Attached files

| file | filename |

|---|---|

| 8-K - THE TEXT OF THE FILING WE ARE MAKING TO DISCLOSE PRESENTATION MATERIALS - PROASSURANCE CORP | bodyoffiling.htm |

Forward

Looking Statements

This

presentation contains Forward Looking Statements and other information

designed

to convey our projections and expectations regarding future results. There are a number

of factors which could cause our actual results to vary materially from those projected in

this presentation. The principal risk factors that may cause these differences are

described in various documents we file with the Securities and Exchange Commission,

such as our current reports on Form 8-K, and our regular reports on Forms 10-Q and

10-K, particularly in “Item 1A, Risk Factors.” Please review this presentation in

conjunction with a thorough reading and understanding of these risk factors.

to convey our projections and expectations regarding future results. There are a number

of factors which could cause our actual results to vary materially from those projected in

this presentation. The principal risk factors that may cause these differences are

described in various documents we file with the Securities and Exchange Commission,

such as our current reports on Form 8-K, and our regular reports on Forms 10-Q and

10-K, particularly in “Item 1A, Risk Factors.” Please review this presentation in

conjunction with a thorough reading and understanding of these risk factors.

This

presentation contains Non-GAAP measures, and we may reference

Non-GAAP measures in our remarks. A reconciliation of these measures to GAAP

measures is available in our latest quarterly news release, which is available in the

Investor Relations section of our website, www.ProAssurance.com, and in

the related Current Reports on Form 8K disclosing that release.

Non-GAAP measures in our remarks. A reconciliation of these measures to GAAP

measures is available in our latest quarterly news release, which is available in the

Investor Relations section of our website, www.ProAssurance.com, and in

the related Current Reports on Form 8K disclosing that release.

1

Non-GAAP

Measures

ProAssurance:

