Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - PPL Corp | form8k.htm |

| EX-99.1 - EXHIBIT 99.1 - PPL Corp | form8k-exhibit99_1.htm |

EEI

Financial Conference

Hollywood,

Florida

November

1-4, 2009

Exhibit

99.2

1

Cautionary

Statements and Factors That

May Affect Future Results

May Affect Future Results

Any

statements made in this presentation

about future operating results or other future

events are forward-looking statements under

the Safe Harbor Provisions of the Private

Securities Litigation Reform Act of 1995.

Actual results may differ materially from such

forward-looking statements. A discussion of

factors that could cause actual results or

events to vary is contained in the Appendix to

this presentation and in the Company’s SEC

filings.

about future operating results or other future

events are forward-looking statements under

the Safe Harbor Provisions of the Private

Securities Litigation Reform Act of 1995.

Actual results may differ materially from such

forward-looking statements. A discussion of

factors that could cause actual results or

events to vary is contained in the Appendix to

this presentation and in the Company’s SEC

filings.

2

Investment

Highlights

• Significant

increase in financial performance

– Earnings expected

to increase substantially in 2010 driven by transition to market based

electricity prices after approximately 10 years of fixed generation rates

electricity prices after approximately 10 years of fixed generation rates

– Dividends continue

to be viewed as an important component of shareowner return

– Investment grade

credit ratings are a key competitive asset

• Highly attractive

baseload oriented generation fleet

– Competitively

positioned nuclear, hydro and efficient coal

– Attractive nuclear

and hydro uprate/expansion projects equating to 208 additional MWs

– Potential benefit

from carbon regulation

– Underlying value

strongly and positively correlated to a recovery in natural gas

prices

• Disciplined

multiyear hedging program has created significant value

– 99% for 2009, 99%

for 2010, 89% for 2011 and 58% for 2012 of expected baseload

volumes

– Protects against

further weakness in energy prices and allows for upside participation if

near-

term recovery occurs

term recovery occurs

• Focused on growth

in rate regulated businesses

– Achieved formula

rate mechanism for Transmission tariffs at a ROE of 11.64%

– Highly attractive

Susquehanna-Roseland RTEP project; PPL EU’s portion is expected to cost

about $500 million at an approved 12.89% ROE

about $500 million at an approved 12.89% ROE

– Significant

Distribution Capex to support performance of existing network

– WPD DPCR5: Initial

OFGEM proposal constructive; final proposal in November

PPL’s

Generation Portfolio

3

Morony

Ryan

Cochrane

Rainbow

Black

Eagle

Kerr

Thompson

Falls

Holter

Hauser

Madison

Mystic

Lake

Corette

Colstrip

Montour

Keystone

Conemaugh

Lake

Wallenpaupack

Wallenpaupack

Susquehanna

Martins

Creek

Lower

Mount Bethel

Ironwood

Brunner

Island

Island

Safe

Harbor

Holtwood

Hydro

Coal

Nuclear

Gas/Oil

Coal

Nuclear

Gas/Oil

Key

Montana

Generating

capacity - 1,287 MW

Madison

Morony

Mystic Lake

Rainbow

Ryan

Thompson Falls

Morony

Mystic Lake

Rainbow

Ryan

Thompson Falls

Other

generating stations

(1) PPL has signed

agreements to sell Shoreham, Edgewood and

the PPL

Maine hydro assets.

PPL’s

Generation

Portfolio 3 MoronyRyanCochrane Rainbow Black

Eagle Kerr Thompson

Falls Holter Hauser Madison Mystic

Lake

Corette Colstrip Montour Keystone Conemaugh Lake Wallenpaupack Susquehanna Martins

Creek Lower Mount

Bethel Ironwood Brunner Island Safe

Harbor Holtwood HydroCoal Nuclear Gas/Oil Key Montana Generating

capacity – 1,287 MW Black

EagleCochrane ColstripCorette Hauser Holter Kerr Madison MoronyMystic

LakeRainbow RyanThompson Falls Other generating

stations University Park, IL – 540 MW Wallingford, CT –

225 MW Shoreham and Edgewood, Long Island, NY – 159 MW

(1) Nine Hydroelectric Facilities, ME – 39 MW

(1) Wyman, ME – 51 MW PennsylvaniaGenerating capacity –

10,894 MW Brunner Island Holtwood Lake

WallenpaupackLower Mount Bethel Martins

Creek Montour SusquehannaConemaughKeystoneSafe

Harbor Ironwood (1) PPL has signed agreements to sell Shoreham,

Edgewood and the PPL Maine hydro assets.

4

Note:

As of 9/30/2009

…provides

higher level of earnings and cash flow predictability

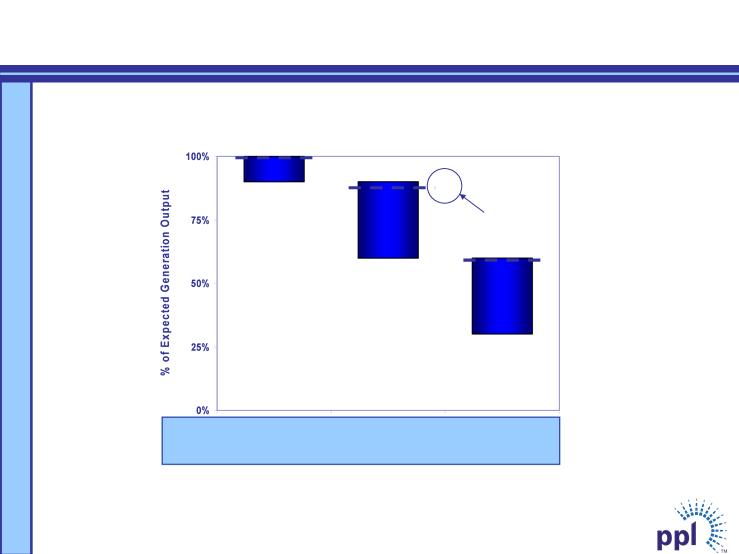

2010 2011 2012

99%

Band

1

Band

2

89%

Band

3

58%

{

Target

Range

Range

Actual

Hedge

Level

Hedge

Level

Hedges

Swaps/Options 96% 89% 58%

Load-following 3% 0% 0%

Multi-year Hedging

Program…

Note: As of

9/30/2009

2009 2010 2011 2012

Uranium 100% 100% 100% 100%

Coal

East 100%

97%

83%

60%

West 100% 100% 100%

90%

Total 100% 98% 88% 68%

$35

$40

$45

$50

$55

Balance

of 2009

2010

2011

max

collar price

fixed

base price

min

collar price

Weighted

Average

$/Ton

at

Mine (1)

