Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - AMERALIA INC | ex32_2.htm |

| EX-31.1 - EXHIBIT 31.1 - AMERALIA INC | ex31_1.htm |

| EX-32.1 - EXHIBIT 32.1 - AMERALIA INC | ex32_1.htm |

| EX-31.2 - EXHIBIT 31.2 - AMERALIA INC | ex31_2.htm |

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

|

FORM

10-K

|

|

|

T

|

ANNUAL

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

|

For

the fiscal year ended June 30, 2009

OR

|

|

£

|

TRANSITION

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

|

For

the transition period

from to

|

Commission file number:

000-15474

|

|

AMERALIA, INC.

|

||

|

(Exact

Name of Registrant as Specified in its Charter)

|

||

|

Utah

|

87-0403973

|

|

|

(State

of other jurisdiction of incorporation or organization)

|

(I.R.S.

Employer Identification No.)

|

|

|

|

|

|

|

3200

County Road 31

|

|

|

|

Rifle, Colorado

|

81650

|

|

|

(Address

of principal executive offices)

|

(Zip

Code)

|

|

|

(720) 876-2373

|

|

(Registrant’s

Telephone Number, including Area

Code)

|

SECURITIES

REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT: None

|

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF

THE ACT: Common Stock, $0.01 par

value

|

|

Indicate

by check mark if the registrant is a well-known seasoned issuer, as

defined in Rule 405 of the Securities Act.

|

|

Yes

£ NoT

|

|

Indicate by check mark if the registrant is not

required to file reports pursuant to Section 13 or Section 15(d) of the

Act. Yes £ No T

|

|

Indicate by checkmark whether the registrant (1)

has filed all reports required to be filed by Section 13 or 15(d) of the

Securities Exchange Act of 1934 during the preceding 12 months (or for

such shorter period that the registrant was required to file such

reports), and (2) has been subject to such filing requirements for the

past 90 days. Yes T No £

|

|

Indicate by checkmark if disclosure of delinquent

filers pursuant to Item 405 of Regulation S-K is not contained herein, and

will not be contained, to the best of the registrant’s knowledge, in

definitive proxy or information statements incorporated by reference in

Part III of this Form 10-K or any amendment to the Form 10-K. £

|

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer, or a smaller reporting

company. See the definitions of “large accelerated

filer,” “accelerated filer” and “smaller reporting company” in Rule

12b-2 of the Exchange Act (Check one):

|

Large

Accelerated Filer £

|

Accelerated

Filer £

|

|

|

Non-Accelerated Filer £

|

Smaller Reporting Company T

|

|

Indicate by check mark whether the registrant is a

shell company (as defined in Rule 12b-2 of the

Act). Yes £ No T

|

|

State the

aggregate market value of the voting and non-voting common equity held by

non-affiliates computed by reference to the price at which the common

equity was last sold, or the average bid and asked price of such common

equity, as of the last business day of the registrant’s most recently

completed second fiscal quarter: $8,872,940 as of December 31,

2008, based on the last sale price on the OTCBB of

$0.85.

|

|

The number of shares of the Registrant’s Common

Stock, $0.01 par value, outstanding as of September 21, 2009 was

66,293,696.

|

Cautionary

Note RegardingForward

Looking Statements

The

information in this Annual Report on Form 10-K contains forward-looking

statements within the meaning of the Private Securities Litigation Reform Act of

1995. These forward-looking statements involve risks and uncertainties regarding

the intent, belief or current expectations of the Company, its directors or its

officers. Any statements contained herein that are not statements of

historical facts may be deemed to be forward-looking statements. In some cases,

you can identify forward-looking statements by terminology such as "may",

"will", "should", "expect", "plan", "intend", "anticipate", "believe",

"estimate", "predict", "potential" or "continue", the negative of such terms or

other comparable terminology. Actual events or results may differ materially. In

evaluating these statements, you should consider various factors, including the

risks we outline from time to time in other reports we file with the Securities

and Exchange Commission (the “SEC”) and under the heading “Risk Factors” in this

Annual Report. These factors may cause our actual results to differ materially

from any forward-looking statement. We disclaim any obligation to publicly

update these forward-looking statements, or disclose any difference between our

actual results and those reflected in these statements, except as required by

law. Given these uncertainties, readers are cautioned not to place undue

reliance on such forward-looking statements.

We

qualify all forward-looking statements in this Annual Report by the foregoing

cautionary note.

Cautionary Note to US

Investors

The

SEC limits disclosure for U.S. reporting purposes to mineral deposits that a

company can economically and legally extract or produce. The reader is cautioned

that the term "resource" is not recognized by SEC guidelines for disclosure of

mineral properties.

Terminology

In

this report “tons” means U.S. Short Tons unless otherwise

specified.

|

Item

|

Page

|

|

|

PART

1

|

||

|

1

|

3 | |

| 5 | ||

| 6 | ||

| 7 | ||

| 9 | ||

| 9 | ||

| 12 | ||

| 16 | ||

| 20 | ||

|

1A

|

21 | |

|

1B

|

24 | |

|

2

|

25 | |

|

3

|

25 | |

|

4

|

25 | |

|

PART

11

|

||

|

5

|

26 | |

|

6

|

27 | |

|

7

|

28 | |

|

8

|

33 | |

|

9

|

33 | |

|

9A(T)

|

34 | |

|

9B

|

34 | |

|

PART

111

|

||

|

10

|

35 | |

|

11

|

39 | |

|

12

|

42 | |

|

13

|

43 | |

|

14

|

47 | |

|

15

|

48 | |

| F-1 | ||

PART

I

|

ITEM 1.

|

DESCRIPTION OF

BUSINESS

|

The

terms “we,” “us,” “our,” “AmerAlia” and the “Company” used in this Annual Report

refer to AmerAlia, Inc. unless otherwise indicated.

AmerAlia,

Inc. was incorporated in Utah on June 7, 1983 as Computer Learning Software,

Inc. and renamed AmerAlia, Inc. in January 1984.

Our

business is to identify and develop natural resource assets. AmerAlia

actively participates in the management and development of the natural sodium

bicarbonate resources and water rights owned by our former direct subsidiary,

Natural Soda Holdings, Inc. (“NSHI”) and NSHI’s wholly-owned subsidiary, Natural

Soda, Inc. (“NSI”).

Currently,

we own 18% of NSHI. We are attempting to acquire some or all of the

outstanding shares of NSHI we do not own from Sentient (defined below) so that

we can secure majority ownership. If we cannot achieve this objective

we shall likely have to register as an investment company or seek alternative

means of complying with the Investment Company Act. We are discussing

this issue with Sentient and the Securities and Exchange

Commission.

NSI

owns various water rights in the Piceance Creek Basin in northwest Colorado, a

part of the Colorado River drainage system. These various rights

allow NSI to draw up to a maximum of 108,812 acre feet (35.46 million gallons)

annually and to store up to 7,980 acre feet of water.

NSHI

and NSI also own the largest Bureau of Land Management (“BLM”) leases in the

Piceance Creek Basin which contains the largest known deposits of nahcolite,

naturally occurring sodium bicarbonate, in the world. NSHI’s and

NSI’s leases are located near the depositional center of the Piceance Creek

Basin where the nahcolite beds are thickest and most

concentrated. Consequently, we believe these deposits are unique and

capable of producing sodium bicarbonate and related sodium products for many

generations.

NSHI

first acquired its interest in a lease known as the Rock School lease in

1989. NSI acquired its operating assets and sodium leases in 2003, an

acquisition financed by loans from a trust and a fund (the “Sentient Entities”)

managed by Sentient Asset Management, an international private equity group

specializing in the development of natural resources.

NSI’s

business is to produce and sell natural sodium bicarbonate, commonly known as

baking soda, for use in a wide variety of products and activities. NSI’s

immediate objectives are, firstly, to be a low cost producer of sodium

bicarbonate and to leverage that low cost advantage to achieve superior profit

margins; and secondly, to profitably utilize its water assets.

