Attached files

| file | filename |

|---|---|

| EX-31.1 - 6D Global Technologies, Inc | v167783_ex31-1.htm |

| EX-32.1 - 6D Global Technologies, Inc | v167783_ex32-1.htm |

UNITED

STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C.

20549

Form 10-K

(Mark

One)

|

þ

|

ANNUAL

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

|

For

the fiscal year ended August 31, 2009

OR

|

o

|

TRANSITION

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

|

For

the transition period

from to

Commission

file number 000-53511

EVERTON

CAPITAL CORPORATION

(Exact

Name of Registrant as Specified in Its Charter)

|

Nevada

|

|

(State

or Other Jurisdiction of

Incorporation

or Organization)

|

603,

Unit 3, DongFeng South Road, NaShiLiJu 34,

ChaoYang

District, Beijing, China 100016

(Address

of Principal Executive Offices) (Zip Code)

01 391 146 5973

(PRC)

(631)

458-0540 (USA)

(Registrant's

telephone number, including area code)

Copies

to:

Robert

Newman, Esq.

The

Newman Law Firm, PLLC

14 Wall

Street, 20th Floor

New York,

NY 10005

Tel.

(212) 227-7422 Fax. (212) 202-6055

Securities

registered pursuant to Section 12(g) of the Act:

|

Title

of Each Class:

|

|

Common

Stock, par value $0.00001 per share

|

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in

Rule 405 of the Securities Act. Yes o No þ

Indicate

by check mark if the registrant is not required to file reports pursuant to

Section 13 or Section 15(d) of the Act. Yes o No þ

Indicate

by check mark whether the registrant: (1) has filed all reports required to

be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934, as

amended (“Exchange Act”) during the preceding 12 months (or for such

shorter period that the registrant was required to file such reports), and

(2) has been subject to such filing requirements for the past

90 days. Yes þ No o

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K is not contained herein, and will not be contained, to the

best of registrant’s knowledge, in definitive proxy or information statements

incorporated by reference in Part III of this Form 10-K or any

amendment to this Form 10-K. o

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer, or a smaller reporting company. See

the definitions of “large accelerated filer,” “accelerated filer” and “smaller

reporting company” in Rule 12b-2 of the Exchange Act. (Check

one):

|

Large

accelerated

filer o

|

Accelerated

filer o

|

Non-accelerated

filer o

|

Smaller

reporting

company þ

|

|||

|

(Do

not check if a smaller reporting

company)

|

State the

aggregate market value of the voting and non-voting common equity held by

non-affiliates computed by reference to the price at which the common equity was

sold, or the average bid and asked price of such common equity, as of February 28, 2009:

$0.00

DOCUMENTS

INCORPORATED BY REFERENCE:

None.

EVERTON

CAPITAL CORPORATION

(AN

EXPLORATION STAGE COMPANY)

ANNUAL

REPORT ON FORM 10-K

FOR

THE FISCAL YEAR ENDED AUGUST 31, 2009

TABLE

OF CONTENTS

|

Page

|

||

|

PART

I

|

||

|

Item

1.

|

Business

|

1

|

|

Item

1A.

|

Risk

Factors

|

8

|

|

Item

1B.

|

Unresolved

Staff Comments

|

8

|

|

Item

2.

|

Properties

|

8

|

|

Item

3.

|

Legal

Proceedings

|

8

|

|

Item

4.

|

Submission

of Matters to a Vote of Security Holders

|

8

|

|

PART II

|

||

|

Item

5.

|

Market

for Registrant’s Common Equity, Related Stockholder Matters and Issuer

Purchases of Equity Securities

|

8

|

|

Item

6.

|

Selected

Financial Data

|

10

|

|

Item

7.

|

Management’s

Discussion and Analysis of Financial Condition and Results of

Operations

|

10

|

|

Item

7A.

|

Quantitative

and Qualitative Disclosures About Market Risk

|

13

|

|

Item

8.

|

Financial

Statements and Supplementary Data

|

14

|

|

Item

9.

|

Changes

in and Disagreements with Accountants on Accounting and Financial

Disclosure

|

14

|

|

Item

9A(T).

|

Controls

and Procedures

|

14

|

|

Item

9B.

|

Other

Information

|

15

|

|

PART III

|

||

|

Item

10

|

Directors,

Executive Officers and Corporate Governance

|

15

|

|

Item

11

|

Executive

Compensation

|

18

|

|

Item

12

|

Security

Ownership of Certain Beneficial Owners and Management and Related

Stockholder Matters

|

20

|

|

Item

13

|

Certain

Relationships and Related Transactions, and Director

Independence

|

20

|

|

Item

14

|

Principal

Accountant Fees and Services

|

21

|

|

PART IV

|

||

|

Item

15.

|

Exhibits

and Financial Statement Schedules

|

22

|

|

Signatures

|

23

|

ITEM

1. BUSINESS

General

We were

incorporated in the State of Nevada on May 9, 2006. We are an exploration stage

company, but currently the Company’s management is evaluating options, including

looking for new business opportunities, which may include a change of control of

the Company. An exploration stage corporation is one engaged in the search for

mineral deposits or reserves which are not in either the development or

production stage. We maintain our statutory registered agent's office at 603,

Unit 3, DongFeng South Road, NaShiLiJu 34, ChaoYang District, Beijing, China

100016. Our telephone numbers are 01-391-146-5973 (PRC) and 631-458-0540

(US).

We have

no revenues, have achieved losses since inception, have no operations, have been

issued a going concern opinion and rely upon the sale of our securities to fund

operations.

Background

In May

2006, Maryna Bilynska, our former president, acquired one mineral property in

trust for us, containing one mining claim in British Columbia, Canada. The

property was staked by Lloyd Brewer. Mr. Brewer was paid $2,500 to stake the

claims. Mr. Brewer is a staking agent located in Vancouver British

Columbia.

Canadian

jurisdictions allow a mineral explorer to claim a portion of available Crown

lands as its exclusive area for exploration by depositing posts or other visible

markers to indicate a claimed area. The process of posting the area is known as

staking. Ms. Bilynska paid Mr. Brewer $2,500 to stake the claims. The claims

were transferred to Ms. Bilynska. The claim was recorded in Ms. Bilynska’s name

to avoid paying additional fees. Ms. Bilynska did not provide us with a signed

or executed bill of sale in our favor. Ms. Bilynska was to issue a bill of sale

to a subsidiary corporation to be formed by us should economically recoverable

mineralized material have been discovered on the property. Mineralized material

is a mineralized body which has been delineated by appropriate spaced drilling

or underground sampling to support sufficient tonnage and average grade of

metals to justify removal.

All

Canadian lands and minerals which have not been granted to private persons are

owned by either the federal or provincial governments in the name of Her

Majesty. Ungranted minerals are commonly known as Crown minerals. Ownership

rights to Crown minerals are vested by the Canadian Constitution in the province

where the minerals are located.

In the

nineteenth century the practice of reserving the minerals from fee simple Crown

grants was established. Legislation now ensures that minerals are reserved from

Crown land dispositions. The result is that the Crown is the largest mineral

owner in Canada, both as the fee simple owner of Crown lands and through mineral

reservations in Crown grants. Most privately held mineral titles are acquired

directly from the Crown. The Company’s property was one such acquisition.

Accordingly, fee simple title to the property resides with the

Crown.

The

claims were mining leases issued pursuant to the British Columbia Mineral Act.

The lease had exclusive rights to mine and recover all of the minerals contained

within the surface boundaries of the lease continued vertically downward. The

lease included the right to use the surface for all operations reasonably

related to the exploration operations. There were no native land claims

that affected title to the property.