7%

11%

%

Diesel Surcharge

78%

5%

0%

%

Collars

88%

89%

%

Fixed Base Price (2)

22%

0%

5

(1) Base prices for

East wholly owned plants, which include Montour & Brunner Island but not

Keystone & Conemaugh.

(2) Excludes contracts

subject to mining-related oil surcharges and/or price

collars.

Current Fuel Hedge

Positions

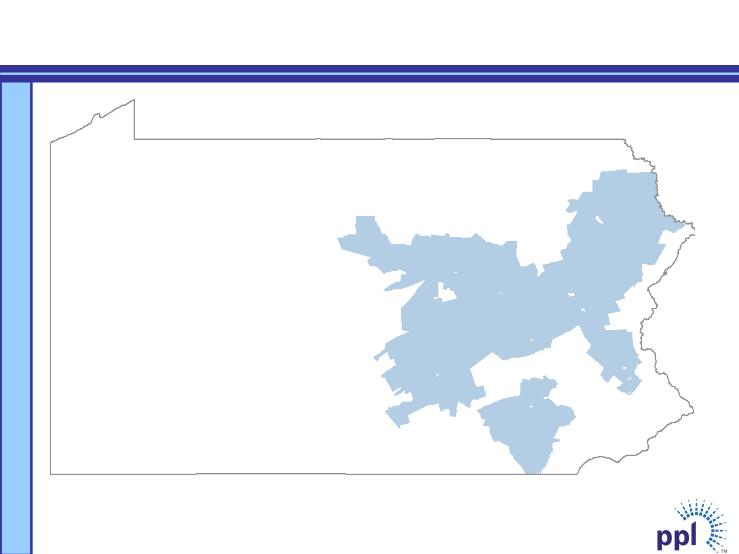

PPL

Electric Utilities

• Transmission and

Distribution business

with 1.4 million customers in Pennsylvania

with 1.4 million customers in Pennsylvania

• Attractive rate

base investment

opportunities to support infrastructure and

reliability

opportunities to support infrastructure and

reliability

• Superior customer

service

• Constructive

regulatory relationships

6

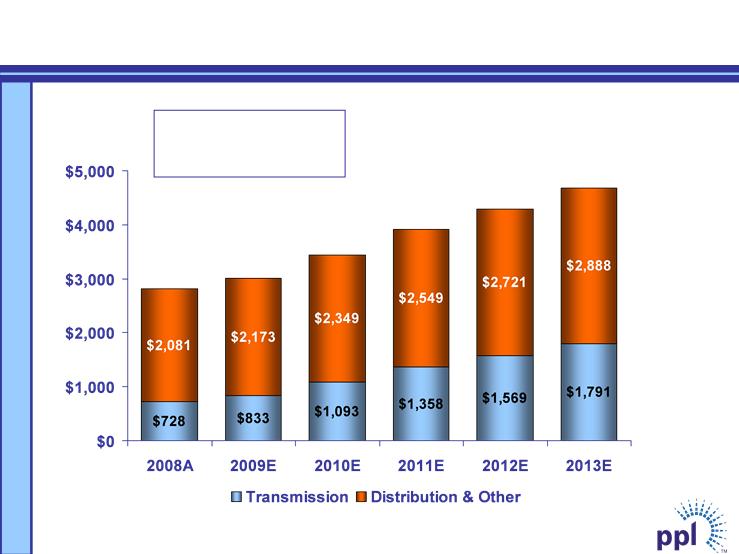

Millions

$3,006

$3,442

$3,907

$4,290

$4,679

$2,809

7

CAGR

Distribution

= 6.8%

Transmission

= 19.7%

PPL

Electric Utilities Rate Base

Attractive

Transmission Development Project 8 • PPL Electric to

build Pennsylvania portion of the 150-mile Susquehanna to Roseland,

NJ 500 kV transmission line. New Jersey portion of the

line to be built by PSEG. • Project needed for reliability

and is part of PJM’s Regional Transmission Expansion

Plan (RTEP) • PJM-directed completion date June

2012 • Cost of PPL’s portion of the line is estimated

at $500 million • Formula rate mechanism for

transmission – Settlement agreement approved by FERC for

11.64% ROE* including RTO adder • PPL rate structure for RTEP

project – 12.89% ROE* – CWIP in rate base –

Recovery of costs if terminated *ROE increases to 11.68% including

RTO adder and to 12.93% for RTEP projects in June 2010

Western

Power Distribution

• Electricity

Distribution company

that delivers electricity to 2.6

million end users in the United

Kingdom

that delivers electricity to 2.6

million end users in the United

Kingdom

• No commodity

exposure

• Highly attractive

regulatory

construct

construct

• Final proposal for

DCPR5

expected in November

expected in November

9

Forecast

10

|

* Earnings

from ongoing operations - See Appendix for the per share reconciliation of

reported earnings and earnings from ongoing operations.