Deposits

of oil shale lie below, above and are interspersed within the nahcolite

contained within the sodium leases. We do not have any rights to

recover oil shale but NSHI and NSI plan to apply for leases to exploit all or

part of this oil shale if and when the United States government formulates

procedures for that purpose. Shell Frontier Oil & Gas Co.

(“Shell”) has three research, development and demonstration leases adjacent to

NSI’s sodium leases. A Shell fact sheet, “Shell Exploration &

Production Technology - to secure our energy future – Mahogany Research Project”

reports an estimated potential recovery rate of up to one million barrels of oil

per surface acre. If we obtain the right to exploit all or part of

this oil shale, we plan to independently determine possible recovery rates and

attempt to develop an economically feasible plan to recover oil from the oil

shale resource contained within the area where NSHI’s and

NSI’s sodium leases are located.

Figure

1: Natural Soda’s Plant Operations, Rifle, Colorado

As

discussed more fully below, on September 25, 2008, AmerAlia, NSHI, NSI, Bill H.

Gunn and Robert van Mourik, directors and executive officers of AmerAlia

(collectively the “AmerAlia Parties”) entered into a “Restructuring Agreement”

with the Sentient Entities. Previously, NSHI owned 46.5% of

NSI. Prior to the closing, the Sentient Entities transferred their

various interests to Sentient USA Resources Fund (“Sentient”). As a

result of the restructuring, NSI became a wholly-owned subsidiary of NSHI,

Sentient converted its loans to NSHI into NSHI equity and AmerAlia’s ownership

in NSHI was reduced from 100% to 18%. Sentient converted its loans to

AmerAlia into additional common stock of AmerAlia. All debts

previously owed to Sentient by NSHI and AmerAlia were

cancelled. AmerAlia also received approximately $10 million in cash,

settled approximately $12 million of debt, terminated indemnification rights

relating to the extinguishment of a $9.9 million bank loan and extinguished

other obligations in exchange for the issue of shares of its common stock as

discussed more fully below. As a result after repaying debts and

other obligations, AmerAlia had approximately $4,300,000 in cash at June 30,

2009. Sentient now owns 72.4% of AmerAlia’s common

stock. When combined with its additional purchase rights, Sentient’s

beneficial ownership is 74.5%. Pursuant to the Restructuring

Agreement, Sentient has the right to nominate Peter Cassidy and up to three

additional suitably qualified persons for election by the shareholders as

directors of AmerAlia.

OVERVIEW

OF CORPORATE STRUCTURE

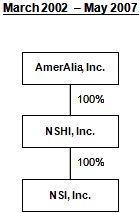

Prior

to May 2007, we owned 100% of the outstanding common stock of NSHI, which in

turn owned 100% of the outstanding common stock of NSI, as shown

below. NSI is an operating company that produces and sells sodium

bicarbonate (baking soda). NSI has several active mineral leases, owns water

rights and a sodium bicarbonate production facility in the Piceance Creek Basin

area of Colorado.

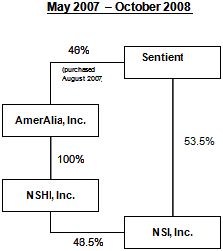

In

2003, the Sentient Entities provided NSHI with short-term financing which was

finalized in 2004. In May 2007, the Sentient Entities converted a

portion of the debt owed by NSHI and NSI into a 53.5% equity interest in

NSI. In August 2007, the Sentient Entities purchased approximately

46% of the equity in AmerAlia from a major shareholder of AmerAlia, and also

acquired additional debt obligations of AmerAlia from the same major

shareholder. These events are reflected in the ownership structure

shown below.

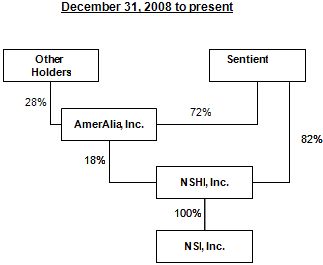

As

part of a restructuring transaction in October 2008:

|

|

·

|

the

Sentient Entities transferred their various interests to

Sentient;

|

|

|

·

|

NSI

became a wholly-owned subsidiary of

NSHI;

|

|

|

·

|

Sentient

converted its loans to NSHI into NSHI equity and AmerAlia’s ownership in

NSHI was reduced from 100% to 18%;

and

|

|

|

·

|

Sentient

converted its loans to AmerAlia into additional common stock of

AmerAlia.

|

This

reorganization resulted in the ownership structure shown below.

In

connection with this restructuring, AmerAlia also received approximately $10

million in cash, settled approximately $12 million of debt, terminated

indemnification rights relating to the extinguishment of a $9.9 million bank

loan and extinguished other obligations in exchange for the issue of 48,961,439

shares of its common stock.

Pursuant

to the Restructuring Agreement, Sentient has the right to nominate Peter

Cassidy, the Chairman of Sentient Group, and up to three additional suitably

qualified persons for election by the shareholders as directors of

AmerAlia.

OUR

PARTICIPATION IN NSHI & NSI

We

have two executive officers, Bill H Gunn, our Chairman and CEO, and Robert van

Mourik, our EVP and CFO. Both officers actively participated in the

development of the Rock School lease and its acquisition, followed by the

negotiations and acquisition of the sodium bicarbonate operations now held by

NSI.

Bill

H. Gunn has been and continues to be the executive chairman of

NSI. He was also a director and president of NSHI until June 2009

when he became vice president. He leads and directs NSI’s management

team including production activities, sales, customer service, distribution, HR,

business planning and budgeting and managing relationships with government

departments and agencies.

Robert

van Mourik is primarily involved in financial functions, internal controls and

procedures, budgeting, planning, reporting and audits. He has been

and continues to be CFO of NSI. He was also the CFO of NSHI until

June 2009. He continues to assist in the oversight of its accounting

functions.

The

board of directors of NSHI comprises Peter Cassidy, Bill H. Gunn, Brad Bunnett,

Stephen Dunn and Johanna Druez. Peter Cassidy is Chairman and also

President of NSHI. Brad Bunnett is President of

NSI. Stephen Dunn and Johanna Druez are Sentient

representatives.

RESTRUCTURING

TRANSACTIONS

On

September 25, 2008, AmerAlia, NSHI, NSI, Bill H. Gunn and Robert van Mourik,

directors and executive officers of AmerAlia (collectively the “AmerAlia

parties”) entered into a Restructuring Agreement with the Sentient

Entities. Previously, NSHI owned 46.5% of NSI.

On

October 31, 2008, the AmerAlia Parties and the Sentient Entities completed an

Amendment to the Restructuring Agreement. As a result of the

amendment, the restructuring transaction was divided into two

closings. In accordance with the amended agreement the first closing

occurred as of October 31, 2008. Prior to the first closing, the

Sentient Entities transferred their various interests to

Sentient. The second closing occurred as of December 31,

2008. In the first and second closings:

|

|

·

|

Sentient

exchanged all its NSHI debentures and all accrued interest thereon, its

one share of NSHI common stock and its 53.5% of the common stock of NSI

for 82% of the issued common stock of

NSHI;

|

|

|

·

|

AmerAlia

exchanged its NSHI debentures and all accrued interest thereon and its

NSHI preferred stock for 12.9% of the issued common stock of NSHI, giving

AmerAlia an aggregate ownership position in NSHI of

18%;

|

|

|

·

|

Intercompany

loans between AmerAlia and NSHI were

extinguished;

|

|

|

·

|

Sentient’s

indemnification rights relating to the extinguishment of a $9.9 million

bank loan were terminated; and

|

|

|

·

|

Sentient

received an aggregate of 40,024,675 shares of AmerAlia common stock as

follows:

|

|

|

o

|

27,427,406

shares of AmerAlia common stock for a total purchase price of

$9,873,866;

|

|

|

o

|

6,619,469

shares in satisfaction of various promissory notes;

and

|

|

|

o

|

5,977,800

shares in satisfaction of debts, rights and obligations acquired from the

Mars Trust in August 2007 at the first

closing.

|

Sentient

no longer holds any debt in either AmerAlia or NSHI. All debentures

issued by NSHI have been cancelled. NSI is now a wholly-owned

subsidiary of NSHI.

