Attached files

| file | filename |

|---|---|

| 8-K - HELIX ENERGY SOLUTIONS GROUP INC FORM 8-K DATED 11/2/09 - HELIX ENERGY SOLUTIONS GROUP INC | form8k.htm |

Company

Update

November

2009

2

The

United States Securities and Exchange Commission permits oil and gas companies,

in their filings with the SEC,

to disclose only proved reserves that a company has demonstrated by actual production or conclusive formation

tests to be economically and legally producible under existing economic and operating conditions. Statements of

proved reserves are only estimates and may be imprecise. Any reserve estimates provided in this presentation that

are not specifically designated as being estimates of proved reserves may include not only proved reserves but also

other categories of reserves that the SEC’s guidelines strictly prohibit the Company from including in filings with the

SEC. Investors are urged to consider closely the disclosure in the Company’s 2008 Form 10-K.

to disclose only proved reserves that a company has demonstrated by actual production or conclusive formation

tests to be economically and legally producible under existing economic and operating conditions. Statements of

proved reserves are only estimates and may be imprecise. Any reserve estimates provided in this presentation that

are not specifically designated as being estimates of proved reserves may include not only proved reserves but also

other categories of reserves that the SEC’s guidelines strictly prohibit the Company from including in filings with the

SEC. Investors are urged to consider closely the disclosure in the Company’s 2008 Form 10-K.

Forward-Looking

Statements

3

Helix

Energy Solutions Group provides life-of-field services and development solutions

to

offshore energy producers worldwide. Helix actively reduces finding and development costs

through a unique mix of offshore production assets, service methodologies, and highly skilled

personnel.

offshore energy producers worldwide. Helix actively reduces finding and development costs

through a unique mix of offshore production assets, service methodologies, and highly skilled

personnel.

Owen

Kratz

Chairman

and Chief Executive Officer

Anthony

Tripodo

Executive

Vice President and Chief Financial Officer

Presenters

4

Historical

Profile

• Deepwater subsea

contracting

• Deepwater well

intervention

•

Robotics

• Oil and

gas

•

Deepwater

•

Shelf

•

Offshore production facilities

•

Shelf contracting (Cal Dive)

•

Reservoir evaluation and consulting

The

Future

• Deepwater

contracting services

• Well

Intervention

•

Robotics

• Subsea

Construction

• Deepwater oil and

gas

• Minimize

exploration capex

and risk

and risk

•

Offshore production facilities

The

result: A

company focused on deepwater

activities and a conservative balance sheet

activities and a conservative balance sheet

Helix:

Transforming the Business Model

Production

Facilities

Pipelay

Intrepid

Express

Intrepid

Express

Caesar

(2009)

ROV

39 ROVs

2 ROV Drill Units

5 Chartered Vessels

39 ROVs

2 ROV Drill Units

5 Chartered Vessels

6 Trenchers

(200 - 2000hp)

Deepwater

Well Intervention

Well Intervention

Q4000

Seawell

Well Enhancer

(2009)

Mobile

SILs

PV-10 $1.9

billion @

12/31/2008

12/31/2008

Proved

reserves = 665 bcfe

(12/31/2008)

(12/31/2008)

2009

projected production

43 - 47 bcfe

43 - 47 bcfe

Helix

Business Segments

The

Helix Fleet

Well

Enhancer and Seawell in Aberdeen, Scotland

7

MODU

DP3 Q4000

MSV

DP2 Well

Enhancer

Helix

provides well operation and decommissioning services with the

Seawell riserless well intervention vessel, the flagship Q4000

semisubmersible, the Well Enhancer wireline / slickline / coiled tubing

intervention vessel, and the Subsea Intervention Lubricator system.

Seawell riserless well intervention vessel, the flagship Q4000

semisubmersible, the Well Enhancer wireline / slickline / coiled tubing

intervention vessel, and the Subsea Intervention Lubricator system.

Well

Intervention Assets

MSV

DP2 Seawell

DP

Reel Lay Vessel

Express

Express

DP

S-Lay Vessel

Caesar (Q4 2009)

Caesar (Q4 2009)

Caesar’s onboard

pipe welding and testing

capability allows the vessel to lay virtually

unlimited lengths of pipe up to 36” in diameter.

capability allows the vessel to lay virtually

unlimited lengths of pipe up to 36” in diameter.