Quick Facts

Fifth

largest1 writer of

medical liability

Writing

business in 491

jurisdictions

Approximately

55,0002

individual

policyholders

policyholders

42,000

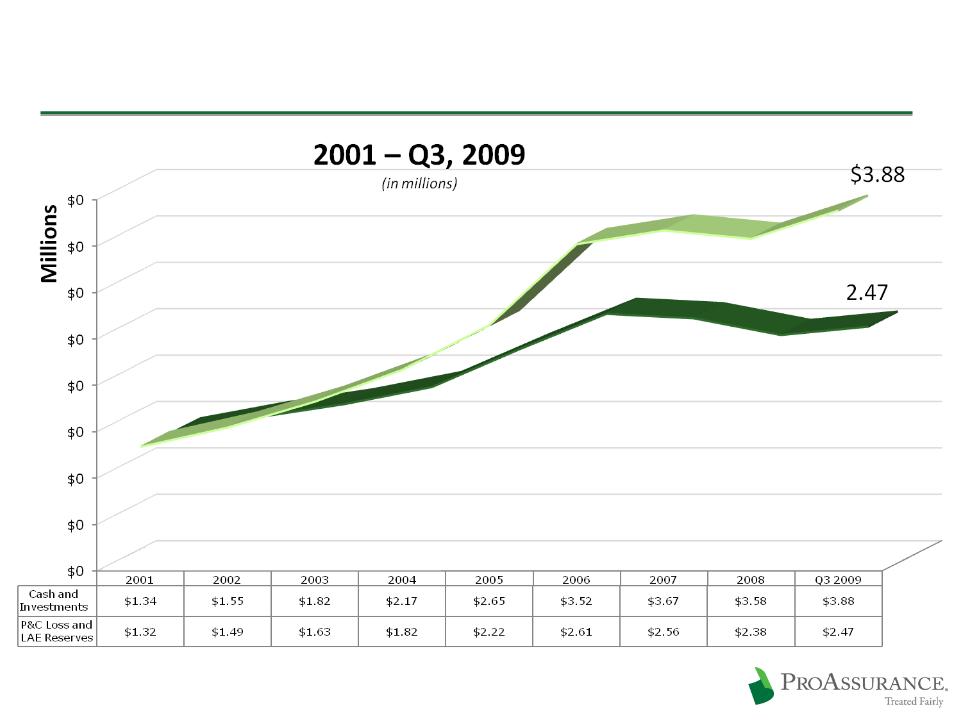

physicians and dentists

8,000

ancillary and other healthcare professionals

4,800

attorneys

Majority

in small or solo practice

500

hospitals and facilities

Highly

rated by A. M. Best and Fitch

2

1 Includes PICA 2 Includes PICA and

Georgia

Lawyers

Lawyers

Recent

Highlights

Completion

of three M&A transactions in 2009

Potential

new premium

is approximately

$100 million on an annualized basis

$100 million on an annualized basis

Restoring

growth to the top line

Existing

markets grew modestly in Q2 2009

Maintaining

profitability

Successful

performance in a challenging

financial market and a demanding line of

insurance

financial market and a demanding line of

insurance

3

Successful

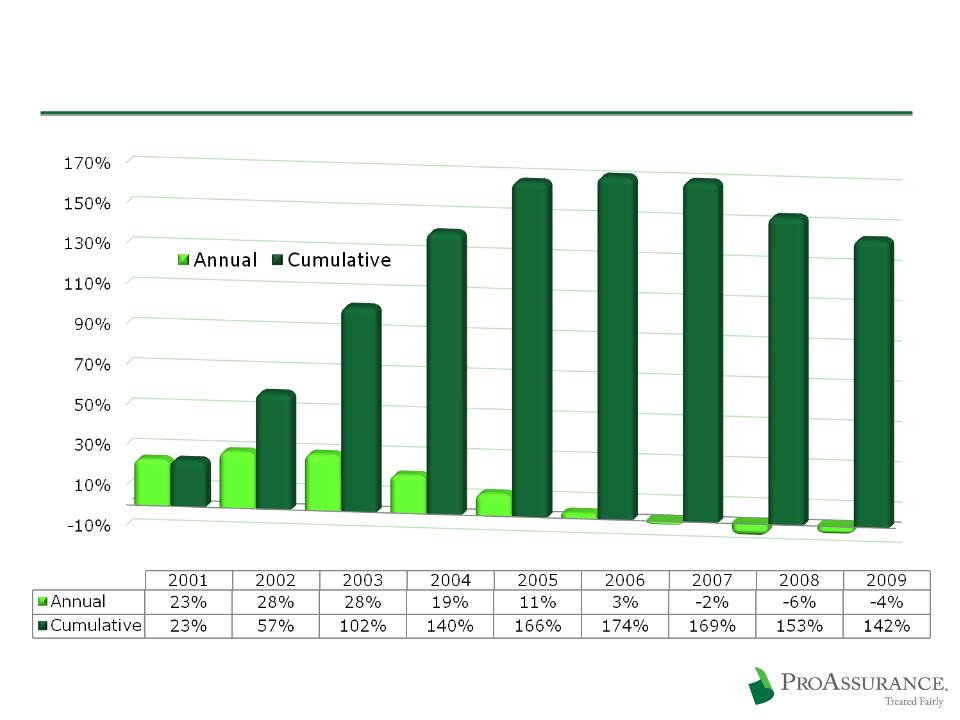

Performance: Book Value

|

Book

Value Growth

|

||

|

|

Cumulative

|

CAGR

|

|

10

year

|

222%

|

12%

|

|

5

year

|

127%

|

18%

|

|

1

year

|

10%

|

10%

|

|

Measured

through Year-End 2008

|

||

Successful

Performance: Stock Price

|

Share

Price Growth

|

||

|

|

Cumulative

|

CAGR

|

|

10

year

|

84%

|

6%

|

|

5

year

|

64%

|

10%

|

|

1

year

|

-5%

|

-5%

|

|

Measured

through Year-End 2008

|

||

5

Share

Price at Year End Since Inception

Recent

Business Highlights

Again

recognized as one of

the 50 top performing

property casualty insurance

companies by The Ward Group

the 50 top performing

property casualty insurance

companies by The Ward Group

Top 3% of

all P&C companies

Our third

straight year

Upgrade to

“A” (Excellent)