AmerAlia

extinguished other obligations in exchange for the issue of shares of our common

stock as discussed more fully below and in our financial

statements. Sentient now owns 72.4% of AmerAlia’s common

stock. When combined with its limited additional purchase rights,

Sentient’s beneficial ownership is 74.5%.

Repayment

of Obligations Due to Officers and Directors

In

September 2008, we issued 495,820 shares of restricted common stock to the Karen

O. Woolard Trust, an affiliate of our director, Robert C. Woolard, in

satisfaction and cancellation of a promissory note and accrued interest with a

total value of $1,175,889.

On

October 31, 2008, in conjunction with the Restructuring Agreement, our officers

and directors and their affiliates subscribed for shares of AmerAlia common

stock in satisfaction of various notes and accrued compensation as

follows:

|

Shareholder

|

Relationship

|

Number of

Shares

|

Consideration

|

|||||||

|

Bill

H Gunn

|

Chairman

& CEO

|

700,000 | $ | 252,000 | ||||||

|

Robert

van Mourik

|

Director,

EVP & CFO

|

250,000 | 90,000 | |||||||

|

James

V Riley Trust

|

Affiliate

of James V. Riley, Director

|

1,583,333 | 570,000 | |||||||

|

J.

Jeffrey Geldermann

|

Director

|

1,003,400 | 361,224 | |||||||

|

Karen

O. Woolard Trust

|

Affiliate

of Robert C. Woolard,

Director

|

925,000 | 333,000 | |||||||

|

Glendower

Investments Pty

Ltd

|

Affiliate

of Neil E. Summerson,

Director

|

153,000 | 55,080 | |||||||

|

Geoffrey C. Murphy

|

Director

|

486,125 | 175,005 | |||||||

|

TOTALS:

|

5,100,858 | $ | 1,836,309 | |||||||

Issues

of Shares to settle Debt Obligations

In

addition to the shares issued to Sentient, our officers and our directors as

described above, we issued 2,433,706 shares to settle promissory notes and

accrued interest valued at $876,134 to unaffiliated accredited

investors.

Uses

of Cash

The

$9,873,866 we received as cash was used to pay outstanding obligations and

provide working capital as set forth in the table below. The working

capital includes a reserve solely to fund AmerAlia’s share of anticipated

capital calls by NSHI, AmerAlia’s share of which is $2,880,000. As

discussed at Item 13, we contributed $450,000 to our share of a capital call in

July 2009.

|

Recipient

|

Relationship

|

Nature

of

Obligation

|

Amount

Paid

|

|||||

|

Karen

O. Woolard Trust

|

Affiliate

of Robert C. Woolard,

Director

|

Balance

of Note &

interest

|

$ | 977,188 | ||||

|

Robert

van Mourik

|

Director,

EVP & CFO

|

Accrued

compensation advances

& expenses (1)

|

920,064 | |||||

|

Bill

H. Gunn

|

Director

& CEO

|

Accrued

compensation advances

& expenses (2)

|

794,657 | |||||

|

Ahciejay

Pty Ltd

|

Affiliate

of Robert

van Mourik

|

Promissory

note &

interest (3)

|

169,816 | |||||

|

James

V Riley Trust

|

Affiliate

of James

V. Riley, Director

|

Promissory

note interest

& directors fees

|

151,524 | |||||

|

J.

Jeffrey Geldermann

|

Director

|

Promissory

note interest

& directors fees

|

95,881 | |||||

|

Neil

E. Summerson

|

Director

|

Director’s

fees &

expenses

|

54,215 | |||||

|

Geoffrey

C. Murphy

|

Director

|

Director’s

fees &

expenses

|

36,550 | |||||

|

Robert

C. Woolard

|

Director

|

Directors

fees

|

23,792 | |||||

|

Note

holders

|

Unrelated

parties

|

Notes

& interest

|

1,983,801 | |||||

|

Various

creditors, taxes and

working capital

|

4,666,378 | |||||||

|

TOTAL:

|

$ | 9,873,866 | ||||||

|

1.

|

Includes

accrued outstanding compensation and related employee withholding taxes,

reimbursement of expenses and advances and current year

compensation.

|

|

2.

|

Includes

accrued outstanding compensation and related employee withholding taxes,

reimbursement of expenses, advances and current year

compensation.

|

|

3.

|

Includes

withholding taxes.

|

Shareholders

Agreement

The

Restructuring Agreement included an undertaking by the AmerAlia Parties and the

Sentient Parties to terminate the existing Securityholders

Agreement. Accordingly, NSHI, AmerAlia and Sentient entered into a

new Shareholders Agreement dated October 31, 2008. The agreement

contains provisions restricting transfers of shares by shareholders and a right

of first refusal on sales to third parties of the shares held by

AmerAlia. Under the agreement, if Sentient decides to sell its NSHI

shares, it can force AmerAlia to sell its NSHI shares on the same terms and

conditions as Sentient, or “drag-along” AmerAlia, subject to any required

approval by the AmerAlia shareholders. The agreement also provides

for additional funding of NSHI on a pro rata basis by AmerAlia and

Sentient. Although Sentient does not have any contractual obligation

to fund any capital contributions, if Sentient does fund its pro rata portion,

it does have the option to fund any pro rata capital contribution that AmerAlia

does not make, which would even further dilute AmerAlia’s ownership of

NSHI.

ACTIVITIES

OF NSHI & NSI

|

1.

|

Sodium Leases

|

Sodium

Leases and Operations

Nahcolite,

a naturally occurring mineral form of sodium bicarbonate, is only known to exist

in large quantities in the Piceance Creek Basin in northwest

Colorado. Access to these deposits is governed by the BLM, a part of

the Department of Interior, which has granted some leases to allow recovery of

the sodium bicarbonate. NSI owns four sodium leases, collectively

known as the Wolf Ridge Mining Unit, and NSHI owns the adjoining Rock School

lease.

The

geology of the Piceance Creek Basin has been described and discussed in two

reports. In March 1983, Rex D. Cole, Ph.D. Consulting Geologist,

Grand Junction, Colorado, issued a report “Geologic Framework of Federal Sodium

Lease C-0118326, Piceance Creek Basin, Colorado”. On Page 3 of

“Summary and Conclusions” the report states “Total nahcolite resources for the

lease area are between 6 and 8 billion tons.” The lease to which Cole

refers (C-0118326) is the

Wolf Ridge lease, one of the four leases comprising the Wolf Ridge Mining Unit

being mined by NSI; therefore, NSI’s holdings extend beyond the particular lease

to which Cole refers.

A

second report by Cole, Daub & Weston entitled “Review of Geology, Mineral

Resources, and Ground-Water Hydrology of the Green River Formation,

North-Central Piceance Creek Basin, Colorado” was published by the Grand

Junction Geological Society, Grand Junction, Colorado, in 1995. The

authors state “…subsequent drilling established that the world’s largest

deposits of naturally occurring sodium bicarbonate (nahcolite) are present in

the Piceance Creek Basin” and “…the estimated in-situ resources of nahcolite and

dawsonite are placed at 29 and 19 billion tons, respectively”. A more

recent USGS Nahcolite and Dawsonite Piceance Creek Basin resource estimate in

2009 placed the nahcolite at 43.3 billion short tons. However, NSHI’s

and NSI’s leases only cover a portion of this resource of which we believe only

a portion will be recoverable.

