Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended November 28, 2009

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 001-09225

H.B. FULLER COMPANY

(Exact name of registrant as specified in its charter)

| Minnesota | 41-0268370 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| 1200 Willow Lake Boulevard, St. Paul, Minnesota | 55110-5101 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (651) 236-5900

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Common Stock, par value $1.00 per share |

New York Stock Exchange | |

| Common Stock Purchase Rights |

New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: none

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to the Form 10-K. x

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes ¨ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer x | Accelerated filer ¨ | |

| Non-accelerated filer ¨ (Do not check if a smaller reporting company) | Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the Common Stock, par value $1.00 per share, held by non-affiliates of the registrant as of May 29, 2009 was approximately $827,202,228 (based on the closing price of such stock as quoted on the New York Stock Exchange of $17.02 on such date).

The number of shares outstanding of the Registrant’s Common Stock, par value $1.00 per share, was 48,715,480 as of January 8, 2010.

DOCUMENTS INCORPORATED BY REFERENCE

Part III incorporates information by reference to portions of the registrant’s Proxy Statement of the Annual Meeting of Shareholders to be held on April 15, 2010.

Table of Contents

2009 Annual Report on Form 10-K

Table of Contents

| PART I | 3 | |||

| Item 1. |

3 | |||

| Item 1A. |

6 | |||

| Item 1B. |

8 | |||

| Item 2. |

9 | |||

| Item 3. |

10 | |||

| Item 4. |

12 | |||

| 15 | ||||

| Item 5. |

15 | |||

| Item 6. |

16 | |||

| Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

17 | ||

| Item 7A. |

38 | |||

| Item 8. |

42 | |||

| Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

80 | ||

| Item 9A. |

80 | |||

| Item 9B. |

81 | |||

| 82 | ||||

| Item 10. |

82 | |||

| Item 11. |

82 | |||

| Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

82 | ||

| Item 13. |

Certain Relationships and Related Transactions and Director Independence |

83 | ||

| Item 14. |

83 | |||

| 84 | ||||

| Item 15. |

84 | |||

| 88 | ||||

2

Table of Contents

| Item 1. | Business |

H.B. Fuller Company was founded in 1887 and incorporated as a Minnesota corporation in 1915. Our stock is traded on the New York Stock Exchange (NYSE) under the ticker symbol FUL. As used herein, “H.B. Fuller”, “we”, “us”, “our”, “management” or “company” includes H.B. Fuller and its subsidiaries unless otherwise indicated.

We are a leading worldwide formulator, manufacturer and marketer of adhesives, sealants, paints and other specialty chemical products. Sales operations span 38 countries in North America, Europe, Latin America, the Asia Pacific region, the Middle East and Africa. Industrial adhesives represent our core product offering, totaling over 80 percent of our annual revenue. Customers use our adhesives products in manufacturing common consumer goods, including food and beverage containers, disposable diapers, windows, doors, flooring, appliances, sportswear and footwear. We also provide adhesives for a variety of industrial applications such as water filtration products and multi-wall bags. Through leveraging strong relationships with our customers, our adhesives help improve the performance of our customers’ products or improve efficiencies in their manufacturing processes. We also provide our customers with technical support and unique solutions designed to address their specific needs. Our adhesives revenue, as a percent of total net revenue, was 82 percent, 81 percent, and 80 percent for 2009, 2008 and 2007 respectively.

We have established a variety of product offerings for residential specialty construction markets such as tile-setting adhesives, grout, sealants and related products. These products are sold primarily in North America and represent approximately 10 percent, 11 percent and 12 percent of our total revenue for 2009, 2008 and 2007, respectively. Liquid paint and related products are manufactured and sold in Central America, representing approximately 8 percent of our total revenue.

Our business is reported in four regional operating segments: North America, EMEA (Europe, Middle East and Africa), Latin America and Asia Pacific. The North America segment accounted for 43 percent of 2009 net revenue. EMEA, Latin America and Asia Pacific accounted for 29 percent, 18 percent and 10 percent, respectively.

Segment Information

Each of our four operating segments apply core industrial adhesives products in a variety of markets: Assembly (appliances, filters, construction, etc.), packaging (food and beverage containers, consumer goods, durable and non-durable goods, etc.), converting (corrugation, tape and label, paper converting, multi-wall bags and sacks), nonwoven and hygiene (disposable diapers, feminine care, medical garments, tissue and towel), performance wood (windows, doors, wood flooring), textile (footwear, sportswear, etc.), flexible packaging, graphic arts and envelope.

The North America operating segment key business components are adhesives, about 78 percent of the segment’s annual revenue, and specialty construction. Adhesives includes a full range of specialty adhesives such as thermoplastic, thermoset, water-based and solvent-based products. Sales are primarily made through a direct sales force with a smaller portion of sales through distributors. Specialty construction includes products used for tile setting (adhesives, grouts, mortars, sealers, levelers, etc.) and HVAC and insulation applications (duct sealants, weather barriers and fungicidal coatings, block fillers, etc.). Specialty construction sales are made through a direct sales force, distributors and retailers.

The EMEA operating segment is comprised of an adhesives component with the same range of products as North America. EMEA adhesives sales are made through both a direct sales force and distributors.

3

Table of Contents

The Latin America operating segment includes adhesives and liquid paints business components. The adhesives component is similar to that of North America and sales are made primarily through a direct sales force. The paints component has a leading market position, in Central America, under the Glidden® and Protecto® brands. Paints sales are primarily made through distributors and our network of retail stores located throughout Central America selling liquid paint for residential and commercial applications (architectural, marine, highway safety, etc.).

The Asia Pacific operating segment is similar to that of North America, with one exception. The Asia Pacific adhesive component also includes caulks and sealants for the consumer market, sold through retailers. Adhesives sales are made through a direct sales force and distributors.

Financial Information with respect to our segments and geographic areas is set forth in Note 14 to the Consolidated Financial Statements and is incorporated herein by reference.

Non-U.S. Operations

The principal markets, products and methods of distribution outside the United States vary with each of our four regional operations generally maintaining integrated business units that contain dedicated supplier networks, manufacturing, logistics and sales organizations. The vast majority of the products sold within any region are produced within the region and the respective regions do not import significant amounts of product from other regions. At the end of 2009, we had sales offices and manufacturing plants in 17 countries outside the United States and satellite sales offices in another 17 countries.

We have adopted policies and processes, and conduct employee training, all of which are intended to ensure compliance with various economic sanctions and export controls, including the regulations of the U.S. Treasury Department’s Office of Foreign Assets Control (“OFAC”). We do not conduct any business in countries that are subject to U.S. economic sanctions such as Cuba, Iran, Sudan and Syria, whether through subsidiaries, joint ventures or other direct or indirect arrangements, nor do we have any assets, employees or operations in these countries.

Competition

Many of our markets are highly competitive and we maintain a healthy position due to our adhesives, sealants and coatings portfolio. Within the adhesives and other specialty chemical markets, we believe few suppliers have comparable global reach and corresponding ability to deliver quality and consistency to multinational customers. Our competition is made up of two types of companies, similar multinational suppliers and regional suppliers that typically compete in only one region and often within a narrow geographic area within a region. The multinational competitors typically maintain a broad product offering and range of technology while regional companies tend to have limited product ranges and technology.

Principal competitive factors in the sale of adhesives and other specialty chemicals are product performance, supply assurance, technical service, quality, price and customer service.

Customers

We have cultivated strong, integrated relationships with a diverse set of customers worldwide, who are among the technology and market leaders in consumer goods, construction, and industrial markets. We pride ourselves on long-term, collaborative customer relationships and a diverse portfolio of customers where no single client accounted for more than 10 percent of consolidated net revenue.