by A. M. Best

by A. M. Best

Positive

outlook

assigned by S & P

assigned by S & P

6

Recent

Employee Highlights

Named The

Best Mid-Size

Insurance Employer

in America by

Business Insurance

Insurance Employer

in America by

Business Insurance

Named one

of America’s

Top Ten Companies for

Employee Financial Security

by The Principal

Top Ten Companies for

Employee Financial Security

by The Principal

7

Operational

Strategies

Spreading

Risk is Vital

Broad

geographic diversification provides an

unmatched spread of risk

unmatched spread of risk

9

Our spread

of risk provides

better market awareness and

more data points to gauge loss

trends

better market awareness and

more data points to gauge loss

trends

Our

internal

actuarial

depth

allows us to assess emerging

trends and respond quickly

allows us to assess emerging

trends and respond quickly

Corporate

Headquarters

Corporate

Headquarters

Claims

Offices

Claims

Offices

Claims

/ Underwriting Offices

Claims

/ Underwriting Offices

PICA

and/or E&S States

PICA

and/or E&S States

PICA

Headquarters

PICA

Headquarters

(Birmingham)

(Nashville)

We

Dare to Defend

Our

balance sheet strength and deep expertise

ensures our insureds have the option of an

uncompromising defense of their claim

ensures our insureds have the option of an

uncompromising defense of their claim

We defend

our insureds at trial more often

than any other company in our line

than any other company in our line

Provides a

long-term financial and marketing

advantage

advantage

A key

differentiating factor in the market

as claims data becomes public

as claims data becomes public

10

Respond

to Transparency

Malpractice

judgments/settlements now

disclosed in 18 states

disclosed in 18 states

Public

access to the

National Practitioner

Data Bank is the

next step

National Practitioner

Data Bank is the

next step

Disciplinary

actions

now disclosed in

almost every state

now disclosed in

almost every state

11

Board /

Discipline / Med Mal

Med Mal

disclosure

legislation proposed

legislation proposed

P

Claims

Trends Remain Favorable

Frequency

trends are

stable after declining

since 2005/2006

stable after declining

since 2005/2006

The

results is fewer

cases to try

cases to try

Severity

trends also

stable

stable

Trends are

much the

same in states with or

without Tort Reform

same in states with or

without Tort Reform

12

ProAssurance

Claims Tried

to a Verdict

to a Verdict

Health

Care Reform & Tort Reform

No major

changes in the tort system based on

currently written legislation

currently written legislation

Demonstration

projects do not provide meaningful

reform or immediate data

reform or immediate data

Signals a

desire to leave the tort system in

the hands of each state

the hands of each state

We set

prices and reserves as if there is no tort

reform, until results reflect otherwise

reform, until results reflect otherwise

We are

prepared, operationally and financially, if

reforms are struck down in our states

reforms are struck down in our states

13

Maintaining

Pricing Discipline

14

Pricing

developed using multiple years

Using

credits allows us to maintain existing

rate filings

rate filings

Not unduly

influenced by current market

conditions

conditions

Rates on

renewing physician business down

less than 12% from peak pricing in 2006

less than 12% from peak pricing in 2006

Rate

Change History

15

Pricing

in a Low Interest Environment

Pricing

Discipline is Even More Critical

Combined

ratio

required to generate

a 13% after-tax ROE

required to generate

a 13% after-tax ROE

Strategy:

Actuarial Conservatism

|

$

2.4

|

|

|

$

2.6

|

|

|

$

2.6

|

|

|

$

2.2

|

|

|

$

1.8

|

|

Combined

Ratio Comparison

18

Source: A.

M. Best Aggregates and Averages 2009

Medical Malpractice Lines of Business Net

Medical Malpractice Lines of Business Net

Strategy:

Treated Fairly

Treated

Fairly is our brand enhancement initiative

Affirms

our existing, enduring commitment to

every stakeholder

every stakeholder

Insureds

Agents

Investors

The

public

We run our

business as owners who are

rewarded for long-term success

rewarded for long-term success

19

Growth

Strategies

Key

Opportunities

New

insurance buyers will emerge as

healthcare reform evolves

healthcare reform evolves

New

products will respond to physician/hospitals

combinations

combinations

The

outcome of medical liability claims will

become more transparent

become more transparent

Financial

issues will highlight the need for

successful, long-term companies with superior

balance sheets strength and outstanding ratings

successful, long-term companies with superior

balance sheets strength and outstanding ratings

21

2009:

Consolidation of:

Mid-Continent General Agency

Mid-Continent General Agency

2009:

Consolidation of:

Mid-Continent General Agency

Mid-Continent General Agency

Georgia

Lawyers Insurance Co.