1

Claims

The

following was the tenure number, claim, date of recording and expiration date of

the claim:

|

|

|

Number of

|

Date of

|

|||

|

Claim No.

|

Document Description

|

Cells

|

Expiration

|

|||

|

521315

|

Jade

Mine

|

9

|

January

18,

2009

|

The

claims were for approximately 460 acres.

In order

to maintain the claims Ms. Bilynska had to pay a fee of CDN$100 per year per

claim. Ms. Bilynska could have renewed the claim indefinitely. The

property was selected because Mr. Brewer advised us that jade was discovered on

an other property nearby. No technical information was used to select the

property.

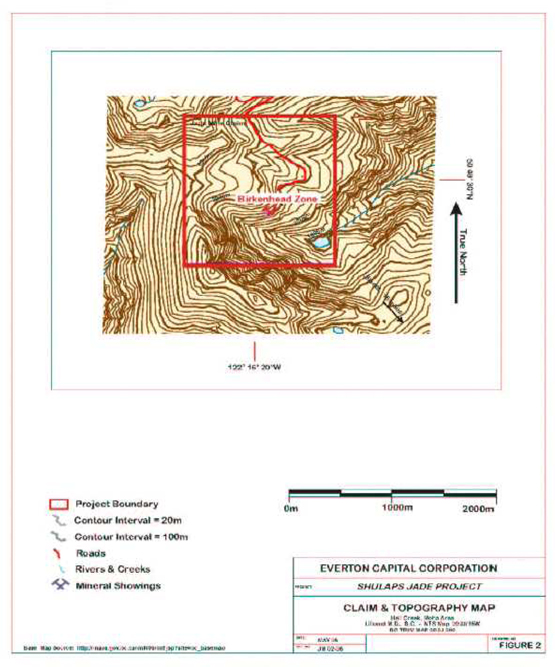

Location

and Access

The

property is located within the southwestern area of British Columbia, Canada,

approximately 125 miles northeast of Vancouver, near the town site of Moha. The

town of Lillooet lies 16 miles to the southeast of the property.

The

property is in the Lillooet Mining Division, and is centered at approximately

50o49'30"N latitude and 122o16'20"W longitude on NTS Map Sheet 092J/16W,

alternatively on BC TRIM map 092J 089.

The

property can be accessed from Lillooet by following the Bridge River Road to the

town site of Moha, at this point turn north onto the Yalakom River Road. Follow

this road for approximately 8 miles, at which point a rough four-wheel drive

road branches from the Yalakom River Road. This road leads to, and terminates

at, the property.

2

Map

1

3

Map

2

Physiography

The

property is located on the southern end of the Shulaps Mountain Range within the

Coast Mountain Physiographic Region. The property covers the ridge, and the

southern slope of the ridge, that forms the height of land from which Hell Creek

originates. Elevations within the claims range from 6,200 feet to 7,700 feet.

The lower elevation of 6,200 feet is located within southeastern corner of the

property. The highest elevation of 7,700 feet is located northwestern quadrant

of the property. The main area of interest within the project is located at

6,900 feet at the approximate center of the property.

4

Slopes

within the property area are moderate to steep throughout the property. Areas

within the property that are above the 6,800 foot level are above the tree line

and vegetation is limited to alpine grass, lichen and moss. Vegetation below

this level consists primarily of stunted sub-alpine fir and pine

trees

The local

climate features warm summers having an average mean summer temperature of

60oF

and cold winters having an average mean winter temperature of -5oF. The

Shulaps Jade area is fairly dry in the summer and a heavy snow pack is present

through the winter months. The average yearly precipitation (rain) as calculated

from a 30-year period is 30 inches. A snow pack of approximately ten feet begins

to accumulate in mid November and lingers in places into mid May. The

recommended field season for initial phases of exploration is from mid May to

early November. Drilling can be carried out on a year-round basis with the aid

of a bulldozer, or other snow removal equipment, to keep access roads snow-free

although it would be more practical and cost effective to conduct all

exploration and development of the zone to the snow-free period of the

year.

Ample

water to support all phases of exploration and development is available from

small lake at the headwaters of Hell Creek. Power requirements for future

development is available as two high-voltage (40kW) transmission line located

approximately 3 miles south of the Project. Gas or diesel powered generators

would be required to provide any electrical power requirements during the

exploration stage.

Regional

Geology

The

property is located on the eastern flank of the Coast Crystalline Plutonic

Complex, a major intrusive region of the Canadian Cordillera bounded by

Intermontaine Belt on the east and the Insular Belt on the west.

The

regional geology comprises a package of highly deformed lithological units

structurally enclosed between two major northwesterly striking dextral fault

structures – the Yalakom Fault on the east and the Marshall Creek Fault on the

west. Northeasterly trending Astress” faults occur between the two

aforementioned faults throughout the length of the Shulaps Mountain

Range.

Three

major assemblages occur within the area of interest.

Shulaps

Ultramafic Complex

The

oldest rock unit in the Shulaps Range is the pre-middle Cretaceous age Shulaps

Ultramafic Complex that is interpreted as dismembered ophiolite structurally

stacked by thrust faulting.

Foliation is parallel or sub-parallel to thrust planes or composition

planes. Sedimentary inclusions and adjacent metasediments often have bedding

parallel to the foliation within the serpentinite. The complex is a serpentinite

mélange unit that represents ancient oceanic floor composed of serpentinite

derived from ultramafic cumulates with knockers of ultramafic rocks, gabbro,

diorite, pillowed and massive greenstone, chert, phyllite, limestone, sandstone

and conglomerate.

Bridge

River Complex

The

predominantly oceanic rocks of the Permian to Jurassic Bridge River Group

consist of ribbon chert, argillite, pillowed to massive greenstone, with lesser

amounts of limestone, gabbro, diabase, chert, volcanic greywacke, pebble

conglomerate and serpentinite. The Bridge River Group rocks have been highly

metamorphosed. Locally, the most common rock types are phyllite (siltstone),

chert, argillite, schist and minor limestone.

Intrusive

Rocks – Rexmount Porphyry

The

Rexmount Porphyry is a light grey weathered rock consisting of phenocrysts of

plagioclase, hornblende, biotite and quartz set in a fine grained or aphanitic

felsic groundmass. The porphyry, which is interpreted as being the intrusive

equivalent of the dacite volcanics, occasionally contains laminations of

epidote-chlorite parallel to the contact. Whether this is an alteration or a

flow layering is not known.

5

Property

Geology and Mineralization

Jade

outcrops at the head of Hell Creek, a northeasterly flowing tributary of the

Bridge River. The mass of jade is fault bounded by serpentine of the Permian and

older Shulaps Ultramafic Complex on the west and by slightly metamorphosed

argillaceous sediments of the Mississippian to Jurassic age Bridge River Complex

on the east.

The

tabular shaped mass is 8 feet wide and trends northwest for 980 feet to where it

is cut by a granitic intrusion. The body remains open to the

southeast.

The east

contact is bordered by a 1-foot wide talc zone. Cross fractures pervade the

jade, trending 065 degrees and plunging 70 degrees southeast.

The jade

is described as good to fair quality, the quality being decreased by the

presence of coarse tremolite patches, talc and opaque minerals.

History

of Previous Work

There was no evidence of previous exploration of the property.

Our

Proposed Exploration Program

We were

prospecting for jade. Our target was mineralized material. Our success depended

upon finding economically recoverable mineralized material. Mineralized material

is a mineralized body which has been delineated by appropriate spaced drilling

or underground sampling to support sufficient tonnage and average grade of

metals to justify removal. Upon commencement, we did not know if we

would have found mineralized material. We do not claim to have any minerals

or reserves whatsoever at this time on any of the property.

