Attached files

Exhibit

10.7

FAIRNESS

OPINION

Prepared

in conjunction with

A

Sale & Purchase of Assets by

Bluegate

Corporation

("SELLER")

And

A

Sperco Entity, Trilliant Corporation and SAI Corporation

("PURCHASERS")

November

6, 2009

1

November

6, 2009

Mr.

Charles Leibold

Chief

Financial Officer

Bluegate

Corporation

701 North

Post Oak Road, Suite 600

Houston,

Texas 77024

Dear Mr.

Leibold:

Convergent

Capital Appraisers, LLC (CCA) has been engaged by Bluegate Corporation (Company

or Bluegate or BGAT) to render a Fairness Opinion in regard to the following

described transactions.

Stephen Sperco (through a

Sperco entity controlled by him) will purchase certain assets from Bluegate

Corporation (“BGAT”) with payment made by a combination of cash and the

conversion of debt. The assets to be purchased will be the BGAT Medical Grade

Network (“MGN”) operation that supports clients with field engineers,

consulting, and the sale of product. Trilliant Corporation will purchase certain

assets from BGAT with a cash payment. The assets to be purchased will be the

Trilliant Technology Groups (“TTG”) consulting operation. SAI Corporation

(“SAIC”) will purchase certain assets from BGAT in exchange for a Mutual Release

in Full of certain claims. The assets to be purchased will be the Healthcare

Information Management Systems (“HIMS”) consulting operation. The

remaining Carrier/Circuit business will remain in Bluegate

Corporation.

2

Compliance

Standards - 5150 Fairness Opinions*

While we

are not specifically bound by the pronouncements of the Financial Industry

Regulatory Authority, Inc. (FINRA- formerly the National Association of

Securities Dealers NASD), it is our assessment that since the guidelines have

been endorsed by the United States Securities and Exchange Commission (SEC) as

being consistent with current disclosure regulations, we believe it prudent to

comply with the following disclosures.

*This

rule was introduced with the filing of SR-FINRA-2008-028 which has been approved

by the SEC. This rule became effective on December 15, 2008.

Disclosures

If at the

time a fairness opinion is issued to the board of directors of a company the

member issuing the fairness opinion knows or has reason to know that the

fairness opinion will be provided or described to the company's public

shareholders, the member must disclose in the fairness opinion:

|

|

(1)

if the member has acted as a financial advisor to any party to the

transaction that is the subject of the fairness opinion, and, if

applicable, that it will receive compensation that is contingent upon the

successful completion of the transaction, for rendering the fairness

opinion and/or serving as an

advisor;

|

|

|

(2)

if the member will receive any other significant payment or compensation

contingent upon the successful completion of the

transaction;

|

|

|

(3)

any material relationships that existed during the past two years or that

are mutually understood to be contemplated in which any compensation was

received or is intended to be received as a result of the relationship

between the member and any party to the transaction that is the subject of

the fairness opinion;

|

|

|

(4)

if any information that formed a substantial basis for the fairness

opinion that was supplied to the member by the company requesting the

opinion concerning the companies that are parties to the transaction has

been independently verified by the member, and if so, a description of the

information or categories of information that were

verified;

|

|

|

(5)

whether or not the fairness opinion was approved or issued by a fairness

committee; and

|

|

|

(6)

whether or not the fairness opinion expresses an opinion about the

fairness of the amount or nature of the compensation to any of the

company's officers, directors or employees, or class of such persons,

relative to the compensation to the public shareholders of the

company.

|

Disclosure

Responses

CCA has

not had and does not anticipate any involvement in the foregoing transaction

except to the extent of rendering this opinion regarding the fairness of the

transaction.

CCA’s

compensation in this matter is being paid by Bluegate Corporation and is based

upon hourly rates and a total fee estimate that has been contractually

agreed.

The only

relationship with Bluegate and CCA is through the predecessor firm of McClure,

Schumacher & Associates, LLP which provided valuation services relative to

accounting issues and FASB 141 in conjunction with the purchase of Trilliant in

2006 and 2007.

We have

not attempted to verify independently public or private information considered

in our valuation.

We have

expressed no opinions regarding the compensation of any parties to this

transaction.

Conclusion

Based

upon the criteria outlined in this report, and based upon our research and

analysis, it is our opinion that: (i) the overall terms and conditions of the

Purchase Transaction are fair from a financial point of view and (ii) pursuant

to the Transaction Terms, the shareholders of Bluegate are receiving no less

than adequate consideration.

Company

Overview

The

following business description is taken from the Company’s second quarter 10Q,

filed in July 2009. The Company has been trying to establish itself

as a leader in the healthcare information technology business. The

efforts have not been successful as indicated by the subsequent financial

information that shows continuous losses and the auditor’s opinion regarding

questions of “going concern.”