Georgia

Lawyers Insurance Co.

2004: Purchased

Selected Renewal Rights from:

OHIC Insurance Company

OHIC Insurance Company

2004: Purchased

Selected Renewal Rights from:

OHIC Insurance Company

OHIC Insurance Company

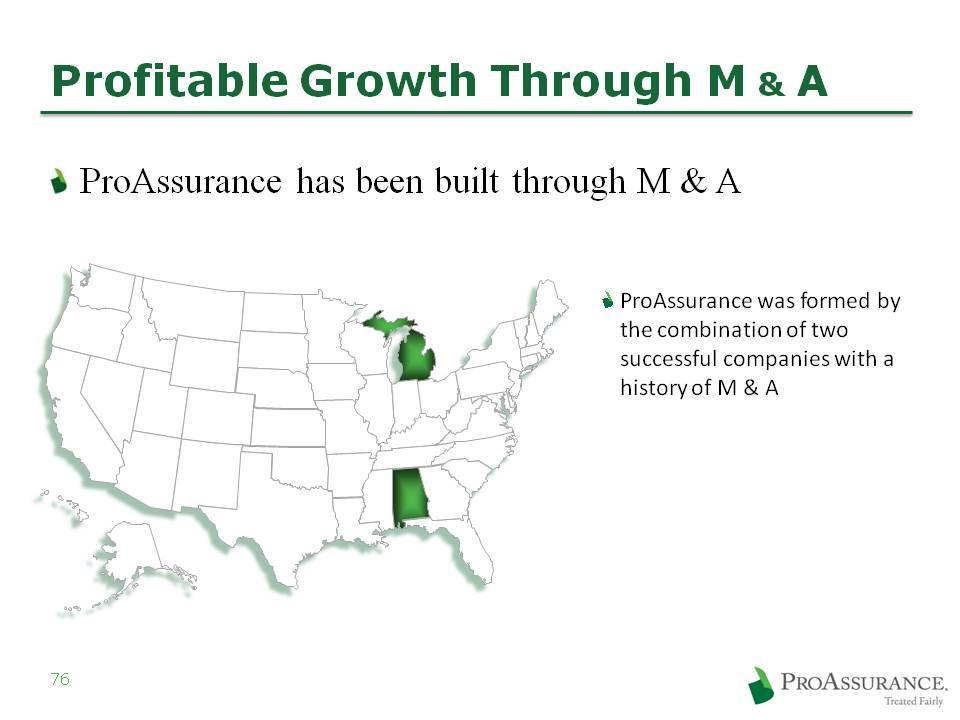

We

Created a Leader Through Consolidation

1994: Consolidation

of:

West Virginia Hosp. Ins Co.

West Virginia Hosp. Ins Co.

1994: Consolidation

of:

West Virginia Hosp. Ins Co.

West Virginia Hosp. Ins Co.

1995: Consolidation

of;

1995: Consolidation

of;

Physicians

Ins Co of Indiana

Physicians

Ins Co of Indiana

Assumed

business of:

Physicians Ins Co of Ohio

Physicians Ins Co of Ohio

Assumed

business of:

Physicians Ins Co of Ohio

Physicians Ins Co of Ohio

1996:

Consolidation

of:

1996:

Consolidation

of:

Missouri

Medical Ins Co

Missouri

Medical Ins Co

1995: Assumed

business of:

Associated Physicians Ins Co. (IL)

Associated Physicians Ins Co. (IL)

1995: Assumed

business of:

Associated Physicians Ins Co. (IL)

Associated Physicians Ins Co. (IL)

1998: Consolidation

of:

Physicians Protective Trust Fund (FL)

Physicians Protective Trust Fund (FL)

1998: Consolidation

of:

Physicians Protective Trust Fund (FL)

Physicians Protective Trust Fund (FL)

1996: Assumed

business of:

American Medical Ins Exchange (IN)

American Medical Ins Exchange (IN)

1996: Assumed

business of:

American Medical Ins Exchange (IN)

American Medical Ins Exchange (IN)

Founding

in the

1970’s

Founding

in the

1970’s

1999: Assumed

business of:

Medical Defense Associates (MO)

Medical Defense Associates (MO)

1999: Assumed

business of:

Medical Defense Associates (MO)

Medical Defense Associates (MO)

