Attached files

| file | filename |

|---|---|

| EX-3.2 - EXHIBIT 3.2 - CLOUD PEAK ENERGY INC. | a2195113zex-3_2.htm |

| EX-23.2 - EX-23.2 - CLOUD PEAK ENERGY INC. | a2195113zex-23_2.htm |

| EX-23.1 - EX-23.1 - CLOUD PEAK ENERGY INC. | a2195113zex-23_1.htm |

| EX-21.1 - EX-21.1 - CLOUD PEAK ENERGY INC. | a2195113zex-21_1.htm |

| EX-10.21 - EXHIBIT 10.21 - CLOUD PEAK ENERGY INC. | a2195113zex-10_21.htm |

| EX-10.42 - EX-10.42 - CLOUD PEAK ENERGY INC. | a2195113zex-10_42.htm |

Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO THE FINANCIAL STATEMENTS

As filed with the Securities and Exchange Commission on November 2, 2009

Registration No. 333-161293

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 3

TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

CLOUD PEAK ENERGY INC.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation) |

1221 (Primary Standard Industrial Classification Code Number) |

26-3088162 (I.R.S. Employer Identification Number) |

505 S. Gillette Ave.

Gillette, WY 82716

(307) 687-6000

(Address, including zip code, and telephone number, including area code, of registrant's principal executive offices)

Colin Marshall

Chief Executive Officer

Cloud Peak Energy Inc.

505 S. Gillette Ave.

Gillette, WY 82716

(307) 687-6000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Stuart H. Gelfond, Esq. Vasiliki B. Tsaganos, Esq. Fried, Frank, Harris, Shriver & Jacobson LLP One New York Plaza New York, NY 10004 Tel: (212) 859-8000 Fax: (212) 859-4000 |

Shane Orians, Esq. Rio Tinto Services Inc. 4700 Daybreak Parkway South Jordan, UT 84095 Tel: (801) 204-2803 Fax: (801) 204-2892 |

Richard A. Drucker, Esq. Davis Polk & Wardwell LLP 450 Lexington Avenue New York, NY 10017 Tel : (212) 450-4000 Fax: (212) 450-3800 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act (check one):

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý (Do not check if a smaller reporting company) |

Smaller reporting company o |

CALCULATION OF REGISTRATION FEE

|

||||

| Title of each class of securities to be registered |

Proposed maximum aggregate offering price(1)(2) |

Amount of registration fee |

||

|---|---|---|---|---|

Common stock, par value $0.01 per share |

$650,000,000 | $36,270(3) | ||

|

||||

- (1)

- Estimated

solely for the purpose of computing the amount of the registration fee pursuant to Rule 457(o) under the Securities Act of 1933.

- (2)

- Including

shares of common stock which may be purchased by the underwriters to cover over-allotments, if any.

- (3)

- Includes a $27,900 registration fee previously paid with the initial filing of this Form S-1 on August 12, 2009.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED NOVEMBER 2, 2009

Shares

CLOUD PEAK ENERGY INC.

Common Stock

This is the initial public offering of our common stock. We are selling shares of common stock. Prior to this offering, there has been no public market for our common stock. The initial public offering price of our common stock is expected to be between $ and $ per share. Our common stock has been approved for listing on the New York Stock Exchange under the symbol "CLD."

Immediately prior to this offering, we will acquire an interest in Rio Tinto America Inc.'s western U.S. coal business (other than the Colowyo mine) through the purchase of certain membership units indirectly held by Rio Tinto America in Cloud Peak Energy LLC or CPE LLC. We will use the net proceeds of this offering to finance this acquisition from Rio Tinto America. See "Use of Proceeds" and "Structuring Transactions and Related Agreements."

We will be a holding company and our sole asset will be our managing member interest in CPE LLC. Following the completion of the transactions described in this prospectus, we will own approximately % and Rio Tinto America will own indirectly approximately % of the economic interest in CPE LLC, assuming no exercise of the underwriters' overallotment option. Our only business will be acting as the sole manager of CPE LLC and, as such, we will operate and control all of the business and affairs of CPE LLC.

The underwriters have an option to purchase a maximum of additional shares of common stock from us to cover over-allotments of shares of common stock. If the underwriters exercise their option, we will use the net proceeds from the over-allotment option to purchase additional common membership units of CPE LLC indirectly held by Rio Tinto America.

Investing in our common stock involves risks. See "Risk Factors" on page 23.

| |

Price to Public |

Underwriting Discounts and Commissions |

Proceeds, before expenses, to us |

|||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Per Share | $ | $ | $ | |||||||

| Total | $ | $ | $ | |||||||

Delivery of the shares of common stock will be made on or about , 2009.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Credit Suisse | Morgan Stanley | RBC Capital Markets |

The date of this prospectus is , 2009.

You should rely only on the information contained in this document or any free writing prospectus prepared by or on behalf of us or to which we have referred you. We have not authorized anyone to provide you with information that is different from the information contained in this document or any free writing prospectus prepared by or on behalf of us or to which we have referred you. This document may only be used where it is legal to sell these securities. The information in this document may only be accurate on the date of this document.

Dealer Prospectus Delivery Obligation

Until , 2009 (25 days after the commencement of this offering), all dealers that effect transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealer's obligation to deliver a prospectus when acting as an underwriter and with respect to unsold allotments or subscriptions.

i

This summary highlights information contained elsewhere in this prospectus. This summary does not contain all of the information you should consider before investing in our common stock. You should read the entire prospectus carefully, including the section describing the risks of investing in our common stock under "Risk Factors" and the consolidated financial statements of our predecessor, Rio Tinto Energy America Inc., contained elsewhere in this prospectus before making an investment decision. Some of the statements in this summary constitute forward-looking statements. See "Special Note Regarding Forward-Looking Statements."

In this prospectus, unless the context otherwise requires, references to:

- •

- "Cloud Peak Energy," "we," "us," "our" or the "Company" refer to Cloud Peak Energy Inc.,

which was incorporated on July 31, 2008 in preparation for this offering, and its consolidated subsidiary CPE LLC and the businesses that CPE LLC will operate after giving effect

to the structuring transactions described in this prospectus and assuming completion of this offering;

- •

- "CPE LLC" refers to Cloud Peak Energy LLC, a Delaware limited liability company,

formerly known as Rio Tinto Sage LLC, that will be the operating company for our business, and in which the Company will acquire a managing member interest and become a member and the sole

manager in connection with this offering;

- •

- "Rio Tinto Energy America" or "RTEA" refers to Rio Tinto Energy America Inc., our

predecessor for accounting purposes, which contributed certain assets used in the operations of CPE LLC;

- •

- "Rio Tinto America" refers to Rio Tinto America Inc., which indirectly contributed certain

assets used in the operations of CPE LLC through its subsidiaries and is the owner of RTEA;

- •

- "Rio Tinto" refers to Rio Tinto plc and Rio Tinto Limited and their subsidiaries,

collectively, one of the largest mining companies in the world. Rio Tinto plc is the ultimate parent company of Rio Tinto America and RTEA;

and

- •

- "KMS" refers to Kennecott Management Services Company, a wholly-owned subsidiary of Rio Tinto America.

Certain industry and other technical terms used throughout this prospectus relating primarily to our business, including terms related to the coal industry, coal reserves, mining equipment and coal regions in the U.S. are defined under "Glossary of Selected Terms" beginning on page 231 of this prospectus.

Cloud Peak Energy Inc.