Our leading customers include manufacturers of food and beverages, hygiene products, clothing, major appliances, filters, construction materials, wood flooring, furniture, cabinetry, windows, doors, tissue and towel, corrugation, tube winding, packaging, labels and tapes.

4

Table of Contents

Our products are delivered to customers primarily from our manufacturing plants, with additional deliveries made through distributors and retailers.

Backlog

No significant backlog of unfilled orders existed at November 28, 2009 or November 29, 2008.

Raw Materials

We use several principal raw materials in our manufacturing process, include tackifying resins, polymers, synthetic rubbers, vinyl acetate monomer and plasticizers. We generally avoid sole source supplier arrangements for raw materials.

The majority of our raw materials are petroleum/natural gas based derivatives. Under normal conditions, raw materials are available on the open market. Prices and availability are subject to supply and demand market mechanisms. Higher crude oil and natural gas costs usually result in higher prices for raw materials; however, supply and demand balances also can have a significant impact.

Patents, Trademarks and Licenses

Much of the technology, which we use in our manufacturing processes is available in the public domain. For technology not available in the public domain, we rely on trade secrets and patents when appropriate to protect our competitive position. We also license some patented technology from other sources. Our business is not materially dependent upon licenses or similar rights or on any single patent or group of related patents.

Agreements extend with many employees to protect rights to technology and intellectual property. Confidentiality commitments also are routinely obtained from customers, suppliers and others to safeguard proprietary information.

We own numerous trademarks and service marks in various countries. Trademarks, such as H.B. Fuller®, Advantra®, Adalis®, Sesame®, Protecto®, TEC®, Plasticola®, Color Caulk®, Amco Tool®, AIMTM, Rakoll®, Tile-Perfect® and ChapCo® are important in marketing products. Many of our trademarks and service marks are registered. U.S. trademark registrations are for a term of ten years and are renewable every ten years as long as the trademarks are used in the regular course of trade. We also license the Glidden® trademark for use in our Latin America paints business.

Research and Development

Our investment in research and development creates new and innovative adhesive technology platforms, enhances product performance, ensures a competitive cost structure and leverages available raw materials. New product development is a key research and development outcome, providing higher-value solutions to existing customers or meeting new customers needs. Projects are coordinated globally through our network of laboratories.

Through designing and developing new polymers and new formulations, we will continue to grow in our current markets. We also develop new applications for existing products and technologies, and improve manufacturing processes to enhance productivity and product quality. Research and development efforts are closely aligned to customer needs, but we do not engage in customer sponsored activities. We foster open innovation and seek supplier-driven new technology and use links with academic and other institutions to enhance our capabilities.

Research and development expenses were $17.0 million, $16.5 million and $16.9 million in 2009, 2008 and 2007, respectively. Research and development costs are included in selling, general and administrative expenses.

5

Table of Contents

Environmental, Health and Safety

We comply with applicable regulations relating to environmental protection and workers’ safety. This includes regular review of and upgrades to environmental policies, practices and procedures as well as improved production methods to minimize our facilities’ outgoing waste, based on evolving societal standards and increased environmental understanding.

Environmental expenditures to comply with environmental regulations over the next two years are estimated to be approximately $6.2 million, including approximately $1.1 million of capital expenditures. See additional disclosure under Item 3. Legal Proceedings.

Seasonality

Our North America and EMEA operating segment revenues have historically been lower in winter months, which is primarily our first fiscal quarter, partially due to the seasonal decline in construction activities.

Employees

Approximately 3,100 individuals were employed on November 28, 2009, of which approximately 1,100 were in the United States.

Available Information

For more information about us, visit our website at: http://www.hbfuller.com.

We file annual, quarterly and current reports, proxy statements and other information with the Securities and Exchange Commission (SEC) via EDGAR. Our SEC filings are available free of charge to the public at our website as soon as reasonably practicable after they have been filed with or furnished to the SEC. You may also request a copy of these filings (other than an exhibit to a filing unless that exhibit is specifically incorporated by reference into that filing) at no cost, by writing to or telephoning us at the following address: Office of the Corporate Secretary, H.B. Fuller Company, 1200 Willow Lake Boulevard, P.O. Box 64683, St. Paul, Minnesota 55164-0683, (651) 236-5825.

| Item 1A. | Risk Factors |

As a global manufacturer of adhesives, sealants, paints and other specialty chemical products, we operate in a business environment that is subject to various risks and uncertainties. Below are the most significant factors that could adversely affect our business, financial condition and results of operations.

Adverse conditions in the global economy could continue to negatively impact our customers and therefore our financial results.

An economic downturn in the businesses or geographic areas in which we sell our products could reduce demand for these products and result in a decrease in sales volume that could have a negative impact on our results of operations. Product demand often depends on end-use markets. Economic conditions that reduce consumer confidence or discretionary spending may reduce product demand. Challenging economic conditions may also impair the ability of customers to pay for products they have purchased, and as a result, our reserves for doubtful accounts and write-offs of accounts receivable may increase.

Increases in prices and declines in the availability of raw materials could negatively impact our financial results.

Raw materials needed to manufacture products are obtained from a number of suppliers and many of the materials are petroleum-based derivatives, minerals and metals. Under normal market conditions, these materials

6

Table of Contents

are generally available on the open market from a variety of producers. While alternate supplies of most key raw materials are available, supplier production outages may lead to strained supply-demand situations for certain raw materials. The substitution of key raw materials requires us to identify new supply sources, reformulate, retest and may require seeking re-approval from our customers using those products. From time to time, the prices and availability of these raw materials may fluctuate, which could impair the ability to procure necessary materials, or increase the cost of manufacturing products. If the prices of raw materials increase in a short period of time, we may be unable to pass these increases on to our customers in a timely manner and could experience reductions to our profit margins.

Uncertainties in foreign political and economic conditions and fluctuations in foreign currency may adversely affect our results.

Approximately 58 percent, or $714 million, of net revenue was generated outside the United States in 2009. International operations could be adversely affected by changes in political and economic conditions, trade protection measures, restrictions on repatriation of earnings, differing intellectual property rights and changes in regulatory requirements that restrict the sales of products or increase costs. Also, fluctuations in exchange rates between the U.S. dollar and other currencies could potentially result in increases or decreases in earnings and may adversely affect the value of our assets outside the United States. Although we utilize risk management tools, including hedging, as appropriate, to mitigate market fluctuations in foreign currencies, any changes in strategy in regard to risk management tools can also affect sales revenue, expenses and results of operations and there can be no assurance that such measures will result in cost savings or that all market fluctuation exposure will be eliminated.

We experience substantial competition in each of the operating segments and geographic areas in which we operate.

A wide variety of products are sold in numerous markets, each of which is highly competitive. Our competitive position in markets is, in part, subject to external factors. For example, supply and demand for certain of our products is driven by end-use markets and worldwide capacities which, in turn, impact demand for and pricing of our products. Many of our direct competitors are part of large multi-national companies and may have more resources than we do. Any increase in competition may result in lost market share or reduced prices, which could result in reduced profit margins. This may impair the ability to grow or even to maintain current levels of revenues and earnings. While we have an extensive customer base, loss of certain top customers could adversely affect our financial condition and results of operations until such business is replaced, and no assurances can be made that we would be able to regain or replace any lost customers.

Failure to protect our intellectual property could negatively impact our future performance and growth.

We continually apply for and obtain U.S. and foreign patents to protect the results of our research for use in our operations and licensing. We are party to a substantial number of patent licenses and other technology agreements. We rely on patents, confidentiality agreements and internal security measures to protect our intellectual property. Failure to protect this intellectual property could negatively affect our future performance and growth.