Mutual

Assurance

Physicians

Ins. Co. of

Michigan

Professionals

Group

Creation

of:

Creation

of:

2005: Consolidation

of:

NCRIC Group

NCRIC Group

2005: Consolidation

of:

NCRIC Group

NCRIC Group

2006:

Consolidation of:

PIC Wisconsin Group

PIC Wisconsin Group

2006:

Consolidation of:

PIC Wisconsin Group

PIC Wisconsin Group

2007: PRI

renewal rights deal

2002: SERTA

renewal rights deal

2001: OUM

renewal rights deal

2000: DPM

Merger

1999: PACO

Acquisition

22

Experienced

Management Team

|

Name

|

Position

|

Years

at

Company |

Years

Affiliated

With The Industry |

|

Stan

Starnes

|

Chairman

& CEO

|

2

|

31

|

|

Victor

Adamo

|

President

|

24

|

29

|

|

Jeff

Bowlby

|

Chief

Marketing Officer

|

11

|

25

|

|

Howard

Friedman

|

Liability

Group President / Chief Underwriting Officer

|

13

|

29

|

|

Jeff

Lisenby

|

Corporate

Counsel

|

8

|

8

|

|

Frank

O'Neil

|

Investor

Relations Officer

|

22

|

22

|

|

Ned

Rand

|

Chief

Financial Officer

|

5

|

17

|

|

Darryl

Thomas

|

Liability

Group President / Chief Claims Officer

|

12

|

22

|

|

Hayes

Whiteside

|

Chief

Medical Officer

|

6

|

6

|

|

|

Average

|

11

|

21

|

|

Our

Team Understands Integration

|

|

Joined PRA

from Medical Assurance

|

|

Joined PRA

From Professionals Group

|

|

Joined PRA

after merger

|

Officers,

Directors & Employees Own ~9% of ProAssurance

23

Recent

M

& A

Transactions

24

Significant growth

in our core business

Geographical

expansion

Extends our core

business

Broadens our medically-related range

Geographical expansion

Broadens our medically-related range

Geographical expansion

Adds

to our lawyers’ book

Geographical

expansion

Affirms our

interest in this line

Extending

our Reach in MPL

Podiatry

Insurance Company of America (PICA)

Dominant

(70%), profitable, national company

~$96

million Direct Premium in 2008

Renewals

at expected levels in 2009

$13.7

million added to PRA premium in Q2 2009

Podiatry

is growing in importance as a specialty

Involved

in treating complications in a population with an

increasing prevalence of diabetes

increasing prevalence of diabetes

Increases

our understanding of policies that are

higher volume, lower cost

higher volume, lower cost

25

With

PICA We Are a National Carrier

Leveraging

the benefits of our many M &

A

transactions through

long-term customer relationships and local and specialty

knowledge

long-term customer relationships and local and specialty

knowledge

26

Corporate

Headquarters

Corporate

Headquarters

Claims

Offices

Claims

Offices

Claims

/ Underwriting Offices

Claims

/ Underwriting Offices

PICA

and/or E&S States

PICA

and/or E&S States

PICA

Headquarters

PICA

Headquarters

(Birmingham)

(Nashville)

Opening

New Avenues in MPL

Mid-Continent

General Agency

Large

writer of ancillary healthcare

Healthcare

reform will emphasize care delivery from a

larger array of lower-cost providers

larger array of lower-cost providers

Home

health care

Physician-extenders

~$26

million in total premium in 2008

$20

million healthcare related

PRA will

write most of this business

$3.6

million added to PRA premium in Q2 2009

Commission

derived from business we choose not to write

27

Adding

to our Legal E&O Book

Georgia

Lawyers Insurance Company

A leading

insurer of Georgia attorneys

2008

Premium: $5.7 million

Highlights

our desire to grow in this line

Sets the

stage for expansion in the southeast

Our

existing legal professional business is primarily in

the midwest

the midwest

Approximately

2,650 attorneys in 600 law firms

2008 Total

Legal E&O Premium: $7.8 million

New MGA’s

writing in the West and mid-Atlantic

28

ProAssurance

Growth Strategy

The legal

and regulatory environment must be

favorable

favorable

Understanding

why companies are available

Not all

M&A opportunities should be pursed

We don’t

“bet the farm” and can acquire

without “breaking the bank”

without “breaking the bank”

