Attached files

| file | filename |

|---|---|

| EX-31 - EXHIBIT 31.1 - CAMBER ENERGY, INC. | lei093009qex311.htm |

| EX-32 - EXHIBIT 32.1 - CAMBER ENERGY, INC. | lei093009qex321.htm |

| EX-32 - EXHIBIT 32.2 - CAMBER ENERGY, INC. | lei093009qex322.htm |

| EX-31 - EXHIBIT 31.2 - CAMBER ENERGY, INC. | lei093009qex312.htm |

1

| LUCAS ENERGY, INC. | |||

| FORM 10-Q | |||

| For the Quarterly Period Ended September 30, 2009 | |||

| TABLE OF CONTENTS | |||

| Page | |||

| PART I – FINANCIAL INFORMATION | |||

| Item 1. | Financial Statements | ||

| o | Consolidated Balance Sheets as of September 30, 2009 and March 31, 2009 (unaudited) | 3 | |

| o | Consolidated Statements of Operations for the three months ended September 30, 2009 | ||

| and 2008 and for the six months ended September 30, 2009 and 2008 (unaudited) | 4 | ||

| o | Consolidated Statement of Stockholders’ Equity for the six months ended September 30, | ||

| 2009 (unaudited) | 5 | ||

| o | Consolidated Statements of Cash Flows for the six months ended September 30, 2009 and | ||