Helix’s

flagship pipelay and subsea construction

vessel has established an extensive track record

of field installation projects around the world.

vessel has established an extensive track record

of field installation projects around the world.

Intrepid has the

flexibility to be deployed as a

pipelay, installation or saturation diving vessel.

pipelay, installation or saturation diving vessel.

Subsea

Construction Vessels

Helix

is an industry leading provider of ROV and subsea trenching

services to deepwater operators worldwide.

services to deepwater operators worldwide.

The

Helix ROV fleet

consists of 39 vehicles,

covering the spectrum of

deepwater construction

services.

consists of 39 vehicles,

covering the spectrum of

deepwater construction

services.

The 600

hp Supertrencher II

system is designed to

operate at water depths in

excess of 6,500 feet.

system is designed to

operate at water depths in

excess of 6,500 feet.

The

state of the art I-Trencher

system trenches, lays pipe up

to 16” in diameter, and backfills

in a single operation.

system trenches, lays pipe up

to 16” in diameter, and backfills

in a single operation.

Helix

ROV Systems

Island

Pioneer

Olympic

Triton

Olympic

Canyon

Seacor

Canyon

Northern

Canyon

Chartered

support vessels allows Helix to adjust the size and

capability of its fleet to cost-effectively meet industry demands.

capability of its fleet to cost-effectively meet industry demands.

