Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

x Quarterly Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the quarterly period ended September 30, 2009

oTransition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the transition period from __to ___

Commission file number 1-9735

BERRY PETROLEUM COMPANY

(Exact name of registrant as specified in its charter)

|

DELAWARE |

77-0079387 |

|

(State of incorporation or organization) |

(I.R.S. Employer Identification Number) |

1999 Broadway, Suite 3700

Denver, Colorado 80202

(Address of principal executive offices, including zip code)

Registrant's telephone number, including area code: (303) 999-4400

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

YES x NO o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every

Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the

preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES o NO o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filerx Accelerated filero Non-accelerated filero Smaller reporting companyo

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). YES o NO x

As of October 19, 2009, the registrant had 42,860,540 shares of Class A Common Stock ($.01 par value) outstanding. The registrant also had 1,797,784 shares of Class B Stock ($.01 par value) outstanding on October 19, 2009 all of which is held by an affiliate of the registrant.

1

BERRY PETROLEUM COMPANY

THIRD QUARTER 2009 FORM 10-Q

TABLE OF CONTENTS

|

PART I. FINANCIAL INFORMATION |

Page | |

|

Item 1. Financial Statements |

3 | |

|

3 | ||

|

4 | ||

|

4 | ||

|

5 | ||

|

5 | ||

|

6 | ||

|

7 | ||

|

19 | ||

|

31 | ||

|

35 | ||

|

PART II.

OTHER INFORMATION |

||

|

36 | ||

|

36 | ||

|

38 | ||

|

38 | ||

|

38 | ||

|

38 | ||

|

39 |

BERRY PETROLEUM COMPANY

Unaudited Condensed Balance Sheets

(In Thousands, Except Share Information)

|

September 30, 2009 |

December 31, 2008 |

|||||||

|

ASSETS |

||||||||

|

Current assets: |

||||||||

|

Cash and cash equivalents |

$ | 975 | $ | 240 | ||||

|

Short-term investments |

67 | 66 | ||||||

|

Accounts receivable, net of allowance for doubtful accounts of $38,508 and $38,511 |

67,726 | 65,873 | ||||||

|

Fair value of derivatives |

30,460 | 111,886 | ||||||

|

Crude oil inventory |

1,393 | - | ||||||

|

Prepaid expenses and other |

8,780 | 11,015 | ||||||

|

Total current assets |

109,401 | 189,080 | ||||||

|

Oil and gas properties (successful efforts basis), buildings and equipment, net |

2,096,897 | 2,254,425 | ||||||

|

Fair value of derivatives |

1,002 | 79,696 | ||||||

|

Other assets |

33,245 | 19,182 | ||||||

| $ | 2,240,545 | $ | 2,542,383 | |||||

|

LIABILITIES AND SHAREHOLDERS' EQUITY |

||||||||

|

Current liabilities: |

||||||||

|

Accounts payable |

$ | 53,755 | $ | 119,221 | ||||

|

Revenue and royalties payable |

14,325 | 34,416 | ||||||

|

Accrued liabilities |

45,630 | 34,566 | ||||||

|

Line of credit |

12,500 | 25,300 | ||||||

|

Income taxes payable |

498 | 187 | ||||||

|

Fair value of derivatives |

21,441 | 1,445 | ||||||

|

Deferred income taxes |

892 | 45,490 | ||||||

|

Total current liabilities |

149,041 | 260,625 | ||||||

|

Long-term liabilities: |

||||||||

|

Deferred income taxes |

250,045 | 270,323 | ||||||

|

Senior secured revolving credit facility |

365,000 | 931,800 | ||||||

|

8 ¼ % Senior subordinated notes due 2016 |

200,000 | 200,000 | ||||||

|

10 ¼ % Senior notes due 2014, net of unamortized discount of $14,075 and $0, respectively |

435,925 | - | ||||||

|

Abandonment obligation |

43,229 | 41,967 | ||||||

|

Other long-term liabilities |

20,828 | 5,921 | ||||||

|

Fair value of derivatives |

41,316 | 4,203 | ||||||

|

Total long-term liabilities |

1,356,343 | 1,454,214 | ||||||

|

Shareholders' equity: |

||||||||

|

Preferred stock, $.01 par value, 2,000,000 shares authorized; no shares outstanding |

- | - | ||||||

|

Capital stock, $.01 par value: |

||||||||

|

Class A Common Stock, 100,000,000 shares authorized; 42,855,902 shares issued and outstanding (42,782,365 in 2008) |

427 | 427 | ||||||

|

Class B Stock, 3,000,000 shares authorized; 1,797,784 shares issued and outstanding in 2009 and 2008 (liquidation preference of $899) |

18 | 18 | ||||||

|

Capital in excess of par value |

87,398 | 79,653 | ||||||

|

Accumulated other comprehensive (loss) income |

(17,210 | ) | 113,697 | |||||

|

Retained earnings |

664,528 | 633,749 | ||||||

|

Total shareholders' equity |

735,161 | 827,544 | ||||||

| $ | 2,240,545 | $ | 2,542,383 | |||||

The accompanying notes are an integral part of these financial statements.

BERRY PETROLEUM COMPANY

Unaudited Condensed Statements of Operations

Three Months Ended September 30, 2009 and 2008

(In Thousands, Except Per Share Data)

|

Three months ended September 30, |

||||||||

|

2009 |

2008 |

|||||||

|

REVENUES AND OTHER INCOME ITEMS |

||||||||

|

Sales of oil and gas |

$ | 127,455 | $ | 193,890 | ||||

|

Sales of electricity |

9,137 | 18,317 | ||||||

|

Gas marketing |

5,217 | 13,284 | ||||||

|

Gain on derivatives |

531 | 701 | ||||||

|

Gain on sale of assets |

828 | 95 | ||||||

|

Interest and other income, net |

287 | 747 | ||||||

| 143,455 | 227,034 | |||||||

|

EXPENSES |

||||||||

|

Operating costs - oil and gas production |

39,195 | 52,486 | ||||||

|

Operating costs - electricity generation |

6,892 | 13,706 | ||||||

|

Production taxes |

3,874 | 8,912 | ||||||

|

Depreciation, depletion & amortization - oil and gas production |

33,502 | 37,354 | ||||||

|

Depreciation, depletion & amortization - electricity generation |

951 | 646 | ||||||

|

Gas marketing |

4,633 | 12,034 | ||||||

|

General and administrative |

10,686 | 14,251 | ||||||

|

Interest expense |

14,562 | 8,031 | ||||||

|

Extinguishment of debt |

329 | - | ||||||

|

Dry hole, abandonment, impairment and exploration |

69 | 1,488 | ||||||

| 114,693 | 148,908 | |||||||

|

Income before income taxes |

28,762 | 78,126 | ||||||

|

Provision for income taxes |

10,423 | 28,511 | ||||||

|

Income from continuing operations |

18,339 | 49,615 | ||||||

|

Income from discontinued operations, net of taxes |

668 | 3,733 | ||||||

|

Net income |

$ | 19,007 | $ | 53,348 | ||||

|

Basic net income from continuing operations per share |

$ | 0.41 | $ | 1.10 | ||||

|

Basic net income from discontinued operations per share |

$ | 0.01 | $ | 0.08 | ||||

|

Basic net income per share |

$ | 0.42 | $ | 1.18 | ||||

|

Diluted net income from continuing operations per share |

$ | 0.40 | $ | 1.08 | ||||

|

Diluted netincome from discontinued operations per share |

$ | 0.01 | $ | 0.08 | ||||

|

Diluted net income per share |

$ | 0.41 | $ | 1.16 | ||||

|

Dividends per share |

$ | 0.075 | $ | 0.075 | ||||

Unaudited Condensed Statements of Comprehensive Income

Three Months Ended September 30, 2009 and 2008

(In Thousands)

|

Net income |

$ | 19,007 | $ | 53,348 | ||||

|

Unrealized gains (losses) on derivatives, net of income taxes (benefits) of ($345) and $144,881, respectively |

(563 | ) | 225,693 | |||||

|

Reclassification of realized (losses) gains on derivatives included in net income, net of income taxes (benefits) of ($279) and $18,745, respectively |

(454 | ) | 30,584 | |||||

|

Comprehensive income |

$ | 17,990 | $ | 309,625 |

The accompanying notes are an integral part of these financial statements.