| 2008 (unaudited) | 6 | ||

| o | Notes to the Consolidated Financial Statements (unaudited) | 7 | |

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 14 | |

| Item 3. | Quantitative and Qualitative Disclosures about Market Risk | 21 | |

| Item 4. | Controls and Procedures | 21 | |

| PART II – OTHER INFORMATION | |||

| Item 1. | Legal Proceedings | 22 | |

| Item 1A. | Risk Factors | 22 | |

| Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds | 22 | |

| Item 3. | Defaults Upon Senior Securities | 22 | |

| Item 4. | Submission of Matters to a Vote of Security Holders | 22 | |

| Item 5. | Other Information | 22 | |

| Item 6. | Exhibits | 23 | |

| EXHIBITS | 25 | ||

2

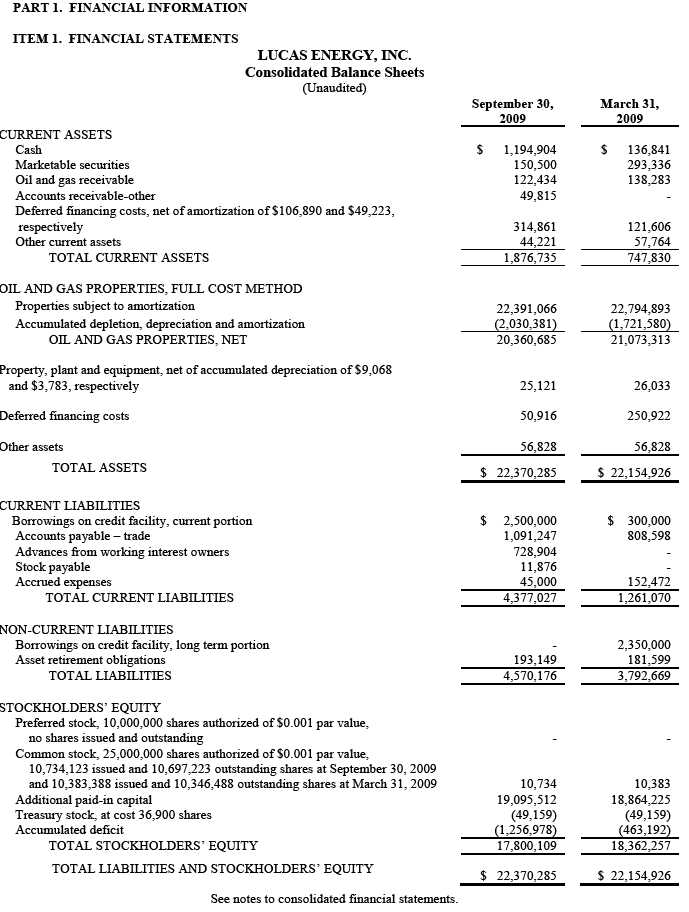

3

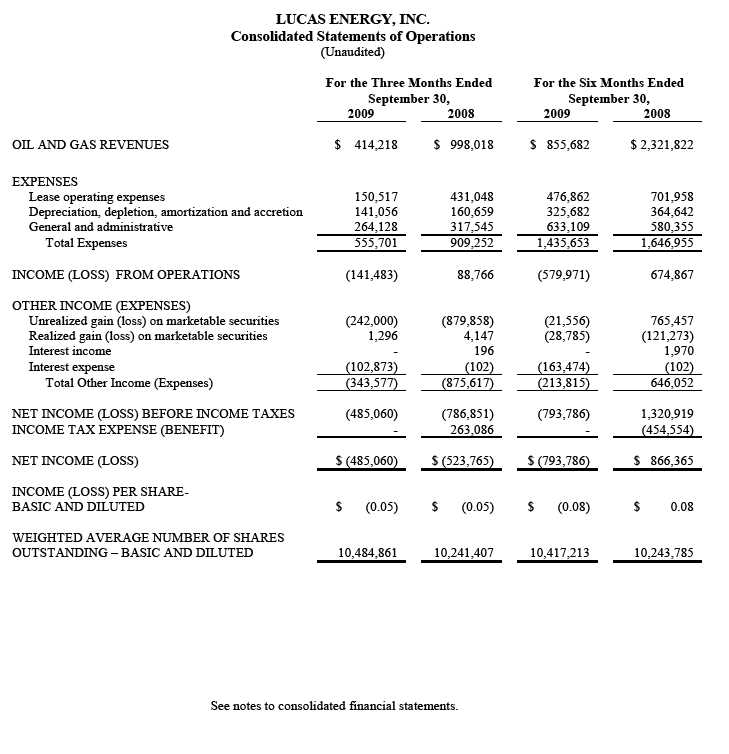

4

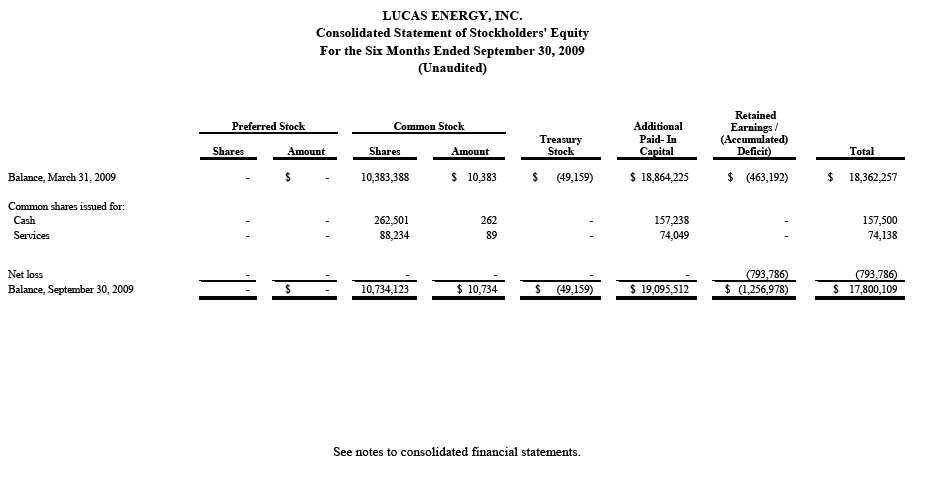

5

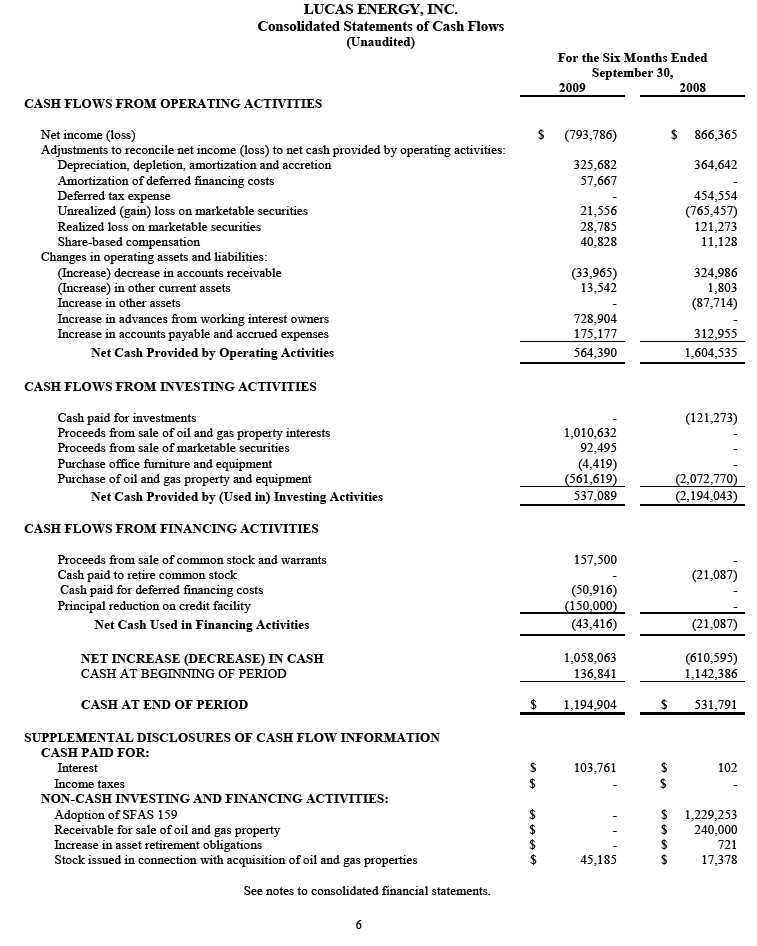

LUCAS ENERGY, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

NOTE 1. BASIS OF PRESENTATION

The accompanying unaudited interim consolidated financial statements of Lucas Energy, Inc. ("Lucas") have been prepared in accordance with accounting principles generally accepted in the United States of America and the rules of the Securities and Exchange Commission, and should be read in conjunction with the audited financial statements and notes thereto contained in Lucas' annual report filed with the SEC on Forms 10-K and 10-K/A for the year ended March 31, 2009. In the opinion of management, all adjustments, consisting of normal recurring adjustments, necessary for a fair presentation of financial position and the results of operations for the interim periods presented have been reflected herein. The results of operations for interim periods are not necessarily indicative of the results to be expected for the full year. Notes to the financial statements which would substantially duplicate the disclosure contained in the audited financial statements for the most recent fiscal year 2009 as reported in Form 10-K have been omitted.

NOTE 2 – ORGANIZATION AND HISTORY

The Company was incorporated on December 16, 2003 in the State of Nevada as Panorama Investments, Corp

( Panorama ). On June 16, 2006 the Company consummated a share exchange with Lucas Energy Resources, Inc. ( Lucas Resources ), a privately held oil and gas company which held oil and gas lease acreage and producing reserves in the State of Texas. The share exchange was made pursuant to a May 19, 2006 Acquisition and Exchange Agreement whereby the Company acquired all of the issued and outstanding capital stock from the Lucas Resources shareholders. The share exchange was effected through an exchange of shares with the prior shareholders of Lucas Resources assuming control of and responsibilities for the Company’s activities. In conjunction with the share exchange, the name of Panorama was changed to Lucas Energy, Inc. ( Lucas ).

NOTE 3 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Use of Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Lucas' consolidated financial statements are based on a number of significant estimates, including oil and gas reserve quantities which are the basis for the calculation of depreciation, depletion and impairment of oil and gas properties, estimates of tax benefits and obligations and timing and costs associated with its retirement obligations.

Cash and Cash Equivalents

Cash and cash equivalents include cash in banks and financial instruments which mature within three months of the date of purchase.

Concentration of Credit Risk

Financial instruments that potentially subject Lucas to concentration of credit risk consist of cash and accounts receivable. Cash balances exceeded FDIC insurance protection levels by approximately $820,900 at September 30, 2009 and at certain points throughout the quarter subjecting Lucas to risk related to the uninsured balance. Lucas’ deposits are held at large established bank institutions and it believes that the risk of loss associated with these uninsured balances is remote.

7

Accounts receivable are recorded at invoiced amount and generally do not bear interest. Any allowance for doubtful accounts is based on management's estimate of the amount of probable losses due to the inability to collect from customers. As of September 30, 2009, no allowance for doubtful accounts has been recorded. Lucas’ oil and gas accounts receivable are collateral to the Revolving Line of Credit with Amegy Bank.

Sales to one customer comprised 89% and 87% of Lucas’ total oil and gas revenues for the three and six months ended September 30, 2009, respectively. Lucas believes that, in the event that its primary customer was unable or unwilling to continue to purchase Lucas’ production, there are several alternative buyers for its production at comparable prices.