|

|

|

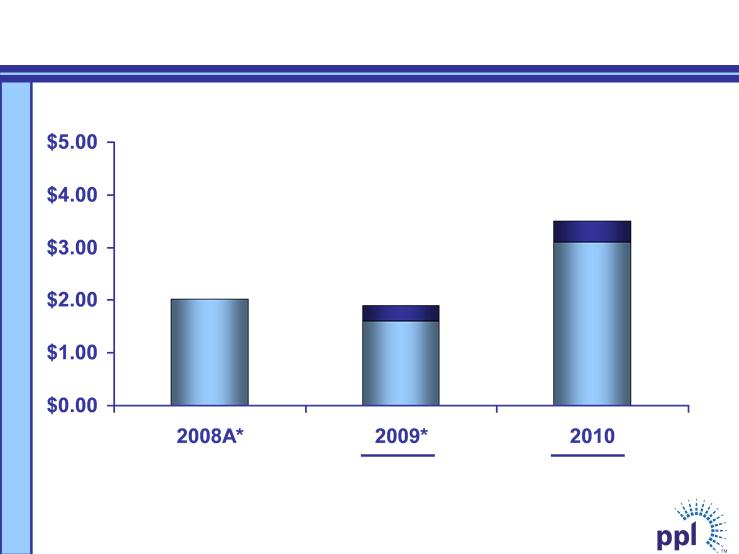

$2.02

$3.50

Per

Share

$1.90

$1.60

$3.10

Strong Expected

Earnings Growth

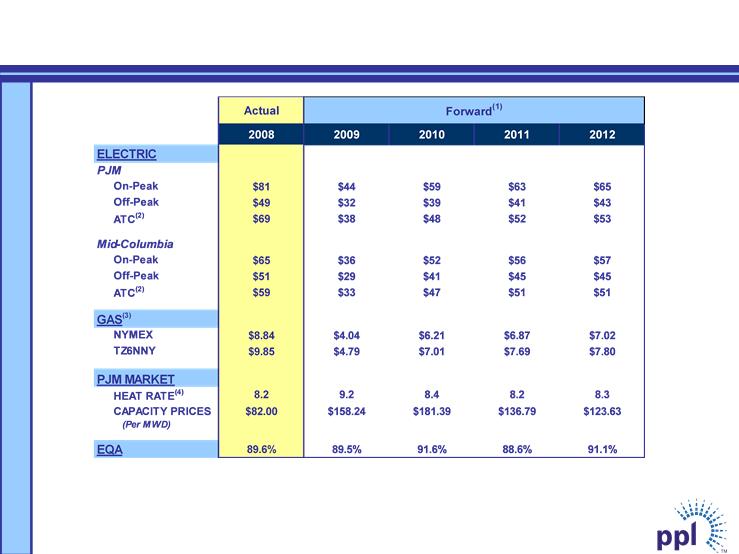

(1) Market prices based

on the average of broker quotes as of 9/30/2009

(2) 24-hour

average

(3) NYMEX and TZ6NNY

forward gas prices on 9/30/2009

(4) Market Heat Rate =

PJM on-peak power price divided by TZ6NNY gas price

A-1

Market

Prices

Market

Prices (1) Market prices based on the average of broker quotes

as of 9/30/2009 (2) 24-hour average (3) NYMEX and TZ6NNY

forward gas prices on 9/30/2009 (4) Market Heat Rate = PJM on-peak

power price divided by TZ6NNY gas price Actual 2008 2009

2010 2011 2012 $81 $44 $59 $63 $65 $49 $32 $39 $41

$43 $69 $38 $48 $52 $53 $65 $36 $52 $56 $57 $51

$29 $41 $45 $45 $59 $33 $47 $51 $51 $8.84 $4.04 $6.21

$6.87 $7.02 $9.85 $4.79 $7.01 $7.69 $7.80 8.2 9.2 8.4 8.2

8.3 $82.00 $158.24 $181.39 $136.79 $123.63 89.6% 89.5%

91.6% 88.6% 91.1% (Per MWD) EQA HEAT

RATE(4) TZ6NNY PJM

MARKET ATC(2) NYMEX GAS(3) CAPACITY

PRICES Mid-Columbia Forward(1) On-Peak Off-Peak ATC(2) ELECTRIC PJM On-Peak Off-Peak A-1

Market

Segment

Baseload

63%

Peaking

18%

Intermediate

19%

Installed

Capacity

MW

Coal

34%

Gas/Oil

38%

Nuclear

18%

Hydro

8%

QFs

2%

Diverse and

Balanced Fleet

Geography

Production

GWh

PJM

85%

WECC

11%

Coal

49%

Gas/Oil

10%

10%

Nuclear

32%

Hydro

9%

NEPOOL

3%

NYISO

1%

Baseload

oriented fleet augmented by attractive load-following capabilities

A-2

Note: As of

September 30, 2009

PPL

has proactively complied with current environmental regulations on an economic

basis

(1)

Colstrip is located in Montana

(2)