We

intended to implement an exploration program which consisted of core sampling.

Core sampling is the process of drilling holes to a depth of up to 1,400 feet in

order to extract a samples of earth. Ms. Bilynska determined where drilling

would occur on the property in consultation with the consultant. Ms. Bilynska

did not receive fees, salary, or other compensation for her services. The

samples were to be tested to determine if mineralized material were located on

the property.

Competitive

Factors

The jade

mining industry is fragmented. We competed with other exploration companies

looking for jade. We were one of the smallest exploration companies in

existence. We were an infinitely small participant in the jade mining market.

While we competed with other exploration companies, there was no competition for

the exploration or removal or mineral from the property. Readily available jade

markets exist in Canada and around the world for the sale of jade. Therefore, we

would have been able to sell any jade that we were able to recover.

Regulations

Our

mineral exploration program was subject to the Canadian Mineral Tenure Act

Regulation. This act sets forth rules for

|

*

|

locating

claims

|

|

*

|

posting

claims

|

|

*

|

working

claims

|

|

*

|

reporting

work performed

|

6

We were

also subject to the British Columbia Mineral Exploration Code which tells us how

and where we can explore for minerals. Compliance with these rules and

regulations did not adversely affect our operations.

Environmental

Law

We were

also subject to the Health, Safety and Reclamation Code for Mines in British

Columbia. This code deals with environmental matters relating to the exploration

and development of mining properties. Its goals are to protect the environment

through a series of regulations affecting:

|

1.

|

Health

and Safety

|

|

2.

|

Archaeological

Sites

|

|

3.

|

Exploration

Access

|

We were

responsible to provide a safe working environment, not disrupt archaeological

sites, and conduct our activities to prevent unnecessary damage to the

property.

We are in

compliance with the act and will continue to comply with the act in the future.

We believe that compliance with the act will not adversely affect our business

operations in the future.

Employees

We

intended to use the services of subcontractors for manual labor exploration work

on our properties. Ms. Bilynska handled our administrative duties. Because our

former sole officer and director was inexperienced with exploration, she hired

independent contractors to perform the surveying of the property. We cannot

determine at this time the precise number of people we will retain in employ of

the Company.

Employees

and Employment Agreements

We have

one employee, Jonathan Woo, our sole officer and director. Mr. Woo devotes

approximately 10% of his time or four hours per week to our operations. Mr. Woo

does not have an employment agreement with us. We presently do not have pension,

health, annuity, insurance, stock options, profit sharing or similar benefit

plans; however, we may adopt plans in the future.

Recent

Developments

Everton

has recently determined that this property contains reserves that are not

economically recoverable. The recoverability of amounts from the property was

dependent upon the discovery of economically recoverable reserves, confirmation

of Everton’s interest in the underlying property, the ability of Everton to

obtain necessary financing to satisfy the expenditure requirements under the

property agreement and to complete the development of the property and upon

future profitable production or proceeds for the sale thereof. The

Company was advised by Madman Mining, its consultant, that "Due to the shattered

nature of the jade/nephrite material present (due to previous blasting), and the

numerous amount of inclusions (of talc) within the matrix of the jade itself, it

is recommended that no further exploration be conducted on this project and that

the project should be dropped." The Company’s management is evaluating

options, including looking for new business opportunities, which may include a

change of control of the Company.

Pursuant

to a Majority Stock Purchase Agreement (MSPA) dated April 23, 2009, the

Company’s former majority stockholder and officer sold to an individual

5,000,000 shares of the Company’s common stock, for $25,000; former majority

stockholder agreed to assume and be liable for any and all liabilities and

obligations of Everton that were occurred prior to closing of the stock

purchase. Pursuant to the terms of the MSPA and effective as of the closing

of the transactions contemplated by the MSPA, the new shareholder owns 5,000,000

shares of the Company’s common stock out of a total of 5,501,000

shares issued and outstanding, or 90.89%.

7

ITEM

1A. RISK FACTORS

We are a

smaller reporting company as defined by Rule 12b-2 of the Exchange Act and are

not required to provide the information under this item.

ITEM

1B. UNRESOLVED STAFF COMMENTS

None.

ITEM

2. PROPERTIES

We

do not own any property.

ITEM

3. LEGAL PROCEEDINGS

We are

not presently a party to any litigation.

ITEM

4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY

HOLDERS

During the fourth quarter of our fiscal

year, there were no matters submitted to a vote of our

shareholders.

PART

II

ITEM

5. MARKET FOR COMMON STOCK AND RELATED STOCKHOLDER

MATTERS

Our stock

was listed for trading on the Bulletin Board operated the Financial Industry

Regulatory Authority (FINRA) on October 23, 2008 under the symbol “EVCP”.

However, during the fiscal year ended August 31, 2009, no trades of our common

stock occurred through the facilities of the OTC Bulletin Board.

The

quotations on the OTC Bulletin Board reflect inter-dealer prices, without retail

mark-up, mark-down, or commissions and may not represent actual

transactions.

There are

no outstanding options or warrants to purchase, or securities convertible into,

our common stock.

|

Fiscal

Year

|

||||||||

|

2009

|

High Bid

|

Low Bid

|

||||||

|

Fourth

Quarter: 6/1/09 to 8/31/09

|

$ | 0.00 | $ | 0.00 | ||||

|

Third

Quarter: 3/1/09 to 5/31/09

|

$ | 0.00 | $ | 0.00 | ||||

|

Second

Quarter: 12/1/08 to 2/28 /09

|

$ | 0.00 | $ | 0.00 | ||||

|

First

Quarter: 9/1/08 to 11/30/08

|

$ | 0.00 | $ | 0.00 | ||||

|

Fiscal

Year

|

||||||||

|

2008

|

High Bid

|

Low Bid

|

||||||

|

Fourth

Quarter: 6/1/08 to 8/31/08

|

$ | 0.00 | $ | 0.00 | ||||

|

Third

Quarter: 3/1/08 to 5/31/08

|

$ | 0.00 | $ | 0.00 | ||||

|

Second

Quarter: 10/1/07 to 2/29/08

|

$ | 0.00 | $ | 0.00 | ||||

|

First

Quarter: 7/1/07 to 9/30/07

|

$ | 0.00 | $ | 0.00 | ||||

8

Holders

On August

31, 2009, we had 47 shareholders of record of our common stock.

Dividend

Policy

We have

not declared any cash dividends. We do not intend to pay dividends in the

foreseeable future, but rather plan to reinvest earnings, if any, in our

business operations.

Section

15(g) of the Securities Exchange Act of 1934

Our

shares are covered by section 15(g) of the Securities Exchange Act of 1934, as

amended that imposes additional sales practice requirements on broker/dealers

who sell such securities to persons other than established customers and

accredited investors (generally institutions with assets in excess of $5,000,000

or individuals with net worth in excess of $1,000,000 or annual income exceeding

$200,000 or $300,000 jointly with their spouses). For transactions covered by

the Rule, the broker/dealer must make a special suitability determination for

the purchase and have received the purchaser's written agreement to the

transaction prior to the sale. Consequently, the Rule may affect the ability of

broker/dealers to sell our securities and also may affect your ability to sell

your shares in the secondary market.