OUR

BUSINESS

Bluegate

provides the nation's only Medical Grade Network that facilitates physician and

clinical integration between hospitals and physicians in a secure private

environment. As a leader in providing the Healthcare industry outsourced

Information Technology (IT) solutions and remote IT management services,

Bluegate provides hospitals and physicians with a single source solution for all

of their clinical integration and IT needs. Additionally Bluegate provides IT

and telecommunications consulting through its professional services

organization.

CONSULTING

PRACTICE

Healthcare

institutions have very unique requirements not found in a typical commercial

environment. Our Healthcare consulting practice works with medical facilities

and systems on evaluation, procurement and implementation of healthcare related

voice, data, video, infrastructure and applications for the Healthcare

environment with a particular emphasis on the deployment of Electronic Medical

Record applications. Our IT/Telecommunications consulting practice works in

various industry verticals providing evaluation, procurement and implementation

of IT/Telecommunications solutions for our clients. Our Applications consulting

practice provides specific applications development, enhancement, coding, and

integration work for various industry verticals.

OUTSOURCING

Our

outsourcing offering includes help desk support and break-fix operations as well

as acquisition and special financing of equipment and services. It also can

include provisions for technology refresh, change management, and level of

service agreements. Our target market for such services consists of

private-practice physicians whose office staffs typically lack the in-house

technical expertise to support mission-critical computer systems and associated

hardware. In many cases, these private-practice physicians are affiliated with

our larger medical facility clients, creating a logical foundation for Bluegate

to establish and maintain long-term business relationships.

SYSTEMS

INTEGRATION AND MANAGED SECURITY SOLUTIONS

Our

systems integration and managed security group enables secure, HIPAA-compliant

data communication between hospitals, medical facilities and physician practices

from all locations via the services of our Bluegate Medical Grade Network

ultimately enhancing patient care. We also provide affordable access to

compatible medical-focused content and applications over a secure IT

infrastructure to improve practice efficiency and service. We extend IT Best

Practices to the edge of the healthcare network ensuring every access point for

the physician and healthcare location is as secure as the hospital

itself.

3

MARKET

OPPORTUNITY IN HEALTHCARE

Electronic

data communication networks have vast potential for enhancing the quality of

patient care, mitigating the soaring costs of healthcare, and protecting patient

privacy. To harness this potential, the current administration, Congress, and

administrative agencies are advocating that all physicians get connected to the

proposed national health information network (NHIN) system. A NHIN is expected

to enable physicians to write electronic prescriptions (eRx) and securely share

patient electronic health records (EHR), including medical images, with other

healthcare providers at hospitals, clinics, and individual physician

offices.

In

order to access and use the NHIN, individual physicians must have the

appropriate IT environment at their offices, and the hospitals where they admit

patients. Further, the hospitals' credentialed physicians must be on a common

HIPAA compliant network. Once the hospital has installed the necessary secure

electronic connectivity behind their firewall, the "last mile" of connectivity,

the figurative distance from the telecommunication provider's switch to an end

user (i.e. the physician), still presents a major challenge. In addition to

being HIPAA-compliant, the networks also need to be interoperable, which

requires assessing and augmenting physicians' existing IT equipment and

resources. Adequate training and technical support is necessary to ensure the

highest possible network availability and security and the ability to move and

manage information back and forth.

The

Administrative Simplification provisions of Title II of HIPAA require the United

States Department of Health and Human Services to establish national standards

for electronic healthcare transactions and national identifiers for providers,

health plans, and employers. It also addresses the security and privacy of

health data. Adopting these standards will improve the efficiency and

effectiveness of the nation's Healthcare system by encouraging the widespread

use of electronic data interchange in Healthcare. As the result of increasing

pressure for healthcare providers to adopt electronic health records and the

favorable healthcare IT environment created by the Stark Law exceptions there is

rapidly increasing demand for Bluegate's networks, technologies, remote

management, and professional IT services.

BLUEGATE

STRATEGY

Healthcare

Our

current short term strategies are to: (1) increase our market penetration of the

Houston hospital, centralized Healthcare, and physician markets; (2) commence

deployment of services in other Texas cities; and, (3) commence deployment of

services in other cities in the U.S. Our long term strategy is fivefold: (1)

fill as much of the national HIPAA-compliant secured communications void that

exists between the physician and the hospital as we can; (2) sell our services

to the physicians that utilize our Medical Grade Network enabling

them to choose Bluegate as their electronic health solutions firm and

as the IT outsource firm of choice for all of their technology needs; (3) to be

"THE" IT solutions resource to medical institutions, Healthcare facilities,

regional health information organizations (RHIOs), and centralized Healthcare

organizations (HCOs) for all their IT needs; (4) partner with a wide array of

third party providers of software, managed systems, pharmacy benefits, and many

other applications that must run on electronic networks and be installed in

hospitals, HCOs and medical practices; and (5) become the premier "boutique"

consulting practice supporting the deployment of Electronic Medical Record

systems and services.