Keystone & Conemaugh: PPL is a minority owner and does not

operate

A-3

Environmental

Control Equipment

Environmental

Control Equipment Keystone(2) Conemaugh(2) Control

Device Removes Unit 1 Unit 2 Unit 3 Unit 1 Unit 2 Unit 3 & 4 Unit 3 & 4

Unit 1 & 2 Unit 1 & 2 Low Nox Burners NOx SCR

NOx Scrubbers SO2 Brunner Island Montour

Colstrip(1) = Installed = Potential = Under

Construction PPL has proactively complied with current environmental

regulations on an economic basis (1) Colstrip is located in

Montana (2) Keystone & Conemaugh: PPL is a minority owner and

does not operate A-3

A-4

Supply

Segment Asset Hedge Positions

2009 2010

Expected Gross Margin $35 Mil $35 Mil

Expected Gross Margin $35 Mil $35 Mil

Geographic

Diversity

2009 2010

NEPOOL

24%

MISO

2%

PJM

74%

PJM

71%

NEPOOL

27%

MISO

2%

A-5

Supply Segment

Marketing and Trading Overview

A-6

Pennsylvania

Electricity Distribution Rate Regulation

• Retail

distribution of electricity and natural gas are regulated by the

Pennsylvania Public Utility Commission

Pennsylvania Public Utility Commission

– Pennsylvania

deregulated the generation of electricity in 1997

– Transmission and

wholesale sales of electricity are regulated by the Federal

Energy Regulatory Commission

Energy Regulatory Commission

• Retail

distribution rates are set by a combination of base rate

proceedings and automatic adjustment clauses

proceedings and automatic adjustment clauses

• Base rate

proceedings

– Initiated by a

utility filing or, rarely, through a Commission investigation

– Based upon the

traditional cost of service, rate of return model

– The utility must

have the opportunity to earn a "fair rate of return“ on used and

useful rate base

useful rate base

– The utility must

file historic data; may file future data

– The Commission

must enter an order within nine months of the utility's filing or the

proposed rates go into effect subject to refund

proposed rates go into effect subject to refund

• Automatic

adjustment clauses

– Specifically

authorized in the Public Utility Code

– Limited by court

decision to expense items, not capital costs

– Usually based on a

forecast of costs with an annual reconciliation to actual costs

– Have been used to

recover the costs of: energy, stranded investment,

transmission and universal service

transmission and universal service

PPL

Electric Utilities 2011 to mid-2013

Procurement Plan

Procurement Plan

A-7

• Residential load

to be supplied under 12- and 24-month

load-following contracts, 5- and 10-year fixed block

products, and spot purchases

load-following contracts, 5- and 10-year fixed block

products, and spot purchases

• Small commercial

and industrial to be supplied under 12-

and 24-month load-following contracts, and spot

purchases

and 24-month load-following contracts, and spot

purchases

• Large commercial

and industrial load to be supplied

under hourly pricing products and an optional fixed-price

product

under hourly pricing products and an optional fixed-price

product

A-8

August 11,

2009 July

19, 2011

October 20,

2009

October 18, 2011

January 19,

2010

January 9, 2012

April

20, 2010 April

3, 2012

July

20, 2010 July

17, 2012

October 19,

2010

October 16, 2012

April

18, 2011

January 22, 2013

P

P

P

Completed

PPL

Electric Utilities 2011 to mid-2013

Procurement Plan Schedule

Procurement Plan Schedule

• Due dates for

bids:

A-9

UK

Electricity Distribution Regulation

• Electricity and

natural gas supply and distribution are regulated by the UK’s Office of

Gas and Electricity Markets (OFGEM)

Gas and Electricity Markets (OFGEM)

• Electricity

distribution revenues are set every five years through a Distribution

Price

Control Review (DPCR) process

Control Review (DPCR) process

– Price control is

based on a forward looking assessment of income sufficient to finance

an

efficient business

efficient business

– Revenues must

cover operating and capital costs at an efficient level for the service

territory

• Efficiency is

determined through a detailed comparative analysis of all UK

electricity

distribution companies

distribution companies

– Typically, the

DPCR results in a one-time price reduction followed by annual adjustments

for

inflation less an efficiency factor

inflation less an efficiency factor

• An incentive /

penalty arrangement exists for reliability and customer service

levels

• The revenue that a

company can earn in each of the five years is the sum of:

– The Regulator’s

view of efficient operating costs,

– A return on the

value of Regulated Asset Base (“RAB”), and

– A return of

capital being the depreciation of the RAB

• The DPCR is

currently in process with the next five-year period beginning April 1,

2010

2010

A-10

$1,503

$1,299

$1,888

$2,185

$1,933

$1,845

Capital

Expenditures by Segment

Millions

A-11

Note: See

Appendix for reconciliation of cash from operations to free cash flow before

dividends

Free

Cash Flow before Dividends Forecast

(1) Reported as of

9/30/2009

A-12

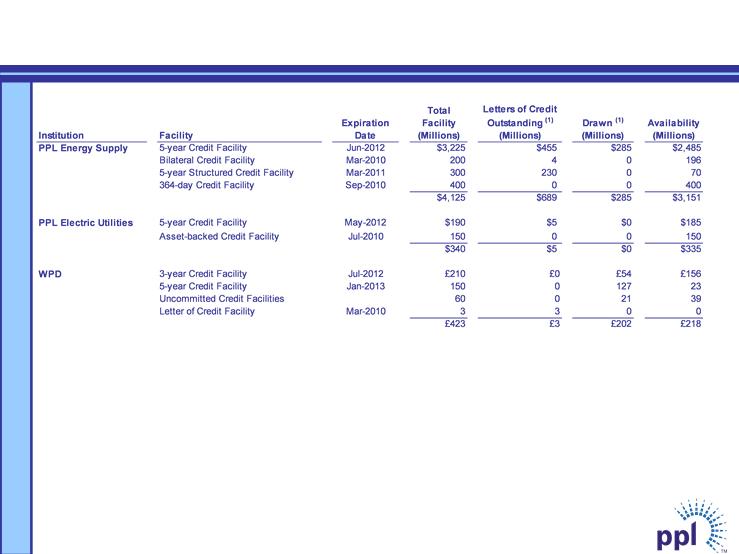

Domestic

facilities consist of a diverse bank group, with no bank and its

affiliates providing an aggregate commitment of more than 15% of the total

committed capacity.

affiliates providing an aggregate commitment of more than 15% of the total

committed capacity.

Liquidity

Profile

Liquidity Profile (1)

Reported as of 9/30/2009 A-12 Institution Facility Expiration

Date Total Facility (Millions) Letters of Credit

Outstanding (1) (Millions) Drawn (1) (Millions)

Availability (Millions) PPL Energy Supply 5-year Credit

Facility Jun-2012 $3,225 $455 $285 $2,485 Bilateral Credit Facility

Mar-2010 200 4 0 196 5-year Structured Credit Facility Mar-2011 300 230 0

70 364-day Credit Facility Sep-2010 400 0 0 400 $4,125 $689 $285

$3,151 PPL Electric Utilities 5-year Credit Facility May-2012 $190 $5 $0

$185 Asset-backed Credit Facility Jul-2010 150 0 0 150 $340 $5 $0

$335 WPD 3-year Credit Facility Jul-2012 £210 £0 £54 £156 5-year

Credit Facility Jan-2013 150 0 127 23 Uncommitted Credit Facilities 60 0

21 39 Letter of Credit Facility Mar-2010 3 3 0 0 £423 £3 £202 £218

Domestic facilities consist of a diverse bank group, with no bank and its

affiliates providing an aggregate commitment of more than 15% of the total

committed capacity.