Section

15(g) also imposes additional sales practice requirements on broker/dealers who

sell penny securities. These rules require a one page summary of certain

essential items. The items include the risk of investing in penny stocks in both

public offerings and secondary marketing; terms important to in understanding of

the function of the penny stock market, such as id and offer quotes, a dealers

spread and broker/dealer compensation; the broker/dealer compensation, the

broker/dealers duties to its customers, including the disclosures required by

any other penny stock disclosure rules; the customers rights and remedies in

causes of fraud in penny stock transactions; and, the FINRA’s toll free

telephone number and the central number of the North American Administrators

Association, for information on the disciplinary history of broker/dealers and

their associated persons.

Securities

Authorized for Issuance Under Equity Compensation Plans

We have

no equity compensation plans and accordingly we have no shares authorized for

issuance under an equity compensation plan.

Use

of Proceeds

On

August, 2008, we completed our public offering of shares of common stock. SEC

File No. 333-138995, effective December 18, 2007. There was no underwriter

involved in our public offering. We sold 501,000 shares of common stock and

raised $50,100. Since completing our public offering, we spent the proceeds as

follows:

9

|

Everton

Capital Corporation

|

||||

|

Use

of Proceeds

|

||||

|

August

31, 2009

|

||||

|

Bank

service charge

|

548 | |||

|

Stock

transfer

|

11,839 | |||

|

Project

advance

|

10,000 | |||

|

Office

|

2,892 | |||

|

Legal/Accounting

|

16,142 | |||

|

Rent

|

6,263 | |||

|

Working

Capital

|

2,417 | |||

|

TOTAL

|

50,100 | |||

ITEM

6. SELECTED FINANCIAL DATA

We are a

smaller reporting company as defined by Rule 12b-2 of the Exchange Act and are

not required to provide the information under this item.

ITEM

7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS.

This

Annual Report on Form 10-K includes forward-looking statements within

the meaning of Section 27A of the Securities Act of 1933, as amended, and

Section 21E of the Securities Exchange Act of 1934, as amended. We

have based these forward-looking statements on our current expectations and

projections about future events. These forward-looking statements are

subject to known and unknown risks, uncertainties and assumptions about us that

may cause our actual results, levels of activity, performance or achievements to

be materially different from any future results, levels of activity, performance

or achievements expressed or implied by such forward-looking

statements. In some cases, you can identify forward-looking

statements by terminology such as “may,” “will,” “should,” “could,” “would,”

“expect,” “plan,” anticipate,” believe,” estimate,” continue,” or the negative

of such terms or other similar expressions. The following discussion

should be read in conjunction with our Financial Statements and related Notes

thereto included elsewhere in this report. Throughout this Annual Report we will

refer to Everton Capital Corporation as "Everton," the "Company,"

"we," "us," and "our."

Plan of Operation

We are a

start-up, exploration stage corporation, but currently the Company’s management

is evaluating options, including looking for new business opportunities, which

may include a change in control of the Company. We have not yet generated or

realized any revenues from our business operations.

In May

2006, Maryna Bilynska, our former president, acquired one mineral property in

trust for us, containing one mining claim in British Columbia, Canada. The

property was staked by Lloyd Brewer. Mr. Brewer was paid $2,500 to stake the

claims. Mr. Brewer is a staking agent located in Vancouver British

Columbia.

We

conducted research in the form of exploration of the property. An exploration

stage corporation is one engaged in the search for mineral deposits or reserves

which are not in either the development or production stage.

There is

substantial doubt we can continue as an on-going business for the next twelve

months unless we obtain additional capital to pay our bills. This is because we

have not generated any revenues and no revenues are anticipated. If we can’t or

don’t raise more money, we will cease operations. We do not intend to

hire additional employees at this time. We are not going to buy or sell any

plant or significant equipment during the next twelve months

10

Milestones

Everton

completed Phase 1A exploration stage on the property in August 2008 and was

advised by Madman Mining, its consultant, that "Due to the shattered nature of

the jade/nephrite material present (due to previous blasting), and the numerous

amount of inclusions (of talc) within the matrix of the jade itself, it is

recommended that no further exploration be conducted on this project and that

the project should be dropped." Our management is looking for new

business opportunities, which may include a change of control of the

Company.

On April

23, 2009, the Company’s former majority stockholder sold an individual 5,000,000

shares of the Company’s common stock for $25,000 pursuant to a Majority Stock

Purchase Agreement (MSPA); former majority stockholder agreed to assume and be

liable for any and all liabilities and obligations of Everton occurred prior to

the stock purchase transaction. Pursuant to the terms of the MSPA and

effective as of the closing of the transactions contemplated by the MSPA, the

new shareholder owns 5,000,000 shares of the Company’s common stock out of

5,501,000 shares issued and outstanding, or approximately

90.89%.

Limited

Operating History; Need for Additional Capital

There is

no historical financial information about us upon which to base an evaluation of

our performance. We are an exploration stage corporation and have not generated

any revenues from operations. We cannot guarantee we will be successful in our

business operations. Our business is subject to risks inherent in the

establishment of a new business enterprise, including limited capital

resources.

Results

of Operations

From

Inception on May 10, 2006

The

Shulaps jade project is located approximately 25 kilometers from Lillooet,

southwestern British Columbia. The jade project is on the southeastern extension

of the Shulaps Range just north of Carpenter Lake. Access to the property is

reached by gravel road along the Yalakom River. A turn off just past La Rochelle

Creek leads to the head waters Hell Creek, the location of Jade project. Access

to the project can also be reached by helicopter, 20 min flight one

way.

In August 2008 we obtained samples from the property and identified the location

of Jade outcrops.

The

landing site for the helicopter was beside an old cabin in a flat area at

approximately 551390E 5630890N 2100 m zone 10. The afternoon of the 30th was

spent walking southeast of the cabin along the road. A number of trenches were

found along the road cut but no exposed outcrops of Jade were observed. The road

however switch backed between the serpentine of the Permian and older Shulaps

Ultramafic complex on the west and the metamorphosed argillaceous sediments of

the Mississippian to Jurassic age Bridge River Complex on the east. The

ultramafic complex is light green to black with variable degrees of hardness.

The Bridge River complex is dark brown to rusty red with obvious sedimentary

layering. The contact between the two units is typically buried by overburden

but can be identified to within 5 m.

Three

samples, obtained using a diamond bladed generated powered rock saw, were taken

from boulders that contained talc, serpentine and variable amounts of

Jade.

Due to

the shattered nature of the jade/nephrite material present (due to previous

blasting), and the numerous amount of inclusions (of talc) within the matrix of

the jade itself, Madman recommended that no further exploration be conducted on

this project and that the project should be dropped.

During

the period of December 1, 2008 through August 31, 2009, no activity was

conducted on the property.

11

Since

inception, Maryna Bilynska, our former sole officer and director paid all our

expenses to stake the property, to incorporate us, and for legal and accounting

expenses. Net cash provided by Ms. Bilynska from inception on May 10, 2006 to

August 31, 2009 was $43,654.

Liquidity and Capital

Resources

We do not

have sufficient cash to operate for the next 12 months. The Company’s management

is currently evaluating options, including looking for new business

opportunities, which may include a change of control of the Company.

Our

former sole officer and director loaned us money for our operations as needed

prior to consummation of the Majority Stock Purchase Agreement dated April 23,

2009. At the present time, we have not made any arrangements to raise additional

cash. If we need additional cash and can't raise it we will either have to

suspend operations until we do raise the cash, or cease operations

entirely.

As of the

date of this report, we have yet to begin operations and therefore we have not

generated any revenues from our business operations.

In July

2006, we issued 5,000,000 shares of common stock to Maryna Bilynska, our sole

officer and director, pursuant the exemption from registration contained in

Regulation S of the Securities Act of 1933. This was accounted for as a purchase

of shares of common stock, in consideration of $50.