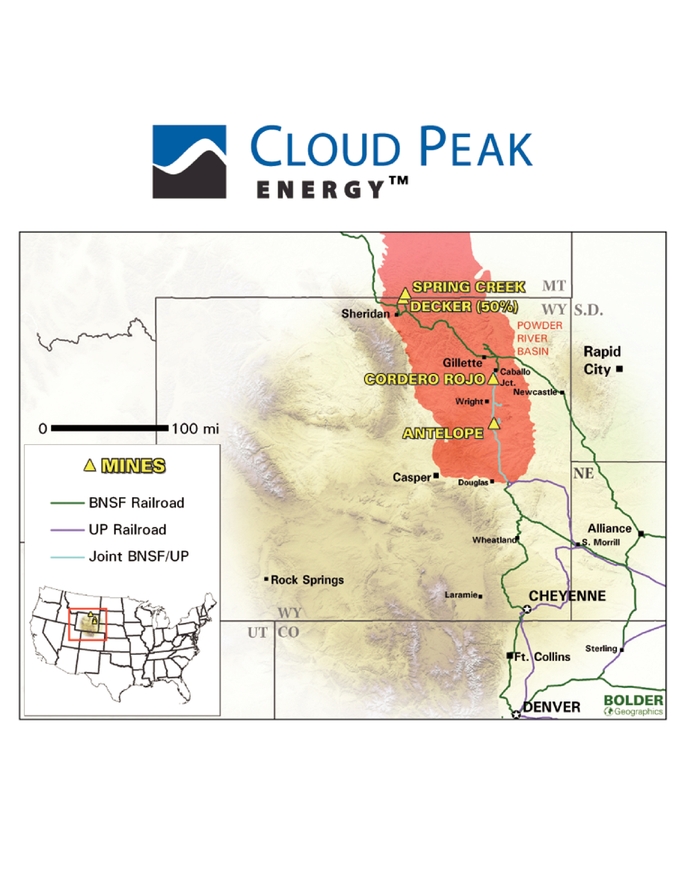

We are the third largest producer of coal in the U.S. and in the Powder River Basin, or PRB, based on 2008 coal production. We operate some of the safest mines in the industry. According to data from the Mine Safety and Health Administration, or MSHA, in 2008 we had the lowest employee all injury incident rate among the five largest U.S. coal producing companies. We operate solely in the PRB, the lowest cost coal producing region of the major coal producing regions in the U.S., and operate two of the five largest coal mines in the region and in the U.S. Our operations include three wholly-owned surface coal mines, two of which are in Wyoming and one in Montana. We also own a 50% interest in a fourth surface coal mine in Montana. We produce sub-bituminous steam coal with low sulfur content and sell our coal primarily to domestic electric utilities. Steam coal is primarily consumed by electric utilities and industrial customers as fuel for electricity generation. In 2008, the coal we produced generated approximately 4.4% of the electricity produced in the U.S.

Following the completion of this offering, CPE LLC will own Rio Tinto America's western U.S. coal business, except for the Colowyo coal mine in Colorado. We will be a holding company that manages CPE LLC, and our only business and sole asset will be our managing member interest in CPE LLC. Following the completion of the transactions described in this prospectus, Cloud Peak Energy Inc. will own approximately % and Rio Tinto America indirectly will own approximately

1

% of the economic interest in CPE LLC, assuming no exercise of the underwriters' overallotment option and including shares of restricted common stock issued to directors and employees in connection with this offering.

On October 1, 2009, CPE LLC (formerly known as Rio Tinto Sage LLC) sold the Jacobs Ranch mine to Arch Coal, Inc. and did not retain the proceeds from that sale. We refer to this transaction as the Jacobs Ranch Sale. The Colowyo and Jacobs Ranch mines are reflected as discontinued operations in the consolidated financial statements of our predecessor, RTEA, contained elsewhere in this prospectus.

For the year ended December 31, 2008 and the nine months ended September 30, 2009 we:

- •

- produced 97.1 million and 69.9 million tons of coal, respectively;

- •

- generated revenues of $1.24 billion and $1.06 billion, respectively; and

- •

- had income from continuing operations of $88.3 million and $147.3 million, respectively.

The tables below summarize the tons of coal produced and proven and probable coal reserves by mine as of December 31, 2008 and other data regarding our controlled coal:

Mine

|

Tons Produced in 2008 | Proven Coal Reserves | Probable Coal Reserves |

Total Proven and Probable Coal Reserves |

|||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

(in millions) |

(nearest million) |

(nearest million) |

(nearest million) |

|||||||||

Antelope |

35.8 | 286 | 40 | 326 | |||||||||

Cordero Rojo |

40.0 | 331 | 72 | 402 | |||||||||

Spring Creek |

18.0 | 263 | 54 | 317 | |||||||||

Decker(1) |

3.3 | 5 | — | 5 | |||||||||

Total |

97.1 | 885 | 165 | 1,050 | |||||||||

- (1)

- Based on our 50% interest in our Decker mine.

Non-reserve Coal Deposits

|

Million Tons | |||

|---|---|---|---|---|

Other Non-reserve Coal Deposits as of December 31, 2008 (includes 108 million tons of non-reserve coal deposits acquired in April 2008 with the South Maysdorf LBA tract). |

261 | |||

Additional Acquired Tonnage in May 2009 relating to our Cordero Rojo mine (according to Bureau of Land Management estimates) |

55 | |||

The following chart sets out the weighted average price per ton for tons committed for sale under our fixed-price customer coal contracts in the following years:

Contracted Coal as of September 30, 2009(1)

| |

2009 | 2010 | 2011 | 2012 | 2013 | |||||

|---|---|---|---|---|---|---|---|---|---|---|

Contracted coal sales (millions of tons) |

93 | 90 | 54 | 32 | 19 | |||||

Average sold-to price ($/ton) |

$11.89 | $12.80 | $13.68 | $13.00 | $12.37 |

- (1)

- Contracted coal sales include fixed price and index-based price tons under contract. Excludes contracted coal sales from Decker.

Our business and operations, including our strengths and strategy listed below, are subject to numerous risks and uncertainties, including risks related to coal prices and mining operations, coal consumption, including electricity demand, and economic and financial conditions, among others, any

2

or all of which could materially and adversely affect our business and market position. See "Risk Factors" beginning on page 23 of this prospectus.

Our Strengths

We believe that the following strengths enhance our market position:

We are the third largest coal producer in the U.S. and in the PRB and have a significant reserve base. Based on 2008 production of 97.1 million tons, we are the third largest coal producer in the U.S. and in the PRB. As of December 31, 2008, we controlled approximately 1.3 billion tons of coal, consisting of approximately 1.05 billion tons of proven and probable coal reserves and approximately 261 million tons of non-reserve coal deposits.

We operate highly productive mines located solely in the PRB, the lowest cost coal producing region of the major coal producing regions in the U.S. All of our mines are located in the PRB, which is the lowest cost coal producing region of the major coal producing regions in the U.S. We operate two of the five largest mines in the PRB and the U.S. We believe that our large PRB mines provide us with significant economies of scale. We benefit from the fact that our mines are among the lowest cost and highest producing mines in the U.S. Because the operational costs of PRB mines are low relative to other major coal producing regions, we believe that we are better able to maintain production levels at low costs despite the adverse impact of economic downturns on our revenues. However, our coal mining operations are subject to numerous operating risks which could result in materially increased operating expenses or decreased production levels.

Our acquisition of additional LBAs and surface rights and our substantial capital investments in our mines in recent years have positioned us well for the future. We have focused on strategic acquisitions and subsequent expansions of large, low operating cost, low-sulfur operations in the PRB and replacement of, and additions to, our reserves through the federal coal leasing process, also known as the Lease by Application, or LBA, process and the acquisition of related surface rights. From January 1, 2005 to September 1, 2009, we acquired 444 million tons of reserves, in addition to the North Maysdorf tract that the BLM estimates to contain 55 million tons of non-reserve coal deposits. We acquired the North Maysdorf tract for a total commitment of $48.1 million, of which we have already made cash installment payments of $9.6 million. From January 1, 2006 to September 30, 2009, we have also made significant capital expenditures in our mining facilities and equipment, investing $371.3 million. These investments have increased our existing mines' capacity and productivity. We have also nominated LBA tracts of land that we believe contain, as applied for, approximately 800 million tons of non-reserve coal deposits according to our estimates and subject to final determination by the BLM of the final boundaries and tonnage for these tracts. Accordingly, we believe we are well-positioned for the future through the strategic acquisition of additional LBAs and surface rights. If we are unable to acquire additional LBAs or surface rights, our business, financial condition or results of operations could be adversely affected.