A-13

PPL

Energy Supply Collateral Profile

Note: As of

9/30/2009

A-14

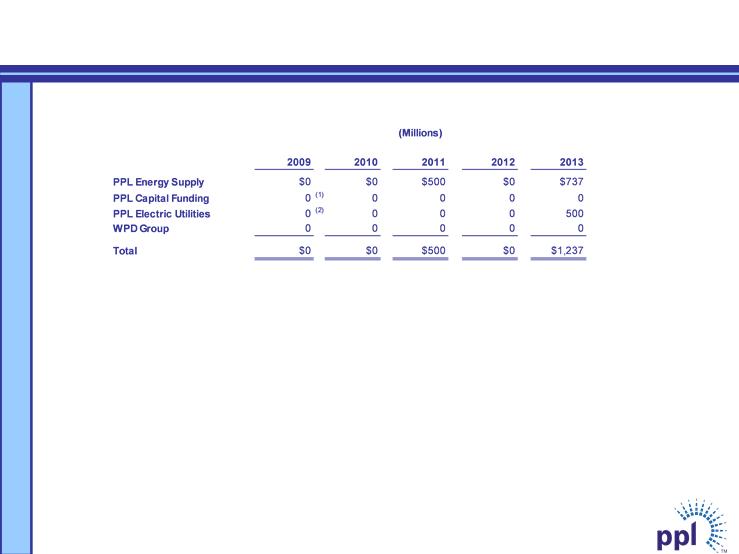

(1) PPL Capital Funding

$201 million maturity paid off in March 2009

(2) PPL Electric

Utilities $486 million maturity paid off in August 2009

Debt

Maturities

Debt

Maturities Note: As of 9/30/2009 A-14 2009 2010 2011

2012 2013 PPL Energy Supply $0 $0 $500 $0 $737 PPL

Capital Funding 0 (1) 0 0 0 0 PPL Electric Utilities 0 (2) 0 0 0 500

WPD Group 0 0 0 0 0 Total $0 $0 $500 $0 $1,237

(Millions) (1) PPL Capital Funding $201 million maturity paid off in

March 2009 (2) PPL Electric Utilities $486 million maturity paid

off in August 2009

(Millions)

A-15

|

|

2008

|

2009

|

2010

|

|

Cash from

Operations

|

$

595

|

$741

|

$1,437

|

|

Increase/(Decrease)

in cash due to:

|

|

|

|

|

Capital

Expenditures

|

(939)

|

(753)

|

(892)

|

|

Investment

in Energy Project

|

(203)

|

|

|

|

Asset

Sales

|

|

216

|

39

|

|

Other

Investing Activities-net

|

(58)

|

(15)

|

(61)

|

|

Free Cash

Flow before Dividends

|

($605)

|

$189

|

$523

|

|

|

|

|

|

Actual Projected

Note: Asset

Sales in 2009 include the anticipated proceeds from the announced pending sale

of most of the Maine generating assets

and all of the Long Island generating assets. Closing of the sale of the Maine assets is expected on or about November 1,

2009. Closing on the sale of the Long Island assets is expected later in 2009 or in the first quarter of 2010. Asset sales in

2010 include the anticipated proceeds from the announced pending sale of the remaining Maine generating assets.

and all of the Long Island generating assets. Closing of the sale of the Maine assets is expected on or about November 1,

2009. Closing on the sale of the Long Island assets is expected later in 2009 or in the first quarter of 2010. Asset sales in

2010 include the anticipated proceeds from the announced pending sale of the remaining Maine generating assets.

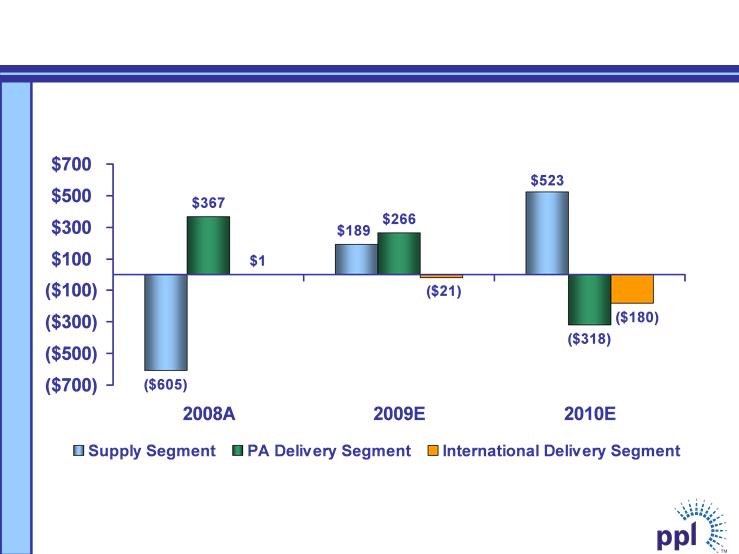

Supply Segment

Reconciliation of Cash from Operations

to Free Cash Flow before Dividends

to Free Cash Flow before Dividends

(Millions)

A-16

|

|

2008

|

2009

|

2010

|

|

Cash from

Operations

|

$

643

|

$561

|

$250

|

|

Less

Transition Bond Repayment

Increase/(Decrease)

in cash due to:

|

(293)

|

|

|

|

Capital

Expenditures

|

(286)

|

(295)

|

(568)

|

|

Asset

Sales & Other

|

303

|

|

|

|

Free Cash

Flow before Dividends

|

$367

|

$266

|

($318)

|

|

|

|

|

|

Note: Asset

Sales in 2008 includes the net proceeds from the sale of gas and propane

businesses

Actual Projected

PA

Delivery Segment Reconciliation of Cash from

Operations to Free Cash Flow before Dividends

Operations to Free Cash Flow before Dividends

(Millions)