Professional

Services

In

addition to the Professional Services initiatives in Healthcare, Bluegate

intends to continue to grow in the following areas through its Trilliant

Technology Group organization: (1) Further establish its reputation as one of

the top Telecommunications consulting organizations in the U.S.; and (2) expand

its IT Infrastructure consulting base.

GOING

CONCERN ISSUES

We

remain dependent on outside sources of funding for continuation of our

operations. Our independent registered public accounting firm included a going

concern qualification in their report dated April 9, 2009 (included in our

annual report on Form 10-K for the year ended December 31, 2008), which raises

substantial doubt about our ability to continue as a going concern.

During

the six months ended June 30, 2009 and the year ended December 31, 2008, we have

been unable to generate cash flows sufficient to support our operations and have

been dependent on debt and equity raised from qualified individual investors and

loans from a related party.

During

the six months ended June 30, 2009 and 2008, we experienced negative financial

results as follows:

|

Six

Months Ended June 30,

|

2009

|

2008

|

||||||

|

Net

loss

|

$ | (41,102 | ) | $ | (1,424,496 | ) | ||

|

Negative

cash flow from operations

|

$ | (127,269 | ) | $ | (208,669 | ) | ||

|

Negative

working capital

|

$ | (1,505,020 | ) | $ | (1,243,245 | ) | ||

|

Stockholders'

deficit

|

$ | (1,477,367 | ) | $ | (1,189,289 | ) | ||

These

factors raise substantial doubt about our ability to continue as a going

concern. The financial statements contained herein do not include any

adjustments relating to the recoverability and classification of recorded asset

amounts or amounts and classification of liabilities that might be necessary

should we be unable to continue in existence. Our ability to continue as a going

concern is dependent upon our ability to generate sufficient cash flows to meet

our obligations on a timely basis, to obtain additional financing as may be

required, and ultimately to attain profitable operations. However, there is no

assurance that profitable operations or sufficient cash flows will occur in the

future.

4

We

have supported the above operations by: (1) loans from a related party, (2)

raising additional operating cash through the private sale of our preferred and

common stock, (3) selling convertible debt and common stock to certain key

stockholders and (4) issuing stock and options as compensation to certain

employees and vendors in lieu of cash payments.

These

steps have provided us with the cash flows to continue our business plan, but

have not resulted in significant improvement in our financial position. We are

considering alternatives to address our cash flow situation that include: (1)

raising capital through additional sale of our common stock and/or debt

Securities and (2) reducing cash operating expenses to levels that are in line

with current revenues.

These

alternatives could result in substantial dilution of existing stockholders.

There can be no assurance that our current financial position can be improved,

that we can raise additional working capital or that we can achieve positive

cash flows from operations. Our long-term viability as a going concern is

dependent upon the following:

-

Our ability to locate sources of debt or equity funding to meet current

commitments and near-term future requirements.

-

Our ability to achieve profitability and ultimately generate sufficient cash

flow from operations to sustain our continuing operations.

Updated

Financial Analysis

In

preparing this report, we requested that Management through Mr. Charles Leibold

prepare an updated assessment of the financial picture of the Company as of the

middle of October 2009. The response is as follows:

|

·

|

Bluegate

Corporation is a public company traded on the OTCBB with 26 million shares

outstanding (50% of the outstanding shares are owned by three directors

who have differences among

themselves).

|

|

·

|

Bluegate

has had negative cash flow problems for several years and has never

received a clean opinion from the external auditors which have

consistently cited “going concern”

issues.

|

|

·

|

Revenue is decreasing as two

lines of business Trilliant Techology Group (TTG) and Healthcare

Information Management Systems (HIMS) have not generated any substantial

new business over the past year and will go dormant by end of November

2009. (2009 first half of year had

Revenue of ~$2M with P/L at around break-even, 2009 Q3 will have Revenue

~$760K with a loss from operations of ~$60K, and Forecast for 2009 Q4 is

Revenue ~$460K with a loss from operations of

~$300K)

|

|

·

|

Current

liabilities (there is no long term debt) of approximately $1,900,000

exceed current assets of approximately $300,000. Of the

$1,900,000 of liabilities, approximately $1,500,000 is owed to related

parties - Single secured creditor for $1,300,000 with UCC filing on all of

the Company’s assets and stock (from entity controlled by CEO/Director)

and approximately $90,000 from two Directors who were formerly

officers.

|

|

·

|

Operation

will not have cash to sustain another 30-45

days

|

Items

of Intangible Value within Bluegate – Not Included in the Sale

Public

filings indicate that the Company has a negative net worth based on tangible

assets. The following analysis examines the items of value that may

not be reported on the financial statements at fair value as defined

below.