We are well-positioned to take advantage of favorable long-term industry trends in the U.S. and in the PRB region. Historically, increases in U.S. coal consumption have been driven primarily by increased use of existing electricity generation capacity and the construction of new coal-fired power plants. While demand for electricity in our target markets has decreased since mid-2008, it is expected to recover as the economy strengthens. According to the U.S. Energy Information Administration, or EIA (report released April 2009), annual U.S. coal demand is projected to reach 1.24 billion tons by 2020, compared to demand of 1.12 billion tons in 2008. Production constraints and increased export demand for eastern U.S. coal reduces the availability of eastern U.S. coal to the U.S. domestic market. As a result, we expect coal consumers may increasingly substitute their use of eastern U.S. coal with PRB coal. Increasingly stringent air quality laws, safety regulations and the related costs of scrubbers may favor low-sulfur PRB coal over other types of coal, which may increase domestic demand for PRB

3

coal. According to the EIA, the western U.S. represented 54% of U.S. coal production in 2008 and is expected to represent approximately 57% of U.S. coal production in 2020. PRB coal demand is expected to increase during this same time period by 70 million tons. The EIA's projections take into account the provisions of the American Recovery and Reinvestment Act of 2009, or ARRA, and assume that no pending or proposed federal or state carbon emissions legislation is enacted and that a number of additional coal-fired power plants will be built during this period. If greenhouse gas emissions from coal-fired power plants are subject to extensive new regulation in the U.S. pursuant to future U.S. treaty obligations, statutory or regulatory changes under the Clean Air Act, or federal or additional state adoption of a greenhouse gas regulatory scheme, or if reductions in greenhouse gas emissions are mandated by courts or through other legally enforceable mechanisms, absent other factors, the EIA's projections with respect to the demand for coal may not be met. If the increased demand for electricity is met by new power plants fueled by alternative energy sources, such as natural gas, or if additional state or federal mandates are implemented to support or mandate the use of alternative energy sources, these long-term industry trends may not continue.

Our employee-related liabilities are low for our industry. We only operate surface mines. As a result, our exposure to certain health claims and post-retirement liabilities, such as black-lung disease, is lower relative to some of our publicly traded competitors that operate underground mines. Following the completion of this offering, the obligations for future pension and post-retirement welfare for active employees will be assumed by us, and obligations for employees who have retired as of the date of the completion of this offering will be retained by Rio Tinto.

We have a strong safety and environmental record. We operate some of the industry's safest mines. According to data from MSHA, in 2008 we had the lowest employee all injury incident rate among the five largest U.S. coal producing companies. All of the mines we operate are certified to the international standard for environmental management systems (ISO 14001). We are committed to continuing to maintain a system that controls and reduces the environmental impacts of mining operations. We have also won numerous state and federal awards for our strong safety and environmental record.

We have longstanding relationships with our customers, a majority of whom have an investment grade credit rating. We focus on building long-term relationships with creditworthy customers through our reliable performance and commitment to customer service. We supply coal to over 46 electric utilities and over 80% of our sales were to customers with an investment grade credit rating as of September 2009. Moreover, over 74% of our 2008 sales were to customers with whom we have had relationships for more than 10 years.

Our senior management team has extensive industry experience. Our named executive officers have significant work experience in the mining and energy industries, with an average of 20 years of relevant mining experience. Most of our named executive officers gained this experience through various positions held within Rio Tinto, one of the largest mining companies in the world.

Our Strategy

Our business strategy is to:

Capitalize on favorable long-term market conditions for PRB coal producers. Subject to market conditions and other factors, we have the ability to take advantage of potential growth capacity in our existing mines. Our managed mines have the capacity to increase their total annual production by up to 8 million tons with minimal additional capital expenditures over the next four years. The long-term market dynamics for coal producers in the PRB remain favorable. The EIA estimates that PRB coal demand is expected to grow by 70 million tons between 2008 and 2020. Production constraints and increased export demand for eastern U.S. coal reduces the availability of eastern U.S. coal to the U.S. domestic market. As a result, we expect coal consumers may increasingly substitute their use of eastern

4

U.S. coal with PRB coal. Increasingly stringent air quality laws, safety regulations and the related cost of scrubbers favor low-sulfur PRB coal over other types of coal. We intend to continue to capitalize on these market dynamics. By seeking additional expansion opportunities in existing and new mines in the PRB, we aim to maintain or improve our market position in the PRB. Furthermore, while only a small percentage of PRB coal is currently exported, we intend to seek opportunities to increase exports for our higher Btu coal from our Spring Creek mine.

Continue to build our reserves. We have historically focused on strategic acquisitions and subsequent expansions of large, low-cost, low-sulfur operations in the PRB and replacement of, and additions to, our reserves through the acquisition of companies, mines and reserves. We will continue to seek to increase our reserve position to maintain our existing production capacity by acquiring federal coal through the LBA process and by purchasing surface rights for land adjoining our current operations in Wyoming and Montana. We have applications outstanding for two LBAs that we anticipate to be bid at some time during the next four years. These LBAs cover, as applied for, approximately 800 million tons of non-reserve coal deposits according to our estimates and subject to final determination by the BLM of the final boundaries and tonnage for these LBA tracts. We will continue to explore additional opportunities to increase our reserve base; however, if we are unable to do so, we may be unable to maintain our current production capacity.

Focus on operating efficiency and leverage our economies of scale. We seek to control our costs by continuing to improve on our operating efficiency. Following this offering, we will remain the third largest producer of coal in the U.S. based on 2008 production statistics. We believe we will continue to benefit from significant economies of scale through the integrated management and operation of our three wholly-owned mines, although our results as a stand-alone public company could be significantly different from our historical financial results as part of Rio Tinto. We have historically improved our existing operations and evaluated and implemented new mining equipment and technologies to improve our efficiency. Our large fleet of mining equipment, information technology systems and coordinated equipment utilization and maintenance management functions allow us to enhance our efficiency. Our experienced and well-trained workforce is key in identifying and implementing business improvement initiatives.

Leverage our excellence in safety and environmental compliance. We operate some of the safest coal mines in the U.S. We have also achieved recognized standards of environmental stewardship. We continue to implement safety measures and environmental initiatives to promote safe operating practices and improved environmental stewardship. We believe the ability to minimize injuries and maintain our focus on environmental compliance improves our productivity, lowers our costs, helps us attract and retain our employees and makes us an attractive candidate for ventures with third parties.

Opportunistically pursue acquisitions that will create value and expand our core business. We intend to pursue acquisition opportunities that are consistent with our business strategy and that we believe will create value for our shareholders. However, we may be unable to successfully integrate these acquired companies or realize the benefits we anticipate from an acquisition. In the long term and subject to market conditions, we may pursue international acquisitions.

Coal Market Outlook

Coal markets and coal prices are influenced by a number of factors and vary materially by region. Coal consumption in the U.S., particularly with respect to coal produced in the PRB, has been driven in recent periods by several market dynamics and trends, which may or may not continue, including the following:

Favorable outlook for the U.S. steam coal market. Growth in electricity demand continues to drive domestic demand for steam coal. The recent economic slowdown has reduced electricity and coal demand since mid-2008 and the demand for, and consumption of, coal in the electric power sector in

5

2009 is projected to decline. The long-term demand for electricity, however, is projected to increase at an average annual rate of approximately 0.5% from 2008 through 2020, according to the EIA. The EIA's projections that were issued in April 2009 take into account the provisions of the ARRA and assume that no pending or proposed federal or state carbon emissions legislation is enacted and that a number of additional coal-fired power plants will be built during the period. The EIA projects that increased utilization rates by existing power plants and new power plant construction will be drivers of coal demand. For 2010, the EIA is forecasting that total electricity generation will increase by 1.3% over 2009, assuming a recovering economy. Coal consumption for the electric power sector is projected to increase to 968.3 million tons in 2010, a 22.3 million ton increase over estimated 2009 consumption of 946.0 million tons. However, a smaller number of plants than projected may be built, existing plants may not be able to significantly increase capacity or utilization rates and the number of planned plant retirements may increase more than expected. In addition, if greenhouse gas emissions from coal-fired power plants are subject to extensive new regulation in the U.S. pursuant to future U.S. treaty obligations, statutory or regulatory changes under the Clean Air Act, or federal or additional state adoption of a greenhouse gas regulatory scheme, or if reductions in greenhouse gas emissions are mandated by courts or through other legally enforceable mechanisms, absent other factors, the EIA's projections with respect to the demand for coal may not be met.