BERRY PETROLEUM COMPANY

Unaudited Condensed Statements of Operations

Nine Months Ended September 30, 2009 and 2008

(In Thousands, Except Per Share Data)

|

Nine months ended September 30, |

||||||||

|

2009 |

2008 |

|||||||

|

REVENUES AND OTHER INCOME ITEMS |

||||||||

|

Sales of oil and gas |

$ | 374,117 | $ | 514,578 | ||||

|

Sales of electricity |

26,032 | 51,223 | ||||||

|

Gas marketing |

17,646 | 28,046 | ||||||

|

Gain (loss) on derivatives |

6,565 | (27 | ) | |||||

|

Gain on sale of assets |

828 | 510 | ||||||

|

Interest and other income, net |

1,375 | 2,509 | ||||||

| 426,563 | 596,839 | |||||||

|

EXPENSES |

||||||||

|

Operating costs - oil and gas production |

111,317 | 144,158 | ||||||

|

Operating costs - electricity generation |

22,071 | 45,620 | ||||||

|

Production taxes |

14,411 | 20,663 | ||||||

|

Depreciation, depletion & amortization - oil and gas production |

104,271 | 87,462 | ||||||

|

Depreciation, depletion & amortization - electricity generation |

2,938 | 1,991 | ||||||

|

Gas marketing |

16,149 | 26,087 | ||||||

|

General and administrative |

37,143 | 36,312 | ||||||

|

Interest expense |

35,201 | 14,910 | ||||||

|

Extinguishment of debt |

10,823 | - | ||||||

|

Dry hole, abandonment, impairment and exploration |

209 | 7,396 | ||||||

| 354,533 | 384,599 | |||||||

|

Income before income taxes |

72,030 | 212,240 | ||||||

|

Provision for income taxes |

24,681 | 79,377 | ||||||

|

Income from continuing operations |

47,349 | 132,863 | ||||||

|

(Loss) income from discontinued operations, net of taxes |

(6,323 | ) | 12,657 | |||||

|

Net income |

$ | 41,026 | $ | 145,520 | ||||

|

Basic net income from continuing operations per share |

$ | 1.04 | $ | 2.95 | ||||

|

Basic net (loss) income from discontinued operations per share |

$ | (0.14 | ) | $ | 0.28 | |||

|

Basic net income per share |

$ | 0.90 | $ | 3.23 | ||||

|

Diluted net income from continuing operations per share |

$ | 1.03 | $ | 2.90 | ||||

|

Diluted net (loss) income from discontinued operations per share |

$ | (0.14 | ) | $ | 0.28 | |||

|

Diluted net income per share |

$ | 0.89 | $ | 3.18 | ||||

|

Dividends per share |

$ | 0.225 | $ | 0.225 | ||||

Unaudited Condensed Statements of Comprehensive Income

Nine Months Ended September 30, 2009 and 2008

(In Thousands)

|

Net income |

$ | 41,026 | $ | 145,520 | ||||

|

Unrealized gains (losses) on derivatives, net of income taxes (benefits) of $104,173 and $58,260, respectively |

169,966 | (95,055 | ) | |||||

|

Reclassification of realized (losses)gains on derivatives included in net income, net of income taxes (benefits) of ($23,940) and $52,341, respectively |

(39,059 | ) | 85,399 | |||||

|

Comprehensive income |

$ | 171,933 | $ | 135,864 |

The accompanying notes are an integral part of these financial statements.

BERRY PETROLEUM COMPANY

Unaudited Condensed Statements of Cash Flows

Nine Months Ended September 30, 2009 and 2008

(In Thousands)

|

Nine months ended September 30, |

||||||||

|

2009 |

2008 |

|||||||

|

Cash flows from operating activities: |

||||||||

|

Net income |

$ | 41,026 | $ | 145,520 | ||||

|

Depreciation, depletion and amortization |

109,397 | 98,579 | ||||||

|

Extinguishment of debt |

10,823 | - | ||||||

|

Dry hole and impairment |

9,643 | 6,858 | ||||||

|

Commodity derivatives |

4,796 | (8 | ) | |||||

|

Stock-based compensation expense |

7,054 | 6,653 | ||||||

|

Deferred income taxes |

13,546 | 76,502 | ||||||

|

Loss (gain) on sale of oil and gas properties |

79 | (510 | ) | |||||

|

Other, net |

(362 | ) | (1,500 | ) | ||||

|

Cash paid for abandonment |

(293 | ) | (3,957 | ) | ||||

|

Change in book overdraft |

(20,199 | ) | 3,935 | |||||

|

Increase in current assets other than cash and cash equivalents |

(9,828 | ) | (35,361 | ) | ||||

|

(Decrease) increase in current liabilities other than book overdraft, line of credit and fair value of derivatives |

(17,303 | ) | 34,537 | |||||

|

Net cash provided by operating activities |

148,379 | 331,248 | ||||||

|

Cash flows from investing activities: |

||||||||

|

Exploration and development of oil and gas properties |

(93,592 | ) | (302,266 | ) | ||||

|

Property acquisitions |

(11,904 | ) | (667,030 | ) | ||||

|

Additions to vehicles, drilling rigs and other fixed assets |

(1,044 | ) | (4,146 | ) | ||||

|

Proceeds from sale of assets |

139,796 | 2,038 | ||||||

|

Capitalized interest |

(21,145 | ) | (15,461 | ) | ||||

|

Net cash provided by (used in) investing activities |

12,111 | (986,865 | ) | |||||

|

Cash flows from financing activities: |

||||||||

|

Proceeds from line of credit |

323,100 | 308,000 | ||||||

|

Payments on line of credit |

(335,900 | ) | (303,000 | ) | ||||

|

Proceeds from issuance of long-term debt |

1,099,238 | 1,481,300 | ||||||

|

Payments on long-term debt |

(1,231,076 | ) | (817,000 | ) | ||||

|

Debt issuance cost |

(23,857 | ) | (8,353 | ) | ||||

|

Proceeds from financing obligation |

18,295 | - | ||||||

|

Dividends paid |

(10,247 | ) | (10,084 | ) | ||||

|

Proceeds from stock option exercises |

601 | 2,834 | ||||||

|

Excess tax benefit and other |

91 | 1,663 | ||||||

|

Net cash (used in) provided by financing activities |

(159,755 | ) | 655,360 | |||||

|

Net increase (decrease) in cash and cash equivalents |

735 | (257 | ) | |||||

|

Cash and cash equivalents at beginning of year |

240 | 316 | ||||||

|

Cash and cash equivalents at end of period |

$ | 975 | $ | 59 | ||||

The accompanying notes are an integral part of these financial statements.

Berry Petroleum Company

Notes to the Unaudited Condensed Financial Statements

|

1. |

General |

All adjustments which are, in the opinion of management, necessary for a fair statement of Berry Petroleum Company’s (the Company) financial position at September 30, 2009 and December 31, 2008 and results of operations and other comprehensive income for the three and nine months ended September 30, 2009 and 2008, and its cash

flows for the nine months ended September 30, 2009 and 2008 have been included. All such adjustments, except as described below, are of a normal recurring nature. The results of operations and cash flows are not necessarily indicative of the results for a full year.

The accompanying unaudited condensed financial statements have been prepared on a basis consistent with the accounting principles and policies reflected in the December 31, 2008 financial statements, except that the DJ basin operations are now accounted for as discontinued operations as a result of the 2009 sale. The audited

financial statements for the three years ended December 31, 2008 and at December 31, 2007 and 2008 included in our Form 8-K filed on August 11, 2009, which give effect to the classification of the DJ Basin assets as discontinued operations, should be read in conjunction herewith. The year-end condensed Balance Sheet was derived from audited financial statements, but does not include all disclosures required by accounting principles generally accepted in the United States of America.

Our cash management process provides for the daily funding of checks as they are presented to the bank. Included in accounts payable at September 30, 2009 and December 31, 2008 is $11.6 million and $31.8 million, respectively, representing outstanding checks in excess of the bank balance (book overdraft).

|

2. |

Recent Accounting Developments |

In December 2007, the Financial Accounting Standards Board (FASB) issued authoritative guidance to establish accounting and reporting standards for the noncontrolling interests in a subsidiary (formerly called minority interests) and for the deconsolidation of a subsidiary. The adoption of this authoritative guidance did not have

a material impact on our financial statements.

