Attached files

| file | filename |

|---|---|

| EX-32.1 - Benda Pharmaceutical, Inc. | v167398_ex32-1.htm |

| EX-31.1 - Benda Pharmaceutical, Inc. | v167398_ex31-1.htm |

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

WASHINGTON,

D.C. 20549

_______________

FORM

10-Q

_______________

|

x

|

QUARTERLY

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

|

For

the quarterly period ended September 30, 2009

|

o

|

TRANSITION

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

|

For the transition period from

______to______.

BENDA PHARMACEUTICAL, INC.

(Exact

name of registrant as specified in Charter

|

Delaware

|

000-16397

|

41-2185030

|

||

|

(State

or other jurisdiction of

incorporation

or organization)

|

(Commission

File No.)

|

(IRS

Employee Identification No.)

|

Taibei

Mingju, 4th

Floor,

6

Taibei Road, Wuhan, Hubei Province, 430015, PRC

(Address

of Principal Executive Offices)

_______________

+86

(27) 85494916

(Issuer

Telephone number)

_______________

(Former

Name or Former Address if Changed Since Last Report)

Check

whether the issuer (1) has filed all reports required to be filed by Section 13

or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter

period that the issuer was required to file such reports), and (2)has been

subject to such filing requirements for the past 90 days. Yes x No

o

Indicate

by check mark whether the registrant has submitted electronically and posted on

its corporate Web site, if any, every

Interactive

Data File required to be submitted and posted pursuant to Rule 405 of Regulation

S-T (§232.405 of this chapter) during the preceding 12 months (or for such

shorter period that the registrant was required to submit and post such

files).

Yes o No o

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer or a smaller reporting company filer.

See definition of “accelerated filer” and “large accelerated filer” in

Rule 12b-2 of the Exchange Act (Check one):

Large

Accelerated Filer o Accelerated

Filer o Non-Accelerated

Filer o Smaller

Reporting Company x

Indicate

by check mark whether the registrant is a shell company as defined in Rule 12b-2

of the Exchange Act.

Yes o No

x

State the

number of shares outstanding of each of the issuer’s classes of common equity,

as of November 23, 2009: 105,155,355 shares of common stock.

BENDA

PHARMACEUTICAL, INC.

FORM

10-Q

September

30, 2009

INDEX

|

PART

I-- FINANCIAL INFORMATION

|

|||

|

Item

1.

|

Financial

Statements

|

3

|

|

|

Item

2.

|

Management’s

Discussion and Analysis of Financial Condition

|

4

|

|

|

Item

3.

|

Quantitative

and Qualitative Disclosures About Market Risk

|

9

|

|

|

Item

4T.

|

Control

and Procedures

|

9

|

|

|

PART

II-- OTHER INFORMATION

|

|||

|

Item

1

|

Legal

Proceedings

|

10

|

|

|

Item

2.

|

Unregistered

Sales of Equity Securities and Use of Proceeds

|

12

|

|

|

Item

3.

|

Defaults

Upon Senior Securities

|

12

|

|

|

Item

4.

|

Submission

of Matters to a Vote of Security Holders

|

13

|

|

|

Item

5.

|

Other

Information

|

13

|

|

|

Item

6.

|

Exhibits

|

13

|

|

|

SIGNATURE

|

14

|

||

2

Item 1. Financial

Information

BENDA

PHARMACEUTICAL, INC.

(an

exploration stage company)

FINANCIAL

STATEMENTS

AS

OF SEPTEMBER 30, 2009

CONTENTS

|

F1

|

CONDENSED

BALANCE SHEETS AS OF SEPTEMBER 30, 2009 (UNAUDITED) AND AS OF DECEMBER 31,

2008 (AUDITED).

|

|

|

F2

|

CONDENSED

STATEMENTS OF OPERATIONS FOR THE SIX MONTHS ENDED SEPTEMBER 30, 2009 AND

2008 AND FOR THE PERIOD FROM DECEMBER 17, 1999 (INCEPTION) TO SEPTEMBER

30, 2009 (UNAUDITED).

|

|

|

F5

|

CONDENSED

STATEMENT OF CHANGES IN STOCKHOLDERS’ EQUITY/(DEFICIENCY) FOR THE PERIOD

FROM DECEMBER 17, 1999 (INCEPTION) TO SEPTEMBER 30, 2009

(UNAUDITED).

|

|

|

F3

- F4

|

CONDENSED

STATEMENTS OF CASH FLOWS FOR THE SIX MONTHS ENDED SEPTEMBER 30, 2009 AND

2008 AND FOR THE PERIOD FROM DECEMBER 17, 1999 (INCEPTION) TO SEPTEMBER

30, 2009 (UNAUDITED).

|

|

|

F6

- F39

|

NOTES

TO CONDENSED FINANCIAL STATEMENTS

(UNAUDITED).

|

3

Benda

Pharmaceutical, Inc.

Consolidated

Balance Sheets

(Amounts

expressed in U.S. Dollars)

|

September

30

|

December

31

|

|||||||

|

2009

|

2008

|

|||||||

|

(Unaudited)

|

(Audited)

|

|||||||

|

Assets

|

||||||||

|

Current

Assets

|

||||||||

|

Cash

and cash equivalents

|

$ | 1,378,053 | $ | 569,019 | ||||

|

Trade

receivables, net (Note 5)

|

8,683,364 | 9,336,915 | ||||||

|

Other

receivables (Note 5)

|

678,528 | 504,349 | ||||||

|

Short-term

loan receivables

|

- | 146,685 | ||||||

|

Prepaid

tax (Note 23)

|

1,509,892 | 771,549 | ||||||

|

Due

from related parties (Note 18)

|

7,634 | 11,000 | ||||||

|

Inventories

(Note 7)

|

2,343,783 | 2,344,562 | ||||||

|

Prepaid

expenses and deposits (Note 5)

|

2,540,267 | 918,209 | ||||||

|

Total

current assets

|

17,141,521 | 14,602,288 | ||||||

|

Due

from related parties (Note 18)

|

3,063,153 | 2,961,744 | ||||||

|

Property

and equipments, net (Note 8)

|

27,901,030 | 29,057,225 | ||||||

|

Intangible

assets, net (Note 9)

|

5,454,525 | 6,003,102 | ||||||

|

Restricted

cash (Note 11)

|

5,847,894 | 6,162,849 | ||||||

|

Refundable

purchase price paid (Note 6)

|

1,200,000 | 1,200,000 | ||||||

|

Other

assets (Note 12)

|

1,830,556 | 1,830,634 | ||||||

|

Debt

issue costs (Note 24)

|

- | 55,485 | ||||||

|

Total

Assets

|

$ | 62,438,679 | $ | 61,873,327 | ||||

|

Liabilities

& Shareholders' Equity

|

||||||||

|

Current

Liabilities

|

||||||||

|

Bank

indebtedness (Note 11)

|

$ | 1,199,965 | $ | 1,288,257 | ||||

|

Bank

loans payable (current portion) (Note 13)

|

2,984,433 | 2,984,560 | ||||||

|

Short-term

loans payable

|

1,042,955 | - | ||||||

|

Long

term debt payable (current portion) (Note 14)

|

2,234,115 | 2,234,210 | ||||||

|

Accounts

payable and accrued liabilities (Note 15)

|

9,757,230 | 7,228,400 | ||||||

|

Commercial

notes payable (Note 11)

|

9,075,536 | 9,297,169 | ||||||

|

Taxes

payable

|

262,761 | 516,302 | ||||||

|

Acquisition

cost payable (Note 10)

|

1,426,430 | 1,426,491 | ||||||

|

Long-term

convertible promissory notes (current portion) (Note 24)

|

7,260,000 | 6,395,951 | ||||||

|

Wages

payable

|

1,180,027 | 630,475 | ||||||

|

Payable

under redeemable common stock (Note 19)

|

7,376,366 |

7,376,366

|

||||||

|

Due

to related parties (Note 18)

|

467,842 | 1,457,803 | ||||||

|

Total

current liabilities

|

44,267,660 | 40,835,984 | ||||||

|

Due

to related parties (Note 18)

|

960,406 | 997,593 | ||||||

|

Total

Liabilities

|

45,228,066 | 41,833,577 | ||||||

|

Equity

|

||||||||

|

Preferred

stock, $0.001 par value; 5,000,000 shares authorized;