In

August, 2008, we completed our public offering by selling 501,000 shares of

common stock and raising $50,100.

On April

23, 2009, Ms. Bilynska sold her 5,000,000 shares to an individual for

$25,000. Ms. Bilynska assumed all the liabilities and obligation that

occurred prior to the stock purchase transaction.

Recent

accounting pronouncements

On July

1, 2009, the Company adopted Accounting Standards Update (“ASU”) No.

2009-01, “Topic 105 - Generally Accepted Accounting Principles - amendments

based on Statement of Financial Accounting Standards No. 168 , “The FASB

Accounting Standards Codification™ and the Hierarchy of Generally Accepted

Accounting Principles” (“ASU No. 2009-01”). ASU No. 2009-01

re-defines authoritative GAAP for nongovernmental entities to be only comprised

of the FASB Accounting Standards Codification™ (“Codification”) and, for SEC

registrants, guidance issued by the SEC. The Codification is a

reorganization and compilation of all then-existing authoritative GAAP for

nongovernmental entities, except for guidance issued by the SEC. The

Codification is amended to effect non-SEC changes to authoritative

GAAP. Adoption of ASU No. 2009-01 only changed the referencing

convention of GAAP in Notes to the Consolidated Financial

Statements.

In June

2009, the Financial Accounting Standards Board (“FASB”) issued SFAS No. 167,

“Amendments to FASB Interpretation No. 46(R)” (“SFAS 167”), codified as FASB ASC

Topic 810-10, which modifies how a company determines when an entity that is

insufficiently capitalized or is not controlled through voting (or similar

rights) should be consolidated. SFAS 167 clarifies that the determination of

whether a company is required to consolidate an entity is based on, among other

things, an entity’s purpose and design and a company’s ability to direct the

activities of the entity that most significantly impact the entity’s economic

performance. SFAS 167 requires an ongoing reassessment of whether a company is

the primary beneficiary of a variable interest entity. SFAS 167 also requires

additional disclosures about a company’s involvement in variable interest

entities and any significant changes in risk exposure due to that involvement.

SFAS 167 is effective for fiscal years beginning after November 15, 2009. The

Company does not believe the adoption of SFAS 167 will have an impact on its

financial condition, results of operations or cash flows.

In June

2009, the FASB issued SFAS No. 166, “Accounting for Transfers of Financial

Assets — an amendment of FASB Statement No. 140” (“SFAS 166”), codified as FASB

Topic ASC 860, which requires entities to provide more information regarding

sales of securitized financial assets and similar transactions, particularly if

the entity has continuing exposure to the risks related to transferred financial

assets. SFAS 166 eliminates the concept of a “qualifying special-purpose

entity,” changes the requirements for derecognizing financial assets and

requires additional disclosures. SFAS 166 is effective for fiscal years

beginning after November 15, 2009. The Company does not believe the adoption of

SFAS 166 will have an impact on its financial condition, results of operations

or cash flows.

12

In May

2009, the FASB issued SFAS No. 165, “Subsequent Events” (“SFAS 165”) codified in

FASB ASC Topic 855-10-05, which provides guidance to establish general standards

of accounting for and disclosures of events that occur after the balance sheet

date but before financial statements are issued or are available to be issued.

SFAS 165 also requires entities to disclose the date through which subsequent

events were evaluated as well as the rationale for why that date was selected.

SFAS 165 is effective for interim and annual periods ending after June 15, 2009,

and accordingly, the Company adopted this pronouncement during the year ended

August 31, 2009. SFAS 165 requires that public entities evaluate subsequent

events through the date that the financial statements are issued. The Company

has evaluated subsequent events through November 25, 2009.

In

April 2009, the FASB issued FSP No. SFAS 107-1 and APB 28-1, “Interim

Disclosures about Fair Value of Financial Instruments,” which is codified in

FASB ASC Topic 825-10-50. This FSP essentially expands the disclosure about fair

value of financial instruments that were previously required only annually to

also be required for interim period reporting. In addition, the FSP requires

certain additional disclosures regarding the methods and significant assumptions

used to estimate the fair value of financial instruments. These additional

disclosures are required beginning with the quarter ending June 30, 2009. The

Company does not believe the adoption of this FSP will have an impact on its

financial condition, results of operations or cash flows.

In

April 2009, the FASB issued FSP No. FAS 115-2 and FAS 124-2, “Recognition

and Presentation of Other-Than-Temporary Impairments,” which is codified in FASB

ASC Topic 320-10. This FSP modifies the requirements for recognizing

other-than-temporarily impaired debt securities and changes the existing

impairment model for such securities. The FSP also requires additional

disclosures for both annual and interim periods with respect to both debt and

equity securities. Under the FSP, impairment of debt securities will be

considered other-than-temporary if an entity (1) intends to sell the security,

(2) more likely than not will be required to sell the security before recovering

its cost, or (3) does not expect to recover the security’s entire amortized cost

basis (even if the entity does not intend to sell). The FSP further indicates

that, depending on which of the above factor(s) causes the impairment to be

considered other-than-temporary, (1) the entire shortfall of the security’s fair

value versus its amortized cost basis or (2) only the credit loss portion would

be recognized in earnings while the remaining shortfall (if any) would be

recorded in other comprehensive income. FSP 115-2 requires entities to initially

apply the provisions of the standard to previously other-than-temporarily

impaired debt securities existing as of the date of initial adoption by making a

cumulative-effect adjustment to the opening balance of retained earnings in the

period of adoption. The cumulative-effect adjustment potentially reclassifies

the noncredit portion of a previously other-than-temporarily impaired debt

security held as of the date of initial adoption from retained earnings to

accumulate other comprehensive income. The Company adopted FSP No. SFAS 115-2

and SFAS 124-2 beginning April 1, 2009. This FSP had no material impact on the

Company’s financial position, results of operations or cash flows.

In April

2009, the Financial Accounting Standards Board (“FASB”) issued FSP

No. SFAS 157-4, “Determining Fair Value When the Volume and Level of

Activity for the Asset or Liability Have Significantly Decreased and Identifying

Transactions That Are Not Orderly” (“FSP No. SFAS 157-4”). FSP

No. SFAS 157-4, which is codified in FASB ASC Topics 820-10-35-51 and

820-10-50-2, provides additional guidance for estimating fair value and

emphasizes that even if there has been a significant decrease in the volume and

level of activity for the asset or liability and regardless of the valuation

technique(s) used, the objective of a fair value measurement remains the same.

The Company adopted FSP No. SFAS 157-4 beginning April 1, 2009.

This FSP had no material impact on the Company’s financial position, results of

operations or cash flows.

ITEM

7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET

RISK.

We

are a smaller reporting company as defined by Rule 12b-2 of the Exchange Act and

are not required to provide the information under this item.

13

ITEM

8. FINANCIAL STATEMENTS AND SUPPLEMENTARY

DATA.

The

financial statements, together with the report thereon, of Everton Capital

Corporation, as listed under Item 15 appear in a separate section of

this report beginning on page F-1

ITEM 9.

CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL

DISCLOSURE.

On April

23, 2009, the Company dismissed Malone & Bailey, PC (“Malone & Bailey”)

as its principal independent public accountant, and engaged Goldman Parks

Kurland Mohidin, LLP (“GPKM”) as its new principal independent accountant. This

decision was approved by the Board of Directors of the Company. Malone &

Bailey audited the Registrant’s financial statements from May 9, 2006

(inception) through February 28, 2009.