In March 2008, the FASB issued authoritative guidance, which changes the disclosure requirements for derivative instruments and hedging activities. Expanded disclosures are required to provide information about (a) how and why an entity uses derivative instruments, (b) how derivative instruments and related hedged items are accounted for

and (c) how derivative instruments and related hedged items affect an entity’s financial position, financial performance, and cash flows. The adoption of this authoritative guidance did not have a material impact on our financial statements. We have expanded our disclosures accordingly. See Note 4 to the unaudited financial statements.

In June 2008, the FASB issued authoritative guidance, which clarifies that share-based payment awards that entitle their holders to receive nonforfeitable dividends before vesting should be considered participating securities. As participating securities, these instruments should be included in the earnings allocation in computing basic earnings

per share under the two-class method described in authoritative guidance. All prior period earnings per share data presented shall be adjusted retrospectively to conform with the provisions of this guidance. This guidance is effective for financial statements issued for fiscal years beginning after December 15, 2008 and interim periods within those years. The adoption of this authoritative guidance did not have a material impact on our financial statements. See Note 12 to the unaudited

financial statements.

In December 2008, the Securities and Exchange Commission adopted revisions to its oil and gas disclosure requirements that are intended to align them with current practices and changes in technology. Among other things, the amendments will: replace the single-day year-end pricing assumption with a twelve-month average pricing assumption;

permit the disclosure of probable and possible reserves; allow the use of certain technologies to establish reserves; require the disclosure of the qualifications of the technical person primarily responsible for preparing the reserves estimates or conducting a reserves audit; require the filing of the independent reserve engineers' summary report; and permit the disclosure of a reserves sensitivity analysis table to illustrate the impact of different price and/or cost assumptions on reserves. These amendments

are effective for registration statements filed on or after January 1, 2010, and for annual reports on Form 10-K for fiscal years ending on December 31, 2009, with early adoption prohibited. The Company is currently evaluating the impact that the adoption of this pronouncement will have on the Company's financial position, results of operations, and disclosures.

In April 2009, the FASB issued authoritative guidance which requires disclosures about the fair value of financial instruments for interim reporting periods as well as in annual financial statements. The adoption of this authoritative guidance did not have a material impact

on our financial statements. We have expanded our disclosures accordingly. See Note 3 to the unaudited financial statements.

Berry Petroleum Company

Notes to the Unaudited Condensed Financial Statements

In May 2009, the FASB issued authoritative guidance, which establishes general standards of accounting for and disclosure of events that occur after the balance sheet date but before financial statements are issued or are available to be issued. We implemented this guidance during the

second quarter of 2009 and we expanded our disclosures accordingly. See Note 15 to the unaudited financial statements.

In June 2009, the FASB approved the FASB Accounting Standards Codification (ASC), which after its effective date of July 1, 2009 is the single source of authoritative, nongovernmental U.S. Generally Accepted Accounting Principles (GAAP). The Codification reorganizes all previous U.S. GAAP pronouncements into roughly 90 accounting

topics and displays all topics using a consistent structure. All existing standards that were used to create the Codification are now superseded, replacing the previous references to specific Statements of Financial Accounting Standards (SFAS) with numbers used in the Codification’s structural organization. The adoption of this authoritative guidance did not have a material impact on our financial statements. We have updated our disclosures accordingly.

|

3. |

Fair Value Measurements |

In September 2006, the Financial Accounting Standards Board (FASB) issued authoritative guidance that clarifies the definition of fair value, establishes a framework for measuring fair value, and expands disclosures about fair value measurements. We adopted the authoritative guidance as of January 1, 2008 for all financial and nonfinancial

assets and liabilities recognized or disclosed at fair value on a recurring basis. We have also adopted the authoritative guidance as it relates to all nonfinancial assets and liabilities that are not recognized or disclosed on a recurring basis as of January 1, 2009 pursuant to the authoritative guidance issued by the FASB in February 2008. The adoption of the authoritative guidance did not have a material impact on our financial statements.

The authoritative guidance establishes a three-tier fair value hierarchy, which prioritizes the inputs used to measure fair value. These tiers include: Level 1, defined as unadjusted quoted prices in active markets for identical assets or liabilities; Level 2, defined as inputs other than quoted prices in active markets that are

either directly or indirectly observable; and Level 3, defined as unobservable inputs for use when little or no market data exists, therefore requiring an entity to develop its own assumptions.

A financial instrument’s categorization within the valuation hierarchy is based upon the lowest level of input that is significant to the fair value measurement. The Company’s assessment of the significance of a particular input to the fair value measurement requires judgment and may affect the classification of assets

and liabilities within the fair value hierarchy. Our oil swaps, natural gas swaps and interest rate swaps are valued using internal models which are based on active market data and are classified within Level 2 of the valuation hierarchy. The observable inputs include underlying commodity and interest rate levels and quoted prices of these instruments on actively traded markets. Derivatives that are valued based upon models with significant unobservable market inputs (primarily volatility),

and that are normally traded less actively are classified within Level 3 of the valuation hierarchy. Level 3 derivatives include oil collars, natural gas collars and natural gas basis swaps.

The following tables sets forth by level within the fair value hierarchy the Company’s assets and liabilities that were measured at fair value on a recurring basis as of September 30, 2009 and December 31, 2008.

|

September 30, 2009 (in millions) |

Total carrying value on the condensed Balance Sheet |

Level 2 |

Level 3 |

|||||||||

|

Commodity derivative asset (liability) |

$ | (21.5 | ) | $ | (54.1 | ) | $ | 32.6 | ||||

|

Interest rate swap asset (liability) |

(9.8 | ) | (9.8 | ) | - | |||||||

|

Total fair value asset (liability) |

$ | (31.3 | ) | $ | (63.9 | ) | $ | 32.6 | ||||

|

December 31, 2008 (in millions) |

Total carrying value on the condensed Balance Sheet |

Level 2 |

Level 3 |

|||||||||

|

Commodity derivative asset (liability) |

$ | 198.4 | $ | 25.9 | $ | 172.5 | ||||||

|

Interest rate swap asset (liability) |

(12.5 | ) | (12.5 | ) | - | |||||||

|

Total fair value asset (liability) |

$ | 185.9 | $ | 13.4 | $ | 172.5 | ||||||

Berry Petroleum Company

Notes to the Unaudited Condensed Financial Statements

Changes in Level 3 fair value measurements

The following table sets forth a reconciliation of changes in the fair value of financial instruments classified as Level 3 in the fair value hierarchy:

|

Three months ended September 30, |

Nine months ended September 30, |

|||||||||||||||

|

(in millions) |

2009 |

2008 |

2009 |

2008 |

||||||||||||

|

Fair value of Level 3 derivative assets, beginning of period |

$ | 43.1 | $ | 569.6 | $ | 172.5 | $ | 194.3 | ||||||||

|

Total realized and unrealized losses included in Gain (loss) on derivatives |

(1.0 | ) | (0.6 | ) | (1.7 | ) | 0.2 | |||||||||

|

Purchases, sales and settlements, net |

(9.5 | ) | (360.1 | ) | (141.6 | ) | 14.4 | |||||||||

|

Transfers in and/or out of Level 3 |

- | - | 3.4 | - | ||||||||||||

|

Fair value of Level 3 derivative assets, September 30, 2009 |

$ | 32.6 | $ | 208.9 | $ | 32.6 | $ | 208.9 | ||||||||

|

Total unrealized gains (losses) included in income related to financial assets and liabilities on the condensed balance sheet at September 30, 2009 |

$ | (0.7 | ) | $ | - | $ | (1.3 | ) | $ | - | ||||||

The $3.4 million of transfers into Level 3 for the nine months ended September 30, 2009 represent crude oil collars that were converted to crude oil swaps during the first quarter of 2009.