|

||||||||

|

None

issued and outstanding

|

- | - | ||||||

|

Common

stock, $0.001 par value; 150,000,000 shares authorized;

|

||||||||

|

105,155,355

shares issued and outstanding as of 9/30/2009

|

||||||||

|

and

12/31/2008 respectively;

|

105,155 | 105,155 | ||||||

|

Additional

paid in capital (Note 25)

|

22,108,427 | 22,108,427 | ||||||

|

Retained

earnings (unrestricted)

|

(18,736,213 | ) | (16,047,561 | ) | ||||

|

Statutory

surplus reserve fund (Note 17)

|

2,642,775 | 2,642,775 | ||||||

|

Accumulative

other comprehensive income

|

6,344,117 | 6,347,547 | ||||||

|

Shares

issuable for acquisition and services

|

503,860 | 503,860 | ||||||

|

Total

Benda Pharmaceutical, Inc. Shareholders' Equity

|

12,968,121 | 15,660,203 | ||||||

|

Noncontrolling

interest

|

4,242,492 | 4,379,547 | ||||||

|

Total

Equity

|

17,210,613 | 20,039,750 | ||||||

|

Total

Liabilities & Equity

|

$ | 62,438,679 | $ | 61,873,327 | ||||

The

accompanying notes are an integral part of these consolidated financial

statements.

F-1

Benda

Pharmaceutical, Inc.

Consolidated

Statements of Operations

(Amounts

expressed in U.S. Dollars)

|

Nine

Months Ended September 30

|

Three

Months Ended September 30

|

|||||||||||||||

|

2009

|

2008

|

2009

|

2008

|

|||||||||||||

|

(Unaudited)

|

(Unaudited)

|

(Unaudited)

|

(Unaudited)

|

|||||||||||||

|

Revenue

|

$ | 17,345,065 | $ | 19,860,057 | $ | 5,904,653 | $ | 6,634,434 | ||||||||

|

Cost

of goods sold

|

(9,770,370 | ) | (12,610,394 | ) | (3,071,291 | ) | (4,213,540 | ) | ||||||||

|

Gross

profit

|

7,574,695 | 7,249,663 | 2,833,362 | 2,420,894 | ||||||||||||

|

Selling

expenses

|

(1,868,482 | ) | (2,122,689 | ) | (852,116 | ) | (691,477 | ) | ||||||||

|

General

and administrative expenses

|

||||||||||||||||

|

Amortization

of intangible assets

|

(119,118 | ) | (148,591 | ) | (39,718 | ) | (50,643 | ) | ||||||||

|

Amortization

of debt issue costs (Note 24)

|

(55,485 | ) | (198,360 | ) | - | (66,603 | ) | |||||||||

|

Depreciation

|

(707,622 | ) | (373,639 | ) | (328,327 | ) | (130,144 | ) | ||||||||

|

Bad

debts

|

(3,080,334 | ) | (534,124 | ) | (271,472 | ) | 239,769 | |||||||||

|

Write-down

of inventory to net realizable value (recovery)

|

(196,628 | ) | - | (72,389 | ) | - | ||||||||||

|

Director

remuneration

|

(67,500 | ) | (162,968 | ) | (22,500 | ) | (22,500 | ) | ||||||||

|

Penalty

to investors

|

- | (1,380,173 | ) | - | (266,768 | ) | ||||||||||

|

Other

general and administrative expenses (Note 21)

|

(1,885,994 | ) | (2,764,256 | ) | (898,062 | ) | (743,982 | ) | ||||||||

|

Total

general and administrative expenses

|

(6,112,681 | ) | (5,562,111 | ) | (1,632,468 | ) | (1,040,871 | ) | ||||||||

|

Research

and development expenses

|

(283,473 | ) | (249,357 | ) | (165,390 | ) | (79,576 | ) | ||||||||

|

Total

operating expenses

|

(8,264,636 | ) | (7,934,157 | ) | (2,649,974 | ) | (1,811,924 | ) | ||||||||

|

Operating

income / (loss)

|

(689,941 | ) | (684,494 | ) | 183,388 | 608,970 | ||||||||||

|

Interest

income / (expenses) (Note 24)

|

(2,104,510 | ) | (3,339,457 | ) | (471,263 | ) | (998,877 | ) | ||||||||

|

Other

income / (expenses) (Note 20)

|

106,161 | 10,140 | 60,388 | (237,918 | ) | |||||||||||

|

Government

subsidies / grants (Note 22)

|

26,386 | - | - | - | ||||||||||||

|

Loss

before provision for income taxes and noncontrolling

interest

|

(2,661,904 | ) | (4,013,811 | ) | (227,487 | ) | (627,825 | ) | ||||||||

|

Income

taxes (Note 23)

|

(163,803 | ) | (907,176 | ) | (79,391 | ) | (382,368 | ) | ||||||||

|

Net

loss

|

(2,825,707 | ) | (4,920,987 | ) | (306,878 | ) | (1,010,193 | ) | ||||||||

|

Net

loss attributable to the noncontrolling interest

|

137,055 | 256,486 | (65,519 | ) | 168,270 | |||||||||||

|

Net

loss attributable to Benda Pharmaceutical, Inc.

|

$ | (2,688,652 | ) | (4,664,501 | ) | $ | (372,397 | ) | $ | (841,923 | ) | |||||

|

Basic

and fully diluted loss per share

|

||||||||||||||||

|

Net

loss attributable to Benda Pharmaceutical, Inc. common

shareholders

|

$ | (0.03 | ) | (0.05 | ) | $ | (0.00 | ) | $ | (0.01 | ) | |||||

|

Weighted

average shares outstanding (Note 26)

|

105,155,355 | 100,887,853 | 105,155,355 | 101,556,376 | ||||||||||||

The accompanying notes are an integral part of these consolidated financial

statements.

F-2

Benda

Pharmaceutical, Inc.

Consolidated

Statements of Cash Flows

(Amounts

expressed in U.S. Dollars)

|

Nine

Months Ended September 30,

|

||||||||

|

2009

|

2008

|

|||||||

|

(Unaudited)

|

(Unaudited)

|

|||||||

|

Cash

Flows From Operating Activities

|

||||||||

|

Net

loss

|

$ | (2,825,707 | ) | $ | (4,920,987 | ) | ||

|

Adjustments

to reconcile net loss to net cash provided by operating

activities:

|

||||||||

|

Bad

Debt provision

|

3,080,334 | 534,125 | ||||||

|

Inventory

written down to net realizable value (recovery)

|

196,628 | - | ||||||

|

Depreciation

|

1,609,314 | 1,414,763 | ||||||

|

Amortization

of intangible assets

|

547,919 | 567,016 | ||||||

|

Amortization

of debt issue costs (Note 24)

|

55,485 | 198,360 | ||||||

|

Interest

expense (amortization of debt discount) (Note 24)

|

864,049 | 2,614,667 | ||||||

|

Penalty

to investors settled by issuance of common stock

|

- | 497,081 | ||||||

|

Directors

remuneration settled by issuance of common stock

|

- | 75,900 | ||||||

|

Changes

in operating assets and liabilities:

|

||||||||

|

Trade

receivables

|

(2,427,968 | ) | (2,312,392 | ) | ||||

|

Other

receivables

|

(174,180 | ) | 239,155 | |||||

|

Prepaid

expenses and deposits

|

(1,622,058 | ) | (85,211 | ) | ||||

|

Inventories

|

(195,849 | ) | (835,895 | ) | ||||

|

Accounts

payable and accrued liabilities

|

3,078,386 | 1,856,143 | ||||||

|

Taxes

payable

|

(991,888 | ) | (281,668 | ) | ||||

|

Net

cash provided by operating activities

|

1,194,465 | (438,943 | ) | |||||

|

Cash

Flows From Investing Activities

|

||||||||

|

Purchases

of property and equipment and construction-in-progress

|

(455,488 | ) | (210,254 | ) | ||||

|

Proceeds

and repayments of borrowings under short-term loan

receivables

|

146,685 | (146,304 | ) | |||||

|

Net

cash used in investing activities

|

(308,803 | ) | (356,558 | ) | ||||

|

Cash

Flows From Financing Actives

|

||||||||

|

Proceeds

and repayments of borrowings under related parties, net

|

(1,125,192 | ) | (1,247,617 | ) | ||||

|

Proceeds

and repayments of borrowings under government debts payable,

net

|

(88,236 | ) | 297,545 | |||||

|

Proceeds

and repayments of borrowings under commercial bank notes, net (Note

11)

|

93,266 | 1,876,424 | ||||||

|

Proceeds

and repayments of borrowings under bank loans, net

|

1,042,955 | (81,082 | ) | |||||

|

Net

cash provided by (used in) financing activities

|

(77,207 | ) | 845,270 | |||||

|

Effect

of exchange rate changes on cash

|

579 | 369,366 | ||||||

|

Net

increase in cash and cash equivalents

|

809,034 | 419,135 | ||||||

|

Cash

and cash equivalents, beginning of period

|

569,019 | 1,266,240 | ||||||

|

Cash

and cash equivalents, end of period

|

$ | 1,378,053 | $ | 1,685,375 | ||||

|

Supplemental

Disclosure of Cash Flow Information

|

||||||||

|

Cash

paid for interest

|

$ | 298,139 | $ | 823,037 | ||||

|

Cash

paid for income taxes

|

$ | 935,208 | $ | 954,431 | ||||

The accompanying notes are an

integral part of these consolidated financial statements.