Expected long-term increases in international demand and the U.S. export market. International demand for coal continues to be driven by rapid growth in electrical power generation capacity in Asia, particularly in China and India. China and India represented approximately 48% of total world coal consumption in 2006 and are expected to account for approximately 59% by 2030, according to the EIA. During 2007 and the first half of 2008, coal exports increased significantly as demand for U.S. steam and metallurgical coal from the Appalachian and PRB regions increased. Demand for steam and metallurgical coal has declined since mid-2008, as the United States economy and most international economies deteriorated due to the global economic downturn. We expect that these economic challenges will result in lower U.S. exports of coal in 2009 than in 2008. If global economic conditions improve, we anticipate that U.S. exports of coal would eventually increase; however, future exports of coal may not meet or exceed 2008 levels. To the extent that production constraints and increased export demand for eastern U.S. coal reduces the availability of eastern U.S. coal to the U.S. domestic market, we expect coal consumers may increasingly substitute their use of eastern U.S. coal with PRB coal.

Changes in U.S. regional production. Coal production in the Central Appalachian region of the U.S. has declined in recent years because of production difficulties, reserve degradation and difficulties acquiring permits needed to conduct mining operations. In addition, underground mining operations have become subject to additional, more costly and stringent safety regulations, increasing their operating costs and capital expenditure requirements. We believe that many eastern utilities are considering blending coals as an option to offset production issues and meet more stringent environmental requirements. Shortages and decreases in supply in the eastern U.S. continue to affect pricing in the entire U.S. market.

Coal remains a cost-competitive energy source relative to alternative fossil fuels and other alternative energy sources. Coal generally, and PRB coal in particular, has historically been a low-cost source of energy relative to its substitutes because of the high prices for alternative fossil fuels. Coal also has a lower all-in cost relative to other alternative energy sources, such as nuclear, hydroelectric, wind and solar power. Although the price for certain alternative fuels, such as natural gas, has recently declined, PRB coal continues to be a cost-competitive energy source because it exists in greater abundance and is easier and cheaper to mine than coal produced in other regions. Changes in the prices for other fossil fuels or alternative energy sources in the future could impact the price of coal. Current low natural gas prices in the U.S. and Europe are expected to lower demand for coal and lead to reduced demand for exports in the near term. In addition, if greenhouse gas emissions from coal-fired power plants are subject to extensive new regulation in the U.S. pursuant to future U.S. treaty obligations,

6

statutory or regulatory changes under the Clean Air Act, or federal or additional state adoption of a greenhouse gas regulatory scheme, or if reductions in greenhouse gas emissions are mandated by courts or through other legally enforceable mechanisms, alternative energy sources may become more cost-competitive with coal, which may lead to lower demand for coal. See "Risk Factors—Risks Related to Our Business—New and potential future regulatory requirements relating to greenhouse gas emissions could affect our customers and could reduce the demand for coal as a fuel source and cause coal prices and sales of our coal to materially decline" and "Environmental and Other Regulatory Matters—Climate Change."

Developments in clean coal technology and related regulatory initiatives. The U.S. government has recently accelerated its investment in clean coal technology development with the ARRA signed into law by President Obama in February 2009. The ARRA targets $3.4 billion for U.S. Department of Energy fossil fuel programs, including $1.52 billion for carbon capture and sequestration, or CCS, research, $800 million for the Clean Coal Power Initiative, a 10-year program supporting commercial CCS, and $50 million for geology research. Although laws regulating greenhouse gas emissions may result in decreased demand for coal in the short-term, we believe that successful development and funding of these technologies through the ARRA could result in stable demand for coal in the long term. However, cost-effective technologies may not be developed and deployed in a timely manner.

Near-term pricing volatility. U.S. coal markets have recently experienced significant volatility. By the end of 2008, published thermal coal prices in most major markets declined from their mid-2008 highs, largely reversing gains from the first half of 2008. Declining coal demand, coupled with increasing customer stockpiles and spurred by the onset of the global economic downturn, has further softened pricing in 2009. The EIA projects that domestic electricity demand in 2009 will decline from 2008 levels. In addition, the prices for alternative fossil fuels, such as oil and natural gas, have declined relative to the recent highs. Future decreases in the price of alternative fuels could impact the price of coal. See "Risk Factors—Risks Related to Our Business—Coal prices are subject to change and a substantial or extended decline in prices could materially and adversely affect our revenues and results of operations, as well as the value of our coal reserves."

Increasingly stringent air quality regulations. A series of more stringent requirements related to particulate matter, ozone, haze, mercury, sulfur dioxide, nitrogen oxide and other air pollutants have been proposed and/or enacted by federal and/or state regulatory authorities in recent years. As a result of some of these regulations, demand for western U.S. coal has increased as coal-fired electricity producers have switched from bituminous coal to lower sulfur sub-bituminous coal. The PRB has benefited from this switch and its market share has increased accordingly. However, increasingly stringent air regulations may lead some coal-fired plants to install additional pollution control equipment, such as scrubbers, thereby reducing the need for low-sulfur coal. Considerable uncertainty is associated with these air emission regulations, some of which have been the subject of legal challenges in courts, and the actual timing of implementation remains uncertain. As a result, it is not possible to determine the impact of such regulatory initiatives on coal demand nationwide, but it may be materially adverse. See "Risk Factors—Risks Related to Our Business—Extensive environmental regulations, including existing and potential future regulatory requirements relating to air emissions, affect our customers and could reduce the demand for coal as a fuel source and cause coal prices and sales of our coal to materially decline" and "—Because we produce and sell coal with low-sulfur content, a reduction in the price of sulfur dioxide emission allowances or increased use of technologies to reduce sulfur dioxide emissions could materially and adversely affect the demand for our coal and our results of operations" and "Environmental and Other Regulatory Matters."

See "The Coal Industry" and "The Coal Industry—Special Note Regarding the EIA's Market Data and Projections."

7

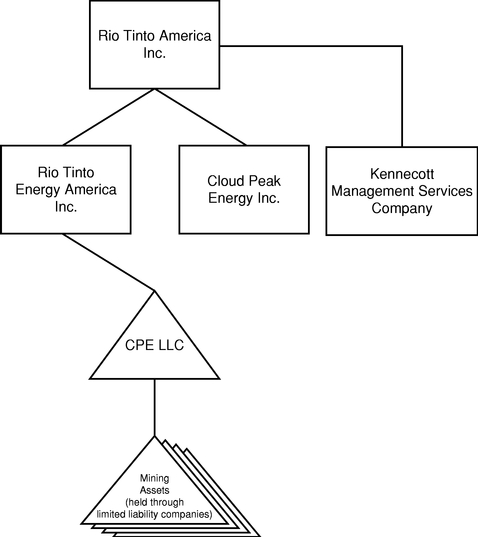

Our Corporate History and Structure

Rio Tinto initially formed RTEA in 1993 as Kennecott Coal Company which was subsequently renamed Kennecott Energy and Coal Company. Between 1993 and 1998, Kennecott Energy and Coal Company acquired the Antelope, Colowyo, Jacobs Ranch and Spring Creek coal mines and the Cordero coal mine and Caballo Rojo coal mine, which are currently operated together as the Cordero Rojo coal mine, and a 50% interest in the Decker coal mine, which is managed by a third-party mine operator. In 2006, Kennecott Energy and Coal Company was renamed Rio Tinto Energy America Inc., as part of Rio Tinto's global branding initiative. In order to separate certain businesses from RTEA, in December 2008, RTEA contributed Rio Tinto America's western U.S. coal business to CPE LLC (other than the Colowyo mine, which was not contributed to CPE LLC due to restrictions contained in its existing financing arrangements and which is now owned indirectly by Rio Tinto America). On October 1, 2009 we sold the Jacobs Ranch mine to Arch Coal, Inc. and did not retain the proceeds from that sale.

Cloud Peak Energy Inc. was incorporated in Delaware on July 31, 2008. Prior to this offering, it did not engage in any activities, except in preparation for this offering, and has had no operations.

The following simplified diagram depicts our organizational structure prior to this offering.

See "Structuring Transactions and Related Agreements—History" for a more complete diagram depicting our organizational structure prior to this offering.