A-17

|

|

2008

|

2009

|

2010

|

|

Cash from

Operations

|

$

279

|

$230

|

$248

|

|

Increase/(Decrease)

in cash due to:

|

|

|

|

|

Capital

Expenditures

|

(278)

|

(251)

|

(428)

|

|

Free Cash

Flow before Dividends

|

$ 1

|

($ 21)

|

($180)

|

|

|

|

|

|

Actual Projected

International

Delivery Segment Reconciliation of Cash

from Operations to Free Cash Flow before Dividends

from Operations to Free Cash Flow before Dividends

A-18

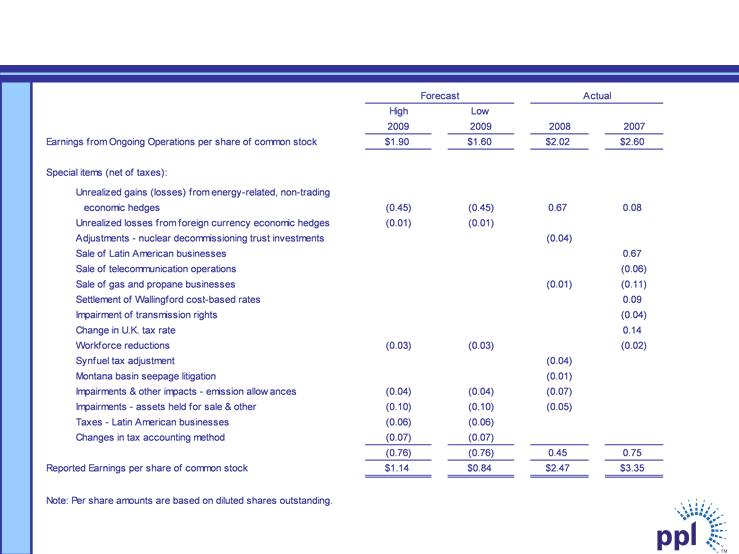

Reconciliation of

PPL’s Reported Earnings and

Earnings from Ongoing Operations

Earnings from Ongoing Operations

Reconciliation of PPL’s Reported Earnings and Earnings

from Ongoing Operations Forecast Actual High Low

2009 2009 2008 2007 Earnings from Ongoing Operations per share

of common stock $1.90 $1.60 $2.02 $2.60 Special items (net of

taxes): Unrealized gains (losses) from energy-related, non-trading

economic hedges (0.45) (0.45) 0.67 0.08 Unrealized losses from

foreign currency economic hedges (0.01) (0.01) Adjustments -nuclear

decommissioning trust investments (0.04) Sale of Latin American businesses

0.67 Sale of telecommunication operations (0.06) Sale of gas and

propane businesses (0.01) (0.11) Settlement of Wallingford cost-based

rates 0.09 Impairment of transmission rights (0.04) Change in U.K.

tax rate 0.14 Workforce reductions (0.03) (0.03) (0.02) Synfuel tax

adjustment (0.04) Montana basin seepage litigation (0.01)

Impairments & other impacts - emission allow ances (0.04) (0.04)

(0.07) Impairments - assets held for sale & other (0.10) (0.10) (0.05)

Taxes - Latin American businesses (0.06) (0.06) Changes in tax

accounting method (0.07) (0.07) (0.76) (0.76) 0.45 0.75

Reported Earnings per share of common stock $1.14 $0.84 $2.47 $3.35

Note: Per share amounts are based on diluted shares outstanding.

Credit

Ratings

A-19

|

|

Moody’s

|

Standard

& Poor’s

|

Fitch

|

|

PPL

Corporation

|

|

|

|

|

Issuer

Rating

|

Baa2

|

BBB

|

BBB

|

|

Outlook

|

NEGATIVE

|

NEGATIVE

|

STABLE

|

|

|

|

|

|

|

PPL

Energy Supply

|

|

|

|

|

Issuer

Rating

|

|

BBB

|

BBB

|

|

Tax-Exempt

Bonds*

|

Aaa

|

AAA

|

|

|

Senior

Notes

|

Baa2

|

BBB

|

BBB+

|

|

Outlook

|

STABLE

|

NEGATIVE

|

STABLE

|

|

|

|

|

|

|

PPL

Capital Funding

|

|

|

|

|

Issuer

Rating

|

|

|

BBB

|

|

Senior

Unsecured Debt

|

Baa2

|

BBB-

|

BBB

|

|

Subordinated

Debt

|

Baa3

|

BB+

|

BBB-

|

|

Outlook

|

NEGATIVE

|

|

STABLE

|

|

|

|

|

|

|

PPL

Electric Utilities

|

|

|

|

|

Issuer

Rating

|

Baa1

|

A-

|

BBB

|

|

First

Mortgage Bonds

|

A3

|

A-

|

A-

|

|

Tax-Exempt

Bonds**

|

A3/Baa1

|

A/A-

|

|

|

Senior

Secured Debt

|

A3

|

A-

|

A-

|

|

Commercial

Paper

|

P-2

|

A-2

|

F-2

|

|

Preferred

Stock

|

Baa3

|

BBB

|

BBB

|

|

Preference

Stock

|

Baa3

|

BBB

|

BBB

|

|

Outlook

|

NEGATIVE

|

NEGATIVE

|

STABLE

|

* Letter

of Credit-Backed Security

** Includes

both Insured and Non-Insured Securities

Credit Ratings

(cont.)