F-3

Benda

Pharmaceutical, Inc.

Statements

of Consolidated Comprehensive Income

(Amounts

expressed in U.S. Dollars)

|

Nine

Months Ended June 30,

|

||||||||

|

2009

|

2008

|

|||||||

|

(Unaudited)

|

(Unaudited)

|

|||||||

|

Net

loss

|

$ | (2,825,707 | ) | $ | (4,920,987 | ) | ||

|

Other

comprehensive income (loss)

|

||||||||

|

Foreign

currency translation adjustment

|

(3,430 | ) | 2,997,021 | |||||

|

Comprehensive

loss

|

(2,829,137 | ) | (1,923,966 | ) | ||||

|

Comprehensive

loss attributable to the noncontrolling interest

|

137,055 | 256,486 | ||||||

|

Comprehensive

loss attributable to Benda Pharmaceutical, Inc.

|

$ | (2,692,082 | ) | $ | (1,667,480 | ) | ||

The accompanying notes are an integral part of these consolidated financial

statements.

F-4

Benda

Pharmaceutical, Inc.

Consolidated

Statement of Changes in Equity

(Amounts

expressed in U.S. Dollars)

|

Shares

|

||||||||||||||||||||||||||||||||||||||||

|

Issuable

|

||||||||||||||||||||||||||||||||||||||||

|

Common

|

Statutory

|

Accumulated

|

for

|

|||||||||||||||||||||||||||||||||||||

|

Shares

|

Additional

|

Retained

|

Surplus

|

Other

|

Acquisition

|

Non-

|

||||||||||||||||||||||||||||||||||

|

Issued

and

|

Comprehensive

|

Common

|

Paid-in

|

Earnings

|

Reserve

|

Comprehensive

|

and

|

Controlling

|

||||||||||||||||||||||||||||||||

|

Outstanding

|

Total

|

Income

|

Stock

|

Capital

|

(Unrestricted)

|

Fund

|

Income

|

Services

|

Interest

|

|||||||||||||||||||||||||||||||

|

Balance

at December 31, 2008

|

105,155,355 | $ | 20,039,750 | $ | - | $ | 105,155 | $ | 22,108,427 | $ | (16,047,561 | ) | $ | 2,642,775 | $ | 6,347,547 | $ | 503,860 | $ | 4,379,547 | ||||||||||||||||||||

|

Comprehensive

loss:

|

||||||||||||||||||||||||||||||||||||||||

|

Net

loss

|

(1,236,563 | ) | (1,236,563 | ) | - | - | (1,040,557 | ) | - | - | - | (196,006 | ) | |||||||||||||||||||||||||||

|

Other

comprehensive income (loss)

|

||||||||||||||||||||||||||||||||||||||||

|

Foreign

currency translation adjustment

|

(52,320 | ) | (52,320 | ) | - | - | - | - | (52,320 | ) | - | - | ||||||||||||||||||||||||||||

|

Comprehensive

loss

|

(1,288,883 | ) | $ | (1,288,883 | ) | |||||||||||||||||||||||||||||||||||

|

Dividend

paid

|

- | |||||||||||||||||||||||||||||||||||||||

|

Balance

at March 31, 2009 (unaudited)

|

105,155,355 | $ | 18,750,868 | $ | 105,155 | $ | 22,108,427 | $ | (17,088,117 | ) | $ | 2,642,775 | $ | 6,295,227 | $ | 503,860 | $ | 4,183,541 | ||||||||||||||||||||||

|

Comprehensive

loss:

|

||||||||||||||||||||||||||||||||||||||||

|

Net

loss

|

(1,282,266 | ) | (1,282,266 | ) | - | - | (1,275,698 | ) | - | - | - | (6,568 | ) | |||||||||||||||||||||||||||

|

Other

comprehensive income (loss)

|

||||||||||||||||||||||||||||||||||||||||

|

Foreign

currency translation adjustment

|

5,169 | 5,169 | - | - | - | - | 5,169 | - | - | |||||||||||||||||||||||||||||||

|

Comprehensive

loss

|

(1,277,098 | ) | $ | (1,277,097 | ) | |||||||||||||||||||||||||||||||||||

|

Dividend

paid

|

- | |||||||||||||||||||||||||||||||||||||||

|

Balance

at June 30, 2009 (unaudited)

|

105,155,355 | $ | 17,473,770 | $ | 105,155 | $ | 22,108,427 | $ | (18,363,816 | ) | $ | 2,642,775 | $ | 6,300,396 | $ | 503,860 | $ | 4,176,973 | ||||||||||||||||||||||

|

Comprehensive

loss:

|

||||||||||||||||||||||||||||||||||||||||

|

Net

loss

|

(306,878 | ) | (306,878 | ) | (372,397 | ) | 65,519 | |||||||||||||||||||||||||||||||||

|

Other

comprehensive income (loss)

|

||||||||||||||||||||||||||||||||||||||||

|

Foreign

currency translation adjustment

|

43,721 | 43,721 | 43,721 | |||||||||||||||||||||||||||||||||||||

|

Comprehensive

loss

|

(263,157 | ) | (263,157 | ) | ||||||||||||||||||||||||||||||||||||

|

Dividend

paid

|

- | |||||||||||||||||||||||||||||||||||||||

|

Balance

at September 30, 2009 (unaudited)

|

105,155,355 | $ | 16,947,456 | $ | 105,155 | $ | 22,108,427 | $ | (18,736,213 | ) | $ | 2,642,775 | $ | 6,344,117 | $ | 503,860 | $ | 4,242,492 | ||||||||||||||||||||||

The accompanying notes are an integral part of these consolidated

financial statements.

F-5

Benda

Pharmaceutical, Inc.

Notes

to Consolidated Financial Statements

(Amounts

expressed in U.S. Dollars)

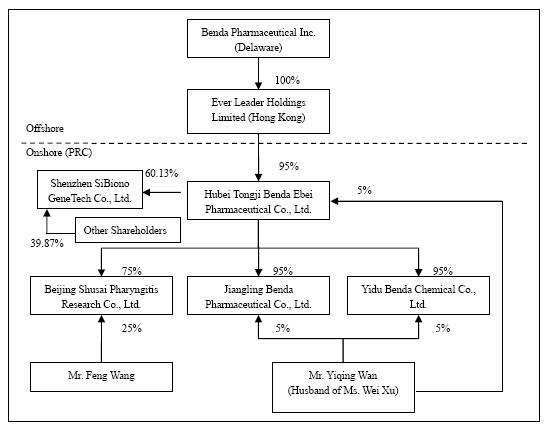

1.

Organization

Benda

Pharmaceutical, Inc. (“Benda”) is a corporation organized under the Florida Laws

and headquartered in Hubei Province, the People’s Republic of China

(“PRC”).

Ever

Leader Holdings Limited (“Ever Leader”), a wholly owned subsidiary of Benda, is

a company incorporated under the laws of Hong Kong SAR.