We may be required to record impairment charges on our long-lived assets.

Weak demand may cause underutilization of our manufacturing capacity or elimination of product lines; contract terminations or customer shutdowns may force sale or abandonment of facilities and equipment; or other events associated with weak economic conditions or specific product or customer events may require us to record an impairment on tangible assets, such as facilities and equipment, as well as intangible assets, such as intellectual property or goodwill, which would have a negative impact on our financial results.

7

Table of Contents

We have lawsuits and claims against us with uncertain outcomes.

Our operations from time to time are parties to or targets of lawsuits, claims, investigations, and proceedings, including product liability, personal injury, asbestos, patent and intellectual property, commercial, contract, environmental, antitrust, health and safety, and employment matters, which are handled and defended in the ordinary course of business. The results of any future litigation or settlement of such lawsuits and claims are inherently unpredictable, but such outcomes could be adverse and material in amount. See Item 3. Legal Proceedings for a discussion of current litigation.

Costs and expenses resulting from compliance with environmental laws and regulations may negatively impact our operations and financial results.

We are subject to numerous environmental laws and regulations that impose various environmental controls on us or otherwise relate to environmental protection, the sale and export of certain chemicals or hazardous materials, and various health and safety matters. The costs of complying with these laws and regulations can be significant and may increase as applicable requirements and their enforcement become more stringent and new rules are implemented. Adverse developments and/or periodic settlements could negatively impact our results of operations and cash flows. See Item 3. Legal Proceedings for a discussion of current environmental matters.

Distressed financial markets may result in dramatic deflation of asset valuations and a general disruption in capital markets.

Adverse equity market conditions and volatility in the credit markets could have a negative impact on the value of our pension trust assets and our future estimated pension liabilities, and other post-retirement benefit plans. In addition, we could be required to provide increased pension plan funding. As a result, our financial results could be negatively impacted. Reduced access to capital markets may affect our ability to invest in strategic growth initiatives such as acquisitions. In addition, the reduced credit availability could limit our customers’ ability to invest in their businesses, refinance maturing debt obligations, or meet their ongoing working capital needs. If these customers do not have sufficient access to the financial markets, demand for our products may decline.

The inability to make or effectively integrate acquisitions may affect our results.

As part of our growth strategy, we intend to pursue acquisitions of complementary businesses or products and joint ventures. The ability to grow through acquisitions or joint ventures depends upon our ability to identify, negotiate, complete and integrate suitable acquisitions or joint venture arrangements. If we fail to successfully integrate acquisitions into our existing business, our results of operations and cash flows could be adversely affected.

Catastrophic events could disrupt our operations or the operations of our suppliers or customers, having a negative impact on our financial results.

Unexpected events, including natural disasters and severe weather events, acts of war or terrorism, supply disruptions or breaches of security of our information technology systems could increase the cost of doing business or otherwise harm our operations, our customers and our suppliers. Such events could reduce demand for our products or make it difficult or impossible for us to receive raw materials from suppliers and deliver products to our customers.

The inability to attract and retain qualified personnel could adversely impact our business.

Sustaining and growing our business depends on the recruitment, development and retention of qualified employees. The inability to recruit and retain key personnel or the unexpected loss of key personnel may adversely affect our operations.

| Item 1B. | Unresolved Staff Comments |

None.

8

Table of Contents

| Item 2. | Properties |

Principal executive offices and central research facilities are located in the St. Paul, Minnesota area. These facilities are company owned and contain 247,630 square feet. Manufacturing operations are carried out at 16 plants located throughout the United States and at 18 plants located in 17 other countries. In addition, numerous sales and service offices are located throughout the world. We believe that the properties owned or leased are suitable and adequate for our business. Operating capacity varies by product line, but additional production capacity is available for most product lines by increasing the number of shifts worked. The following is a list of our manufacturing plants as of November 28, 2009 (each of the listed properties is owned by us, unless otherwise specified):

| Region |

Manufacturing Sq Ft |

Region |

Manufacturing Sq Ft | |||

| North America | Asia Pacific | |||||

| California - Roseville |

82,202 | Australia - Dandenong South, VIC | 71,280 | |||

| Florida - Gainesville |

6,800 | Republic of China - Huangpu Guangzhou¹ |

68,380 | |||

| Georgia - Covington |

73,500 | Philippines - Laguna | 10,759 | |||

| - Dalton |

72,000 | Asia Pacific Total | 150,419 | |||

| - Tucker |

69,000 | |||||

| Illinois - Aurora |

149,000 | EMEA | ||||

| - Palatine |

55,000 | Austria - Wels¹ | 66,500 | |||

| Kentucky - Paducah |

252,500 | Egypt - 6th of October City | 8,525 | |||

| Michigan - Grand Rapids |

65,689 | Germany - Lueneburg | 64,249 | |||

| Minnesota - Fridley |

15,850 | - Nienburg |

139,248 | |||

| - Vadnais Heights |

53,145 | Italy - Borgolavezzaro, (No) | 24,219 | |||

| New Jersey - Edison |

9,780 | Portugal - Porto | 90,193 | |||

| Ohio - Blue Ash |

102,000 | United Kingdom - Dukinfield | 17,465 | |||

| Texas - Houston |

11,000 | EMEA Total | 410,399 | |||

| - Mesquite |

25,000 | |||||

| Washington - Vancouver |

35,768 | Latin America | ||||

| Total U.S. |

1,078,234 | Argentina - Buenos Aires | 10,367 | |||

| Brazil - Sorocaba, SP² | 7,535 | |||||

| Chile - Maipu, Santiago | 64,099 | |||||

| Colombia - Itagui, Antioquia¹ | 7,800 | |||||

| Canada - Boucherville, QC |

36,500 | Costa Rica - Alajuela | 4,993 | |||

| - Alto de Ochomogo Cartago |

167,199 | |||||

| Honduras - San Pedro Sula | 23,346 | |||||

| Republic of Panama - Tocumen |

30,588 | |||||

| North America Total |

1,114,734 | Latin America Total | 315,927 | |||

| 1 | Leased Property |

| 2 | Idle Property |

9

Table of Contents

| Item 3. | Legal Proceedings |

Environmental Matters. From time to time, we are identified as a “potentially responsible party” (PRP) under the Comprehensive Environmental Response, Compensation and Liability Act (CERCLA) and/or similar state laws that impose liability for costs relating to the clean up of contamination resulting from past spills, disposal or other release of hazardous substances. We are also subject to similar laws in some of the countries where current and former facilities are located. Our environmental, health and safety department monitors compliance with applicable laws on a global basis.

Currently we are involved in various environmental investigations, clean up activities and administrative proceedings and lawsuits. In particular, we are currently deemed a PRP in conjunction with numerous other parties, in a number of government enforcement actions associated with hazardous waste sites. As a PRP, we may be required to pay a share of the costs of investigation and clean up of these sites. In addition, we are engaged in environmental remediation and monitoring efforts at a number of current and former operating facilities, including remediation of environmental contamination at the Sorocaba, Brazil facility. Soil and water samples were collected on and around the Sorocaba facility, and test results indicated that certain contaminants, including carbon tetrachloride and other solvents, exist in the soil at the Sorocaba facility and in the groundwater at both the Sorocaba facility and some neighboring properties. We are continuing to work with Brazilian regulatory authorities to implement and operate a remediation system at the site. As of November 28, 2009, $1.3 million was recorded as a liability for expected remediation expenses remaining for this site. Depending on the results of the testing of our current remediation actions, we may be required to record additional liabilities related to remediation costs at the Sorocaba facility.