During

the Company’s two most recent fiscal years and any subsequent interim period

through April 23, 2009, there have been no disagreements or reportable events

with Malone & Bailey on any matter of accounting principles or practices,

financial statement disclosure or auditing scope or procedure, which

disagreements, if not resolved to the satisfaction of Malone & Bailey, would

have caused them to make reference thereto in their reports on the financial

statements for such year. Malone & Bailey’s report on the Company’s

financial statements for the Company’s two most recent fiscal years did not

contain an adverse opinion or disclaimer of opinion, and was not modified as to

uncertainty, audit scope, or accounting principles except that Malone &

Bailey’s report on the financial statements of the Company as of and for the

year ended August 31, 2008 contained a separate paragraph stating:

“The

accompanying financial statements have been prepared assuming that Everton will

continue as a going concern. As discussed in Note 3 to the financial statements,

Everton has suffered recurring losses from operations which raises substantial

doubt about its ability to continue as a going concern. Management’s plans

regarding those matters also are described in Note 3. The financial statements

do not include any adjustments that might result from the outcome of this

uncertainty.”

During

the Registrant’s most recent two fiscal years, as well as the subsequent interim

period through the April 23, 2009, Malone & Bailey did not advise the

Company of any of the matters identified in Item 304(a)(1)(v)(A) - (D) of

Regulation S-K.

During

the Registrant’s two most recent fiscal years and the interim period ended April

23, 2009, the Company has not consulted with GPKM regarding any matters or

reportable events described in Items 304(a)(2)(i) and (ii) of Regulation

S-K.

ITEM 9A (T).

CONTROLS AND PROCEDURES.

Evaluation

of Disclosure Controls and Procedures

We

maintain “disclosure controls and procedures,” as such term is defined in Rule

13a-15(e) under the Securities Exchange Act of 1934 (the “Exchange Act”), that

are designed to ensure that information required to be disclosed in our Exchange

Act reports is recorded, processed, summarized and reported within the time

periods specified in the Securities and Exchange Commission rules and forms, and

that such information is accumulated and communicated to our management,

including our Chief Executive Officer and Chief Financial Officer, as

appropriate, to allow timely decisions regarding required disclosure. We

conducted an evaluation (the “Evaluation”), under the supervision and with the

participation of our Chief Executive Officer (“CEO”) and Chief Financial Officer

(“CFO”), of the effectiveness of the design and operation of our disclosure

controls and procedures (“Disclosure Controls”) as of the end of the period

covered by this report pursuant to Rule 13a-15 of the Exchange Act. Based on

this Evaluation, our CEO and CFO concluded that our Disclosure Controls were

effective as of the end of the period covered by this report.

14

Management’s

Report on Internal Control over Financial Reporting

The

following report shall not be deemed to be filed for purposes of Section 18

of the Exchange Act or otherwise subject to the liabilities of that section,

unless we specifically state that the report is to be considered “filed” under

the Exchange Act or incorporate it by reference into a filing under the

Securities Act or the Exchange Act.

Our management is

responsible for establishing and maintaining adequate internal control over

financial reporting as defined under Exchange Act Rules 13a-15(f). Internal

control over financial reporting is designed to provide reasonable assurance

regarding the reliability of our financial reporting and preparation of

financial statements for external purposes in accordance with U.S. GAAP.

Internal control over financial reporting includes maintaining records that in

reasonable detail accurately and fairly reflect our transactions; providing

reasonable assurance that transactions are recorded as necessary for preparation

of our financial statements in accordance with U.S. GAAP; providing

reasonable assurance that our receipts and expenditures are made in accordance

with authorizations of our management and directors; and providing reasonable

assurance that unauthorized acquisition, use or disposition of our assets that

could have a material effect on our financial statements would be prevented or

detected on a timely basis. Because of its inherent limitations, internal

control over financial reporting is not intended to provide absolute assurance

that a misstatement of our financial statements would be prevented or detected.

Furthermore, management does not expect that our disclosure controls and

procedures or our internal control over financial reporting will prevent or

detect all error and fraud. Any control system, no matter how well designed and

operated, is based upon certain assumptions and can provide only reasonable, not

absolute, assurance that its objectives will be met. Further, no evaluation of

controls can provide absolute assurance that misstatements due to error or fraud

will not occur or that all control issues and instances of fraud, if any, within

the Company have been detected.

An

evaluation was performed, under the supervision and with the participation of

Company management, including the CEO and the CFO, of the effectiveness of the

design and operation of the Company’s disclosure controls and procedures (as

defined in Rules 13a-14(c) and 15d-14(c) under the Exchange Act). Based on that

evaluation, management, including the CEO and CFO, has concluded that, as of

August 31, 2009, the Company’s disclosure controls and procedures were adequate

to ensure that information required to be disclosed in reports that the Company

files or submits under the Exchange Act has been recorded, processed, summarized

and reported in accordance with the rules and forms of the SEC.

This

annual report does not include an attestation report of the company’s registered

public accounting firm regarding internal control over financial reporting.

Management’s report was not subject to attestation by the company’s registered

public accounting firm pursuant to temporary rules of the Securities and

Exchange Commission that permit the company to provide only management’s report

in this annual report.

Changes

in Internal Controls

We

have also evaluated our internal controls for financial reporting, and there

have been no significant changes in our internal controls or in other factors

that could significantly affect those controls subsequent to the date of their

last evaluation.

ITEM

9B. OTHER INFORMATION

None.

PART

III

ITEM

10. DIRECTORS, EXECUTIVE OFFICERS, PROMOTERS AND

CONTROL PERSONS; COMPLIANCE WITH SECTION 16(a) OF THE EXCHANGE ACT.

Officers

and Directors

Our

sole director serves until his successor is elected and qualified. Our sole

officer is elected by the board of directors to a term of one (1) year and

serves until her successor is duly elected and qualified, or until he is removed

from office. We do not have a nominating committee or a compensation committee.

We do have an audit committee and disclosure committee.

15

The name, address, age and position of our present sole officer and director is

set forth below:

|

Name and Address

|

Age

|

Position(s)

|

|

Jonathan

Woo

|

30

|

president,

principal executive officer, treasurer

|

|

principal

financial officer, principal accounting officer

|

||

|

and

the sole member of the board of

directors.

|

603, Unit

3, DongFeng South Road, NaShiLiJu 34,

ChaoYang

District, Beijing, China 100016

Effective

on April 23, 2009, the Board of Directors (the "Board") appointed Jonathan Woo

as a director of the Company and accepted the resignation of Maryna Bilynska as

Chief Executive Officer, President, Chief Financial Officer, Treasurer,

Secretary, and director of the Company. Ms. Bilynska resigned in order to pursue

other interests and did not indicate that her resignation was a result of any

disagreement with the Company on any matter relating to the Company's

operations, policies or practices. The board appointed Mr. Woo as the Chief

Executive Officer, President, Chief Financial Officer, Treasurer and

Secretary.

Mr. Woo

is 30 years old and has been an independent business consultant advising

companies in strategic development and corporate communications since 2006. From

2004 to 2005 he worked as a deputy director at the GanSu Municipal Government in

charge of administrative and corporate liaison. From 1998 to 2003, he was an

information services officer at the Chinese military academy. During the same

period, he received a Bachelor’s degree in computer information systems from the

Chinese College of Higher Education distance program.