Fair Market Value of Financial Instruments

The Company used various assumptions and methods in estimating the fair values of its financial instruments. The carrying amounts of cash and cash equivalents and accounts receivable approximated their fair value due to the short-term maturity of these instruments. The carrying amount of the Company's credit facilities approximated fair value,

because the interest rates on the credit facilities are variable. The fair values of our 8 ¼ % senior subordinated notes due 2016 and our 10 ¼ % senior notes due 2014 were estimated based on quoted market prices. The fair values of the Company's derivative instruments and other investments are discussed above.

|

(in millions) |

Carrying Amount |

Estimated Fair Value |

||||||

|

Line of credit |

$ | 13 | $ | 13 | ||||

|

Senior secured revolving credit facility |

365 | 365 | ||||||

|

8 ¼ % Senior subordinated notes due 2016 |

200 | 191 | ||||||

|

10 ¼ % Senior notes due 2014 |

436 | 479 | ||||||

| $ | 1,014 | $ | 1,048 | |||||

|

4. |

Hedging |

To minimize the effect of a downturn in oil and gas prices and protect our profitability and the economics of our development plans, we enter into crude oil and natural gas hedge contracts from time to time. The terms of contracts depend on various factors, including management's view of future crude oil and natural gas prices, acquisition

economics on purchased assets and our future financial commitments. This price hedging program is designed to moderate the effects of a severe crude oil and natural gas price downturn while allowing us to participate in some commodity price increases. We benefit from lower natural gas pricing as we are a consumer of natural gas in our California operations. In the Rocky Mountains and East Texas we benefit from higher natural gas pricing. We have hedged, and may hedge in the future, both natural gas

purchases and sales as determined appropriate by management. Management regularly monitors the crude oil and natural gas markets and our financial commitments to determine if, when, and at what level some form of crude oil and/or natural gas hedging and/or basis adjustments or other price protection is appropriate in accordance with policy established by our Board of Directors. Currently, our hedges are in the form of swaps and collars. However, we may use a variety of hedge instruments

in the future to hedge WTI or the index gas price. We also utilize interest rate derivatives to protect against changes in interest rates on our floating rate debt.

Berry Petroleum Company

Notes to the Unaudited Condensed Financial Statements

The related cash flow impact of all of our hedges is reflected in cash flows from operating activities. At September 30, 2009, our net fair value derivative liability was $31.3 million as compared to a net fair value asset of $185.9 million at December 31, 2008 which reflects changes in commodity prices and interest rates. Based on NYMEX

strip pricing as of September 30, 2009, we expect to receive hedge payments under the existing derivatives of $14.7 million during the next twelve months. At September 30, 2009, “Accumulated Other Comprehensive Income (Loss)” (“AOCL”) consisted of $17.2 million, net of tax, of unrealized losses from our crude oil and natural gas swaps and collars that qualified for hedge accounting treatment at September 30, 2009. Deferred net losses recorded in AOCL at September 30, 2009 and subsequent

mark-to-market changes in the underlying hedging contracts are expected to be reclassified to earnings in the same period that the forecasted transaction impacts earnings.

We present our derivative assets and liabilities on our Condensed Balance Sheets on a net basis. We net derivative assets and liabilities whenever we have a legally enforceable master netting agreement with a counterparty to a derivative contract. We use these agreements to manage

and reduce our potential counterparty credit risk.

The following table disaggregates our net derivative assets and liabilities into gross components on a contract-by-contract basis before giving effect to master netting arrangements. Finally, we identify the line items on our Condensed Balance Sheets in which these fair value amounts are included. The

gross asset and liability values in the table below are segregated between those derivatives designated in qualifying hedge accounting relationships and those not designated in hedge accounting relationships. We use the end of period accounting designation to determine the classification for each derivative position.

|

As of September 30, 2009 |

||||||||||

|

Derivative Assets |

Derivative Liabilities |

|||||||||

|

(in millions) |

Balance Sheet Location |

Fair Value |

Balance Sheet Location |

Fair Value |

||||||

|

Commodity – Oil |

Current assets |

$ | 31.7 |

Current liability |

$ | 14.5 | ||||

|

Commodity – Natural Gas |

Current assets |

1.4 | ||||||||

|

Commodity – Oil |

Long term assets |

1.0 |

Long term liabilities |

37.3 | ||||||

|

Commodity – Natural Gas |

Long term liabilities |

0.3 | ||||||||

|

Commodity – Natural Gas |

Current liability |

0.7 | ||||||||

|

Interest rate contracts |

Current assets |

2.7 | ||||||||

|

Interest rate contracts |

Current liabilities |

3.6 | ||||||||

|

Interest rate contracts |

Long term liabilities |

3.4 | ||||||||

|

Total derivatives designated as hedging instruments under authoritative guidance |

34.8 | 61.8 | ||||||||

|

Commodity – Oil |

- |

Current liabilities |

3.1 | |||||||

|

Commodity – Natural Gas |

- |

Current liabilities |

0.9 | |||||||

|

Commodity – Natural Gas |

- |

Long term liabilities |

0.3 | |||||||

|

Total derivatives not designated as hedging instruments under authoritative guidance |

- | 4.3 | ||||||||

|

Total Derivatives |

$ | 34.8 | $ | 66.1 | ||||||

Berry Petroleum Company

Notes to the Unaudited Condensed Financial Statements

The tables below summarize the Statement of Operations impacts of our derivative instruments for the three and nine months ending September 30,2009 (in millions):

|

Derivatives cash flow hedging relationships |

Amount of gain (loss) Recognized in AOCI on Derivative

(Effective portion) |

Location of Gain (Loss) Reclassified from AOCI into Income (Effective Portion) |

Amount of Gain (Loss) Reclassified from AOCI into Income (Effective Portion) |

Location of Gain (loss) Recognized in Income of Derivative (Ineffective Portion and Amount Excluded from Effectiveness Testing) |

Amount of Gain (loss) Recognized in Income of Derivative (Ineffective Portion and Amount Excluded from Effectiveness Testing) |

|||||||||

|

Three Months Ended

September 30, 2009 |

Three Months Ended

September 30, 2009 |

Three Months Ended

September 30, 2009 |

||||||||||||

|

Commodity - Oil |

$ | (2.5 | ) |

Sales of oil and gas |

$ | 1.0 |

Sales of oil and gas |

$ | - | |||||

|

Commodity - Natural Gas |

1.8 |

Sales of oil and gas |

0.6 |

Gain (loss) on derivatives |

(0.6 | ) | ||||||||

|

Interest rate |

0.7 |

Interest expense |

(1.1 | ) |

Gain (loss) on derivatives |

0.1 | ||||||||

|

Total |

$ | - | $ | 0.5 | $ | (0.5 | ) | |||||||

|

Derivatives cash flow hedging relationships |

Amount of gain (loss) Recognized in AOCI on Derivative

(Effective portion) |

Location of Gain (Loss) Reclassified from AOCI into Income (Effective Portion) |

Amount of Gain (Loss) Reclassified from AOCI into Income (Effective Portion) |

Location of Gain (loss) Recognized in Income of Derivative (Ineffective Portion and Amount Excluded from Effectiveness Testing) |

Amount of Gain (loss) Recognized in Income of Derivative (Ineffective Portion and Amount Excluded from Effectiveness Testing) |

|||||||||

|

Nine Months Ended

September 30, 2009 |

Nine Months Ended

September 30, 2009 |

Nine Months Ended

September 30, 2009 |

||||||||||||

|

Commodity - Oil |

$ | 161.4 |

Sales of oil and gas |

$ | 36.4 |

Sales of oil and gas |

$ | - | ||||||

|

Commodity - Natural Gas |

13.1 |

Sales of oil and gas |

5.4 |

Gain (loss) on derivatives |

14.0 | |||||||||

|

Interest rate |

(3.9 | ) |

Interest expense |

(2.7 | ) |

Gain (loss) on derivatives |

(0.2 | ) | ||||||

|

Total |

$ | 170.6 | $ | 39.1 | $ | 13.8 | ||||||||

Amount of Gain or (Loss) Recognized in Income on Derivatives not designated as Hedging Instruments under authoritative guidance:

|

Derivatives not designated as Hedging Instruments under authoritative guidance |

Location of Gain (Loss) Recognized in Income on Derivative |

Amount of Gain (Loss) Recognized in Income on Derivatives not designated as Hedging Instruments under authoritative guidance |

Amount of Gain (Loss) Recognized in Income on Derivatives not designated as Hedging Instruments under authoritative guidance |

||||||

|

Three months ended

September 30, 2009 |

Nine months ended

September 30, 2009 |

||||||||

|

Commodity – Oil |

Gain (loss) on derivatives |

$ | 1.6 | (5.7 | ) | ||||

|

Commodity - Natural Gas |

Gain (loss) on derivatives |

(0.5 | ) | (1.5 | ) | ||||

|

Commodity - Natural Gas |

(Loss) income from discontinued operations, net of taxes |

- | (0.5 | ) | |||||

|

Total Derivatives |

$ | 1.1 | (7.7 | ) | |||||

We did not enter into any crude oil or natural gas hedges during the three months ended September 30, 2009.

Berry Petroleum Company

Notes to the Unaudited Condensed Financial Statements

During the first quarter of 2009, we converted oil collars for 6,000 Bbl/D for the full year 2010 into swaps for the same volumes with swap prices ranging from $61.00 to $64.80.