Ever

Leader owns 95% of the issued and outstanding capital of Hubei Tongi Benda Ebei

Pharmaceutical Co. Ltd. (“Benda Ebei”), a Sino-Foreign Equity Joint Venture

company incorporated under the laws of PRC. Mr. Yiqing Wan owns 5% of the issued

and outstanding capital stock of Benda Ebei. Benda Ebei owns: (i) 95% of the

issued and outstanding capital stock of Jiangling Benda Pharmaceutical Co. Ltd.,

(“Jiangling Benda”) a company formed under the laws of PRC; (ii) 95% of the

issued and outstanding capital stock of Yidu Benda Chemical Co. Ltd., (“Yidu

Benda”) a company incorporated under the laws of PRC; and (iii) 75% of the

issued and outstanding capital stock of Beijing Shusai Pharyngitis Research Co.

Ltd., (“Beijing Shusai”) a company incorporated under the laws of PRC. Mr.

Yiqing Wan owns: (i) 5% of the issued and outstanding capital stock of Jingling

Benda; and (ii) 5% of the issued and outstanding capital stock of Yidu Benda.

Mr. Feng Wang owns 25% of the issued and outstanding capital stock of Beijing

Shusai.

On April

5, 2007, Benda Ebei entered into an Equity Transfer Agreements with Shenzhen

Yuanzheng Investment Development Co., Ltd. and Shenzhen Yuanxing Gene City

Development Co., Ltd., the then shareholders of Shenzhen SiBiono GeneTech Co.,

Ltd (“SiBiono”), to purchase 27.57% and 30% respectively of the shares of

SiBiono’s common stock for total consideration of Rmb60 million (or $7.88

million) due and payable on or before April 30, 2007. On June 11, 2007, Benda

Ebei entered into an Equity Transfer Agreements with Huimin Zhang and Yaojin

Wang, the individual shareholders of SiBiono, and to purchase 1.6% and 0.96%

respectively of the shares of SiBiono’s common stock for total consideration of

Rmb2.56 million (or $0.34 million) due and payable on or before June 30, 2007.

Altogether, the total consideration for 60.13% shares of SiBiono’s common stock

was Rmb62.56 million or $9.18 million. As of September 30, 2009, an accumulated

amount, approximately Rmb52.84 million or $7.76 million was paid and leaving a

balance of Rmb 9.72 million or $1.42 million (please refer to Note 10 for the

details).

Benda,

Ever Leader, Benda Ebei, Jingling Benda, Yidu Benda, Beijing Shusai and SiBiono

shall be referred to herein collectively as the “Group”. The Group is engaged

principally in the business of identifying, discovering, developing, and

manufacturing conventional medicines, active pharmaceuticals, bulk chemicals (or

pharmaceutical immediates), and Traditional Chinese Medicines (“TCM”) for the

treatment of some of the most widespread common ailments and diseases (e.g.

common cold, diabetes, and cancer).

F-6

As of

September 30, 2009, the organization and ownership structure of the Group is as

follows:

2.

Basis

of Preparation, Consolidation and Going Concern

The

unaudited consolidated financial statements of Benda and its subsidiaries have

been prepared in accordance with U.S. generally accepted accounting principles

for interim financial information and pursuant to the requirements for reporting

on Form 10-Q. Accordingly, they do not include all the information and footnotes

required by accounting principles generally accepted in the United States

of America for annual financial statements. However, the information included in

these interim financial statements reflects all adjustments (consisting solely

of normal recurring adjustments) which are, in the opinion of management,

necessary for the fair presentation of the consolidated financial position and

the consolidated results of operations. Results shown for interim periods are

not necessarily indicative of the results to be obtained for a full year. The

consolidated balance sheet information as of December 31, 2008 was derived from

the audited consolidated financial statements included in the Group’s Annual

Report on Form 10-K. These interim financial statements should be read in

conjunction with that report. We have reclassified amounts previously reported

in the Group’s financial statements to conform to the current

presentation related to redeemable common stock. The Group has

evaluated subsequent events through the date that the financial statements

were issued which was November 22, 2009, the date immediately preceding the

date of the Group’s Quarterly Report on Form 10-Q for the period ended September

30, 2009.

In the

Group’s Annual Report on Form 10-K for the fiscal year ended December 31, 2008,

the Report of the Independent Registered Public Accounting Firm includes an

explanatory paragraph that describes substantial doubt about the Group’s ability

to continue as a going concern. The Group’s interim financial statements for the

three and nine months ended September 30, 2009 have been prepared on a going

concern basis, which contemplates the realization of assets and the settlement

of liabilities and commitments in the normal course of business. The

Group reported a net loss of $2,825,707 for the nine months ended September 30,

2009 and has a working capital deficit of approximately $27,126,139 and

accumulated deficit of approximately $18,736,213 as of September 30,

2009.

Currently,

the Group does not have the ability to substantially increase its loan

indebtedness with any financial institution , nor can the Group provide any

assurance it will be able to enter into any loan agreements in the future, or be

able to raise funds through further issuance of debt or equity in the

Group. Moreover, the Group presently has little additional resources

with which to obtain or develop new operations.

These

factors raise substantial doubt about the Group’s ability to continue as a going

concern. The financial statements do not contain any adjustments

relating to the recoverability and classification of assets or the amounts and

classification of liabilities that might be necessary should the Group be unable

to continue as a going concern.

While the

Group is attempting to produce sufficient revenues, the Group’s cash position

may not be enough to support the Group’s daily operations. Management

intends to raise additional funds by way of a public or private

offering. Management believes that the actions presently being taking

to further implement its business plan and generate sufficient revenues provide

the opportunity for the Group to continue as a going concern. While

the Group believes in the viability of its strategy to increase revenues and in

its ability to raise additional funds, there can be no assurance to that

effect. The ability of the Group to continue as a going concern is

dependent upon the Group’s ability to further implement its business plan and

generate sufficient revenues. The financial statements do not include

any adjustments that might be necessary it the Group is unable to continue as a

going concern.

F-7

3.

Use

of Estimates

The

preparation of financial statements in conformity with US GAAP requires

management to make estimates and assumptions that affect the reported amounts of

assets and liabilities and disclosure of contingent assets and liabilities at

the date of the financial statements, and the reported amounts of revenue and

expenses during the reporting period. Actual results when ultimately realized

could differ from those estimates.

4.

Significant

Accounting Policies

Cash

and Cash Equivalents

Cash and cash equivalents include cash

on hand, cash on deposit with various financial institutions, and all highly-liquid

investments with original maturities of three months or less at the time of

purchase.

Estimates

Affecting Trade Receivables, Other Receivables, Prepaid and Deposits and

Inventories

The

preparation of our consolidated financial statements requires management to make

estimates and assumptions that affect our reporting of assets and liabilities

(and contingent assets and liabilities). However, it is explicated that the

changes in estimation were not material in the preparation of our consolidation

financial statements.

As of

September 30, 2009 and 2008, the Group provided a $6,867,978 and $1,552,068,

respectively for the allowance of doubtful accounts against trade receivables

(please refer to Note 5 for details). Management's estimate of the appropriate

allowance on those accounts receivable for the reporting periods was based on

the aged nature of these accounts. In making its judgment, management assessed

its customers' ability to continue to pay their outstanding invoices and the

collectibility of those accounts on a timely basis, and whether their financial

position might deteriorate significantly in the future, which would result in

their inability to pay their debts to the Company.

Inventories,

which are primarily comprised of raw materials, packaging materials, and

finished goods, are stated at the lower of cost or net realizable value. Cost

being determined on the basis of a moving average. The Group evaluates the need

for reserves associated with obsolete, slow-moving and non-salable inventory by

reviewing net realizable values on a periodic basis.

As of

September 30, 2009 and 2008, the Group provided a reserve against its obsolete,

slow-moving or non-salable inventory amounting to $ 4,925,299 and $4,191,726,

respectively (please refer to Note 7 for details).

F-8

Property

and Equipment

Property

and equipment are recorded at cost and depreciated using the straight-line

method, with an estimated 5% salvage value of original cost, over the estimated

useful lives of the assets as follows:

|

20-30years

|

|

|

Machinery

and equipment

|

10-15

years

|

|

5

years

|

|

|

Electronics

and office equipment

|

5

years

|

Expenditures

for repairs and maintenance, which do not improve or extend the expected useful

lives of the assets, are expensed as incurred while major replacements and

improvements are capitalized.

When

property or equipment is retired or disposed of, the cost and accumulated

depreciation are removed from the accounts, with any resulting gains or losses

being included in net income or loss in the year of disposition, Impairment of

Long-Lived Assets.