From time to time, we become aware of compliance matters relating to, or receive notices from, federal, state or local entities regarding possible or alleged violations of environmental, health or safety laws and regulations. We review the circumstances of each individual site, considering the number of parties involved, the level of potential liability or contribution of us relative to the other parties, the nature and magnitude of the hazardous substances involved, the method and extent of remediation, the estimated legal and consulting expense with respect to each site and the time period over which any costs would likely be incurred. To the extent we can reasonably estimate the amount of our probable liabilities for environmental matters, we establish a financial provision. As of November 28, 2009, we had reserved $3.0 million, which represents our best estimate of probable liabilities with respect to environmental matters, inclusive of the accrual related to the Sorocaba facility as described above. However, the full extent of our future liability for environmental matters is difficult to predict because of uncertainty as to the cost of investigation and clean up of the sites, our responsibility for such hazardous substances and the number of and financial condition of other potentially responsible parties.

While uncertainties exist with respect to the amounts and timing of the ultimate environmental liabilities, based on currently available information, we do not believe that these matters, individually or in aggregate, will have a material adverse effect on our long-term financial condition. However, adverse developments and/or periodic settlements could negatively impact the results of operations or cash flows in one or more future quarters.

Other Legal Proceedings. From time to time and in the ordinary course of business, we are a party to, or a target of, lawsuits, claims, investigations and proceedings, including product liability, personal injury, contract, patent and intellectual property, health and safety and employment matters. While we are unable to predict the outcome of these matters, we do not believe, based upon currently available information, that the ultimate resolution of any pending matter, individually or in aggregate, including the asbestos litigation described in the following paragraphs, will have a material adverse effect on our long-term financial condition. However, adverse developments and/or periodic settlements could negatively impact the results of operations or cash flows in one or more future quarters.

We have been named as a defendant in lawsuits in which plaintiffs have alleged injury due to products containing asbestos manufactured more than 25 years ago. The plaintiffs generally bring these lawsuits against multiple

10

Table of Contents

defendants and seek damages (both actual and punitive) in very large amounts. In many cases, plaintiffs are unable to demonstrate that they have suffered any compensable injuries or that the injuries suffered were the result of exposure to products manufactured by us. We are typically dismissed as a defendant in such cases without payment. If the plaintiff presents evidence indicating that compensable injury occurred as a result of exposure to our products, the case is generally settled for an amount that reflects the seriousness of the injury, the length, intensity and character of exposure to asbestos containing products, the number and solvency of other defendants in the case, and the jurisdiction in which the case has been brought.

A significant portion of the defense costs and settlements in asbestos-related litigation continues to be paid by third parties, including indemnification pursuant to the provisions of a 1976 agreement under which we acquired a business from a third party. Historically, this third party routinely defended all cases tendered to it and paid settlement amounts resulting from those cases. In the 1990s, the third party sporadically reserved its rights, but continued to defend and settle all asbestos-related claims tendered to it by us. In 2002, the third party rejected the tender of certain cases and indicated it would seek contributions for past defense costs, settlements and judgments. However, this third party is defending and paying settlement amounts, under a reservation of rights, in most of the asbestos cases tendered to the third party. As discussed below, during the fourth quarter of 2007, we and a group of other defendants, including the third party obligated to indemnify us against certain asbestos-related claims, entered into negotiations with certain law firms to settle a number of asbestos-related lawsuits and claims.

In addition to the indemnification arrangements with third parties, we have insurance policies that generally provide coverage for asbestos liabilities (including defense costs). Historically, insurers have paid a significant portion of our defense costs and settlements in asbestos-related litigation. However, certain of our insurers are insolvent. We have entered into cost-sharing agreements with our insurers that provide for the allocation of defense costs and, in some cases, settlements and judgments, in asbestos-related lawsuits. Under these agreements, we are required in some cases to fund a share of settlements and judgments allocable to years in which the responsible insurer is insolvent.

As referenced above, during the fourth quarter of 2007, we and a group of other defendants entered into negotiations with certain law firms to settle a number of asbestos-related lawsuits and claims over a period of years. In total, we expect to contribute up to $4.1 million towards the settlement amount to be paid to the claimants in exchange for a full release of claims. Of this amount, our insurers have committed to pay $2.0 million based on a probable liability of $4.1 million. In 2009 $1.1 million was paid toward this settlement, with our insurers paying $0.5 million of that amount. Given that the remaining settlement payouts are expected to occur over a period of years and that the accrual is based on the maximum number of cases to be settled, we applied a present value approach and have accrued $2.9 million and recorded a receivable of $1.5 million as of November 28, 2009.

In addition to the group settlement referenced above, a summary of the number of and settlement amounts for asbestos-related lawsuits and claims is as follows:

| ($ in millions) |

Year Ended November 28, 2009 |

Year Ended November 29, 2008 |

Year Ended December 01, 2007 | ||||||

| Lawsuits and claims settled |

7 | 5 | 6 | ||||||

| Settlements reached |

$ | 0.8 | $ | 0.8 | $ | 0.4 | |||

| Insurance payments received or expected to be received |

$ | 0.6 | $ | 0.6 | $ | 0.3 | |||

We do not believe that it would be meaningful to disclose the aggregate number of asbestos-related lawsuits filed against us because relatively few of these lawsuits are known to involve exposure to asbestos-containing products that we manufactured. Rather, we believe it is more meaningful to disclose the number of lawsuits that are settled and result in a payment to the plaintiff.

11

Table of Contents

To the extent we can reasonably estimate the amount of our probable liabilities for pending asbestos-related claims, we establish a financial provision and a corresponding receivable for insurance recoveries. As of November 28, 2009, our probable liabilities and insurance recoveries related to asbestos claims were $3.5 million and $1.9 million respectively. We have concluded that it is not possible to reasonably estimate the cost of disposing of other asbestos-related claims (including claims that might be filed in the future) due to our inability to project future events. Future variables include the number of claims filed or dismissed, proof of exposure to our products, seriousness of the alleged injury, the number and solvency of other defendants in each case, the jurisdiction in which the case is brought, the cost of disposing of such claims, the uncertainty of asbestos litigation, insurance coverage and indemnification agreement issues, and the continuing solvency of certain insurance companies.

Based on currently available information, we do not believe that asbestos-related litigation, individually or in aggregate, will have a material adverse effect on our long-term financial condition. However, adverse developments and/or periodic settlements in such litigation could negatively impact the results of operations or cash flows in one or more future quarters.

In addition to product liability claims discussed above, we are involved in other claims or legal proceedings related to our products, which we believe are not out of the ordinary in a business of the type and size in which we are engaged.

| Item 4. | Submission of Matters to a Vote of Security Holders |

None.