Figure

2: NSHI’s and NSI’s Sodium Leases are located

about

54 miles northwest of Rifle, Colorado

We

first acquired an interest in the Rock School lease in Rio Blanco County,

Colorado in 1989 and subsequently acquired it in 1992. We have never

produced sodium bicarbonate from the Rock School lease which is now owned by

NSHI and remains an untapped asset.

NSHI’s

and NSI’s leases are located near the depositional center of the Piceance Creek

Basin where the nahcolite beds are thickest with the highest concentration of

nahcolite. The Wolf Ridge Mining Unit leases issued to NSI cover a total of

8,223 acres. When combined with the Rock School lease issued to NSHI,

the leases cover a total of 9,543 acres.

Each

of the four Wolf Ridge leases and the Rock School lease was renewed effective

July 1, 2001 for a ten year term with a preferential right to subsequent

renewals provided that sodium is being produced in paying

quantities. Under the unit agreement, production in paying quantities

from one lease is sufficient to extend all four Wolf Ridge

leases. The leases bear a production royalty payable to the federal

government of 2.0% of the gross value of the production exiting the processing

plant. Each of these leases contains covenants to protect the in situ

oil shale, water, and historical resources. We believe BLM general practice is

that the conduct of NSHI and NSI’s activities will be sufficient to enable lease

renewals. However, there can be no assurance that the conduct of such

activities or additional development will be sufficient for the BLM to grant

further lease renewals. NSHI may have to undertake some additional

development in order to renew the Rock School lease.

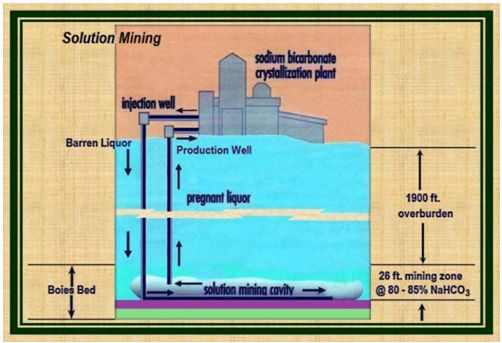

Production

Cavities and Solution Mining

The

Wolf Ridge leases contain the unique Boies Bed, the richest and most

economically recoverable bed of nahcolite in the Piceance Creek

Basin. The Boies Bed contains an interval at an approximate depth of

1,900 feet that, while variable, averages approximately 30 feet thick with

nahcolite constituting over 65% of the material in that

interval. Solution mining requires pumping hot water into the

nahcolite-bearing rock zone, the nahcolite dissolves and is pumped to the

surface in near saturated solution known as pregnant liquor and brought into the

plant for the sodium bicarbonate to be crystallized, dried, graded and bagged in

50 pound or 2,000 pound bags or stored for bulk sales. The remaining

underground cavity comprises a honeycomb like rock rubble. The spent

liquor is reheated and recycled underground to continue the solution mining

process. The dried sodium bicarbonate is then screened and stored

Figure

3: Samples of nahcolite

NSI’s

operations to recover sodium products from these leases are governed by a BLM

approved mine plan defining our cavity program to support our solution mining

process. NSI has invested $6,566,202 developing the well field and

its cavities. In the past, as the need for an additional cavity has

arisen, NSI has proposed a new cavity in accordance with the mine plan and after

a period of consultation, the BLM has authorized the recovery of an amount of

additional sodium bicarbonate. Consequently, NSI has been able to

maintain its operations and retain access to this resource. The

following table illustrates this process for the last four

years:

|

Authorized Recovery (tons)

|

||||||

|

Year ending

|

Additions

|

Production

|

Balance

|

|||

|

June

30, 2005

|

467,271

|

|||||

|

June

30, 2006

|

-

|

(90,369)

|

376,902

|

|||

|

June

30, 2007

|

-

|

(98,145)

|

278,757

|

|||

|

June

30, 2008

|

150,000

|

(100,189)

|

328,568

|

|||

|

June

30, 2009

|

(99,293)

|

229,275

|

||||

As

the above table shows, NSI had authority, as of June 30, 2009, to recover up to

229,275 tons of sodium bicarbonate from the three existing connected cavities

denominated as 5H, 6H and 7H. In early September 2009 NSI completed a

new cavity, 10H, at a cost of approximately $2,750,000 that increased NSI’s

authorized recovery by 385,000 tons. However we only expect to

recover approximately 308,000 tons from this new cavity. NSI is

currently embarking on another drilling program at an estimated cost of

$2,400,000 to establish another new well, 11H, and expects to secure a further

increase of approximately 300,000 tons to its authorized recovery to ensure a

reliable supply of feed liquor to its plant for several years. Along

with these wells, NSI has installed an additional pipeline to carry the

recovered liquor to the plant at a cost of approximately

$715,000. This pipeline will support 10H, 11H and an additional

future cavity.

These

activities are part of an exploration and production cavity installation program

which is expected to cost approximately $9 million over time. While NSI is

generating sufficient free cash flow to provide for most of this expenditure,

NSI needed additional financing to fund the initial

investment. Consequently, AmerAlia and Sentient completed a

Contribution Agreement and we advanced $450,000 as our share of $2,500,000 NSHI

raised from ourselves and Sentient in July 2009. See Item 15, Exhibit

10.56.

During

the last year, some occasional, expected and normal partial cavity collapses

occurred in cavities 5H and 6H which had the effect of lowering the brine grade

of the pregnant liquor causing a lowered level of product yield from those two

cavities and a consequent need to increase plant liquor throughput to maintain

the production rate. Brine grade and liquor throughput determine the

production rate of our cavities and these vary from time to

time. The new cavities will assist in safeguarding future

production and provide additional production flexibility to enable NSI to

optimise its production rates.

Figure

4: A general illustration of the solution mining process

Products

& Other Potential Uses

Sodium

bicarbonate is used as a component in animal feed, human food, pharmaceutical

and industrial applications, especially as an environmentally benign cleaning

agent. Sodium bicarbonate can also be used as an agent for flue gas

desulfurization, a market that may expand in the future.

Currently,

the oil shale in the Piceance Creek Basin is the subject of considerable

interest as a result of the increasing recognition of the need for the United

States to become more self sufficient in energy and reduce its reliance on

foreign energy sources. If that interest led to investment in

developing the oil shale resource, NSI’s proximity to the oil shale industry may

allow it to benefit from any increased demand for its water or for additional

sodium bicarbonate products such as those used in cleaning the

environment.

|

2.

|

NSI’s

Sodium Bicarbonate

Business

|

NSI’s

business is to produce and sell natural sodium bicarbonate, commonly known as

baking soda, for use in a wide variety of products and

activities. NSI is a wholly-owned subsidiary of NSHI.

The

Sodium Bicarbonate Market

According

to the 2006 Chemical Economics Handbook – SRI Consulting, the United States

production of sodium bicarbonate in 2005 was 580,000 metric

tons. Further, the Handbook reports “Apparent U.S. consumption of

sodium bicarbonate increased from 331 thousand metric tons in 1989 to an

estimated 534 metric tons in 2005, representing an average annual growth rate of

3.0%. Actual consumption growth is expected to average 2.1% per year

through 2010, reaching a level of 576,000 metric tons.”