ROV

/ Construction Support Vessel Fleet

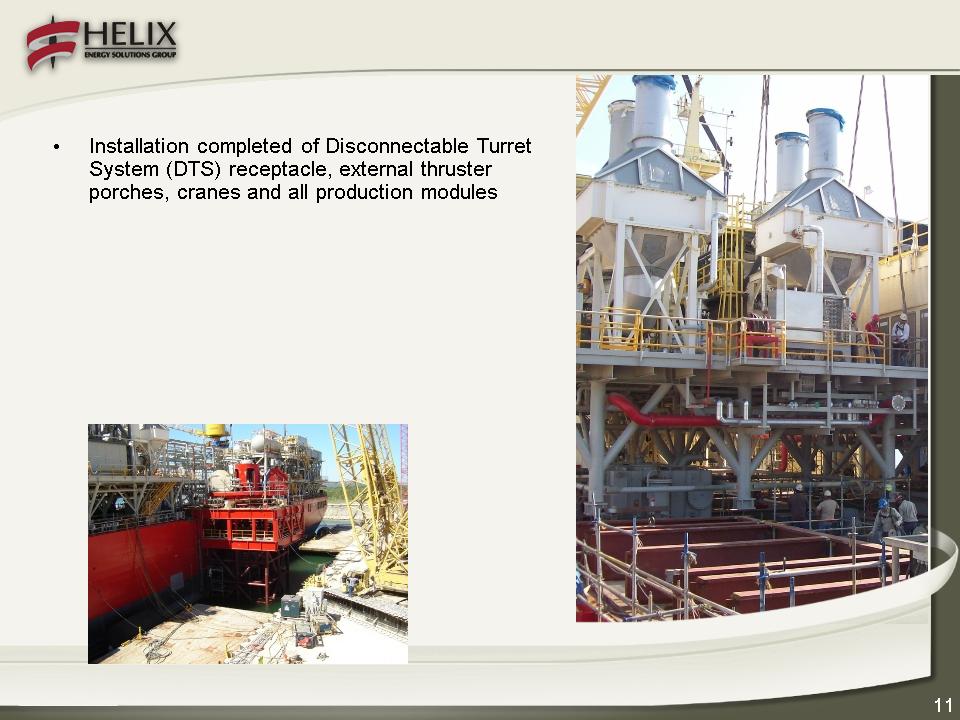

• DTS buoy loaded out

and to be installed by

Q4000 in November 2009

Q4000 in November 2009

• Installation of

2,500-ton production modules

underway and expected to be completed

November with hook-up to follow

underway and expected to be completed

November with hook-up to follow

• Expect deployment in

Phoenix field

in Q2 2010

in Q2 2010

HPI

production module installation

Disconnectable

Transfer System

Transfer System

Helix

Producer I

– Pipe stalk length

5,230 feet

– 300’ x 700’slip can

accommodate two

Helix Subsea Construction vessels side

by side

Helix Subsea Construction vessels side

by side

• Welding of Helix

Danny 36-mile

8 x 12-inch pipe-in-pipe began early August

8 x 12-inch pipe-in-pipe began early August

Aerial

view of Ingleside Shore Base

Helix

Danny pipe welding

Automated

pipe tension system

Contracting

Services

14

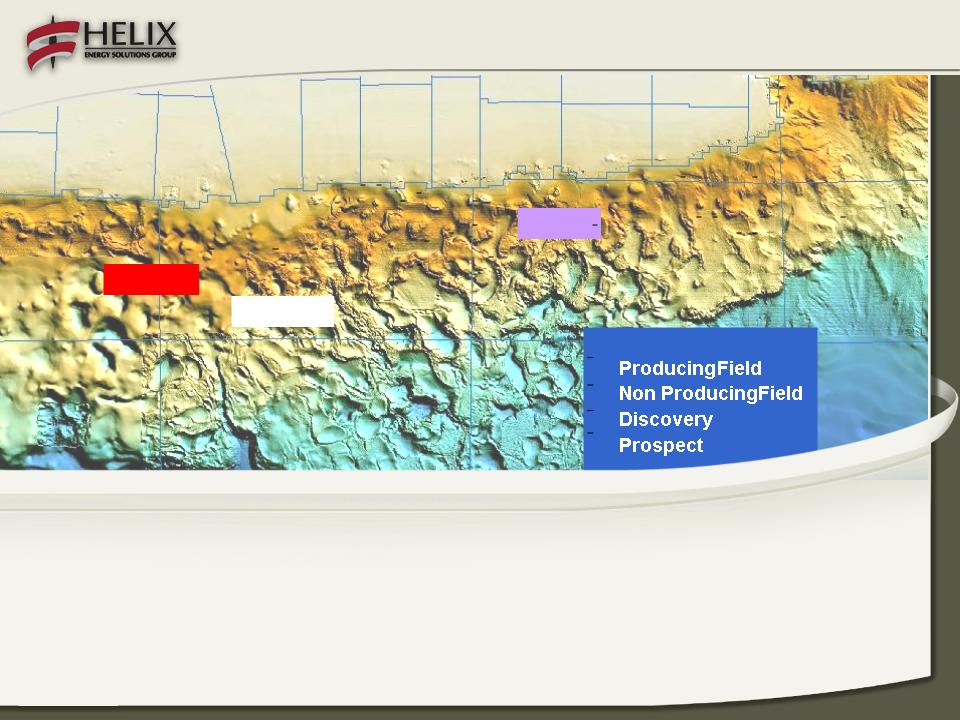

Legend:

Gunnison

Bushwood

Phoenix

Interests in 47

Deepwater Blocks -13 Developed, 34 Undeveloped

379

BCFE Proved Reserves- 32 MMCFE Net Daily Production

2.7 Net

TCFE Un-Risked Reserve Potential, 1.0 TCFE Risked

Internal Prospect

Generation via Large, In-House 3-D Seismic Library Large,

Recent Long Offset 3-D Seismic Database,+1,500 Blocks

Recent Long Offset 3-D Seismic Database,+1,500 Blocks

Experienced

Exploration/Drilling/Operations Team - 25+ years avg.