We generally utilize NYMEX WTI based derivatives to hedge cash flows from our California oil sales. Our oil sales contracts with multiple refiners are primarily based on the field posting prices. There is a high correlation between WTI and the field posting prices which allows us to utilize hedge accounting. As

there is a ready market for our crude oil in California, we do not believe the loss of any particular contract impacts the probability that our hedged forecasted transactions will occur. We generally hedge our natural gas at the basis location that corresponds to the forecasted sale.

While we designate the majority of our hedges as cash flow hedges, we have not elected hedge accounting on certain of our crude oil and natural gas hedges. During the three and nine months ended September 30, 2009, we recorded $0.5 million and $6.6 million under the caption “Gain (loss) on derivatives” related

to hedges for which we either did not elect hedge accounting or which no longer qualified for hedge accounting. In conjunction with the sale of the DJ basin assets, during the first quarter of 2009, we concluded that the forecasted transaction in certain of our hedging relationships was not probable of occurring. As such, we reclassified a gain of $14.3 million from accumulated other comprehensive income (loss) to the statement of operations under the caption “Gain (loss) on derivative.” Additionally,

a portion of the change in fair value for hedges that we have designated as cash flow hedges may impact our income as our sales price is not perfectly correlated with our hedges. We recognized an unrealized net loss of $0.5 million and $0.4 million on the statement of operations under the caption “Gain (loss) on derivatives” for the three and nine months ended September 30, 2009, respectively, as a result of ineffectiveness. During the first quarter of 2009, we entered into natural

gas derivatives on behalf of the purchaser of our DJ assets. We did not elect hedge accounting for these hedges and recorded an unrealized net loss of $0.5 million on the statement of operations under the caption “(Loss) income from discontinued operations, net of taxes.”

Our hedge contracts have been executed only with counterparties that are party to our senior secured revolving credit facility.

Neither we nor our counterparties are required to post collateral in connection with our derivative positions and netting agreements are in place with each of our counterparties allowing us to offset our commodity derivative asset and liability positions. The credit rating of each of these counterparties was AA-/Aa2, or better

as of September 30, 2009. Our derivatives are held with a small number of counterparties and as of September 30, 2009, our largest four counterparties accounted for 90% of the value of our total derivative positions.

As of September 30, 2009, we had the following commodity hedges:

|

2009 |

2010 |

2011 |

2012 | |

|

Oil Bbl/D: |

17,535 |

14,930 |

9,020 |

3,000 |

|

Natural Gas MMBtu/D: |

14,000 |

14,000 |

5,000 |

5,000 |

|

5. |

Crude Oil Inventory |

In May 2009, we entered into a sales agreement with a refiner for 1,500 barrels per day of production from our Poso Creek property for the months of May and June 2009. Under this agreement, we delivered approximately 100,000 barrels of oil to the refiner and received inventory of a slightly higher quality crude oil at the refinery. This

transaction was accounted for as a non-monetary exchange and the amount was recorded in crude oil inventory. The refiner purchased 50,000 barrels from us during the third quarter of 2009 and the remaining balance in “Crude Oil Inventory” at September 30, 2009 reflects the cost of production, transportation costs and quality differentials for the remaining 50,000 barrels of inventory volume.

|

6. |

Asset Retirement Obligations |

The following table summarizes the change in abandonment obligation for the nine months ended September 30, 2009 (in thousands):

|

Beginning balance at January 1, 2009 |

$ | 41,967 | ||

|

Liabilities incurred |

1,407 | |||

|

Liabilities settled |

(3,044 | ) | ||

|

Revisions in estimated liabilities |

- | |||

|

Accretion expense |

2,899 | |||

|

Ending balance at September 30, 2009 |

$ | 43,229 |

Berry Petroleum Company

Notes to the Unaudited Condensed Financial Statements

The asset retirement obligation (“ARO”) reflects the estimated present value of the amount of dismantlement, removal, site reclamation and similar activities associated with our oil and gas properties. Inherent in the fair value calculation of the ARO are numerous assumptions and judgments including the ultimate settlement amounts,

inflation factors, credit adjusted discount rates, timing of settlement, and changes in the legal, regulatory, environmental and political environments. To the extent future revisions to these assumptions impact the fair value of the existing ARO liability, a corresponding adjustment is made to the oil and gas property balance.

|

7. |

Acquisitions |

During the nine months ended September 30, 2009, we completed acquisitions totaling $11.9 million. In June 2009, we acquired property near McKittrick, California, the deep rights to one of the leases in our Darco property in East Texas, and additional interests in our Piceance Garden Gulch assets.

|

8. |

Dispositions and Discontinued Operations |

On July 17, 2009, we completed the financing of our East Texas gas gathering system for $18.4 million in cash. We entered into concurrent long-term gas gathering agreements for the East Texas production which contained an embedded lease. The transaction was treated as a financing obligation. Accordingly,

the net book value of the property of $16.7 million will be depreciated over the remaining useful life of the asset and the cash received of $18.4 million was recorded as a financing obligation. A portion of future payments will be recorded as gathering expense, a portion as interest expense and the balance as a reduction in the financing obligation. There is no minimum payment required under these agreements.

On March 3, 2009, we entered into an agreement to sell our DJ basin assets and related hedges for $154 million before customary closing adjustments. The closing date of the sale of the assets was April 1, 2009. We recorded a pre-tax impairment loss of $9.6 million related to the sale, which is aggregated within the $6.3 million

“(Loss) income from discontinued operations, net of taxes” on our statement of operations for the nine months ended September 30, 2009.

(Loss) income from discontinued operations, net of tax on our accompanying statements of operations is comprised of the following (in thousands):

|

For the Three Months Ended

September 30, |

For the Nine Months Ended

September 30, |

|||||||||||||||

|

2009 |

2008 |

2009 |

2008 |

|||||||||||||

|

Oil and gas revenue |

$ | - | $ | 13,972 | $ | 5,396 | $ | 43,111 | ||||||||

|

Loss on sale of asset |

(578 | ) | - | (908 | ) | - | ||||||||||

|

Other revenue |

- | 350 | 623 | 1,441 | ||||||||||||

|

Total Revenue |

(578 | ) | 14,322 | 5,111 | 44,552 | |||||||||||

|

Operating expenses |

- | 3,552 | 2,576 | 8,694 | ||||||||||||

|

Production taxes |

- | 761 | 195 | 2,458 | ||||||||||||

|

DD&A |

- | 3,086 | 2,188 | 9,126 | ||||||||||||

|

General and administrative |

- | 273 | 388 | 755 | ||||||||||||

|

Interest expense |

- | 724 | 815 | 1,534 | ||||||||||||

|

Commodity derivatives |

- | - | 484 | - | ||||||||||||

|

Dry hole, abandonment, impairment and exploration |

- | 84 | 9,637 | 1,766 | ||||||||||||

|

Total Expenses |

- | 8,480 | 16,283 | 24,333 | ||||||||||||

|

(Loss) income from discontinued operations, before income taxes |

(578 | ) | 5,842 | (11,172 | ) | 20,219 | ||||||||||

|

Income tax benefit (expense) |

1,246 | (2,109 | ) | 4,849 | (7,562 | ) | ||||||||||

|

Income (Loss) from discontinued operations |

$ | 668 | $ | 3,733 | $ | (6,323 | ) | $ | 12,657 | |||||||

Berry Petroleum Company

Notes to the Unaudited Condensed Financial Statements

|

9. |

Dry Hole, Abandonment and Impairment |

During the nine months ended September 30, 2009 and 2008, we recorded dry hole, abandonment, impairment and exploration expense of $0.2 million and $7.4 million, respectively. Charges of $2.7 million, $2.6 million and $1.5 million were recorded during the first, second and third quarters of 2008, respectively for

technical difficulties that were encountered on five wells in the Piceance basin before reaching total depth. These holes were abandoned in favor of drilling to the same bottom hole location by drilling new wells. In addition, $0.5 million of exploration expense was recorded during the nine months ended September 30, 2008 for exploration activities which were primarily 3-D seismic in nature.

|

10. |

Pro Forma Results |

On July 15, 2008, the Company acquired certain interests in natural gas producing properties on 4,500 net acres in Limestone and Harrison Counties in East Texas for $668 million cash (East Texas Acquisition) including an initial purchase price of $622 million, and normal post closing adjustments of $46 million.