In

addition, the Handbook reports U.S. consumption of sodium bicarbonate by end

user (thousands of metric tons) in 2005. For convenience, the

equivalent U.S. Short Tons is also shown:

|

End User

|

Metric Tons

(‘000)

|

Equivalent

U.S. Short

Tons (‘000)

|

|||||

|

Food

|

170 | 187.4 | |||||

|

Animal

Feed

|

134 | 147.7 | |||||

|

Pharmaceuticals

and Personal Care

|

48 | 52.9 | |||||

|

Chemicals

|

46 | 50.7 | |||||

|

Cleaning

Products

|

44 | 48.5 | |||||

|

Water

Treatment

|

33 | 36.4 | |||||

|

Blast

Media

|

19 | 20.9 | |||||

|

Fire

Extinguishers

|

9 | 9.9 | |||||

|

Other

|

17 | 18.7 | |||||

|

Total

|

520 | 573.2 | |||||

The

market use is dominated by the food industry (baking soda) and animal nutrition

(rumen buffer), accounting for a majority of the total market. The

remaining market is split between a variety of uses from pharmaceuticals,

personal care (toothpaste), deodorizers, industrial uses, cleaning products,

chemical, blasting media, etc. Presently, NSI’s share of the animal

feed and food segments is in line with its share of industry production

capacity, however, it is underrepresented in the specialty

segments.

The

Plant

The

26,500 square foot processing plant located on one of the Wolf Ridge leases

consists of a single building with crystallizers, boilers, centrifuge, dryers

and other equipment capable of producing various grades of sodium

bicarbonate. The plant has a name plate capacity of 125,000 tons per

year. In FY2008 it produced 100,189 tons. Until NSI attempts to

obtain higher levels of production it will remain uncertain as to its actual

capacity. However, NSI is increasing production capacity of the plant

by an initial program of drilling more cavities and further improving the

efficiency and output of the surface plant and facilities. NSI

intends to reengineer and expand the production capacity of the plant by a

significant amount when such an expansion can be justified. It is

currently developing designs for expansion and obtaining estimates of costs to

aid in this evaluation. The plant is capable of producing all grades

of sodium bicarbonate except that used for kidney dialysis.

There

are also several other buildings associated with the plant - one building of

approximately 50 feet in diameter used for bulk storage with a storage capacity

of 3,000 tons - and three small sheds (lube storage shed, fire pump house shed

and hazardous materials shed). The plant, the bulk storage facility

and one of the sheds are of metal construction; the other two sheds are of wood

construction, each on concrete pads.

There

is no rail transportation to the plant. Product that is to be shipped

by rail is transported by truck to a rail loading facility in Rifle, Colorado

that is operated by a third party. Water for operations is available

from water wells on NSI’s property (see Water Rights below). Electric

power and gas are provided by local suppliers.

Marketing

Arrangements

NSI

sells animal feed grade product through five independent

distributors. The largest of these is Bunnett & Company of Lago

Vista, Texas which represents the largest part of our animal feed

sales. The principal of Bunnett & Company is Bill Bunnett, father

of Brad Bunnett who is a director of both NSHI and NSI and President of

NSI. The majority of NSI’s industrial and United States

pharmaceutical (“USP”) grade products is distributed by an agent, Vitusa

Products, Inc. of Berkeley Heights, New Jersey. Sales distributed

through Bunnett & Company accounted for 27% of NSI’s sales revenues in the

fiscal year ended June 30, 2009 and sales distributed through Vitusa Products

accounted for 25% of our sales revenues during the same period. A

third distributor, Agri Dealers, Inc. of Louisville, Kentucky, an animal feed

distributor, accounted for 10% of NSI’s sales revenues during the same

period. There are no other significant marketing relationships that

constitute more than 10% of our sales.

Historically,

the plant has shipped up to approximately 55% of its production as bulk product

and the remainder as bagged product. NSI packages product in various

crystal sizes in 50 lb. bags, 2000 lb. “supersacks”, or in bulk and transports

the product to its customers by truck or rail. NSI sells most of its

products throughout the United States, Canada and Mexico.

NSI’s

products have many uses and applications. They include sales to the

animal feed, industrial, food and pharmaceutical grade

markets. Sodium bicarbonate is used in baking products, personal care

products including toothpaste and antacid remedies; household products including

deodorizers, cleaning products, detergents, carpet cleaners, bath salts and cat

litter. Sodium bicarbonate is also used in industrial situations such

as leather tanning, fire extinguishers, blast media and waste water

treatment.

Figure

5: A Finished Product Sample

Competitive

Advantage

There

are five other competitors in the sodium bicarbonate market according to the

2006 Chemical Economics Handbook – SRI Consulting. NSI’s principal

competitors are Church & Dwight, manufacturers of the Arm & Hammer

brand; FMC Corporation and Solvay. Church & Dwight is by far the

largest manufacturer in the United States and NSI’s competitors have far greater

financial resources than NSI. NSI is the only producer of sodium

bicarbonate from nahcolite, the naturally occurring form of sodium

bicarbonate. All other production of sodium bicarbonate utilizes

trona, a mixed form of sodium bicarbonate and sodium carbonate, from Green

River, Wyoming. An alternative method is to produce sodium carbonate

synthetically from sodium chloride in an industrial plant. We believe

that both these production methods are more expensive than the solution mining

and simple re-crystallisation of sodium bicarbonate from naturally occurring

nahcolite NSI employs. We believe that NSI is the lowest cash cost

producer. NSI competes on the basis of service and

price.

In

addition, there are significant barriers to overcome for competitors seeking to

establish solution mining operations on BLM leases in the Piceance Creek

Basin. The only other sodium leases issued by the BLM in the Piceance

Creek Basin are the 4,956 acre Yankee Gulch lease, and the Nielsen-Juhann-Hogle

lease covering 2,186 acres. The Nielsen-Juhann-Hogle lease has not

been permitted and would require a public filing of a mining plan, an

environmental impact study and a series of public meetings to secure extensive

government approvals before it can be brought into production.

We

believe that NSHI and NSI have the largest available resource of nahcolite

in the Piceance Creek Basin that is currently able to be mined.

Sales

and Revenue Performance

Fiscal

year 2004 was the first complete fiscal year of NSI’s ownership of its

processing plant. NSI’s annual sales in tonnages and gross revenues

are shown in the following tables:

|

Fiscal

Year

|

Sales

(tons)

|

%

Change

on prior FY

|

||

|

2004

|

84,103 | |||

|

2005

|

85,038 | + 1.1 | ||

|

2006

|

88,910 | + 4.6 | ||

|

2007

|

101,970 | +14.7 | ||

|

2008

|

101,614 | - 0.4 | ||

|

2009

|

97,729 | -3.8 | ||

|

Fiscal

Year

|

Gross

Revenues

($)

|

%

Change

on prior FY

|

||

|

2004

|

12,609,041 | |||

|

2005

|

14,141,500 | + 12.2 | ||

|

2006

|

15,293,688 | + 8.1 | ||

|

2007

|

16,951,997 | + 10.8 | ||

|

2008

|

17,947,800 | + 5.9 | ||

|

2009

|

19,835,160 | + 10.5 | ||

During

2009, sales were constrained by production interruptions and cavity limitations

as discussed above. NSI now expects that NSI’s new cavities will

improve production and supply capability. NSI’s sales history is

illustrated on a quarterly basis in the following graph.

Environmental

Issues

The

sodium bicarbonate production is licensed under the EPA and BLM as a zero water

emission business. NSI must not allow any water stream from the

production process to enter the environment. All breaches must be

reported.

Waste

water streams are collected in two ponds where the water is evaporated and the

residual salts collected for disposal by an approved method.

During

our fiscal year ended June 30, 2009, NSI did not allow any water stream to enter

the environment and consequently no breaches were reported.

|

3.

|

NSI’s

Water Rights

|

General

NSI

owns numerous water rights in Northwestern Colorado in the Piceance Creek Basin

from the Piceance and Yellow Creeks. These streams flow into the

headwaters of the White River which flows into the Green and Colorado

Rivers. Yellow Creek traverses NSI’s property; Piceance Creek, Yampa

River and the White River are nearby. These water rights incorporate

direct pumping rights, direct flow water rights and pumping rights from the

White River. We also have a reservoir right associated with the White River

pumping rights called the Wolf Ridge Reservoir and NSI owns the Larson Reservoir

at the headwaters of Piceance Creek.