12

Table of Contents

Executive Officers of the Registrant

The following table shows the name, age and business experience, for the past five years, of the executive officers as of January 15, 2010. Unless otherwise noted, the positions described are positions with H.B. Fuller or its subsidiaries.

| Name |

Age | Positions |

Period Served | |||

| Michele Volpi |

45 | President and Chief Executive Officer Group President, General Manager, Global Adhesives |

December 2006-Present

December 2004-December 2006 | |||

| James R. Giertz |

52 | Senior Vice President, Chief Financial Officer Senior Managing Director, Chief Financial Officer, GMAC ResCap (real estate finance company) Senior Vice President, Commercial & Industrial Products, Donaldson Company, Inc. (global provider of filtration equipment and replacement parts) |

March 2008-Present

2006-2007

2000-2006 | |||

| Kevin M. Gilligan |

43 | Vice President, Asia Pacific Group Vice President, General Manager, H.B. Fuller Window |

March 2007-Present

December 2004-March 2007 | |||

| Timothy J. Keenan |

52 | Vice President, General Counsel and Corporate Secretary General Counsel and Corporate Secretary Deputy General Counsel, Assistant Corporate Secretary |

December 2006-Present December 2005-December 2006

August 2004-December 2005 | |||

| Steven Kenny |

48 | Senior Vice President, EMEA and India President, Specialty Packaging Division, Pregis Corporation (international manufacturer, marketer, and supplier of protective packaging products and specialty packaging solutions) Corporate Vice President and General Manager, Europe, Middle East and Africa, National Starch & Chemical Company, Adhesives Division (manufacturer of adhesives, sealants, specialty synthetic polymers and industrial starches) Divisional Vice President and General Manager, Vinamul Polymers North America, National Starch & Chemical Company |

October 2009-Present

August 2008-September 2009

2005-2008

2002-2005 | |||

| James C. McCreary, Jr. |

53 | Vice President, Corporate Controller Interim Chief Financial Officer, Vice President and Corporate Controller Vice President, Corporate Controller |

February 2008-Present

February 2007-February 2008 November 2000-February 2007 | |||

13

Table of Contents

| Name |

Age | Positions |

Period Served | |||

| James J. Owens |

45 | Senior Vice President, North America Senior Vice President, Henkel Corporation (global manufacturer of adhesives, sealants and surface treatments) Corporate Vice President and General Manager, National Starch & Chemical Company, Adhesives Division (manufacturer of adhesives, sealants, specialty synthetic polymers and industrial starches) |

September 2008-Present

April 2008-August 2008

December 2004-April 2008 | |||

| Ann B. Parriott |

51 | Vice President, Human Resources Vice President (Human Resources), Applied Global Services, Applied Materials (supplier of manufacturing systems and related services to the global semiconductor industry) |

January 2006 -Present

2004-2005 | |||

| Barry S. Snyder |

47 | Vice President, Chief Technology Officer Global Technology Director, Celanese Corporation (global manufacturer of chemicals for consumer and industrial applications) Global Research Director/Adhesives and Sealants, Rohm and Haas Company (global manufacturer of specialty chemicals) |

October 2008-Present

2007-October 2008

2004-2006 | |||

| Ramon Tico Farre |

46 | Vice President, Latin America Regional Group Vice President, Global Adhesives, Latin America Core Business Manager, GE Silicones Europe, General Electric (manufacturer and marketer of silicone products such as elastomers, sealants, coatings and fluids) |

March 2007-Present

October 2005-March 2007

2003-2005 | |||

The Board of Directors elects the executive officers annually.

14

Table of Contents

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Our common stock is traded on the New York Stock Exchange under the symbol “FUL.” As of January 8, 2010, there were 2,510 common shareholders of record for our common stock. The following table shows the high and low sales price per share of our stock and the dividends declared for the fiscal quarters.

| High and Low Sales Price | Dividends (Per Share) | |||||||||||||||||

| 2009 | 2008 | |||||||||||||||||

| High | Low | High | Low | 2009 | 2008 | |||||||||||||

| First quarter |

$ | 16.89 | $ | 11.03 | $ | 27.07 | $ | 17.02 | $ | 0.0660 | $ | 0.0645 | ||||||

| Second quarter |

18.94 | 9.70 | 25.75 | 18.70 | 0.0680 | 0.0660 | ||||||||||||

| Third quarter |

21.50 | 16.47 | 26.64 | 20.43 | 0.0680 | 0.0660 | ||||||||||||

| Fourth quarter |

23.06 | 18.61 | 27.84 | 12.23 | 0.0680 | 0.0660 | ||||||||||||

There are no significant contractual restrictions on our ability to declare or pay dividends. We currently expect that comparable dividends on our common stock will continue to be paid in the future.

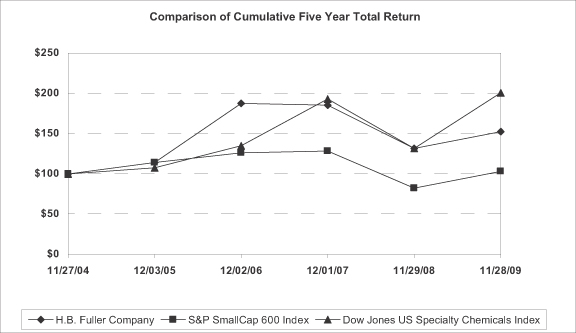

Total Shareholder Return Graph

The line graph below compares the cumulative total shareholder return on our common stock for the last five fiscal years with cumulative total return on the S&P SmallCap 600 Index and Dow Jones U.S. Specialty Chemicals Index. This graph assumes a $100 investment in each of H.B Fuller, the S&P SmallCap 600 Index and the Dow Jones U.S. Specialty Chemicals Index at the close of trading on November 27, 2004, and also assumes the reinvestment of all dividends.

15

Table of Contents

| Item 6. | Selected Financial Data |

| (Dollars in thousands, except per share amounts) |

Fiscal Years | ||||||||||||||

| 2009 | 2008 | 2007¹ | 2006¹ ² | 2005¹ ³ | |||||||||||

| Net revenue |

$ | 1,234,659 | $ | 1,391,554 | $ | 1,400,258 | $ | 1,386,108 | $ | 1,329,647 | |||||

| Income from continuing operations |

$ | 83,654 | $ | 18,889 | $ | 101,144 | $ | 72,701 | $ | 53,183 | |||||

| Percent of net revenue |

6.8 | 1.4 | 7.2 | 5.2 | 4.0 | ||||||||||

| Total assets |

$ | 1,100,445 | $ | 1,081,328 | $ | 1,364,602 | $ | 1,478,471 | $ | 1,107,557 | |||||

| Long-term debt, excluding current installments |

$ | 162,713 | $ | 204,000 | $ | 137,000 | $ | 224,000 | $ | 112,001 | |||||

| Stockholders’ equity |

$ | 591,354 | $ | 535,611 | $ | 798,993 | $ | 777,792 | $ | 587,085 | |||||

| Per Common Share: |

|||||||||||||||

| Income from continuing operations before cumulative effect of accounting change: |

|||||||||||||||

| Basic |

$ | 1.73 | $ | 0.37 | $ | 1.69 | $ | 1.24 | $ | 0.93 | |||||

| Diluted |

$ | 1.70 | $ | 0.36 | $ | 1.66 | $ | 1.21 | $ | 0.91 | |||||

| Dividends declared and paid |

$ | 0.2700 | $ | 0.2625 | $ | 0.2560 | $ | 0.2488 | $ | 0.2413 | |||||

| Book value |

$ | 12.15 | $ | 11.06 | $ | 13.91 | $ | 12.98 | $ | 10.06 | |||||

| Number of employees |

3,129 | 3,141 | 3,234 | 3,574 | 3,603 | ||||||||||

| 1 | All amounts have been adjusted for removal of discontinued operations (see Note 2 to the Consolidated Financial Statements). |

| 2 | All amounts have been adjusted for: a) the July 2006 2-for-1 stock split and b) reclassifications associated with the adoption of SFAS 123R. |

| 3 | 53-week fiscal year. |

16

Table of Contents

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

Overview

H.B. Fuller Company is a global formulator, manufacturer and marketer of adhesives and other specialty chemical products. We are managed through four regional operating segments – North America, Europe, Middle East and Africa (EMEA), Latin America and Asia Pacific.

Each of the four segments manufactures and supplies adhesives products in the assembly, packaging, converting, nonwoven and hygiene, performance wood, flooring, textile, flexible packaging, graphic arts and envelope markets. In addition, the North America segment provides specialty construction products such as ceramic tile installation products and HVAC adhesives and sealants. The Latin America segment also manufactures and sells paints primarily in the Central American countries.