8

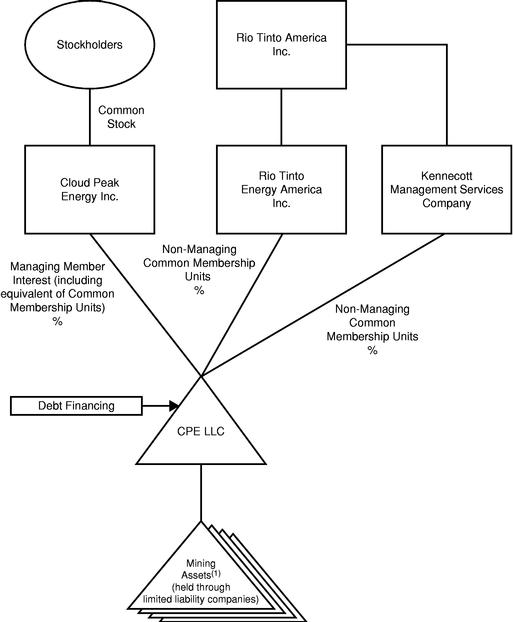

Immediately prior to the completion of this offering, we will enter into an acquisition agreement, or the Acquisition Agreement, with RTEA pursuant to which we will acquire a portion of RTEA's interest in Rio Tinto America's western U.S. coal business (other than the Colowyo mine) represented by common membership units of CPE LLC in exchange for a promissory note that we will issue to RTEA, or the CPE Note. The Acquisition Agreement will require us to use the net proceeds of this offering to immediately repay the CPE Note. After the completion of this offering, we will be a holding company that manages CPE LLC, and our only business and material asset will be our managing member interest in CPE LLC. Following the completion of the transactions described in this prospectus, we will own approximately % and Rio Tinto America indirectly will own approximately % of the economic interest in CPE LLC, assuming no exercise of the underwriters' overallotment option. Our only source of cash flow from operations will be distributions from CPE LLC pursuant to its LLC Agreement and management fees and cost reimbursements pursuant to a management services agreement between us and CPE LLC.

Concurrently with this offering, CPE LLC is also expected to enter into a $ million revolving secured credit facility and to issue $ million aggregate principal amount of senior unsecured notes to be issued in two tranches maturing in and , in accordance with Rule 144A under the Securities Act of 1933, as amended, which we refer to collectively as the senior notes. We estimate that the net proceeds of the senior notes offering, after deducting estimated original issue discount, initial purchasers' discounts and commissions and offering expenses, will be approximately $ million. We expect that CPE LLC will use the net proceeds from the senior notes offering together with the net proceeds of this offering as described under "Use of Proceeds." This offering, the senior notes offering and the closing of CPE LLC's revolving secured credit facility are each conditioned upon the closing of each other.

The concurrent offering of the senior notes will not be registered under the Securities Act of 1933, as amended, or the Securities Act, or the securities laws of any other jurisdiction, and the senior notes may not be offered or sold in the United States absent registration or an applicable exemption from registration requirements. The senior notes will only be offered to qualified institutional buyers in the United States pursuant to Rule 144A under the Securities Act and outside the United States pursuant to Regulation S under the Securities Act. This description and the other information in this prospectus regarding the concurrent offering of the senior notes is included in this prospectus solely for informational purposes. Nothing in this prospectus should be construed as an offer to sell, or the solicitation of an offer to buy, the senior notes.

9

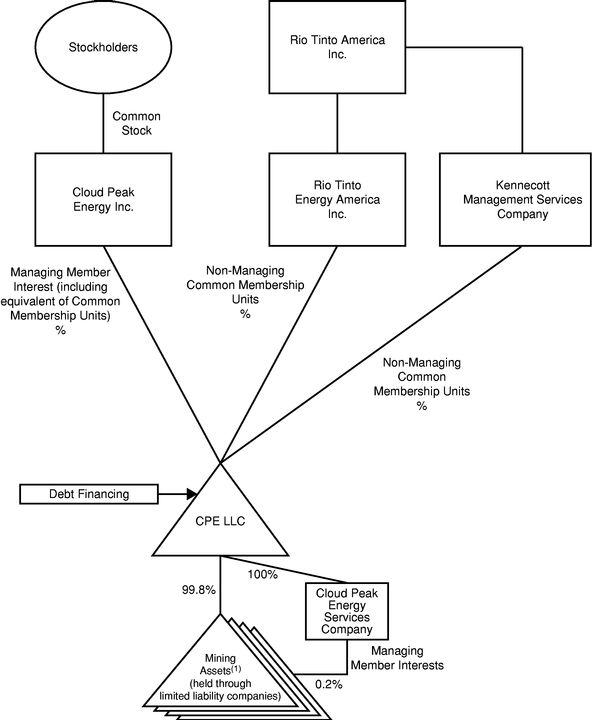

The following simplified diagram depicts our organizational structure immediately after the transactions described in this prospectus (assuming no exercise of the underwriters' overallotment option):

- (1)

- CPE LLC's wholly-owned domestic restricted subsidiaries will serve as guarantors of CPE LLC's debt in connection with the debt financing transactions.

See "Structuring Transactions and Related Agreements—Holding Company Structure" for a more complete diagram depicting our organizational structure following this offering and additional information regarding these transactions. References to our managing member interest mean the management and ownership interest as the managing member in CPE LLC, which will initially include membership interests equivalent to approximately % of the outstanding common membership units (assuming no exercise of the underwriters' overallotment option), and includes any and all benefits to which the managing member is entitled as provided in CPE LLC's LLC Agreement, together with all obligations of the managing member to comply with the terms and provisions of CPE LLC's LLC Agreement.

10

Our principal executive office is located at 505 S. Gillette Avenue, Gillette, Wyoming 82716, and our telephone number at that address is (307) 687-6000. Following the completion of this offering, we intend to maintain a website at www.cloudpeakenergy.com. The information that will be contained on, or that will be accessible through, our website is not part of this prospectus.

"Cloud Peak Energy" and the Cloud Peak Energy logo are trademarks and service marks of Cloud Peak Energy Inc. All other trademarks, service marks or trade names appearing in this prospectus are owned by their respective holders.

Presentation of Our Coal Data and Pro Forma Consolidated Financial Information and Coal Market Data

Our Historical Financial Information

Rio Tinto Energy America Inc., or RTEA, is considered to be our predecessor for accounting purposes and its consolidated financial statements are our historical consolidated financial statements. Unless otherwise indicated, historical references contained in this prospectus in "—Summary Actual and Pro Forma Consolidated Financial Data," "Selected Consolidated Financial and Operating Data," "Management's Discussion and Analysis of Financial Condition and Results of Operations—Results of Operations," and our historical consolidated financial statements contained elsewhere in this prospectus, relate to RTEA and include, as discontinued operations, results from the Colowyo mine, the Jacobs Ranch mine and the uranium mining venture, which will not be owned by CPE LLC after this offering.

Pro Forma Financial Information

When we refer to our pro forma financial information we are giving effect to:

- •

- the structuring transactions and related agreements, including the separation from Rio Tinto to be completed in connection

with this offering as described in "Structuring Transactions and Related Agreements";

- •

- the $ million revolving secured credit facility and $ million aggregate

principal amount of senior unsecured notes to be issued in two tranches maturing in and , which CPE LLC will enter into and issue concurrently with

this offering,

and which we refer to as the debt financing transactions;

- •

- the issuance of approximately shares of restricted common stock to be

issued to our directors and

employees in connection with this offering, which vest three years after the pricing of our initial public offering; and

- •

- the issuance of the shares of our common stock in this offering and subsequent use of proceeds.

The pro forma consolidated statement of operations presents financial information through income (loss) from continuing operations. Accordingly, the income (loss) from discontinued operations related to the Colowyo mine, the Jacobs Ranch mine and the uranium mining venture are not reflected in continuing operations and no pro forma adjustment will be necessary in the pro forma consolidated statement of operations.

Our Coal Data

References to our coal production, sales and purchases and our reserves and similar items contained in this prospectus exclude the Colowyo mine and the Jacobs Ranch mine which will not be owned by CPE LLC after this offering.

11

References to BLM estimates are given as of the date we acquired the lease for the related LBA tract.

Through our indirect, wholly-owned subsidiary, we currently hold a 50% interest in the Decker mine in Montana through a joint-venture agreement with an indirect, wholly-owned subsidiary of Level 3 Communications, Inc., or Level 3. The Decker mine is managed by a third-party mine operator. Information related to our coal production, reserves, purchases and revenues, contained in this prospectus and information in our consolidated financial statements contained elsewhere in this prospectus, unless otherwise indicated, includes amounts reflecting our 50% interest in the Decker mine.