Ability to

use our stock in transactions

Attractive

because of strong book-value multiple

Cash flow

remains strong

29

30

ProAssurance

Growth Strategy

The

current market environment favors growth by

acquisition

acquisition

DE NOVO

GROWTH vs. GROWTH

BY ACQUISITION

DE NOVO

GROWTH vs. GROWTH

BY ACQUISITION

- Must

price your way into the market + Pricing

can be adjusted

- Must

price your way into the market + Pricing

can be adjusted

- No

prior history + Prior

history available

- No

prior history + Prior

history available

- Lack of

experienced personnel + Local

expertise available

- Lack of

experienced personnel + Local

expertise available

- Limited

access to key defense lawyers + Access

to proven defense lawyers

- Limited

access to key defense lawyers + Access

to proven defense lawyers

- Must

establish distribution + Utilize

existing distribution

- Must

establish distribution + Utilize

existing distribution

- Must

create brand awareness + Build on

existing relationships with

insureds and organized medicine, etc.

insureds and organized medicine, etc.

- Must

create brand awareness + Build on

existing relationships with

insureds and organized medicine, etc.

insureds and organized medicine, etc.

+ No

integration risk - Integration

risk

+ No

integration risk - Integration

risk

+ No

reserve risk - Reserve

risk—need for careful due diligence

+ No

reserve risk - Reserve

risk—need for careful due diligence

Financial

Highlights

2009

YTD Income Statement Highlights

32

in

millions, except per share data

Gross

Premiums Written $ 435

$ 374 $ 472

Net

Investment Income 113 122 158

Total

Revenue

489 431 567

Total

Expenses

295 294 470

Operating

Income $ 136 $ 127 207

Net

Income (Includes Investment Losses) $ 137 $ 101 178

Operating

Income/Diluted Share $ 2.50 $ 2.43 $ 6.07

September

30,

Year-End

2009 2008

2008

We

have reversed the decline in premiums with new

business from PICA, Mid-Continent and Georgia Lawyers

business from PICA, Mid-Continent and Georgia Lawyers

Strategy:

Enduring Financial Strength

33

Emphasizing

an appropriate balance of risk vs. return

Committed

to enduring balance sheet strength

Responding

to the low interest rate environment

Stockholder’s

Equity Up

Over 16% Since 12/31/07

Over 16% Since 12/31/07

Strategy:

Use Capital Prudently

Using

capital to build through M&A

Preserving

capital for future opportunities

Enhancing

shareholder value by repurchasing shares

at prices that build Book Value

at prices that build Book Value

34

Source: SNL

Financial

Our

Strong Capital/Low Leverage Position

35

(in

millions)

Prepared

for an

improving market

improving market

Prudent

capital

management

management

Premiums to

Surplus

for Each year

for Each year

$567

$

96 (PICA

pro

forma)