The unaudited pro forma results presented below for the three and nine months ended September 30, 2008 have been prepared to give effect to the East Texas Acquisition on the Company’s results of continuing operations under the purchase method of accounting as if it had been consummated at January 1, 2008. The unaudited pro

forma results (in millions) do not purport to represent the results of continuing operations that actually would have occurred on such date or to project the Company’s results of operations for any future date or period:

|

Three Months Ended

September 30, 2008 |

Nine Months Ended

September 30, 2008 |

|||||||

|

Pro forma revenue |

$ | 233,236 | $ | 643,396 | ||||

|

Pro forma income from operations |

$ | 83,575 | $ | 217,351 | ||||

|

Pro forma net income |

$ | 52,977 | $ | 136,016 | ||||

|

Pro forma basic earnings per share |

$ | 1.17 | $ | 3.02 | ||||

|

Pro forma diluted earnings per share |

$ | 1.16 | $ | 2.97 | ||||

|

11. |

Income Taxes |

The effective income tax rate was 36.2% for the third quarter of 2009 compared to 36.1% for the second quarter of 2009 and 36.5% for the third quarter of 2008. The effective tax rate was 34.3% and 37.4% for the nine months ended September 30, 2009 and 2008, respectively. The change for the nine month period ended September

30, 2009 when compared to the same period in 2008 was primarily due to reduced state tax rates and the reduction in our liability related to uncertain tax positions. Our estimated annual effective tax rate varies from the 35% federal statutory rate due to the effects of state income taxes and estimated permanent differences.

As of September 30, 2009, we had a gross liability for uncertain tax benefits of $7.4 million of which $6.2 million, if recognized, would affect the effective tax rate. The liability related to uncertain tax positions was reduced during the nine months ended September 30, 2009 due to the resolution of our IRS examination for 2005.

Due to the uncertainty about the future periods in which other examinations will be completed and limited information related to current audits, we are not able to make reasonably reliable estimates of the periods in which cash settlements will occur with taxing authorities for the noncurrent liabilities.

|

12. |

Earnings per Share |

In June 2008, the FASB issued authoritative guidance, which clarifies that share-based payment awards that entitle their holders to receive nonforfeitable dividends before vesting should be considered participating securities. As participating securities, these instruments should be included in the earnings allocation in computing basic

earnings per share under the two-class method. All prior period earnings per share data presented were adjusted retrospectively to conform with the provisions of the guidance which is effective for financial statements issued for fiscal years beginning after December 15, 2008 and interim periods within those years.

Berry Petroleum Company

Notes to the Unaudited Condensed Financial Statements

The following table shows the computation of basic and diluted net (loss) income per share from continuing and discontinued operations for the three and nine months ended September 30, 2009 and 2008 (in thousands):

|

Three months ended

September 30, |

Nine months ended

September 30, |

|||||||||||||||

|

2009 |

2008 |

2009 |

2008 |

|||||||||||||

|

Net income from continuing operations |

$ | 18,339 | $ | 49,615 | $ | 47,349 | $ | 132,863 | ||||||||

|

Less: Income allocable to participating securities |

445 | 691 | 1,153 | 1,841 | ||||||||||||

|

Income available for shareholders |

17,894 | 48,924 | 46,196 | 131,022 | ||||||||||||

|

Net income (loss) from discontinued operations |

668 | 3,733 | (6,323 | ) | 12,657 | |||||||||||

|

Less: Income allocable to participating securities |

17 | 53 | - | 178 | ||||||||||||

|

Income (loss) from discontinued operations available for shareholders |

651 | 3,680 | (6,323 | ) | 12,479 | |||||||||||

|

Basic earnings per share from continuing operations |

0.41 | 1.10 | 1.04 | 2.95 | ||||||||||||

|

Basic earnings (loss) per share from discontinued operations |

0.01 | 0.08 | (0.14 | ) | 0.28 | |||||||||||

|

Basic earnings per share |

0.42 | 1.18 | 0.90 | 3.23 | ||||||||||||

|

Diluted earnings per share from continuing operations |

0.40 | 1.08 | 1.03 | 2.90 | ||||||||||||

|

Diluted earnings (loss) per share from discontinued operations |

0.01 | 0.08 | (0.14 | ) | 0.28 | |||||||||||

|

Diluted earnings per share |

$ | 0.41 | $ | 1.16 | $ | 0.89 | $ | 3.18 | ||||||||

|

Weighted average shares outstanding – basic |

44,633 | 44,527 | 44,607 | 44,466 | ||||||||||||

|

Add: dilutive effects of stock options |

303 | 651 | 189 | 702 | ||||||||||||

|

Weighted average shares outstanding – dilutive |

44,936 | 45,178 | 44,796 | 45,168 | ||||||||||||

Options to purchase 1.2 million and 1.6 million shares were not included in the diluted (loss) earnings per share calculation for the three and nine months ended September 30, 2009, respectively, because their effect would have been anti-dilutive. Options to purchase 0.2 million and 0.1 million shares were not included in the diluted

(loss) earnings per share calculation for the three and nine months ended September 30, 2008, respectively, because their effect would have been anti-dilutive.

The adoption of the guidance issued by the FASB decreased basic earnings per share from continuing operations by $0.02 and $0.04 for the three and nine months ended September 30, 2008, respectively, and dilutive earnings per share from continuing operations by $0.01 and $0.02 for the three and nine months ended September 30, 2008, respectively. Basic

and dilutive (loss) earnings per share from discontinued operations remained unchanged for the three and nine months ended September 30, 2008.

|

13. |

Debt Obligations |

Short-term lines of credit

In 2005, we completed an unsecured uncommitted money market line of credit (Line of Credit). Borrowings under the Line of Credit may be up to $30 million for a maximum of 30 days. The Line of Credit may be terminated at any time upon written notice by either us or the lender. In conjunction with the amendment to our

senior secured credit facility, on July 15, 2008, the Line of Credit was secured by our assets. At September 30, 2009 and December 31, 2008, the outstanding balance under this Line of Credit was $12.5 million and $25.3 million, respectively. Interest on amounts borrowed is charged at LIBOR plus a margin of approximately 1.6%.

Senior Secured Revolving Credit Facility

Our Senior Secured Revolving Credit Facility (the Agreement) has a current borrowing base and lender commitments of $938 million. The LIBOR and prime rate margins are between 2.25% and 3.0% based on the ratio of credit outstanding to the borrowing base and the annual commitment fee on the unused portion of the credit facility is 0.50%.

Berry Petroleum Company

Notes to the Unaudited Condensed Financial Statements

Covenants under the Agreement are as follows:

|

Total funded debt to EBITDAX ratio not greater than: |

Senior secured debt to EBITDAX ratio not greater than: | ||||||

|

2009 |

2010 |

Thereafter |

to Sep 2010 |

Mar 2011 |

Sep 2011 |

Thereafter | |

|

4.75 |

4.50 |

4.00 |

3.75 |

3.50 |

3.25 |

3.0 | |

The write off of $38.5 million to bad debt expense associated with the bankruptcy of Big West Oil of California (‘Big West”) is excluded from the calculation of EBITDAX, per the Agreement.

The Agreement contains a current ratio covenant which, as defined, must be at least 1.0. During the third quarter of 2009 our borrowing base decreased from $969 billion to $938 million as a result of the add-on of our senior unsecured notes. The total outstanding debt at September 30, 2009 under the Agreement, as amended,

and the Line of Credit was $365 million and $13 million, respectively, and $4 million in letters of credit have been issued under the facility, leaving $556 million in borrowing capacity available. The maximum amount available is subject to semi-annual redeterminations of the borrowing base, based on the value of our proved oil and gas reserves, in April and October of each year in accordance with the lenders’ customary procedures and practices. Both we and the banks have the bilateral

right to one additional redetermination each year.

Second Lien Term Loan

On April 27, 2009 we completed a $140 million second lien credit facility, with lenders from among our current lending group, with a maturity of January 16, 2013. We paid off the second lien term loan on May 29, 2009 from the proceeds of our senior unsecured notes issuance and wrote off $7.2 million in deferred loan fees for the

nine months ended September 30, 2009.