Marketable Securities

Lucas reports its short-term investments and other marketable securities at fair value. At September 30, 2009, Lucas' short-term investments consisted of shares of common stock held in Bonanza Oil & Gas, Inc. ( Bonanza ). The shares of Bonanza common stock held by Lucas have always been recorded on Lucas' balance sheet at fair value. Prior to

Lucas’ adoption of Statement of Financial Accounting Standards ( SFAS ) No. 159, The Fair Value Option for Financial Assets and Financial Liabilities – Including an Amendment of FASB Statement No. 115 ( Statement No. 159 , ASC 825 Financial Instruments) on April 1, 2008, Lucas reported changes in the fair value marketable securities that it held directly to stockholders’ equity as part of accumulated other comprehensive income ,

Upon the April 1, 2008 adoption of Statement No. 159 provisions allowing the Company the option to value its financial assets and liabilities at fair value on an investment by investment basis, the changes in the fair value of assets and liabilities are now reported in Lucas’ results of operations in the period that the change in fair value occurs. Prior to the adoption of Statement No. 159, Lucas had cumulative unrealized gains on Bonanza common stock of $1,229,253 (net of deferred taxes of $633,252) that were reported as other comprehensive income. The cumulative historical unrealized gain was reclassified on Lucas’ balance sheet from accumulated other comprehensive income to retained earnings on April 1, 2008, and the associated deferred tax portion of the unrealized gain totaling $633,252 was reflected in deferred tax liabilities.

For the six month period ended September 30, 2009 Lucas reported a non-cash unrealized loss on its Bonanza shares of common stock of $21,556 pursuant to mark-to-market accounting requirements. For the six month period ended September 30, 2009 Lucas realized a loss on the sale of a portion of the Bonanza shares held totaling $28,785.

Fair Value of Financial Instruments

As of September 30, 2009, the fair value of cash, accounts receivable and accounts payable approximate carrying values because of the short-term maturity of these instruments.

Oil and Gas Properties, Full Cost Method

Lucas uses the full cost method of accounting for oil and gas producing activities. Costs to acquire mineral interests in oil and gas properties, to drill and equip exploratory wells used to find proved reserves, and to drill and equip development wells including directly related overhead costs and related asset retirement costs are capitalized.

Under this method, all costs, including internal costs directly related to acquisition, exploration and development activities are capitalized as oil and gas property costs on a county by country basis. Properties not subject to amortization consist of exploration and development costs which are evaluated on a property-by-property basis. Amortization of these unproved property costs begins when the properties become proved or their values become impaired. Lucas assesses the realizability of unproved properties, if any, on at least an annual basis or when there has been an indication that impairment in value may have occurred. Impairment of unproved properties is assessed based on management's intention with regard to future exploration and development of individually significant properties and the ability of Lucas to obtain funds to finance such exploration and development. If the results of an assessment indicate that the properties are impaired, the amount of the impairment is added to the capitalized costs to be amortized.

Costs of oil and gas properties are amortized using the units of production method. Amortization expense calculated per equivalent physical unit of production amounted to $20.56 per barrel of oil equivalent ( BOE ) for the fiscal year ended

March 31, 2009 and $20.30 for the quarter period ended September 30, 2009.

8

Ceiling Test

In applying the full cost method, Lucas performs an impairment test (ceiling test) at each reporting date, whereby the carrying value of property and equipment is compared to the estimated present value, of its proved reserves discounted at a 10-percent interest rate of future net revenues, based on current economic and operating conditions at the end of the period, plus the cost of properties not being amortized, plus the lower of cost or fair market value of unproved properties included in costs being amortized, less the income tax effects related to book and tax basis differences of the properties. If capitalized costs exceed this limit, the excess is charged as an impairment expense. As of September 30, 2009 no impairment of oil and gas properties was recorded.

Furniture and Office Equipment

Furniture and office equipment are stated at cost. Depreciation is computed on a straight-line basis over the estimated useful lives of two to five years.

Deferred Taxes

Deferred taxes are provided on the liability method whereby deferred tax assets are recognized for deductible temporary differences and operating loss and tax credit carry forwards and deferred tax liabilities are recognized for taxable temporary differences. Temporary differences are the differences between the reported amounts of assets and liabilities and their tax bases. Deferred tax assets are reduced by a valuation allowance when, in the opinion of management, it is more likely than not that some portion or all of the deferred tax assets will not be realized. Deferred tax assets and accrued tax liabilities are adjusted for the effects of changes in tax laws and rates on the date of enactment.

Earnings per Share of Common Stock

Basic and diluted net income per share calculations are calculated on the basis of the weighted average number of common shares outstanding during the reporting period. Purchases of treasury stock reduce the outstanding shares commencing on the date that the stock is purchased. Common stock equivalents are excluded from the calculation when a loss is incurred as their effect would be anti-dilutive. On September 30, 2009 all options and warrants outstanding were out of the money ; and are therefore, anti-dilutive and excluded from the calculation of basic and diluted net income (loss) earnings per share.

Revenue and Cost Recognition

Lucas recognizes oil and natural gas revenue under the sales method of accounting for its interests in producing wells as oil and natural gas is produced and sold from those wells. Oil and natural gas sold by Lucas is not significantly different from Lucas’ share of production. Costs associated with production are expensed in the period incurred.

Recent Accounting Pronouncements

In April 2009, the FASB issued FSP No. FAS 157-4, “Determining Fair Value When the Volume and Level of Activity for the Asset or Liability Have Significantly Decreased and Identifying Transactions That Are Not Orderly” (FAS 157-4, ASC 820 Fair Value Measurement and Disclosures) to amend SFAS 157, . FAS 157-4 provides additional guidance for estimating fair value in accordance with SFAS 157 when the volume and level of activity for an asset or liability has significantly decreased. In addition, FAS 157-4 includes guidance on identifying circumstances that indicate a transaction is not orderly. FAS 157-4 is effective for interim and annual reporting periods ending after June 15, 2009. The Company is currently assessing the impact, if any, that the adoption of this pronouncement will have on the

Company’s operating results, financial position or cash flows.

In December 2008, the SEC released Final Rule, Modernization of Oil and Gas Reporting The new disclosure requirements include provisions that permit the use of new technologies to determine proved reserves if those technologies have been demonstrated empirically to lead to reliable conclusions about reserve volumes. The new requirements also will allow companies to disclose their probable and possible reserves to investors. In addition, the new disclosure requirements require that companies 1) report the independence and qualifications of its reserves

9

preparer or auditor, 2) file reports when a third party is relied upon to prepare reserves estimates or conduct a reserves audit, 3) report oil and gas reserves using an average price based upon the prior 12-month period rather than year-end prices. The new disclosure requirements are effective for financial statements for fiscal years ending on or after December 31, 2009. Early adoption is not permitted. The Company is currently assessing the impact, if any that the adoption of the pronouncement will have on the Company’s operating results, financial position or cash flows.