The

Statement of Financial Accounting Standards No. 157(FAS 157)

“Fair

Value” is defined in FAS 157 as: the price that would be received to sell an

asset or paid to transfer a liability in an orderly transaction between market

participants at the measurement date. Because that exit price

objective applies for all assets and liabilities measured at fair value, any

fair value measurement requires that the reporting entity

determine:

|

|

·

The particular asset or liability that is the subject of the measurement

(consistent with its unit of

account);

|

|

|

·

For an asset, the valuation premise appropriate for the measurement

(consistent with its highest and best

use);

|

|

|

·

The principal (or most advantageous) market for the asset or liability

(for an asset, consistent with its highest and best

use);

|

|

|

·

The valuation technique(s) appropriate for the measurement, considering

the availability of data with which to develop inputs that represent the

assumptions that market participants would use in pricing the asset or

liability and the level in the fair value hierarchy within which the

inputs fall.

|

At the

end of the business description filed with the SEC (excerpted previously), there

is a note regarding networking services. This operation appears to be

the only one that has on-going value because there is an expectation that it

will generate a consistent flow of cash flow in excess of the cost of

services. It provides internet connectivity to corporate clients on a

subscription basis; essentially operating as a broker. It has several

customers and expects to generate about $350,000 in revenue and net about

$180,000 in gross margin or profit. In addition, whenever there are

technical issues or an opportunity to provide IT support, those tasks have

traditionally been referred to other operations within the Company or to outside

contractors. This operation is NOT included in the contemplated

transactions and it is to remain with Bluegate Corporation.

5

Terms

of the Deal

A Sperco

entity is an entity owned by Mr. Stephen Sperco who is also the largest

shareholder of Bluegate Corporation (BGAT) holding 4.5 million out of a total of

26 million shares outstanding. The MGN tangible and intangible assets

purchased from BGAT will be moved into a Sperco entity and the HIMS tangible

assets purchased from BGAT will be moved into SAI Corporation (“SAIC”) which an

entity is owned by Stephen Sperco.

Sperco

entity’s purchase price for the MGN assets will consist of $100,000 cash and

$100,000 in forgiveness of debt, plus an adjustment on a dollar for dollar basis

for any working capital. SAIC’s purchase price for the HIMS assets

will consist of a Mutual Release in Full of certain claims. The only tangible

assets to be transferred will be about $40,000 worth of furniture, fixtures and

electronic equipment that are part of the MGN and HIMS operations.

The

intangible assets include the following:

|

1.

|

Medical

Grade Network

|

|

a.

|

a

registered mark – “Medical Grade

Network”

|

|

b.

|

a

workforce of about 11 people

|

|

c.

|

approved

vendor status for the following:

|

|

MHHNP

|

Memorial

Hermann Health Ntwrk Prov-9401

|

|

Northwestern

Memorial Hospital

|

Bone

and Joint Clinic of Houston

|

|

Renaissance

HealthCare Systems

|

Global

Imaging

|

|

Memorial

Hermann Health Sys-Radiology

|

Malcolm

Bremer, MD

|

|

Houston

Digestive Disease Consultants

|

Southwest

Nephrology Associates, LLP

|

|

Advanced

Orthopedics & Sports Medicine

|

Cindy

Ivanhoe, MD, PA

|

|

Diabetes

Centers of America

|

Northwest

Oral Maxillofacial Surgery

|

|

G.I.

Specialists of Houston, LLP

|

Women's

Healthcare of Houston

|

|

Memorial

MRI & Diagnostic

|

Neurology,

Headache & Pain

|

|

Houston

Allergy & Asthma Associates

|

Houston

Fertility Institute

|

|

Urology

Associates

|

Memorial

Hermann Home Health

|

|

Pulmonary

Critical Care & Sleep Medicine

|

Cardiology

Associates of Houston

|

|

Texan

Imaging Centers (formerly Okomed)

|

Center

for Pain Recovery, PA

|

|

Gateway

To Care

|

Dynamic

Orthotics and Prosthetics

|

|

Leachman

Cardiology Associates, PA

|

US

Imaging

|

|

2.

|

Healthcare

Information Management Systems

|

Since the

HIMS operation has no on-going business it will go dormant by the end of

November 2009, and it is our assessment that without on-going operations this

operation has no intangible fair value.

|

3.

|

Trilliant

Corporation’s (“Trilliant”) (a company owned by William Koehler, former

Director/Corporate Officer of BGAT) purchase price for Trilliant

Technology Group, Inc’s. (“TTG”) assets of $5,000 cash and will

include:

|

|

a.

|

the

Trilliant corporate name

|

|

b.

|

future

revenues of about $20,000 (residual work on two ending contracts – which

will require hiring contract labor which is expected to cost as much as

the revenue)

|

In

additional to the tangible and intangible assets, it is important to note the

following circumstances and details regarding the transaction.

|

1.

|

Lease

and Labor

|

|

a.

|

BGAT

is obligated on a building lease for 7,290 square feet that runs until

2013 and costs about $9,000 per

month.