Total Company: When reviewing our financial statements, it is important to understand how certain external factors impact us. These factors include:

| • | Changes in the prices of commodities, such as crude oil and natural gas |

| • | Global supply and demand of raw materials |

| • | Economic growth rates, and |

| • | Currency exchange rates compared to the U.S. dollar |

We purchase thousands of raw materials, the majority of which are petroleum/natural gas derivatives. With over 70 percent of our cost of sales accounted for by raw materials, our financial results are extremely sensitive to changing costs in this area. In addition to the impact from commodity prices, the supply and demand of raw materials also have a significant impact on our costs. As demand increases in high-growth areas, such as the Asia Pacific region, the supply of key raw materials may tighten, resulting in certain materials being put on allocation. Natural disasters, such as hurricanes, also can have an impact as key raw material producers are shut down for extended periods of time. We continually monitor areas such as capacity utilization figures, market supply and demand conditions, feedstock costs and inventory levels, as well as derivative and intermediate prices, which affect our raw materials.

In 2009 we generated 42 percent of our net revenue in the U.S. and 29 percent in EMEA. Net revenue generated in the U.S. was $520.9 million, $578.2 million and $625.1 million for 2009, 2008 and 2007, respectively. The pace of economic growth in these areas directly impacts certain industries to which we supply products. For example, adhesives-related revenues from durable goods customers in areas such as appliances, furniture and other woodworking applications tend to fluctuate with the overall economic activity. In business components such as specialty construction and insulating glass, revenues tend to move with more specific economic indicators such as housing starts and other construction-related activity.

The movement of foreign currency exchange rates as compared to the U.S. dollar impacts the translation of the foreign entities’ financial statements into U.S. dollars. As foreign currencies strengthen against the dollar, our revenues and costs increase as the foreign currency-denominated financial statements translate into more dollars. The fluctuations of the Euro against the U.S. dollar have the largest impact on our financial results as compared to all other currencies. In 2009, the currency fluctuations had a negative impact on net revenue of $48.9 million as compared to 2008. Although the dollar weakened sequentially throughout 2009, on average, the dollar was stronger than it was in 2008. The estimated impact on earnings per share was a decrease of $0.08—$0.09 as compared to 2008.

Key financial results and transactions for 2009 included the following:

| • | Net revenue declined 11.3 percent from 2008 primarily due to declines in sales volume resulting from the depressed global economy. |

17

Table of Contents

| • | Gross profit margin improved to 30.1 percent from 26.2 percent in 2008. |

| • | Contributed $143.9 million to fund our defined benefit pension plans, primarily in the U.S. and Germany. |

| • | Cash flow generated from operating activities, was $71.4 million in 2009 as compared to $43.3 million in 2008. |

| • | Settled a lawsuit with the former owners of the Roanoke Companies Group, a business we acquired in 2006. The settlement resulted in a pretax gain of $18.8 million which was $11.8 million after tax or $0.24 per diluted share. |

| • | Completed acquisition of the outstanding shares of Nordic Adhesive Technology GmbH. located in Buxtehude, Germany on April 20, 2009 for approximately $4.2 million. |

The global economic conditions continued to have a negative impact on our sales volume in 2009. The economic slowdown that began primarily in the U.S. construction and housing markets in 2007, expanded to most major markets and industries in 2008 and continued throughout 2009. The credit crisis in late 2008 exacerbated the situation. Our sales volume decreased 11.7 percent in 2009 as compared to 2008, however we started to see positive signs in our sales volumes in the fourth quarter as sales volumes declined only 4.5 percent as compared to the fourth quarter of 2008.

Although 2009 was a challenging year in terms of the economic environment, we were able to improve our EPS to $1.70 per share from $0.36 in 2008. The 2008 figure included a negative $1.05 per share related to goodwill and other impairment charges. In 2009 we continued to invest to make H.B. Fuller a stronger company. Investments made in 2009 included additional resources in our sales and marketing organizations, strengthening our management team, building a manufacturing facility in China, and the Nordic acquisition in Germany.

2010 Outlook

There remains a significant amount of uncertainty for 2010 in regards to end-market demand. While we believe the worst is most likely behind us, we do not anticipate a quick return to pre-recession demand levels. In terms of net revenue growth, with the investments we have made and will continue to make in our sales and technical organizations, we expect to have positive revenue growth in 2010. The gross profit margin will come under some pressure in 2010 as raw material costs are expected to increase. SG&A expenses will most likely increase in 2010 as compared to 2009 as we continue to invest in the future of the company and we will also have the full-year impact of investments made in 2009.

The current economic environment makes it very difficult to make accurate projections of future financial results. Therefore, no specific quantitative guidance for 2010 is included in this report. We are committed to executing our long-range strategy while managing through the economic uncertainties.

Critical Accounting Policies and Significant Estimates: Management’s discussion and analysis of our results of operations and financial condition are based upon consolidated financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States of America (U.S. GAAP). The preparation of these financial statements requires us to make estimates and judgments that affect the reported amounts of assets, liabilities, revenues and expenses and related disclosure of contingent assets and liabilities. We believe the critical accounting policies and areas that require the most significant judgments and estimates to be used in the preparation of the consolidated financial statements are pension and other postretirement plan assumptions; goodwill impairment assessment; long-lived assets recoverability; share-based compensation accounting; product, environmental and other litigation liabilities; and income tax accounting.

Pension and Other Postretirement Plan Assumptions: We sponsor defined-benefit pension plans in both U.S. and foreign entities. Also in the U.S. we sponsor other postretirement plans for health care and life insurance

18

Table of Contents

costs. Expenses and liabilities for the pension plans and other postretirement plans are actuarially calculated. These calculations are based on our assumptions related to the discount rate, expected return on assets, projected salary increases and health care cost trend rates. Through 2008, the annual measurement date for the benefit obligations and plan assets was August 31, but in accordance with changes in U.S. GAAP we now measure our benefit obligations and plan assets as of our fiscal year end. Note 10 to the Consolidated Financial Statements includes disclosure of assumptions employed in these measurements for both the non-U.S. and U.S. plans.

The discount rate assumption is determined using an actuarial tool that applies a yield curve approach which enables us to select a discount rate that reflects the characteristics of the plan. The tool identifies a broad universe of corporate bonds that meet the quality and size criteria for the particular plan. This is in contrast to using a specific index that has a certain set of bonds that may or may not be representative of the characteristics of our particular plan. A lower discount rate increases the present value of the pension obligations, which results in higher pension expense. The discount rate for the U.S. pension plan was 5.72 percent at November 28, 2009, as compared to 6.94 percent at August 31, 2008 and 6.25 percent at August 31, 2007. Net periodic pension cost for a given fiscal year is based on assumptions developed at the end of the previous fiscal year. A discount rate reduction of 0.5 percentage points at November 28, 2009 would increase pension and other postretirement plan expense approximately $2.6 million (pretax) in fiscal 2010. Discount rates for non-U.S. plans are determined in a manner consistent with the U.S. plan.

The expected return on assets assumption on the investment portfolios for the pension and other postretirement benefit plans is based on the long-term expected returns for the investment mix of assets in the portfolio. The disruption in the credit markets at the end of 2008 and the ongoing economic slowdown impacted our investment strategy for the pension portfolios, which in turn, has impacted our assumption for the expected return on assets. Our current investment strategy for the U.S. pension plan is to invest 60 percent of the portfolio in equities and 40 percent in fixed income securities. This strategy represents a change from an allocation in prior years of 80 percent equities and 20 percent fixed income. The change in strategy was primarily intended to reduce volatility of plan assets in future periods and to more closely match the duration of the plan assets with the duration of the plan liabilities. Higher volatility in the asset values results in higher volatility in the annual expenses associated with the plans.

