaudited) Year Ended Quarter Ended December December September June March December 2009 2008 2009 2009 2009 2009 2008 Numerator for GAAP earnings (loss per diluted common share $ 108,776 $ 105,285 $ (2,499) $41,903 $42,387 $41,839 $19,167 Exclude financial results associated with non-core investments in commercial real estate loans 42,434 (2,914) 40,313 592 1,238 291 (757) Change in dividends on antidilutive convertible preferred shares 19,932 – 5,058 – – – – Change in earnings impact of non-vested stock awards (242) 19 (210) (3) (7) (2) 5 Numerator for Core Earnings per diluted common share Denominator for GAAP earnings (loss) per diluted common share 65,449 54,468 68,849 75,436 73,140 72,771 60,384 Change in net effect of dilutive stock awards – – 67 – – – – Change in net effect of dilutive convertible preferred shares 9,627 – 9,940 – – – – Denominator for Core Earnings per diluted common share 75,076 54,468 78,856 75,436 73,140 72,771 60,384 Earnings (loss) per diluted common share (a GAAP financial measure) $1.66 $ 1.93 $(0.04) $ 0.56 $ 0.58 $ 0.57 $ 0.32 Change due to above adjustments 0.62 (0.05) 0.58 – 0.02 0.01 (0.02) Core Earnings per diluted common share (a non-GAAP financial measure) $ 170,900 $ 102,390 $ 42,662 $ 42,492 $ 43,618 $ 42,128 $ 18,415 $ 2.28 $ 1.88 $ 0.54 $ 0.56 $ 0.60 $ 0.58 $ 0.30 |