|

|

b.

|

BGAT

requires only five or six people to operate its carrier

business

|

|

c.

|

The

new Sperco entity will require less than 2,000 square feet for all its

operations post transaction. This would equate to about 27% of

the space or about $2,500 per

month.

|

|

d.

|

The

new Sperco entity has agreed to supply BGAT with accounting and

administrative staff, as well as technical support for the carrier

business, at no charge in exchange for free

rent.

|

|

e.

|

BGAT

intends to sublease as much of the space as possible as soon as

possible.

|

|

f.

|

Occupancy

by the new Sperco entity will defer to BGAT’s needs and

opportunities.

|

|

2.

|

Carrier

or Connectivity Operation

|

|

a.

|

This

operation is staying with BGAT

|

|

b.

|

This

is the only operation of BGAT that has been adequately

profitable.

|

|

c.

|

The

new Sperco entity is acquiring the Medical Grade Network operation which

provides maintenance support to BGAT’s Carrier customers. As

part of the transaction, Sperco agrees to continue providing that

support.

|

6

|

3.

|

Medical

Grade Network (MGN) Operation – Fair Value

Assessment

|

|

a.

|

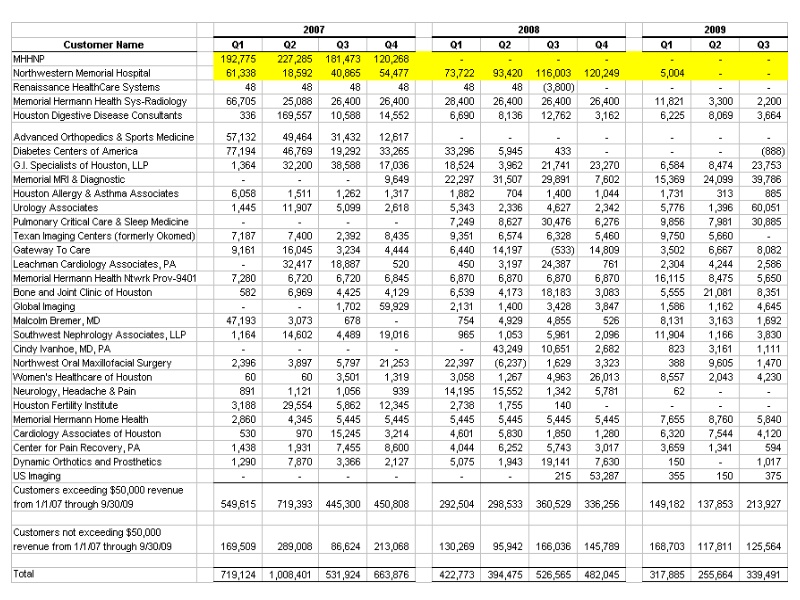

Revenues

have been declining over the last three years as indicated by the

following table. They appear to have stabilized in 2009 at

around $100,000 per month. The increase in revenues in quarter

3 of 2009 is attributed to several larger dollar projects that are not

expected to recur at the historic

levels.

|

|

b.

|

For

the nine months ended September 2009, this entity generated slightly more

than $900,000 in revenues and produced a gross margin (profit after direct

costs) of $130,000 or about 14%. However, after including

direct labors costs (reported as compensation) of $150,000, the operation

lost $20,000.

|

|

c.

|

It

must be noted that BGAT’s corporate overhead expense to maintain this

business operation far exceeds an industry norm of 10%, which accounts in

part for continuing ongoing losses.

|

|

d.

|

It

is our assessment that while “Medical Grade Network” has been registered

as a proprietary service mark, it does not appear (based on the trend of

revenues and with no pending contracts) to have developed independent

commercial recognition. What value does exist is subsumed

within the forecast cash flows as previously

analyzed.

|

|

4.

|

Healthcare

Information Management Systems (“HIMS”) Operation – Fair Value

Assessment

|

|

a.

|

Revenues

have been steadily declining during the nine months ended September 2009

and the remaining two contracts will end during November

2009.

|

|

b.

|

Since

the HIMS operation has no on-going business it will go dormant by the end

of November 2009, and it is our assessment that without on-going

operations this operation has no intangible fair

value.

|

|

5.

|

Trilliant

– Fair Value Assessment

|

|

a.

|

This

entity has no work force as of the end of September 2009 because of a lack

of on-going projects.

|

|

b.

|

The

remaining $20,000 in contract revenues will be earned through the use of

outside contractors (former Trilliant employees). The

expectation is that the additional cost of using outside contractors

rather than employees will consume any profit

potential.

|

|

c.

|

The

Trilliant name has not been established as a brand although it may be

recognized among previous

customers.

|

|

d.

|

Given

there are no pending contracts and no pending bids, the value of the

Trilliant name is considered to be minimal at

best.