ERT

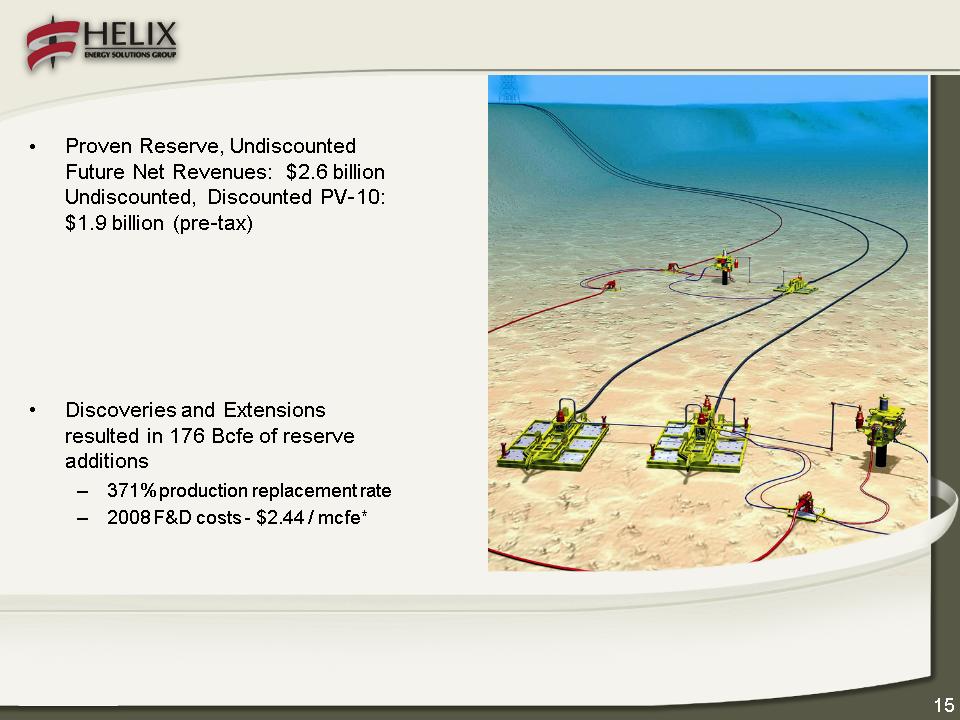

Deepwater Portfolio

• 665 Bcfe Proved

Reserves

– 379 Bcfe

deepwater,

273 Bcfe shelf, 13 North Sea

273 Bcfe shelf, 13 North Sea

– Proved Developed /

PUD Ratio -

50/50

50/50

– Natural Gas / Oil

Mix - 70/30

*2008 Exploration +

Development + Proved Property Acquisition / Exploratory Additions (U.S.

Only)

O&G

- 2008 Reserve Report Highlights

Helix

Producer I topside module installation progress at Kiewit Offshore Services

fabrication yard

• Express dry-dock,

transit and utilization on

Danny pipeline is affecting second half, 2009

revenues

Danny pipeline is affecting second half, 2009

revenues

• Capital expenditures

of approximately $385

million

million

• $200 million

relates to completion of three

major vessel projects (Well Enhancer, Caesar

and Helix Producer I)

major vessel projects (Well Enhancer, Caesar

and Helix Producer I)