Asset values declined significantly from the August 31 measurement date in 2008 into the second quarter of 2009 due to the deterioration of the credit markets before rebounding for the remainder of 2009. The combination of the reduced asset values and the higher pension obligations due to the lower discount rate resulted in our pension plans being significantly under-funded. Therefore, in the fourth quarter of 2009 we elected to contribute $75 million to the U.S. pension plan for the purpose of restoring the asset values up to the level of the projected benefit obligations and to reduce 2010 net periodic benefit cost. As of November 28, 2009 the U.S. pension plan assets were just 1.3 percent below the plan’s projected benefit obligations. As of November 28, 2009 the $75 million had not yet been allocated to the targeted investments; therefore, the investment mix of assets as of November 28, 2009 was 49.5 percent equities and 50.5 percent fixed income securities. We plan to reallocate the portfolio to the new target allocation in the first six months of 2010. Our investment strategy for the non-U.S. pension plans was also amended in 2009 to being more balanced between equities and fixed income securities. For reasons similar to the U.S. plan, we also contributed $50 million to the German plan in the fourth quarter of 2009.

The expected return on assets used in calculating the net periodic benefit cost for the U.S. pension plan was 8.75 percent for 2009 and 9.00 percent for 2008 and 2007. For 2010, the rate will decrease to 7.90 percent to reflect the change in the target mix of assets to 60 percent equities and 40 percent fixed income. A change of 0.5 percentage points for the expected return on assets assumption would impact U.S. net pension and other postretirement plan expense by approximately $ 1.8 million (pretax). Expected return on asset assumptions for non-U.S. plans is determined in a manner consistent with the U.S. plan.

The projected salary increase assumption is based on historic trends and comparisons to the external market. Higher rates of increase result in higher pension expenses. As this rate is also a long-term expected rate, it is less likely to change on an annual basis. In the U.S., we have used the rate of 4.18 percent for 2009, 4.23 percent for 2008 and 4.22 percent for 2007.

19

Table of Contents

Goodwill: Goodwill is the excess of cost of an acquired entity over the amounts assigned to assets acquired and liabilities assumed in a purchase business combination. Goodwill is assigned to reporting units at the date the goodwill is initially recorded. Once goodwill has been assigned to a reporting unit, it no longer retains its association with a particular acquisition and all the activities within a reporting unit are available to support the value of goodwill. Accounting standards require us to test goodwill for impairment annually or more often if circumstances or events indicate a change in the estimated fair value.

The goodwill impairment analysis is a two-step process. The first step used to identify potential impairment involves comparing each reporting unit’s estimated fair value to its carrying value, including goodwill. We use a discounted cash flow approach to estimate the fair value of our reporting units. Our judgment is required in developing the assumptions for the discounted cash flow model. These assumptions include revenue growth rates, profit margin percentages, discount rates, perpetuity growth rates, future capital expenditures, etc. If the estimated fair value of a reporting unit exceeds its carrying value, goodwill is considered to not be impaired. If the carrying value exceeds estimated fair value, there is an indication of potential impairment and the second step is performed to measure the amount of impairment.

The second step of the process involves the calculation of an implied fair value of goodwill for each reporting unit for which step one indicated impairment. The implied fair value of goodwill is determined similar to how goodwill is calculated in a business combination, by measuring the excess of the estimated fair value of the reporting unit as calculated in step one, over the estimated fair values of the individual assets, liabilities and identifiable intangibles as if the reporting unit was being acquired in a business combination. If the implied fair value of goodwill exceeds the carrying value of goodwill assigned to the reporting unit, there is no impairment. If the carrying value of goodwill assigned to a reporting unit exceeds the implied fair value of the goodwill, an impairment charge is recorded for the excess. An impairment loss cannot exceed the carrying value of goodwill assigned to a reporting unit, and the loss establishes a new basis in the goodwill. Subsequent reversal of goodwill impairment losses is not permitted.

In 2008 after our initial assessment, completed during the fourth quarter based on balance sheet information as of the end of our third quarter, we determined that none of our goodwill was impaired. After our initial assessment, as economic conditions worsened and the capital markets became distressed, we determined that circumstances had changed enough to trigger another goodwill impairment assessment as of November 29, 2008. That assessment resulted in the determination that the fair value of our specialty construction reporting unit was less than the carrying value of its net assets, including goodwill. This was due to a decline in the estimated future discounted cash flows expected from the reporting unit. The adverse economic conditions, especially in the U.S. housing and other construction markets, were the primary driver of the reduction in forecasted discounted cash flows. The amount of the pretax impairment charge in the fourth quarter of 2008 was $85.0 million ($52.8 million after tax). The $85.0 million pretax charge was an estimated amount as of November 29, 2008.

The final valuation work was completed in the first quarter of 2009 and resulted in an additional pretax impairment charge of $0.8 million ($0.5 million after tax). The amount of goodwill assigned to the specialty construction reporting unit was $99.1 million prior to any impairment charges. After the final valuation and additional impairment charge, the amount of goodwill is $13.3 million.

In the fourth quarter of 2009, we conducted the required annual test of goodwill for impairment. There were no indications of impairment. The specialty construction reporting unit continues to be the only reporting unit with a significant risk of impairment. As the construction markets, particularly U.S. housing starts, continued to slide in 2009, the specialty construction reporting unit fell short of its revenue projections in 2009. Profit margins did improve however to significantly offset the impact of the net revenue decline. The fair value for the specialty construction reporting unit exceeded its carrying value by approximately 23 percent. The projected cash flows used in the fair value calculation were based on no economic growth in 2010 as the net revenue growth projected for 2010 for specialty construction was based primarily on new business that was already procured during 2009. For years beyond 2010, the net revenue projections assume slightly higher growth in 2011 and 2012 with a

20

Table of Contents

leveling off in the low-single digits for the remaining years. Profit margins for the specialty construction reporting unit are projected to grow primarily due to sales volume increases as the cost structure and manufacturing capability is in place to support a significantly higher sales volume than was recorded in 2009.

Although we believe the assumptions used to estimate the fair value of the specialty construction reporting unit were realistic, the continued slowdown of the U.S. residential construction industry could have an adverse impact on specialty construction’s future cash flows. If the reporting unit does not meet its revenue and cash flow projections for 2010, then the fair value could fall below the carrying value of the net assets. That would trigger a step 2 analysis and could lead to an impairment charge if the implied goodwill is calculated to be less than the $13.3 million goodwill balance.

In all other reporting units, the calculated fair value significantly exceeded the carrying value of the net assets.

See Note 6 to the Consolidated Financial Statements for further discussion.

Recoverability of Long-Lived Assets: The assessment of the recoverability of long-lived assets reflects our assumptions and estimates. Factors that we must estimate when performing impairment tests include sales volume, prices, inflation, currency exchange, and tax rates and capital spending. Significant judgment is involved in estimating these factors, and they include inherent uncertainties. The measurement of the recoverability of these assets is dependent upon the accuracy of the assumptions used in making these estimates and how the estimates compare to the eventual future operating performance of the specific businesses to which the assets are attributed.

Judgments made by us related to the expected useful lives of long-lived assets and the ability to realize undiscounted cash flows in excess of the carrying amounts of such assets are affected by factors such as the ongoing maintenance and improvement of the assets, changes in economic conditions and changes in operating performance.