|

Motivation

for the Transaction

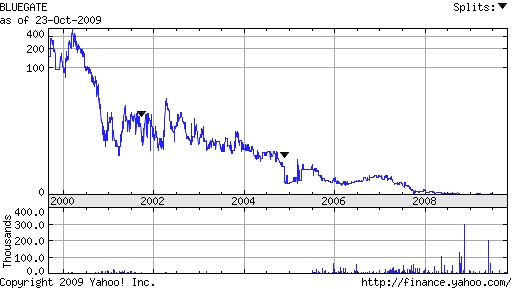

BGAT has

not been profitable since inception and the business model has proven to be

unsuccessful. According to Yahoo Finance, the Company has not

attracted any mutual fund or institutional investors. About 13.0

million of the 26 million shares outstanding – about ½ are held by three

individuals and one company. The price of a share has declined from

dollars to pennies over the last eight years and volume is

negligible.

To

resurrect the various operations will require expenditures for marketing and

business development. Given the poor stock performance, it is

unlikely that funds could be raised through a stock offering. The

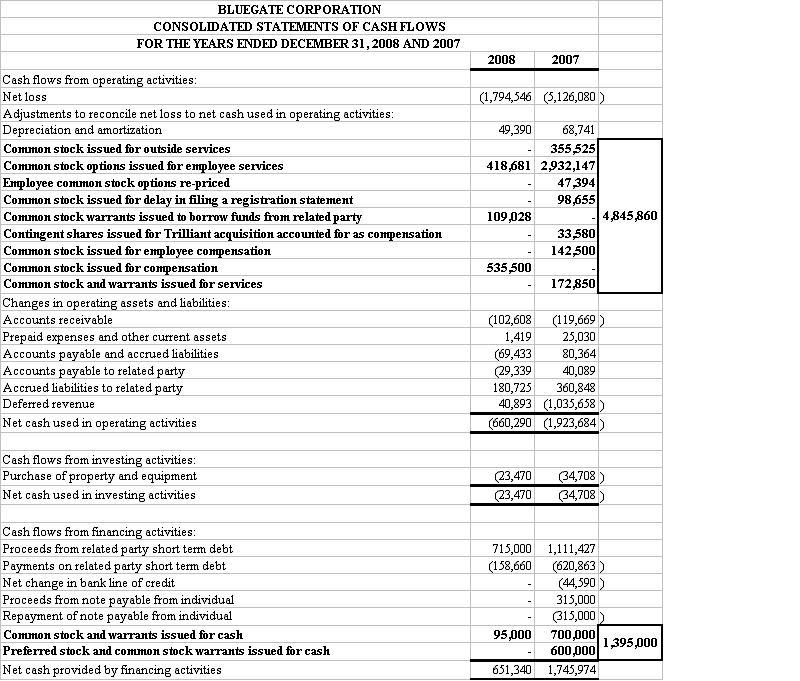

cash flow statement at right shows that over the past two calendar years,

approximately $6.25 million ($4.85 mil + $1.40 mil) has been raised through the

issuance of stock, options and warrants to fund operating losses which total

approximately $6.9 million over the two years ($1.8 mil + $5.1

mil).

All of

the Company’s assets are pledged against more than $1 million in debt, so it is

unlikely that loans could be secured from traditional lending

sources.

It is our

assessment that BGAT has approached a financial impasse that has required

drastic measures if bankruptcy is to be avoided.

7

Financial

tension within the organization has been caused by reduced compensation and

exchanging paychecks for stock as well as major internal

restructuring. This has lead to discord among the current and former

Directors which has the potential to escalate to legal action. If

lawsuits are brought into this already dire financial situation, the cost and

time delays will undoubtedly destroy what little value is left and bankruptcy

will most surely be the inevitable conclusion to BGAT’s existence.

The

proposed strategy is to minimize the loss and avoid

bankruptcy. Management believes that first and foremost, the

potential litigation must go away if progress is to be made. To that

end, it is our understanding that about $90,000 of the $100,000 cash purchase

price paid to BGAT for the MGN assets will be used to repay loans from Mr.

Sternberg and Mr. Koehler (two former Directors/employees/corporate

officers). In exchange, they will provide full release and waivers of

all claims.

Common

Shareholder Dilution

As

indicated by the balance sheet at right, even with an infusion of $100,000 and

the forgiveness of $100,000 of debt, shareholders’ equity will still be

negative. We see from the previous financial statements that the

Company has amassed large losses in the last two years and funded those losses

with dilutive shares. Approximately $1.4 million of cash was raised

while $4.8 million of shares / options / warrants were issued to cover

expenses.

While the

rate of loss has decreased in the last year, there is every expectation that

losses will continue if operations are allowed to continue. To cover

those losses, more and more shares will likely be issued as there is no

collateral for loans.

Continuing

to operate in this fashion will be detrimental to the common shareholders as

their ownership value continues to be diluted.