The Group

evaluates potential impairment of long-lived assets, in accordance with

Statement of FASB Accounting Standards Codification (“ASC”) 360, Propoerty, Plant and

Equipment, which

requires the Group to (a) recognize an impairment loss only if the carrying

amount of a long-lived asset is not recoverable from its undiscounted cash flows

and (b) measure an impairment loss as the difference between the carrying amount

and fair value of the asset. As of September 30, 2009, the Group has provided a

full reserve against its Goodwill in the amount of $7,904,613 (Please refer to

Note 10 for details).

Intangible

Assets

The

Group’s intangible assets are stated at cost less accumulated amortization and

are comprised of land-use rights, drug permits and licenses, patent and

technology formulas know-how. Land-use rights are related to land the Group

occupies in Hubei and Guangdong Province, PRC and are being amortized on a

straight-line basis over a period of 40 years. Other intangible assets are being

amortized on a straight-line basis over a period of 10 years.

Revenue

Recognition

Among the

most important accounting policies affecting the Group’s consolidated financial

statements is its policy of recognizing revenue in accordance with the ASC 650,

Under this policy, all of the following criteria must be met in order for us to

recognize revenue:

1. Persuasive evidence of an arrangement

exists;

2. Delivery has occurred or services have

been rendered;

3. The seller's price to the buyer is fixed

or determinable; and

4. Collectibility is reasonably

assured.

The

majority of the Group's revenue results from sales contracts

with distributors and revenue is recorded upon the shipment of goods.

Management conducts credit background checks for new customers as a means

to reduce the subjectivity of assuring collectibility. Based on these

factors, the Group believes that it can apply the provisions of ASC 650

with minimal subjectivity. Sales are presented net of value added tax (VAT). No

return allowance is made as products returns are insignificant based on

historical experience.

F-9

Research

and Development

Research

and development (“R&D”) costs are expensed as incurred and consist primarily

of salaries and related expenses of personnel engaged in research and

development activities. The Group spent $283,473 and $249,357 on R&D efforts

for the nine month ended September 30, 2009 and 2008, respectively.

Income

Taxes

The Group

accounts for income taxes under the liability method in accordance with

ASC 740, Income

Taxes. Deferred tax assets and liabilities are recorded for the estimated

future tax effects of temporary differences between the tax basis of assets and

liabilities and amounts reported in the accompanying consolidated balance

sheets. Deferred tax assets are reduced by a valuation allowance if current

evidence indicates that it is considered more likely than not that these

benefits will not be realized.

Comprehensive

Income

The Group

has adopted ASC 220, Comprehensive Income, which establishes standards

for reporting and displaying comprehensive income, its components, and

accumulated balances in a full-set of general-purpose financial statements.

Accumulated other comprehensive income represents the accumulated balance of

foreign currency translation adjustments.

Concentration

of Credit Risk

A

significant portion of the Group's cash at September 30, 2009 and 2008 is

maintained at various financial institutions in the PRC which do not provide

insurance for amounts on deposit.

The Group

has not experienced any losses in such accounts and believes it is not exposed

to significant credit risk in this area.

The Group

operates principally in the PRC and grants credit to its customers in this

geographic region. Although the PRC is economically stable, it is

always possible that unanticipated events in foreign countries could disrupt the

Group’s operations.

The

following table shows the individual customer’s revenue and account receivable

balance which was higher than 5% of total revenue and total account receivables

for the nine months and three months ended September 30, 2009 and

2008:

|

NINE

MONTHS ENDED

SEPTEMBER

30,

|

THREE

MONTH ENDED

SEPTEMBER

30,

|

||||||||||||||||||||||||||||||||||

|

2009

|

2008

|

2009

|

2008

|

||||||||||||||||||||||||||||||||

|

(Unaudited)

|

(Unaudited)

|

(Unaudited)

|

(Unaudited)

|

||||||||||||||||||||||||||||||||

|

Revenue

|

$ | 17,345,065 |

%

|

$ | 19,860,057 |

%

|

$ | 5,904,653 |

%

|

$ | 6,634,434 |

%

|

|||||||||||||||||||||||

|

Individual customer's

revenue

|

|||||||||||||||||||||||||||||||||||

| 1 |

Zhuhai

Gongbei Pharmaceutical Co, Ltd.

|

4,195,255 | 24 | % | 3,711,204 | 19 | % | 1,234,516 | 21 | % | 784,911 | 12 | % | ||||||||||||||||||||||

| 2 |

Shenyang

Pharmaceutical Co. Ltd.

|

2,234,332 | 13 | % | 1,985,584 | 10 | % | 661,749 | 11 | % | 711,963 | 11 | % | ||||||||||||||||||||||

| 3 |

Shenzhen

Huihua Pharmaceutical Co. Ltd.

|

2,005,451 | 12 | % | 2,191,049 | 11 | % | 565,257 | 10 | % | 800,653 | 12 | % | ||||||||||||||||||||||

| 4 |

Jiangxi

Huiren Pharmaceutical Co. Ltd.

|

1,149,220 | 7 | % | 1,602,885 | 8 | % | 263,982 | 4 | % | 647,020 | 10 | % | ||||||||||||||||||||||

| 5 |

Hubei

Hengchuan Health Products Co.,Ltd.

|

1,388,420 | 8 | % | 2,221,744 | 11 | % | 687,044 | 12 | % | 578,655 | 9 | % | ||||||||||||||||||||||

| 6 |

Huhan

Jiuding Pharmaceutical Co, Ltd.

|

1,106,645 | 6 | % | - | - | 676,870 | 11 | % | - | - | ||||||||||||||||||||||||

|

Account

receivable, gross

|

$ | 15,551,342 |

%

|

$ | 13,222,313 |

%

|

15,551,342 |

%

|

13,222,313 |

%

|

|||||||||||||||||||||||||

|

Individual customer's

account receivable gross balance

|

|||||||||||||||||||||||||||||||||||

| 1 |

Zhuhai

Gongbei Pharmaceutical Co, Ltd.

|

2,326,483 | 15 | % | 1,769,557 | 13 | % | 2,326,483 | 15 | % | 1,769,557 | 13 | % | ||||||||||||||||||||||

| 3 |

Shenzhen

Huihua Pharmaceutical Co. Ltd.

|

1,593,203 | 10 | % | 1,186,189 | 9 | % | 1,593,203 | 10 | % | 1,186,189 | 9 | % | ||||||||||||||||||||||

| 4 |

Shenyang

Pharmaceutical Co. Ltd.

|

1,429,213 | 9 | % | 963,855 | 7 | % | 1,429,213 | 9 | % | 963,855 | 7 | % | ||||||||||||||||||||||

| 5 |

Hubei

Hengchuan Health Products Co.,Ltd.

|

1,276,973 | 8 | % | 1,232,435 | 9 | % | 1,276,973 | 8 | % | 1,232,435 | 9 | % | ||||||||||||||||||||||

| 2 |

Jiangxi

Huiren Pharmaceutical Co. Ltd.

|

923,509 | 6 | % | 519,536 | 4 | % | 923,509 | 6 | % | 519,536 | 4 | % | ||||||||||||||||||||||

| 6 |

Huhan

Jiuding Pharmaceutical Co, Ltd.

|

944,909 | 6 | % | - | - | 944,909 | 6 | % | - | - | ||||||||||||||||||||||||

F-10

Basic

and Diluted Earnings Per Share

The Group

adopted ASC 260, Earnings Per

Share. ASC 260 requires the presentation of earnings per share (EPS) as

Basic and Diluted EPS. Basic earnings per share are calculated by taking net

income divided by the weighted average shares of common stock outstanding during

the period. Diluted earnings per share is calculated by taking basic weighted

average shares of common stock and increasing it for dilutive common stock

equivalents such as warrants that are in the money.

Foreign

Currency Translation

The

functional currency of the Group is the Renminbi (“RMB”), the PRC’s currency.

The Group maintains its financial statements using the functional

currency. Monetary assets and liabilities denominated in currencies

other than the functional currency are translated into the functional currency

at rates of exchange prevailing at the balance sheet dates. Transactions

denominated in currencies other than the functional currency are translated into

the functional currency at the exchange rates prevailing at the dates of the

transaction. Exchange gains or losses arising from foreign currency transactions

are included in the determination of net income (loss) for the respective

periods.