In June 2009, the FASB issued Statement No. 168, The FASB Accounting Standards Codification and the Hierarchy of Generally Accepted Accounting Principles ( SFAS 168 , ASC 105-10 Generally Accepted Accounting Principles), which amends SFAS No. 162, The Hierarchy of Generally Accepted Accounting Principles . SFAS 168 will become the source of authoritative U.S. GAAP recognized by the FASB to be applied by nongovernmental entities. Rules and interpretive releases of the SEC under the authority of federal securities laws are also sources of authoritative GAAP for SEC registrants. On the effective date, SFAS 168 will supersede all then existing non-SEC accounting and reporting standards. All other non-grandfathered non-SEC accounting literature not included in SFAS 168 will become non-authoritative. SFAS 168 is effective for financial statements issued for interim and annual periods ending after September 15, 2009. The adoption of SFAS 168 did not impact our results of operations or financial condition.

Lucas does not expect that any other recently issued accounting pronouncements will have a significant impact on the financial statements of the Company.

Reclassifications

Certain amounts in prior periods have been reclassified to conform to the current period presentation.

NOTE 4 - FAIR VALUE MEASUREMENTS

The carrying values of cash and cash equivalents, accounts receivable and accounts payable (including income taxes payable and accrued expenses) included in the accompanying consolidated balance sheets approximated fair value at June 30, 2009, and they are not presented in the following table associated with the fair value measurement of Lucas’ investments.

Statement No. 157 (ASC 820) establishes a fair value hierarchy that prioritizes the inputs to valuation techniques used to measure fair value. As presented in the table above, this hierarchy consists of three broad levels. Level 1 inputs on the hierarchy consist of unadjusted quoted prices in active markets for identical assets and liabilities and have the highest priority. Level 2 inputs consist of fair values of the investment in commodity futures contracts, which are estimated valuations provided by counterparties using the Black-Scholes model based upon the forward commodity price curves as of the end of the quarter, implied volatilities of commodities, and a risk free rate (using the treasury yield as of the end of the quarter). Level 3 inputs have the lowest priority. Lucas uses appropriate valuation techniques based on the available inputs to measure the fair values of its assets and liabilities. When available, Lucas measures fair value using Level 1 inputs because they generally provide the most reliable evidence of fair value.

The following methods and assumptions were used to estimate the fair values of the assets and liabilities in the table above.

LEVEL 1 FAIR VALUE MEASUREMENTS

Short-term Investments in Marketable Securities -- The fair values of these investments are based on quoted market prices. Lucas' short-term investments as of September 30, 2009 consisted entirely of trading securities which are subject to market fluctuations.

10

MARKETABLE SECURITIES

At March 31, 2009, Lucas held 3,666,700 shares of Bonanza common stock. During the six months ended September 30, 2009, Lucas sold 1,516,000 shares of Bonanza common stock with a realized loss of $28,785, net of commissions. During the first fiscal quarter ended June 30, 2009 and second fiscal quarter ended September 30, 2009, pursuant to mark-to-market accounting Lucas reported a non-cash unrealized gain on Bonanza common shares held totaling $220,444 and a non-cash unrealized loss on Bonanza common shares totaling $242,000, respectively. The net non-cash unrealized loss for the six months ended September 30, 2009 totaled $21,556. On September 30, 2009, Lucas held 2,150,700 shares of Bonanza common stock.

On May 2, 2008, Lucas purchased six commodity contracts that were linked to the NYMEX crude oil futures contracts. At the time the contracts were closed out in July 2008, Lucas had a realized loss on the NYMEX contracts totaling $125,420.

NOTE 5 - REVOLVING LINE OF CREDIT AND LETTER OF CREDIT FACILITY

On October 8, 2008, Lucas entered into a three-year Revolving Line of Credit and Letter of Credit Facility with Amegy

Bank (the Credit Facility ). The Credit Facility originally provided Lucas with up to a $100 million oil and gas reserve-based revolving line of credit with maturity on October 8, 2011 (the Revolving Line of Credit ). The availability of credit and repayments under the Credit Facility are subject to periodic borrowing base redeterminations. The Credit Facility provides for scheduled semiannual borrowing base redeterminations on June 1 and December 1, or at any other time that Amegy or Lucas may request an unscheduled redetermination; but neither is obligated to accommodate an unscheduled redetermination more than once between the scheduled semiannual redeterminations.

At closing of the Credit Facility in October 2008, Lucas had a lending commitment and borrowing capacity of $3.0 million. Subject to periodic borrowing base redeterminations and compliance with loan covenants, the Credit Facility provides for Lucas’ borrowing capacity and Amegy’s lending commitment under the Credit Facility to periodically increase or decrease as the collateral value of the proved reserves securing the Credit Facility fluctuates from factors such as change in market prices, revisions to reserve estimates and operating cost estimates, and as the results of drilling and development activities are acquired and interpreted. The Credit Facility is secured by first liens on Lucas’ existing and after acquired oil and gas properties.

The interest rate on borrowed funds under the Credit Facility is based on the greater of Amegy’s prime lending rate or

Federal Funds rate plus 0.50% per annum, but not less than 5.0% per annum. The Credit Facility contains a variable commitment fee component for unused borrowing capacity not to exceed a 0.05% annual rate. Borrowings outstanding on the Credit Facility upon the three year term expiration are due October 8, 2011. Since entering into the Credit

Facility with Amegy Bank, Lucas’ interest rate has been 5.0% per annum paid monthly. Lucas incurred front end transaction costs totaling $421,751 on the Amegy Credit Facility and the deferred financing costs are being amortized over the three year term of the Credit Facility using the effective interest rate method. For the six month period ended September 30, 2009, Lucas recorded as interest expense the amortization of the deferred financing costs totaling $57,667 and the unamortized balance of the transaction costs total $314,861 at September 30, 2009.

The Credit Facility contains covenants that Lucas is required to meet including: a) maintain a current ratio not less than 1.00 to 1.00 at any time; b) prohibit the ratio of Indebtedness to adjusted earnings before interest, taxes, depreciation and amortization ( EBITDA ) from being more than 3.75 to 1.00 (as defined in the credit agreement) for the preceding four quarterly periods; and c) limit general and administrative ( G&A ) expenses (determined in accordance with generally accepted accounting principles) during a fiscal quarter to no more than twenty-five percent (25.0%) of revenue less recurring lease operating expenses and taxes for the quarter.

At September 30, 2009, Lucas met the aforementioned current ratio test of 1.0 to 1.0; but, did not meet the EBITDA ratio covenant of 3.75 to 1.00, or the G&A covenant that provides that permitted G&A under the Credit Facility covenant must be no more than 25.0% of revenues less lease operating and taxes for a quarter. Lucas has advised Amegy Bank that it did not meet the EBITDA or the G&A covenants of the Credit Facility at September 30, 2009.

11

In connection with a scheduled periodic borrowing base redetermination, on March 30, 2009, Amegy notified Lucas that they reduced their lending commitment to Lucas under the Credit Facility to $2.7 million, with a further $25,000 per month reduction in their commitment until the next borrowing base redetermination. On September 11, 2009, Amegy advised Lucas that their lending commitment under the Credit Facility was further reduced to $2,465,500 retroactively to August 31, 2009, and that the reduction in their lending commitment to Lucas would increase to $62,500 per month commencing on September 30, 2009. Lucas continues to make principal payments of $25,000 per month, and have requested Amegy provide further data and explanation on the basis for and of the increasing level of reduction in their lending commitment to Lucas.