Without

the Sperco entity purchase, the common shareholders have little or no hope of

realizing any return on their investment.

8

Purchase

Prices Relative to Fair Value and Fairness

Given the

dire financial condition of BGAT, it is unrealistic to suggest that MGN be

placed with a business broker to sell because that would likely require between

six months and a year to locate a buyer and close the

transaction. Moreover, given the revenue trends, and a lack of future

contracts, it is uncertain whether a buyer could be found, particularly in a

down economy with tight credit.

Sperco

(through entities controlled by him) will be contributing the following

values

|

·

|

Cash

- $100,000

|

|

·

|

Forgiveness

of Debt $100,000

|

|

·

|

Accounting

and administrative services and technical support for the carrier business

as needed in exchange for short term free

rent.

|

The

determination of fairness is a measurement of relative values. Does

one party to the transaction benefit disproportionately and to the detriment of

another party. In this case, the question is whether the Sperco

entity, SAIC and Trilliant will benefit to the detriment of the common

shareholders.

Our

analysis of the fair value of the MGN assets included in this transaction

indicates that if anything, the price of $200,000 is likely a high price. The

total tangible collateral in this transaction is something less than $40,000

which means a loan value in the $30,000 range or less. TTG has no

on-going operations while MGN and HIMS’s operations have been trending

downward.

We know

that these three operations are insufficient to support BGAT’s overhead and if

they are not sold in short order, they will likely cease to exist.

Without

these sales, BGAT will continue to be in default on its loans and given the

state of financial resources, will be forced to file for bankruptcy

protection. Between legal and trustee fees, what few resources are

left will be consumed and the common shareholders will receive

nothing.

Conclusion

Based

upon the foregoing evidence and analysis, it is our opinion that this

transaction is fair from a financial point of view as it provides the common

shareholders with more value than any other likely

scenario. Moreover, the prices being paid to BGAT is assessed as

meeting or exceeding what we have determined to be a fair value for the assets

to be sold to the Sperco entity, SAIC and Trilliant.

Certification

In

rendering our opinion, we have relied without independent verification upon the

accuracy and completeness of the financial and other information provided by

Bluegate Corporation and their agents.

We have

assumed such information to be correct and complete in all material

aspects.

We have

not attempted to independently verify public or private information considered

in our valuation.

We have

held discussions with Management regarding the condition and outlook for its

operations, and have made such other investigations and analyses, as we have

deemed necessary.

We have

assumed that there has been no material change in Bluegate Corporation’s

financial condition, results of operations, business or prospects since the date

of the last financial statements unless otherwise noted.

We

believe that the analysis of management’s anticipated performance and resulting

lack of cash flow is a reasonable estimation, based upon past performance and

based on the information available to us at this time. In addition,

Bluegate Corporation’s management has represented that there are no pending

contracts or work in progress that have not been disclosed.

The

preparation of a fairness opinion involves various determinations as to the most

appropriate and relevant quantitative and qualitative methods of financial

analyses and the application of those methods to the particular

circumstances. Therefore, such an opinion is not readily susceptible

to the partial analysis or summary description. Furthermore, in

arriving at our opinion, we did not attribute any particular weight to any

specific analysis or factor. Rather, we have made qualitative

judgments as to the significance and relevance of each.

Accordingly,

Convergent Capital Appraisers believes that our analysis must be considered as a

whole.

In our

analyses, we made numerous assumptions with respect to industry performance,

general business and economic conditions and other matters, many of which are

beyond the control of Bluegate Corporation. Any estimates contained

in these analyses are not necessarily indicative of actual values or predictive

of future results or values, which may be significantly more or less favorable

than as set forth therein.

Convergent

Capital Appraisers or through a predecessor firm McClure, Schumacher and

Associates, LLP have previously performed independent valuations of Bluegate

Corporation or related entities.

Neither

Convergent Capital Appraisers nor the individuals involved with this analysis

have any present or contemplated future interest in the Plan or Bluegate

Corporation or any other interest that might tend to prevent making a fair and

unbiased appraisal.

These

conclusions are based upon methodologies and financial fairness considerations

that we deem appropriate. In accordance with recognized professional

ethics, our fees for this service are not contingent upon the opinions expressed

herein.

This

Opinion is furnished solely for the benefit of Management and the Board of

Directors and may not be relied upon by any other person or for any other

purpose without our express, prior, written consent.

This

Opinion is delivered subject to the conditions, scope of the engagement,

limitations and understandings set forth in this Opinion and our engagement

letter.

9

Convergent

Capital Appraisers shall not be subjected to any personal liability whatsoever

to any person, or on behalf of you or your affiliates. Convergent

Capital Appraisers has been retained on behalf of and has delivered this Opinion

solely to the Management and the Board of Directors.

Notwithstanding

that, Convergent Capital Appraisers’ fees and expenses are being paid by

Bluegate Corporation and certain covenants and representations have been made by

Bluegate Corporation.