$471

Excess

Capital vs. Excess Capacity

36

Conceptual

Model of Projected

A. M. Best BCAR Scores if

A. M. Best BCAR Scores if

Premiums

Increase

Surplus

is Reduced

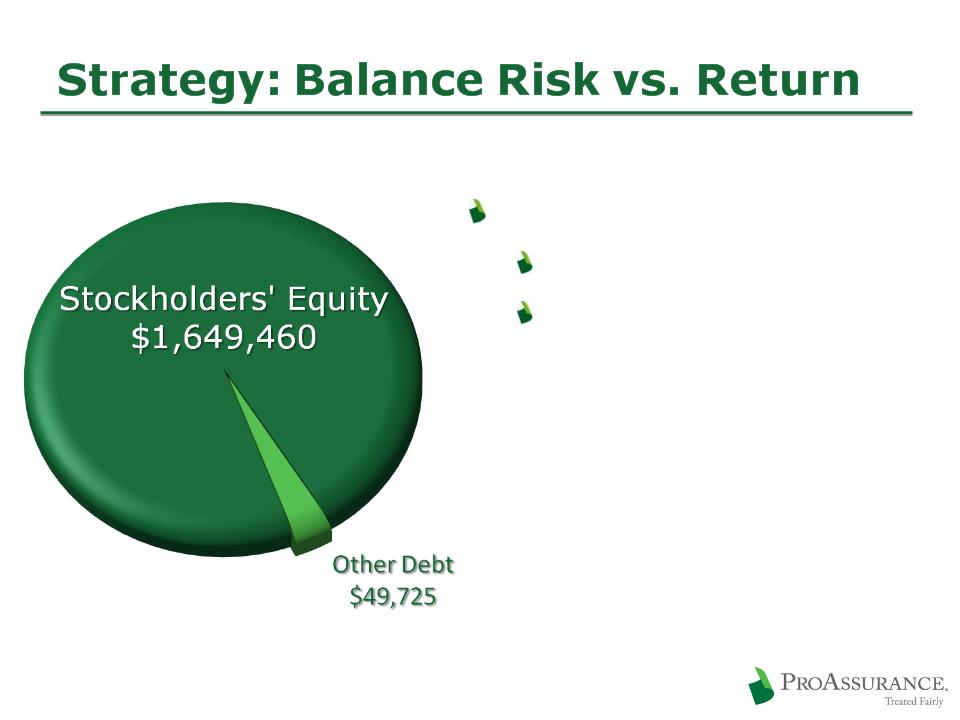

Strategy:

Balance Risk vs. Return

Key

Investment Actions in Q3 09

Reduced

cash and short-term

balances

balances

Added to

corporate bonds

CUSIP-level

portfolio disclosure

on our website:

www.proassurance.com/investorrelations/supplemental.aspx

on our website:

www.proassurance.com/investorrelations/supplemental.aspx

$3.9

Billion

Portfolio

Portfolio

$3.9

Billion

Portfolio

Portfolio

Fixed

Income: 91%

Short

Term: 4%

Short

Term: 4%

Equity

and Other Investments: 3%

Equity

and Other Investments: 3%

BOLI:

2%

BOLI:

2%

37

9/30/09

38

Little

Dependence on Debt

Low Debt

to Cap Ratio

Little

strain on cash flow

9/30/2009

Fixed

Income: $3.6 Billion

39

9/30/09

Summary

ProAssurance

Producing

sustainable shareholder value

Growing

Book Value per Share

Finding

the right M & A opportunities

Significant

share ownership at all levels

Focusing

on long-term

Preparing

for a changing market

Leveraging

financial strength

Protecting

the balance sheet

Maintain

our leading market position

Building

strength for the next cycle turn

41

Appendix:

Market Conditions

Current

Industry Status

43

Appendix:

Claims

Why

Claims Strategy Matters

Favorable

Outcomes:

84.0%

Outcomes:

84.0%

Favorable

Outcomes:

84.0%

Outcomes:

84.0%

Five

Year Average

2004 - 2008

2004 - 2008

Favorable

Outcomes:

75.4%

Outcomes:

75.4%

Favorable

Outcomes:

75.4%

Outcomes:

75.4%

Why

Claims Strategy Matters

Our

ability and willingness to defend claims

allows us to achieve better results

allows us to achieve better results

ProAssurance

vs. Industry

Average Statutory Loss Ratio

Average Statutory Loss Ratio

2003-2008

Legal

Payments

Payments

Loss

Payments

Payments

Trend

for ProAssurance

Stand Alone Statutory Loss Ratio

Stand Alone Statutory Loss Ratio

2006

- 2008

76.0%

*Source: A. M. Best

Aggregates & Averages, Medical Malpractice Predominating

64.3%

80.8%

76.9%

44.2%

Appendix:

Investments

Equities

& Other: $136 Million

48

9/30/09

Represents

3.5% of our Total Investments

Return

by Quarter: Equities & Other

49

Growth

in Investment vs. Reserves

50

Cumulative

Return: Equities & Other

51

Strategy:

Investment Discipline

The

choice: Chase yield or extend duration

We are

maintaining duration, looking for opportunities

52

Loss

in value assuming a 100 basis point shift in the yield curve

Yields based on

Single A composite corporate debt

Municipals:

$1.5 Billion

53

9/30/09

Investment

policy has always

required

investment grade rating prior to applying the

effect of insurance

investment grade rating prior to applying the

effect of insurance

Asset

Backed: $805 Million

Weighted

average rating: “AAA”