• $60 million relates

to development of Danny

and Phoenix oil fields

and Phoenix oil fields

• Most of remaining

CAPEX is regulatory

maintenance

maintenance

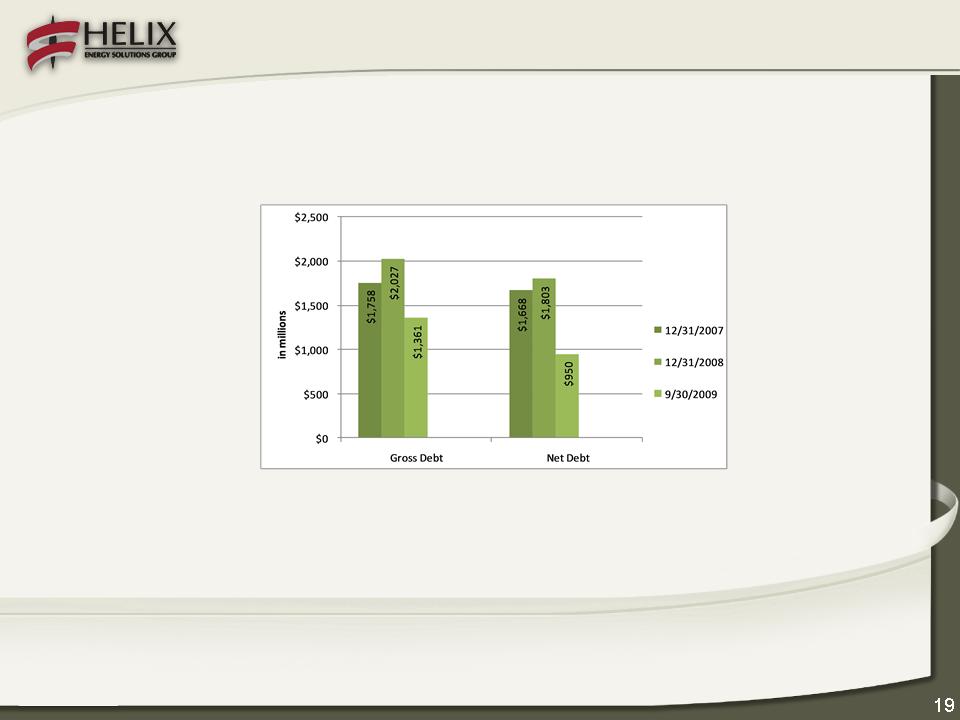

• Improved liquidity

and debt levels (see slide 20)

Express

spooling pipe for ERT Danny project

2009

Outlook

• Production range:

43 - 47 Bcfe

• Oil and gas

prices

• Without hedges:

$4.34 /mcfe;

$64.69 /bbl

$64.69 /bbl

• With realized

hedges and mark-to-

market adjustments (gas only):

$7.52 /mcfe; $70.36 /bbl

market adjustments (gas only):

$7.52 /mcfe; $70.36 /bbl

HPI

pipe racks connecting production modules

to buoy system

to buoy system

2009

Outlook (continued)

Debt

Liquidity*

of $781 million at 9/30/09

* Defined as available revolver capacity plus cash

Significant

Balance Sheet Improvements

• Completed (≈ $600

million pre-tax):

•Oil and gas

assets

• Bass Lite sale

December 08 & January 09 ($49 million)

• EC 316 sale in

February 09 ($18 million)

• Cal

Dive

• Sold a total of

15.2 million shares of Cal Dive common stock to Cal Dive

in January and June 2009 for aggregate proceeds of $100 million

in January and June 2009 for aggregate proceeds of $100 million

• Sold 45.8 million

Cal Dive shares in secondary offerings for proceeds of

≈ $405 million (net of offering costs) in June and September 2009

≈ $405 million (net of offering costs) in June and September 2009

• Sold

Helix RDS for $25 million in April 2009

Company

will continue to seek a sale of its shelf oil and gas properties

Liquidity

and Capital Resources

Company

is in compliance as of 6/30/2009, and based on current forecasts expects

compliance throughout 2009.

compliance throughout 2009.

|

Covenant

|

Test

|

Explanation

|

|

Collateral

Coverage Ratio

|

> 1.75 :

1

|

Basket of

collateral to Senior Secured Debt

|

|

Fixed Charge

Coverage Ratio

|

> 2.75 :

1

|

Consolidated

EBITDA to

consolidated

interest charges |

|

Consolidated

Leverage Ratio

|

< 3.5 :

1

|

Consolidated

EBITDA to

consolidated debt

|

Liquidity

and Capital Resources

Credit

Facilities, Commitments and Amortization

– $435

Million Revolving Credit Facility -

UNDRAWN.

• Facility extended to

November 2012.

• In July 2011,

commitments reduced to $407 million.

• $50 million of LCs

in place.

– $417

Million Term Loan B - Committed

facility through June 2013. $4.3

million

principal payments annually.

principal payments annually.

– $550

Million High Yield Notes - Interest only

until maturity (January 2016) or called

by Helix. First Helix call date is January 2012.

by Helix. First Helix call date is January 2012.

– $300

Million Convertible Notes - Interest only

until put by noteholders or called by

Helix. First put/call date is December 2012, although noteholders have the right to

convert prior to that date if certain stock price triggers are met ($38.56).

Helix. First put/call date is December 2012, although noteholders have the right to

convert prior to that date if certain stock price triggers are met ($38.56).

– $121

Million MARAD - Original 25 year

term; matures February 2027. $4.4

million

principal payments annually.

principal payments annually.

Liquidity

and Capital Resources

Note:

Excludes Cal Dive and Helix RDS revenues from 2005-2008.

See Non-GAAP reconciliations on slide 30.

See Non-GAAP reconciliations on slide 30.