Sincerely,

By: /s/ Jeffrey A. Schumacher

Jeffrey

A. Schumacher

10

Interviews

Multiple

teleconferences were held with Mr. Charles Leibold over the period of October 21

through November 6, 2009. The report has been submitted in draft form

to the Board of Directors for review and comment.

Upon

receiving the Board’s comments and suggestions, the report was finalized and

signature affixed.

Bibliography

|

·

|

Bluegate

Corporation SEC filing 10Q for the quarters ended 2005 –

2008

|

|

·

|

Internally

prepared financial statements and supporting as well as specially prepared

related schedules for the nine months ended September

2009

|

|

·

|

Synopsis

of the purchase and sale contract between the Sperco entity and Bluegate

Corporation

|

11

Curriculum

Vitae

Jeffrey

A. Schumacher, CPA, ABV, ASA

EDUCATION &

CERTIFICATIONS

Certified

Public Accountant (CPA) State of Texas

Accredited

in Business Valuation (ABV)

American Institute of Certified Public

Accountants

Accredited

Senior Appraiser / Business Valuation (ASA)

American Society of

Appraisers

B.B.A. (1976)

Finance Major Valparaiso University

PROFESSIONAL

AFFILIATIONS

American

Institute of Certified Public Accountants

American

Society of Appraisers – Accredited Senior Member

ASA

Houston Chapter Treasurer 2003-2004

ASA

Houston Chapter President 2004-2005

PROFESSIONAL

EXPERIENCE

2007 -

Present FOUNDER

and MANAGING MEMBER

Convergent Capital Appraisers

LLC

Houston, Texas

|

|

Business

valuation, forensic analysis, special issue damages, business interruption

claims, interim management, litigation support, family law issues,

valuation and consulting in mergers and acquisitions, partnership

dissolutions, dissenting stockholder disputes, ESOP appraisals,

partnership disputes, insurance fraud, patent infringement and estate and

gift taxation issues. Jeff was a pioneer in the design of

business valuation software beginning in the early

1980s.

|

1996 -

2007 FOUNDER

and PARTNER

McClure, Schumacher & Associates

L.L.P.

Houston, Texas

|

|

Business

appraisal, litigation support, financial consulting and mergers and

acquisitions

|

1990 -

1996 FOUNDER

and PARTNER

Smith & Schumacher

Houston, Texas

|

|

Business

appraisal, litigation support, financial consulting and mergers and

acquisitions

|

1983 -

1990 ANALYST

|

|

Served

as a contract financial analyst for several valuation firms in Houston and

Dallas, Texas. These firms included Certified Business Brokers,

Abraham & Associates, Highview Services, Aden-Smith, and American

Business Group.

|

12

SPEAKING

ENGAGEMENTS

|

|

Texas Society of

Certified Public Accountants

|

|

|

1995,

1996, 1997 Asset Protection through Family Limited

Partnerships

|

|

|

1994

Litigation Support Conference – Commercial vs. Personal

Goodwill

|

|

|

1997

Litigation Support Conference - Discounts – What’s

Fair

|

|

|

1997

Galveston Family CPE Conference - Basics of Business

Valuation

|

|

|

1998

Galveston Family CPE Conference - Use and Abuse of

Discounts

|

|

|

1999

South Texas School of Law – Litigation Support Conference –Daubert

Discussion Panelist

|

|

|

2000

Advanced Family Law Conference – Internet Research &

Sites

|

|

|

2000

South Texas School of Law – Litigation Support Conference – Damage Models

Discussion Panelist

|

|

|

AWSPA-ASWA 54th Annual

Conference

|

|

|

1994 Basic

Business Valuation Techniques and

Issues

|

|

|

Houston Bar

Association, Family Law

Section

|

|

|

1995

Appraising the Appraiser: Family Law

Valuations

|

|

|

2003

Section 1041 and Marital Property

Divisions

|

|

|

American Society of

Appraisers

|

|

|

1998

Daubert & Robinson

|

|

|

Northeast Harris

County Bar Association

|

|

|

2000

Equitable Interest

|

|

|

University of

Houston

|

|

|

2002

Business Valuation - Discounts

|

|

|

2003

Business Valuation - Discounts

|

|

|

2004

Business Valuation – Discounts

|

|

|

Financial Consulting

Group

|

|

|

2004

A multiple Regression Model for Predicting

Discounts

|

|

|

Materials Marketing

Associates, Inc.

|

|

|

2008

Annual Meeting, Miami, FL – Business Valuation and Exit

Strategies

|

PUBLICATIONS

Houston Business Journal

July 16-22, 1999

So How Much Is My Closely Held Business

Worth?

Houston Business Journal May

16-22, 2003

Small Business Owners May Face Big

Challenges in Divorce Court

Valuation Strategies

September/October 2005

Estimating Minority Interest

Discounts

13