Senior Unsecured 10.25% notes due 2014

On May 27, 2009, we issued in a public offering $325 million of 10.25% senior unsecured notes due 2014 ($325 million Notes). Interest on the $325 million Notes is paid semiannually in June and December of each year. The $325 million Notes were issued at a discount to par value of 93.546%, and are carried on the balance

sheet at their amortized cost. The deferred costs of approximately $9.5 million associated with the issuance of this debt are being amortized over the five year life of the $325 million Notes. Pursuant to the terms of our senior secured credit facility, the issuance of the $325 million Notes automatically reduced our borrowing base by 25 cents per dollar of Notes issued, or approximately $81 million. We wrote off $3.3 million of deferred

loan fees during the second quarter of 2009 as a result of the decrease in our borrowing base.

On August 13, 2009, we issued in a public offering a $125 million add-on to our 10.25% senior unsecured notes due 2014 ($125 million Notes). The $125 million Notes were issued at a premium to par value of 104.75%, and are carried on the balance sheet at their amortized cost. The deferred costs of approximately $1.9 million associated

with the issuance of this debt are being amortized over the five year life of the Notes. Pursuant to the terms of our senior secured credit facility, the issuance of the $125 million Notes automatically reduced our borrowing base by 25 cents per dollar of notes issued, or approximately $31 million. We wrote off $0.3 million of deferred loan fees during the third quarter of 2009 as a result of the decrease in our borrowing base.

The $125 million Notes and the previously issued $325 million Notes will be treated as a single series of debt securities under the indenture and are carried on the balance sheet at their combined amortized cost in which the $325 million Notes discount and the $125 million Notes premium net to a discount.

Senior Subordinated 8.25% notes due 2016

In 2006, we issued in a public offering $200 million of 8.25% senior subordinated notes due 2016 (the Sub notes). Interest on the Sub notes is paid semiannually in May and November of each year. The deferred costs of approximately $5.2 million associated with the issuance of this debt are being amortized over the

ten year life of the Sub notes.

Financial Covenants

The senior secured revolving credit facility contains restrictive covenants as described above. Under our senior subordinated and senior unsecured notes as long as the interest coverage ratio (as defined) is greater than 2.5 times, we may incur additional debt. We were in compliance with all of these covenants

as of September 30, 2009.

Berry Petroleum Company

Notes to the Unaudited Condensed Financial Statements

|

As of

September 30, 2009 |

||

|

Current Ratio (Not less than 1.0) |

5.1 |

|

|

EBITDAX To Total Funded Debt Ratio (Not greater than 4.75) |

3.3 |

|

|

Interest Coverage Ratio (Not less than 2.5) |

4.0 |

|

|

EBITDAX To Senior Secured Debt Ratio (Not greater than 3.75) |

1.2 |

The weighted average interest rate on total outstanding borrowings at September 30, 2009 was 7.0%.

|

14. |

Contingencies and Commitments |

Our contractual obligations as of September 30, 2009 are as follows (in millions):

|

Total |

2009 |

2010 |

2011 |

2012 |

2013 |

Thereafter |

||||||||||||||||||||||

|

Total debt and interest |

$ | 1,385.1 | $ | 30.5 | $ | 71.8 | $ | 71.8 | $ | 430.3 | $ | 62.6 | $ | 718.1 | ||||||||||||||

|

Abandonment obligations |

43.2 | 1.3 | 2.9 | 2.9 | 2.8 | 2.8 | 30.5 | |||||||||||||||||||||

|

Operating lease obligations |

16.6 | 0.6 | 2.4 | 2.4 | 2.5 | 2.5 | 6.2 | |||||||||||||||||||||

|

Drilling and rig obligations |

38.6 | 4.4 | 8.0 | 8.0 | 18.2 | - | - | |||||||||||||||||||||

|

Firm natural gas transportation contracts |

140.1 | 4.6 | 19.1 | 19.1 | 17.8 | 15.7 | 63.8 | |||||||||||||||||||||

|

Total |

$ | 1,623.6 | $ | 41.4 | $ | 104.2 | $ | 104.2 | $ | 471.6 | $ | 83.6 | $ | 818.6 | ||||||||||||||

On July 17, 2009, we closed on the financing of our East Texas gas gathering system for $18.4 million in cash. We entered into concurrent long-term gas gathering agreements for the East Texas production which contained an embedded lease. There is no minimum payment required under these agreements. For the

first nine months of 2009, we have incurred $1.0 million under the agreements.

On June 17, 2009, we amended our natural gas firm transportation agreement with Enbridge Pipelines providing for transportation of our gas from Tex-OK to Orange County, Florida (Zone 1). The agreement provides for minimum volume of 25,000 MMBtu/d and a maximum volume of 55,000 MMBtu/D.

We have two long-term firm transportation contracts that total 35,000 MMBtu/D on the Rockies Express (REX) pipeline for gas production in the Piceance basin. We pay a demand charge for this capacity and our own production did not completely fill that capacity. To maximize the utilization of our firm transportation, we bought our

partners’ share of the gas produced in the Piceance basin at the market rate for that area and used our excess transportation to move this gas to the sales point. The pre-tax net of our gas marketing revenue and our gas marketing expense in the Statements of Operations is $0.6 million and $1.5 million for the three and nine month periods ended September 30, 2009, respectively.

In addition, Berry has signed a binding precedent agreement with El Paso Corporation for an average of 35,000 MMBtu/D of firm transportation on the proposed Ruby Pipeline from Opal, WY to Malin, OR. While it is not certain that this new line will be constructed, the expectation is that the project will proceed and be in service

by 2011. As part of this agreement and in order to access the Ruby pipeline, we also secured firm transportation from the Piceance basin to Opal.

In February 2007, we entered into a multi-staged crude oil sales contract with a refiner for our Uinta basin light crude oil. Under the agreement, the refiner began purchasing 3,200 Bbl/D in July 2007. The refiner has increased its total capacity to 5,000 Bbl/D as provided in our contract. As operator we deliver all produced volumes under

our sales contracts, although our working interest partners or royalty owners may take their respective volumes in kind and market their own volumes. Gross oil production averaged approximately 3,100 BOE/D in the quarter ended September 30, 2009.

On August 13, 2009, we issued in a public offering a $125 million add-on to our 10.25% senior notes due 2014.

On May 27, 2009, we issued in a public offering $325 million of 10.25% senior notes due 2014. Interest on the $325 million Notes is paid semiannually in June and December of each year.

Berry Petroleum Company

Notes to the Unaudited Condensed Financial Statements

In December 2008, Flying J, Inc., and its wholly owned subsidiary Big West Oil and its wholly owned subsidiary BWOC filed for bankruptcy protection under Chapter 11 of the United States Bankruptcy Code. Also in December 2008, BWOC informed the Company that it was unable to receive the Company’s California production. Included

in our allowance for doubtful accounts is $38.5 million due from BWOC. Of the $38.5 million due from BWOC, $11.8 million represents 20 days of our December crude oil sales, an administrative claim under the bankruptcy proceedings, and $26.7 million represents November and the balance of December crude oil sales which would have the same priority as other general unsecured claims. BWOC will also be liable to us for damages under this contract. We have guarantees from Big West Oil and from

Flying J, Inc. in the amount of $75 million each, in the event that our claim is not fully collectible from BWOC. While we believe that we may recover some or all of the amounts due from BWOC, the data received from the bankruptcy proceedings to date has not provided us with adequate data from which to make a conclusion that any amounts will be collected.

We have no material accrued environmental liabilities for our sites, including sites in which governmental agencies have designated us as a potentially responsible party, because it is not probable that a loss will be incurred and the minimum cost and/or amount of loss cannot be reasonably estimated. However, because of the uncertainties

associated with environmental assessment and remediation activities, future expense to remediate the currently identified sites, and sites identified in the future, if any, could be incurred. Management believes, based upon current site assessments, that the ultimate resolution of any matters will not result in substantial costs incurred. We are involved in various other lawsuits, claims and inquiries, most of which are routine to the nature of our business. In the opinion of management, the resolution of these

matters will not have a material effect on our financial position, or on the results of operations or liquidity.

Certain of our royalty payment calculations are being disputed. We believe that our royalty calculations are in accordance with applicable leases and other agreements. However, the disputed amounts that we may be required to pay are up to approximately $6 million.

In July 2009, we received a notice of proposed civil penalty from the Bureau of Land Management (BLM) related to the Company’s alleged non-compliance during 2007 with regulations relating to the operation and position of certain valves in our Uinta Basin operations. The proposed civil penalty was $69.6 million and reflects

the theoretical maximum penalty amount under applicable regulations, absent mitigating factors. In 2007 we immediately remediated the instances of non-compliance, cooperated fully with the BLM’s investigation and we believe no production was lost, all royalties were paid and there was no harm to the environment. Due to the above mitigating factors, among others, we believe this matter will be resolved by the payment of a penalty that will not exceed $2.1 million and accrued such amount

in the second quarter of 2009.