Since entering into the Credit Facility with an initial Amegy lending commitment to Lucas of $3,000,000 million in

October 2008, Amegy’s commitment has been reduced to $2,400,000 at September 30, 2009. The principal balance outstanding on the Credit Facility at September 30, 2009 was $2,500,000, and there was no borrowing capacity available to Lucas under the Credit Agreement.

During the six-month period ended September 30, 2009, Lucas has made principal payment reductions on the Credit Facility totaling $150,000; incurred approximately $64,823 of interest, bank and bank advisor’s fees totaling $38,937, and amortization of the original $421,751 of transaction costs on the Credit Facility totaling $57,667. The interest and associated direct costs of the Credit Facility to Lucas for the six-month period totaled approximately $161,400.

NOTE 6 – EQUITY

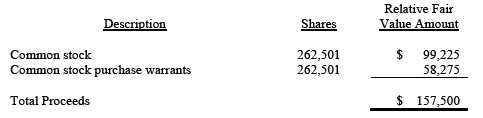

Common stock issued during the six months ended September 30, 2009:

Lucas issued through private equity placement 262,501 units at a purchase price of $0.60 per unit ( Unit ) for net proceeds of $157,500. Each Unit was comprised of one share of common stock and an attached three-year warrant for one share of common stock at $1.00 per share. The relative fair value of the common stock and attached warrant for one share of common stock were as follows:

The relative fair value of the common stock and warrants in the above table were derived through the Black Scholes option pricing model, and variables used in the model were: (i) 0.44% risk-free interest rate, (ii) expected life of one year, (iii) volatility of 120.32%, and (iv) zero expected dividends.

During the quarter ended September 30, 2009, the Company issued 53,234 shares of common stock to consultants and contractors to the Company. The shares were issued at fair value which totaled $41,300, or $0.78 per common share.

On July 20, 2009, the Company issued 25,000 shares of common stock to its corporate secretary and former chief financial officer as part of his compensation package. The shares were issued at fair value totaling $25,000.

On August 26, 2009, the Company issued 10,000 shares of common stock to its current chief financial officer which was part of his compensation package with the Company. The shares were issued at fair value on the volumetric weighted average share price for the period that services were provided to the Company which totaled $7,838, or $0.78 per share.

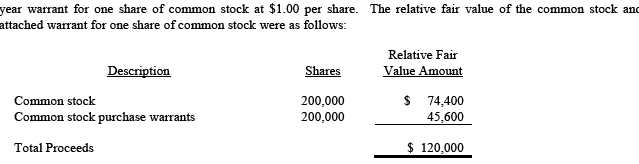

Common stock issued after September 30, 2009:

During October 2009, Lucas issued through private equity placement 200,000 units at a purchase price of $0.60 per unit ( Unit ) for net proceeds of $120,000. Each Unit was comprised of one share of common stock and an attached three-

12

The relative fair value of the common stock and warrants in the above table were derived through the Black Scholes option pricing model, and variables used in the model were: (i) 0.37% risk-free interest rate, (ii) expected life of one year, (iii) volatility of 121.89%, and (iv) zero expected dividends.

On October 20, 2009, the Company issued 4,000 shares of restricted common stock to its current chief financial officer which was part of his compensation package with the Company. The shares were issued at fair value on the grant date being the closing share price on the last day of the calendar month during which services were provided to Lucas or $3,500. On October 20, 2009, the Company issued 13,139 shares of common stock to contractors to the Company for services. The shares were issued at the grant date fair value which totaled $10,237, or $0.78 per common share.

On October 20, 2009, the Company issued 85,443 shares of common stock to renew an existing oil and gas lease. The shares were issued at the grant date fair value which totaled $69,649, or $0.82 per common share.

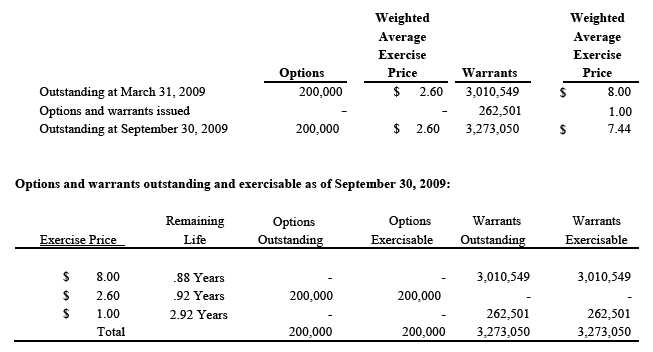

NOTE 7 – OPTIONS AND WARRANTS

Summary information regarding options and warrants are as follows:

All options are vested, and all options and warrants are exercisable. All options and warrants had no intrinsic value at September 30, 2009.

13

ITEM 2. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS.

The following discussion and analysis should be read in conjunction with the unaudited financial statements and notes thereto included elsewhere in this report, and should be read in conjunction with management’s discussion and analysis contained in Lucas’ Annual Report on Form 10-K for the fiscal year ended March 31, 2009 and related discussion of our business and properties contained therein. The terms “Company”, “Lucas Energy”,” “Lucas”, “we”, “us”, and “our” refer to Lucas Energy, Inc.

OVERVIEW

Cautionary Statement Regarding Forward-Looking Statements

This Quarterly Report includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements may relate to such matters as anticipated financial performance, future revenues or earnings, business prospects, projected ventures, new products and services, anticipated market performance and similar matters. We identify forward-looking statements by use of terms such as may, will, expect, anticipate, estimate, hope, plan, believe, predict, envision, intend, will, continue, potential, should, confident, could and similar words and expressions, although some forward-looking statements may be expressed differently. You should be aware that our actual results could differ materially from those contained in the forward-looking statements.

These risks and uncertainties, many of which are beyond our control, include:

| * | the sufficiency of existing capital resources and our ability to raise additional capital to fund cash requirements for future operations; |

| * | uncertainties involved in the rate of growth of our business and acceptance of any products or services; |

| * | volatility of the stock market, particularly within the energy sector; and |

| * | general economic conditions. |

Although we believe the expectations reflected in these forward-looking statements are reasonable, such expectations cannot guarantee future results, levels of activity, performance or achievements.