Share-based Compensation: We have granted stock options, restricted stock and deferred compensation awards to certain employees and non-employee directors. We recognize compensation expense for all share-based payments granted after December 3, 2005 and prior to but not yet vested as of December 3, 2005, in accordance with accounting standards. Under the fair value recognition provisions of the Financial Accounting Standards Board (FASB) Accounting Standards CodificationTM (ASC) 505 and 718, we recognize share-based compensation net of an estimated forfeiture rate and only recognize compensation cost for those shares expected to vest on a straight-line basis over the requisite service period of the award (normally the vesting period).

Determining the appropriate fair value model and calculating the fair value of share-based payment awards require the input of highly subjective assumptions, including the expected life of the share-based payment awards and stock price volatility. We use the Black-Scholes model to value our stock option awards. We believe that future volatility will not materially differ from our historical volatility. Thus, we use the historical volatility of our common stock over the expected life of the award. The assumptions used in calculating the fair value of share-based payment awards represent our best estimates, but these estimates involve inherent uncertainties and the application of our judgment. As a result, if factors change and we use different assumptions, share-based compensation expense could be materially different in the future. In addition, we are required to estimate the expected forfeiture rate and only recognize expense for those shares expected to vest. If the actual forfeiture rate is materially different from the estimate, share-based compensation expense could be significantly different from what has been recorded in the current period. See Note 3 to the Consolidated Financial Statements for a further discussion on share-based compensation.

Product, Environmental and Other Litigation Liabilities: As disclosed in Item 3 and in Note 1 and Note 12 to the Consolidated Financial Statements, we are subject to various claims, lawsuits and other legal proceedings. Accruals for loss contingencies associated with these matters are made when it is determined that a liability is

21

Table of Contents

probable and the amount can be reasonably estimated. The assessment of the probable liabilities is based on the facts and circumstances known at the time that the financial statements are being prepared. For cases in which it is determined that a liability has been incurred but only a range for the potential loss exists, the minimum amount of the range is recorded and subsequently adjusted as better information becomes available.

For cases in which insurance coverage is available, the gross amount of the estimated liabilities is accrued and a receivable is recorded for any probable estimated insurance recoveries. As of November 28, 2009, we have accrued $3.5 million for potential liabilities and $1.9 million for potential insurance recoveries related to asbestos litigation. We have also recorded $3.0 million for environmental investigation and remediation liabilities, including $1.3 million for environmental remediation and monitoring activities at our Sorocaba, Brazil facility as of November 28, 2009. A complete discussion of environmental, product and other litigation liabilities is disclosed in Item 3 and Note 12 to the Consolidated Financial Statements.

Based upon currently available facts, we do not believe that the ultimate resolution of any pending legal proceeding, individually or in the aggregate, will have a material adverse effect on our long-term financial condition. However, adverse developments and/or periodic settlements could negatively impact our results of operations or cash flows in one or more future quarters.

Income Tax Accounting: As part of the process of preparing the consolidated financial statements, we are required to estimate income taxes in each of the jurisdictions in which we operate. The process involves estimating actual current tax expense along with assessing temporary differences resulting from differing treatment of items for book and tax purposes. These temporary differences result in deferred tax assets and liabilities, which are included in the consolidated balance sheet. We record a valuation allowance to reduce our deferred tax assets to the amount that is more likely than not to be realized. We have considered future taxable income and ongoing tax planning strategies in assessing the need for the valuation allowance. Increases in the valuation allowance result in additional expense to be reflected within the tax provision in the consolidated statement of income. At November 28, 2009, the valuation allowance to reduce deferred tax assets totaled $2.9 million. See Note 8 to the Consolidated Financial Statements for further information on income tax accounting.

Results of Operations

Net Revenue:

| ($ in millions) |

2009 | 2008 | 2007 | 2009 vs 2008 | 2008 vs 2007 | ||||||||||

| Net revenue |

$ | 1,234.7 | $ | 1,391.6 | $ | 1,400.3 | (11.3 | )% | (0.6 | )% | |||||

Net revenue in 2009 of $1,234.7 decreased $156.9 million or 11.3 percent from 2008 revenue of $1,391.6 million. The 2008 net revenue was $8.7 million or 0.6 percent below the net revenue of $1,400.3 million in 2007. We review variances in net revenue in terms of changes related to product pricing, sales volume, changes in foreign currency exchange rates and acquisitions. The following table shows the net revenue variance analysis for the past two years:

| 2009 vs 2008 | 2008 vs 2007 | |||||

| Product pricing |

3.3 | % | 2.4 | % | ||

| Sales volume |

(11.7 | )% | (6.4 | )% | ||

| Currency |

(3.6 | )% | 3.3 | % | ||

| Acquisitions |

0.7 | % | 0.1 | % | ||

| (11.3 | )% | (0.6 | )% | |||

Organic sales growth, which we define as the combined variances from product pricing and sales volume, was a negative 8.4 percent (negative 11.7 percent from sales volume and positive 3.3 percent from selling prices) in

22

Table of Contents

2009 as compared to 2008. The sales volume declines were directly related to the continuation of the slow global economy. The volume trend in terms of year-over-year comparisons improved in the second half of the year, partially due to the weaker second half of 2008. The negative currency effects resulted from the stronger U.S. dollar as compared to most major foreign currencies, such as the Euro, Australian dollar and Canadian dollar, as compared to 2008. The net revenue variances from acquisitions were due to the Egymelt acquisition in the fourth quarter of 2008 and the acquisition of Nordic Adhesive Technology during the second quarter of 2009.

Sales volume declines in 2008 vs. 2007 were driven by the economic slowdowns, especially in North America and Europe. Quarterly sales volume decreases as compared to 2007 were improving through the first nine months of the year. During the fourth quarter, however, in conjunction with the disruption in the global financial and credit markets, the fourth quarter negative impact on net revenue due to sales volume declines was 7.4 percent. Revenues generated from increases in selling prices in response to rising raw material costs partially offset the effects of the volume declines. The positive impact from currency resulted primarily from the strengthening of the Euro versus the U.S. dollar. That positive impact through the first nine months of 2008 was 4.9 percent, however in the fourth quarter the dollar strengthened against the Euro and other major currencies.

Cost of Sales:

| ($ in millions) |

2009 | 2008 | 2007 | 2009 vs 2008 | 2008 vs 2007 | |||||||||||||

| Cost of Sales |

$ | 863.4 | $ | 1,027.1 | $ | 981.6 | (15.9 | )% | 4.6 | % | ||||||||

| Percent of net revenue |

69.9 | % | 73.8 | % | 70.1 | % | ||||||||||||

The cost of sales decreased 15.9 percent in 2009 compared to 2008. The decrease was driven primarily by the 11.7 percent decline in sales volume in 2009. Lower raw material prices and the effects of foreign currency fluctuations also contributed to the lower cost of sales in 2009 as compared to 2008. The 2009 cost of sales included $4.7 million of charges related to the realignment of production capacity in the North America operating segment.

The cost of sales increased 4.6 percent in 2008, compared to 2007, despite the sales volume decrease of 6.4 percent. This was a direct result of double-digit growth in raw material costs. The inflation rate on raw materials as measured from year-end 2007 to year-end 2008 was estimated at nearly 18 percent. The impact on raw material expense included in cost of sales was estimated at a 12.5 percent increase. The difference in rates reflects the ramping up of raw material prices throughout the year. A key factor in the raw material cost increase was the price of crude oil, which reached record levels during the year of nearly $150 per barrel. The raw material price increases were tempered late in the year as the economy continued to slow down and the price of oil decreased.

Gross Profit:

| ($ in millions) |

2009 | 2008 | 2007 | 2009 vs 2008 | 2008 vs 2007 | |||||||||||||

| Gross Profit |

$ | 371.3 | $ | 364.5 | $ | 418.7 | 1.9 | % | (13.0 | )% | ||||||||

| Percent of net revenue |