Coal Market Data

Market data used in this prospectus has been obtained from governmental and independent industry sources and publications, such as the U.S. Energy Information Administration, or EIA, the National Mining Association, or NMA, and the Mine Safety and Health Administration, or MSHA, and, unless otherwise indicated, is based on data and reports published in 2008 or 2009 but may relate to prior years. We have not independently verified the data obtained from these sources, and we cannot assure you of the accuracy or completeness of the data. Industry projections of the EIA's report released in April 2009 reflect provisions of the ARRA that were enacted in mid-February 2009. In addition, industry projections of the EIA are subject to numerous assumptions and methodologies chosen by the EIA, including that laws and regulations in effect at the time of the projections remain unchanged and that no pending or proposed federal or state carbon emissions legislation has been enacted and that a number of additional coal-fired power plants will be built during the period. Therefore, the EIA's projections do not take into account potential regulation of greenhouse gas emissions pursuant to future U.S. treaty obligations, statutory or regulatory changes under the Clean Air Act, or federal or additional state adoption of a greenhouse gas regulatory scheme or reductions in greenhouse gas emissions mandated by courts or through other legally enforceable mechanisms. The EIA's projections with respect to the demand for coal may not be met, absent other factors, if comprehensive carbon emissions legislation is enacted. In addition, the economic conditions accounted for in the EIA's industry projections reflect existing and projected economic conditions at the time the projections were made and do not necessarily reflect current economic conditions or any subsequent deterioration of economic conditions. Forward-looking information obtained from these sources is subject to the same qualifications and the additional uncertainties regarding the other forward-looking statements contained in this prospectus. See "Special Note Regarding Forward-Looking Statements" and "The Coal Industry—Special Note Regarding the EIA's Market Data and Projections."

12

Common stock offered by us |

shares | |

Restricted common stock issued to directors and employees in connection with this offering |

shares |

|

Common stock to be outstanding after this offering |

shares |

|

Over-allotment option |

We have granted the underwriters a 30-day option to purchase on a pro rata basis up to additional shares of our common stock at the initial public offering price less underwriting discounts and commissions. The option may be exercised only to cover any over-allotments of common stock. If the underwriters exercise their option in full, we will use the net proceeds from the over-allotment to purchase additional common membership units in CPE LLC held by RTEA, at a price per unit equal to the public offering price per share, less underwriting discounts and commissions. |

|

Common membership units in CPE LLC to be held by us and Rio Tinto immediately after this offering |

common membership units ( common membership units if the underwriters exercise their overallotment option). RTEA and KMS will hold common membership units immediately after this offering ( common membership units if the underwriters exercise their overallotment option). |

|

Redemption rights |

RTEA and KMS have the right to require CPE LLC to acquire by redemption each common membership unit in CPE LLC owned by them in exchange for a cash payment equal to, on a per unit basis, the market price of one share of our common stock. If RTEA and KMS exercise their redemption right, we are entitled to assume CPE LLC's rights and obligations to acquire common membership units held by them and instead acquire such common membership units from them in exchange for, at our election, shares of our common stock on a one-for-one basis or a cash payment equal to, on a per unit basis, the market price of one share of our common stock or a combination of shares of our common stock and cash. We refer to this entitlement as our Assumption Right. If, immediately following this offering, RTEA and KMS exercised their right to require CPE LLC to acquire by redemption all of their common membership units in CPE LLC and we exercised our Assumption Right to acquire their membership units in exchange only for shares of our common stock, Rio Tinto America would indirectly own approximately % of all outstanding shares of our common stock (or approximately % if the underwriters exercised their over-allotment option in full). |

13

Use of proceeds |

We estimate that we will receive net proceeds of approximately $ million, assuming an estimated public offering price of $ per share (the midpoint of the range set forth on the cover page of this prospectus), after deducting underwriting discounts and commissions, all of which will be used to finance our acquisition of an interest in Rio Tinto America's western U.S. coal business (other than the Colowyo mine) represented by common membership units held by RTEA in CPE LLC. We will purchase a number of common membership units from RTEA equal to the number of shares of common stock sold in this offering at a price per unit equal to the public offering price per share, less underwriting discounts and commissions. We expect the net proceeds from CPE LLC's offering of senior notes to be $ million, after deducting estimated original issue discount, initial purchasers' discounts and commissions and offering expenses, approximately $ million of which CPE LLC will distribute to RTEA immediately following the completion of that offering. See "Use of Proceeds." |

|

Dividend policy |

We currently do not intend to pay dividends on our common stock. Upon completion of this offering, we will become a member and the sole manager of CPE LLC. We will be a holding company, will have no direct operations and will be able to pay dividends only from our available cash on hand and funds received from CPE LLC. See "Dividend Policy." |

|

Risk factors |

See "Risk Factors" on page 23 of this prospectus for a discussion of factors you should carefully consider before deciding to invest in our common stock. |

|

New York Stock Exchange symbol |

"CLD" |

Unless otherwise indicated, all information in this prospectus:

- •

- reflects the consummation of the structuring transactions described in "Structuring Transactions and Related Agreements";

- •

- gives effect to the debt financing transactions which CPE LLC will enter into concurrently with this offering; and

- •

- assumes an initial public offering of our shares of common stock at a price of $ per share, the midpoint of the estimated public offering price range set forth on the cover page of this prospectus.

A nominal amount of shares of our common stock are outstanding prior to the completion of this offering. The number of shares to be outstanding after completion of this offering is based on shares of our common stock to be sold in this offering and, except where we state otherwise, the common stock information we present in this prospectus:

- •

- excludes up to shares (assuming no exercise of the underwriters' overallotment option) of our common stock issuable upon, at our election, our assumption of CPE LLC's rights and obligations to acquire common membership units of CPE LLC from RTEA and KMS upon exercise of their redemption right, as described under "Structuring Transactions and Related Agreements—Structure-Related Agreements—CPE LLC Agreement;"

14

- •

- includes approximately shares of restricted common stock to be issued to our directors and

employees in

connection with this offering, which vest three years after the pricing of our initial public offering;

- •

- excludes options to be granted to our named executive officers

and other employees in connection

with this offering and shares of our common stock authorized but unissued under our long term incentive plan; and

- •

- assumes no exercise by the underwriters of their right to purchase a maximum of additional shares of common stock to cover over-allotments of shares.

In addition, unless otherwise indicated, the information regarding common membership units of CPE LLC presented in this prospectus excludes any common membership units that will be issued to us on a one-for-one basis upon the exercise of options to acquire our common stock.

15

SUMMARY ACTUAL AND UNAUDITED PRO FORMA CONSOLIDATED FINANCIAL DATA

The following table provides a summary of our actual and unaudited pro forma consolidated financial data for the periods indicated. This information should be read in conjunction with the sections of this prospectus entitled "Selected Consolidated Financial and Operating Data," "Management's Discussion and Analysis of Financial Condition and Results of Operations," and our historical consolidated and unaudited pro forma consolidated financial information and related notes thereto included elsewhere in this prospectus.

RTEA is considered to be our predecessor for accounting purposes and its consolidated financial statements are our historical consolidated financial statements. Our historical consolidated financial statements include, as discontinued operations, financial information for certain operations that will not be owned by Cloud Peak Energy after this offering, including the Colowyo mine, the Jacobs Ranch mine and the uranium mining venture. Our historical consolidated financial statements are not comparable to the unaudited pro forma condensed consolidated financial information included elsewhere in this prospectus or to the results investors should expect after the offering. To date, Cloud Peak Energy Inc. has had no operations. As described in "Structuring Transactions and Related Agreements—Holding Company Structure," following the completion of this offering we will be a holding company and our sole asset will be our managing member interest in CPE LLC. The consolidated financial statements of RTEA are provided elsewhere in this prospectus.

We have derived the actual consolidated financial data as of December 31, 2007 and 2008 and for each of the three years in the period ended December 31, 2008 from the audited consolidated financial statements of RTEA, included elsewhere in this prospectus. We have derived the actual consolidated balance sheet data as of December 31, 2006 from the audited consolidated financial statements of RTEA, not included in this prospectus. We have derived the actual consolidated financial data as of September 30, 2009 and for the nine months ended September 30, 2008 and 2009 from the unaudited consolidated financial statements of RTEA, included elsewhere in this prospectus. The unaudited consolidated financial information was prepared on a basis consistent with that used in preparing our audited consolidated financial statements and includes all adjustments, consisting of normal and recurring items, that we consider necessary for a fair presentation of the financial position and results of operations for the unaudited periods. The interim results of operations are not necessarily indicative of operations for a full fiscal year.