The

Colorado River Basin covers 244,000 square miles and provides water for 30

million people. The river has an average flow of around 14

million acre feet per year which occasionally increases to 18 million in wet

years and decreases to about 12 million in dry years.

On

the basis of the Colorado River Compact of 1922, the Colorado River Basin is

divided into the Upper Colorado River Basin and Lower Colorado River Basin at

Lee’s Ferry just below the confluence of the Paria River and the Colorado River

near the Utah-Arizona border. The upper Basin and the lower Basin

were each apportioned a consumptive use of 7.5 million acre feet of water

annually, based on an assumption of 15 million acre feet of available water for

the Colorado River. The assumption was demonstrated to be an

overestimate and reduced to 12 million acre feet in a hydrologic study by the

U.S. Bureau of Reclamation (CWCB 2004). In the Upper Colorado River

Basin Compact of 1948, the water of the Upper Colorado River Basin was further

allocated among the states of Arizona, Colorado, New Mexico, Utah, and

Wyoming. Arizona has a fixed allocation of 50,000 acre feet

annually. The remainder is shared by Colorado (51.75%), New Mexico

(11.25%), Utah (23%), and Wyoming (14%).

By

treaty, Mexico must get 1.5 million acre feet annually. California

has a right to a minimum of 4.4 million acre feet while the upper Basin where

NSI is located has an accumulated withdrawal allotment of around 3.6 million

acre feet. The Central Arizona Project, a 335 mile canal and

the largest water transfer system ever built, has the capacity to withdraw more

than 2 million acre feet. State by State allotments are shown in the following

table:

|

Water Allocation from The Colorado River

System

|

||||

|

State

|

Allocation

(Acre Feet per year)

|

|||

|

California

|

4,400,000 | |||

|

Colorado

|

3,881,250 | |||

|

Arizona

|

2,800,000 | |||

|

Utah

|

1,725,000 | |||

|

Mexico

|

1,500,000 | |||

|

Wyoming

|

1,050,000 | |||

|

New

Mexico

|

845,750 | |||

|

Nevada

|

300,000 | |||

| 16,502,000 | ||||

In

Colorado the state requires that groundwater removed from an aquifer be

augmented (i.e. replaced) from surface water sources. Thus, new

groundwater pumping rights cannot be used for any length of time without an

approved plan to augment the water removed from the groundwater

wells.

Colorado

operates under the “Prior Appropriation Doctrine” with respect to water

rights. The Prior Appropriation Doctrine essentially provides that

any person or entity that diverts water and applies the water to beneficial use

before another person or entity has the first and prior right to divert water

under the water right. The doctrine is also commonly known as the

“First in Time – First in Right”. To the extent that a water right

was appropriated prior to another water right, the Prior Appropriation Doctrine

provides that a senior water right is entitled to be fully satisfied before the

junior water right is allowed to take any water. The Colorado General

Assembly requires the claimants of a water right to create documentary evidence

by obtaining a decree from a court confirming the existence of the water

right.

NSI’s

water rights were incorporated into a Decree entered by the District Court in

and for Water Division No. 5 in Case No. 88CW420 on August 13, 1991 (the

“Decree”). The Decree is crucial for continued operations of the

sodium mining business. NSI’s water rights were combined in the

Decree to ensure the reliability of the water supply for mining

operations. In addition, since all the water rights are under common

ownership, the ability to maximize the use and value of the water rights is

enhanced if the water rights could be used for any purpose associated with the

mining operations or other purposes. Another factor leading to the

inclusion of all the water rights in the Decree was that some of the water

rights and facilities for the water rights had not been developed, and the

conditional portion of the water rights could be maintained by legally

integrating and attributing work on some of the water rights to other

conditional water rights.

However,

even though all of the water rights were integrated into the Decree, various

water rights may be separated from the water supply required for mining

operations. As discussed below, NSI’s substitution and exchange

rights and augmentation plan provide additional flexibility in how we can manage

access to NSI’s water rights.

Figure

6: Colorado River System

The

Decree also includes a Water Court approved “plan for

augmentation”. This is a plan that can considerably aid operational

flexibility. NSI’s augmentation plan includes rights under Colorado

law of “substitution and exchange”. Substitution and exchange enables

delivering water at one point on a stream and taking water out at another point

on the stream. Water rights may be acquired to enable substitution

and exchange. While this concept may not seem significant,

“substitution and exchange” can save millions of dollars in dam and pipeline

construction costs and pumping costs to a prospective purchaser who might

otherwise have to bring water from a much greater distance than does

NSI.

For

example, under the Decree, NSI may deliver fully consumable agricultural water

rights to Piceance Creek at its headwaters, and “substitute and exchange” this

water depleted from Piceance Creek by the operation of its wells at the plant

site. NSI thereby avoids the necessity to pipe water from the

headwaters of Piceance Creek to its operations. Further, because

Piceance Creek is such a dry stream, the substitution and exchange ability is

limited and at a premium. As a result of the Decree, NSI owns all or

virtually all of the substitution and exchange potential on Piceance Creek and

Yellow Creek. While someone else may acquire the right to operate a substitution

and exchange on the two streams, that use would be subordinate to NSI’s own

substitution and exchange rights. Potentially, other parties

operating in the Piceance Creek Basin who require water may be prepared to pay

NSI to share in its substitution and exchange rights.

Under

current operations, the water supply for the mining operations is provided by a

single well owned by NSI. The pumping of water from the well causes

depletions to Piceance Creek and Yellow Creek. Colorado law requires

that depletions to Piceance Creek and Yellow Creek must be replaced with other

water from the same drainage system. The Decree provides that senior

water rights on Piceance Creek are used to replace the depletions to Piceance

Creek and part of the depletions to Yellow Creek. Hence in order to

protect mining operations, it is necessary to maintain ownership of well water

rights to supply mining operations and senior water rights to replace the

depletions caused to Piceance Creek and Yellow Creek. NSI has several

different sources of water to replace the depletions to the

streams. Currently, NSI’s water requirements for its sodium

operations are less than one cubic foot per second (“CFS”) or 724 acre feet per

year or less than 1% of our total water rights.

There

are other factors independent of the Decree that enhance the value of NSI’s

water rights. First, no other plan for augmentation has been approved

by the Water Court within the Piceance Creek Basin thereby providing NSI a

significant competitive advantage in the water supply available to its

activities. There is also a value associated with having the

augmentation plan approved and NSI’s Decree completed. Litigation is

always an uncertain venture, and any new augmentation plan application that is

filed will be scrutinized by all the other water rights owners in the Piceance

Creek and Yellow Creek drainages, including the major oil companies that have a

presence in these Basins. Potential users of NSI’s water rights may

find that constructing a pipeline for delivery of water may be more reliable and

cheaper than obtaining a judicially approved plan for augmentation.

NSI’s

total water rights exceed more than 100,000 acre feet per year. We

believe that these water rights can generate a future revenue stream and have

increasing value, especially as any prospective development of the oil shale

resources of the Piceance Creek Basin may require very large volumes of

water. It is our objective to develop and further utilize the water

rights NSI owns.

Agreement

with Shell Frontier Oil & Gas, Inc.

NSI

entered into a contract on January 29, 2007 with Shell, effective January 1,

2007, to sell up to 120 acre feet of water per year at a price equal to $8,146

per acre foot. Shell has been awarded three 160 acre oil shale

research, design and development leases by the Bureau of Land Management

contiguous with NSI’s sodium leases. If Shell purchases any water, it

will remove the water using water transport trucks or by constructing a pipeline

at its own expense.

NSI

will provide water to Shell from one of its existing water wells. The

water will be recovered from the geologic formation commonly known as the “A

Groove” and the quality of the water shall be “as is” upon withdrawal from the

geologic formation without any treatment by NSI. The initial term of

the agreement is five years and renewable thereafter with the purchase price

adjusted according to a formula based on movement in the consumer price

index. A condition of the agreement is that NSI may sell water to

other users provided that such delivery is subordinate to the delivery of water

to Shell. Shell did not purchase any water during the year ended June

30, 2009.