Involvement

in Certain Legal Proceedings

Other

than as described in this section, to our knowledge, during the past five years,

no present or former director or executive officer of our company: (1) filed a

petition under the federal bankruptcy laws or any state insolvency law, nor had

a receiver, fiscal agent or similar officer appointed by a court for the

business or present of such a person, or any partnership in which he was a

general partner at or within two years before the time of such filing, or any

corporation or business association of which he was an executive officer within

two years before the time of such filing; (2) was convicted in a criminal

proceeding or named subject of a pending criminal proceeding (excluding traffic

violations and other minor offenses); (3) was the subject of any order, judgment

or decree, not subsequently reversed, suspended or vacated, of any court of

competent jurisdiction, permanently or temporarily enjoining him from or

otherwise limiting the following activities: (i) acting as a futures commission

merchant, introducing broker, commodity trading advisor, commodity pool

operator, floor broker, leverage transaction merchant, associated person of any

of the foregoing, or as an investment advisor, underwriter, broker or dealer in

securities, or as an affiliated person, director of any investment company, or

engaging in or continuing any conduct or practice in connection with such

activity; (ii) engaging in any type of business practice; (iii) engaging in any

activity in connection with the purchase or sale of any security or commodity or

in connection with any violation of federal or state securities laws or federal

commodity laws; (4) was the subject of any order, judgment or decree, not

subsequently reversed, suspended or vacated, of any federal or state authority

barring, suspending or otherwise limiting for more than 60 days the right of

such person to engage in any activity described above under this Item, or to be

associated with persons engaged in any such activity; (5) was found by a court

of competent jurisdiction in a civil action or by the Securities and Exchange

Commission to have violated any federal or state securities law and the judgment

in subsequently reversed, suspended or vacate; (6) was found by a court of

competent jurisdiction in a civil action or by the Commodity Futures Trading

Commission to have violated any federal commodities law, and the judgment in

such civil action or finding by the Commodity Futures Trading Commission has not

been subsequently reversed, suspended or vacated.

16

Audit

Committee and Charter

We have a

separately-designated audit committee of the board. Audit committee functions

are performed by our board of directors. None of our directors are deemed

independent. All directors also hold positions as our officers. Our audit

committee is responsible for: (1) selection and oversight of our independent

accountant; (2) establishing procedures for the receipt, retention and treatment

of complaints regarding accounting, internal controls and auditing matters; (3)

establishing procedures for the confidential, anonymous submission by our

employees of concerns regarding accounting and auditing matters; (4) engaging

outside advisors; and, (5) funding for the outside auditory and any outside

advisors engagement by the audit committee.

Audit

Committee Financial Expert

None of

our directors or officers have the qualifications or experience to be considered

a financial expert. We believe the cost related to retaining a financial expert

at this time is prohibitive. Further, because of our limited operations, we

believe the services of a financial expert are not warranted.

Disclosure

Committee and Charter

We have a

disclosure committee and disclosure committee charter. Our disclosure committee

is comprised of all of our officers and directors. The purpose of the committee

is to provide assistance to the Chief Executive Officer and the Chief Financial

Officer in fulfilling their responsibilities regarding the identification and

disclosure of material information about us and the accuracy, completeness and

timeliness of our financial reports. A copy of the disclosure committee charter

is filed as an exhibit to this report.

Code

of Ethics

We have

adopted a corporate code of ethics. We believe our code of ethics is reasonably

designed to deter wrongdoing and promote honest and ethical conduct; provide

full, fair, accurate, timely and understandable disclosure in public reports;

comply with applicable laws; ensure prompt internal reporting of code

violations; and provide accountability for adherence to the code. A copy of the

code of ethics has been filed with the SEC.

Section

16(a) Beneficial Ownership Reporting Compliance

Section 16(a) of the Exchange Act

requires our executive officers and directors, and persons who beneficially own

more than 10% of our equity securities, to file reports of ownership and changes

in ownership with the Securities and Exchange Commission. Officers, directors

and greater than 10% shareholders are required by SEC regulation to furnish us

with copies of all Section 16(a) forms they file. Based on our review of the

copies of such forms we received, we believe that during the fiscal year ended

August 31, 2009 all such filing requirements applicable to our officers and

directors were complied with exception that reports were filed late by the

following persons:

|

Failures

|

|||||||

|

To File a

|

|||||||

|

Name and principal

|

Late

|

Not Timely

|

Required

|

||||

|

position

|

Reports

|

Reported

|

Form

|

||||

|

Jonathan

Woo President

|

0

|

0

|

1

|

17

ITEM

11. EXECUTIVE COMPENSATION

The

following table sets forth the compensation paid by us from inception on

November 8, 2006 through our fiscal year end, August 31, 2009, for our former

and current sole officer. This information includes the dollar value of base

salaries, bonus awards and number of stock options granted, and certain other

compensation, if any. The compensation discussed addresses all compensation

awarded to, earned by, or paid to our named executive officer.

Executive

Officer Compensation Table

|

Non-

|

Nonqualified

|

|||||||||||||||||||||||||||||||||

|

Equity

|

Deferred

|

All

|

||||||||||||||||||||||||||||||||

|

Incentive

|

Compensa-

|

Other

|

||||||||||||||||||||||||||||||||

|

Stock

|

Option

|

Plan

|

tion

|

Compen-

|

||||||||||||||||||||||||||||||

|

Name and

|

Salary

|

Bonus

|

Awards

|

Awards

|

Compensation

|

Earnings

|

sation

|

Total

|

||||||||||||||||||||||||||

|

Principal Position

|

Year

|

(US$)

|

(US$)

|

(US$)

|

(US$)

|

(US$)

|

(US$)

|

(US$)

|

(US$)

|

|||||||||||||||||||||||||

|

(a)

|

(b)

|

(c)

|

(d)

|

(e)

|

(f)

|

(g)

|

(h)

|

(i)

|

(j)

|

|||||||||||||||||||||||||

|

Maryna

Bilynska

|

2009

|

0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |||||||||||||||||||||||||

|

Former

President

|

2008

|

0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |||||||||||||||||||||||||

|

|

2007

|

0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |||||||||||||||||||||||||

|

2006

|

0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | ||||||||||||||||||||||||||

|

Jonathan

Woo

|

2009

|

0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |||||||||||||||||||||||||

|

President

|

||||||||||||||||||||||||||||||||||

We have

not plan to pay any additional salaries at this time. We will not begin paying

salaries again until we have adequate funds to do so.

Long-Term

Incentive Plan Awards

We not

have any long-term incentive plans that provide compensation intended to serve

as incentive for performance.

Employment

Contracts

As of the

date hereof, we have not entered into employment contracts with any of our

officers and do not intend to enter into any employment contracts until such

time as it profitable to do so.

18

Indemnification

Under our

Bylaws, we may indemnify an officer or director who is made a party to any

proceeding, including a lawsuit, because of her position, if she acted in good

faith and in a manner she reasonably believed to be in our best interest. We may

advance expenses incurred in defending a proceeding. To the extent that the

officer or director is successful on the merits in a proceeding as to which she

is to be indemnified, we must indemnify her against all expenses incurred,

including attorney's fees. With respect to a derivative action, indemnity may be

made only for expenses actually and reasonably incurred in defending the

proceeding, and if the officer or director is judged liable, only by a court

order. The indemnification is intended to be to the fullest extent permitted by

the laws of the State of Nevada.

Regarding

indemnification for liabilities arising under the Securities Act of 1933, which

may be permitted to directors or officers under Nevada law, we are informed

that, in the opinion of the Securities and Exchange Commission, indemnification

is against public policy, as expressed in the Act and is, therefore,

unenforceable.

Change-In-Control

Agreements

We do not

have any existing arrangements providing for payments or benefits in connection

with the resignation, severance, retirement or other termination of any of our

named executive officers, changes in their compensation or a change in

control.