All forward-looking statements included in this report and all subsequent written or oral forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by these cautionary statements. The forward-looking statements speak only as of the date made, other than as required by law, and we undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

NATURE OF OPERATIONS

Lucas is an independent oil and gas company based in Houston, Texas with approximately 15,000 gross and 12,000 net acres of oil and gas leases in South Texas primarily in the Gonzales County, Texas area. Our strategy is to acquire underperforming oil and gas properties in which we believe we can restore, revitalize or increase production. We currently operate 32 producing wells that produce in the aggregate approximately 80 – 135 barrels of oil per day ( BOPD ), gross. We control another 16 shut-in or plugged wellbores. As of September 30, 2009 we owned 100% working interests in all but seven of our operated wells. Our average daily production, net to our interest, from our oil and gas properties totaled approximately 72 and 83 barrels of oil equivalent ( boe ) per day for the three and six months ended September 30, 2009, respectively.

On July 28, 2009 we kicked-off our LEI 2009-II capital program which is being conducted through a capital program with two working interest partners. One working interest party is a U.S. limited partnership of a foreign entity that bought into and acquired an eighty percent (80%) working interest (before payout) in six existing wellbores that are currently shut-in or plugged and abandoned. The working interest partner has funded its 80% share of the capital costs totaling $1,710,000 to fund their share of the drilling and completion capital expenditures required to re-enter the six

14

wells and restore production. The other partner has a 10% working interest that is carried by Lucas through the tanks. We retained a 10% working interest in the wells prior to payout, and have an additional 10% back in , or a 20% working interest, after the 80% working interest partner achieves payout on their capital investment. We operate the six wells that comprise the LEI 2009-II capital program. Drilling and completion of four of the wells has been finished, and the wells are in various stages of being brought online. Two wells have commenced commercial production, and two wells are in the dewatering process and expected to achieve commercial levels of oil production in the near term. Work continues on the remaining two wells that form the capital program.

Crude oil represents approximately 93% of our total production, while approximately 98% of our revenues are derived from the sale of crude oil production. Oil sales are made on a month-to-month basis and our monthly cash flows are positively or negatively affected with upward and downward movements in crude oil price postings. Actual prices realized from our sales of crude oil for the three months ended September 30, 2009 ranged from a low of $61.35 per barrel in July 2009 to a high of $67.55 per barrel in August 2009.

Acquisitions of shut-in wells, plugged and abandoned wells or wells with marginal production are core to our growth strategy; in that we target wells that our assessment indicate have a high probability of additional recovery of reserves through our revitalization process or through the drilling of new horizontal laterals. We actively seek out opportunities to acquire wells located in mature oil fields that we believe are underdeveloped or have potential to recover significant oil reserves that are still in place. Most of the acquisition prospects that we conduct initial screening on are sourced directly by our senior management or specialized third-party consultants with local area knowledge.

RESULTS OF OPERATIONS

For the Three Months Ended September 30, 2009 Compared to the Three Months Ended September 30, 2009

15

Oil and Gas Revenue

The $583,800 decrease in our oil and gas revenues during the three months ended September 30, 2009 was primarily attributable to a decline of $54.62 per barrel (46%) in the price realized for oil sales and a 1,849 barrel (22%) decrease in oil production sold along with a decline of $5.01 per mcf (67%) in the price realized for natural gas sales and a 1,145 decrease in natural gas production sold compared to the three months ended September 30, 2008. The decrease in oil volumes is due to having several wells down for workovers during the period.

Lease Operating Expenses

Lease operating expenses decreased $280,531 during the three months ended September 30, 2009 as compared to the prior year period principally due to lower workover and treatment costs for the current period.

General and Administrative Expenses

General and administrative expenses decreased $53,417 for the three months ended September 30, 2009 as compared to the prior period primarily due to a decrease in the use of contractors and reduction in professional fees.

Depreciation, Depletion, Amortization and Accretion (“DD&A”)

DD&A decreased $19,603 primarily due to a decrease in production for the current three month period ended September 30, 2009 totaling 2,040 barrels of oil equivalent compared to the prior year period.

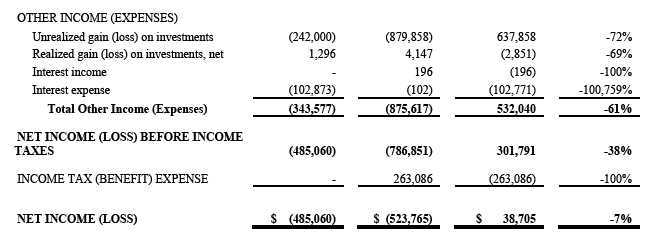

Unrealized and Realized Gains and Losses

The unrealized loss on investments for the three months ended September 30, 2009 totaling $242,000 is due to mark- to-market accounting for shares held by Lucas in Bonanza Oil and Gas, Inc. At June 30, 2009 Bonanza stock closed with a quoted price on the OTC of $0.15 per share compared to September 30, 2009 close price of $0.07 per share. Pursuant to mark-to-market accounting an unrealized loss on the shares held resulted in a write down. During the current three-month period, Lucas sold 1,000,000 shares of Bonanza common stock that it held for $81,296 net of commissions with a realized gain on the sale of $1,296.

Interest Expense

Interest expense increased by $102,771 due to interest, commitment fees and other fees associated with the Amegy Credit Facility executed in October 2008.

16

Interest Income

Interest income decreased $196 for the three months ended compared to the prior year period due to a decrease in the average cash on hand.

Income Tax Expense

Income tax expense was zero for the current period compared to a tax benefit of $263,086 for the same prior in the prior year. The prior year tax benefit was the result of expected future reductions to income tax liability for the net loss for the prior year period and the associated reduction in deferred income taxes. Current year tax benefits have been fully reserved in our valuation allowance.

Net Income (Loss)

The $38,705 decrease in net loss during the current period is primarily attributable to the $637,858 reduction in the unrealized loss on Bonanza shares of common stock being offset by the $583,800 reduction in revenues from oil and gas sales between the current three month period and the prior year three month period.

For the Six Months Ended September 30, 2009 Compared to the Six Months Ended September 30, 2009

17

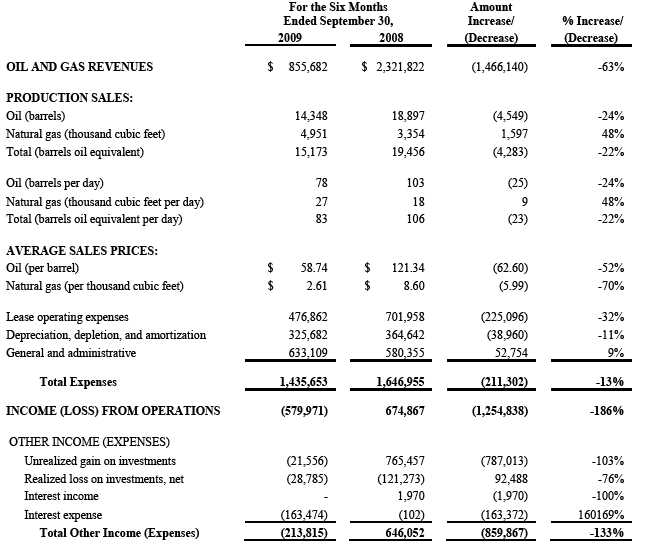

Oil and Gas Revenue

The $1,466,140 decrease in our oil and gas revenues during the six months ended September 30, 2009 was primarily attributable to a decline of $62.60 per barrel (52%) in the price realized for oil sales and a 4,549 barrel (24%) decrease in oil production sold along with a decline of $5.99 per mcf (70%) in the price realized for natural gas sales offset by a 1,597 increase in natural gas production sold compared to the six months ended September 30, 2008. The decrease in oil volumes is due to having several wells down for work-over during the period.