For

financial reporting purposes, the financial statements of the Group, which are

prepared using the RMB, are translated into the Group’s reporting currency,

United States Dollars. Balance sheet accounts are translated using the closing

exchange rate in effect at the balance sheet date and income and expense

accounts are translated using the average exchange rate prevailing during the

reporting period. Adjustments resulting from the translation, if any,

are included in accumulated other comprehensive income (loss) in stockholder’s

equity.

The

exchange rates in effect at September 30, 2009 and 2008 were stated as follows:

(for RMB 1.00):

|

September

30,

|

September

30,

|

|||||||

|

2009

|

2008

|

|||||||

|

(Unaudited)

|

(Unaudited)

|

|||||||

|

Fixed

rate

|

$ | 0.1467 | $ | 0.1463 | ||||

|

Average

rate

|

$ | 0.1466 | $ | 0.1434 | ||||

For the

nine months ended September 30, 2009 and 2008, the foreign exchange loss was

$6,594 and $7,060 respectively; for the three months ended September 30, 2009

and 2008, the foreign exchange loss was $4,360 and $4,904,

respectively.

Fair

Value of Financial Instruments

ASC 825,

Financial Instruments,

defines financial instruments and requires fair value disclosures of those

financial instruments. On January 1, 2008, the Group adopted ASC 820, Fair Value Measurements and

Disclosures, which defines fair value, establishes a three-level

valuation hierarchy for disclosures of fair value measurement and enhances

disclosures requirements for fair value measures. Current assets and current

liabilities qualified as financial instruments and management believes their

carrying amounts are a reasonable estimate of fair value because of the short

period of time between the origination of such instruments and their expected

realization and if applicable, their current interest rate is equivalent to

interest rates currently available. The three levels are defined as

follow:

|

|

·

|

Level

1 -- inputs to the valuation methodology are quoted prices (unadjusted)

for identical assets or liabilities in active

markets.

|

F-11

|

|

·

|

Level

2 -- inputs to the valuation methodology include quoted prices for similar

assets and liabilities in active markets, and inputs that are observable

for the assets or liability, either directly or indirectly, for

substantially the full term of the financial

instruments.

|

|

|

·

|

Level

3 -- inputs to the valuation methodology are unobservable and significant

to the fair value.

|

As of the

balance sheet date, the estimated fair values of the financial instruments were

not materially different from their carrying values as presented due to the

short maturities of these instruments and that the interest rates on the

borrowings approximate those that would have been available for loans of similar

remaining maturity and risk profile at respective period-ends. Determining which

category an asset or liability falls within the hierarchy requires significant

judgment. The Group evaluates the hierarchy disclosures each

quarter.

Recent

Issued Accounting Pronouncements

In

June 2009, the Financial Accounting Standards Board (FASB) issued a

standard that established the FASB Accounting Standards Codification (ASC) and amended the

hierarchy of generally accepted accounting principles (ASC) and amended the

hierarchy of generally accepted accounting principles (GAAP) such that the ASC

became the single source of authoritative nongovernmental U.S. GAAP. The ASC did

not change current U.S. GAAP, but was intended to simplify user access to all

authoritative U.S. GAAP by providing all the authoritative literature related to

a particular topic in one place. All previously existing accounting standard

documents were superseded and all other accounting literature not included in

the ASC is considered non-authoritative. New accounting standards issued

subsequent to June 30, 2009 are communicated by the FASB through Accounting

Standards Updates (ASUs). The Company adopted the ASC on July 1, 2009. This

standard did not have an impact on the Company’s consolidated results of

operations or financial condition. However, throughout the notes to the

consolidated financial statements references that were previously made to

various former authoritative U.S. GAAP pronouncements have been changed to

coincide with the appropriate section of the ASC.

In

September 2006, the FASB issued an accounting standard codified in ASC 820,

Fair Value Measurements and

Disclosures. This standard established a single definition of fair value

and a framework for measuring fair value, set out a fair value hierarchy to be

used to classify the source of information used in fair value measurements, and

required disclosures of assets and liabilities measured at fair value based on

their level in the hierarchy. This standard applies under other accounting

standards that require or permit fair value measurements. One of the amendments

deferred the effective date for one year relative to nonfinancial assets and

liabilities that are measured at fair value, but are recognized or disclosed at

fair value on a nonrecurring basis. This deferral applied to such items as

nonfinancial assets and liabilities initially measured at fair value in a

business combination (but not measured at fair value in subsequent periods) or

nonfinancial long-lived asset groups measured at fair value for an impairment

assessment. The adoption of the fair value measurement standard did not

have a material impact on the Company’s consolidated results of operations or

financial condition.

F-12

In

December 2007, the FASB issued and, in April 2009, amended a new

business combinations standard codified within ASC 805, which changed the

accounting for business acquisitions. Accounting for business combinations under

this standard requires the acquiring entity in a business combination to

recognize all (and only) the assets acquired and liabilities assumed in the

transaction and establishes the acquisition-date fair value as the measurement

objective for all assets acquired and liabilities assumed in a business

combination. Certain provisions of this standard impact the determination of

acquisition-date fair value of consideration paid in a business combination

(including contingent consideration); exclude transaction costs from acquisition

accounting; and change accounting practices for acquisition-related

restructuring costs, in-process research and development, indemnification

assets, and tax benefits. The Company adopted the standard for business

combinations and adjustments to an acquired entity’s deferred tax asset and

liability balances and it had no immediate impact on the Company’s consolidated

financial position or results of operations.

In

December 2007, the FASB issued a new standard which established the

accounting for and reporting of noncontrolling interests (NCIs) in partially

owned consolidated subsidiaries and the loss of control of subsidiaries. Certain

provisions of this standard indicate, among other things, that NCIs (previously

referred to as minority interests) be treated as a separate component of equity,

not as a liability (as was previously the case); that increases and decreases in

the parent’s ownership interest that leave control intact be treated as equity

transactions, rather than as step acquisitions or dilution gains or losses; and

that losses of a partially owned consolidated subsidiary be allocated to the NCI

even when such allocation might result in a deficit balance. This standard also

required changes to certain presentation and disclosure requirements. The

Company adopted the standard beginning January 1, 2009. The provisions of

the standard were applied to all NCIs prospectively, except for the presentation

and disclosure requirements, which were applied retrospectively to all periods

presented. As a result, upon adoption, the Company retroactively reclassified

the “Minority interest in subsidiaries” balance previously included in the

“Other liabilities” section of the consolidated balance sheet to a new component

of equity with respect to NCIs in consolidated subsidiaries. The adoption also

impacted certain captions previously used on the consolidated statement of

income, largely identifying net income including NCI and net income attributable

to the Company. The adoption of this standard did not have a material

impact on the Company’s consolidated financial position or results of

operations.

In

April 2009, the FASB issued an accounting standard which provides guidance

on (1) estimating the fair value of an asset or liability when the volume

and level of activity for the asset or liability have significantly declined and

(2) identifying transactions that are not orderly. The standard also

amended certain disclosure provisions for fair value measurements and

disclosures in ASC 820 to require, among other things, disclosures in interim

periods of the inputs and valuation techniques used to measure fair value as

well as disclosure of the hierarchy of the source of underlying fair value

information on a disaggregated basis by specific major category of investment.

For 3M, this standard was effective prospectively beginning April 1, 2009.

The adoption of this standard did not have a material impact on the Company’s

consolidated results of operations or financial condition.

In

April 2009, the FASB issued an accounting standard which modifies the

requirements for recognizing other-than-temporarily impaired debt securities and

changes the existing impairment model for such securities. The standard also

requires additional disclosures for both annual and interim periods with respect

to both debt and equity securities. Under the standard, impairment of debt

securities will be considered other-than-temporary if an entity (1) intends

to sell the security, (2) more likely than not will be required to sell the

security before recovering its cost, or (3) does not expect to recover the

security’s entire amortized cost basis (even if the entity does not intend to

sell). The standard further indicates that, depending on which of the above

factor(s) causes the impairment to be considered other-than-temporary,

(1) the entire shortfall of the security’s fair value versus its amortized

cost basis or (2) only the credit loss portion would be recognized in

earnings while the remaining shortfall (if any) would be recorded in other

comprehensive income. The standard requires entities to initially apply its

provisions to previously other-than-temporarily impaired debt securities

existing as of the date of initial adoption by making a cumulative-effect

adjustment to the opening balance of retained earnings in the period of

adoption. The cumulative-effect adjustment potentially reclassifies the

noncredit portion of a previously other-than-temporarily impaired debt security

held as of the date of initial adoption from retained earnings to accumulated

other comprehensive income. The adoption of this standard did not have a

material impact on the Company’s consolidated results of operations or financial

condition.