Impact

of Accounting and Tax Treatment of Compensation

Section 162(m)

of the Internal Revenue Code disallows a tax deduction to publicly held

companies for compensation paid to the principal executive officer and to each

of the three other most highly compensated officers (other than the principal

financial officer) to the extent that such compensation exceeds

$1.0 million per covered officer in any fiscal year. The limitation applies

only to compensation that is not considered to be performance-based.

Non-performance-based compensation paid to our executive officers during fiscal

2008 did not exceed the $1.0 million limit per officer, and we do not

expect the non-performance-based compensation to be paid to our executive

officers during fiscal 2009 to exceed that limit. Because it is unlikely that

the cash compensation payable to any of our executive officers in the

foreseeable future will approach the $1.0 million limit, we do not expect

to take any action to limit or restructure the elements of cash compensation

payable to our executive officers so as to qualify that compensation as

performance-based compensation under Section 162(m). We will reconsider

this decision should the individual cash compensation of any executive officer

ever approach the $1.0 million level.

Compensation

of Directors

The following table sets forth the

compensation paid by us for our 2009 fiscal year end, to our former and current

sole director. This information includes the dollar value of base salaries,

bonus awards and number of stock options granted, and certain other

compensation, if any. The compensation discussed addresses all compensation

awarded to, earned by, or paid to our named director. Our directors do not receive any

compensation for serving as members of the board of directors.

We do not maintain a

medical, dental or retirement benefits plan for the

directors.

19

|

Director’s Compensation Table

|

||||||||||||||||||||||||||||

|

Fees

|

||||||||||||||||||||||||||||

|

Earned

|

Nonqualified

|

|||||||||||||||||||||||||||

|

or

|

Non-Equity

|

Deferred

|

||||||||||||||||||||||||||

|

Paid in

|

Stock

|

Option

|

Incentive Plan

|

Compensation

|

All Other

|

|||||||||||||||||||||||

|

Cash

|

Awards

|

Awards

|

Compensation

|

Earnings

|

Compensation

|

Total

|

||||||||||||||||||||||

|

Name

|

(US$)

|

(US$)

|

(US$)

|

(US$)

|

(US$)

|

(US$)

|

(US$)

|

|||||||||||||||||||||

|

(a)

|

(b)

|

(c)

|

(d)

|

(e)

|

(f)

|

(g)

|

(h)

|

|||||||||||||||||||||

|

Maryna

Bilynska

|

0 | 0 | 0 | 0 | 0 | 0 | 0 | |||||||||||||||||||||

|

Jonathan

Woo

|

0 | 0 | 0 | 0 | 0 | 0 | 0 | |||||||||||||||||||||

ITEM

12. SECURITY OWNERSHIP OF CERTAIN BENEFICIAL

OWNERS AND MANAGEMENT

The

following table sets forth, as of August, 31, 2009, the total number of shares

owned beneficially by each of our directors, officers and key employees,

individually and as a group, and the present owners of 5% or more of our total

outstanding shares. The stockholder listed below have direct ownership of

his/her shares and possess voting and dispositive power with respect to the

shares. The percentage of ownership set forth below is based on 5,501,000 shares

of our common stock issued and outstanding as of August, 31, 2009.

|

|

Direct Amount of

|

Percent

|

|||||||

|

Name of Beneficial Owner

|

Ownership

|

Position

|

of Class

|

||||||

|

Jonathan

Woo

|

5,000,000 |

President,

Principal Executive Officer,

|

90.89 | % | |||||

|

Secretary,

Treasurer, Principal Financial

|

|||||||||

|

Officer,

Principal Accounting Officer and

|

|||||||||

|

sole

Director

|

|||||||||

|

All

Officers and Directors as a

|

5,000,000 | 90.89 | % | ||||||

|

Group

(1 Person)

|

|||||||||

Securities

authorized for issuance under equity compensation plans.

We have no equity compensation plans.

ITEM

13. CERTAIN RELATIONSHIPS AND RELATED

TRANSACTIONS

There

were no transactions with any related persons (as that term is defined in Item

404 in Regulation SK) during the fiscal year ended August 31, 2009, or any

currently proposed transaction, in which we were or are to be a participant and

the amount involved was in excess of $120,000 and in which any related person

had a direct or indirect material interest.

20

ITEM

14. PRINCIPAL ACCOUNTING FEES AND

SERVICES

(1)

Audit Fees

The

aggregate fees billed for each of the last two fiscal years for professional

services rendered by the principal accountant for our audit of annual financial

statements and review of financial statements included in our Form 10-Qs or

services that are normally provided by the accountant in connection with

statutory and regulatory filings or engagements for those fiscal years

was:

|

2009

|

$ | 2,500 |

Goldman Parks Kurland Mohidin, LLP

|

||

|

2009

|

$ | 0 |

Malone & Bailey, P.C.

|

||

|

2008

|

$ | 15,000 |

Malone & Bailey, P.C.

|

||

|

2007

|

$ | 10,000 |

Malone & Bailey, P.C.

|

(2)

Audit-Related Fees

The

aggregate fees billed in each of the last two fiscal years for assurance and

related services by the principal accountants that are reasonably related to the

performance of the audit or review of our financial statements and are not

reported in the preceding paragraph:

|

2009

|

$ | 0 |

Goldman Parks Kurland Mohidin, LLP

|

||

|

2009

|

$ | 0 |

Malone & Bailey, P.C.

|

||

|

2008

|

$ | 0 |

Malone & Bailey, P.C.

|

||

|

2007

|

$ | 0 |

Malone & Bailey, P.C.

|

(3)

Tax Fees

The

aggregate fees billed in each of the last two fiscal years for professional

services rendered by the principal accountant for tax compliance, tax advice,

and tax planning was:

|

2009

|

$ | 0 |

Goldman Parks Kurland Mohidin, LLP

|

||

|

2009

|

$ | 0 |

Malone & Bailey, P.C.

|

||

|

2008

|

$ | 0 |

Malone & Bailey, P.C.

|

||

|

2007

|

$ | 0 |

Malone & Bailey, P.C.

|

(4)

All Other Fees

The

aggregate fees billed in each of the last two fiscal years for the products and

services provided by the principal accountant, other than the services reported

in paragraphs (1), (2), and (3) was:

(5)

Our audit committee’s pre-approval policies and procedures described in

paragraph (c)(7)(i) of Rule 2-01 of Regulation S-X were that the audit committee

pre-approve all accounting related activities prior to the performance of any

services by any accountant or auditor.

(6)

The percentage of hours expended on the principal accountant’s engagement to

audit our financial statements for the most recent fiscal year that were

attributed to work performed by persons other than the principal accountant’s

full time, permanent employees was 0%.

21

ITEM

15. EXHIBITS, FINANCIAL STATEMENT

SCHEDULES.

(a)(1) Financial

Statements

See Index

to Consolidated Financial Statements on page F-1 of this

Form 10-K.

(a)(2) Financial Statement

Schedules:

Not

applicable.

(b) Exhibits

The

exhibits required by this item are set forth on the Exhibit Index attached

hereto.

(c) Financial

Statement Schedules

Not

applicable.

22

(An

Exploration Stage Company)

For

the Years Ended August 31, 2009, and 2008

Contents

|

Page

|

||

|

Reports

of Independent Registered Public Accounting Firms

|

F-2

|

|

|

Financial

Statements:

|

||

|

Balance

Sheets as of August 31, 2009 and 2008

|

F-4

|

|

|

Statements

of Expenses

|

||

|

for

the years ended August 31, 2009 and 2008

|

F-5

|

|

|

Statements

of Cash Flows for the years ended

|

||

|

August

31, 2009 and 2008

|

F-6

|

|

|

Statement

of Stockholders' Deficit for the years ended

|

||

|

August