Bloomberg

Data

9/30/09

9/30/09

Alt-A

LTV 63%

LTV 63%

Prime

MBS

LTV 56%

LTV 56%

Further Details

Provided

on Sub-Prime and CMBS

on following pages

on Sub-Prime and CMBS

on following pages

54

Sub-Prime

Detail

55

$6.7

million market value in AFS portfolio

$4.2

million unrealized loss

$9.6

million market value in

high-yield LP rated B

high-yield LP rated B

LP’s focus

is distressed ABS

|

At

9/30/09

|

Vintage

|

|

$4.8

Mln

|

2004 &

Prior

|

|

$1.9

Mln

|

2005

|

Quality &

Vintage information only on direct holdings at 9/30/09

|

At

9/30/09

|

Type

|

Quality

|

|

$2.9

Mln

|

Mortgage-Backed

|

AA avg -

LTV 68%

|

|

$3.8

Mln

|

Home

Equity

|

A+

avg

|

CMBS

Detail

Vintages

2005 &

Prior- $136 million

2006- $23

million

2007- $3

million

Top

Property Types

Retail-Anchored:

45% of CMBS portfolio

Exposure:

19% - 44% of underlying occupancies

Office:

44% of CMBS portfolio

Exposure:

23% - 49% of

underlying occupancies

Multi

Family: 4% of CMBS portfolio

Mixed Use:

3% of CMBS portfolio

Other: 4%

of CMBS Portfolio

56

CMBS

Detail

$162

million Fair Value in non-agency CMBS

Book

Value: $164 million

5% of

fixed income portfolio

57

|

At

9/30/09

|

Quality

|

|

$160

Mln

|

AAA

|

|

$ 2.0

Mln |

AA

|

|

At

9/30/09

|

Wtd

Avg LTV

|

|

24%

|

<65%

|

|

43%

|

=65-70%

|

|

21%

|

<70-75%

|

|

12%

|

=75-85%

|

|

At

9/30/09

|

Credit

Support

|

|

26%

|

>30%

|

|

52%

|

20% -

30%

|

|

20%

|

10% -

20%

|

|

2%

|

Less than

10%

|

|

At

9/30/09

|

Deal

Cumulative Delinquencies

|

|

27%

|

0% -

0.5%

|

|

3%

|

0.5% -

1.0%

|

|

32%

|

1.0% -

2.0%

|

|

4%

|

2.0% -

3.0%

|

|

22%

|

3.0%-5.0%

|

|

12%

|

5.0%-9.0%

|

|

At 9/30/09

|

Debt

Service Coverage

|

|

69%

|

=>1.5x

|

|

25%

|

1.4x-1.5x

|

|

6%

|

1.3x-1.4x

|

AT

9/30/09

9/30/09

CMBS

Since September 30, 2009

Since

9/30/09:

Sold $50.0

million CMBS

Paydowns

of $8.0 million

As of

November 30, 2009 CMBS:

Market

value: $108

million

Book

value: $110

million

Expecting

pay down of $19 million

by year-end 2009

by year-end 2009

Projecting

~$90 million exposure at year-end

58

Corporates:

$1.0 Billion

59

9/30/09

Corporate:

Detail on Financials

Top 20

Largest Banks/Financials: $ 294 million

$75 mm

FDIC backing

|

BA $44

($23)

|

BNY Mellon

$10

|

|

MS $27

($6)

|

Credit

Suisse $9

|

|

BP Cap

$25

|

Eurohypo

$8

|

|

GECC $25

($8)

|

KEY $6

($6)

|

|

JPM $24

($14)

|

NRUC

$6

|

|

CITI $20

($7)

|

Deutsche

Bank $5

|

|

Wells

$20

|

FMCC

$5

|

|

GS $16

($2)

|

NY Commt’y

Bank $5 ($5)

|

|

PNC $15

($2)

|

Depfa ACS

Covered $5

|

|

Amex

$14

|

John Deere

Cap $5 ($2)

|

|

FDIC backed

amounts listed in parentheses

|

|

60

9/30/2009

Treasury/GSE:

$228 Million

9/30/09

62

9/30/09

Portfolio

Overview: Short Term

$138

Million

Rated

A1/P1 or better

Money

Markets:

Moody’s:

Aaa

S&P:

AAA

63

BOLI:

$65 Million

Weighted

average rating

Moody’s:

AA3

S&P:

AA

A. M.

Best: A+

64

Appendix:

Industry History

Appendix:

Growth Maps