Prior to the consummation of the offering, our consolidated financial statements were prepared on a carve-out basis from our ultimate parent company, Rio Tinto and its subsidiaries. The carve-out consolidated financial statements include allocations of certain general and administrative costs and Rio Tinto's headquarters costs. We do not expect to continue to incur some of these charges as a stand-alone public company. These allocations were based upon various assumptions and estimates and actual results may differ from these allocations, assumptions and estimates. However, the carve-out consolidated financial statements do not reflect additional expenses we expect to incur as a stand-alone public company. Accordingly, the carve-out consolidated financial statements should not be relied upon as being representative of our financial position or operating results had we operated on a stand-alone basis, nor are they representative of our financial position or operating results following the offering.

We have derived the unaudited pro forma consolidated financial data as of September 30, 2009 and for the year ended December 31, 2008 and for the nine months ended September 30, 2009, from the unaudited pro forma condensed consolidated financial information, included elsewhere in this prospectus. See "Unaudited Pro Forma Condensed Consolidated Financial Information." The unaudited pro forma condensed consolidated financial information is based on our actual consolidated financial statements, included elsewhere in this prospectus. The unaudited pro forma adjustments are based on available information and certain assumptions that we believe are reasonable and are described below in the accompanying notes. The unaudited pro forma condensed consolidated balance

16

sheet as of September 30, 2009 and the unaudited pro forma condensed consolidated statements of operations for the year ended December 31, 2008 and for the nine months ended September 30, 2009 are presented on a pro forma basis to give effect, in each case, to the following adjustments as if they occurred on September 30, 2009 for balance sheet adjustments and January 1, 2008 for statement of operations adjustments:

- •

- the structuring transactions and related agreements, including the separation from Rio Tinto to be completed in connection

with this offering as described in "Structuring Transactions and Related Agreements";

- •

- the debt financing transactions which CPE LLC will enter into concurrently with this offering;

- •

- the issuance of approximately shares of restricted common stock

to be issued to our directors and

employees in connection with this offering, which vest three years after our initial public offering; and

- •

- the issuance of the shares of our common stock in this offering and subsequent use of proceeds.

The pro forma condensed consolidated statement of operations presents financial information through income (loss) from continuing operations. Accordingly, the income (loss) from discontinued operations related to the Colowyo mine, the Jacobs Ranch mine and the uranium mining venture are not reflected in continuing operations and no pro forma adjustment will be necessary in the pro forma condensed consolidated statement of operations.

The unaudited pro forma consolidated financial data is for informational purposes only, and is not intended to represent what our results of operations would be after giving effect to the offering, or to indicate our results of operations for any future period. Therefore, investors should not place undue reliance on the unaudited pro forma consolidated financial data.

17

Summary Unaudited Pro Forma Consolidated Financial Data

(dollars in thousands)

| |

For the Year Ended December 31, 2008(10) |

For the Nine Months Ended September 30, 2009(10) |

|||||||

|---|---|---|---|---|---|---|---|---|---|

| |

Pro Forma |

Pro Forma |

|||||||

Statement of Operations Data |

|||||||||

Revenues(1) |

$ | $ | |||||||

Costs and expenses |

|||||||||

Cost of product sold (exclusive of depreciation, depletion, amortization and accretion, shown separately) |

|||||||||

Depreciation and depletion |

|||||||||

Amortization(2) |

|||||||||

Accretion |

|||||||||

Exploration costs |

|||||||||

Selling, general and administrative expenses(3) |

|||||||||

Asset impairment charges(4) |

|||||||||

Total costs and expenses |

|||||||||

Total other expense |

|||||||||

Income from continuing operations before income tax provision and earnings from unconsolidated affiliates |

|||||||||

Income tax provision |

|||||||||

Earnings from unconsolidated affiliates, net of tax |

|||||||||

Income from continuing operations |

|||||||||

Income from continuing operations attributable to non controlling interest |

|||||||||

Income from continuing operations attributable to controlling interest |

$ | $ | |||||||

Income from continuing operations per share: |

|||||||||

Basic |

$ | $ | |||||||

Diluted |

$ | ||||||||

Weighted-average shares outstanding |

|||||||||

Basic |

|||||||||

Diluted |

|||||||||

| |

As of September 30, 2009 |

|||

|---|---|---|---|---|

| |

Pro Forma |

|||

Balance Sheet Data |

||||

Cash and cash equivalents |

$ | |||

Accounts receivable, net |

||||

Inventories, net |

||||

Property, plant and equipment, net |

||||

Intangible assets, net |

||||

Total assets |

||||

Total long-term debt(6) |

||||

Total liabilities |

||||

Shareholders' equity attributable to controlling interest |

||||

| |

For the Year Ended December 31, 2008 |

For the Nine Months Ended September 30, 2009 |

|||||

|---|---|---|---|---|---|---|---|

| |

Pro Forma |

Pro Forma |

|||||

Other Data |

|||||||

EBITDA(7) |

$ | $ | |||||

18

Summary Actual Consolidated Financial Data

(dollars in thousands)

| |

For the Years Ended December 31, | For the Nine Months Ended September 30, |

|||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2006 | 2007 | 2008 | 2008 | 2009 | ||||||||||||

Statement of Operations Data |

|||||||||||||||||

Revenues(1) |

$ | 942,841 | $ | 1,053,168 | $ | 1,239,711 | $ | 904,627 | $ | 1,061,286 | |||||||

Costs and expenses |

|||||||||||||||||

Cost of product sold (exclusive of depreciation, depletion, amortization and accretion, shown separately)(3) |

699,121 | 754,464 | 892,649 | 653,544 | 702,569 | ||||||||||||

Depreciation and depletion |

59,352 | 80,133 | 88,972 | 69,258 | 68,383 | ||||||||||||

Amortization(2) |

34,957 | 34,512 | 45,989 | 37,027 | 24,770 | ||||||||||||

Accretion |

10,088 | 12,212 | 12,742 | 8,926 | 8,402 | ||||||||||||

Exploration costs |

2,325 | 816 | 1,387 | 787 | 1,156 | ||||||||||||

Selling, general and administrative expenses(3) |

48,130 | 50,003 | 70,485 | 50,833 | 49,075 | ||||||||||||

Asset impairment charges(4) |

— | 18,297 | 2,551 | 1,014 | — | ||||||||||||

Total costs and expenses |

853,973 | 950,437 | 1,114,775 | 821,389 | 854,355 | ||||||||||||

Operating income |

88,868 | 102,731 | 124,936 | 83,238 | 206,931 | ||||||||||||

Other income (expense) |

|||||||||||||||||

Interest income |

3,604 | 7,302 | 2,865 | 2,682 | 228 | ||||||||||||

Interest expense |

(38,785 | ) | (40,930 | ) | (20,376 | ) | (19,974 | ) | (1,007 | ) | |||||||

Other, net |

2 | 274 | 1,715 | 1,631 | 15 | ||||||||||||

Total other expense |

(35,179 | ) | (33,354 | ) | (15,796 | ) | (15,661 | ) | (764 | ) | |||||||

Income from continuing operations before income tax provision and earnings (losses) from unconsolidated affiliates |