F-13

In

April 2009, the FASB issued an accounting standard regarding interim

disclosures about fair value of financial instruments. The standard essentially

expands the disclosure about fair value of financial instruments that were

previously required only annually to also be required for interim period

reporting. In addition, the standard requires certain additional disclosures

regarding the methods and significant assumptions used to estimate the fair

value of financial instruments. The adoption of this standard did not have a

material impact on the Company’s consolidated results of operations or financial

condition.

In

May 2009, the FASB issued a new accounting standard regarding subsequent

events. This standard incorporates into authoritative accounting literature

certain guidance that already existed within generally accepted auditing

standards, with the requirements concerning recognition and disclosure of

subsequent events remaining essentially unchanged. This guidance addresses

events which occur after the balance sheet date but before the issuance of

financial statements. Under the new standard, as under previous practice, an

entity must record the effects of subsequent events that provide evidence about

conditions that existed at the balance sheet date and must disclose but not

record the effects of subsequent events which provide evidence about conditions

that did not exist at the balance sheet date. This standard added an additional

required disclosure relative to the date through which subsequent events have

been evaluated and whether that is the date on which the financial statements

were issued. For the Company,

this standard was effective beginning April 1, 2009.

In

June 2009, the FASB issued a new standard regarding the accounting for

transfers of financial assets amending the existing guidance on transfers of

financial assets to, among other things, eliminate the qualifying

special-purpose entity concept, include a new unit of account definition that

must be met for transfers of portions of financial assets to be eligible for

sale accounting, clarify and change the derecognition criteria for a transfer to

be accounted for as a sale, and require significant additional disclosure. The

standard is effective for new transfers of financial assets beginning

January 1, 2010. The adoption of this standard is not expected to have a

material impact on the Company’s consolidated results of operations or financial

condition.

In

June 2009, the FASB issued an accounting standard that revised the

consolidation guidance for variable-interest entities. The modifications include

the elimination of the exemption for qualifying special purpose entities, a new

approach for determining who should consolidate a variable-interest entity, and

changes to when it is necessary to reassess who should consolidate a

variable-interest entity. The standard is effective January 1, 2010. The

Company is currently evaluating the impact of this standard, but would not

expect it to have a material impact on the Company’s consolidated results of

operations or financial condition.

F-14

In

August 2009, the FASB issued ASU No. 2009-05, Measuring Liabilities at Fair

Value, which provides additional guidance on how companies should measure

liabilities at fair value under ASC 820. The ASU clarifies that the quoted price

for an identical liability should be used. However, if such information is not

available, a entity may use, the quoted price of an identical liability when

traded as an asset, quoted prices for similar liabilities or similar liabilities

traded as assets, or another valuation technique (such as the market or income

approach). The ASU also indicates that the fair value of a liability is not

adjusted to reflect the impact of contractual restrictions that prevent its

transfer and indicates circumstances in which quoted prices for an identical

liability or quoted price for an identical liability traded as an asset may be

considered level 1 fair value. This ASU is effective October 1, 2009. The

Company is currently evaluating the impact of this standard, but would not

expect it to have a material impact on the Company’s consolidated results of

operations or financial condition.

In

September 2009, the FASB issued ASU No. 2009-12, Investments in Certain Entities That

Calculate Net Asset Value per Share (or Its Equivalent), that amends ASC

820 to provide guidance on measuring the fair value of certain alternative

investments such as hedge funds, private equity funds and venture capital funds.

The ASU indicates that, under certain circumstance, the fair value of such

investments may be determined using net asset value (NAV) as a practical

expedient, unless it is probable the investment will be sold at something other

than NAV. In those situations, the practical expedient cannot be used and

disclosure of the remaining actions necessary to complete the sale is required.

The ASU also requires additional disclosures of the attributes of all

investments within the scope of the new guidance, regardless of whether an

entity used the practical expedient to measure the fair value of any of its

investments. This ASU is effective October 1, 2009. The Company is

currently evaluating the impact of this standard, but would not expect it to

have a material impact on the Company’s consolidated results of operations or

financial condition.

In

October 2009, the FASB issued ASU No. 2009-13, Multiple-Deliverable Revenue

Arrangements—a consensus of the FASB Emerging Issues Task Force, that

provides amendments to the criteria for separating consideration in

multiple-deliverable arrangements. As a result of these amendments,

multiple-deliverable revenue arrangements will be separated in more

circumstances than under existing U.S. GAAP. The ASU does this by establishing a

selling price hierarchy for determining the selling price of a deliverable. The

selling price used for each deliverable will be based on vendor-specific

objective evidence if available, third-party evidence if vendor-specific

objective evidence is not available, or estimated selling price if neither

vendor-specific objective evidence nor third-party evidence is available. A

vendor will be required to determine its best estimate of selling price in a

manner that is consistent with that used to determine the price to sell the

deliverable on a standalone basis. This ASU also eliminates the residual method

of allocation and will require that arrangement consideration be allocated at

the inception of the arrangement to all deliverables using the relative selling

price method, which allocates any discount in the overall arrangement

proportionally to each deliverable based on its relative selling price. Expanded

disclosures of qualitative and quantitative information regarding application of

the multiple-deliverable revenue arrangement guidance are also required under

the ASU. The ASU does not apply to arrangements for which industry specific

allocation and measurement guidance exists, such as long-term construction

contracts and software transactions. The ASU is effective beginning

January 1, 2011. The Company is currently evaluating the impact of this

standard on 3M’s consolidated results of operations and financial

condition.

F-15

In

October 2009, the FASB issued ASU No. 2009-14, Certain Revenue Arrangements That

Include Software Elements—a consensus of the FASB Emerging Issues Task

Force, that reduces the types of transactions that fall within the

current scope of software revenue recognition guidance. Existing software

revenue recognition guidance requires that its provisions be applied to an

entire arrangement when the sale of any products or services containing or

utilizing software when the software is considered more than incidental to the

product or service. As a result of the amendments included in ASU

No. 2009-14, many tangible products and services that rely on software will

be accounted for under the multiple-element arrangements revenue recognition

guidance rather than under the software revenue recognition guidance. Under the

ASU, the following components would be excluded from the scope of software

revenue recognition guidance: the tangible element of the product,

software products bundled with tangible products where the software components

and non-software components function together to deliver the product’s essential

functionality, and undelivered components that relate to software that is

essential to the tangible product’s functionality. The ASU also provides

guidance on how to allocate transaction consideration when an arrangement

contains both deliverables within the scope of software revenue guidance

(software deliverables) and deliverables not within the scope of that guidance

(non-software deliverables). The ASU is effective beginning January 1,

2011. The Company is currently evaluating the impact of this standard on the

Company’s consolidated results of operations and financial

condition.

5.