A-20

Commercial

Paper

A-

BBB+

Baa1

Senior

Unsecured Debt

F2

A-2

P-2

Commercial

Paper

POSITIVE

NEGATIVE

STABLE

Outlook

BBB+

BBB+

Baa1

Issuer

Rating

A-

BBB+

Baa1

Senior

Unsecured Debt

F2

A-2

Commercial

Paper

POSITIVE

NEGATIVE

STABLE

Outlook

Western

Power Distribution (South West) PLC

BBB+

BBB+

Issuer

Rating

Western

Power Distribution (South Wales) PLC

POSITIVE

NEGATIVE

STABLE

Outlook

POSITIVE

Outlook

BBB

Issuer

Rating

WPD

Holdings LLP

BBB-

BBB-

Baa3

Issuer

Rating

BBB

BBB-

Baa3

Senior

Unsecured Debt

A-3

Commercial

Paper

WPD

Holdings Limited

BBB

BBB-

Baa3

Pass-Through

Certificates

STABLE

STABLE

Outlook

PPL

Montana

Fitch

Standard

& Poor’s

Moody’s

A-21

PPL

Corporation

(NYSE:

PPL) is a Fortune 500 company with headquarters in Allentown, Pa. The

Company’s diversified

corporate strategy is to achieve growth in energy supply margins while limiting volatility in both cash flows and earnings and to

achieve stable, long-term growth in regulated delivery businesses through efficient operations and strong customer and

regulatory relations. The strategy is carried out through four principal subsidiaries:

corporate strategy is to achieve growth in energy supply margins while limiting volatility in both cash flows and earnings and to

achieve stable, long-term growth in regulated delivery businesses through efficient operations and strong customer and

regulatory relations. The strategy is carried out through four principal subsidiaries:

PPL

EnergyPlus, which markets

energy in key U. S. markets.

PPL

Generation, which operates

more than 12,000 megawatts of electricity generating capacity in Pennsylvania,

Montana,

Maine, Illinois, New York and Connecticut, with an additional 208 megawatts of planned uprate projects.

Maine, Illinois, New York and Connecticut, with an additional 208 megawatts of planned uprate projects.

PPL

Electric Utilities, which delivers

electricity to 1.4 million customers in Pennsylvania.

PPL

Global, which delivers

electricity to 2.6 million customers in the United Kingdom.

Security

Ratings

Moody’s S&P Fitch

PPL

Corp.

Corporate

Credit Rating Baa2 BBB BBB

PPL

Capital Funding, Inc.

Senior

Unsecured Debt Baa2 BBB- BBB

PPL

Electric Utilities Corp.

First

Mortgage Bonds A3 A- A-

Senior

Secured Bonds A3 A- A-

PPL

Energy Supply

Senior

Unsecured Notes Baa2 BBB BBB+

WPD

Holdings Limited

Senior

Unsecured Debt Baa3 BBB- BBB

WPD

Operating Cos.

Senior

Unsecured Debt Baa1 BBB+ A-

Contacts

Joseph

P. Bergstein, Jr.

Manager-Investor

Relations

Phone: (610)

774-5609

Fax: (610)

774-5106

jpbergstein@pplweb.com

www.pplweb.com

PPL

Facts

A-22

Statements

contained in this presentation, including statements with respect to future

earnings, energy prices,

margins and sales, growth, revenues, expenses, cash flow, asset disposition, marketing performance, hedging,

regulation, corporate strategy and generating capacity and performance, are “forward-looking statements” within

the meaning of the federal securities laws. Although PPL Corporation believes that the expectations and

assumptions reflected in these forward-looking statements are reasonable, these statements are subject to a

number of risks and uncertainties, and actual results may differ materially from the results discussed in the

statements. The following are among the important factors that could cause actual results to differ materially from

the forward-looking statements: market demand and prices for energy, capacity and fuel; weather conditions

affecting customer energy usage and operating costs; competition in power markets; the effect of any business

or industry restructuring; the profitability and liquidity of PPL Corporation and its subsidiaries; new accounting

requirements or new interpretations or applications of existing requirements; operating performance of plants and

other facilities; environmental conditions and requirements and the related costs of compliance, including

environmental capital expenditures and emission allowance and other expenses; system conditions and

operating costs; development of new projects, markets and technologies; performance of new ventures; asset

acquisitions and dispositions; any impact of hurricanes or other severe weather on our business, including any

impact on fuel prices; receipt of necessary government permits, approvals, rate relief and regulatory cost

recovery; capital market conditions and decisions regarding capital structure; the impact of state, federal or

foreign investigations applicable to PPL Corporation and its subsidiaries; the outcome of litigation against PPL

Corporation and its subsidiaries; stock price performance; the market prices of equity securities and the impact

on pension income and resultant cash funding requirements for defined benefit pension plans; the securities and

credit ratings of PPL Corporation and its subsidiaries; political, regulatory or economic conditions in states,

regions or countries where PPL Corporation or its subsidiaries conduct business, including any potential effects

of threatened or actual terrorism or war or other hostilities; foreign exchange rates; new state, federal or foreign

legislation, including new tax legislation; and the commitments and liabilities of PPL Corporation and its

subsidiaries. Any such forward-looking statements should be considered in light of such important factors and in

conjunction with PPL Corporation’s Form 10-K and other reports on file with the Securities and Exchange

Commission.

margins and sales, growth, revenues, expenses, cash flow, asset disposition, marketing performance, hedging,

regulation, corporate strategy and generating capacity and performance, are “forward-looking statements” within

the meaning of the federal securities laws. Although PPL Corporation believes that the expectations and

assumptions reflected in these forward-looking statements are reasonable, these statements are subject to a

number of risks and uncertainties, and actual results may differ materially from the results discussed in the

statements. The following are among the important factors that could cause actual results to differ materially from

the forward-looking statements: market demand and prices for energy, capacity and fuel; weather conditions

affecting customer energy usage and operating costs; competition in power markets; the effect of any business

or industry restructuring; the profitability and liquidity of PPL Corporation and its subsidiaries; new accounting

requirements or new interpretations or applications of existing requirements; operating performance of plants and

other facilities; environmental conditions and requirements and the related costs of compliance, including

environmental capital expenditures and emission allowance and other expenses; system conditions and

operating costs; development of new projects, markets and technologies; performance of new ventures; asset

acquisitions and dispositions; any impact of hurricanes or other severe weather on our business, including any

impact on fuel prices; receipt of necessary government permits, approvals, rate relief and regulatory cost

recovery; capital market conditions and decisions regarding capital structure; the impact of state, federal or

foreign investigations applicable to PPL Corporation and its subsidiaries; the outcome of litigation against PPL

Corporation and its subsidiaries; stock price performance; the market prices of equity securities and the impact

on pension income and resultant cash funding requirements for defined benefit pension plans; the securities and

credit ratings of PPL Corporation and its subsidiaries; political, regulatory or economic conditions in states,

regions or countries where PPL Corporation or its subsidiaries conduct business, including any potential effects

of threatened or actual terrorism or war or other hostilities; foreign exchange rates; new state, federal or foreign

legislation, including new tax legislation; and the commitments and liabilities of PPL Corporation and its

subsidiaries. Any such forward-looking statements should be considered in light of such important factors and in

conjunction with PPL Corporation’s Form 10-K and other reports on file with the Securities and Exchange

Commission.