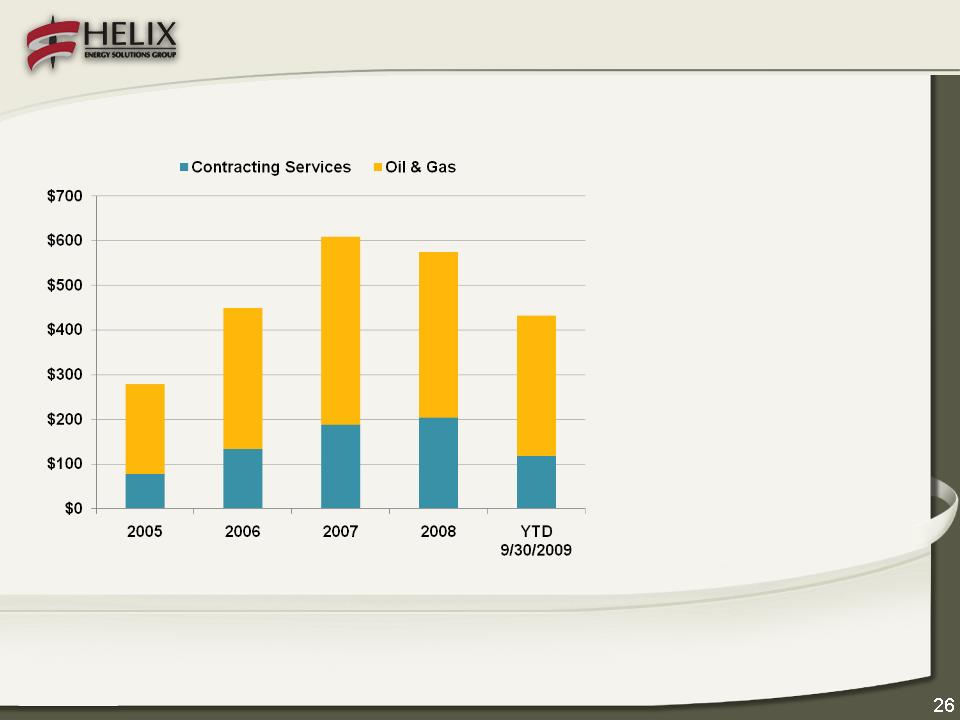

Consistent

Top Line Growth

($

amounts in millions)

$575

$840

$891

$1,337

$1,152

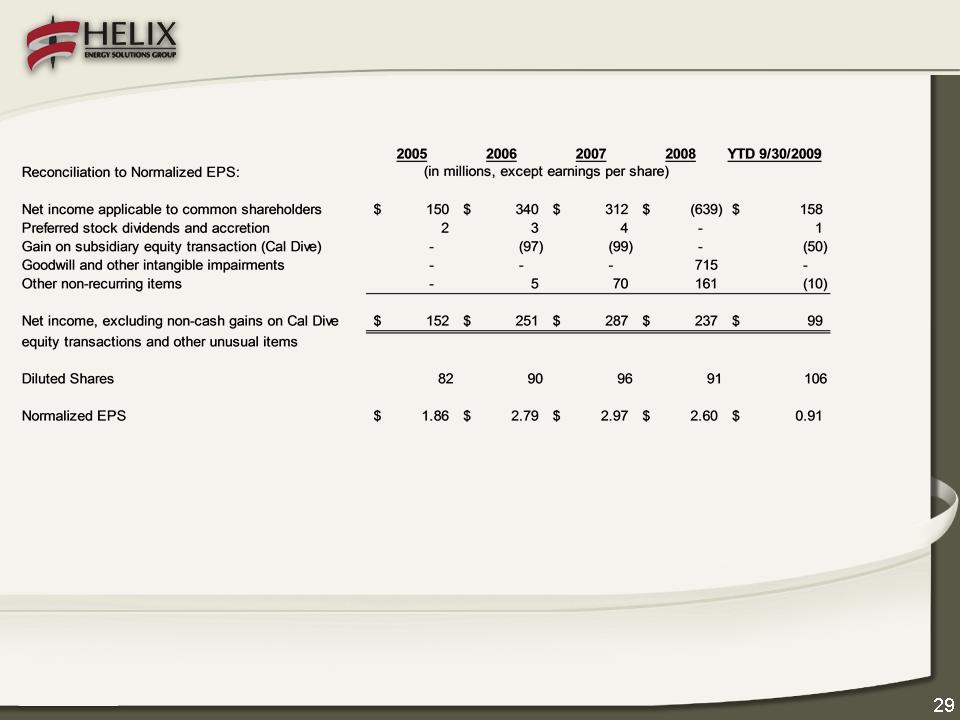

Earnings

Per Share (a)