The

agreement will be extended automatically for successive periods of five years

although Shell may elect to terminate the agreement by providing written notice

prior to the end of the initial term or each subsequent renewal date. Similarly,

NSI can terminate the agreement by providing written notice on the same

basis. In addition, the agreement terminates if NSI ceases to have an

interest in the sodium leases. See Item 3 “Legal Proceedings” for

additional information.

Appraisals

The

current value of NSI’s water rights is unknown. The most valuable

component relates to the Wolf Ridge Reservoir and Pipeline Water

rights. These rights produce a large quantity of water that may be

used for commercial purposes. They could be separately developed and

are not currently being used for mining purposes. The market value of

the Wolf Ridge Rights is a function of the amount of fully consumable water

available under these water rights.

Water

rights are assets routinely bought and sold in the State of

Colorado.

The

Wolf Ridge Reservoir and Pipeline Water right allows NSI to construct a

reservoir and pipeline for storage of 7,379.70 acre feet of water, fed by the

pipeline at the rate of 100 CFS, equivalent to 44,800 gallons per

minute. A prospective purchaser of these rights could move the points

of diversion or location of the structures to a new location and still take

advantage of the relatively senior priority of the rights on the White

River.

Identification

of Water Rights

Our

water rights can be categorized and summarized as follows:

|

Water

Flow Rights

|

Location

|

Flow

Rate

(CFS)

|

Flow

Rate

(acre ft/yr)

|

Percent

of

Annual Flow

|

|

Direct

pumping

|

13

wells on site

|

45.0

|

32,579

|

30%

|

|

Direct

Flow rights

|

Piceance

Creek

|

5.3

|

3,837

|

3%

|

|

River pumping

|

White River

|

100.0

|

72,397

|

67%

|

|

Total flow

|

150.3

|

108,813

|

100%

|

|

Water

Storage

Right

|

Location

|

Volume

(acre feet)

|

Percent

of

Storage

|

|

Wolf

Ridge Reservoir

|

Plateau

|

7,380

|

92%

|

|

Larson Reservoir

|

Piceance Creek headwaters

|

600

|

8%

|

|

Total flow

|

7,980

|

100%

|

Direct Pumping

Rights - Well Water

NSI

owns thirteen well water rights located adjacent to the sodium bicarbonate

process plant as described in the Decree. These rights have priority

dates from the 1970s so they are very “junior” water rights. Under

Colorado law, the Well Water Rights cannot divert water without having a plan of

augmentation approved by the Water Court. NSI’s Decree includes a

plan for augmentation authorizing, among other things, wells that have a

hydraulic connection to the surface stream to pump water, provided that

depletions to the surface stream caused by well pumping are augmented (i.e.

replaced) with other water supplies. As discussed above, the Well

Water Rights are included within the Decree.

Senior Direct Flow Water

Rights in the Piceance Creek Basin

NSI

owns the following senior direct flow water rights:

|

Name

|

Appropriation Date

|

Decree Date

|

Flow Rate (CFS)

|

|

Morgan

Ditch No. 1

|

April

15, 1883

|

April

28, 1890

|

1.00

|

|

Enlargement

and Extension of Morgan

Ditch No. 1

|

September

27, 1886

|

April

28, 1890

|

0.40

|

|

Morgan

No. 2 Ditch

|

September

27, 1886

|

April

28, 1890

|

0.40

|

|

Home

Supply Ditch

|

September

19, 1886

|

May

10, 1889

|

1.00

|

|

Larson Ditch

|

September 17, 1886

|

May 10, 1889

|

2.50

|

The

direct flow water rights located adjacent to the Larson Reservoir on the upper

reaches of Piceance Creek are among the most senior water rights in the Piceance

Creek Basin. They were originally decreed for agricultural irrigation

however the Water Court in its Decree changed the direct flow water rights for

numerous purposes including commercial and industrial purposes. In

addition, the Water Court imposed certain terms and conditions on the use of the

water, including annual volumetric limitations on the use of the water

rights. The average annual amount of water that may be diverted and

consumed pursuant to the direct flow rights is approximately 234 acre

feet.

Wolf Ridge Reservoir and

Feed Pipeline Water Rights to the White River

The

Wolf Ridge Reservoir and Wolf Ridge Feeder Pipeline water rights were decreed in

the 1970s. However, unlike the Well Water Rights that divert water

from the aquifer tributary to Piceance Creek, the Wolf Ridge Water Rights divert

water primarily from the White River approximately 12 miles from the current

sodium bicarbonate production operations. Piceance Creek has lower

flows in the summer, but the White River is a much larger

stream. Hence a 1970s water right diverting out of the White River

will have water available for diversion on a yearly basis. As

discussed above, the Wolf Ridge Water Rights provide for the construction of a

reservoir originally intended to be adjacent to the current sodium bicarbonate

processing facility to contain a maximum of 7,379.70 acre feet. This

reservoir could be fed by the Wolf Ridge feeder Pipeline at the rate of 100

CFS. (44,800 gallons per minute). This is equivalent to

72,396 acre feet per year.

Larson Reservoir and Larson

Reservoir Enlargement Water Rights

The

Larson Reservoir located on the upper reaches of the Piceance Creek was

originally decreed for 62 acre feet of water storage rights with an

appropriation date of July 20, 1888 and a decree date of May 10,

1889. Hence it is a very “senior” water right. The Water

Court Decree changed the uses of the Larson Reservoir Right to include

industrial and commercial uses and allows the consumption of approximately 39

acre feet of fully consumable water per year.

The

Decree also approved an additional water right referred to as the Larson

Reservoir Enlargement Water Right. It has an appropriation date of

April 5, 1988 and may store up to 600 acre feet of water, with the right to

refill the Larson Reservoir with 600 acre feet of water per

year. This has not been constructed but could be constructed on land

entirely owned by NSI. The Larson Reservoir Enlargement Water Right

could only divert water during the early spring runoff period, so NSI estimates

approximately 300 acre feet of water could be stored annually if a reservoir was

constructed. The Larsen Reservoir presently has a large deposit of

silt. NSI intends to evaluate the possibility of excavating the silt

and extending the reservoir to provide for a greater storage

capacity.

|

4.

|

Oil

Shale Potential

|

The

Energy Policy Act of 2005 directed the Task Force on Strategic Unconventional

Fuels to make recommendations and develop an integrated program to coordinate

and accelerate the development of fuels from domestic unconventional fuels

resources. The Task Force found in February, 2007:

|

“Global

and domestic demand for crude oil and refined products continues to

expand, driven by rapid economic growth in developing economies and

domestic consumer habits. At the same time, finding and

producing oil reserves to meet rising demand is increasingly difficult and

costly. Companies are failing to replace produced reserves,

shrinking the world’s conventional oil reserves base. Excess

production capacity is also shrinking, reducing the ability to supply

disruptions, increasing price volatility, and driving up

prices. Domestic crude oil production is declining as demand

rises, increasing our dependence on imports of oil and refined

products……….Increasingly, oil and refined products must be imported from

nations unfriendly to the United States or threatened by political

instability, reducing the security and reliability of supplies critical to

our economy, our military, and our national security.” (Page

ES-1).

|

|

“Oil

shale is extremely well suited for producing premium quality refinery

feedstocks for diesel and jet fuels. The manufacturing

processes can also yield significant quantities of value-added chemical

by-products…….America’s commercial quality oil shale resources exceed 2

trillion barrels, including about 1.5 trillion barrels of oil equivalent

in high quality shales concentrated in the Green River Formation in

Colorado, Utah and Wyoming.” (Page I-16).

|

The

Cole report described on Page 5 of this Annual Report, states “Shale-Oil

resources for the Saline zone under the lease are between 12 and 14 billion

barrels.” The Saline zone sits under one of NSI’s sodium bicarbonate

leases from the BLM. We have not conducted any additional studies on

oil shale resources on this specific lease nor the Rock School lease or the

other Wolf Ridge leases.