Lease Operating Expenses

Lease operating expenses decreased $225,096 during the six months ended September 30, 2009 as compared to the prior year period principally due to lower work-over and treatment costs for the current period.

General and Administrative Expenses

General and administrative expenses increased $52,754 for the six months ended September 30, 2009 as compared to the prior period. The increase resulted from an increase in non-cash stock based compensation for employees and contractors, costs associated with building investor awareness of Lucas in connection with financing initiatives partially offset with a reduction in professional fees for outside service providers.

Depreciation, Depletion, Amortization and Accretion (“DD&A”)

DD&A decreased $38,960 primarily due to a decrease in production for the current six month period ended September 30, 2009 totaling 4,283 barrels of oil equivalent compared to the prior year six month period.

Unrealized and Realized Losses

The unrealized loss on investments for the six months ended September 30, 2009 of $21,556 is due to the mark-to-market accounting for shares held by Lucas in Bonanza Oil and Gas, Inc. The unrealized loss compares to a net unrealized gain totaling $765,457 for the same period ended September 30, 2008 on shares of common stock held in Bonanza that were the result of mark-to-market accounting for Bonanza shares held by Lucas. Lucas sold 1,516,000 shares of Bonanza common stock during the current six month period with a realized loss of $28,785. No sales were made during the same prior year period.

Interest Expense

Interest expense increased by $163,372 due to interest, commitment fees and other fees associated with the Amegy Credit Facility executed in October 2008.

Interest Income

Interest income decreased $1,970 for the six months ended compared to the prior year period due to a decrease in the average cash on hand as cash raised in the sale of common stock in the fiscal year 2008 was expended.

18

Income Tax Expense

Income tax expense was zero for the current period due to the net loss before income taxes. For the prior year income tax expense totaled $454,554 for expected future tax obligations associated with the net income during the prior year period. Current year tax benefits have been fully reserved in our valuation allowance.

Net Income (Loss)

The $1,660,151 decrease in net income is primarily attributable to the $787,013 increase in the unrealized gain on Bonanza shares of common stock between the current six month period and the prior year six month period, and the $1,466,140 reduction in revenues from oil and gas sales partially offset with the $454,554 reduction in deferred income taxes due to the net loss for the current three month period.

Liquidity and Capital Resources

From the end of our prior fiscal year of March 31, 2009 to September 30, 2009, our cash increased by $1,058,063 with cash at September 30, 2009 totaling $1,194,904. With the inclusion of the total outstanding principal balance on the Amegy Credit Facility totaling $2,500,000 classified as current, we had negative working capital at September 30, 2009 of $2,500,292. At March 31, 2009 our negative working capital totaled $513,240, which included $300,000 of the then total outstanding balance under the Credit Facility with Amegy of $2,650,000.

During the six-month period ended September 30, 2009, we raised approximately $1.2 million in financing proceeds through working interest buy-in participation in our six well LEI 2009-II capital program; private equity placements; and our sale of interests in four non producing or marginally producing wellbores that did not meet our technical screening requirements for inclusion in our future drilling and development programs.

We anticipate that cash flows from operating activities coupled with cash on hand will be sufficient to cover our operating and general and administrative requirements for the remainder of our 2010 fiscal year. We expect to fund our capital expenditure requirements including finishing out the six wells of the LEI 2009-II capital program and ramping up the LEI 2009-III capital program through a combination of joint venture arrangements, working interest participants buy-in to existing wells and programs, and other sources of capital such as private equity and debt placements, shelf registrations now available to non-accelerated filers such as Lucas, public offerings, and traditional reserve based financing and credit facilities.

We currently have no definitive agreements or arrangements for additional funding, and financings could result in significant dilution to our shareholders or not be available on acceptable terms in the time frame necessary, or may not be available or acceptable to us at all.

Cash flow from operating activities

For the six months ended September 30, 2009, net cash provided by operating activities was $564,390 compared to net cash provided from operating activities of $1,604,535 for the six months ended September 30, 2008. The $1,040,145 decrease in net cash provided from operating activities is primarily due to the reduction in net income for the current period deriving from reduced revenues associated with lower volumes and substantially lower prices.

Cash flow from investing activities

For the six months ended September 30, 2009 net cash provided by investing activities was $537,089 compared to net cash used in investing activities for the prior year period of $2,194,043. Cash provided by investing activities was principally derived from the sale of working interests in a farmout agreement. Cash used in investment activities declined to due to a scaling back and reduction in capital expenditures associated with our oil and gas properties as the price for crude oil declined.

19

Cash flow from financing activities

For the six months ended September 30, 2009, net cash flow used in financing activities was $43,416 resulting from a reduction in the outstanding principal balance on the Amegy Credit Facility and deferred financing costs offset by proceeds from a private equity placement. For the six months ended September 30, 2008, net cash flow used in financing activities was $21,087 resulting from a retirement of common stock by the Company.

Hedging

We did not hedge any of our oil or natural gas production during fiscal 2009 and have not entered into any such hedges through the date of this filing.

Contractual Commitments

None

Off-Balance Sheet Arrangements

None.

Related Party Transactions

None.

Critical Accounting Policies

Our discussion and analysis of our financial condition and results of operations is based on our consolidated financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States of America. The preparation of these financial statements requires us to make estimates and judgments that affect the reported amounts of assets, liabilities and expenses. We base our estimates on historical experience and on various other assumptions that we believe to be reasonable under the circumstances, the results of which form the basis for making judgments about the carrying values of assets and liabilities that are not readily apparent from other sources. Actual results may differ from these estimates under different assumptions or conditions.

In February 2007, the Financial Accounting Standards Board ( FASB ) issued SFAS No. 159 ( SFAS 159 , ASC 825 Financial Instruments), The Fair Value Option for Financial Assets and Financial Liabilities—Including an Amendment of FASB Statement No. 115. This pronouncement permits entities to use the fair value method to measure certain financial assets and liabilities by electing an irrevocable option to use the fair value method at specified election dates. After election of the option, subsequent changes in fair value would result in the recognition of unrealized gains or losses as period costs during the period the change occurred. SFAS 159 becomes effective as of the beginning of the first fiscal year that begins after November 15, 2007, with early adoption permitted. However, entities may not retroactively apply the provisions of SFAS 159 to fiscal years preceding the date of adoption. We are currently evaluating the impact that SFAS 159 may have on our financial position, results of operations or cash flows.