Trade

Receivables, Other Receivables, Prepaid expenses and Deposits

As

mentioned in Note 4 that the company estimates of the appropriate allowance on

those accounts receivable for the reporting periods was based on the aged nature

of these accounts. The table below shows the allowance for doubtful debts of the

Group’s trade receivables, other receivables and prepaid expenses and

deposits as of September 30, 2009 and December 31, 2008:

|

September

30,

|

December

31,

|

|||||||

|

2009

|

2008

|

|||||||

|

(Unaudited)

|

||||||||

|

Trade

receivables, gross

|

15,551,342 | $ | 13,123,374 | |||||

|

Allowance

for doubtful debts

|

(6,867,978 | ) | (3,786,459 | ) | ||||

|

Trade

receivables, net

|

8,683,364 | $ | 9,336,915 | |||||

|

September

30,

|

December

31,

|

|||||||

|

2009

|

2008

|

|||||||

|

Other receivables,

gross

|

678,528 | $ | 504,349 | |||||

|

Allowance

for doubtful debts

|

- | - | ||||||

|

Other receivables,

net

|

678,528 | $ | 504,349 | |||||

|

September

30,

|

December

31,

|

|||||||

|

2009

|

2008

|

|||||||

|

Prepaid

and deposits, gross

|

2,540,267 | $ | 918,209 | |||||

|

Allowance

for doubtful debts

|

- | |||||||

|

Prepaid

and deposits, net

|

2,540,267 | $ | 918,209 | |||||

F-16

The

change of the allowance for doubtful debts between the reporting periods, as of

September 30, 2009 and 2008, is displayed as follows:

|

NINE

MONTHS ENDED

SEPTEMBER

30,

|

||||||||

|

2009

|

2008

|

|||||||

|

(Unaudited)

|

(Unaudited)

|

|||||||

|

Balance

at beginning of period

|

$ | (3,786,459 | ) | $ | (943,647 | ) | ||

|

Provision

during the period

|

(3,080,334 | ) | (534,124 | ) | ||||

|

Foreign

exchange difference

|

(1,185 | ) | (74,297 | ) | ||||

|

Balance

at end of period

|

$ | (6,867,978 | ) | $ | (1,552,068 | ) | ||

The Group

set full allowance for trade receivables aged over 120 days which is general

credit term granted to the customers. After deducting those allowances from the

gross trade receivable, based on the management’s past experience, there would

be no collectability issue on the net amount.

6.

Refundable

Purchase Price Paid

On,

December 7, 2006, Benda Ebei paid $1.2 million to SECO (Shenzhen) Biotech Co.,

Ltd. (“SECO”) pursuant to a purchase agreement signed between SECO and Benda

Ebei on December 3, 2006 to acquire a technology know-how and drug

specifications and technical parameters in producing a Gastropathy drug owned by

SECO. According to the signed contract:

|

·

|

The

amount paid is refundable only if SECO fails to pass the examination

conducted by Benda Ebei;

|

|

·

|

Altogether,

there are three phases for the examination; however there is no specific

time-table for the examination;

|

|

·

|

The

contract is valid for 10 years upon the contract

signed.

|

As at

September 30, 2009, the deal has not been closed as the product is still under

the process of development. As the date when could SECO pass the examination

conducted by Benda Ebei cannot be determined, thus the amount paid is reported

as non-current assets as of September 30, 2009.

7.

Inventories,

Net

The

Group’s inventories at September 30, 2009 and December 31, 2008 comprised as

follows:

|

September

30,

|

December

31,

|

|||||||

|

2009

|

2008

|

|||||||

|

(Unaudited)

|

||||||||

|

Raw

materials

|

$ | 899,885 | $ | 874,180 | ||||

|

Packing

materials

|

161,938 | 481,724 | ||||||

|

Other

materials / supplies

|

83,510 | 88,412 | ||||||

|

Finished

goods

|

626,561 | 754,838 | ||||||

|

Work-in-process

|

5,497,187 | 5,086,780 | ||||||

|

Total

inventories at cost

|

7,269,082 | 7,285,934 | ||||||

|

Less:

Reserves on inventories

|

(4,925,299 | ) | (4,941,372 | ) | ||||

|

Total

inventories, net

|

$ | 2,343,783 | $ | 2,344,562 | ||||

F-17

A reserve

for obsolete, slow-moving or non-salable inventory was made on raw materials,

packing materials, other material and suppliers, finished goods and

work-in-process at the amount of $82,026, $39,786, $54,563, $6,507 and

$4,742,417 respectively as of September 30, 2009. As of December 31, 2008, there

was a reserve made on raw materials, packing materials, finished goods and

work-in-process at the amount of $122,433, $7,118, $269,749 and $4,542,072

respectively.

The

provision of reserve on work-in-process was resulted from the manufacturing

process of Gendicine, SiBiono’s sole product and SiBiono was acquired by the

company in April 2007.

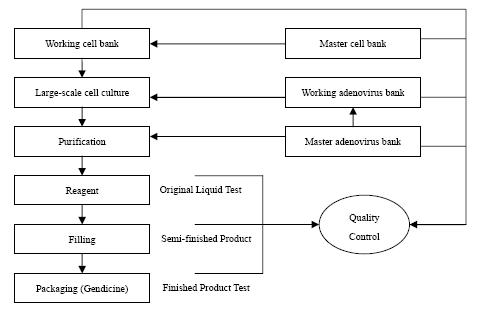

The

following chart shows the manufacturing process of Gendicine

(Ad-p53):

In the

production process of finished goods, Gendicine, several working steps are

needed: (i) large-scale culturing of adenovirus from master adenovirus bank;

(ii) culturing of cell from master cell bank; (iii) purification. The whole

process including step (i) to step (iii) takes approximately twenty-four days to

make reagent (“original liquid”). This particular liquid can only be stored for

approximately five years. It takes approximately another seven days for mixing

and bottling original liquid to finished goods which is known as

Gendicine.

Therefore,

up to the stage of reagent, all the related production costs are treated as

work-in-process. The major components of those production costs are: (i) direct

labor; (ii) direct materials; (iii) power; (iv) supplies and other materials and

(v) manufacturing overheads.

Before

acquisition, as of March 31, 2007, the accumulated units of original liquid

produced was 198,075 and which could be converted to approximately 226,736 vials

of Gendicine. However, the accumulated vials of Gendicine sold throughout the

years 2004 to three-months period ended March 31, 2007 were only approximately

18,424 vials. The accumulated production costs of $4,080,644 were remained as

work-in-process as of three-month period ended March 31, 2007.

F-18

Furthermore,

due to the special feature of the original liquid which can only be stored for

five years, and most of the original liquid was produced in the year of 2004,

and the provision of reserve on work in process was $3,696,083 as of three-month

period ended March 31, 2007.

After the

acquisition with the effective date April 1, 2007, the same accounting treatment

was adopted for the treatment of the provision of reserve on work-in-process. As

of September 30, 2009, the provision of reserve on work in process was

$4,742,417.

8.

Property

and Equipment, Net

The Group’s property and equipment at September 30, 2009 and December 31, 2008 were comprised as

follows:

|

December

31, 2008

|

Addition

|

Disposal

|

Foreign

Currency Translation Difference

|

September

30,

2009

|

||||||||||||||||

|

(Unaudited)

|

(Unaudited)

|

(Unaudited)

|

(Unaudited)

|

|||||||||||||||||

|

Buildings

|

$ | 9,692,441 | - | - | 3,261 | 9,695,702 | ||||||||||||||

|

Machinery

and equipment

|

16,769,328 | 10,444 | - | (890 | ) | 16,778,882 | ||||||||||||||

|

Office

equipment

|

40,728 | 3,356 | - | (3,779 | ) | 40,305 | ||||||||||||||

|

Motor

Vehicles

|

252,163 | - | - | (14 | ) | 252,149 | ||||||||||||||

|

Cost

|

26,754,660 | 13,800 | - | (1,421 | ) | 26,767,039 | ||||||||||||||

|

Less:

Accumulated Depreciation

|

||||||||||||||||||||

|

Buildings

|

$ | (1,559,511 | ) | (341,070 | ) | - | (367 | ) | (1,900,948 | ) | ||||||||||

|

Machinery

and equipment

|

(4,160,667 | ) | (1,221,246 | ) | - | (480 | ) | (5,382,393 | ) | |||||||||||

|

Office

equipment

|

(30,839 | ) | (17,970 | ) | - | (9 | ) | (48,818 | ) | |||||||||||

|

Motor

Vehicles

|

(89,863 | ) | (29,028 | ) | - | (14 | ) | (118,905 | ) | |||||||||||

|

Accumulated

Depreciation

|

(5,840,880 | ) | (1,609,314 | ) | - | (870 | ) | (7,451,064 | ) | |||||||||||

|

Construction

in progress

|

$ | 8,143,445 | 441,765 | 77 | (78 | ) | 8,585,055 | |||||||||||||

|

Total

property and equipment, net

|

$ | 29,057,225 | 27,901,030 | |||||||||||||||||

As

mentioned in Note 11, Benda Ebei entered into a commercial bank note issuance

agreement with Shanghai Pudong Development Bank on August 14, 2007 and a

supplementary agreement on January 21, 2008. Under the agreements the credit

facility is secured by the buildings, machinery and equipment of Benda Ebei and

Jiangling Benda. As of September 30, 2009, the net book value of pledged

property and equipment was approximately Rmb123.40 million (or $18.1 million) in

total.

The