In

2006, the BLM issued five oil shale research leases adjacent to NSI’s sodium

bicarbonate operations in accordance with its regulations at that

time. Three of these leases were issued to Shell, as mentioned

above. It is expected that the US Government will evaluate the

results achieved by existing holders of these research leases before any

commercial leases will be issued.

We

currently do not have the right to evaluate or extract these oil shale resources

and the Department of Interior does not have any current rules for applying for

a lease to evaluate or extract these resources, even on a research

basis. If the Department of Interior issues rules for applying for

oil shale research leases, NSHI and NSI may apply for a lease to evaluate these

oil shale resources to determine whether we can extract the oil shale on a

commercially viable basis. The Department of Interior may never issue

new rules for leases to evaluate or extract oil shale and if they do, we may not

qualify for such a lease.

EMPLOYEES

AmerAlia’s

day to-day business activities are managed by Bill H. Gunn, Chairman

and President; and Robert van Mourik, Executive Vice President and Chief

Financial Officer. See Item 11 “Executive Compensation”.

NSI

has 39 employees in production, sales & marketing, financial, environmental

compliance and human resources roles.

|

ITEM

1A:

|

RISK

FACTORS

|

AmerAlia

is a minority shareholder in NSHI and cannot control NSHI or its wholly-owned

subsidiary NSI.

We

own only 18% of the equity of NSHI which owns all of NSI so we cannot determine

the composition of the boards of directors or management of those companies or

their conduct. Consequently, they may act in a manner that is not in

our best interests. For example, NSHI may make capital calls on its

shareholders when AmerAlia has limited funds such that it could face dilution of

its ownership interests.

We

may have to take certain actions to avoid registration under the Investment

Company Act of 1940.

AmerAlia’s

only asset is its 18% equity interest in NSHI. Generally, a company

must register as an investment company under the Investment Company Act and

comply with significant restrictions on operations and transactions with

affiliates if its interest in securities, other than majority owned

subsidiaries, exceeds 40% of the company's total assets, or if it holds itself

out as being primarily engaged in the business of investing, owning or holding

securities. We have held discussions with the SEC regarding

Investment Company Act compliance and unless we can increase our shareholding in

NSHI to at least 50% ownership or otherwise meet an exemption from registration

under the Investment Company Act, we will need to register as an investment

company and will be subject to the various, extensive provisions of the

Investment Company Act and its regulations. We believe that such

registration would adversely affect our operations and cause us to incur

significant registration and compliance costs. Any violation of this

Act could subject us to material adverse consequences including any contracts

that AmerAlia entered into while an unregistered investment company would be

void.

We

have large accumulated losses, we expect future losses and we may not achieve or

maintain profitability.

We

have incurred substantial losses and used substantial cash to support our

activities through the development stage, complete our acquisition of the

assets, refurbish NSI’s plant, expand NSI’s cavities and our restructuring while

sustaining our activities to date. Our accumulated losses were

approximately $111 million at June 30, 2009. While the restructuring

and additional capital we have received has provided us with approximately

$8,700,000 of shareholders equity at that date, we may continue to lose money

unless we can access any income generated by NSI. As a minority

shareholder of NSHI we do not have any rights to access NSHI’s cash flow and may

not receive any distributions of dividends. Hence we do not have any

source of incoming cash flow. We will continue to lose money unless

we significantly increase our revenues. If we cannot operate

profitably we may not be able to contribute to further capital calls or raise

new capital. We cannot predict when, if ever, we will operate

profitably.

We

rely on key employees in NSI to manage its operations and may have difficulty

replacing them if they were to leave our employ.

While

Bill H. Gunn is intensively involved in NSI’s management, we conduct our

operations with a relatively small management team so the loss of an employee

through an extended illness or resignation could adversely impact our capacity

to successfully fulfill our obligations and thereby impact our sales, margins

and operating profitability.

NSI’s

pricing of its products is determined in a competitive environment in which it

is not generally able to lead prices.

Our

industry is dominated by Church & Dwight, a long time manufacturer of the

Arm & Hammer brand of baking soda and related products. NSI’s

major competitors also include FMC and Solvay, major corporations with

considerable resources, marketing expertise and broader access to customers than

we do. Consequently, if there is a price war with the major companies

that dominate the industry NSI’s margins and profitability may be

threatened. In addition, NSI’s business has high fixed

costs. From time to time, NSI may need to reduce prices for some of

its products to respond to competitive and customer pressures and to maintain

market share. Consequently, NSI’s operating results may suffer.

The

loss of any of NSI’s principal customers could significantly lower its sales and

profitability.

NSI

primarily sells its animal feed grade product through customers who act as

distributors. The largest of these in tonnages and revenues is

Bunnett & Company who account for the majority of NSI’s animal feed

sales. In addition, NSI sells most of its higher grade products

through Vitusa Products, Inc. of Berkeley Heights, New

Jersey. Another customer, Agri Dealers, Inc., represented nearly 10%

of NSI’s sales and together these three constituted approximately 62% of NSI’s

sales through June 30, 2009 and about 63% of NSI’s accounts receivable at June

30, 2009. Consequently, there is also a concentration of credit risk

associated with the continuing successful performance of these

customers. The loss of all or part of their business could be

injurious to NSI’s sales, margins and profitability.

NSI

may not be able to continue to recover sodium bicarbonate economically or at all

from the cavities if there are failures in the underground

operations.

NSI

recovers its sodium bicarbonate from cavities that are about 1,900 feet

underground and does so by pumping hot water through a pipe into the cavity and

then recovering the pregnant liquor through a recovery pipe that is about 8

inches in diameter. If portions of an underground cavity collapse, as

happened last year, or if there are blockages in the wells, NSI’s ability to

recover pregnant liquor can be severely affected. It is possible a

well may become unusable so that NSI would have to drill new a new cavity and

associated injection and recovery wells at considerable expense and delays to

its production. As continuity of production requires having

operational cavities and as it can take some months to drill new cavities and

bring them into production, failure of existing cavities can severely jeopardize

NSI’s production capability.

This

is a high fixed cost business and if there are underground production problems

such as cavity collapses that cause difficulties in recovering product or if NSI

is unable to sell sufficient tonnages, the relatively high fixed operating costs

applied to a low volume of sales may cause the operation to not be

viable. NSI’s resource of naturally occurring sodium bicarbonate has

a zone that contains some sodium chloride. The presence of too much

sodium chloride in the pregnant liquor adversely impacts plant productivity and

potentially may cause a reduction in the amount of sodium bicarbonate that might

be recovered from a cavity.

Increasing

gas, power and fuel costs could erode NSI’s profit margins and harm operating

results.

Energy

costs and transport costs represent a major component of NSI’s cost

structure. It may be difficult to pass on increased costs to its

customers so that NSI’s profitability may be adversely impacted. This

could harm NSI’s financial condition and operating results.

NSI’s

operations are subject to a significant amount of regulatory scrutiny and

regulation from federal and state authorities.

NSI’s

mining and processing operations operate under permits from several state and

federal authorities, including the Environmental Protection Agency, the Bureau

of Land Management, and the Colorado Division of Minerals and Geology. Failure to comply with

government conditions and permitting requirements may cause these permits to be

revoked with material and adverse effects on NSI, NSHI and

AmerAlia. If NSI loses its permits, NSI may have to cease operations

while it seeks their renewal. If NSI cannot do this, it will be out

of business. NSI also requires BLM approval in accordance with NSI’s

approved mine plan to establish new cavities. If this approval is

denied, then NSI will lose its ability to recover sodium bicarbonate from the