In December 2008, the SEC released Final Rule, Modernization of Oil and Gas Reporting . The new disclosure requirements include provisions that permit the use of new technologies to determine proved reserves if those technologies have been demonstrated empirically to lead to reliable conclusions about reserve volumes. The new requirements also will allow companies to disclose their probable and possible reserves to investors. In addition, the new disclosure requirements require that companies 1) report the independence and qualifications of its reserves preparer or auditor, 2) file reports when a third party is relied upon to prepare reserves estimates or conduct a reserves audit, 3) report oil and gas reserves using an average price based upon the prior 12-month period rather than year-end prices. The new disclosure requirements are effective for financial statements for fiscal years ending on or after December 31, 2009. Early adoption is not permitted. We are currently assessing the impact, if any, that the adoption of the pronouncement will have on our operating results, financial position or cash flows.

20

In June 2009, the FASB issued Statement No. 168, The FASB Accounting Standards Codification and the Hierarchy of Generally Accepted Accounting Principles ( SFAS 168 , ASC 105-10 Generally Accepted Accounting Principles), which amends SFAS No. 162, The Hierarchy of Generally Accepted Accounting Principles . SFAS 168 will become the source of authoritative U.S. GAAP recognized by the FASB to be applied by nongovernmental entities. Rules and interpretive releases of the SEC under the authority of federal securities laws are also sources of authoritative GAAP for SEC registrants. On the effective date, SFAS 168 will supersede all then existing non-SEC accounting and reporting standards. All other non-grandfathered non-SEC accounting literature not included in SFAS 168 will become non-authoritative. SFAS 168 is effective for financial statements issued for interim and annual periods ending after September 15, 2009. The adoption of SFAS 168 did not impact our results of operations or financial condition.

ITEM 3. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK.

Market risk is the risk of loss arising from adverse changes in market rates and prices. We are exposed to risks related to increases in the prices of fuel and raw materials consumed in exploration, development and production. We do not engage in commodity price hedging activities.

ITEM 4. CONTROLS AND PROCEDURES.

Disclosure Controls and Procedures.

Disclosure controls and procedures (as defined in Rules 13a-15(e) and 15d-15(e) under the Securities

Exchange Act of 1934 (the Exchange Act )) are designed to ensure that information required to be disclosed in reports filed or submitted under the Exchange Act is recorded, processed, summarized and reported within the time periods specified in Securities and Exchange Commission rules and forms and that such information is accumulated and communicated to management, including the Chief Executive Officer and Chief Financial Officer, to allow timely decisions regarding required disclosures.

Management’s Report on Internal Control over Financial Reporting

Management of the Company is responsible for establishing and maintaining adequate internal control over financial reporting, as such term is defined in Rules 13a-15(f) and 15d-15(f) under the Exchange Act. Internal control over financial reporting is a process designed under the supervision of our principal executive and principal financial officers to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with GAAP.

Due to inherent limitations, internal control over financial reporting may not prevent or detect misstatements and, even when determined to be effective, can only provide reasonable, not absolute, assurance with respect to financial statement preparation and presentation. Projections of any evaluation of effectiveness to future periods are subject to risk that controls may become inadequate as a result of changes in conditions or deterioration in the degree of compliance.

Under the supervision and with the participation of our management, including our chief executive officer and chief financial officer, we evaluated the effectiveness of the design and operation of our disclosure controls and procedures as of the end of the period covered by this report. Based on the evaluation, our management concluded that the design and operation of such disclosure controls and procedures were effective.

Changes in Internal Control Over Financial Reporting

There have not been any changes in our internal control over financial reporting that have materially affected, or are reasonably likely to materially affect, our internal control over financial reporting.

21

PART II - OTHER INFORMATION

ITEM 1. LEGAL PROCEEDINGS.

The Company is not aware of any significant litigation, pending or threatened, that would have a material adverse effect on our financial position or results of operations.

ITEM 1A. RISK FACTORS.

There have been no material changes to the risk factors set forth in our Annual Report on Form 10-K for the year ended March 31, 2009, as filed with the SEC on June 29, 2009. The risk factors disclosed in our Annual Report on Form 10-K for the fiscal year ended March 31, 2009, in addition to the other information set forth in this quarterly report, could materially affect our business, financial condition or results of operations. Additional risks and uncertainties not currently known to us or that we deem to be immaterial could also materially adversely affect our business, financial condition or results of operations.

ITEM 2. UNREGISTERED SALES OF EQUITY SECURITIES AND USE OF PROCEEDS.

On October 20, 2009, the Company has issued through private placement 100,000 units at a purchase price of $0.60 per unit (the Units ). Each Unit was comprised of one share of common stock and an attached three-year warrant for one share of common stock at $1.00 per share. The shares and warrants were sold to accredited investors pursuant to the exemption from the registration requirements of the Securities Act provided by Section 4(2) and Regulation D under the Securities Act.

On October 20, 2009, the Company issued 4,000 shares of restricted common stock to its chief financial officer which was part of his compensation package with the Company. The shares were issued at fair value on the grant date which was $3,500, or $0.88 per share. The shares were issued to accredited investors pursuant to the exemption from the registration requirements of the Securities Act provided by Section 4(2) and Regulation D under the Securities Act.

On October 20, 2009, the Company issued 13,139 shares of common stock to contractors to the Company. The shares were issued at fair value on the grant date which totaled $10,237, or $0.78 per common share. The shares were issued to accredited investors pursuant to the exemption from the registration requirements of the Securities Act provided by Section 4(2) and Regulation D under the Securities Act.

On October 20, 2009, the Company issued 85,443 shares of common stock to renew an existing oil and gas lease. The shares were issued at fair valueon the grant date which totaled $69,649, or $0.82 per common share. The shares were issued to accredited investors pursuant to the exemption from the registration requirements of the Securities Act provided by Section 4(2) and Regulation D under the Securities Act.

ITEM 3. DEFAULTS UPON SENIOR SECURITIES.

None.

ITEMS 4. SUBMISSION OF MATTERS TO A VOLTE OF SECURITY HOLDERS.

None.

ITEM 5. OTHER INFORMATION.

None.

22

23

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the Registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| Signature | Title | Date |

| /s/ William A. Sawyer | President and C.E.O. | November 16, 2009 |

| William A. Sawyer | (Principal Executive Officer) | |

| /s/ Donald L. Sytsma | Chief Financial Officer and | November 16, 2009 |

| Donald L. Sytsma | Accounting Officer | |

24

25