53,689 | 69,377 | 109,140 | 67,577 | 206,167 | ||||||||||||

Income tax provision |

(11,717 | ) | (18,050 | ) | (25,318 | ) | (15,676 | ) | (59,888 | ) | |||||||

(Losses) earnings from unconsolidated affiliates, net of tax |

(1,435 | ) | 2,462 | 4,518 | 3,109 | 989 | |||||||||||

Income from continuing operations |

40,537 | 53,789 | 88,340 | 55,010 | 147,268 | ||||||||||||

(Loss) income from discontinued operations, net of tax |

(2,599 | ) | (21,482 | ) | (25,215 | ) | (29,189 | ) | 42,790 | ||||||||

Net income |

$ | 37,938 | $ | 32,307 | $ | 63,125 | $ | 25,821 | $ | 190,058 | |||||||

Net income (loss) per share—basic and diluted: |

|||||||||||||||||

Income from continuing operations |

$ | 40,537 | $ | 53,789 | $ | 88,340 | $ | 55,010 | $ | 147,268 | |||||||

(Loss) income from discontinued operations |

(2,599 | ) | (21,482 | ) | (25,215 | ) | (29,189 | ) | 42,790 | ||||||||

Net income per share |

$ | 37,938 | $ | 32,307 | $ | 63,125 | $ | 25,821 | $ | 190,058 | |||||||

Weighted-average shares outstanding, basic and diluted |

1 | 1 | 1 | 1 | 1 | ||||||||||||

19

| |

As of December 31, | As of September 30, |

|||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2006 | 2007 | 2008 | 2009 | |||||||||

| |

(dollars in thousands) |

||||||||||||

Balance Sheet Data |

|||||||||||||

Cash and cash equivalents |

$ | 19,585 | $ | 23,616 | $ | 15,935 | $ | 18,319 | |||||

Accounts receivable, net |

74,541 | 92,060 | 79,451 | 81,390 | |||||||||

Inventories, net |

42,771 | 49,816 | 55,523 | 62,996 | |||||||||

Property, plant and equipment, net |

703,726 | 719,743 | 927,910 | 981,248 | |||||||||

Intangible assets, net |

117,031 | 82,518 | 31,916 | 7,146 | |||||||||

Assets of discontinued operations(5) |

694,066 | 721,835 | 587,168 | 582,304 | |||||||||

Total assets |

1,723,335 | 1,781,201 | 1,785,191 | 1,977,312 | |||||||||

Total long-term debt(6) |

665,735 | 571,559 | 209,526 | 175,604 | |||||||||

Liabilities of discontinued operations(5) |

269,987 | 270,049 | 127,220 | 139,359 | |||||||||

Total liabilities |

1,433,480 | 1,446,240 | 800,025 | 796,924 | |||||||||

Shareholder's equity(5)(11) |

289,855 | 334,961 | 985,166 | 1,180,388 | |||||||||

| |

For the Years Ended December 31, |

For the Nine Months Ended September 30, |

|||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2006 | 2007 | 2008 | 2008 | 2009 | ||||||||||||

| |

(dollars in thousands) |

||||||||||||||||

Other Data |

|||||||||||||||||

EBITDA(8) |

$ | 191,832 | $ | 232,324 | $ | 278,872 | $ | 203,189 | $ | 309,490 | |||||||

Tons of coal sold from production (millions) |

91.8 | 94.2 | 97.0 | 72.0 | 70.5 | ||||||||||||

Tons of coal purchased for resale (millions) |

8.1 | 8.1 | 8.1 | 6.0 | 7.2 | ||||||||||||

Tons of coal sold (millions)(9) |

99.9 | 102.3 | 105.1 | 78.0 | 77.7 | ||||||||||||

- (1)

- Freight

revenues accounted for 2.6%, 1.4% and 4.5% of our total revenues for the years ended December 31, 2006, 2007 and 2008, respectively, and 2.7%

and 6.9% of our total revenues for the nine months ended September 30, 2008 and 2009, respectively. As a general matter, our customers pay their own freight costs. We pay the freight costs,

however, for shipping coal to some of our customers and in these cases the customers pay us in respect of these freight costs and the payments are included in our revenues. See Note 3 of Notes

to Consolidated Financial Statements included elsewhere in this prospectus.

- (2)

- Primarily

reflects amortization under our brokerage contract related to the Spring Creek mine.

- (3)

- Allocations

of corporate, general and administrative expenses incurred by Rio Tinto America and other Rio Tinto affiliates were $18.3 million,

$24.4 million and $25.4 million for the years ended December 31, 2006, 2007 and 2008, respectively, and $17.6 million and $19.8 million for the nine months ended

September 30, 2008 and 2009, respectively. Of this total, $15.1 million, $20.2 million and $21.0 million, for the years ended December 31, 2006, 2007 and 2008,

respectively, and $14.5 million and $16.0 million for the nine months ended September 30, 2008 and 2009, respectively, is included in selling, general and administrative expenses

in the consolidated statements of operations. The remaining $3.2 million, $4.2 million and $4.4 million, for the years ended December 31, 2006, 2007 and 2008, respectively,

and $3.1 million and $3.8 million for the nine months ended September 30, 2008 and 2009, respectively, are included in cost of product sold. Also included in selling, general and

administrative expenses are costs incurred as a result of actions to divest RTEA, either through a trade sale or an initial public offering, of $25.8 million, $21.0 million, and

$11.3 million for the year ended December 31, 2008, and the nine months ended September 30, 2008 and 2009, respectively.

- (4)

- Asset impairment charges for the year ended December 31, 2007 reflects capitalized cost of an abandoned enterprise resource planning, or ERP, systems implementation. The ERP systems implementation was a worldwide Rio Tinto initiative designed to align processes, procedures, practices and reporting across all Rio Tinto business units. The implementation would have taken our stand-alone ERP system and moved it to a shared Rio Tinto platform, which could not be transferred to a new stand-alone company. We do not currently use, and will not use following this offering, this ERP system. Asset impairment charges for the year ended December 31, 2008 included a $4.6 million charge to write-off certain contract rights, a $1.0 million

20

charge for an abandoned cost efficiency project, and a $3.0 million favorable adjustment to the ERP system costs that were included in the 2007 asset impairment charge.

- (5)

- Certain

operations will not be owned by Cloud Peak Energy following the completion of this offering, including the Colowyo coal mine, the Jacobs Ranch coal

mine and the uranium mining venture. Accordingly, the consolidated financial statements report the financial position, results of operations and cash flows of the Colowyo mine, the Jacobs Ranch mine

and the uranium mining venture as discontinued operations. Amounts presented as discontinued operations as of December 31, 2008 and September 30, 2009 and for the nine months ended

September 30, 2009 reflect the Jacobs Ranch mine only as the Colowyo mine and uranium mining venture were distributed to Rio Tinto America on October 7, 2008. See Note 4 of Notes

to Consolidated Financial Statements included elsewhere in this prospectus.

- (6)

- Total

long-term debt includes the current and long-term portions of the long-term debt—related party,

federal coal leases and long-term debt—other. See Note 9 of Notes to Consolidated Financial Statements included elsewhere in this prospectus for additional information

on our long-term debt.

- (7)

- Pro forma EBITDA is derived from the unaudited pro forma condensed consolidated statement of operations for the year ended December 31, 2008 and nine months ended September 30, 2009, included elsewhere in this prospectus. A reconciliation of pro forma EBITDA to pro forma net income for the periods presented, is as follows:

| |

For the Year Ended December 31, 2008 |

For the Nine Months Ended September 30, 2009 |

|||||

|---|---|---|---|---|---|---|---|

| |

(dollars in thousands) |

||||||

Pro forma |

|||||||

Pro forma income from continuing operations |

$ | $ | |||||

Pro forma depreciation and depletion |

|||||||

Pro forma accretion |

|||||||

Pro forma amortization |

|||||||

Pro forma interest expense |

|||||||

Pro forma interest income |

|||||||

Pro forma income tax provision |

|||||||

Pro forma EBITDA |

$ | $ | |||||

See Note 8 below for a discussion of our use of EBITDA.

- (8)

- EBITDA,

a performance measure used by management, is defined as income (loss) from continuing operations plus: interest expense (net of interest income),

income tax provision, depreciation and depletion, amortization and accretion as shown in the table below. EBITDA, as presented for the years ended December 31, 2006, 2007 and 2008 and for the

nine months ended September 30, 2008 and 2009, is not defined under accounting principles generally accepted in the United States of America, or U.S. GAAP, and does not purport to be an

alternative to net income as a measure of operating performance. Because not all companies use identical calculations, this presentation of EBITDA may not be comparable to other similarly titled

measures of other companies. We use, and we believe investors benefit from the presentation of, EBITDA in evaluating our operating performance because it provides us and our investors with an

additional tool to compare our operating performance on a consistent basis by removing the impact of certain items that management believes do not directly reflect our core operations. We believe that

EBITDA is useful to investors and other external users of our consolidated financial statements in evaluating our operating performance because EBITDA is widely used by investors to measure a

company's operating performance without regard to items such as interest expense, taxes, depreciation and depletion, amortization and accretion, which can vary substantially from company to company

depending upon accounting methods and book value of assets and liabilities, capital structure and the method by which assets were acquired.

However, using EBITDA as a performance measure has material limitations as compared to net income, or other financial measures as defined under U.S. GAAP, as it excludes certain recurring items which may be meaningful to investors. EBITDA excludes interest expense or interest income; however, as we have

21