Forward-Looking

Information Statement

A-23

“Earnings

from ongoing operations” excludes the impact of special items. Special items

include charges or credits that are unusual or

nonrecurring. Special items also include unrealized gains and losses from energy-related, non-trading economic hedges, foreign

currency-related economic hedges and impairments of securities in PPL’s nuclear decommissioning trust funds. The energy-related, non

-trading economic hedges are used to hedge a portion of the economic value of PPL’s generation assets and PPL’s load-following and

retail activities. This economic value is subject to changes in fair value due to market price volatility of the input and output commodities

(e.g., fuel and power). Also included in this special item is the ineffective portion of qualifying cash flow hedges. The foreign currency-

related economic hedges are used to hedge a portion of the net income of the international delivery business segment. This economic

value in U.S. dollars is subject to changes in the British Pound Sterling to U.S. dollar exchange rate. Management believes that the

exclusion of such amounts provides a better matching of ongoing earnings to the actual amounts settled for our underlying hedged

assets. Earnings from ongoing operations should not be considered as an alternative to reported earnings, or net income attributable to

PPL, which is an indicator of operating performance determined in accordance with generally accepted accounting principles (GAAP).

PPL believes that earnings from ongoing operations, although a non-GAAP measure, is also useful and meaningful to investors because

it provides them with PPL’s underlying earnings performance as another criterion in making their investment decisions. PPL’s

management also uses earnings from ongoing operations in measuring certain corporate performance goals. Other companies may use

different measures to present financial performance.

nonrecurring. Special items also include unrealized gains and losses from energy-related, non-trading economic hedges, foreign

currency-related economic hedges and impairments of securities in PPL’s nuclear decommissioning trust funds. The energy-related, non

-trading economic hedges are used to hedge a portion of the economic value of PPL’s generation assets and PPL’s load-following and

retail activities. This economic value is subject to changes in fair value due to market price volatility of the input and output commodities

(e.g., fuel and power). Also included in this special item is the ineffective portion of qualifying cash flow hedges. The foreign currency-

related economic hedges are used to hedge a portion of the net income of the international delivery business segment. This economic

value in U.S. dollars is subject to changes in the British Pound Sterling to U.S. dollar exchange rate. Management believes that the

exclusion of such amounts provides a better matching of ongoing earnings to the actual amounts settled for our underlying hedged

assets. Earnings from ongoing operations should not be considered as an alternative to reported earnings, or net income attributable to

PPL, which is an indicator of operating performance determined in accordance with generally accepted accounting principles (GAAP).

PPL believes that earnings from ongoing operations, although a non-GAAP measure, is also useful and meaningful to investors because

it provides them with PPL’s underlying earnings performance as another criterion in making their investment decisions. PPL’s

management also uses earnings from ongoing operations in measuring certain corporate performance goals. Other companies may use

different measures to present financial performance.

“Free

cash flow before dividends” is derived by deducting capital expenditures and

other investing activities-net, as well as the

repayment of transition bonds, from cash flow from operations. Free cash flow before dividends should not be considered as an

alternative to cash flow from operations, which is determined in accordance with GAAP. PPL believes that free cash flow before

dividends, although a non-GAAP measure, is an important measure to both management and investors since it is an indicator of the

company’s ability to sustain operations and growth without additional outside financing beyond the requirement to fund maturing debt

obligations. Other companies may calculate free cash flow before dividends in a different manner.

repayment of transition bonds, from cash flow from operations. Free cash flow before dividends should not be considered as an

alternative to cash flow from operations, which is determined in accordance with GAAP. PPL believes that free cash flow before

dividends, although a non-GAAP measure, is an important measure to both management and investors since it is an indicator of the

company’s ability to sustain operations and growth without additional outside financing beyond the requirement to fund maturing debt

obligations. Other companies may calculate free cash flow before dividends in a different manner.

"Domestic

Gross Energy Margins" is intended to supplement the investors' understanding of

PPL’s domestic non-trading and trading

activities by combining applicable income statement line items and related adjustments to calculate a single financial measure. PPL

believes that "Domestic Gross Energy Margins" is useful and meaningful to investors because it provides them with the results of PPL's

domestic non-trading and trading activities as another criterion in making their investment decisions. "Domestic Gross Energy Margins"

is not intended to replace "Operating Income," which is determined in accordance with GAAP, as an indicator of overall operating

performance. PPL's management also uses "Domestic Gross Energy Margins" in measuring certain corporate performance goals used

in determining variable compensation. Other companies may use different measures to present the results of their non-trading and

trading activities.

activities by combining applicable income statement line items and related adjustments to calculate a single financial measure. PPL

believes that "Domestic Gross Energy Margins" is useful and meaningful to investors because it provides them with the results of PPL's

domestic non-trading and trading activities as another criterion in making their investment decisions. "Domestic Gross Energy Margins"

is not intended to replace "Operating Income," which is determined in accordance with GAAP, as an indicator of overall operating

performance. PPL's management also uses "Domestic Gross Energy Margins" in measuring certain corporate performance goals used

in determining variable compensation. Other companies may use different measures to present the results of their non-trading and

trading activities.

Definitions of

Non-GAAP Financial Measures