During the California energy crisis in 2000 and 2001, we had electricity sales contracts with various utilities and a portion of the electricity prices paid to us under such contracts from December 2000 to March 27, 2001 has been under a degree of legal challenge since that time. It is possible that we may have a liability pending

the final outcome of the CPUC proceedings on the matter. There are ongoing proceedings before the CPUC in which Edison and PG&E are seeking credit against future payments they are to make for electricity purchases based on retroactive adjustments to pricing under contracts with us. Whether or not retroactive adjustments will be ordered, how such adjustments would be calculated and what period they would cover are too uncertain to estimate at this time.

|

15. |

Subsequent Events |

The Company evaluates subsequent events through the date the financial statements are issued, which for the quarterly period ended September 30, 2009, is October 30, 2009. No subsequent events requiring disclosure were identifited by the Company.

Berry Petroleum Company

Management's Discussion and Analysis of Financial Condition and Results of Operations

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

General. The following discussion provides information on the results of operations for the three and nine months ended September 30, 2009 and 2008 and our financial condition, liquidity and capital resources as of September 30, 2009. The unaudited financial statements

and the notes thereto contain detailed information that should be referred to in conjunction with this discussion.

The profitability of our operations in any particular accounting period will be directly related to the realized prices of oil, gas and electricity sold, the type and volume of oil and gas produced and electricity generated and the results of development, exploitation, acquisition, exploration and hedging activities. The realized prices for

natural gas and electricity will fluctuate from one period to another due to regional market conditions and other factors, while oil prices will be predominantly influenced by global supply and demand. The aggregate amount of oil and gas produced may fluctuate based on the success of development and exploitation of oil and gas reserves pursuant to current reservoir management. The cost of natural gas used in our steaming operations and electrical generation, production rates, labor, equipment costs, maintenance

expenses, and production taxes are expected to be the principal influences on operating costs. Accordingly, our results of operations may fluctuate from period to period based on the foregoing principal factors, among others.

Overview. We seek to increase shareholder value through consistent growth in our production and reserves, both through the drill bit and acquisitions. We strive to operate our properties in an efficient manner to maximize the cash flow and earnings of our assets. The

strategies to accomplish these goals include:

|

|

· |

Maximize production from our base oil assets |

|

|

· |

Grow oil production from our inventory of organic development projects |

|

|

· |

Increase natural gas production that will meet the growing demand for steam generation |

|

|

· |

Acquire additional resources with an emphasis on crude oil |

Notable Third Quarter Items.

|

|

· |

Achieved production averaging 28,417 BOE/D, of which 68% is crude oil production, with $22 million of capital investment |

|

|

· |

Increased Diatomite net production to an average of 3,119 BOE/D, up 49% from the third quarter of 2008 |

|

|

· |

Secured twelve month contracts for approximately 90% of our California crude oil |

|

|

· |

Issued a $125 million add-on to our 10.25% senior unsecured notes due in 2014 with a yield of 9% |

|

|

· |

Paid down $78 million of additional debt and increased liquidity to approximately $550 million |

|

|

· |

Completed the sale of our East Texas midstream assets for $18 million |

|

|

· |

Tested our new completion method in the Piceance basin, delivering a 25% improvement compared to our historical field average |

|

|

· |

Received category exemption allowing 25 wells to be drilled in the Uinta basin in Ashley Forest |

Notable Items and Expectations for the Fourth Quarter and Full Year 2009.

|

|

· |

Completed our credit facility borrowing base redetermination and reconfirmed our $938 million borrowing base |

|

|

· |

Initiate a steam flood pilot on the McKittrick, California property |

|

|

· |

Expect to drill our first East Texas Haynesville well during the fourth quarter of 2009 |

|

|

· |

Expect production to average approximately 30,000 BOED for the full year 2009 |

Overview of the Third Quarter of 2009. We had net income from continuing operations of $18 million, or $0.40 per diluted share, and cash provided from operations was $89 million in the third quarter of 2009. Net income includes $1 million from the sale

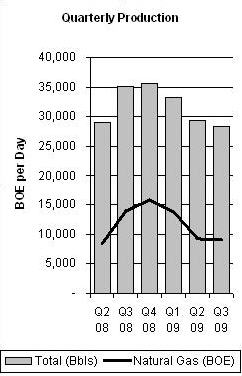

of crude oil inventory. We drilled 32 gross wells, and capital expenditures excluding property acquisitions totaled $22 million. We achieved average production of 28,417 BOE/D in the third quarter of 2009.

Acquisitions. In June 2009, we acquired the Section 21Z property in McKittrick, California. We believe this acquisition provides us with another opportunity to increase our crude oil production and reserves with potential similar to our Poso Creek

asset. We also acquired deep rights to one of the leases in our Darco property in East Texas, providing us with an additional 13 Haynesville horizontal locations, and increased our interest at Garden Gulch in the Piceance.

Berry Petroleum Company

Management's Discussion and Analysis of Financial Condition and Results of Operations

Asset Dispositions.

On July 17, 2009, we completed the sale of our East Texas gas gathering system for $18.4 million in cash. See Note 8 to the unaudited financial statements.

On March 3, 2009, we entered into an agreement to sell our DJ basin assets and related hedges for $154 million before customary closing adjustments. The closing date of the sale of our DJ basin assets was April 1, 2009. We recorded an impairment charge associated with the sale of $9.6 million during the first quarter of 2009. Post

closing adjustments recorded in the second and third quarters of 2009 totaled $0.5 million income, net of tax. The total loss on sale was recorded within “(Loss) income from discontinued operations, net of tax,” on the condensed statements of operations for the nine months ended September 30, 2009.

Results of Operations. The following results from continuing operations are in millions (except per share data) for the three and nine month periods ended:

|

Three months ended, |

Nine months ended, |

|||||||||||||||||||

|

Sept 30, 2009 |

Sept 30, 2008 |

June 30, 2009 |

Sept 30, 2009 |

Sept 30, 2008 |

||||||||||||||||

|

Sales of oil |

$ | 109 | $ | 146 | $ | 103 | $ | 311 | $ | 423 | ||||||||||

|

Sales of gas |

18 | 48 | 16 | 63 | 92 | |||||||||||||||

|

Total sales of oil and gas |

$ | 127 | $ | 194 | $ | 119 | $ | 374 | $ | 515 | ||||||||||

|

Sales of electricity |

9 | 18 | 6 | 26 | 51 | |||||||||||||||

|

Gas Marketing |

5 | 13 | 5 | 18 | 28 | |||||||||||||||

|

Gain (loss) on derivative |

1 | 1 | (31 | ) | 7 | - | ||||||||||||||

|

Interest and other income, net |

1 | 1 | 1 | 2 | 3 | |||||||||||||||

|

Total revenues and other income |

$ | 143 | $ | 227 | $ | 100 | $ | 427 | $ | 597 | ||||||||||

|

Net income (loss) from continuing operations |

$ | 18 | $ | 50 | $ | (13 | ) | $ | 47 | $ | 133 | |||||||||

|

Diluted earnings (loss) per share from continuing operations |

$ | 0.40 | $ | 1.08 | $ | (0.28 | ) | $ | 1.03 | $ | 2.90 | |||||||||

Our revenues may vary significantly from period to period as a result of changes in commodity prices and/or production volumes. Crude oil sales in the three months ended September 30, 2009 were higher compared to the three months ended June 30, 2009 resulting from realized price increases of 1%, sales volume increases of 6% and

we recognized revenue of $2.7 million resulting from the sale of 50,000 barrels of crude oil inventory. The decrease in crude oil revenue when compared to the third quarter of 2008 is primarily the result of a 24% decrease in realized prices. Natural gas revenues increased from the quarter ended June 30, 2009 as a result of a 12% increase in realized prices and a 2% decrease in volumes from our Piceance and Uinta properties where no capital activity occurred during the quarter. Natural

gas revenues were lower in the third quarter of 2009 compared to the third quarter of 2008 primarily due to a 58% decrease in realized prices.

|

|

Berry Petroleum Company

Management's Discussion and Analysis of Financial Condition and Results of Operations

Operating data. The following table is for the three months ended:

|

September 30, 2009 |

% |

September 30, 2008 |

% |

June 30, 2009 |

% |

|||||||||||||||||||

|

Heavy Oil Production (Bbl/D) |