- 2006

results exclude the impact of

the gain on sale in the Cal Dive IPO

and estimated incremental

overhead costs during the year.

the gain on sale in the Cal Dive IPO

and estimated incremental

overhead costs during the year.

- 2007

results exclude the impact of

the Cal Dive gain, impairments and

other unusual items.

the Cal Dive gain, impairments and

other unusual items.

- 2008 results exclude

non-cash

charges of $964 million for

reduction in carrying values of

goodwill and certain oil and gas

properties.

charges of $964 million for

reduction in carrying values of

goodwill and certain oil and gas

properties.

(a) See

Non-GAAP reconciliations on slide 29.

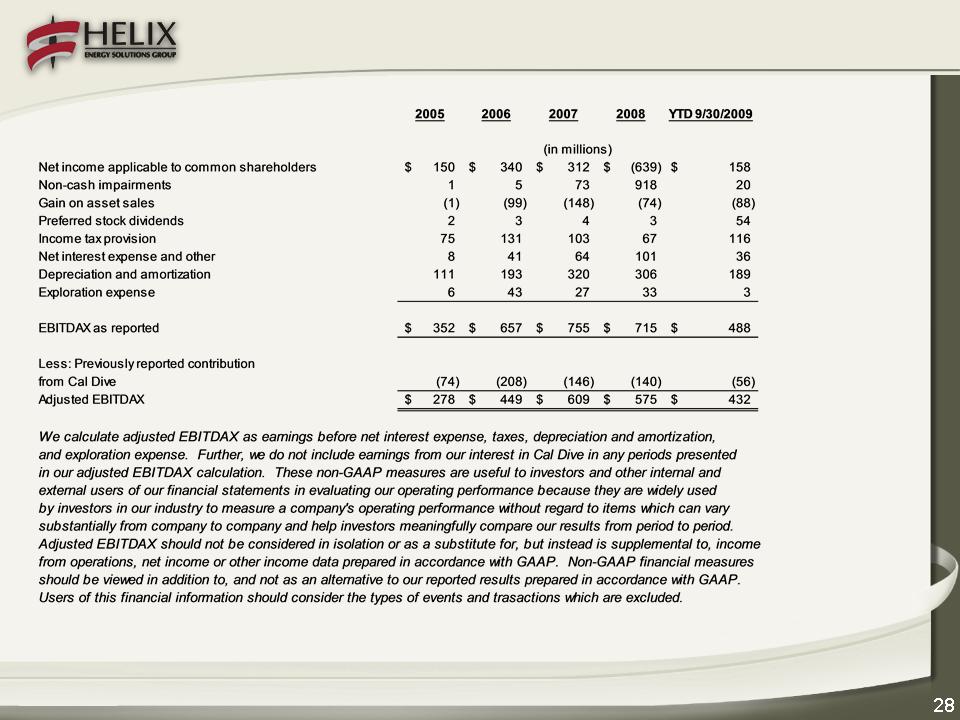

Significant

Cash Generation - EBITDAX(a)

-2006

results exclude the impact

of the gain on sale in the Cal

Dive IPO and estimated

incremental overhead costs

during the year.

of the gain on sale in the Cal

Dive IPO and estimated

incremental overhead costs

during the year.

-2007

results exclude the impact

of the Cal Dive gain,

impairments and other unusual

items.

of the Cal Dive gain,

impairments and other unusual

items.

-2008 results exclude

non-cash

impairments.

impairments.

-Excludes Cal Dive

contribution.

(a) See

Non-GAAP reconciliations on slide 28.

($

amounts in millions)

$278

$449

$432

$575

$609

Non

GAAP Reconciliations

Non

GAAP Reconciliations

Non

GAAP Reconciliations